Indonesia

Auto Added by WPeMatico

Auto Added by WPeMatico

Intudo Ventures, the “Indonesia-only” investment firm, announced today it has closed its third fund, totaling $115 million. Called Intudo Ventures Fund III, it was raised in less than three months and oversubscribed.

Fund III’s limited partners include Black Kite Investments, the family office of Singaporean businessman Koh Bon Hwee; Wasson Enterprises, the family office of former Walgreens Boots Alliance chief executive officer Greg Wasson; and PIDC, the investment arm of Taiwan-based retail conglomerate Uni-President Enterprises Corp. Other LPs include more than 30 Indonesian families and their conglomerates; over 20 leading global funds and managing partners; and more than 10 founders of tech unicorns.

Intudo founding partners Patrick Yip and Eddy Chan launched the firm in June 2017 as the first Indonesia-only venture capital firm, with a debut fund of $10 million. At first, many people were dubious that a country-specific fund focused on early-stage Indonesian companies would take off, especially since Yip and Chan wanted to build a small portfolio and work closely with startups.

Then in 2019, Intudo closed its $50 million second fund with LPs including Founders Fund, which Chan said helped validate its mission. Portfolio companies from its first two funds include Pintu, TaniHub Group and Gredu.

At the beginning, “when we said we were going to raise $10 million, we got laughed out of the room by many managers, but four years into it, we’re running roughly $200 million dollars,” he told TechCrunch. “It shows that for the right markets, hyperlocal is the way to go.”

For its third fund, Intudo intends to invest in about 12 to 14 startups, in sectors like agriculture, B2B and enterprise, education, finance and insurance, healthcare and logistics. Initial check sizes will range from $1 million to $10 million. Leading early-stage and Series A rounds will continue to be Intudo’s core focus, but it also plans to invest in Series B and C rounds for companies from its first two funds.

Unlike many funds that have a handful of anchor investors, all of Intudo’s limited partners are capped at 10% of the total fund size so it can maintain its independent investment thesis and ensure all LPs are treated equally.

“I think 10% is a nice number, where it signals to the founder that we are doing what’s best for their company and not for one special interest group,” said Chan.

The firm will look for companies with competitive moats, like strong intellectual property or deep tech. It also looks for companies that operate in heavily-regulated sectors that are difficult for competitors to enter.

Chan pointed to crypto-exchange Pintu as a good example of Intudo’s investment thesis.

“Everyone was like, you invested in this because it’s trendy, but you have to understand that we met the founder when Bitcoin had dropped down to $6,000. When we gave him the term sheet, six months later in March 2019, Bitcoin was at $3,000,” he said. “The moral of the story is we knew the founder was legit and we were able to pick up all the best talent because you can’t go to a lot of major unicorns to work on crypto.”

Many of Intudo’s portfolio founders are pulkam kampung, or Indonesians who have studied and worked overseas, but returned to launch companies, and it runs a program called Pulkam S.E.A. Turtle Fellowship to mentor aspiring founders. One-third of the deals from Intudo’s first two funds were sourced from universities and the tech community in the United States.

Intudo works closely with founders after signing checks. For example, all of its companies have made a commercial deal sourced through the firm’s network before receiving an investment. Its country-specific approach is also an advantage during the pandemic, because Intudo can continue to hold in-person meetings with founders on an almost weekly basis.

“The founder community has obviously gone through a tough time this year and last year due to COVID,” said Yip. “A lot of these founders needed to make course adjustments and corrections to their business plans. I think our role as an in-market, involved investor has been even more enhanced. A lot of the companies that have gone under, they did not have an in-country partner from the get-go.”

He added, “I think our involved approach and having a concentrated portfolio is something that is appreciated by the founder community as well, so that’s definitely something we intend to rinse and repeat going into Fund III.”

07

Powered by WPeMatico

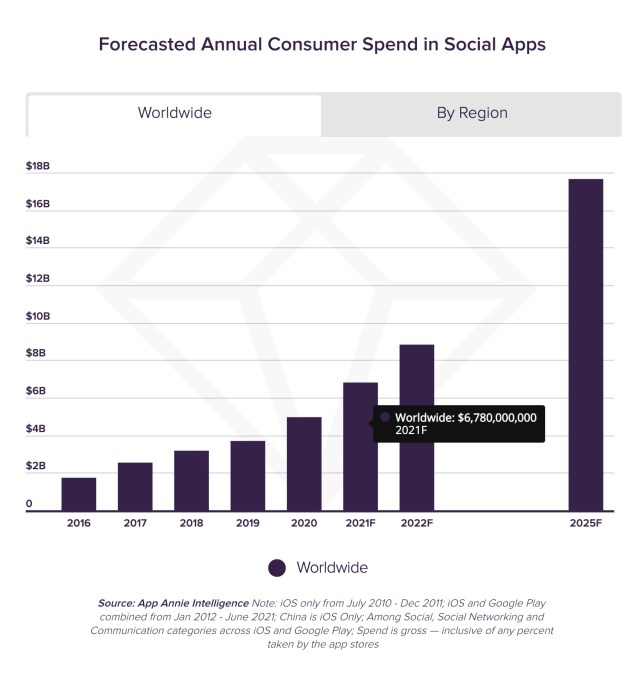

The livestreaming boom is driving a significant uptick in the creator economy, as a new forecast estimates consumers will spend $6.78 billion in social apps in 2021. That figure will grow to $17.2 billion annually by 2025, according to data from mobile data firm App Annie, which notes the upward trend represents a five-year compound annual growth rate (CAGR) of 29%. By that point, the lifetime total spend in social apps will reach $78 billion, the firm reports.

Image Credits: App Annie

Initially, much of the livestream economy was based on one-off purchases like sticker packs, but today, consumers are gifting content creators directly during their livestreams. Some of these donations can be incredibly high, at times. Twitch streamer ExoticChaotic was gifted $75,000 during a live session on Fortnite, which was one of the largest-ever donations on the game-streaming social network. Meanwhile, App Annie notes another platform, Bigo Live, is enabling broadcasters to earn up to $24,000 per month through their livestreams.

