infrastructure

Auto Added by WPeMatico

Auto Added by WPeMatico

Picture yourself in the role of CIO at Roblox in 2017.

At that point, the gaming platform and publishing system that launched in 2005 was growing fast, but its underlying technology was aging, consisting of a single data center in Chicago and a bunch of third-party partners, including AWS, all running bare metal (nonvirtualized) servers. At a time when users have precious little patience for outages, your uptime was just two nines, or less than 99% (five nines is considered optimal).

Unbelievably, Roblox was popular in spite of this, but the company’s leadership knew it couldn’t continue with performance like that, especially as it was rapidly gaining in popularity. The company needed to call in the technology cavalry, which is essentially what it did when it hired Dan Williams in 2017.

Williams has a history of solving these kinds of intractable infrastructure issues, with a background that includes a gig at Facebook between 2007 and 2011, where he worked on the technology to help the young social network scale to millions of users. Later, he worked at Dropbox, where he helped build a new internal network, leading the company’s move away from AWS, a major undertaking involving moving more than 500 petabytes of data.

When Roblox approached him in mid-2017, he jumped at the chance to take on another major infrastructure challenge. While they are still in the midst of the transition to a new modern tech stack today, we sat down with Williams to learn how he put the company on the road to a cloud-native, microservices-focused system with its own network of worldwide edge data centers.

Powered by WPeMatico

IBM, a company that originally made its name out of its leadership in building myriad enterprise hardware (quite literally: its name is an abbreviation for International Business Machines), is taking one more step away from that legacy and deeper into the world of cloud services. The company today announced that it plans to spin off its managed infrastructure services unit as a separate public company, a $19 billion business in annual revenues, to help it focus more squarely on newer opportunities in hybrid cloud applications and artificial intelligence.

Infrastructure services include a range of managed services based around legacy infrastructure and digital transformation related to it. It includes things like testing and assembly, but also product engineering and lab services, among other things. A spokesperson confirmed to me that the deal will not include the company’s servers business, only infrastructure services.

IBM said it expects to complete the process — a tax-free spin-off for shareholders — by the end of 2021. It has not yet given a name to “NewCo” but it said that out of the gate the spun-off company will have 90,000 employees, 4,600 big enterprise clients in 115 countries, a backlog of $60 billion in business “and more than twice the scale of its nearest competitor” in the area of infrastructure services.

Others that compete against it include the likes of BMC and Microsoft. The remaining IBM business is about three times as big: it currently generates some $59 billion in annual revenues.

At the same time that IBM announced the news, it also gave some updated guidance for Q3, which it plans to report officially later this month. It said it expects revenues of $17.6 billion, with GAAP diluted earnings per share from continuing operations of $1.89, and operating (non-GAAP) earnings per share of $2.58. As a point of comparison, in Q3 2019 it reported revenues of $18 billion. And last quarter IBM reported revenues of $18.1 billion. Tellingly, the division that contains infrastructure services saw declines last quarter.

The market seems to like the news: IBM shares are trading up some 10% ahead of the market opening.

The move is a significant shift for the company and underscores a bigger sea change in how enterprise IT has evolved and looks to continue changing in the future.

IBM is betting that legacy infrastructure and the servicing of it, while continuing to net revenues, will not grow as it has in the past, and as companies continue with their modernization (or “digital transformation,” as consultants like to refer to it today), they will turn increasingly to outsourced infrastructure and using cloud services, both to run their businesses and to build the services that interface with consumers. IBM, meanwhile, is in a race competing against the likes of Microsoft and Google in cloud services, and so doubling down on that part of the business is another way to focus on it for growth.

But IBM, often referred to as “Big Blue”, is also using the announcement as the start of an effort to streamline its business to spur growth (maybe we’ll have to rename it “Medium Blue”).

“IBM is laser-focused on the $1 trillion hybrid cloud opportunity,” said Arvind Krishna, IBM CEO, in a statement. “Client buying needs for application and infrastructure services are diverging, while adoption of our hybrid cloud platform is accelerating. Now is the right time to create two market-leading companies focused on what they do best. IBM will focus on its open hybrid cloud platform and AI capabilities. NewCo will have greater agility to design, run and modernize the infrastructure of the world’s most important organizations. Both companies will be on an improved growth trajectory with greater ability to partner and capture new opportunities – creating value for clients and shareholders.”

Its $34 billion purchase of Red Hat in 2019 is perhaps its most notable investment in recent times in IBM’s own transformation.

“We have positioned IBM for the new era of hybrid cloud,” said Ginni Rometty, IBM Executive Chairman in a statement. “Our multi-year transformation created the foundation for the open hybrid cloud platform, which we then accelerated with the acquisition of Red Hat. At the same time, our managed infrastructure services business has established itself as the industry leader, with unrivaled expertise in complex and mission-critical infrastructure work. As two independent companies, IBM and NewCo will capitalize on their respective strengths. IBM will accelerate clients’ digital transformation journeys, and NewCo will accelerate clients’ infrastructure modernization efforts. This focus will result in greater value, increased innovation, and faster execution for our clients.”

