impact investing

Auto Added by WPeMatico

Auto Added by WPeMatico

Revenue-based investing (RBI), also known as revenue-based financing, or revenue-share investing,1 is a natural next step for the private equity and early-stage venture investment industry. However, due to RBI being a relatively new model, publicly available data is limited.

To address this foundational gap in market information, we have developed a proprietary data set of 32 RBI investment firms, 57 distinct funds and 134 companies that have secured revenue-based investing.

Bootstrapp developed this extensive analysis on revenue-based investing for the purpose of accelerating the shift toward greater transparency and standardization within the industry.

Upon thoroughly analyzing the data, we’ve been able to identify the total number of investment firms and amount of capital that comprise the RBI industry, the specific verticals and business models that are most actively leveraging RBI, and the typical profile of companies that access this form of capital.

These findings are summarized below; a full industry-spanning report that defines the overall revenue-based investing market as it stands today is available to download here.

As context, the financial structures used by VCs haven’t evolved much since they first emerged in 1957. Today, the model is almost precisely the same, with only incremental changes such as more efficient capital markets and industry standards for structuring deals, pricing companies and more.

More recently, we have seen numerous new investment models and financing instruments, including shared earnings agreements and point-of-sale capital. One of the most prominent and popular new models for investors is revenue-based investing (RBI).

However, because the model is new, there is a lack of publicly available data, industry standards have not yet been fully established, and similarly to the equity investment market, there is little transparency into the cost of capital that investees truly pay in exchange for taking on a revenue-based investment.

Thankfully, there have been some notable efforts to drive transparency in the RBI market. For example, Bigfoot Capital open-sourced its RBI model, outlining it in a blog post and sharing their RBI financial model and anonymized term sheet, but a thorough, quantitative, industry-wide analysis has not been conducted until now.

In order to raise RBI, the company must normally be generating revenue, but is not necessarily required to be profitable, although profitability, or at least a near-term path to profitability, is often an important criteria for many investors. “For startups with revenue, RBI may be a good option because, even though the startup may not be profitable, it can reduce dilution — especially for founders,” said Emily Campbell of The Campbell Firm PLLC, a law firm that represents serial entrepreneurs and venture-backed businesses.

“Taking in some smart equity or convertible debt and balancing that money with other financing can be a good strategy for a startup,” she said. Profitability decreases the risk of default and assures that the investee has the ability to service the debt.

In regards to the applications that are best suited to RBI, B2B software-as-a-service (SaaS) companies rise to the top of the list primarily because one is able to — in essence — securitize the revenue being generated by a company and then lend capital against that theoretical security. In addition to SaaS companies, RBI is being used quite frequently in the impact investing community as it solves the problem of a lack of normal M&A or IPO exit paths for impact-driven companies and are sometimes marketed as a nonextractive form of investment structure.

Beyond B2B SaaS and impact investing, many other verticals are adopting the model as well, including e-commerce/D2C, consumer software, food and beverage, and more. It ought to be noted, however, that regardless of the specific business model a company employs, the investee is typically required to have repeatable sales and a track record that demonstrates a strong revenue stream, and therefore a clear ability to return the capital to the investors.