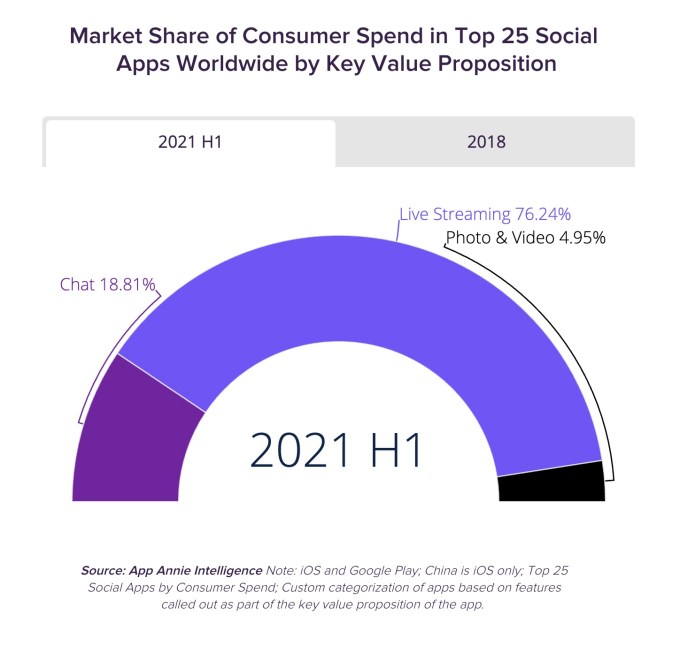

Apps that offer livestreaming as a prominent feature are also those that are driving the majority of today’s social app spending, the report says. In the first half of this year, $3 out every $4 spent in the top 25 social apps came from apps that offered livestreams, for example.

Image Credits: App Annie

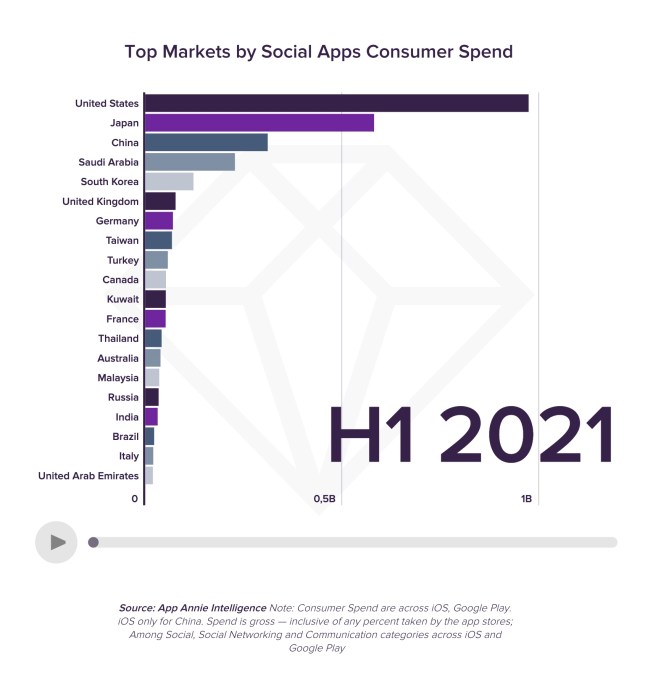

During the first half of 2021, the U.S. become the top market for consumer spending inside social apps, with 1.7x the spend of the next largest market, Japan, and representing 30% of the market by spend. China, Saudi Arabia and South Korea followed to round out the top 5.

Image Credits: App Annie

While both creators and the platforms are financially benefitting from the livestreaming economy, the platforms are benefitting in other ways beyond their commissions on in-app purchases. Livestreams are helping to drive demand for these social apps and they help to boost other key engagement metrics, like time spent in app.

One top app that’s significantly gaining here is TikTok.

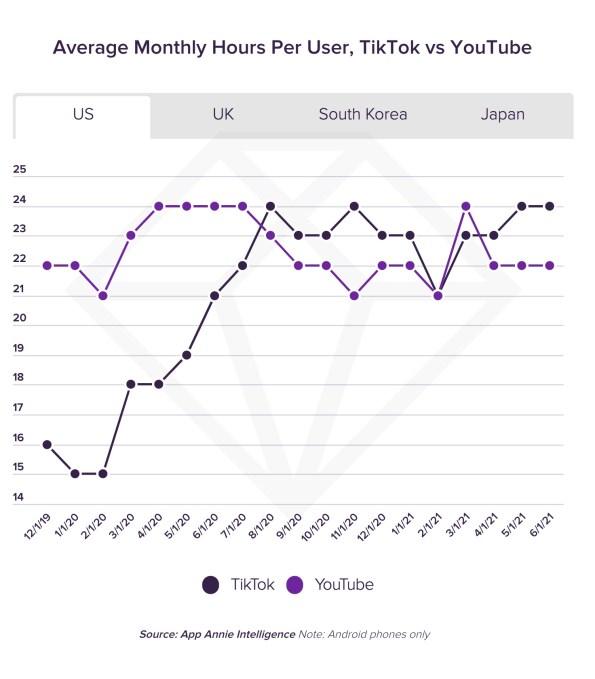

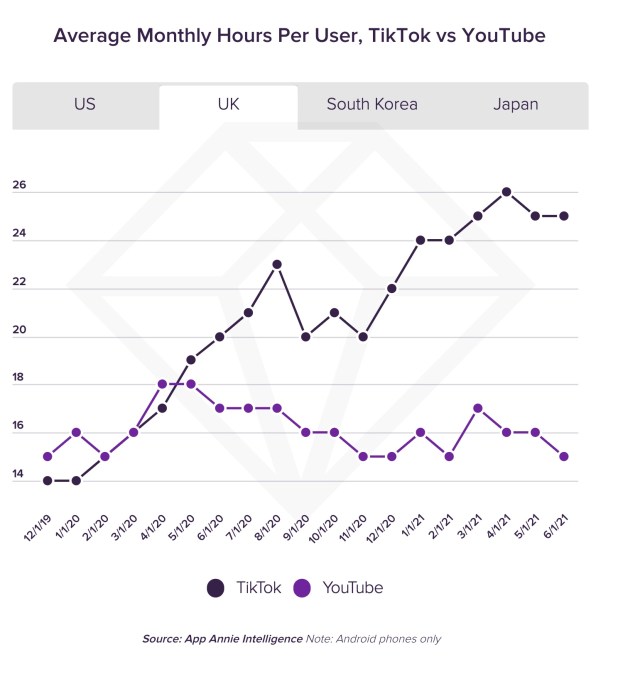

Last year, TikTok surpassed YouTube in the U.S. and the U.K. in terms of the average monthly time spent per user. It often continues to lead in the former market, and more decisively leads in the latter.

Image Credits: App Annie

Image Credits: App Annie

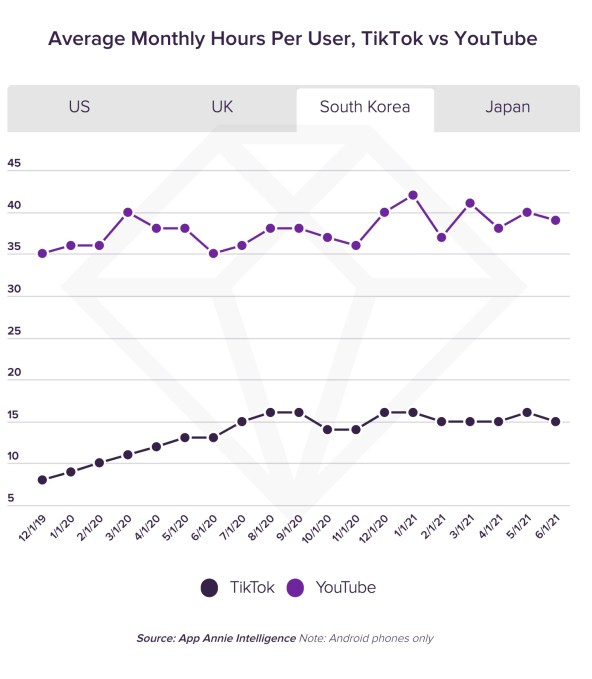

In other markets, like South Korea and Japan, TikTok is making strides, but YouTube still leads by a wide margin. (In South Korea, YouTube leads by 2.5x, in fact.)