More to come.

Powered by WPeMatico

There’s something to be said for consistency through good times and bad, and one company that has had a staggeringly consistent track record is international data center vendor, Equinix. It just recorded its 69th straight positive quarter, according to the company.

That’s an astonishing record, and covers over 17 years of positive returns. That means this streak goes back to 2003. Not too shabby.

The company had a decent quarter, too. Even in the middle of an economic mess, it was still up 6% YoY to $1.445 billion and up 2% over last quarter. The company runs data centers where companies can rent space for their servers. Equinix handles all of the infrastructure providing racks, wiring and cooling — and customers can purchase as many racks as they need.

If you’re managing your own servers for even part of your workload, it can be much more cost-effective to rent space from a vendor like Equinix than trying to run a facility on your own.

Among its new customers this quarter are Zoom, which is buying capacity all over the place, having also announced a partnership with Oracle earlier this month, and TikTok. Both of those companies deal in video and require lots of different types of resources to keep things running.

This report comes against a backdrop of a huge increase in resource demand for certain sectors like streaming video and video conferencing, with millions of people working and studying at home or looking for distractions.

And if you’re wondering if they can keep it going, they believe they can. Their guidance calls for 2020 revenue of $5.877-$5.985 billion, a 6-8% increase over the previous year.

You could call them the anti-IBM. At one point Big Blue recorded 22 straight quarters of declining revenue in an ignominious streak that stretched from 2012 to 2018 before it found a way to stop the bleeding.

When you consider that Equnix’s streak includes the period of 2008-2010, the last time the economy hit the skids, it makes the record even more impressive, and certainly one worth pointing out.

Powered by WPeMatico

In order to have innovative smart city applications, cities first need to build out the connected infrastructure, which can be a costly, lengthy, and politicized process. Third-parties are helping build infrastructure at no cost to cities by paying for projects entirely through advertising placements on the new equipment. I try to dig into the economics of ad-funded smart city projects to better understand what types of infrastructure can be built under an ad-funded model, the benefits the strategy provides to cities, and the non-obvious costs cities have to consider.

Consider this an ongoing discussion about Urban Tech, its intersection with regulation, issues of public service, and other complexities that people have full PHDs on. I’m just a bitter, born-and-bred New Yorker trying to figure out why I’ve been stuck in between subway stops for the last 15 minutes, so please reach out with your take on any of these thoughts: @Arman.Tabatabai@techcrunch.com.

When we talk about “Smart Cities”, we tend to focus on these long-term utopian visions of perfectly clean, efficient, IoT-connected cities that adjust to our environment, our movements, and our every desire. Anyone who spent hours waiting for transit the last time the weather turned south can tell you that we’ve got a long way to go.

But before cities can have the snazzy applications that do things like adjust infrastructure based on real-time conditions, cities first need to build out the platform and technology-base that applications can be built on, as McKinsey’s Global Institute explained in an in-depth report released earlier this summer. This means building out the network of sensors, connected devices and infrastructure needed to track city data.

However, reaching the technological base needed for data gathering and smart communication means building out hard physical infrastructure, which can cost cities a ton and can take forever when dealing with politics and government processes.

Many cities are also dealing with well-documented infrastructure crises. And with limited budgets, local governments need to spend public funds on important things like roads, schools, healthcare and nonsensical sports stadiums which are pretty much never profitable for cities (I’m a huge fan of baseball but I’m not a fan of how we fund stadiums here in the states).

As city infrastructure has become increasingly tech-enabled and digitized, an interesting financing solution has opened up in which smart city infrastructure projects are built by third-parties at no cost to the city and are instead paid for entirely through digital advertising placed on the new infrastructure.

I know – the idea of a city built on ad-revenue brings back soul-sucking Orwellian images of corporate overlords and logo-paved streets straight out of Blade Runner or Wall-E. Luckily for us, based on our discussions with developers of ad-funded smart city projects, it seems clear that the economics of an ad-funded model only really work for certain types of hard infrastructure with specific attributes – meaning we may be spared from fire hydrants brought to us by Mountain Dew.

While many factors influence the viability of a project, smart infrastructure projects seem to need two attributes in particular for an ad-funded model to make sense. First, the infrastructure has to be something that citizens will engage – and engage a lot – with. You can’t throw a screen onto any object and expect that people will interact with it for more than 3 seconds or that brands will be willing to pay to throw their taglines on it. The infrastructure has to support effective advertising.

Second, the investment has to be cost-effective, meaning the infrastructure can only cost so much. A third-party that’s willing to build the infrastructure has to believe they have a realistic chance of generating enough ad-revenue to cover the costs of the projects, and likely an amount above that which could lead to a reasonable return. For example, it seems unlikely you’d find someone willing to build a new bridge, front all the costs, and try to fund it through ad-revenue.

