IPO

Auto Added by WPeMatico

Auto Added by WPeMatico

This morning DigitalOcean, a provider of cloud computing services to SMBs, filed to go public. The company intends to list on the New York Stock Exchange (NYSE) under the ticker symbol “DOCN.”

DigitalOcean’s offering comes amidst a hot streak for tech IPOs, and valuations that are stretched by historical norms. The cloud hosting company was joined by Coinbase in filing its numbers publicly today.

DigitalOcean’s offering comes amidst a hot streak for tech IPOs.

However, unlike the cryptocurrency exchange, DigitalOcean intends to raise capital through its offering. Its S-1 filing lists a $100 million placeholder number, a figure that will update when the company announces an IPO price range target.

This morning let’s explore the company’s financials briefly, and then ask ourselves what its results can tell us about the cloud market as a whole.

TechCrunch has covered DigitalOcean with some frequency in recent years, including its early-2020 layoffs, its early-2020 $100 million debt raise and its $50 million investment from May of the same year that prior investors Access Industries and Andreessen Horowitz participated in.

From those pieces we knew that the company had reportedly reached $200 million in revenue during 2018, $250 million in 2019 and that DigitalOcean had expected to reach an annualized run rate of $300 million in 2020.

Those numbers held up well. Per its S-1 filing, DigitalOcean generated $203.1 million in 2018 revenue, $254.8 million in 2019 and $318.4 million in 2020. The company closed 2020 out with a self-calculated $357 million in annual run rate.

During its recent years of growth, DigitalOcean has managed to lose modestly increasing amounts of money, calculated using generally accepted accounting principles (GAAP), and non-GAAP profit (adjusted EBITDA) in rising quantities. Observe the rising disconnect:

Powered by WPeMatico

Hims & Hers, a San Francisco-based telehealth startup that sells sexual wellness and other health products and services to millennials, began trading publicly today on the NYSE after completing a reverse merger with the blank-check company Oaktree Acquisition Corp.

Its shares slipped a bit, ending the day down 5% from where they started, but the company, which was founded in 2017 and now claims nearly 300,000 paying subscribers for its various offerings, has never been focused on a splashy headline about its first-day performance, co-founder and CEO Andrew Dudum told us earlier today.

On the contrary, Dudum says that while Hims might have once imagined a traditional IPO, it decided to go the special purpose acquisition company (SPAC) route because of their pricing mechanisms and because it was approached by a SPAC led by renowned money manager Howard Marks, the founder of the global alternative investment firm Oaktree Capital Management. (“We fell in love with the Oaktree team and the capital market experience and deep resources they have.”)

We talked with Dudum about that SPAC’s structure; the lockups involved now that Hims’ shares are trading; and how much of the business still centers around one of its first offerings, which was a generic version of erectile dysfunction pills. Our conversation has been edited lightly for length and clarity.

TC: You’re a Bay Area-based company selling to a mostly U.S. audience. How are you thinking about expanding that footprint geographically?

AD: We do have a small operation selling in the U.K.; we’re getting our feet wet in that market and building out a team and infrastructure and fulfillment. If you look at the regulatory landscape, there’s a huge amount of room [to grow] in Europe, Australia, Canada, the Middle East and Asia, and so in that order, we’ll start to [move into those markets].

TC: What is your average customer cost?

AD: It has come down from $200 when we first launched, to roughly $100 last year, and we make, on average, close to $300 in the first couple of years in terms of a patient’s lifetime value.

TC: How quickly do customers churn?

AD: We break down lifetime value projections by quarter cohorts, and quarter over quarter, year over year, we’re monetizing each of these cohorts better, with high-margin profiles.

As of last quarter, the business was growing 90% year-over-year, with 76% gross margins and greater cash efficiency, and that’s because as we provide more offerings, there is more cross-purchasing. Also, word of mouth is becoming more of a dynamic, with more than 50% of the traffic to the site free at this point because we have built a brand with a young demographic.

TC: When are you projecting that you’ll turn profitable?

AD: We’ve reduced our annual burn and increased our margin efficiency and organic growth, so on a quarterly basis, we think in the next couple of years is a real possibility.

Image Credits: Hims & Hers

TC: Hims’ first wellness offerings included pills for male pattern hair loss and erectile dysfunction. How much revenue does that ED business account for?

AD: What we’ve disclosed is that roughly half [of our revenue] is that sexual health category — which includes [medicines for] generic erectile dysfunction, birth control, STDs, UTIs and premature ejaculation. The other half is predominately dermatology, including hair care [to address hair loss] and acne, and we’ve more recently moved into primary care and behavioral health.

TC: For retail investors, how do you differentiate the business from that of your rival Ro, which heavily promotes its ED products?

AD: There are a number of core differences between us and public and private players. First is our real focus on diversifying our offerings. With our focus on sexual health, dermatology, primary care and behavioral health, it’s in our DNA to quickly expand into new businesses.

We also think we’re different from most [rivals] in that we really invest time in building deep relationships with [those who represent] the future of healthcare markets — people in their teens, 20s and 30s. This demographic has a different set of tech expectations and consumer expectations than people in their 40s, 50s and 60s, and if we want to build for the future, that means building for the largest body of payers in the future.

