Internal Revenue Service

Auto Added by WPeMatico

Auto Added by WPeMatico

Embedded fintech company Zeal secured $13 million in Series A funding to continue developing its platform for building individualized payroll products.

Spark Capital led the Series A, with participation from Commerce Ventures and a group of individual investors, including Marqeta CEO Jason Gardner and CRO Omri Dahan, Robinhood founder Vlad Tenev, UltimateSoftware executives Mitch Dauerman and Bob Manne and Namely founder Matt Straz. The latest round now gives the company $14.6 million in total funding, which includes a $1.6 million seed round in 2020, CEO Kirti Shenoy told TechCrunch.

The Bay Area company’s origin was as Puzzl, a payment processing startup for the gig economy, founded in 2018 by Shenoy and CTO Pranab Krishnan. It was part of Y Combinator’s 2019 cohort. The pair had to pivot the company after needing to move some of its thousands of 1099 contractors to W2 employee status.

They went looking for payroll processors that could handle high volumes of payroll automatically, like ADP or Paycor, but found they didn’t match some of the capabilities Shenoy and Krishnan wanted, including to pay workers daily and customize earning components.

To ensure other companies didn’t run into the same problem, they decided to build a payroll API that enables their customers to build their own payroll products, even being able to pay their workers everyday. Traditionally, companies would layer together antiquated third-party payroll tools and spend millions of dollars on consulting fees. Zeal’s API tool modernizes the payroll process and takes on the payroll liability while managing the back-end payment logistics, Shenoy said.

Currently, enterprises use Zeal to pay large volumes of workers and keep payment data on their own native systems, while software platforms that sell business-to-business services use Zeal to build their own payroll product to sell to their customers.

“Our mission is to touch every American paycheck with our tax and payment technology, ensuring that American employees are paid correctly and efficiently,” Krishnan said.

And that is a complex goal: there are 200 million American employees, over $8.8 trillion of payroll is processed annually in the U.S. and the country’s 11,000 tax jurisdictions produce over 25,000 income tax code changes a year.

Meanwhile, Shenoy cited IRS data that showed more than 40% of small and medium businesses pay at least one payroll penalty per year. That was one of the drivers for Zeal’s latest product, the Abacus gross-to-net calculator, which payroll companies can use to ensure they are compliant in paying their income taxes.

The co-founders intend to use the new funding to build out their team and strengthen compliance measures to ensure its track record with enterprises.

“We are starting to win more enterprise deals and moving millions of dollars each day,” Shenoy said. “This has been a legacy space for so long, so companies want to work with a provider to move fast.”

Shenoy predicts that more companies will shift to hyper-customized experiences in the next five to 10 years. Whereas the default was a company like ADP, companies will want to control their own data and build products so their customers can do everything payroll-related from one platform.

As part of the investment, Spark Capital’s partner Natalie Sandman has joined Zeal’s board of directors. The firm previously invested in other embedded fintech companies like Affirm and Marqeta, and she thinks there are new experiences in the sector that APIs can unlock.

Sandman felt the payroll-building pain points herself when she worked at Zenefits. At the time, the company was trying to do the same thing, but there were no APIs to connect with. There were all of these spreadsheets to transfer data, but one wrong deduction would trickle down and cause a tax penalty.

Shenoy and Krishnan are both “customer-obsessed,” she said, and are balancing speed with thoughtfulness when it comes to understanding how their customers want to build payroll products.

She is seeing a macro shift to audience-driven human resources where bringing new employees online will mean embedding them into products that will be more valuable versus the traditional spreadsheet.

“To me, it is a no-brainer that APIs provide flexibility in the way wages and deductions need to be made,” Sandman said. “You can lose trust in your employer. Payroll is at the deepest trust point and where you want transparency and a robust solution to solve that need.”

