IPOs

Auto Added by WPeMatico

Auto Added by WPeMatico

Sprinklr, a New York-based customer experience company, announced today it has filed a confidential S-1 ahead of a possible IPO.

“Sprinklr today announced that it has confidentially submitted a draft registration statement on Form S-1 with the Securities and Exchange Commission (the ‘SEC”) relating to the proposed initial public offering of its common stock,” the company said in a statement.

It also indicated that it will determine the exact number of shares and the price range at a later point after it receives approval from the SEC to go public.

The company most recently raised $200 million on a $2.7 billion valuation last year. It was its first fundraise in 4 years. At the time, founder and CEO Ragy Thomas said his company expected to end 2020 with $400 million in ARR, certainly a healthy number on which to embark as a public company.

He also said that Sprinklr’s next fundraise would be an IPO, making him true to his word. “I’ve been public about the pathway around this, and the path is that the next financial milestone will be an IPO,” he told me at the time of the $200 million round. He said that with COVID, it probably was a year or so away, but the timing appears to have sped up.

Sprinklr sees customer experience management as a natural extension of CRM, and as such a huge market potentially worth $100 billion, according to Thomas. But he also admitted that he was up against some big competitors like Salesforce and Adobe, helping explain why he fundraised last year.

Sprinklr was founded in 2009 with a focus on social media listening, but it announced a hard push into customer experience in 2017 when it added marketing, advertising, research, customer and e-commerce to its social efforts.

The company has raised $585 million to date, and has also been highly acquisitive, buying 11 companies along the way as it added functionality to the base platform, according to Crunchbase data.

Powered by WPeMatico

When Vista Equity Partners acquired backup and disaster recovery firm Datto in 2017, it was easy to think that was the end of the company’s story. It would be comfortably absorbed into the private equity portfolio continuing to make money for the firm, but that’s not really the way Vista works. It tends to build up its companies, sometimes eventually taking them public, and yesterday that’s what happened when Datto filed its S-1.

Datto has been busy since it was acquired and reports a healthy $507 million in annual recurring revenue (ARR) along with 17,000 managed service provider (MSP) customers. Among those, it has more than 1000 customers contributing over $100,000 in ARR. MSPs are service providers that act as a company’s IT department when they don’t have internal resources.

The company has included a standard $100 million placeholder for the amount they intend to raise for the event, and that will almost certainly change. In a nod to its manage service provider customer base, the company’s ticker symbol will be MSP.

When the company raised its $75 million Series B in 2015, former CEO and founder Austin McChord, said that the company was already profitable at that point, two years before Vista came knocking. “As a profitable company, Datto isn’t raising capital to fund operations, but instead, to enter new markets and build new products and technology,” he said in a statement at the time.

You can see that in the company’s financials. In the first six months of 2020, the company had subscription revenues of $234 million and a gross profit of $178 million. When sales and marketing and other costs are added in, the company had a net income of $10 million. That’s compared to $196 million in subscription revenue in the same period of 2019, a gross profit of $143 million, and a net loss of about $26 million.

In short, the company has managed to grow top-line revenue, keep its cost of revenues flat, and manage the growth of its other expenses to limit their effect on the bottom line. That swung its net income per share from -$0.19 to $0.07.

Of course, companies like Datto always try to make the numbers look good in preparation for a public offering, so the real understanding will come in the next few quarters as we see if Datto can sustain its growth and keep expenses in check.

When I spoke to Alan Cline, senior managing director at Vista last year, he said his firm tends to like high-performing startups like Datto that have built substantial companies.

“Software is the easiest place to innovate inside of technology. We see a huge advantage in terms of the productivity that it drives for the end business customer, and to us that high ROI is powerful because whether it’s an up market or a down market, if I can prove to you you’re going to make more money or save money in your own operations by using my software, you can find the budget,” Cline told TechCrunch.

Just last year another company in the Vista portfolio, Ping Identity, filed to go public for the same $100 million placeholder, eventually offering 12.5 million shares at $15 per share. Today the company is trading at $31.68 per share with a market cap of over $2.5 billion.