Traditional healthcare companies monetize only the sick, but optimizing around that demographic precludes you from understanding what the next generation really needs and wants. I’ve never seen such a divergence between a patient population and legacy experience, and that’s a real advantage to us as a business.

TC: Hims just went public through a SPAC in a deal that gives the company around $280 million in cash — $205 million of that from Oaktree’s blank-check company and another $75 million through a private placement deal. How much runway does that give you?

AD: The company doesn’t burn a tremendous amount — between $10 million and $20 million a year — so a relatively long runway if we keep operating the business as is. But it does allow us to expand and grow into new businesses, too, including into big categories like sleep, infertility, diabetes and other chronic conditions.

TC: What about acquisitions?

AD: We’ll keep an eye open for strategic opportunities and consolidation opportunities. More than a dozen businesses a month come to us to be consolidated into the brand, but generally speaking, we’ve had the belief that so much is in front of us that we don’t want to be distracted.

TC: Is there a lockup period for anyone?

AD: There’s a traditional lockup for executives and employees and the board.

TC: Did your SPAC sponsors get a board seat?

AD: No.

TC: How much do they now own of the company, and can they sell?

AD: Oaktree owns a couple percent and [the syndicate they brought to do the private placement] [owns] 12%. But the very reason we went with them was the quality of the team and the organization . . . and they have the added incentive for the next year or two from a compensation standpoint for the company to succeed and to prove [out their thesis that Hims is a smart investment].

TC: Do you think the traditional IPO process is broken?

AD: The traditional IPO market hasn’t changed. It takes 12 to 18 months of preparation, which is a crazy amount of time for management to be distracted, then there’s this one-day PIPE that gives institutions a tremendous amount of money instantaneously. Maybe it makes for a good CNBC headline, but at tremendous cost to the company. It’s atrocious. If you were a founder or employee and getting diluted twice as much as you have to be, you’d be really upset. It’s no surprise to me that founders like myself are looking at other modalities with better pricing and better structures.

Powered by WPeMatico

As expected, shares of Poshmark exploded this morning, blasting over 130% higher in afternoon trading from the company’s above-range IPO price of $42. The enormous and noisy debut of Poshmark comes a day after Affirm, another IPO, was treated similarly by the public markets.

Both explosive debuts were preceded by huge December debuts from C3.ai, Doordash and Airbnb. It seems today that any venture-backed company that can claim some sort of tech mantle is being treated to a strong IPO pricing run and a huge first-day result.

This is, of course, annoying to some people. Namely, certain elements of the venture capital community who would prefer to keep all outsized gains in their own pockets. But, no matter. You might be wondering what is going on. Let’s talk about it.

TechCrunch has covered the IPO window as closely as we can over the last few years. And the late-stage venture capital markets, along with the changing value of tech stocks and the huge boom in consumer (retail) investing.

Based on my participation in as much of that reporting as I could take part in here’s how you get a 130% first-day IPO pop in a company that has actually been around long enough for investors to math-out reasonable growth and profit expectations for the future:

Powered by WPeMatico

UiPath, the robotic process automation startup that has been growing like gangbusters, filed confidential paperwork with the SEC today ahead of a potential IPO.

“UiPath, Inc. today announced that it has submitted a draft registration statement on a confidential basis to the U.S. Securities and Exchange Commission (the “SEC”) for a proposed public offering of its Class A common stock. The number of shares of Class A common stock to be sold and the price range for the proposed offering have not yet been determined. UiPath intends to commence the public offering following completion of the SEC review process, subject to market and other conditions,” the company said in a statement.

The company has raised more than $1.2 billion from investors like Accel, CapitalG, Sequoia and others. Its biggest raise was $568 million led by Coatue on an impressive $7 billion valuation in April 2019. It raised another $225 million led by Alkeon Capital last July when its valuation soared to $10.2 billion.

At the time of the July raise, CEO and co-founder Daniel Dines did not shy away from the idea of an IPO, telling me:

We’re evaluating the market conditions and I wouldn’t say this to be vague, but we haven’t chosen a day that says on this day we’re going public. We’re really in the mindset that says we should be prepared when the market is ready, and I wouldn’t be surprised if that’s in the next 12-18 months.

This definitely falls within that window. RPA helps companies take highly repetitive manual tasks and automate them. So for example, it could pull a number from an invoice, fill in a number in a spreadsheet and send an email to accounts payable, all without a human touching it.

It is a technology that has great appeal right now because it enables companies to take advantage of automation without ripping and replacing their legacy systems. While the company has raised a ton of money, and seen its valuation take off, it will be interesting to see if it will get the same positive reception as companies like Airbnb, C3.ai and Snowflake.

Powered by WPeMatico

Affirm, a consumer finance business founded by PayPal mafia member Max Levchin, filed to go public this afternoon.

The company’s financial results show that Affirm, which doles out personalized loans on an installment basis to consumers at the point of sale, has an enticing combination of rapidly expanding revenues and slimming losses.

Growth and a path to profitability has been a winning duo in 2020 as a number of unicorns with similar metrics have seen strong pricing in their debuts, and winsome early trading. Affirm joins DoorDash and Airbnb in pursuing an exit before 2020 comes to a close.