A LinkNYC kiosk enabling access to the internet in New York on Saturday, February 20, 2016. Over 7500 kiosks are to be installed replacing stand alone pay phone kiosks providing free wi-fi, internet access via a touch screen, phone charging and free phone calls. The system is to be supported by advertising running on the sides of the kiosks. ( Richard B. Levine) (Photo by Richard Levine/Corbis via Getty Images)

To get a better understanding of the types of smart city hardware that might actually make sense for an ad-funded model, we can look at the engagement levels and cost structures of smart kiosks, and in particular, the LinkNYC project. Smart kiosks – which provide free WiFi, connectivity and real-time services to citizens – have been leading examples of ad-funded smart city projects. Innovative companies like Intersection (developers of the LinkNYC project), SmartLink, IKE, Soofa, and others have been helping cities build out kiosk networks at little-to-no cost to local governments.

LinkNYC provides public access to much of its data on the New York City Open-Data website. Using some back-of-the-envelope math and a hefty number of assumptions, we can try to get to a very rough range of where cost and engagement metrics generally have to fall for an ad-funded model to make sense.

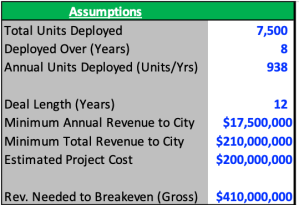

To try and retrace considerations for the developers’ investment decision, let’s first look at the terms of the deal signed with New York back in 2014. The agreement called for a 12-year franchise period, during which at least 7,500 Link kiosks would be deployed across the city in the first eight years at an expected project cost of more than $200 million. As part of its solicitation, the city also required the developers to pay the greater of either a minimum annual payment of at least $17.5 million or 50 percent of gross revenues.

Let’s start with the cost side – based on an estimated project cost of around $200 million for at least 7,500 Links, we can get to an estimated cost per unit of $25,000 – $30,000. It’s important to note that this only accounts for the install costs, as we don’t have data around the other cost buckets that the developers would also be on the hook for, such as maintenance, utility and financing costs.

Source: LinkNYC, NYC.gov, NYCOpenData

Turning to engagement and ad-revenue – let’s assume that the developers signed the deal with the expectations that they could at least breakeven – covering the install costs of the project and minimum payments to the city. And for simplicity, let’s assume that the 7,500 links were going to be deployed at a steady pace of 937-938 units per year (though in actuality the install cadence has been different). In order for the project to breakeven over the 12-year deal period, developers would have to believe each kiosk could generate around $6,400 in annual ad-revenue (undiscounted).

Source: LinkNYC, NYC.gov, NYCOpenData

The reason the kiosks can generate this revenue (and in reality a lot more) is because they have significant engagement from users. There are currently around 1,750 Links currently deployed across New York. As of November 18th, LinkNYC had over 720,000 weekly subscribers or around 410 weekly subscribers per Link. The kiosks also saw an average of 18 million sessions per week, or 20-25 weekly sessions per subscriber, or around 10,200 weekly sessions per kiosk (seasonality might even make this estimate too low).

And when citizens do use the kiosks, they use it for a long time! The average session for each Link unit was four minutes and six seconds. The level of engagement makes sense since city-dwellers use these kiosks in time or attention-intensive ways, such making phone calls, getting directions, finding information about the city, or charging their phones.

The analysis here isn’t perfect, but now we at least have a (very) rough idea of how much smart kiosks cost, how much engagement they see, and the amount of ad-revenue developers would have to believe they could realize at each unit in order to ultimately move forward with deployment. We can use these metrics to help identify what types of infrastructure have similar profiles and where an ad-funded project may make sense.

Bus stations, for example, may cost about $10,000 – $15,000, which is in a similar cost range as smart kiosks. According to the MTA, the NYC bus system sees over 11.2 million riders per week or nearly 700 riders per station per week. Rider wait times can often be five-to-ten minutes in length if not longer. Not to mention bus stations already have experience utilizing advertising to a certain degree. Projects like bike-share docking stations and EV charging stations also seem to fit similar cost profiles while having high engagement.

And interactions with these types of infrastructure are ones where users may be more receptive to ads, such as an EV charging station where someone is both physically engaging with the equipment and idly looking to kill up sometimes up to 30 minutes of time as they charge up. As a result, more companies are using advertising models to fund projects that fit this mold, like Volta, who uses advertising to offer charging stations free to citizens.

When it makes sense for cities and third-party developers, advertising-funded smart city infrastructure projects can unlock a tremendous amount of value for a city. The benefits are clear – cities pay nothing, citizens are offered free connectivity and real-time information on local conditions, and smart infrastructure is built and can possibly be used for other smart city applications down the road, such as using locational data tracking to improve city zoning and congestion.