Powered by WPeMatico

It was several years ago, at a tech conference in Laguna Beach, Calif., that the venture capitalist Bill Gurley issued one of what would become repeated warnings that startups were staying private too long. Comparing companies that refuse to go public to undergrads whose college careers extend several years past the point that they should, Gurley suggested they should be embarrassed, not proud, for keeping their shares in private hands. “Until you get liquid, you really haven’t accomplished anything,” Gurley said.

Whether Gurley was referring to Uber at the time, only he knows. Though his firm, Benchmark, eventually forced out Travis Kalanick, the co-founder and longtime CEO of Uber, the tipping point was seemingly not Kalanick’s determination to keep Uber privately held as long as possible, but rather an investigation into sexual harassment investigations and the employee misconduct that was discovered in the process.

Either way, it’s looking increasingly like Gurley had a point. As you may have noticed if you care anything about the public markets, they took a nosedive today. In fact, they fell to a new low for the year this afternoon, a reaction in part to the Federal Reserve’s decision earlier today to raise its benchmark overnight lending rate for the fourth time in 2018.

The Fed also signaled minimal rate hikes for next year — forecasting two rate hikes instead of three — but investors were apparently hoping for even better news.

It’s hard to blame them for seeking out more of a silver lining, given everything else that’s going on. Tech stocks are getting battered, with the FANG companies (Facebook, Apple, Netflix and Google) down meaningfully from their share prices of six months ago. (Amazon has held up the best.)

The economy of China — the U.S.’s third largest export partner and its largest import partner — is slowing sharply, which is expected to have an impact on the U.S. and world economies. Add trade tensions into the mix, a sprinkling of uncertainty about regulations, a splash of a possible government shutdown and the growing prospect that Donald Trump will be impeached, and you start to appreciate why the market is finally going off the rails.

Despite so much uncertainty, Uber, Lyft, Slack and now Pinterest, among many others, are racing to become publicly traded at long last. According to Dealogic data quoted in today’s WSJ, 38 unicorn companies went public this year, and more are expected to test the market in 2019. Their venture backers will tell you it’s because the markets recognize a strong growth company when they see it, and that each is finally positioned well to tell their story, aided by some dazzling metrics. Yet it seems just as likely that they see the window, which flew open this year, starting to swing back in the other direction. And if this month is any indicator, it could be hard to pry it open again, at least in the first quarter or two.

“The market is basically closed between now, and the start of a new year is always slow because companies don’t start roadshows [until the markets re-open],” says Kathleen Smith, a principal of Renaissance Capital and the manager of its IPO exchange-traded fund. Pre-IPO companies like Uber are also waiting on their audits to close before they put any numbers in a public document, she notes. But it could be far from smooth sailing after that, suggests Smith. “In normal times, late January and February and March become very active, but we aren’t in a typical market. I can predict from other times that we’ve seen a bear market like this that it will have an impact on IPO activity.”

It’s all part of a vicious cycle, Smith suggests. As public market shareholders begin to feel less affluent and more risk averse, they start redeeming their public market shares. That leaves fund managers who might otherwise gamble on new issuers with less capital to invest, and less flexibility. “Investors are just not going to want to take on any risk positions when market has [taken a turn for the worse],” says Smith.

Put another way, if the markets are as crummy early next year as looks to be the case, it’s too bad, too sad for unicorn companies. “They made the choice to stay private and get capital,” says Smith. “I’ve stated many times that they should be getting while the getting is good. The pain can happen if money dries up, and it will dry up when the public market dries up.”

That doesn’t mean tech’s favorite unicorn companies are doomed, of course, especially those that can show strong fundamentals. For her part, Smith notes that what often happens in a downturn is that offerings get heavily discounted. “Valuations will be chopped if the companies want investors to participate. They’ll have to be sure to make money.”

Even if they don’t get the rich prices that ambitious bankers might pitch them (or that their VCs assigned them before that), they can always grow into the valuations their investors want to see. One need look no further than Facebook to remember why a bumpy offering doesn’t mean all that much longer term.

“Just because a stock crashes below its IPO price isn’t a sign of a bubble,” says Pivotal Research analyst Brian Wieser. “You also have to keep in mind the dynamic of companies going public,” he says. “You expect IPOs to be overvalued. Investors in these companies are necessarily selling to the greatest fool.”