Let’s get a scratch at its financial results, and what made those numbers possible.

Affirm recorded impressive historical revenue growth. In its 2019 fiscal year, Affirm booked revenues of $264.4 million. Fast forward one year and Affirm managed top line of $509.5 million in fiscal 2020, up 93% from the year-ago period. Affirm’s fiscal year starts on July 1, a pattern that allows the consumer finance company to fully capture the U.S. end-of-year holiday season in its figures.

The San Francisco-based company’s losses have also narrowed over time. In its 2019 fiscal year, Affirm lost $120.5 million on a fully-loaded basis (GAAP). That loss slightly fell to $112.6 million in fiscal 2020.

More recently, in its first quarter ending September 30, 2020, Affirm kept up its pattern of rising revenues and falling losses. In that three-month period, Affirm’s revenue totaled $174.0 million, up 98% compared to the year-ago quarter. That pace of expansion is faster than the company managed in its most recent full fiscal year.

Accelerating revenue growth with slimming losses is investor catnip; Affirm has likely enjoyed a healthy tailwind in 2020 thanks to the COVID-19 pandemic boosting ecommerce, and thus gave the unicorn more purchase in the realm of consumer spend.

Again, comparing the company’s most recent quarter to its year-ago analog, Affirm’s net losses dipped to just $15.3 million, down from $30.8 million.

Affirm’s financials on a quarterly basis — located on page 107 of its S-1 if you want to follow along — give us a more granular understanding of how the fintech company performed amidst the global pandemic. After an enormous fourth quarter in calendar year 2019, growing its revenues to $130.0 million from $87.9 million in the previous quarter, Affirm managed to keep growing in the first, second, and third calendar quarters of 2020. In those periods, the consumer fintech unicorn recorded a top line of $138.2 million, $153.3 million, and $174 million, as we saw before.

Perhaps best of all, the firm turned a profit of $34.8 million in the quarter ending June 30, 2020. That one-time profit, along with its slim losses in its most recent period make Affirm appear to be a company that won’t hurt for future net income, provided that it can keep growing as efficiently as it has recently.

The pandemic has had more impact on Affirm than its raw revenue figures can detail. Luckily its S-1 filing has more notes on how the company adapted and thrived during this Black Swan year.

Certain sectors provided the company with fertile ground for its loan service. Affirm said that it saw an increase in revenue from merchants focused on home-fitness equipment, office products, and home furnishings during the pandemic. For example, its top merchant partner, Peloton, represented approximately 28% of its total revenue for the 2020 fiscal year, and 30% of its total revenue for the three months ending September 30, 2020.

Peloton is a success story in 2020, seeing its share price rise sharply as its growth accelerated across an uptick in digital fitness.

Investors, while likely content to cheer Affirm’s rapid growth, may cast a gimlet eye at the company’s dependence for such a large percentage of its revenue from a single customer; especially one that is enjoying its own pandemic-boost. If its top merchant partner losses momentum, Affirm will feel the repercussions, fast.

Regardless, Affirm’s model is resonating with customers. We can see that in its gross merchandise volume, or total dollar amount of all transactions that it processes.

GMV at the startup has grown considerably year-over-year, as you likely expected given its rapid revenue growth. On page 22 of its S-1, Affirm indicates that in its 2019 fiscal year, GMV reached $2.62 billion, which scaled to $4.64 billion in 2020.

Akin to the company’s revenue growth, its GMV did not grow by quite 100% on a year-over-year basis. What made that growth possible? Reaching new customers. As of September 30, 2020, Affirm has more than 3.88 million “active customers,” which the company defines as a “consumer who engages in at least one transaction on our platform during the 12 months prior to the measurement date.” That figure is up from 2.38 million in the September 30, 2019 quarter.

The growth is nice by itself, but Affirm customers are also becoming more active over time, which provides a modest compounding effect. In its most recent quarters, active customers executed an average of 2.2 transactions, up from 2.0 in third quarter of calendar 2019.

Also powering Affirm has been an ocean of private capital. For Affirm, having access to cash is not quite the same as a strictly-software company, as it deals with debt, which likely gives the company a slightly higher predilection for cash than other startups of similar size.

Luckily for Affirm, it has been richly funded throughout its life as a private company. The fintech unicorn has raised funds well in excess of $1 billion before its IPO, including a $500 million Series G in September of 2020, a $300 million Series F in April of 2019, and a $200 million Series E in December of 2017. Affirm also raised more than $400 million in earlier equity rounds, and a $100 million debt line in late 2016.

What to make of the filing? Our first-read take is that Affirm is coming out of the private markets as a healthier business than the average unicorn. Sure, it has a history of operating losses and not yet proven its ability to turn a sustainable profit, but its accelerating revenue growth is promising, as are its falling losses.

More tomorrow, with fresh eyes.

Powered by WPeMatico

David Chao, the cofounder of the cross-border venture firm DCM, speaks English, Japanese, and Mandarin. But he also knows how to talk to founders.