Yes, ads are usually annoying – but maybe understanding that advertising models only work for specific types of smart city projects may help quell fears that future cities will be covered inch-to-inch in mascots. And ads on projects like LinkNYC promote local businesses and can tap into idiosyncratic conditions and preferences of regional communities – LinkNYC previously used real-time local transit data to display beer ads to subway riders that were facing heavy delays and were probably in need of a drink.

Like everyone’s family photos from Thanksgiving, the picture here is not all roses, however, and there are a lot of deep-rooted issues that exist under the surface. Third-party developed, advertising-funded infrastructure comes with externalities and less obvious costs that have been fairly criticized and debated at length.

When infrastructure funding is derived from advertising, concerns arise over whether services will be provided equitably across communities. Many fear that low-income or less-trafficked communities that generate less advertising demand could end up having poor infrastructure and maintenance.

Even bigger points of contention as of late have been issues around data consent and treatment. I won’t go into much detail on the issue since it’s incredibly complex and warrants its own lengthy dissertation (and many have already been written).

But some of the major uncertainties and questions cities are trying to answer include: If third-parties pay for, manage and operate smart city projects, who should own data on citizens’ living behavior? How will citizens give consent to provide data when tracking systems are built into the environment around them? How can the data be used? How granular can the data get? How can we assure citizens’ information is secure, especially given the spotty track records some of the major backers of smart city projects have when it comes to keeping our data safe?

The issue of data treatment is one that no one has really figured out yet and many developers are doing their best to work with cities and users to find a reasonable solution. For example, LinkNYC is currently limited by the city in the types of data they can collect. Outside of email addresses, LinkNYC doesn’t ask for or collect personal information and doesn’t sell or share personal data without a court order. The project owners also make much of its collected data publicly accessible online and through annually published transparency reports. As Intersection has deployed similar smart kiosks across new cities, the company has been willing to work through slower launches and pilot programs to create more comfortable policies for local governments.

But consequential decisions related to third-party owned smart infrastructure are only going to become more frequent as cities become increasingly digitized and connected. By having third-parties pay for projects through advertising revenue or otherwise, city budgets can be focused on other vital public services while still building the efficient, adaptive and innovative infrastructure that can help solve some of the largest problems facing civil society. But if that means giving up full control of city infrastructure and information, cities and citizens have to consider whether the benefits are worth the tradeoffs that could come with them. There is a clear price to pay here, even when someone else is footing the bill.

Powered by WPeMatico

The FCC is pushing for speedy deployment of 5G networks nationwide with an order adopted today that streamlines what it perceives as a patchwork of obstacles, needless costs and contradictory regulations at the state level. But local governments say the federal agency is taking things too far.

5G networks will consist of thousands of wireless installations, smaller and more numerous than cell towers. This means that wireless companies can’t use existing facilities, for all of it at least, and will have to apply for access to lots of new buildings, utility poles and so on. It’s a lot of red tape, which of course impedes deployment.

To address this, the agency this morning voted 3 to 1 along party lines to adopt the order (PDF) entitled “Accelerating Wireline Broadband Deployment by Removing Barriers to Infrastructure Investment.” What it essentially does is exert FCC authority over state wireless regulators and subject them to a set of new rules superseding their own.

First the order aims to literally speed up deployment by standardizing new, shorter “shot clocks” for local governments to respond to applications. They’ll have 90 days for new locations and 60 days for existing ones — consistent with many existing municipal time frames but now to be enforced as a wider standard. This could be good, as the longer time limits were designed for consideration of larger, more expensive equipment.

On the other hand, some cities argue, it’s just not enough time — especially considering the increased volume they’ll be expected to process.

Cathy Murillo, mayor of Santa Barbara, writes in a submitted comment:

The proposed ‘shot clocks’ would unfairly and unreasonably reduce the time needed for proper application review in regard to safety, aesthetics, and other considerations. By cutting short the necessary review period, the proposals effectively shift oversight authority from the community and our elected officials to for-profit corporations for wireless equipment installations that can have significant health, safety, and aesthetic impacts when those companies have little, if any, interest to respect these concerns.

Next, and even less popular, is the FCC’s take on fees for applications and right-of-way paperwork. These fees currently vary widely, because as you might guess it is far more complicated and expensive — often by an order of magnitude or more — to approve and process an application for (not to mention install and maintain) an antenna on 5th Avenue in Manhattan than it is in outer Queens. These are, to a certain extent anyway, natural cost differences.

The order limits these fees to “a reasonable approximation of their costs for processing,” which the FCC estimated at about $500 for one application for up to five installations or facilities, $100 for additional facilities, and $270 per facility per year, all-inclusive.