Image Credits: App Annie

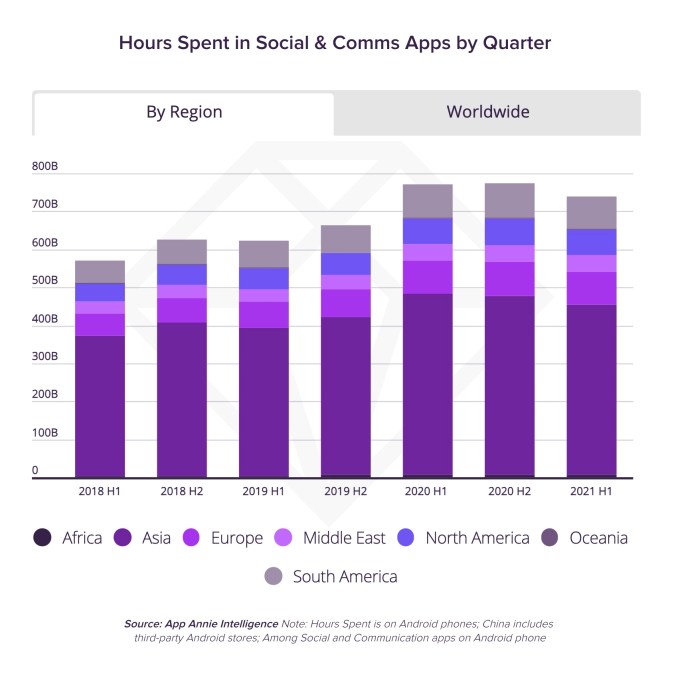

Beyond just TikTok, consumers spent 740 billion hours in social apps in the first half of the year, which is equal to 44% of the time spent on mobile globally. Time spent in these apps has continued to trend upwards over the years, with growth that’s up 30% in the first half of 2021 compared to the same period in 2018.

Today, the apps that enable livestreaming are outpacing those that focus on chat, photo or video. This is why companies like Instagram are now announcing dramatic shifts in focus, like how they’re “no longer a photo sharing app.” They know they need to more fully shift to video or they will be left behind.

The total time spent in the top five social apps that have an emphasis on livestreaming are now set to surpass half a trillion hours on Android phones alone this year, not including China. That’s a three-year CAGR of 25% versus just 15% for apps in the Chat and Photo & Video categories, App Annie noted.

Image Credits: App Annie

Thanks to growth in India, the Asia-Pacific region now accounts for 60% of the time spent in social apps. As India’s growth in this area increased over the past 3.5 years, it shrunk the gap between itself and China from 115% in 2018 to just 7% in the first half of this year.

Social app downloads are also continuing to grow, due to the growth in livestreaming.

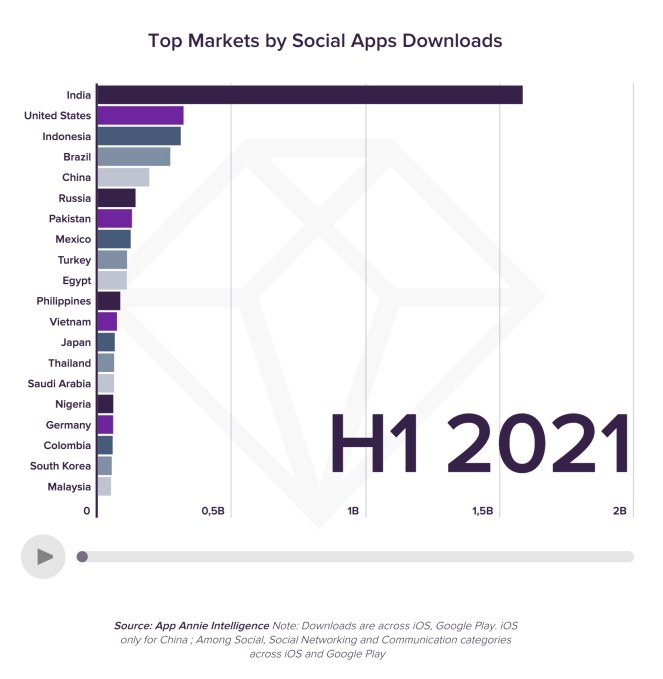

To date, consumers have downloaded social apps 74 billion times, and that demand remains strong, with 4.7 billion downloads in the first half of 2021 alone — up 50% year-over-year. In the first half of the year, Asia was the largest region region for social app downloads, accounting for 60% of the market.

This is largely due to India, the top market by a factor of 5x, which surpassed the U.S. back in 2018. India is followed by the U.S., Indonesia, Brazil and China, in terms of downloads.

Image Credits: App Annie

The shift toward livestreaming and video has also impacted what sort of apps consumers are interested in downloading, not just the number of downloads.

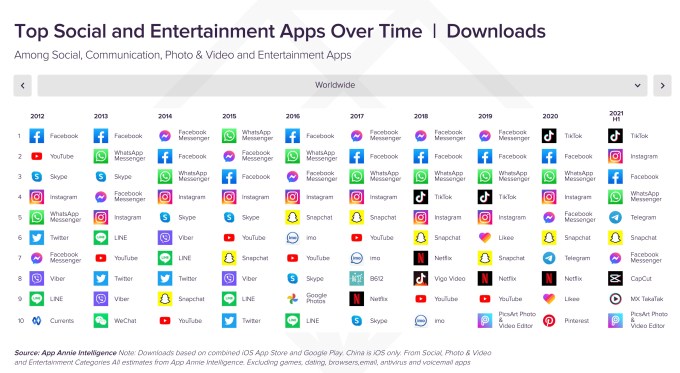

A chart that shows the top global apps from 2012 to the present highlights Facebook’s slipping grip. While its apps (Facebook, Messenger, Instagram and WhatsApp) have dominated the top spots over the years in various positions, TikTok popped into the number one position last year, and continues to maintain that ranking in 2021.

Further down the chart, other apps that aid in video editing have also overtaken others that had been more focused on photos or chat.

Image Credits: App Annie

Video apps like YouTube (#1), TikTok (#2) Tencent Video (#4), Bigo Live (#5), Twitch (#6), and others also now rank at the top of the global charts by consumer spending in the first half of 2021.