It’s worth a lot. Consider that DCM could see more than $1 billion from the $26.4 million it invested across 14 years in the cloud-based business-to-business payments company Bill.com, starting with its A round. Indeed, by the time Bill.com went public last December, when its shares priced at $22 apiece, DCM’s stake — which was 16% sailing into the IPO — was worth a not-so-small fortune.

Since then, Wall Street’s lust for both digital payments and subscription-based revenue models has driven Bill.com’s shares to roughly $90 each. Little wonder that in recent weeks, DCM has sold roughly 70 percent of a stake that’s currently valued at roughly $900 million and was worth more than $1 billion a few weeks ago. (It still owns 30 percent of its position and says the shares are free and clear to trade.)

We talked with Chao earlier today about Bill.com, on whose board he sits and whose founder, René Lacerte, is someone Chao backed previously. We also talked about another very lucrative stake DCM holds right now, about DCM’s newest fund, and about how Chao navigates between the U.S. and China as relations between the two countries worsen. Our conversation has been edited lightly for length and clarity.

TC: I’m seeing you owned about 33% of Bill.com after the first round. How did that initial check come to pass? Had you invested before in Lacerte?

DC: That’s right. René started [an online payroll] company called PayCycle and we’d backed him and it sold to Intuit [in 2009] and René made good money and we made money. And when he wanted to start this next thing, he said, ‘Look, I want to do something that’s a bigger outcome. I don’t want to sell the company along the way. I just want this time to do a big public company.’

TC: Why did he sell PayCycle if that was his ambition?

DC: It was largely because when you’re a first-time CEO and entrepreneur and a large company offers you the chance to make millions and millions of dollars, you’re a bit more tempted to sell the company. And it was a good price. For where the company was, it was a decent price.

Bill.com was a little bit different. We had good offers before going public. We even had an offer right before we went public. But René said, ‘No, this time, I want to go all the way.’ And he fulfilled that promise he’d made to himself. It’s a 14-year success story.

TC: You’ve sold most of your stake in recent weeks; how does that outcome compare with other recent exits for DCM?

DC: We actually have another recent one that’s phenomenal. We invested in a company called Kuaishou in China. It’s the largest competitor to Bytedance’s TikTok in China. We’ve invested $49.3 million altogether and now that stake is worth $3.8 billion. The company is still private held, but we actually cashed out around 15% of our holdings. and with just that sale alone we’ve already [seen 10 times] that $30 million.

TC: How do you think about selling off your holdings, particularly once a company has gone public?

DC: It’s really case by case. In general, once a company goes public, we probably spend somewhere between 18 months to three years [unwinding our position]. We had two big IPOs in Japan last year. One company [has] a $1.6 billion market cap; the other is a $2.6 billion company. There are some [cases] that are 12 months and there are some [where we own some shares] for four or five years.

TC: What types of businesses are these newly public companies in Japan?

DC: They’re both B2B. One is pretty much the Bill.com of Japan. The other makes contact management software

TC: Isn’t DCM also an investor in Blued, the LGBTQ dating app that went public in the U.S. in July?

DC: Yes, our stake wasn’t very big, but we were probably the first major VC to jump in because it was controversial.

TC: I also saw that you closed a new $880 million early stage fund this summer.

DC: Yes, that’s right. It was largely driven by the fact that many of our funds have done well. We’re now on fund nine, but our fund seven is on paper today 9x, and even the fund that Bill.com is in, fund four, is now more than 3x. So is fund five. So we’re in a good spot.

TC: As a cross-border fund, what does the growing tension between the U.S and China mean for your team and how it operates?

DC: It’s not a huge impact. If we were currently investing in semiconductor companies, for example, I think it would be a pretty rough period, because [the U.S.] restricts all the money coming from any foreign sources. At least, you’d be under strong scrutiny. And if we invested in a semiconductor company in China, you might not be able to go public in the U.S.

But the kinds of deals that we do, which are largely B2B and B2C — more on the software and services side — they aren’t as impacted. I’d say 90% of our deals in China focus on the domestic market. And so it doesn’t really impact us as much.

I think some of the Western institutions putting money into the Chinese market — that might be decreasing, or at least they’re a little bit more on the sidelines, trying to figure out whether they should be continuing to invest in China. And maybe for Chinese companies, less companies will go public in the U.S., etcetera. But some of these companies can go public in Hong Kong.

TC: How you feel about the U.S. administration’s policies? Do you understand them? Are you frustrated by them?

DC: I think it requires patience, because what [is announced and] goes on the news, versus what is really implemented and how it truly affects the industry, there’s a huge gap.

[Correction: This story originally reported that DCM had sold nearly $900 worth of shares and maintains another 30%; the firm’s entire position is currently worth $900 million, with 30% of those shares still held.]

Powered by WPeMatico

Today is the day for huge VC returns.

We talked a bit about Sequoia’s coming huge win with the IPO of game engine Unity this morning. Now, Sequoia might actually have the second largest return among companies filing to go public with the SEC today.