For some places, to be sure, that may be perfectly reasonable. But as Catherine Pugh, mayor of Baltimore, put it in a letter (PDF) to the FCC protesting the proposed rules, it sure isn’t for her city:

An annual fee of $270 per attachment, as established in the above document, is unconscionable when the facility may yield profits, in some cases, many times that much in a given month. The public has invested and installed these assets [i.e. utility poles and other public infrastructure], not the industry. The industry does not own these assets; the public does. Under these circumstances, it is entirely reasonable that the public should be able to charge what it believes to be a fair price.

There’s no doubt that excessive fees can curtail deployment and it would be praiseworthy of the FCC to tackle that. But the governments they are hemming in don’t seem to appreciate being told what is reasonable and what isn’t.

“It comes down to this: three unelected officials on this dais are telling state and local leaders all across the country what they can and cannot do in their own backyards,” said FCC Commissioner Jessica Rosenworcel in a statement presented at the vote. “This is extraordinary federal overreach.”

New York City’s commissioner of information technology told Bloomberg that his office is “shocked” by the order, calling it “an unnecessary and unauthorized gift to the telecommunications industry and its lobbyists.”

The new rules may undermine deployment deals that already exist or are under development. After all, if you were a wireless company, would you still commit to paying $2,000 per facility when the feds just gave you a coupon for 80 percent off? And if you were a city looking at a budget shortfall of millions because of this, wouldn’t you look for a way around it?

Chairman Ajit Pai argued in a statement that “When you raise the cost of deploying wireless infrastructure, it is those who live in areas where the investment case is the most marginal—rural areas or lower-income urban areas—who are most at risk of losing out.”

But the basic market economics of this don’t seem to work out. Big cities cost more and are more profitable; rural areas cost less and are less profitable. Under the new rules, big cities and rural areas will cost the same, but the former will be even more profitable. Where would you focus your investments?

The FCC also unwisely attempts to take on the aesthetic considerations of installations. Cities have their own requirements for wireless infrastructure, such as how it’s painted, where it can be located and what size it can be when in this or that location. But the FCC seems (as it does so often these days) to want to accommodate the needs of wireless providers rather than the public.

Wireless companies complain that the rules are overly restrictive or subjective, and differ too greatly from one place to another. Municipalities contend that the restrictions are justified and, at any rate, their prerogative to design and enforce.

“Given these differing perspectives and the significant impact of aesthetic requirements on the ability to deploy infrastructure and provide service, we provide guidance on whether and in what circumstances aesthetic requirements violate the [Communications] Act,” the FCC’s order reads. In other words, wireless industry gripes about having to paint their antennas or not hang giant microwave arrays in parks are being federally codified.

“We conclude that aesthetics requirements are not preempted if they are (1) reasonable, (2) no more burdensome than those applied to other types of infrastructure deployments, and (3) published in advance,” the order continues. Does that sound kind of vague to you? Whether a city’s aesthetic requirement is “reasonable” is hardly the jurisdiction of a communications regulator.

For instance, Hudson, Ohio city manager Jane Howington writes in a comment on the order that the city has 40-foot limits on pole heights, to which the industry has already agreed, but which would be increased to 50 under the revisions proposed in the rule. Why should a federal authority be involved in something so clearly under local jurisdiction and expertise?

This isn’t just an annoyance. As with the net neutrality ruling, legal threats from states can present serious delays and costs.

“Every major state and municipal organization has expressed concern about how Washington is seeking to assert national control over local infrastructure choices and stripping local elected officials and the citizens they represent of a voice in the process,” said Rosenworcel. “I do not believe the law permits Washington to run roughshod over state and local authority like this and I worry the litigation that follows will only slow our 5G future.”

She also points out that the predicted cost savings of $2 billion — by telecoms, not the public — may be theorized to spur further wireless deployment, but there is no requirement for companies to use it for that, and in fact no company has said it will.

In other words, there’s every reason to believe that this order will sow discord among state and federal regulators, letting wireless companies save money and sticking cities with the bill. There’s certainly a need to harmonize regulations and incentivize wireless investment (especially outside city centers), but this doesn’t appear to be the way to go about it.

Powered by WPeMatico

The UK government has set out a package of measures it’s hoping will futureproof domestic networks and boost international competitiveness by supporting a nationwide rollout of full fiber broadband and 5G mobile technology.

The Future Telecoms Infrastructure Review, published today, follows the announcement of a market review last year as part of the government’s Industrial Strategy as it seeks to chart a technology-enabled course for growth and competitiveness.

Yet, at the same time, the UK seriously lags several European competitors on the fiber broadband front — so the strategy is also intended to try to reboot current poor performance.

The government says its telecoms plan emphasizes greater consumer choice and initiatives to promote quicker rollout — and an eventual full switch over — from copper to fiber.

It wants full fibre broadband to reach 15 million premises (up from the ’10M over the next decade’ set out in the Conservative party manifesto) by 2025, and also 5G mobile network coverage to reach the majority of the population.

By 2033, it wants full fiber broadband coverage to reach across all of the UK.