But YouTube (#1) still dominates in time spent compared with TikTok (#5), and others from Facebook — the company holds the next three spots for Facebook, WhatsApp and Instagram, respectively.

This could explain why TikTok is now exploring the idea of allowing users to upload even longer videos, by increasing the limit from 3 minutes to 5, for instance.

TikTok is testing a longer 5 minute video upload limit

pic.twitter.com/qiRbJmHkma

— Matt Navarra (@MattNavarra) August 25, 2021

In addition, because of livestreaming’s ability to drive growth in terms of time spent, it’s also likely the reason why TikTok has been heavily investing in new features for its TikTok LIVE platform, including things like events, support for co-hosts, Q&As and more, and why it made the “LIVE” button a more prominent feature in its app and user experience.

App Annie’s report also digs into the impact livestreaming has had on specific platforms, like Twitch and Bigo Live, the former which doubled its monthly active user base from the pre-pandemic era, and the latter which saw $314.2 million in consumer spend during H1 2021.

“The ability of social media users to communicate with each other using live video – or watch others’ live broadcasts – has not only maintained the growth of a social media app market, but contributed to its exponential growth in engagement metrics like time spent, that might otherwise have saturated some time ago,” wrote App Annie’s Head of Insights, Lexi Sydow, when announcing the new report.

The full report is available here.

Powered by WPeMatico

Choosing an insurance policy is one of the most complicated financial decisions a person can make. Jakarta-based Lifepal wants to simplify the process for Indonesians with a marketplace that lets users compare policies from more than 50 providers, get help from licensed agents and file claims. The startup, which says it is the country’s largest direct-to-consumer insurance marketplace, announced today it has raised a $9 million Series A. The round was led by ProBatus Capital, a venture firm backed by Prudential Financial, with participation from Cathay Innovation and returning investors Insignia Venture Partners, ATM Capital and Hustle Fund.

Lifepal was founded in 2019 by former Lazada executives Giacomo Ficari and Nicolo Robba, along with Benny Fajarai and Reza Muhammed. The new funding brings its total raised to $12 million.

The marketplace’s partners currently offer about 300 policies for life, health, automotive, property and travel coverage. Ficari, who also co-founded neobank Aspire, told TechCrunch that Lifepal was created to make comparing, buying and claiming insurance as simple as shopping online.

“The same kind of experience a customer has today on a marketplace like Lazada—the convenience, all digital, fast delivery—we saw was lacking in insurance, which is still operating with offline, face-to-face agents like 20 to 30 years ago,” he said.

Indonesia’s insurance penetration rate is only about 3%, but the market is growing along with the country’s gross domestic product thanks to a larger middle-class. “We are really at a tipping point for GDP per capita and a lot of insurance carriers are focusing more on Indonesia,” said Ficari.

Other venture-backed insurtech startups tapping into this demand include Fuse, PasarPolis and Qoala. Both Qoala and PasarPolis focus on “micro-policies,” or inexpensive coverage for things like damaged devices. PasarPolis also partners with Gojek to offer health and accident insurance to drivers. Fuse, meanwhile, insurance specialists an online platform to run their businesses.

Lifepal takes a different approach because it doesn’t sell micro-policies, and its marketplace is for customers to purchase directly from providers, not through agents.

Based on Lifepal’s data, about 60% of its health and life insurance customers are buying coverage for the first time. On the other hand, many automotive insurance shoppers had policies before, but their coverage expired and they decided to shop online instead of going to an agent to get a new one.

Ficari said Lifepal’s target customers overlap with the investment apps that are gaining traction among Indonesia’s growing middle class (like Ajaib, Pluang and Pintu). Many of these apps provide educational content, since their customers are usually millennials investing for the first time, and Lifepal takes a similar approach. Its content side, called Lifepal Media, focuses on articles for people who are researching insurance policies and related topics like personal financial planning. The company says its site, including its blog, now has about 4 million monthly visitors, creating a funnel for its marketplace.

While one of Lifepal’s benefits is enabling people to compare policies on their own, many also rely on its customer support line, which is staffed by licensed insurance agents. In fact, Ficari said about 90% of its customers use it.

“What we realize is that insurance is complicated and it’s expensive,” said Ficari. “People want to take their time to think and they have a lot of questions, so we introduced good customer support.” He added Lifepal’s combination of enabling self-research while providing support is similar to the approach taken by PolicyBazaar in India, one of the country’s largest insurance aggregators.

To keep its business model scalable, Lifepal uses a recommendation engine that matches potential customers with policies and customer support representatives. It considers data points like budget (based on Lifepal’s research, its customers usually spend about 3% to 5% of their yearly income on insurance), age, gender, family composition and if they have purchased insurance before.

Lifepal’s investment from ProBatus will allow it to work with Assurance IQ, the insurance sales automation platform acquired by Prudential Financial two years ago.

In a statement, ProBatus Capital founder and managing partner Ramneek Gupta said Lifepal’s “three-pronged approach” (its educational content, online marketplace and live agents for customer support) has the “potential to change the way the Indonesian consumer buys insurance.”

Part of Lifepal’s funding will be used to build products to make it easier to claim policies. Upcoming products include Insurance Wallet, which will include an application process with support on how to claim a policy—for example, what car repair shop or hospital a customer should go to—and escalation if a claim is rejected. Another product, called Easy Claim, will automate the claim process.

“The goal is to stay end-to-end with the customer, from reading content, comparing policies, buying and then renewing and using them, so you really see people sticking around,” said Ficari.

Lifepal is Cathay Innovation’s third insurtech investment in the past 12 months. Investment director Rajive Keshup told TechCrunch in an email that it backed Lifepal because “the company grew phenomenally last year (12X) and is poised to beat its aggressive 2021 plan despite the proliferation of the COVID delta variant, accentuating the fact that Lifepal is very much on track to replicate the success of similar global models such as Assurance IQ (US) and PolicyBazaar (India).”

Powered by WPeMatico

Singapore is home to fewer than six million people, making it one of the smallest ASEAN countries, in terms of population. It is a young country as well — having gained independence in 1963 — and resides in a neighborhood with far larger economies, including China, Indonesia, and Vietnam. When the country first became independent, its mandate was to simply survive rather than thrive.

So how does a country evolve from a position of relative uncertainty, with comparatively few resources, to one that leads the ASEAN region in venture capital investment and has been home to 10 unicorns?

Countries around the world examine Singapore’s ecosystem from a distance, hoping to learn from, and emulate, its story. The World Bank Group recently published a report, The Evolution and State of Singapore’s Start-up Ecosystem, documenting the country’s experience in building its startup ecosystem and the challenges facing it.

This article presents an overview of the report’s key findings and offers a few key recommendations on what other countries can learn from Singapore’s experience, as well as what Singapore itself can do to maintain progress.