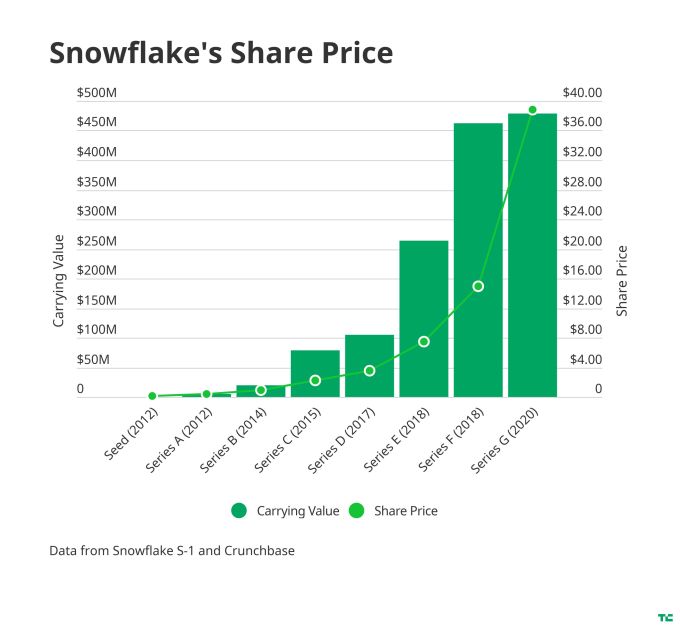

Snowflake filed its S-1 this afternoon, and it looks like Sutter Hill is going to make bank. The long-time VC firm, which invests heavily in the enterprise space and generally keeps a lower media profile, is the big winner across the board here, coming out with an aggregate 20.3% stake in the data management platform, which was last privately valued at $12.4 billion earlier this year. At its last valuation, Sutter Hill’s full stake is worth $2.5 billion. My colleagues Ron Miller and Alex Wilhelm looked a bit at the financials of the IPO filing.

Sutter Hill has been intimately connected to Snowflake’s early build-out and success, providing a $5 million Series A funding back in 2012, the year of the company’s founding, according to Crunchbase.

Now, there are some caveats on that number. Sutter Hill Ventures (aka “the fund”) owns roughly 55% of the firm’s total stake, with the balance owned by other entities owned by the firm’s management committee members. Michael Speiser, the firm’s partner who sits on Snowflake’s board, owns slightly more than 10% of Sutter Hill’s stake directly himself according to the SEC filing.

In addition to Sutter Hill, Sequoia also got a large slice of the data computing company: its growth fund is listed as having an 8.4% stake in the coming IPO. That makes for two Sequoia Growth IPOs today — a nice way to start the week this Monday afternoon.

Finally, Altimeter Capital, which did the Series C, owns 14.8%; ICONIQ owns 13.8%; and Redpoint, which did the Series B, owns 9.0%.

To see the breakdown in returns, let’s start by taking a look at the company’s share price and carrying values for each of its rounds of capital:

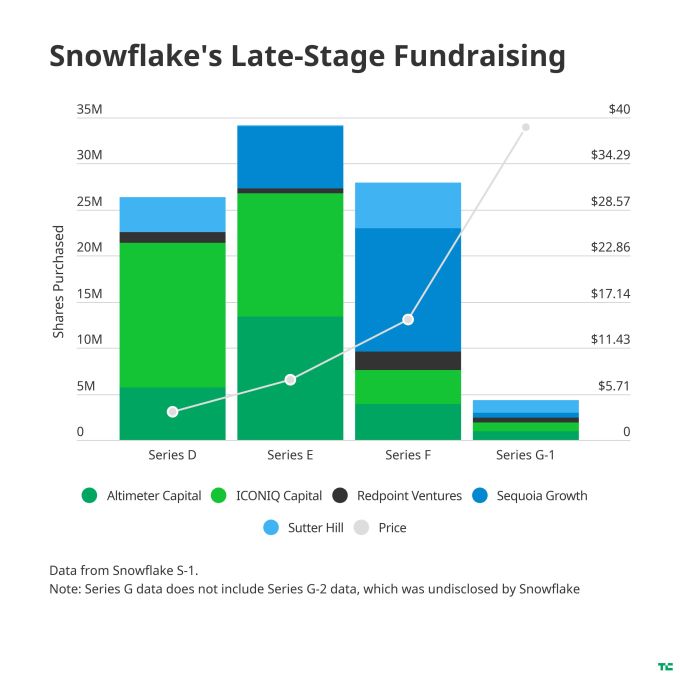

On top of that, what’s interesting is that Snowflake broke down the share purchases by firm for the last four rounds (D through G-1) the company fundraised:

That level of detail actually allows us to grossly compare the multiples on invested capital for these firms.

Sutter Hill, despite owning large sections of the company early on, continued to buy up shares all the way through the Series G, investing an additional $140 million in the later-stage rounds of the company. Adding in the entirety of its $5 million Series A round and a bit from the Series B assuming pro rata, the firm is looking on the order of a 16x return (assuming the IPO price is at least as good as the last round price).

Outside Sutter Hill, Redpoint has the best multiple return profile, given that it only invested $60 million in these later-stage rounds while still maintaining a 9.0% ownership stake. Both Sutter Hill and Redpoint purchased roughly 20% of their overall stakes in these later-stage rounds. Doing some roughly calculating, Redpoint is looking at a return of about 12-13x.