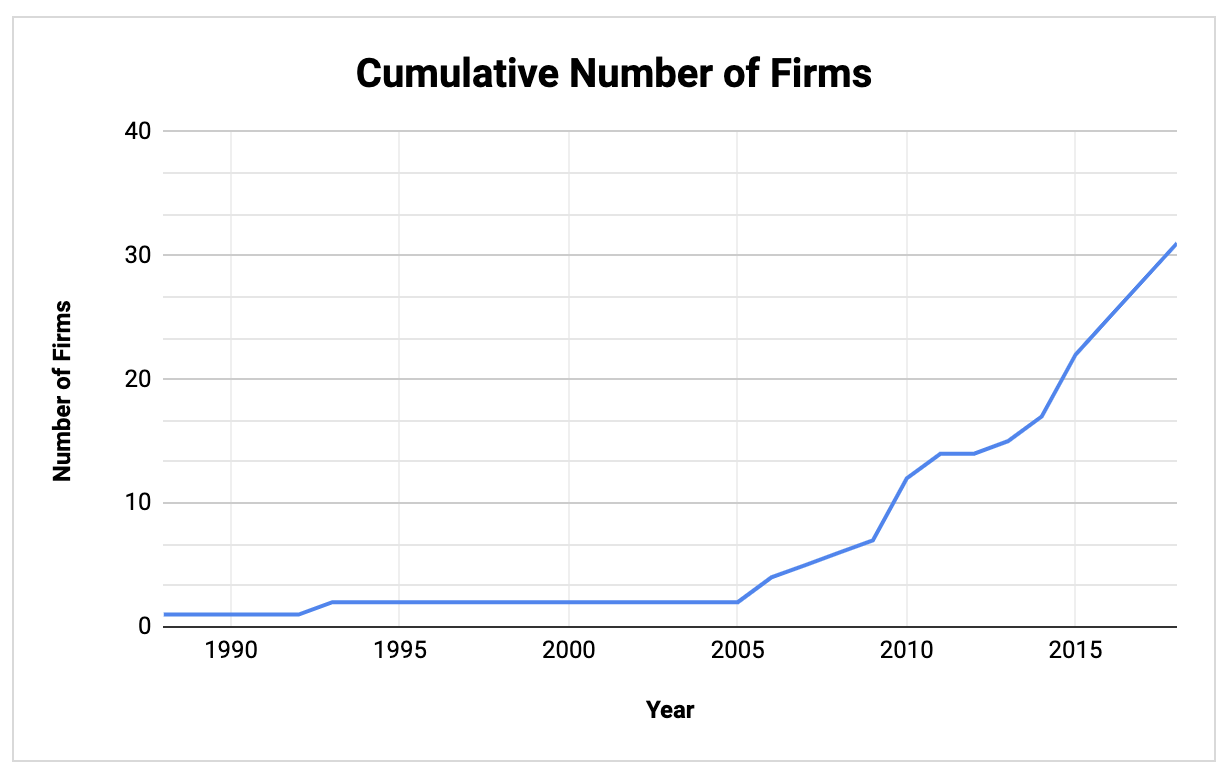

We have identified 32 U.S.-based firms actively investing via a revenue-based investing instrument, with those firms managing 57 distinct funds representing an estimated $4.31 billion in capital. Through our analysis of those firms, funds and investees, we found that:

Firms were included in the data set (and by extension, determined to be actively making revenue-based investments) if they:

The specific number of firms we believe to be quite accurate, representing only active, U.S.-based revenue-based investing firms. The number of funds, however, may be underestimated. This is due to the fact that, although each firm is associated with at least one fund, we did not include additional funds beyond that unless they were confirmed through other sources, such as the firms’ public communications, their SEC Form D or other sources as outlined in the methodology section at the conclusion of the full report.

The total amount of RBI capital that has already been allocated to companies across all firms and all years is $2.1 billion. However, it should be noted that this includes the outliers in our dataset, namely Kapitus, Clearbanc, Braavo and United Capital Source. Once we remove those firms, the remaining 28 firms, representing 51 funds, have allocated $592.8 million.

This figure of $592.8 million is almost certainly an underestimate due to the fact that only 19 of 32 firms had a known “amount of allocated capital,” whereas the remaining 13 firms have unknown values (i.e., zeros) for the amount of capital they have allocated thus far. Therefore, if all 32 firms had a valid and confirmed amount of allocated capital, we can logically conclude that the number would rise dramatically from the current figure of $592.8 million.

New RBI firms have been founded every year since 2013. In 2010, five firms were founded and in 2015 four additional firms were founded, then from 2014-2019, two or more firms were founded each year.

Image Credits: Bootstrapp (opens in a new window)

Clearly, there has been a major uptick in RBI firms being founded since 2005, with a relatively consistent number of new firms being founded over the 15 years since then. In the last 10 years alone, 25 RBI firms have been founded.

Powered by WPeMatico

Funding of Latin American startups has doubled each year over the past two years.

And while most of this capital has been directed toward Brazil and Mexico, this surge is starting to have an effect on startups in the region’s smaller markets. The increased availability of capital for later rounds is creating more opportunities for startups to scale both regionally and globally. And while it may not be one of the largest countries in Latin America, Peru continues to have one of the best-performing economies and fastest-growing startup scenes.

In 2019, a new record was set for the amount of capital invested into Peruvian startups, at least $11 million, a 24% increase compared to 2018. Most of the money went to fintech (47%) and edtech (37%) startups. Over the past four years, more than $22.7 million in public funds went toward startup-related projects as well.

The government-backed program Innóvate Perú awarded approximately $13.8 million of its total investments almost exclusively to startups. Total venture capital investment will likely exceed US$25 million in 2020, doubling what was achieved in 2019, and will continue to grow from there.

In 2019, Peru’s development bank, COFIDE, announced a new fund of funds to invest in venture capital firms, mirroring similar entities such as Chile’s CORFO, Colombia’s Bancoldex and Mexico’s NAFIN. While there are plenty of opportunities to secure seed-stage capital in Peru, many startups still have to look abroad for growth capital. Keynua, Xertica, Turismoi and Runa are just a few of the Peruvian startups that sought international investors to lead their rounds over $1 million. Following in the path of similar funds, the fund of funds will invest $20 million in half a dozen venture capital firms, which would in turn invest in approximately 120 startups.