As of 2019, Singapore had over $19 billion in PE and VC assets under management, more than twice that of neighboring Indonesia, Philippines, Vietnam, Malaysia, and Thailand combined. In that same year, the country was home to an estimated 3,600 tech startups and nearly 200 different intermediary and supporting organizations (accelerators, co-working spaces, coding academies, etc.) – some which have a multinational presence, such as Blk71, whose Singapore headquarters has been referred to as “the world’s most tightly packed entrepreneurial ecosystem.”

While assessing the size and strength of startup ecosystems is an evolving method, Start-up Genome priced Singapore’s ecosystem at over $25 billion, five times the global median.

Arguably, the most eye-catching hallmark of this ecosystem is its population of current and former unicorns. Collectively, Singapore has been home to ten unicorns, three of which have offered an IPO (Nanofilm, Razer and Sea) and two of which have been acquired – one by giant Alibaba (Lazada) and one by Chinese streaming powerhouse YY (Bigo Live). The remaining five are Trax, Acronis, JustCo, PatSnap, and Grab – the ASEAN region’s largest unicorn to date.

The education sector is also prominent in Singapore’s ecosystem. Universities like the National University of Singapore (NUS) and Nanyang Technological University (NTU) are deeply embedded into this ecosystem, helping with R&D commercialization linkages, incubation, talent/knowledge transfer, and other areas.

Numerous factors have contributed to building Singapore’s startup ecosystem, with government intervention and leadership being the dominant driving forces. The government has spent more than USD60 billion over the past several decades to enhance the country’s R&D infrastructure, create VC funds, and launch accelerators and other support organizations.

Powered by WPeMatico

The gamification of payments is not a new concept.

A number of companies are attempting to combine gamification and payments in creative ways. And today, one such company, Play2Pay, has raised $13 million in a Series A round of funding.

The Miami-based startup has a straightforward mission. It wants to give consumers a way to reduce their bills — it claims by an average of 30%! — by playing games, watching videos and completing daily challenges, offers and surveys.

Play2Pay was bootstrapped for the first five years of its life, raising its first external capital in June of 2020 — a $7.5 million seed round from individual angel investors. Telesoft Partners led its Series A round, which included participation from Harbor Spring Capital and individual investors including former AT&T vice chairman Ralph de la Vega, former Reuters CEO Tom Glocer, Madison Dearborn Partners co-founder and senior advisor Jim Perry and Virtusa founder and former CEO, Kris Canekeratne.

The alternative payment platform says it brokers a “value exchange” between brands and consumers, converting attention and engagement into a currency, which can be redeemed for bill payment. Meanwhile, brands get a new way to promote their products and services.

Play2Pay founder and CEO Brian Boroff started the company in 2015 based on a vision that prepaid mobile phone users should have an alternative way to pay for their mobile phone service and that wireless carriers would adopt an ad-funded commercial model.

Today, the company claims to be positioned to be the world’s first “ad supported payment rail” directly integrated into payments platforms of major service providers and financial institutions. It also claims to be the only company that converts user engagement directly into bill payment.

Image Credits: Play2Pay

The “opt-in” offering is currently available to more than 100 million mobile subscribers across the United States, United Kingdom, Mexico, Brazil and Indonesia through partnerships with telecom companies such as AT&T Mexico, Cricket in the U.S., TIM in Brazil, lndosat Ooredoo in Indonesia and U.K.-based Lycamobile.

The rewarding approach seems to be resonating with users. From June 2020 to June 2021, the startup saw its ARR (annual recurring revenue) spike by nearly 300%, according to Boroff, a telecom veteran.

Among the users engaged on the platform, about 25% generated revenue daily, he said. And service providers realized up to 17% revenue expansion as a result of subscriber engagement on the Play2Pay platform, according to Boroff.

“Our distribution model is B2B2C, with Tier-1 service providers worldwide directly integrating our bill payment capability. We’re growing our audience through promotion of the service to their customer base,” he told TechCrunch.

End users, he added, can share their targeting preferences in exchange for value, giving mobile app developers and brands more information when promoting their own products and services to Play2Pay’s audience.

The platform is free for service providers and merchants, meaning the payment does not have costs or fees from interchange, acquirers, chargebacks or gateways.

Instead, Play2Pay generates revenue from mobile app developers and brands. Those developers and brands pay to access Play2Pay’s mobile audience in order to promote their products and services. For example, a mobile gaming company might pay Play2Pay $100 for every user that downloads their app from the Play2Pay app and plays the game for a period of time (such as two hours). Through its technology and partner network, Play2Pay has attribution tracking to ensure that the end user and mobile gaming company both know how much progress has been made toward completing that goal. Other formats include watching videos, completing surveys and more conventional native advertising in some areas.

Powered by WPeMatico

Carro, one of the largest automotive marketplaces in Southeast Asia, announced it has hit unicorn valuation after raising a $360 million Series C led by SoftBank Vision Fund 2. Other participants include insurance giant MSIG and Indonesian-based funds like EV Growth, Provident Growth and Indies Capital. About 90% of vehicles sold through Carro are secondhand, and it offers services that cover the entire lifecycle of a car, from maintenance to when it is broken down and recycled for parts.

Founded in 2015, Carro started as an online marketplace for cars, before expanding into more verticals. Co-founder and chief executive officer Aaron Tan told TechCrunch that, roughly speaking, the company’s operations are divided into three sections: wholesale, retail and fintech. Its wholesale business works with car dealers who want to purchase inventory, while its retail side sells to consumers. Its fintech operation offers products for both, including B2C car loans, auto insurance and B2B working capital loans.

Carro’s last funding announcement was in August 2019, when it said it had extended its Series B to $90 million. The company’s latest funding will be used to fund acquisitions, expand its financial services portfolio and develop its AI capabilities, which Carro uses to showcase cars online, develop pricing models and determine how much to charge insurance policyholders.

It also plans to expand retail services in its main markets: Indonesia, Thailand, Malaysia and Singapore. Carro currently employs about 1,000 people across the four countries and claims its revenue grew more than 2.5x during the financial year ending March 2021.

The COVID-19 pandemic helped Carro’s business because people wanted their own vehicles to avoid public transportation and became more receptive to shopping for cars online. Those factors also helped competitors like OLX Autos and Carsome fare well during the pandemic.

The adoption of electric vehicles across Southeast Asia has resulted in a new tailwind for Carro, because people who buy an EV usually want to sell off their combustion engine vehicles. Carro is currently talking to some of the largest electric vehicle countries in the world that want to launch in Southeast Asia.

“For every car someone typically buys in Southeast Asia, there’s always a trade-in. Where do cars go, right? We are a marketplace, but on a very high level, what we’re doing is reusing and recycling. That’s a big part in the environmental sustainability of the business, and something that sets us apart of other players in the region,” Tan said.

