IPO

Auto Added by WPeMatico

Auto Added by WPeMatico

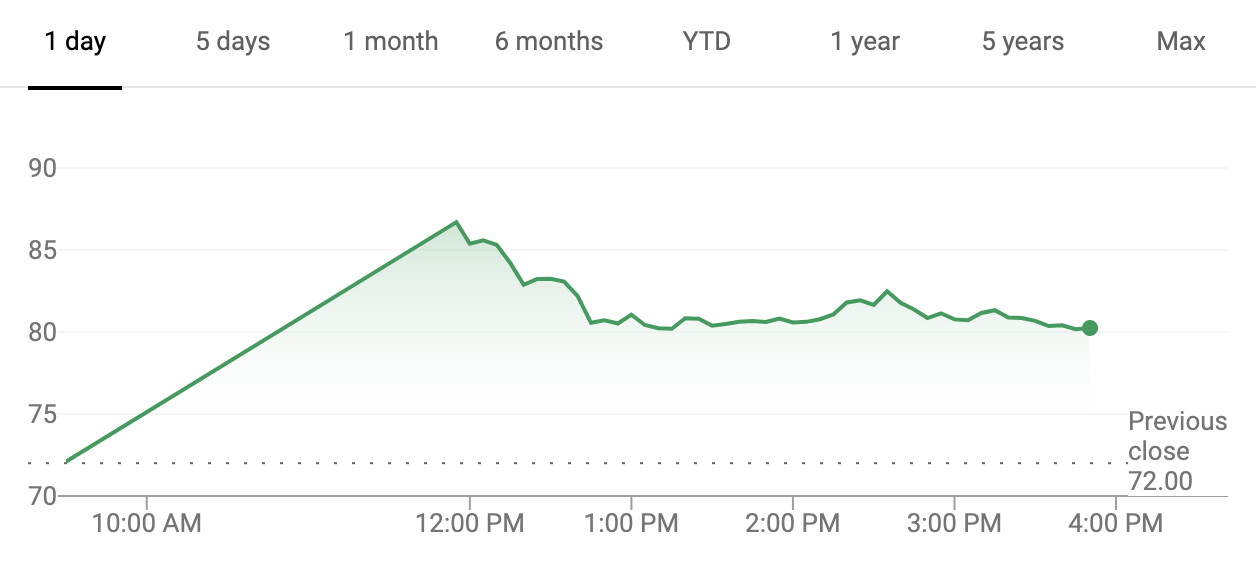

PagerDuty debuted on the New York Stock Exchange today, and as we type, shares of the nine-year-old, San Francisco-based incident response software company are trading at nearly $39.

That’s up more than 60 percent above their IPO range of $24 per share, which was itself adjusted from the range of $21 to $23 that had been expected earlier and gives the company a valuation of close to $3 billion. That’s an awful lot for a company whose software helps technical teams at 11,000 companies spot problems with applications and respond to incidents. Though it’s growing quickly — revenue was up 48 percent last year — it still pulled in just $117.8 million in 2018. Meanwhile, its net loss widened last year, to $40.7 million from $38.1 million in 2017.

Certainly, its performance has to make the company’s investors — who last assigned the company a valuation of $1.3 billion back in September — very happy. Some of the VCs poised to win big if PagerDuty’s shares continue flying high include Andreessen Horowitz, which owned 18.4 percent of PagerDuty’s shares sailing into the IPO; Accel, which owned 12.3 percent; and Bessemer, which owned 12.2 percent. Other winners include Baseline Ventures (6.7 percent) and Harrison Metal (5.3 percent).

It’s also exciting for CEO Jennifer Tejada, a proven operator who was brought in to lead PagerDuty in 2016 and now becomes part of a small — but growing — club of women CEOs to take their tech companies public, including Katrina Lake of Stitch Fix and Julia Hartz of Eventbrite.

We talked with Tejada earlier today about the company’s big day. In addition to crediting company co-founders (and shareholders) Andrew Miklas and Baskar Puvanathasan, both of whom have since left the company, Tejada thanked PagerDuty co-founder Alex Solomon, who remains the company’s CTO. She also told us a little bit about what today has been like, and how the IPO changes things — and doesn’t. Our chat has been edited for length.

TC: First and foremost, how are you feeling?

JT: It’s been an incredible day. It’s been an incredible several months. You have to enjoy it when it’s going well.

TC: How does the vision for the company change now that it’s public? Have you been thinking ahead to possible acquisitions?

JT: The vision doesn’t change. We intend to do exactly what we’ve been doing, which is to provide the best real-time operations platform available to companies as they undergo digital transformation to meet the growing demands of their customers. We think we’re [facing] an early and very large opportunity that will be available to us for a long time. So our job continues to be to build great products, stay close to our customers, expand regionally and continue doing what has allowed us to be a successful private company.

TC: You and I had talked about the challenges of retaining employees in San Francisco when we sat down together in November. It’s a battle for every local company. How do you keep employees beyond the lock-up period? How do you ensure they stay focused on performance and not your share price?