Currently the UK only has 4% full fiber connections, which compares dismally to 71% in Spain and 89% in Portugal. While France has around 28% — which the government notes is “increasing quickly”.

Included in the government’s strategy is public investment in full fiber for rural areas; and new legislation to guarantee full fiber connections in new build developments; as well as a series of regulatory reforms intended to drive investment and competition — which it says will be tailored to different local market conditions.

It’s also planning for an industry-led switch over from copper to full fiber — to avoid businesses being saddled with the expense and burden of running copper and fiber networks in parallel.

There’s no fixed timing for this, as the government says it will depend on the pace of fiber rollouts and take-up, but it suggests it’s “realistic to assume that switchover could happen in the majority of the country by 2030”.

To boost competition to drive commercial fiber rollouts, the government is proposing regulatory reform to allow for “unrestricted access” to Openreach ducts and poles — i.e. the wholly BT-owned company’s own physical infrastructure where fiber can be laid — for both residential and business broadband use, including for essential mobile infrastructure.

It also wants to open up other avenues for laying broadband fiber, saying other existing infrastructure (including pipes and sewers) owned by other utilities such as power, gas and water, should be “easy to access, and available for both fixed and mobile use”.

And it says it will shortly publish consultations on the proposed legislative changes to streamline wayleaves and mandate fiber connections in new builds.

Another key recommendation in the review, given that the expense of digs to lay fiber remains one of the biggest barriers to broadband upgrades, is for a new nationwide framework aimed at reducing the costs, time and disruption caused by street-works by standardising the approach across the country.

With its planned regulatory tweaks, the government reckons that market competition will be able to deliver full fiber networks across the majority of the UK (~80%) — leaving around ~20% which it’s expecting will require “bespoke solutions to ensure rollout of networks”. And for around half of that fifth it also expects taxpayer funding will be needed to deliver a fiber/5G upgrade.

It estimates that nationwide availability of ‘full fiber’ is likely to require additional (public) funding of around £3BN to £5BN to support commercial investment in the final ~10% of areas that would otherwise be overlooked — stressing that these “often rural areas must not be forced to wait until the rest of the country has connectivity before they can access gigabit-capable networks”.

So it’s planning to pursue an “outside-in” strategy, allowing network competition to serves commercially viable areas while laying down government support investment in parallel on what it describes as “the most difficult to reach areas”.

“We have already identified around £200M within the existing Superfast broadband programme that can further the delivery of full fibre networks immediately,” it notes on that.

Although it’s not clear at this stage how the government intends to fund the full proposals for a taxpayer-funded broadband bill running to multiple billions.

On the mobile connectivity front, it’s proposing increased access to spectrum for “innovative 5G services”, and says it will allow mobile network operators to make far greater use of government buildings to boost coverage across the UK.

“We should consider whether more flexible, shared spectrum models can maintain network competition between MNOs while also increasing access to spectrum to support new investment models, spurring innovation in industrial internet of things, wireless automation and robotics, and improving rural coverage,” it writes on that.

Over the longer term it says is expecting to see a more converged telecoms sector — so it’s leaving itself some ‘last mile’ wiggle room on the ‘full fiber’ push, for example by pointing out that: “Fixed fibre networks and 5G are complementary technologies, and 5G will require dense fibre networks. In some places, 5G may provide a more cost-effective way of providing ultra-fast connectivity to homes and businesses.”

“We want everyone in the UK to benefit from world-class connectivity no matter where they live, work or travel,” said the new Secretary of State for digital, culture, media and sport, Jeremy Wright, commenting on the review in a statement, and dubbing it a “radical new blueprint for the future of telecommunications in this country”.

“[The strategy] will increase competition and investment in full fiber broadband, create more commercial opportunities and make it easier and cheaper to roll out infrastructure for 5G,” he added.

The UK’s incumbent telco, BT, which owns and operates the country’s largest broadband network, has long pursued the opposite strategy to the one the government is here pursuing: i.e. by seeking to eke out its own ex-monopoly copper infrastructure, such as by applying technologies that speed up fiber to the cabinet technology, instead of making the major financial commitment to invest in substantially expanding full fiber to the home coverage (and thereby futureproof national network infrastructure).

For years competitors (and, indeed, frustrated consumers) have also accused the company of foot-dragging on providing access to its network — thereby undermining other commercial players’ ability to fund and build out next-gen network coverage.

Last year BT agreed with telecoms watchdog Ofcom to legally separate its network division Openreach — around a decade after a functional separation has been imposed by the regulator. Albeit, it’s still not the full structural separation some have called for.

“It is too early to determine whether legal separation will be sufficient to deliver positive changes on investment in full fibre infrastructure,” writes the government in its review, adding that it will “closely monitor legal separation, including Ofcom’s reports on the effectiveness of the new arrangements”.