Cars typically stay in Carro’s inventory for less than 60 days. Its platform uses computer vision and sound technology to replicate the experience of inspecting a vehicle in-person. When someone clicks on a Carro listing, an AI bot automatically engages with them, providing more details about the cost of the car and answering questions. They also see a 360-degree view of the vehicle, its interior and can virtually start the engine to see how it sounds. Listings also provide information about defects and inspection reports.

Since many customers still want to get an in-person look before finalizing a purchase, Carro recently launched a beta product called Showroom Anywhere. Currently available in Singapore, it allows people to unlock Carro cars parked throughout the city, using QR codes, so they can inspect it at any time of the day, without a salesperson around. The company plans to add test driving to Showroom Anywhere.

“As a tech company, our job is to make sure we automate everything we can,” said Tan. “That’s the goal of the company and you can only assume that our cost structure and our revenue structure will get better along the years. We expect greater margin improvement and a lot more in cost reduction.”

Pricing is fixed, so shoppers don’t have to engage in haggling. Carro determines prices by using machine-learning models that look at details about a vehicle, including its make, model and mileage, and data from Carro’s transactions as well as market information (for example, how much of a particular vehicle is currently available for sale). Carro’s prices are typically in the middle of the market’s range.

Cars come with a three or seven-day moneyback guarantee and 30-day warranty. Once a customer decides to buy a car, they can opt to apply for loans and insurance through Carro’s fintech platform. Tan said Carro’s loan book is about five years old, almost as old as the startup itself, and is currently about $200 million.

Carro’s insurance is priced based on the policyholders driving behavior as tracked by sensors placed in their cars. This allows Carro to build a profile of how someone drives and the likelihood that they have an accident or other incident. For example, someone will get better pricing if they typically stick to speed limits.

“It sounds a bit futuristic,” said Tan. “But it’s something that’s been done in the United States for many years, like GEICO and a whole bunch of other insurers,” including Root Insurance, which recently went public.

Tan said MSIG’s investment in Carro is a “statement that we are really trying to triple down in insurance, because an insurer has so much linkage with what we do. The reason that MSIG is a good partner is that, like ourselves, they believe a lot in data and the difference in what we call ‘new age’ insurance, or data-driven insurance.”

Carro is also expanding its after-sale services, including Carro Care, in all four of its markets. Its after-sale services reach to the very end of a vehicle’s lifecycle and its customers include workshops around the world. For example, if a Toyota Corolla breaks down in Singapore, but its engine is still usable, it might be extracted and shipped to a repair shop in Nairobi, and the rest of its parts recycled.

“One thing I always ask in management meetings, is tell me where do cars go to die in Indonesia? Where do cars go to die in Thailand? There has to be a way, so if there is no way, we’re going to find a way,” said Tan.

In a statement, SoftBank Investment Advisers managing partner Greg Moon said, “Powered by AI, Carro’s technology platform provides consumers with full-stack services and transparency throughout the car ownership process. We are delighted to partner with Aaron and the Carro team to support their ambition to expand into new markets and use AI-powered technology to make the car buying process smarter, simpler and safer.”

Powered by WPeMatico

BukuWarung, a fintech focused on Indonesia’s micro, small and medium enterprises (MSMEs), announced today it has raised a $60 million Series A. The oversubscribed round was led by Valar Ventures, marking the firm’s first investment in Indonesia, and Goodwater Capital. The Jakarta-based startup claims this is the largest Series A round ever raised by a startup focused on services for MSMEs. BukuWarung did not disclose its valuation, but sources tell TechCrunch it is estimated to be between $225 million to $250 million.

Other participants included returning backers and angel investors like Aldi Haryopratomo, former chief executive officer of payment gateway GoPay, Klarna co-founder Victor Jacobsson and partners from SoftBank and Trihill Capital.

Founded in 2019, BukuWarung’s target market is the more than 60 million MSMEs in Indonesia, according to data from the Ministry of Cooperatives and SMEs. These businesses contribute about 61% of the country’s gross domestic product and employ 97% of its workforce.

BukuWarung’s services, including digital payments, inventory management, bulk transactions and a Shopify-like e-commerce platform called Tokoko, are designed to digitize merchants that previously did most of their business offline (many of its clients started taking online orders during the COVID-19 pandemic). It is building what it describes as an “operating system” for MSMEs and currently claims more than 6.5 million registered merchant in 750 Indonesian cities, with most in Tier 2 and Tier 3 areas. It says it has processed about $1.4 billion in annualized payments so far, and is on track to process over $10 billion in annualized payments by 2022.

BukuWarung’s new round brings its total funding to $80 million. The company says its growth in users and payment volumes has been capital efficient, and that more than 90% of its funds raised have not been spent. It plans to add more MSME-focused financial services, including lending, savings and insurance, to its platform.

BukuWarung’s new funding announcement comes four months after its previous one, and less than a month after competitor BukuKas disclosed it had raised a $50 million Series B. Both started out as digital bookkeeping apps for MSMEs before expanding into financial services and e-commerce tools.

When asked how BukuWarung plans to continue differentiating from BukuKas, co-founder and CEO Abhinay Peddisetty told TechCrunch, “We don’t see this space as a winner takes all, our focus is on building the best products for MSMEs as proven by our execution on our payments and accounting, shown by massive growth in payments TPV as we’re 10x bigger than the nearest player in this space.”

He added, “We have already run successful lending experiments with partners in fintech and banks and are on track to monetize our merchants backed by our deep payments, accounting and other data that we collect.”

BukuWarung’s new funding will be used to double its current workforce of 150, located in Indonesia, Singapore and India, to 300 and develop BukuWarung’s accounting, digital payments and commerce products, including a payments infrastructure that will include QR payments and other services.

Powered by WPeMatico

Cloud kitchens are already meant to reduce the burden of infrastructure on food and beverage brands by providing them with centralized facilities to prepare meals for delivery. This means the responsibility falls on cloud kitchen operators to make sure they have enough locations to meet demand from F&B clients, while ensuring fast deliveries to end customers.

Indonesian network DishServe has figured out a way to make running cloud kitchen networks even more asset-light. Launched by budget hotel startup RedDoorz’s former chief operating officer, DishServe partners with home kitchens instead of renting or buying its own facilities. It currently works with almost 100 home kitchens in Jakarta, and focuses on small- to medium-sized F&B brands, serving as their last-mile delivery network. Launched in fall 2020, DishServe has raised an undisclosed amount of pre-seed funding from Insignia Ventures Partners.

DishServe was founded in September 2020 by Rishabh Singhi. After leaving RedDoorz at the end of 2019, Singhi moved to New York, with plans to launch a new hospitality startup that could quickly convert any commercial space into members’ clubs like Soho House. The nascent company had already created sample pre-fabricated rooms and was about to start leasing property when the COVID-19 lockdown hit New York City in March 2020. Singhi said he went on a “soul searching spree” for a couple of months, deciding what to do and if he should return to Southeast Asia.

