Hippo

Auto Added by WPeMatico

Auto Added by WPeMatico

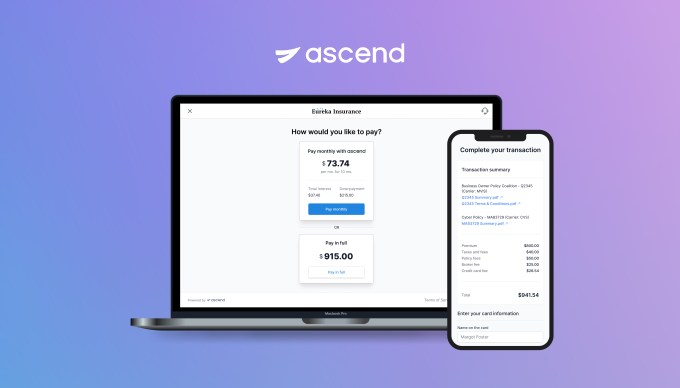

Ascend on Wednesday announced a $5.5 million seed round to further its insurance payments platform that combines financing, collections and payables.

First Round Capital led the round and was joined by Susa Ventures, FirstMark Capital, Box Group and a group of angel investors, including Coalition CEO Joshua Motta, Newfront Insurance executives Spike Lipkin and Gordon Wintrob, Vouch Insurance CEO Sam Hodges, Layr Insurance CEO Phillip Naples, Anzen Insurance CEO Max Bruner, Counterpart Insurance CEO Tanner Hackett, former Bunker Insurance CEO Chad Nitschke, SageSure executive Paul VanderMarck, Instacart co-founders Max Mullen and Brandon Leonardo and Houseparty co-founder Ben Rubin.

This is the first funding for the company that is live in 20 states. It developed payments APIs to automate end-to-end insurance payments and to offer a buy now, pay later financing option for distribution of commissions and carrier payables, something co-founder and co-CEO Andrew Wynn, said was rather unique to commercial insurance.

Wynn started the company in January 2021 with his co-founder Praveen Chekuri after working together at Instacart. They originally started Sheltr, which connected customers with trained maintenance professionals and was acquired by Hippo in 2019. While working with insurance companies they recognized how fast the insurance industry was modernizing, yet insurance sellers still struggled with customer experiences due to outdated payments processes. They started Ascend to solve that payments pain point.

The insurance industry is largely still operating on pen-and-paper — some 600 million paper checks are processed each year, Wynn said. He referred to insurance as a “spaghetti web of money movement” where payments can take up to 100 days to get to the insurance carrier from the customer as it makes its way through intermediaries. In addition, one of the only ways insurance companies can make a profit is by taking those hundreds of millions of dollars in payments and investing it.

Home and auto insurance can be broken up into payments, but the commercial side is not as customer friendly, Wynn said. Insurance is often paid in one lump sum annually, though, paying tens of thousands of dollars in one payment is not something every business customer can manage. Ascend is offering point-of-sale financing to enable insurance brokers to break up those commercial payments into monthly installments.

“Insurance carriers continue to focus on annual payments because they don’t have a choice,” he added. “They want all of their money up front so they can invest it. Our platform not only reduces the friction with payments by enabling customers to pay how they want to pay, but also helps carriers sell more insurance.”

Ascend app

Startups like Ascend aiming to disrupt the insurance industry are also attracting venture capital, with recent examples including Vouch and Marshmallow, which raised close to $100 million, while Insurify raised $100 million.

Wynn sees other companies doing verticalized payment software for other industries, like healthcare insurance, which he says is a “good sign for where the market is going.” This is where Wynn believes Ascend is competing, though some incumbents are offering premium financing, but not in the digital way Ascend is.

He intends to deploy the new funds into product development, go-to-market initiatives and new hires for its locations in New York and Palo Alto. He said the raise attracted a group of angel investors in the industry, who were looking for a product like this to help them sell more insurance versus building it from scratch.

Having only been around eight months, it is a bit early for Ascend to have some growth to discuss, but Wynn said the company signed its first customer in July and six more in the past month. The customers are big digital insurance brokerages and represent, together, $2.5 billion in premiums. He also expects to get licensed to operate as a full payment in processors in all states so the company can be in all 50 states by the end of the year.

The ultimate goal of the company is not to replace brokers, but to offer them the technology to be more efficient with their operations, Wynn said.

“Brokers are here to stay,” he added. “What will happen is that brokers who are tech-enabled will be able to serve customers nationally and run their business, collect payments, finance premiums and reduce backend operation friction.”

Bill Trenchard, partner at First Round Capital, met Wynn while he was still with Sheltr. He believes insurtech and fintech are following a similar story arc where disruptive companies are going to market with lower friction and better products and, being digital-first, are able to meet customers where they are.

By moving digital payments over to insurance, Ascend and others will lead the market, which is so big that there will be many opportunities for companies to be successful. The global commercial insurance market was valued at $692.33 billion in 2020, and expected to top $1 trillion by 2028.