Powered by WPeMatico

There’s a reason startup compensation packages usually include equity, or stock options. For one, it’s a way for startups to remain competitive in the job market and attract top talent. But it’s also a way to reward those employees who join early and give them a tangible reason to stay incentivized to grow the company.

The problem is that while many employees do understand that their equity compensation could mean a big payday in the future — and, in 2021, that’s more likely than ever — they don’t often understand the inevitable complexities of their stock options. That puts employees at risk of not getting the most value after an IPO or, worse, losing them.

If you’ve ever been confused about your equity, or haven’t thought much about it, you’re not alone. That’s why I’m going to share three things all employees joining a startup should do with their equity:

While many startups are getting better at proactively communicating the value of your equity package upfront, some are still figuring out the best way to do it. That’s because, unlike the more straightforward number of a salary, stock options are more nuanced — they’re a living, breathing type of compensation.

The most important pieces of information to pay attention to are your 409A valuation, your strike price, the type of options you were granted and the preferred share price.

The 409A valuation is based on your company’s valuation. This is also referred to as the fair market value (FMV). The 409A valuation can, and does, often change — they have to be updated at least once a year by a third-party valuator in order to meet tax rules. The 409A also changes during a fundraising event. Investors involved in the funding round determine how they value the company and are given options, at that valuation, in exchange for cash.

The most important pieces of information to pay attention to are your 409A valuation, your strike price, the type of options you were granted and the preferred share price.

Since the company has now been valued higher, the 409A changes for everyone. It’s also possible for the 409A to go down if, for any reason, the company is now valued at a lower amount. This is known as a “down round.” Airbnb had a notable down round during the pandemic, though it eventually recovered and went public.

Your strike price is the price at which you can buy your stock options (also known as exercising). Yes, buy. You are given the option to buy them, which is why they are called stock options. But know that your strike price will likely never change. However, if you’re ever given more stock options (perhaps as a future bonus), this would be a separate grant and the strike price could be different. Companies are legally required to issue stock options at the most recent 409A price (or higher).

Powered by WPeMatico

As a small business owner, I was excited to learn about the $2.2 trillion Coronavirus Aid, Relief, and Economic Security Act that offers low-interest loans to firms impacted by the COVID-19 pandemic. However, as I read through the details and began to apply, it became clear that this legislation — while well-intentioned — may not be enough to help many SMBs and startups.

Here’s a quick recap of my experience.

First and foremost: You need to act swiftly. Emergency Economic Injury Grant and Economic Injury Disaster Loan programs included in the CARES Act function on a first-come, first-served basis, and are funded from a limited pool of resources.

I began my company’s application process by submitting our EIDL and EEIG applications through the SBA website. This was easy, if tedious. It took about two hours to complete the necessary online forms and about two seconds to click the EEIG checkbox. Submission was seamless, but I haven’t received any further communication from the SBA since completing my application, which is a bit confusing — EEIG funds are supposed to be dispersed within 3-5 days of the submission date.

However, I know there’s been a huge volume of submissions recently and this must be exceptionally difficult to handle. I look forward to any email correspondence or updates from the SBA that might give me — and other applicants — an updated estimate of the expected dispersal timeline.

Powered by WPeMatico

Every year around this time, Uber drivers, Wag dog walkers, Bird scooter chargers, social media influencers and other gig economy workers face the unsightly challenge of paying their taxes.

Companies like Uber and Lyft classify their drivers as independent contractors, which means you aren’t given any benefits and the company doesn’t withhold any of your taxes. This puts gig workers in a tough position come tax day, especially if they aren’t prepared to shell out big sums to the IRS.