He realized that since many restaurants had to switch to online orders and delivery to survive the pandemic, this could potentially be an equalizer for small F&B brands that compete with larger players, like McDonald’s. But lockdowns meant that a lot of people had to pick from a limited range of restaurants close to where they lived. At the same time, Singhi saw that there were a lot of people who wanted to make more money, but couldn’t work outside of their homes, like stay-at-home moms.

DishServe was created to connect all three sides: F&B brands that want to expand without spending a lot of money, home entrepreneurs and diners hungry for more food options. Its other founders include Stefanie Irma, an early RedDoorz employee who served as its country head for the Philippines; serial entrepreneur Vinav Bhanawat; and Fathhi Mohamed, who also co-founded Sri Lankan on-demand taxi service PickMe.

The company works with F&B brands that typically have between just one to 15 retail locations, and want to increase their deliveries without opening new outlets. DishServe’s clients also include cloud kitchen companies who use its home kitchen network for last-mile distribution to expand their delivery coverage and catering services.

“The brands don’t to have to incur any upfront costs, and it’s a cheaper way to distribute as well because they don’t have to pay for electricity, plumbing and other things like that,” said Singhi. “And for agents, it gives them a chance to earn money from their homes.”

Before adding a home kitchen to its network, DishServe screens applicants by asking them to send in a series of photos, then doing an in-person check. If a kitchen is accepted, DishServe upgrades it so it has the same equipment and functionality as the other home kitchens in its network. The company covers the cost of the conversion process, which usually takes about three hours and costs $500 USD, and maintains ownership of the equipment, taking it back if a kitchen decided to stop working with DishServe. Singhi said DishServe is usually able to recover the cost of a conversion four months after a kitchen begins operating.

Home kitchens start out by serving DishServe’s own white-label brand as a trial run before it opens to other brands. Each can serve up to three additional brands at a time.

One important thing to note is that DishServe’s home kitchens, which are usually run by one person, don’t actually cook any food. Ingredients are provided by F&B brands, and home kitchen operators follow a standard set of procedures to heat, assemble and package meals for pick-up and delivery.

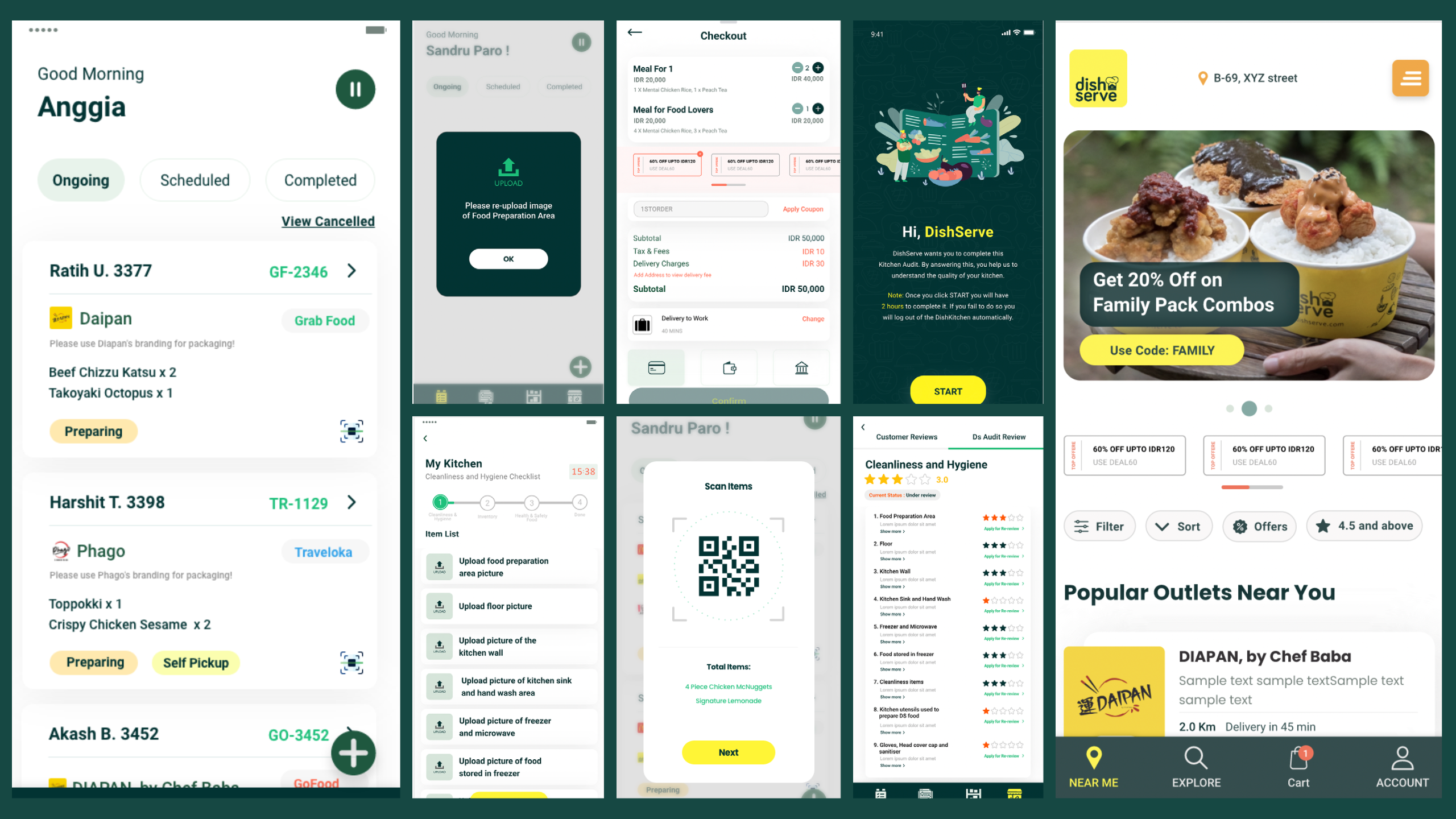

Screenshots of DishServe’s apps for home kitchen operators and customers

DishServe makes sure standard operating procedures and hygiene standards are being maintained through frequent online audits. Agents, or kitchen operators, regularly submit photos and videos of kitchens based on a checklist (i.e. food preparation area, floors, walls, hand-washing area and the inside of their freezers). Singhi said about 90% of its agents are women between the ages of 30 to 55, with an average household income of $1,000. By working with DishServe, they typically make an additional $600 a month once their kitchen is operating at full capacity with four brands. DishServe monetizes through a revenue-sharing model, charging F&B brands and splitting that with its agents.

After joining DishServe, F&B brands pick what home kitchens they want to work with, and then distribute ingredients to kitchens, using DishServe’s real-time dashboard to monitor stock. Some ingredients have a shelf life of up to six months, while perishables, like produce, dairy and eggs, are delivered daily. DishServe’s “starter pack” for onboarding new brands lets them pick pick five kitchens, but Singhi said most brands usually begin with between 10 to 20 kitchens so they can deliver to more spots in Jakarta and save money by preparing meals in bulk.