JT: I think that mindset of, ‘It’s all over when you go public,’ is kind of a Silicon Valley fable. If you look at the most successful SaaS companies on the planet, they’ve gained 10x, 20x, 30x their value post their IPO. I also think what employees look for ahead of their financial success is career success. Am I being developed and recognized and can I build my career at this company? And we’ve worked really hard to create those career opportunities for our employees who [I think see, as I do] the IPO like a racing boat pushing off the dock, across the starting line, and into the open ocean, where the next adventure awaits.

In the meantime, we’ve already lessened our reliance on [overheated job markets] by opening offices in Toronto and Atlanta and Seattle and London and Sydney, even while we’re still hiring in San Francisco and Seattle.

TC: Obviously, Lyft’s shares have been up and down, owing to short sellers. Have you been monitoring short interest? Are you at all concerned about investors driving the price sky high, then selling it on the way down?

JT: I haven’t even looked at the stock price in the last several hours . . . There are a lot of things outside of my control, and the free market is one of them.

TC: PagerDuty is rare in that is doesn’t have a dual-class structure, which can greatly empower leaders over everyone else associated with a company. Presumably, this is a great relief to your investors; I just wonder whether it was ever a consideration?

JT: I’m a little bit of a traditionalist. I’ve been around long enough to know how checks and balances work, and a single-class structure made sense for PagerDuty. Also, dual-class structures tend to emerge more when you have deeply involved founders, and though Alex is still very much a part of the business, PagerDuty’s other two founders have worked outside of the business for some time.

TC: You have plenty of operating experience, including previously running Keynote Systems, but you’ve never taken a company public. Were there ways in which you found the roadshow experience surprising?

JT: I was surprised by how fun it was! [Laughs.] When you have a great story, and a great partner helping you tell it — in my case that’s [PagerDuty CFO] Howard Wilson, who I’ve worked with for 10 years — it’s great. We had a great reception from investors. I loved our IPO team; our Top were both led by women and whenever I had a question, they [had the answer]. I also had this cocoon of experience surrounding me thanks to our board. If anyone tells you that [in this position] they are super comfortable, they’re either lying or [clueless] but I was very lucky. I also have a whole bunch of buddies who are CEOs [and other executives] in SaaS and I’ve been shaking them down for advice for months, so I felt well-prepared.

TC: What was some of the advice you received from those friends about how your life is about to change?

JT: Some of it was about the need to keep people focused and not get distracted, to remind everyone that this is a milestone, not the goal. [Some centered on] surrounding yourself with a great team and the importance of great investor relations, a function you don’t have as a private company but that can create huge value and provide support and understanding of the market.

One CEO said to just make sure you keep having fun, to try and stay “you,” to find joy in the same things as before. There will be stressful moments and tough questions — that’s true of any company that’s scaling — but I heard a lot of advice about just taking care of myself, including on the roadshow. In fact, there were a lot of really supportive notes and private tweets that, in a job that can feel lonely, made me feel not alone, and I’m very appreciative of that.

TC: People call IPOs just another funding event, but that’s kind of baloney, isn’t it? If you had to list the most meaningful moments in your life on a scale from 1 to 10, 1 being the most important, where might today fall? Would today be up there on that list?

JT: When I think of most meaningful moments, I think of the day my daughter was born, and my wedding. Another day that was very meaningful to me was when I approved our pledge to donate one percent [of PagerDuty’s equity, one percent of its product and one percent of employees’ time] to social impact. We did it a lot later in the game than some companies; our equity was already valuable. But we knew that it was going to create meaningful impact over time.

But yes, it is a gratifying day, especially for the co-founders who were pulling the idea together for PagerDuty a couple of years before they even launched it, and for employees who’ve been with the company for nearly as long and who turned down safer and higher-paying jobs along the way. Seeing their joy today — that is a memory that will be in my top 10 for sure.

Powered by WPeMatico

Pink confetti fell from the ceiling Friday as Lyft co-founders Logan Green and John Zimmer celebrated their company’s IPO. The stock offering was a bona fide success, with shares selling for $87.24 apiece Friday morning — 21 percent higher than Lyft’s initial $72 share price — and closing at $78.29 per share.

Lyft raised roughly $2.3 billion Thursday evening, hours before ringing the opening bell of the Nasdaq on Friday around noon Pacific. The IPO gave Lyft an initial market cap of about $24 billion, representing an 11x revenue multiple and a 1.6x step-up from its most recent private valuation of $15.1 billion.

On Bloomberg TV, Lyft’s co-founders discussed the company’s long-term prospects, including international growth, autonomous vehicle plans, the future of car ownership and insurance.

“We are confident that the business will be very profitable,” Green told Emily Chang. “We are making tremendous progress going after this once-in-a-generation shift where this entire industry, a $1.2 trillion market, could flip from an ownership model to a service model and we are leading the way there.”

The pair opted to host their IPO in Los Angeles, Lyft’s largest market.

“We want to make a point that you can both invest in communities and build a great business,” Zimmer said. “It was fun to ring the bell with several members of our driver community and have many of them participate in our IPO because we gave them a bonus to do so.”