“The Government will consider all additional measures if BT Group fails to deliver its commitments and regulatory obligations, and if Openreach does not deliver on its purpose of investing in ways that respond to the needs of its downstream customers,” it adds.

Commenting on the government’s strategy, an Openreach spokesperson told us: “We’re encouraged by the Government’s plan to promote competition, tackle red tape and bust the barriers to investment. As the national provider, we’re ambitious and want to build full fibre broadband to 10 million premises and beyond — so it’s vital that this becomes an attractive investment without creating digital inequality or a lack of choice for consumers and businesses across the country. As the Government acknowledges, the economics of building digital infrastructure remain challenging for everyone, and we believe a review of the current business rates regime is necessary to stimulate the whole sector.

“We’re already building full fibre to around 10,000 homes and businesses every week, and by 2020 we’ll have reached 3 million,” the spokesperson added. “We have a huge, world class engineering team and wherever we build, we’ll deliver the best quality network with the highest levels of service and built-in competition and choice.”

One aspect of the strategy the government is not trumpeting quite so loudly in its PR around the announcement is an intent to promote what it describes as “stable and long-term regulation” as part of its strategy to drive increased competition and unlock business investments.

On this it writes that the overarching strategic priority to “promote efficient competition and investment in world-class digital networks” should be “prioritised over interventions to further reduce retail prices in the near term, recognising these longer-term benefits”.

In the review it suggests moving to longer, five year review periods, for instance — saying this “could provide greater regulatory stability and promote investment”. It also writes that it wants Ofcom to publish guidance that “clearly sets out the approach and information it will use in determining a ‘fair bet’ return”.

It’s therefore possible that UK consumers could end up paying twice over to help fund national fiber broadband infrastructure upgrades; i.e. not just via direct subsidies to fund rural rollouts but also, potentially, via higher broadband prices too. Albeit, the government says that in its view “the interests of consumers are safeguarded as fiber markets become more competitive”.

Though in less commercially attractive areas, where there could be a greater risk of price inflation, the government’s small print does include the recognition that regulatory interventions — such as price controls — may indeed be required. Though of course any such controls would only come in after consumers had been being stung…

“For areas where there is actual or prospective effective competition between networks, Government would not anticipate the need for regulation,” it writes. “For other areas, we would expect the regulatory model for to evolve over time as networks are established. If market power emerges, regulated access (including price controls) may be needed to address competition concerns. These detailed regulatory decisions will be for Ofcom to take.”

This report was updated with comment from Openreach

Powered by WPeMatico

The infrastructure that underpins our lives is not something we ever want to think about. Nothing good has come from suddenly needing to wonder “where does my water come from?” or “how does electricity connect into my home?” That pondering gets even more intense when we talk about cellular infrastructure, where a single dropped call or a choppy YouTube video can cause an expletive-laden tirade.

Recently, I visited Verizon’s cellular switch for the New York City metro area (disclosure: TechCrunch is owned by Oath, and Oath is part of Verizon). It’s a completely nondescript building in a nondescript suburb north of the city, so nondescript that it took Verizon’s representative about 15 minutes of circling around just to find it (frankly, the best security through obscurity I have seen in some time).

This switch, along with its sister, powers all cellular service in New York City, including three million voice or voice over LTE (VoLTE) calls and 708 million data connections a day. High-reliability and redundancy is a must for the facility, where dropping even one in 100,000 connections would create more than 7,000 angry customers a day. As Christine Williams, the senior operations manager who oversees the facility, explained, “It doesn’t matter what percentage of dropped calls you have if you are that person.”

As we walked through the server rows that processed those hundreds of millions of connections, I was surprised by just how little digital equipment was actually in the switch itself. “Software-defined networking” has taken full hold here, according to Michele White, who is Verizon’s Executive Director for Network Assurance in the U.S. northeast. As the team has replaced older equipment, the actual physical footprint has continued to downsize, even today. All of New York City’s traffic is run from a handful of feet of server racks.

The key to network assurance is two-fold. First is multiple levels of redundancy at every level of the infrastructure. Inside the switch, independent server racks can take over from other servers that fail, providing redundancy at the machine level. If the air conditioning — which is critical for machine performance — were to fail, mobile AC units can be deployed to pick up the burden.

All equipment in the building is serviced by DC power, and in the event of an external power loss, two diesel generators connected to a large fuel storage tank will take over. The facility is also equipped with battery backups that can sustain the facility for eight hours if the generators themselves don’t function appropriately.

Diesel generators can sustain power to the switch in the event of an external power outage

At a higher level, the switch and its sister share all New York City cellular traffic, but either one could handle the full load if necessary. In short, the goal of the switch’s design is to ensure that that no matter how small or large a problem it might experience, there is an instant backup ready to go to keep those cellular connections alive.