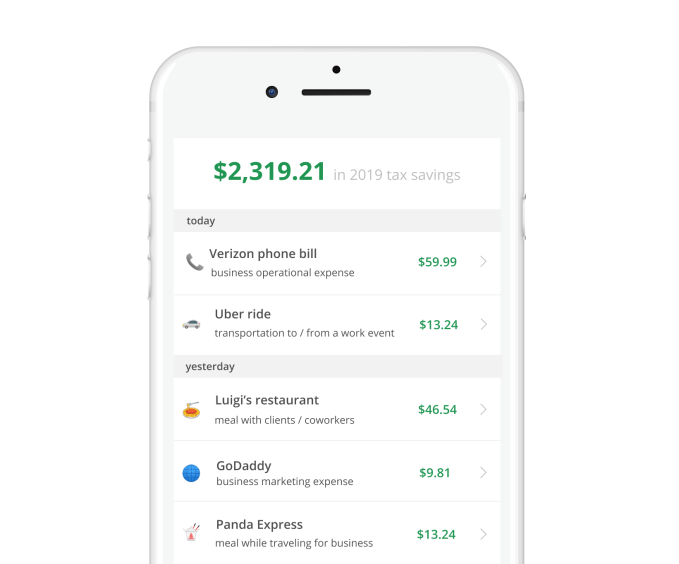

Keeper, a startup that’s just graduated from the Y Combinator startup accelerator, is here to make taxes a lot easier for that demographic and to save them as much money as possible.

Founded by childhood buddies and former debate partners Paul Koullick and David Kang, the San Francisco-based company has raised $1.65 million on a $10 million valuation in a round led by Jake Jolis of Matrix Partners.

Keeper co-founders Paul Koullick (left) and David Kang

The pair entered YC this winter with a big idea and little to show for it. Come March, they had developed a full-fledged product and accumulated 200 paying customers. With their first round of funding, they plan to add to their small but growing team and acquire 10,000 customers in the next 18 months.

“There are some companies that are trying to go very broad and trying to cover the whole spectrum of benefits; we’re just trying to go really deep on taxes,” Kang told TechCrunch. “This is a pain point. This is where people are definitely leaving the most money on the table.”

Keeper guesses the average gig worker in the U.S. is overpaying their taxes by more than 20 percent, or about $1,550 for those making more than $25,000 per year. Why? Because these independent contractors aren’t claiming the tax write-offs available to them, like phone bills, car maintenance fees and even a Spotify subscription for drivers.

“If you’re a dog walker, there are so many things you need to be writing off, like your poop bags, your extra leashes, your parking,” Koullick told TechCrunch. “This population needs the guidance of an accountant, but they can’t afford one and we’re trying to create this third option.”

Like a personal accountant, Keeper monitors gig workers’ expenses all year in search of possible tax deductions, saving each user $173 per month on average, it estimates. The startup uses Plaid to follow its customers’ transaction history, and once per day sends a text message asking if there are any tax write-offs to note. Over time, it gets smarter and smarter, keeping the SMS questions to a minimum.

Keeper doesn’t fully file taxes for 1099 workers yet, but will begin offering a quarterly tax filing service in June. Next year, it plans to offer a full-year tax-filing service.

Koullick, Keeper’s chief executive officer, worked in product at Square before joining another startup, called Stride, where he built and scaled Stride Tax, a mileage and expense-tracking app. Kang, for his part, has spent most of his post-graduate career at a trading firm in Chicago, focused on quantitative modeling. The two toyed with a few startup ideas before landing on Keeper’s tax business.

“We wanted to build something that actually mattered to real people,” Koullick explained. “And we wanted to do it in the financial space where we were happy to wade through ugly details and systems on their behalf.”

Keeper isn’t the only recent YC alum focused on the growing gig economy. Another, Catch, sells health insurance, retirement savings plans and tax-withholding services directly to freelancers, contractors or anyone uncovered. Given the rapid rise of Uber and other gig platforms, it’s no wonder YC startups are tapping into the various business opportunities available there.

“We’re willing to tackle some of these topics that are kind of boring and mundane and really intensive,” Kang added. “Like the average person doesn’t want to think about taxes or filling out forms. We saw that as an opportunity for us to step in and be like, hey, we’ll take it.”

Powered by WPeMatico