Powered by WPeMatico

Lyft raised more than $2 billion Thursday afternoon after pricing its shares at $72 apiece, the top of the expected range of $70 to $72 per share. This gives Lyft a fully diluted market value of $24 billion.

The company will debut on the Nasdaq stock exchange Friday morning, trading under the ticker symbol “LYFT.”

The initial public offering is the first-ever for a ride-hailing business and represents a landmark liquidity event for private market investors, which had invested billions of dollars in the San Francisco-based company. In total, Lyft had raised $5.1 billion in debt and equity funding, reaching a valuation of $15.1 billion last year.

Lyft’s blockbuster IPO is unique for a number of reasons, in addition to being amongst transportation-as-a-service companies to transition from private to public. Lyft has the largest net losses of any pre-IPO business, posting losses of $911 million on revenues of $2.2 billion in 2018. However, the company is also raking in the largest revenues, behind only Google and Facebook, for a pre-IPO company. The latter has made it popular on Wall Street, garnering buy ratings from analysts prior to pricing.

Uber is the next tech unicorn, or company valued north of $1 billion, expected out of the IPO gate. It will trade on the New York Stock Exchange in what is one of the most anticipated IPOs in history. The company, which reported $3 billion in Q4 2018 revenues with net losses of $865 million, is reportedly planning to unveil its IPO prospectus next month.

Next in the pipeline is Pinterest, which dropped its S-1 last week and revealed a path to profitability that is sure to garner support from Wall Street investors. The visual search engine will trade on the NYSE under the symbol “PINS.” It posted revenue of $755.9 million last year, up from $472.8 million in 2017. The company’s net loss, meanwhile, shrank to $62.9 million last year from $130 million in 2017.

Other notable companies planning 2019 stock offerings include Slack, Zoom — a rare, profitable pre-IPO unicorn — and, potentially, Airbnb.

Updating.

Powered by WPeMatico

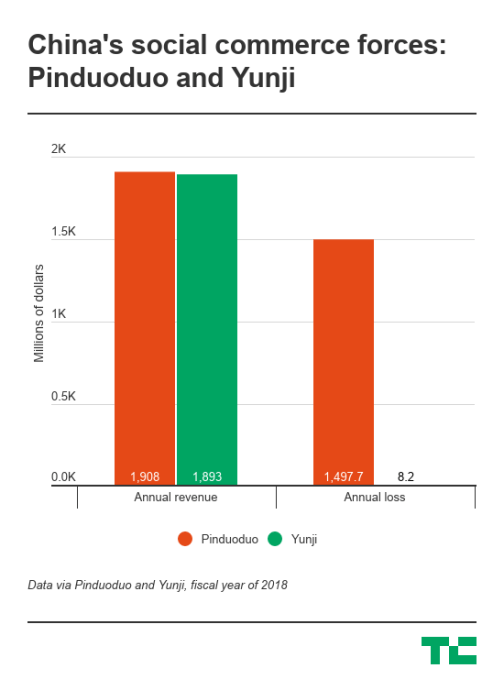

China’s Pinduoduo was all the rage in 2018 as the e-commerce upstart quickly rose to challenge Alibaba and raised $1.63 billion through a Nasdaq listing. Much of its success was attributable to its link to WeChat, China’s messaging leader. Now, another emerging e-commerce player that has leveraged WeChat is gearing up for a listing in the United States.

Yunji, which was founded in 2015 (the same year Pinduoduo launched), is raising up to $200 million according to its prospectus filed with the Securities and Exchange Commission last week. Reuters reported citing sources in September that Yunji planned to raise around $1 billion in the IPO at a valuation of between $7 billion and $10 billion.

Like Pinduoduo, Yunji bills itself as a “social e-commerce” service, which means it takes advantage of social relationships on apps like WeChat to acquire, engage and sell to users. The pair differ, however, in how exactly they make money. Pinduoduo generates the bulk of its revenues — nearly 90 percent in the fourth quarter — from advertising fees collected from merchants. This is akin to Alibaba’s marketplace play of connecting buyers and third-party sellers. Yunji, which was started by e-commerce veteran Xiao Shanglue, focuses on direct sales like Alibaba’s arch-foe JD.com, derived 88 percent of its fourth-quarter revenues from selling to users.

In terms of size, Yunji was about $15 million behind Pinduoduo in revenue last year. It had 23.2 million buyers in 2018, compared to Pinduoduo’s 272.6 million monthly active users. Yunji was, however, much closer to achieving profitability than Pinduoduo, which spent most of its money on sales and marketing. Most of Yunji’s expenses went to fulfillment and logistics.

From inception, Yunji has boasted of its “innovative” membership-based e-commerce model. To join, people typically pay a fee, upon which they gain access to a variety of benefits and discounts as well as the permission to open their own micro-stores. Members then get compensated for successfully selling to others and recruiting new members.