As government support for entrepreneurs continues to pour in, the Peruvian startup ecosystem is entering a new phase. More and more startups are launching, graduating from accelerator programs and seeking ways to reach their next milestone. Local early-stage investors are stepping in to fill the financing gap and have teamed up to form the Peruvian Seed and Venture Capital Association, PECAP, to share investment opportunities and lay a strong foundation for venture capital in Peru. Here’s a look at just a few of the opportunities for more venture capital to step in.

A massive fintech boom is playing out across Latin America, with the size of the industry expected to exceed $150 billion by 2021. Peru is home to an estimated 120 fintech startups actively tackling the issues of financial inclusion and better servicing the region’s small and medium-sized businesses. Peru’s economy is still largely informal, with approximately 14 million people underbanked. In 2017, María Laura Cuya started Peru’s Fintech Association to work alongside regulators, academics and other organizations to improve financial literacy and access to financial products, with a focus on Peruvian SMEs.

A few of Peru’s fintech sectors stand out, including factoring and foreign exchange, where a number of startups are quickly gaining traction and already branching out to neighboring markets. Innova Funding, Innova Factoring, Facturedo, Kambista and Rextie are just a few examples. Peru’s membership in the Pacific Alliance also makes it an attractive initial market prior to launching in other Pacific Alliance countries.

In 2019, Peruvian fintechs Keynua and Apurata were selected for the Y Combinator accelerator program, putting them on the international radar. Traditional banks in Peru are also shifting their mindsets and warming up to fintech partnerships. The publicly traded Peruvian bank, Credicorp, for example, recently set up a corporate venture fund called Krealo. The bank made its first investments in Culqi, a local payments gateway, and Independencia, a lending platform.

Latin America is a top destination for impact investment capital, outpacing many other regions in the world, with a 15% compound annual growth rate over the last five years, according to the Global Impact Investing Network. Edtech represents a rising entry point across the region for impact investors thanks to its potential for both financial and non-financial returns.

According to an OECD report, approximately 30 million young people in Latin America are not participating in any form of education, training or employment, and 76% of this total are women. Laboratoria, co-founded by edtech thought leader Mariana Costa Checa, helps women develop technical skills and has expanded across the region from its headquarters in Lima to train more than 1,000 women so far. The startup has received praise from global companies, including Walmart and Facebook. In 2019, the skills development platform Crehana raised the largest-ever round for a Peruvian startup ($4.5 million) from both regional and global funds.

Peru attracted more impact investment capital than Mexico, a longtime leader in the region, for the first time in 2018. Much of this investment is focused on improving Peru’s education system. Local startups are addressing everything from early childhood education to workforce training, and as more success stories emerge, more resources will be needed to fully tap into Latin America’s large markets for these solutions.

The government-backed program Innóvate Perú has financed more than 3,400 entrepreneurial projects to date, and more than 25 private institutions are now accelerating, incubating and investing in Peruvian startups. New startup creation is at its highest rate ever; however, these companies are outgrowing their angel and seed-stage supporters and are now seeking ways to take their ventures to the next level.

Over the past few years, Latin America has proven that it is a place where startups can scale and succeed. Now, with more startups coming out of the region’s smaller, underserved markets, like Peru, there is an opportunity to deploy capital effectively and bring impactful solutions to millions of people across the region.

*Angel Ventures was an investor in Culqi before it was sold to BCP. Neither Angel Ventures nor Greg Mitchell currently hold any shares.

Powered by WPeMatico

This guest post was written by David Teten, Venture Partner, HOF Capital. You can follow him at teten.com and @dteten. This is part of an ongoing series on revenue-based investing VC that will hit on:

A new wave of revenue-based investors are emerging who are using creative investing structures with some of the upside of traditional VC, but some of the downside protection of debt.

I’ve been a traditional equity VC for 8 years, and I’m researching new business models in venture capital. As I’ve learned about this model, I’ve been impressed by how these venture capitalists are accomplishing a major social impact goal… without even trying to.

Many are reporting that they’re seeing a more diverse pool of applicants than traditional equity VCs — even though virtually none have a particular focus on women or underrepresented founders. In addition, their portfolios look far more diverse than VC industry norms.

For context, revenue-based investing (“RBI”) is a new form of VC financing, distinct from the preferred equity structure most VCs use. RBI normally requires founders to pay back their investors with a fixed percentage of revenue until they have finished providing the investor with a fixed return on capital, which they agree upon in advance. For more background, see “Revenue-based investing: A new option for founders who care about control“.