Still, there may be fewer fools willing to buy what they are selling than there might have been this year or last, and if those numbers really change, today’s unicorns will look like tomorrow’s donkeys. They’re certainly going to face more scrutiny than they might have had they moved sooner.

“Maybe we’ll roar into 2019 and all will be well,” says Lise Buyer, the founder of Class V Group, an advisory firm for IPOs. “But to the extent that investors will be more selective, they’ll look at path to profitability, and they’ll look at the valuations these companies took when they were private.” Then they’ll do their own math, suggests Buyer.

If the market is truly shifting, public market shareholders “won’t care what valuations companies achieved when they were private,” says Buyer. “They’ll only be willing to pay what they are willing to pay.”

Powered by WPeMatico

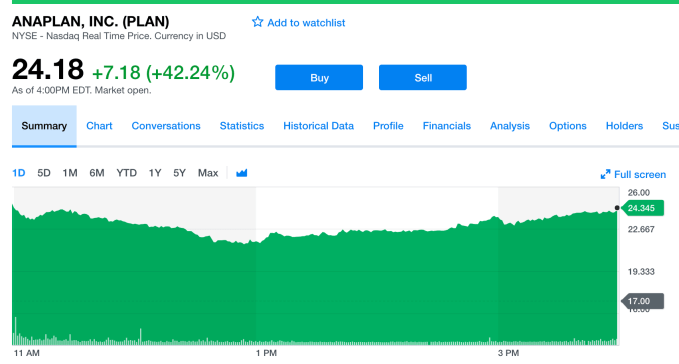

You might think that Anaplan CEO, Frank Calderoni would have had a few sleepless nights this week. His company picked a bad week to go public as market instability rocked tech stocks. Still he wasn’t worried, and today the company had by any measure a successful debut with the stock soaring up over 42 percent. As of 4 pm ET, it hit $24.18, up from the IPO price of $17. Not a bad way to launch your company.

Stock Chart: Yahoo Finance

“I feel good because it really shows the quality of the company, the business model that we have and how we’ve been able to build a growing successful business, and I think it provides us with a tremendous amount of opportunity going forward,” Calderoni told TechCrunch.

Calderoni joined the company a couple of years ago, and seemed to emerge from Silicon Valley central casting as former CFO at Red Hat and Cisco along with stints at IBM and SanDisk. He said he has often wished that there were a tool around like Anaplan when he was in charge of a several thousand person planning operation at Cisco. He indicated that while they were successful, it could have been even more so with a tool like Anaplan.

“The planning phase has not had much change in in several decades. I’ve been part of it and I’ve dealt with a lot of the pain. And so having something like Anaplan, I see it’s really being a disrupter in the planning space because of the breadth of the platform that we have. And then it goes across organizations to sales, supply chain, HR and finance, and as we say, really connects the data, the people and the plan to make for better decision making as a result of all that,” he said.

Calderoni describes Anaplan as a planning and data analysis tool. In his previous jobs he says that he spent a ton of time just gathering data and making sure they had the right data, but precious little time on analysis. In his view Anaplan, lets companies concentrate more on the crucial analysis phase.

“Anaplan allows customers to really spend their time on what I call forward planning where they can start to run different scenarios and be much more predictive, and hopefully be able to, as we’ve seen a lot of our customers do, forecast more accurately,” he said.

Anaplan was founded in 2006 and raised almost $300 million along the way. It achieved a lofty valuation of $1.5 billion in its last round, which was $60 million in 2017. The company has just under 1000 customers including Del Monte, VMware, Box and United.

Calderoni says although the company has 40 percent of its business outside the US, there are plenty of markets left to conquer and they hope to use today’s cash infusion in part to continue to expand into a worldwide company.

Powered by WPeMatico

Dropbox today said it is pricing above the range it originally set ahead of its public listing tomorrow, handing the company a valuation inching ever-closer to its original $10 billion valuation.