DishServe plans to focus on growing its network in Jakarta until at least the end of this year, before expanding into other cities. “One thing we are trying to change about the F&B industry is that instead of highly-concentrated, centralized food business, like what exists today, we are decentralizing it by enabling micro-entrepreneurs to act as a distribution network,” Singhi said.

Powered by WPeMatico

TaniHub Group, an Indonesian startup that helps farmers get better prices and more customers for their crops, has raised a $65.5 million Series B. The funding was led by MDI Ventures, the investment arm of Telkom Group, one of Indonesia’s largest telecoms, with participation from Add Ventures, BRI Ventures, Flourish Ventures, Intudo Ventures, Openspace Ventures, Tenaya Capital, UOB Venture Management and Vertex Ventures.

Openspace and Intudo are returning investors from TaniHub’s $10 million Series A, announced in May 2019. The new funding brings its total raised to about $94 million.

Founded in 2016, TaniHub now has more than 45,000 farmers and 350,000 buyers (including businesses and consumers) in its network. The company helps farmers earn more for their crops by streamlining distribution channels so there are fewer middlemen between farms and the restaurants, grocery stores, vendors and other businesses that buy their products. It does this through three units: TaniHub, TaniSupply and TaniFund.

TaniHub is its B2B e-commerce platform, which connects farmers directly to customers. Then orders are fulfilled through TaniSupply, the company’s logistics platform, which currently operates six warehousing and processing facilities where harvests can be washed, sorted and packed within an hour, before being delivered to buyers by TaniHub’s own couriers or third-party logistics providers.

Finally, TaniFund is a fintech platform that provides loans to farmers they can use while growing crops and pay off by selling through TaniHub. Co-founder and chief executive officer Eka Pamitra told TechCrunch its credit scoring system is based on three years of performance, the company’s agriculture value chain expertise and partnerships with financial institutions.

“More than 100 data points are considered when doing the credit risk assessment. For example, for cultivation financing products, TaniFund tailors each credit scoring based on agriculture risks and market risk of each commodity, on top of the typical borrower E-KYC scoring and process,” he explained. “Beyond credit scoring, having TaniSupply and TaniHub as a standby buyer within the ecosystem also helps to mitigate risk of each loan. TaniFund aims to further boost its credit scoring system with smarter data processing and better machine learning models.”

Pamitra said TaniHub will use its new funding to build the upstream and midstream parts of its supply chain — in other words, new cultivation areas, processing, packing centers and warehouses. The company will also expand its coverage beyond Java and Bali to source and sell locally, and continue improving its supply-demand forecast model to help farmers plan crop cultivation and timing, with the goal of reducing price fluctuations and maintaining a consistent supply. Pamitra added that TaniHub will also explore precision farming technology.

Over the last couple of years, TaniHub has started exporting several types of fruits and spices to the United Arab Emirates, Singapore and South Korea. This year, it plans to focus on expanding within Indonesia because the F&B (food and beverage) market there is worth $137 billion and the Indonesian agriculture sector is still highly fragmented, Pamitra said.

Despite the COVID-19 pandemic, TaniHub says it was able to grow its revenue 600% year-on-year in 2020 as demand for online groceries increased.

“We postponed our branch expansion plan and focused on increasing the seven existing warehouses’ since there was a surge of demand on the B2C segment and the process of onboarding farmers. This benefited us since the adoption of purchasing fresh groceries online increased significantly, and the willingness of farmers to work with us became remarkably high because the local traditional markets were closed due to lockdowns,” Pamitra said. “Since COVID-19, the eagerness of provincial governments to open communications for TaniHub to work with local farmers and SMEs in their region has been quite impactful.”

TaniHub is now working with several Indonesian government agencies, including the Ministry of Trade, Ministry of Agriculture and the Ministry of Cooperatives and SMEs, to onboard more farmers, F&B businesses and increase exports.

In a press statement, MDI Ventures director of portfolio management Sandhy Widyasthana said, “TaniHub Group has an important role in transforming the agriculture sector and has proven that its presence can deliver positive impact on the quality of life of farmers. We hope our investment can help them continue their work and expand their coverage to more and more farming communities in Indonesia.”

Powered by WPeMatico

Hangry, an Indonesian cloud kitchen startup that wants to become a global food and beverage company, has raised a $13 million Series A. The round was led by returning investor Alpha JWC Ventures and included participation from Atlas Pacific Capital, Salt Ventures and Heyokha Brothers. It will be used to increase the number of Hangry’s outlets in Indonesia, including launching its first dine-in restaurants, over the next two years before it enters other countries.

Along with a previous round of $3 million from Alpha JWC and Sequoia Capital’s Surge program, Hangry’s Series A brings its total funding to $16 million. It currently operates about 40 cloud kitchens in Greater Jakarta and Bandung, 34 of which launched in 2020. Hangry plans to expand its total outlets to more than 120 this year, including dine-in restaurants.

Founded in 2019 by Abraham Viktor, Robin Tan and Andreas Resha, Hangry is part of Indonesia’s burgeoning cloud kitchen industry. Tech giants Grab and Gojek both operate networks of cloud kitchens that are integrated with their food delivery services, while other startups in the space include Everplate and Yummy.

One of the main ways Hangry sets itself apart is by focusing on its own brands, instead of providing kitchen facilities and services to restaurants and other third-party clients. Hangry currently has four brands, including Indonesian chicken dishes (Ayam Koplo) and Japanese food (San Gyu), that cost about 15,000 to 70,000 IDR per portion (or about $1 to $6 USD). Its food can be ordered through Hangry’s own app, plus GrabFood, GoFood and ShopeeFood.

“Given that Hangry has developed an extensive cloud kitchen network across Indonesia, we naturally would have interest from other brands to leverage our networks,” chief executive officer Viktor told TechCrunch. “However, our focus is to grow our brands since our brands are rapidly growing in popularity in Indonesia and require all kitchen resources that they need to realize their full potential.”

Providing food deliveries helped Hangry grow during COVID-19 lockdowns and social distancing, but in order to become a global brand within a decade, it needs to operate in multiple channels, he added.

“We knew that we will one day have to serve customers in all channels, including dine in,” said Viktor. “We started the hard way, doing delivery-first business, where we faced the challenges surrounding making sure our food still tastes good when it reaches customers’ homes. Now we feel ready to serve our customers in our restaurant premises. Our dine-in concept is an expansion of everything we’ve done in delivery channels.”

In a press statement, Alpha JWC Ventures partner Eko Kurniadi said, “In the span of 1.5 years, [Hangry] launched multiple brands across myriad tastes and categories, and almost all of them are amongst the best sellers list with superior ratings in multiple platforms, tangible examples of product-market fit. This is only the beginning and we can already foresee their growth to be a top local F&B brand in the country.”

Powered by WPeMatico