Sequoia’s multiple on investment is capped a bit given that it only invested in the most recent funding rounds. Its 8.4% stake was purchased for nearly $272 million, all of which came in these late-stage rounds. At Snowflake’s last round valuation of $12.4 billion, Sequoia’s stake is valued at $1.04 billion — a return of slightly less than 4x. That’s very good for mezzanine capital, but nothing like the multiple that Sutter Hill or Redpoint got for investing early.

Doing the same back-of-the-envelope math and Altimeter is looking at a better than 6x return, and ICONIQ got 7x. As before, if the stock zooms up, those returns will look all the better (and of course, if the stock crashes, well…)

One final note: The pattern for these last four funding rounds is unusual for venture capital: Snowflake appears to have “spread the love around,” having multiple firms build up stakes in the startup over several rounds rather than having one definitive lead.

Powered by WPeMatico

Software valuations are bonkers, which means it’s a great time to go public. Asana, Monday.com, Wrike and every other gosh darn software company that is putting it off, pay attention. Heck, even service-y Palantir could excel in this market.

Let me explain.

Over the past few weeks, TechCrunch has tracked the filing, first pricing, rejiggered pricing range, and, today, the first day of trading for BigCommerce, a Texas-based e-commerce company. You can think of it as a comp with Shopify to a degree.

Image Credits: IMGFlip (opens in a new window)

In the wake of the Canadian phenom’s blockbuster earnings report, BigCommerce boosted its IPO range. Yesterday the company did itself one better, pricing $1 per share above that raised range, selling 9,019,565 shares at $24 per share, of which 6,850,000 came from BigCommerce itself.

Before some additions, there are now 65,843,546 shares of BigCommerce in the world, giving the company an IPO valuation of around $1.58 billion.

Given that the company’s Q2 expected revenue range is “between $35.5 million and $35.8 million,” the company sported a run-rate multiple of 11.1x to 11x, depending on where its final revenue tally comes in. That felt somewhat reasonable, if perhaps a smidgen light.

Then the company opened at $68 per share today, currently trading for $82 per share. Hello, 1999 and other insane times. BigCommerce is now worth, using some rough math, around $5.4 billion, giving it a run-rate multiple of around 38x, using the midpoint of its Q2 revenue range.

Powered by WPeMatico

Now that I’ve offered an overview to help you think through where concentrated stock sits in your overall plan, let’s take a closer look at why selling can be challenging for some.

In the following section, I reveal the facts of the concentrated stock “get rich” myths that reside in the minds of many first-time concentrated stock owners, and I show why it is prudent to consider greater diversification.

Keep reading to learn more about the benefits of diversification, discover how much company stock is likely too much to hold, and the options you have when it comes to diversifying strategically.

There are several hard facts to keep in mind in contemplating maintaining a concentrated position:

The odds of any new IPO being among the top 4% is just slightly better than hitting your lucky number on the roulette wheel. But is your investment portfolio success and the odds of achieving your long-term financial goals something you want to spin the wheel on?

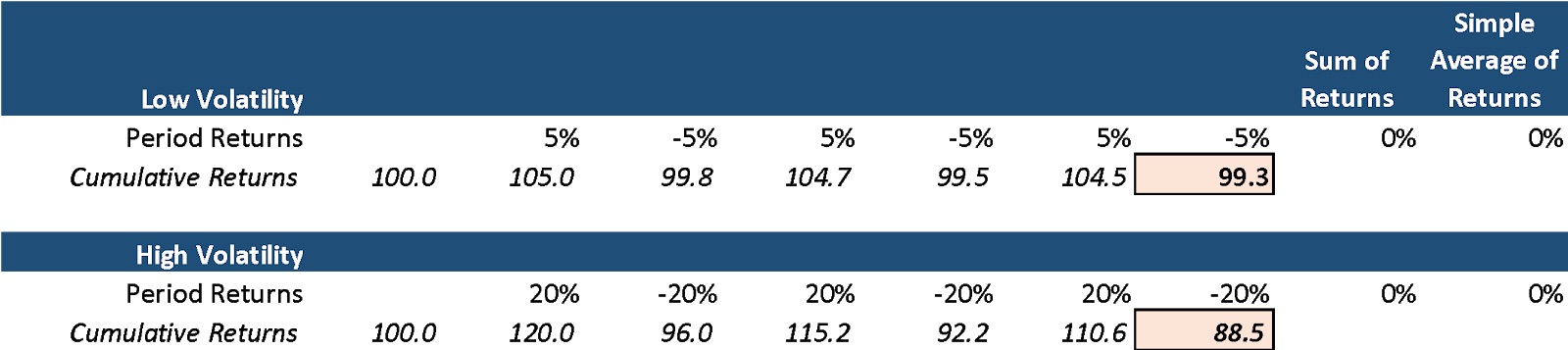

Excess volatility can harm returns. Note the example below that shows the comparison between a low-volatility diversified portfolio versus a high-volatility concentrated portfolio. Despite the same simple average return, the low-volatility portfolio below materially outperforms the high-volatility portfolio.