The marketing practice helped Yunji quickly build up a large network of users. As of 2018, Yunji had 7.4 million members who contributed 11.9 percent of its annual revenues and 66.4 percent of annual transactions. But the firm went too far in exploiting the social links it controlled that it started to look like a pyramid scheme, which is banned in China. In 2017, the local government slapped Yunji with a $1.4 million fine for pyramid selling. The firm subsequently apologized and promised to revamp its marketing strategy. For instance, to avoid crossing the red line of awarding salespeople with “material” or “financial” benefits, Yunji resorted to virtual Yun-coins, which are not redeemable for cash and can only be used as coupons for future purchase.

But Yunji is still on the edge. The company warns in its prospectus that China could at any time redefine what constitutes pyramid selling.

“[T]here is no assurance that the competent governmental authorities in China that we communicate with will not change their views, or the other relevant government authorities will share the same view as our PRC legal counsel, or they will find our business model, not in violation of any applicable regulations, given the uncertainties in the interpretation and application of existing PRC laws, regulations and policies relating to our current business model, including, but not limited to, regulations regulating pyramid selling.”

Some of Yunji’s more notable investors include China’s CDH Investments and Huaxing Growth Capital, China Renaissance’s subsidiary focusing on high-growth startups.

Powered by WPeMatico

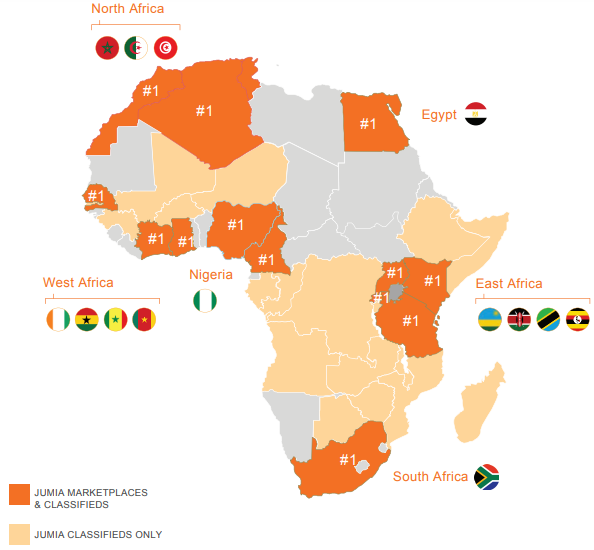

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange today, per SEC documents and confirmation from CEO Sacha Poignonnec to TechCrunch.

The valuation, share price and timeline for public stock sales will be determined over the coming weeks for the Nigeria-headquartered company.

With a smooth filing process, Jumia will become the first African tech startup to list on a major global exchange.

Poignonnec would not pinpoint a date for the actual IPO, but noted the minimum SEC timeline for beginning sales activities (such as road shows) is 15 days after submitting first documents. Lead adviser on the listing is Morgan Stanley .

There have been numerous press reports on an anticipated Jumia IPO, but none of them confirmed by Jumia execs or an actual SEC, S-1 filing until today.

Jumia’s move to go public comes as several notable consumer digital sales startups have faltered in Nigeria — Africa’s most populous nation, largest economy and unofficial bellwether for e-commerce startup development on the continent. Konga.com, an early Jumia competitor in the race to wire African online retail, was sold in a distressed acquisition in 2018.

With the imminent IPO capital, Jumia will double down on its current strategy and regional focus.

“You’ll see in the prospectus that last year Jumia had 4 million consumers in countries that cover the vast majority of Africa. We’re really focused on growing our existing business, leadership position, number of sellers and consumer adoption in those markets,” Poignonnec said.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a $326 funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries, spanning Ghana, Kenya, Ivory Coast, Morocco and Egypt. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Jumia has also opened itself up to traders and SMEs by allowing local merchants to harness Jumia to sell online. “There are over 81,000 active sellers on our platform. There’s a dedicated sellers page where they can sign-up and have access to our payment and delivery network, data, and analytic services,” Jumia Nigeria CEO Juliet Anammah told TechCrunch.

The most popular goods on Jumia’s shopping mall site include smartphones (priced in the $80 to $100 range), washing machines, fashion items, women’s hair care products and 32-inch TVs, according to Anammah.

E-commerce ventures, particularly in Nigeria, have captured the attention of VC investors looking to tap into Africa’s growing consumer markets. McKinsey & Company projects consumer spending on the continent to reach $2.1 trillion by 2025, with African e-commerce accounting for up to 10 percent of retail sales.

Jumia has not yet turned a profit, but a snapshot of the company’s performance from shareholder Rocket Internet’s latest annual report shows an improving revenue profile. The company generated €93.8 million in revenues in 2017, up 11 percent from 2016, though its losses widened (with a negative EBITDA of €120 million). Rocket Internet is set to release full 2018 results (with updated Jumia figures) April 4, 2019.

Jumia’s move to list on the NYSE comes during an up and down period for B2C digital commerce in Nigeria. The distressed acquisition of Konga.com, backed by roughly $100 million in VC, created losses for investors, such as South African media, internet and investment company Naspers .