The other half of network assurance is centralization, something that I was surprised to hear in this supposed era of decentralization. Cellular sites in an urban area like New York are often placed on buildings, as anyone looking at roof lines can see from the street. Given those locations, it can be hard to provide backup generators and other failover infrastructure, and servicing them can also be challenging. With centralization, increasingly only the antenna is located at the site, with almost all other operations handled in central control offices and switches where Verizon has greater control of the environment.

Even with intense focus on redundancy, natural disasters can overwhelm even the best laid plans. The telecom company has an additional layer of redundancy with its mobile units, which are placed in a “barnyard” owing to the names of the equipment stored there. There are GOATs (generator on a truck), and COWs (cell on wheels), and BATs (bi-directional amplifier on a truck). These units get deployed to areas of the network that either are experiencing unusually strong demand (think the U.S. Open or a presidential inauguration) or where a natural disaster has stuck (like Hurricane Harvey).

A barnyard filled with animal-named mobile cell infrastructure, including COWs, COLTs, HORSEs, and others

That said, both White and Williams noted that mobile cell deployment is much rarer than people would guess. One reason is that cell sites are increasingly being installed with Remote Electrical Tilt, which allows nearby cell sites to adjust their antennas so as to provide some signal to an area formerly covered by an out-of-commission cell. That process I was told is increasingly automated, allowing the network to essentially self-heal itself in emergencies.

The other reason their deployment is rare is that network assurance already has to handle a remarkable amount of surging traffic throughout the normal ebb and flow of a dense urban city. “Rush hour in Times Square is pretty heavy,” noted Williams. Even something as heavy as a parade through Midtown Manhattan won’t typically exceed the network’s surge capacity.

One other redundancy that Verizon has been exploring is using drones to provide more adaptive coverage. The company has been testing “femto-cell” drone aircraft designed by American Aerospace Technologies that can provide one square mile of coverage for about sixteen hours. A drone capability could be particularly useful in cases like hurricanes, where roads are often littered with debris, making it hard for network engineers to deploy ground-based mobile cells.

I asked about 5G, which I have been covering more heavily this year as telecom deployments pick up. Given the current design of 5G, White and Williams didn’t expect too much change to happen at the switch level, where most of the core technology was likely to remain unchanged.

The trend that is changing things though is edge computing, which is in vogue due to the need for computing to be located closer to users to power applications like virtual reality and autonomous cars. That’s critical, because 50 milliseconds of extra latency could be the difference between an autonomous car hitting another vehicle or a new support pylon and swerving out of the way just in time.

Edge computing in many ways is decentralizing, and therefore there is a tension with the increasingly centralized nature of mobile communications infrastructure. Switches like this one are getting outfitted with edge technology, and more installations are expected in the coming years. 5G and edge are also deeply connected at the antenna level, and that will likely affect cell deployments far more than the switch infrastructure itself.

Edge, internet of things, 5G — all will increase the quantity and scale of the connections flowing through these networks. In the future, a cellular outage may not just inconvenience that YouTube user, but could also prevent an automobile from successfully navigating to a hospital during a natural disaster. It takes backups, backups, and backups to prevent us from ever having to ask, “where does that signal come from?”

Powered by WPeMatico

Inflect, a startup that wants to make it easier for businesses to buy their own internet infrastructure, today announced that it has raised a $3 million seed funding round. The service, which is still in preview, provides business with the necessary data to make their purchasing decisions when they go out and look for their own data center space, networking services and exchange… Read More

Inflect, a startup that wants to make it easier for businesses to buy their own internet infrastructure, today announced that it has raised a $3 million seed funding round. The service, which is still in preview, provides business with the necessary data to make their purchasing decisions when they go out and look for their own data center space, networking services and exchange… Read More

Powered by WPeMatico

OpenStack, the massive open source project that provides large businesses with the software tools to run their data center infrastructure, is now almost eight years old. While it had its ups and downs, hundreds of enterprises now use it to run their private clouds and there are even over two dozen public clouds that use the project’s tools. Users now include the likes of AT&T,… Read More

OpenStack, the massive open source project that provides large businesses with the software tools to run their data center infrastructure, is now almost eight years old. While it had its ups and downs, hundreds of enterprises now use it to run their private clouds and there are even over two dozen public clouds that use the project’s tools. Users now include the likes of AT&T,… Read More

Powered by WPeMatico

There is always a tension inside companies about whether to build or to buy, whatever the need. A few years ago Dropbox decided it was going to move the majority of its infrastructure requirements from AWS into its own data centers. As you can imagine, it took a monumental effort, but the company believed that the advantages of controlling its own destiny would be worth all of the challenges… Read More

There is always a tension inside companies about whether to build or to buy, whatever the need. A few years ago Dropbox decided it was going to move the majority of its infrastructure requirements from AWS into its own data centers. As you can imagine, it took a monumental effort, but the company believed that the advantages of controlling its own destiny would be worth all of the challenges… Read More

Powered by WPeMatico