Image Credits: Peyton Carr

Beyond the math, unexpected spikes in volatility can cause significant price declines. Volatility increases the chances that an investor reacts emotionally and makes a poor investment decision. I’ll cover the behavioral finance aspect of this later. Lowering your portfolio volatility can be as simple as increasing your portfolio diversification.

The Russell 3000, an index representing the 3,000 largest U.S.-based publicly traded companies, has lower volatility when compared against 95%+ of all single stocks. So, how much return do you give up for having lower volatility?

According to Northern Trust Research, the 5.96% annualized average return of the Russell 3000 is 0.73% more than the 5.23% return of the median stock. Additionally, owning the Russell 3000, rather than a single stock, eliminates the likelihood of catastrophic loss scenarios — more than 20% of shares averaged a loss of more than 10% per year over a 20-year time frame.

If this establishes that the avoidance of overly concentrated portfolios is important, how much stock is too much? And at what price should you sell?

We consider any stock position or exposure greater than 10% of a portfolio to be a concentrated position. There is no hard number, but the appropriate level of concentration is dependent on several factors, such as your liquidity needs, overall portfolio value, the appetite for risk and the longer-term financial plan. However, above 10% and the returns and volatility of that single position can begin to dominate the portfolio, exposing you to high degrees of portfolio volatility.

The company “stock” in your portfolio often is only a fraction of your overall financial exposure to your company. Think about your other sources of possible exposure such as restricted stock, RSUs, options, employee stock purchase programs, 401k, other equity compensation plans, as well as your current and future salary stream tied to the company’s success. In most cases, the prudent path to achieving your financial goals involves a well-diversified portfolio.

Facts aside, maintaining a concentrated position in your company stock is far more tempting than taking a more measured approach. Token examples like Zuckerberg and Bezos tend to outshine the dull rationale of reality, and it’s hard to argue against the possibility of becoming fabulously wealthy by betting on yourself. In other words, your emotions can get the best of you.

But your goals — not your emotions — should be driving your investment strategy and decisions regarding your stock. Your investment portfolio and the company stock(s) within it should be used as tools to achieve those goals.

So first, we’ll take a deep dive into the behavioral psychology that influences our decision-making.

Despite all the evidence, sometimes that little voice remains.

“I want to hold the stock.”

Why is it so hard to shake? This is a natural human tendency. I get it. We have a strong impetus to rationalize our biases and not believe we are vulnerable to being influenced by them.

Becoming attached to your company is common, since after all, that stock has made you, or has the potential of making you wealthy. More often than not, selling and diversifying is the tough, but more rational decision.

Numerous studies have furnished insights into the correlation between investing and psychology. Many unrecognized psychological barriers and behavioral biases can influence you to hold concentrated stock even when the data shows that you should not.

Understanding these biases can be helpful when deciding what to do with your stock. These behavioral biases are hard to spot and even harder to overcome. However, awareness is the first step. Here are a few more common behavioral biases, see if any apply to you:

Familiarity bias: Familiarity is likely why so many founders are willing to hold concentrated positions in their own company’s stock. It is easy to confuse the familiarity with your own company with the safety in the stock. In the stock market, familiarity and safety are not always related. A great (safe) company sometimes can have a dangerously overvalued stock price, and terrible companies sometimes have terrifically undervalued stock prices. It’s not just about the quality of the company but the relationship between the quality of a company and its stock price that dictates whether a stock is likely to perform well in the future.

Another way this manifests is when a founder has less experience with stock market investing and has only owned their company stock. They may think the market has more risk than their company when in actuality, it is usually safer than holding just their individual position.

Overconfidence: Every investor is exhibiting overconfidence when they hold an overly concentrated position in an individual stock. Founders are likely to believe in their company; after all, it already achieved enough success to IPO. This confidence can be misplaced in the stock. Founders often are reluctant to sell their stock if it has been going up since they believe it will continue to go up. If the stock has sold off, the opposite is true, and they are convinced it will recover. Often, it is challenging for founders to be objective when they are so close to the company. They commonly believe that they have unique information and know the “true” value of the stock.

Anchoring: Some investors will anchor their beliefs to something they experienced in the past. If the price of the concentrated stock is down, investors may anchor their belief that the stock is worth its recent previous higher value and be unwilling to sell. This previous value of the stock is not an indicator of its real value. The real value is the current price where buyers and sellers exchange the stock while incorporating all presently available information.

Endowment effect: Many investors tend to place a higher value on an asset they currently own than if they did not own it at all. It makes it harder to sell. An excellent way to check for the endowment effect is to ask yourself: “If I did not own these shares, would I purchase them today at this price?” If you are not willing to purchase the shares at this price today, it likely means you are only holding onto the shares because of the endowment effect.

A fun spin on this is to look into the IKEA effect study, which demonstrates that people assign more value to something that they made than it is potentially worth.

When framed this way, investors can make more intentional decisions on whether to continue holding concentrated stock or selling. At times, these biases are hard to spot, which is why having a second person, a co-pilot, or an advisor, is helpful.

Congratulations to those of you with a concentrated stock position in your company; it is hard-earned and likely represents a material wealth. Understand, there is no “right” answer when it comes to managing concentrated stock. Each situation is unique, so it is essential to speak with a professional about options specific to your situation.