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

As demonstrated in other global startup markets, consumer-focused online retail can be a game of capital attrition to outpace competitors and reach critical mass before turning a profit. With its unicorn status and pending windfall from an NYSE listing, Jumia could be better positioned than any venture to win on e-commerce at scale in Africa.

Powered by WPeMatico

Visual search engine Pinterest has joined a long list of high-flying technology companies planning to go public in 2019. The business has confidentially submitted paperwork to the Securities and Exchange Commission for an initial public offering slated for later this year, according to a report from The Wall Street Journal.

Pinterest declined to comment.

Founded in 2008 by Ben Silbermann, earlier reports indicated the company was planning to debut on the stock market in April. In late January, Pinterest took its first official step toward a 2019 IPO, hiring Goldman Sachs and JPMorgan Chase as lead underwriters for its offering.

The company garnered a $12.3 billion valuation in 2017 with a $150 million financing.

Touting 250 million monthly active users, Pinterest has raised nearly $1.5 billion in venture capital funding from key stakeholders Bessemer Venture Partners, Andreessen Horowitz, FirstMark Capital, Fidelity and SV Angel. The business brought in some $700 million in ad revenue in 2018, per reports, a 50 percent increase year-over-year.

Pinterest employs 1,600 people across 13 cities, including Chicago, London, Paris, São Paulo, Berlin and Tokyo. The company says half its users live outside the U.S.

Pinterest will likely follow Lyft, Uber and Slack to the public markets, which have all filed confidential paperwork for IPOs or, in Slack’s case, a reported direct listing, expected in the coming months.

Powered by WPeMatico

Slack, the provider of workplace communication and collaboration tools, has submitted paperwork with the Securities and Exchange Commission to go public later this year, the company announced on Monday.

This is its first concrete step toward becoming a publicly listed company, five years after it launched.

Headquartered in San Francisco, Slack has raised more than $1 billion in venture capital investment, including a $427 million funding round in August. The round valued the business at $7.1 billion, cementing its position as one of the most valuable privately held businesses in the U.S.

The company counted 10 million daily active users around the world and 85,000 paying users as of January 2019. According to data provided (via email) by SensorTower, Slack’s new users on mobile increased roughly 21 percent last quarter compared to Q4 2017, while total installs on mobile grew 24 million. The company recorded 8 million installs in 2018, up 21 percent year-over-year.

Slack’s investors include SoftBank’s Vision Fund, Dragoneer Investment Group, General Atlantic, T. Rowe Price Associates, Wellington Management, Baillie Gifford, Social Capital and IVP, as well as early investors Accel and Andreessen Horowitz.

Slack is one of several tech unicorns on deck to go public this year. Uber and Lyft have both similarly filed confidentially to go public in what are expected to be traditional initial public offerings. Slack, however, is expected to pursue a direct listing, following in Spotify’s footsteps. Instead of issuing new shares, Slack will sell directly to the market existing shares held by insiders, employees and investors, a move that will allow it to bypass a roadshow and some of Wall Street’s exorbitant IPO fees.

Powered by WPeMatico

Pinterest, the 11-year-old, San Francisco-based site known for the photos its users post about everything from wedding to beauty trends, has hired Goldman Sachs and JPMorgan Chase as lead underwriters for an IPO that it’s planning to stage later this year.

Reuters first reported the news. TechCrunch sources have since confirmed the development. A Pinterest spokesperson declined to “comment on rumors and speculation” when asked this afternoon for more information.

Pinterest has raised roughly $1.5 billion over the years and was valued at $12 billion by its private investors during its last fundraising round in 2017. Notably, its backers include Goldman Sachs Investment Partners, among many other investment firms, both early and later-stage, like Valiant Capital Partners, Wellington Management, Andreessen Horowitz and Bessemer Venture Partners.

The company’s revenue last year was $700 million, more than double what the company generated in revenue in 2017.

It has 250 million monthly active users, compared with the 200 million monthly active users who were on the platform as of mid 2017.

Whether Pinterest has ever been profitable, we couldn’t learn this afternoon. But the company employs 1,600 people across 13 cities globally, including Chicago, London, Paris, São Paulo, Berlin, and Tokyo, and half its users now live outside the U.S., with the international market its fastest-growing segment.

Perhaps unsurprisingly, more than 80 percent of people access the service via its mobile app.

Assessing how Pinterest’s shares might be received by public market shareholders has become a favorite parlor game for Silicon Valley denizens. In a recent report, the outlet The Information posited that Pinterest’s offering could suffer because it’s a social media company that’s frequently lumped together with companies like Facebook and Twitter that have repeatedly raised concerns about users’ privacy and have faced a nearly year-long backlash as a result.

Yet Pinterest is far afield from what most users think of as social media and more akin to a visual search and discovery platform, with people looking for ideas and inspiration rather than to reach other people. So thinks venture capitalist Venky Ganesan of Menlo Ventures, who noted on a recent TechCrunch podcast that “there are no Russian trolls” on Pinterest. More, he’d said, “I haven’t seen Pinterest sell [users’] data. They’re using data to [figure out] advertising on Pinterest; they aren’t brokering [that information] to others.”