Dropbox earlier this week said it would price its initial public offering in a range between $18 and $20 per share, settling on a valuation near $8 billion at the high end of the range (or closer to $8.75 billion, based on its fully-diluted share count). With the new pricing, Dropbox will be valuing itself at around $8.4 billion — or a hair above $9 billion based on its fully-diluted share count. That $18 to $20 range, too, was a step up from its original proposed range, which fell between $16 and $18. Dropbox will be raising more than $700 million in the IPO, in addition to existing shareholders selling more than 9 million shares as part of the process.

What all this means is that Dropbox initially tested the waters to gauge interest, and clearly there was a lot. Companies sometimes set conservative price ranges (though this isn’t always the case) and then revise upwards as they see how much interest there is in potential investors buying shares at that price. Dropbox will make its public debut tomorrow, and the usual process here aims to get as much value for the company as possible while still ensuring the so-called IPO “pop” — usually a jump of around 20%. We’ll probably get the formal price in the form of an SEC filing this evening as it gets ready to list tomorrow.

Should that be successful, Dropbox would fall above the valuation of its last financing round, which gave the company a $10 billion valuation amid a hype wave of consumer startups. Dropbox, one of the original pioneers of online storage, in recent years has found itself looking to slowly scoop up more and more enterprise customers as it tries to create a second lucrative line of business. The company deploys a classic playbook of attracting initial customers within teams and then growing up to the point it reaches the C-Suite of companies, though the reverse is certainly possible as Dropbox matures over time.

CNBC first reported the news.

Powered by WPeMatico

After previously investing in Mulesoft, it looks like Salesforce may finish off the deal and is in advanced talks to acquire the data management software provider altogether, according to a report from Reuters this morning.

Mulesoft works with companies to bring together different sources of data like varying APIs. That’s important for companies that have data coming in from all over the place, whether that’s online applications or actual devices, and the company says it has Netflix and Spotify as customers. It would also give Salesforce another piece of the lock-in puzzle for enterprises that need to increasingly manage larger and larger pools of data as they look to start pumping out machine learning tools that can act on all that data.

As usual, these talks could fall apart — we saw this happen with Twitter a few years ago after the company looked at buying what was essentially the largest customer service channel on the planet (as in, great for whining at brands) — but Reuters reports that the deal could be announced as soon as this week. Mulesoft’s stock jumped nearly 20% this year after it went public last year amid a wave of enterprise IPOs jumping through the so-called IPO window while it’s open.

Salesforce is increasingly making a push into AI with products like Einstein, which it launched in 2016. Those tools give businesses predictive services and recommendations, a hallmark of what can come out of increasing piles of data based on customer activity. But all of that data has to come from somewhere, and for now, there are providers outside of the Salesforce ecosystem that stitch all that together. Having it all in one central place makes it easier to parse them through these machine learning algorithms and start building predictive models for their operations.

We reached out to Salesforce and Mulesoft for comment and will update the post when we hear back.

Powered by WPeMatico

Zuora, which helps businesses handle subscription billing and forecasting, filed for an initial public offering this afternoon following on the heels of Dropbox’s filing earlier this month.

Zuora’s IPO may signal that Dropbox going public, and seeing a price range that while under its previous valuation seems relatively reasonable, may open the door for coming enterprise initial public offerings. Cloud security company Zscaler also made its debut earlier this week, with the stock doubling once it began trading on the Nasdaq. Zuora will list on the New York Stock Exchange under the ticker “ZUO.” Zuora CEO Tien Tzuo told The Information in October last year that it expected to go public this year.