It starts with having a financial plan, complete with specific investment goals that you want to achieve. Once you have a clear picture of what you want to accomplish, you can look at the facts in a new light and gain a deeper appreciation for the dangers of holding a concentrated position in company stock versus the benefits of diversification, considering all of the implications and opportunities involved in rational decision-making and investment behavior.

Most individuals understand they can simply and directly sell their equity, but there are a variety of other strategies. Some of these opportunities may be far better at minimizing taxes or better at achieving the desired risk or return profile. Some might wonder what the best timing is to sell. I will cover these topics in the final article of the series.

Powered by WPeMatico

After going private in 2016 after accepting a $32 per share, or $4.3 billion, price from Apollo Global Management, Rackspace is looking once again to the public markets. First going public in 2008, Rackspace is taking second aim at a public offering around 12 years after its initial debut.

The company describes its business as a “multicloud technology services” vendor, helping its customers “design, build and operate” cloud environments. That Rackspace is highlighting a services focus is useful context to understand its financial profile, as we’ll see in a moment.

But first, some basics. The company’s S-1 filing denotes a $100 million placeholder figure for how much the company may raise in its public offering. That figure will change, but does tell us that firm is likely to target a share sale that will net it closer to $100 million than $500 million, another popular placeholder figure.

Rackspace will list on the Nasdaq with the ticker symbol “RXT.” Goldman, Citi, J.P. Morgan, RBC Capital Markets and other banks are helping underwrite its (second) debut.

Similar to other companies that went private, only later to debut once again as a public company, Rackspace has oceans of debt.

The company’s balance sheet reported cash and equivalents of $125.2 million as of March 31, 2020. On the other side of the ledger, Rackspace has debts of $3.99 billion, made up of a $2.82 billion term loan facility, and $1.12 billion in senior notes that cost the firm an 8.625% coupon, among other debts. The term loan costs a lower 4% rate, and stems from the initial transaction to take Rackspace private ($2 billion), and another $800 million that was later taken on “in connection with the Datapipe Acquisition.”

The senior notes, originally worth a total of $1,200 million or $1.20 billion, also came from the acquisition of the company during its 2016 transaction; private equity’s ability to buy companies with borrowed money, later taking them public again and using those proceeds to limit the resulting debt profile while maintaining financial control is lucrative, if a bit cheeky.

Rackspace intends to use IPO proceeds to lower its debt-load, including both its term loan and senior notes. Precisely how much Rackspace can put against its debts will depend on its IPO pricing.

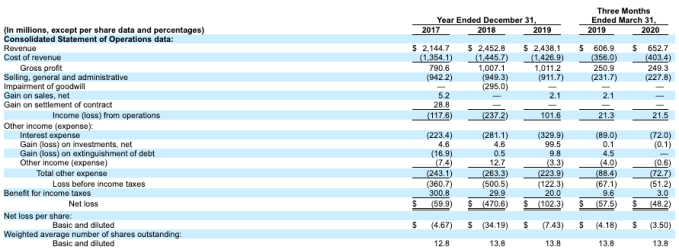

Those debts take a company that is comfortably profitable on an operating basis and make it deeply unprofitable on a net basis. Observe:

Image Credits: SEC

Looking at the far-right column, we can see a company with material revenues, though slim gross margins for a putatively tech company. It generated $21.5 million in Q1 2020 operating profit from its $652.7 million in revenue from the quarter. However, interest expenses of $72 million in the quarter helped lead Rackspace to a deep $48.2 million net loss.

Not all is lost, however, as Rackspace does have positive operating cash flow in the same three-month period. Still, the company’s multi-billion-dollar debt load is still steep, and burdensome.

Returning to our discussion of Rackspace’s business, recall that it said that it sells “multicloud technology services,” which tells us that its gross margins will be service-focused, which is to say that they won’t be software-level. And they are not. In Q1 2020 Rackspace had gross margins of 38.2%, down from 41.3% in the year-ago Q1. That trend is worrisome.

The company’s growth profile is also slightly uneven. From 2017 to 2018, Rackspace saw its revenue expand from $2.14 billion to $2.45 billion, growth of 14.4%. The company shrank slightly in 2019, falling from $2.45 billion in revenue in 2018 to $2.44 billion the next year. Given the economy that year, and the importance of cloud in 2019, the results are a little surprising.

Rackspace did grow in Q1 2020, however. The firm’s $652.7 million in first-quarter top-line easily bested in its Q1 2019 result of $606.9 million. The company grew 7.6% in Q1 2020. That’s not much, especially during a period in which its gross margins eroded, but the return-to-growth is likely welcome all the same.

TechCrunch did not see Q2 2020 results in its S-1 today while reading the document, so we presume that the firm will re-file shortly to include more recent financial results; it would be hard for the company to debut at an attractive price in the COVID-19 era without sharing Q2 figures, we reckon.

How to value Rackspace is a puzzle. The company is tech-ish, which means it will find some interest. But its slow growth rate, heavy debts and lackluster margins make it hard to pin a fair multiple onto. More when we have it.

Powered by WPeMatico