Another potential concern for Pinterest is its reliance advertising, which is often the easiest expense for companies to slash when an economy begins to cool, as may be happening here in the U.S. Ads make up 100 percent of the company’s revenue. Here, too, however, Pinterest could prove more durable than some of its competitors. While brand-image driven advertising often gets cut when budgets tighten, direct response advertising often does even better in down markets, as companies seek out clearer returns on their investment, and much of Pinterest’s revenue is driven by direct response advertising. Users see, they click, and they buy. As Ganesan offered during that same podcast visit, “I’ve got three daughters at home, and they spend a lot of time on Pinterest, and they buy stuff.” (Ganesan isn’t an investor in the company; neither is the broader Menlo Ventures team.)

Pinterest could reportedly seek to raise up to $1.5 billion in an offering, according to past media reports. Whether it targets more or less, we’re likely to learn soon, but an IPO has been expected for some time, in part because the company is now getting up there in years as startups go, in part because of its continued growth, and in part because of some new hires that seemed to suggest the company has been gearing up to become publicly traded.

In November, for example, Pinterest brought aboard its first-ever chief marketing officer in Andréa Mallard, who joined the company from Athleta, Gap’s activewear brand, and who now oversees its global marketing and creative teams.

Roughly a year ago, Pinterest also recruited its first COO, hiring Francoise Brougher, who was previously a business lead at Square and a VP of SMB global sales and operations at Google before that.

In fact, unlike many of today’s buzziest companies, Pinterest seems to have retained almost all of the executives who work at the company with one notable exception, In late 2017, it parted ways with its then president, Tim Kendall, who’d been with Pinterest for more than five years at the time and who left to start his own health wellness company.

Powered by WPeMatico

It’s been 14 years since Mark Shuttleworth first founded and funded Canonical and the Ubuntu project. At the time, it was mostly a Linux distribution. Today, it’s a major enterprise player that offers a variety of products and services. Throughout the years, Shuttleworth self-funded the project and never showed much interest in taking outside money. Now, however, that’s changing.

As Shuttleworth told me, he’s now looking for investors as he looks to get the company on track to an IPO. It’s no secret that the company’s recent re-focusing on the enterprise — and shutting down projects like the Ubuntu phone and the Unity desktop environment — was all about that, after all. Shuttleworth sees raising money as a step in this direction — and as a way of getting the company in shape for going public.

“The first step would be private equity,” he told me. “And really, that’s because having outside investors with outside members of the board essentially starts to get you to have to report and be part of that program. I’ve got a set of things that I think we need to get right. That’s what we’re working towards now. Then there’s a set of things that private investors are looking for and the next set of things is when you’re doing a public offering, there’s a different level of discipline required.”

It’s no secret that Shuttleworth, who sports an impressive beard these days, was previously resistant to this, and he acknowledged as much. “I think that’s a fair characterization,” he said. “I enjoy my independence and I enjoy being able to make long-term calls. I still feel like I’ll have the ability to do that, but I do appreciate keenly the responsibility of taking other people’s money. When it’s your money, it’s slightly different.”

Refocusing Canonical on the enterprise business seems to be paying off already. “The numbers are looking good. The business is looking healthy. It’s not a charity. It’s not philanthropy,” he said. “There are some key metrics that I’m watching, which are the gate for me to take the next step, which would be growth equity.” Those metrics, he told me, are the size of the business and how diversified it is.

Shuttleworth likens this program of getting the company ready to IPO to getting fit. “There’s no point in saying: I haven’t done any exercise in the last 10 years but I’m going to sign up for tomorrow’s marathon,” he said.

The move from being a private company to taking outside investment and going public — especially after all these years of being self-funded — is treacherous, though, and Shuttleworth admitted as much, especially in terms of being forced to setting short-term goals to satisfy investors that aren’t necessarily in the best interest of the company in the long term. Shuttleworth thinks he can negotiate those issues, though.

Interestingly, he thinks the real danger is quite a different one. “I think the most dangerous thing in making that shift is the kind of shallowness of the unreasonably big impact that stock price has on people’s mood,” he said. “Today, at Canonical, it’s 600 people. You might have some that are having a really great day and some that are having a shitty day. And they have to figure out what’s real about both of those scenarios. But they can kind of support each other. […] But when you have a stock ticker, everybody thinks they’re having a great day, or everybody thinks they’re having a shitty day in a way that may be completely uncorrelated to how well they’re actually doing.”

Shuttleworth does not believe that IBM’s acquisition of its competitor Red Hat will have any immediate effect on its business, though. What he does think, however, is that this move is making a lot of people rethink for the first time in years the investment they’ve been making in Red Hat and its enterprise Linux distribution. Canonical’s promise is that Ubuntu, as well as its OpenStack tools and services, are not just competitive but also more cost-effective in the long run, and offer enterprises an added degree of agility. And if more businesses start looking at Canonical and Ubuntu, that can only speed up Shuttleworth’s (and his bankers’) schedule for hitting Canonical’s metrics for raising money and going public.