I contacted every RBI venture capital investor I could identify, and learned:

By contrast, according to PitchBook Data, since the beginning of 2016, companies with women founders have received only 4.4% of venture capital deals. Those companies have garnered only about 2% of all capital invested. This is despite the fact that the data says that in fact you’re better off investing in women.

Paul Graham href=”http://www.paulgraham.com/bias.html”> observes, “many suspect that venture capital firms are biased against female founders. This would be easy to detect: among their portfolio companies, do startups with female founders outperform those without?

A couple months ago, one VC firm (almost certainly unintentionally) published a study showing bias of this type. First Round Capital found that among its portfolio companies, startups with female founders outperformed those without by 63%.”

Image via Getty Images / runeer

Why are RBI investors investing disproportionately in women & underrepresented founders, and vice versa: why do these founders approach RBI investors?

I’d argue it’s not that RBI is so unbiased and attractive; it’s that traditional equity VC is biased structurally against some women and underrepresented founders.

The Boston Consulting Group and MassChallenge, a US-based global network of accelerators, partnered to study why “women-owned startups are a better bet”. Through their analysis and interviews, BCG identified three primary reasons why female founders are less likely to receive VC funds.

The study used multivariate regression analysis to control for education levels and pitch quality to conclude that gender was a statistically significant factor. I argue that these 3 reasons are much less applicable for RBI investors than for conventional VCs.

Traditional equity VCs are looking for high-risk, high-reward, “swing for the fences” models. The founders of such companies inherently are taking financial risk, reputational risk, and career risk.

Paul Graham, co-founder of Y Combinator, said, “few successful founders grew up desperately poor.” Ricky Yean, a serial founder, agrees: “building and sustaining a company that is “designed to grow fast” is especially hard if you grew up desperately poor”.

Most of the founders of the paradigmatic VC home runs were privileged: male, cisgender, well-educated, from affluent families, etc. Think Bill Gates and Mark Zuckerberg .

That privilege makes it easier for them to take very high risk. The average person, worried about students loans and long term employability, quite rationally is less likely to take the huge risk of founding a company. It’s far safer to just get a job.

Investors who back diverse teams can win much higher returns than the industry norm. Both RBI investors and the founders they back will hopefully benefit from this pattern.

Note that none of the lawyers quoted or I are rendering legal advice in this article, and you should not rely on our counsel herein for your own decisions. I am not a lawyer. Thanks to the experts quoted for their thoughtful feedback.

Powered by WPeMatico

Oakland-based venture capital firm Better Ventures recently closed its second fund at $21 million according to cofounder and managing director Wes Selke. The firm was originally founded as an accelerator called Hub Ventures to help social entrepreneurs running so-called “triple bottom line” startups. These companies measure their success not only by revenue and profitability,… Read More

Oakland-based venture capital firm Better Ventures recently closed its second fund at $21 million according to cofounder and managing director Wes Selke. The firm was originally founded as an accelerator called Hub Ventures to help social entrepreneurs running so-called “triple bottom line” startups. These companies measure their success not only by revenue and profitability,… Read More

Powered by WPeMatico

An accelerator that backed for-profit, for-good ventures, Impact Engine, is abandoning the bootcamp approach and shifting its focus to investing in these startups as a seed fund, according to CEO and Partner Jessica Droste Yagan. Based in Chicago’s 1871 startup hub, Impact Engine also closed a $10 million fund to support this pivot. The fund is its fourth, but now Impact Engine will… Read More

An accelerator that backed for-profit, for-good ventures, Impact Engine, is abandoning the bootcamp approach and shifting its focus to investing in these startups as a seed fund, according to CEO and Partner Jessica Droste Yagan. Based in Chicago’s 1871 startup hub, Impact Engine also closed a $10 million fund to support this pivot. The fund is its fourth, but now Impact Engine will… Read More

Powered by WPeMatico

During the Global Entrepreneurship Summit (GES 2016) at Stanford University today, AngelList, the equity fundraising platform, and activist Shiza Shahid announced a partnership to form a fund called NOW Ventures that will back what they’re calling “mission-driven” startups. That’s the latest label for businesses that want to make a positive social and environmental… Read More

During the Global Entrepreneurship Summit (GES 2016) at Stanford University today, AngelList, the equity fundraising platform, and activist Shiza Shahid announced a partnership to form a fund called NOW Ventures that will back what they’re calling “mission-driven” startups. That’s the latest label for businesses that want to make a positive social and environmental… Read More

Powered by WPeMatico