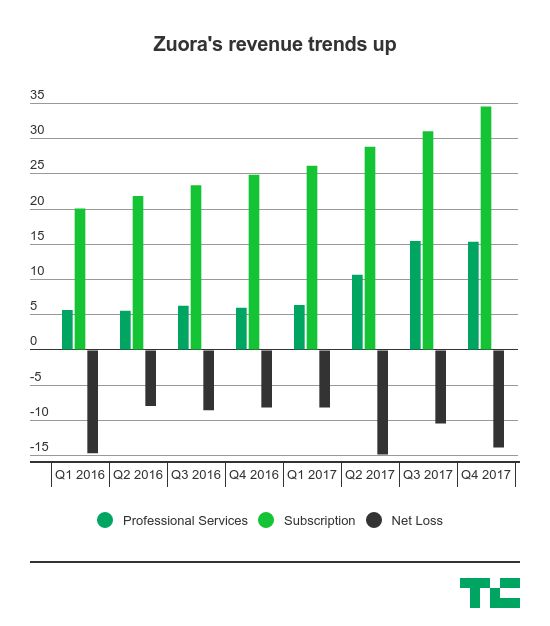

Zuora’s numbers show some revenue growth, with its subscriptions services continue to grow. But its losses are a bit all over the place. While the costs for its subscription revenues is trending up, the costs for its professional services are also increasing dramatically, going from $6.2 million in Q4 2016 to $15.6 million in Q4 2017. The company had nearly $50 million in overall revenue in the fourth quarter last year, up from $30 million in Q4 2016.

But, as we can see, Zuora’s “professional services” revenue is an increasing share of the pie. In Q1 2016, professional services only amounted to 22% of Zuora’s revenue, and it’s up to 31% in the fourth quarter last year. It also accounts for a bigger share of Zuora’s costs of revenue, but it’s an area that it appears to be investing more.

Zuora’s core business revolves around helping companies with subscription businesses — like, say, Dropbox — better track their metrics like recurring revenue and retention rates. Zuora is riding a wave of enterprise companies finding traction within smaller teams as a free product and then graduating them into a subscription product as more and more people get on board. Eventually those companies hope to have a formal relationship with the company at a CIO level, and Zuora would hopefully grow up along with them.

Snap effectively opened the so-called “IPO window” in March last year, but both high-profile consumer IPOs — Blue Apron and Snap — have had significant issues since going public. While both consumer companies, it did spark a wave of enterprise IPOs looking to get out the door like Okta, Cardlytics, SailPoint and Aquantia. There have been other consumer IPOs like Stitch Fix, but for many firms, enterprise IPOs serve as the kinds of consistent returns with predictable revenue growth as they eventually march toward an IPO.

The filing says it will raise up to $100 million, but you can usually ignore that as it’s a placeholder. Zuora last raised $115 million in 2015, and was PitchBook data pegged the valuation at around $740 million, according to the Silicon Valley Business Journal. Benchmark Capital and Shasta Ventures are two big investors in the company, with Benchmark still owning around 11.1% of the company and Shasta Ventures owning 6.5%. CEO Tien Tzuo owns 10.2% of the company.

Powered by WPeMatico

Stitch Fix revised where it would price its IPO lower last night ahead of trading, and it looks like it helped approach the right sweet spot as a result when it made its debut today. The company saw around a 15% pop in its stock when it began trading this morning — the benchmark companies tend to look to hit when they go public is around 20% — and fell around the lower bounds of… Read More

Stitch Fix revised where it would price its IPO lower last night ahead of trading, and it looks like it helped approach the right sweet spot as a result when it made its debut today. The company saw around a 15% pop in its stock when it began trading this morning — the benchmark companies tend to look to hit when they go public is around 20% — and fell around the lower bounds of… Read More

Powered by WPeMatico

MongoDB, a database software company based in New York, has filed to go public with the Securities and Exchange Commission as it continues to burn a ton of cash despite its revenue almost doubling year-over-year. The company, which provides open-source database software that became very attractive among early-stage startups, is one of a myriad of companies that have sought to go public by… Read More

MongoDB, a database software company based in New York, has filed to go public with the Securities and Exchange Commission as it continues to burn a ton of cash despite its revenue almost doubling year-over-year. The company, which provides open-source database software that became very attractive among early-stage startups, is one of a myriad of companies that have sought to go public by… Read More

Powered by WPeMatico

Things are not going so well for Blue Apron this morning after reporting its second-quarter earnings (its first earnings report ever), and the stock is crashing as a result of it. The company’s stock is down more than 14 percent on the earnings report, which came in pretty mixed compared to what Wall Street wanted. Read More

Things are not going so well for Blue Apron this morning after reporting its second-quarter earnings (its first earnings report ever), and the stock is crashing as a result of it. The company’s stock is down more than 14 percent on the earnings report, which came in pretty mixed compared to what Wall Street wanted. Read More

Powered by WPeMatico