Powered by WPeMatico

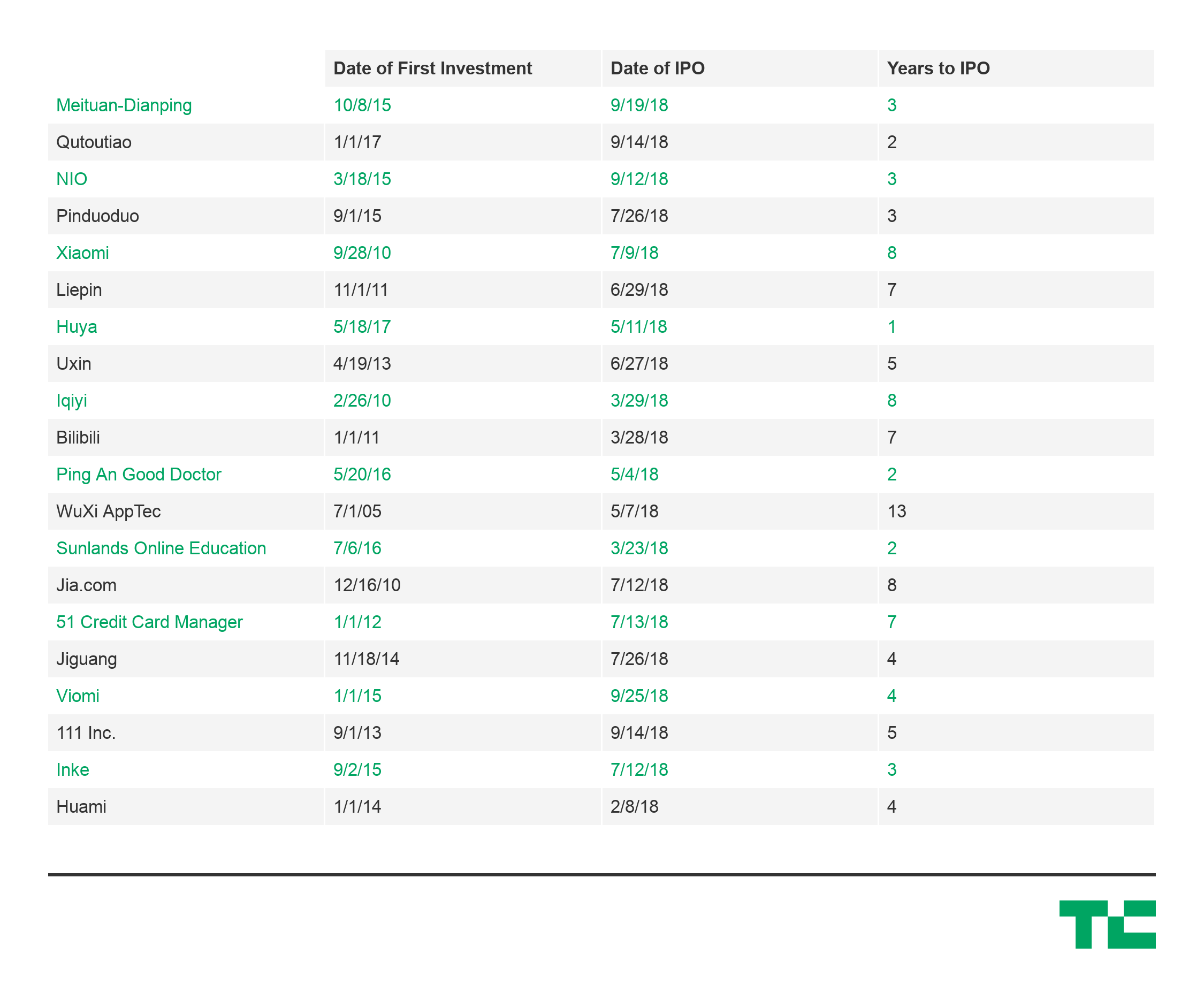

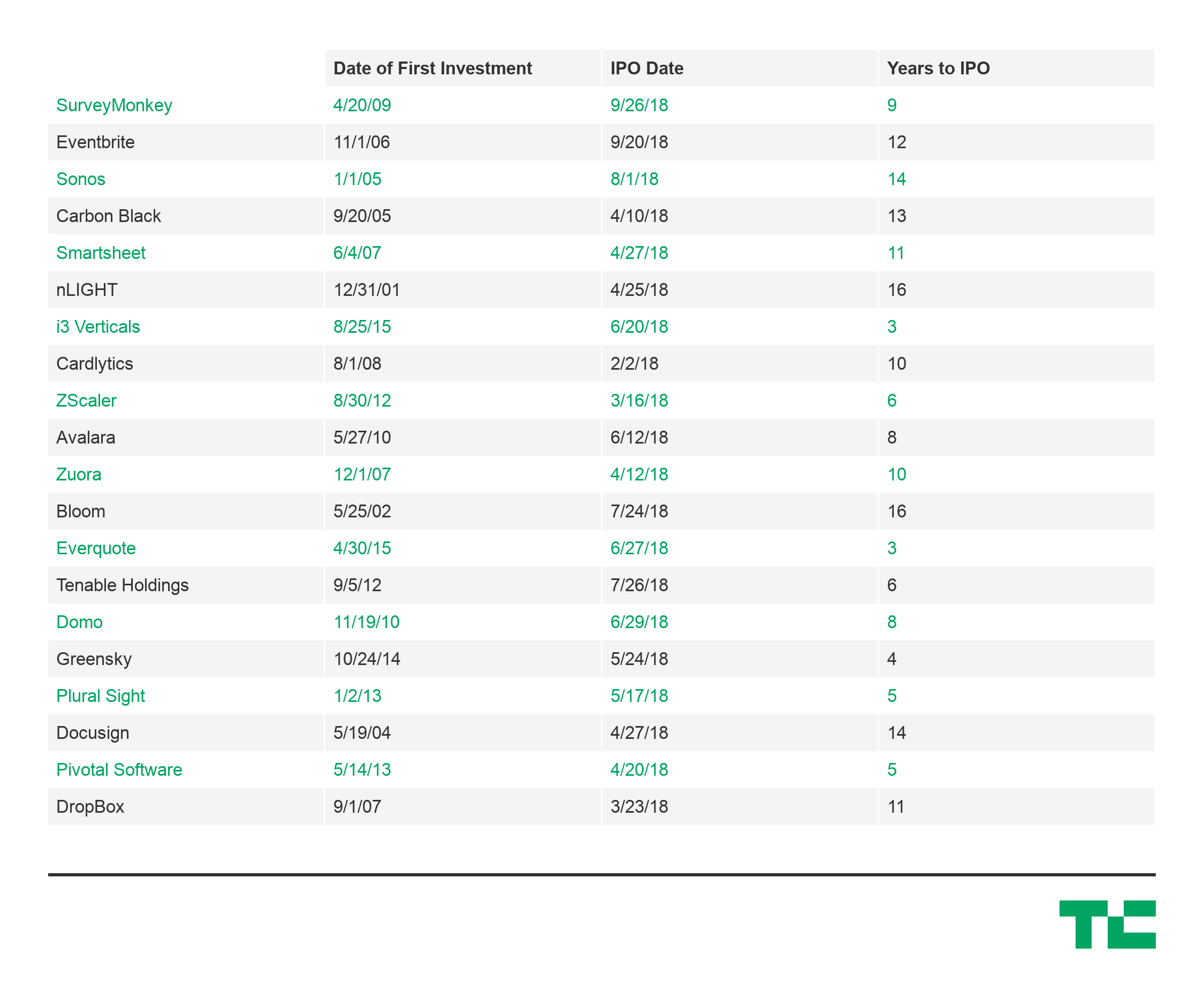

This year’s rush of IPOs from Chinese tech companies has dominated headlines, but what’s more interesting is how quickly they got there.

Traditionally, “going public” represented the gratifying culmination of sleepless nights and missed birthdays that went into building a company. The peak of a lengthy climb, where founders and VCs would finally see the fruits of their labor.

However, Chinese companies appear to be reaching that peak much quicker than their American peers, heading to the public markets only a few years after initial venture investments, and often with little operating history.

Analyzing twenty of the most high profile Chinese tech IPOs this year, the average time from first venture investment to IPO was only around three to five years. Take e-commerce platform Pinduoduo, which pulled in $1.6 billion less than three years after its Series A. Or the recent IPO of EV-manufacturer NIO, which raised a billion dollars just three-and-a-half years after its Series A and having just delivered its first car in June.

China IPO data for 2018 compiled from NASDAQ, Pitchbook, and Crunchbase

That’s less than half the average 10-year timeline for venture-backed US tech companies that went public in 2018, including Dropbox, Eventbrite, and DocuSign, which all IPO’d more than a decade after their initial investments.

Differences in market maturity, government involvement, and support from large tech incumbents all undoubtedly play a factor, but the speed to liquidity for the Chinese companies is still astounding.

Speed to liquidity is a critical metric for the health of a startup ecosystem. It creates a positive cycle where faster liquidity can drive faster fundraising, faster reinvestment, faster startup building, and faster public liquidity again. An accelerated cycle could be especially appealing for funds with LPs that require faster returns due to cash commitments or otherwise.

It’s important to note that venture returns are a function of capital and time, so quicker exits will also drive higher returns for the same amount invested. For example, a $1 million investment with a $5 million exit after ten years would generate an Internal Rate of Return (a commonly used metric to evaluate VC performance) of 20%. If the same exit occurred after five years, the IRR would be 50%.

Liquidity is a key consideration as China’s influence on the flow of global venture capital intensifies. As China’s tech ecosystem sees more of its darlings mature and more consistently deliver smashing exits, investments in China will have to be a more serious consideration for VCs, even if only to minimize the sheer amount of time, resources, and painstaking energy needed to build a company in the U.S.

Powered by WPeMatico