Like other firms, First Round looks for team, product and market when it evaluates a potential investment and Trenchard said Ascend checked off those boxes. Not only did he like how quickly the team was moving to create momentum around themselves in terms of securing early pilots with customers, but also getting well known digital-first companies on board.

“The magic is in how to automate the underwriting, how to create a data moat and be a first mover — if you can do all three, that is great,” Trenchard said. “Instant approvals and using data to do a better job than others is a key advantage and is going to change how insurance is bought and sold.”

Powered by WPeMatico

Marshmallow — a U.K.-based car insurance provider that has made a name for itself in the market by providing a new approach to car insurance aimed at using a wider set of data points and clever algorithms to net a more diverse set of customers and provide more competitive rates — is announcing a milestone today in its life as a startup, as well as in the bigger U.K. tech world.

The London company — co-founded by identical twins Oliver and Alexander Kent-Braham and David Goaté — has raised $85 million in a new round of funding. The Series B valuation is significant on two counts: it catapults Marshmallow to a “unicorn” valuation above $1 billion — specifically, $1.25 billion; and Marshmallow itself becomes one of a very small group of U.K. startups founded by Black people — Oliver and Alexander — to reach that figure.

(To be clear, Marshmallow describes itself as “the first UK unicorn to be founded by individuals that are Black or have Black heritage”, although I can think of at least one that preceded it: WorldRemit, which last month rebranded to Zepz, and is currently valued at $5 billion; co-founder and chairman Ismail Ahmed has been described as the most influential Black Briton.)

Regardless of whether Marshmallow is the first or one of the first, given the dearth of diversity in the U.K. technology industry, in particular in the upper ranks of it, it’s a notable detail worth pointing out, even as I hope that one day it will be less of a rarity.

Meanwhile, Marshmallow’s novel, big-data approach and successful traction in the market speak for themselves. When we covered the company’s most recent funding round before this — a $30 million raise in November 2020 — the startup was valued at $310 million. Now less than a year later, Marshmallow’s valuation has nearly quadrupled, and it has passed 100,000 policies sold in its home country, growing 100% over the last six months.

The plan now, Oliver told me in an interview, will be to deepen its relationships with customers, in part by providing more engagement to make them better drivers, but also potentially selling more services to them, too.

In this, the startup will be tapping into a new approach that other insurtech startups are taking as they rethink traditional insurance models, much like YuLife is positioning its life insurance products within a bigger wellness and personal improvement business. Currently, the average age of Marshmallow’s customers is 20 to 40, Oliver said — and there are thoughts of potentially new products aimed at even younger users. That means there is long-term value in improving loyalty and keeping those customers for many years to come.

Alongside that, Marshmallow will also use the funding to inch closer to its plan to expand to markets outside of the U.K. — a strategy that has been in the works for a while. Marshmallow talked up international expansion in its last round but has yet to announce which markets it will seek to tackle first.

Insurance — and in particular insurance startups — are often thought of together with fintech startups, not least because the two industries have a lot in common: they both operate in areas of assessing and mitigating risk and fraud; they are in many cases discretionary investments on the part of the customers; and they are both highly regulated and require watertight data protection for their users.

Perhaps because so much of the hard work is the same for both, it’s not uncommon to see services built to serve both sectors (FintechOS and Shift Technology being two examples), for fintech companies to dabble in insurance services, and so on.

But in reality, insurance — and specifically car insurance — has seen a massive impact from COVID-19 unique to that industry. Separate reports from EY and the Association of British Insurers noted that 2020 actually saw a lift for many car insurance companies: lockdowns meant that fewer people were driving, and therefore fewer were getting into accidents and making fewer claims.

2021, however, has been a different story: new pricing rules being put into place will likely see a number of providers tip into the red for the year. And the Chartered Insurance Institute points out that it will also be worth watching to see how the low use of cars in one year will impact use going forward: some car owners, especially in urban areas where keeping a car is expensive, will inevitably start to question whether they need to own and insure a car at all.

All of this, ironically, actually plays into the hand of a company like Marshmallow, which is providing a more flexible approach to customers who might otherwise be rejected by more traditional companies, or might be priced out of offerings from them. Interestingly, while neobanks have definitely spurred more traditional institutions to try to update their products to compete, the same hasn’t really happened in insurance — not yet, at least.

“We started with the idea of the power of data and using a wider range of resources [than incumbents], and using that in our pricing led us to be able to offer better rates to more people,” Oliver said, but that hasn’t led to Marshmallow seeing sharper competition from older incumbents. “They are big companies and stuck in their ways. These companies have been around for decades, some for centuries. Change is not happening quickly.”

That leaves a big opportunity for companies like Marshmallow and other newer players like Lemonade, Hippo and Jerry (not an insurance startup per se but also dabbling in the space), and a big opening for investors to back new ideas in an industry estimated to be worth $5 trillion.

“The traction the team has achieved demonstrates the demand for a new kind of insurance provider, one that focuses more on consumer experience and uses the latest technology and data to give fair prices,” said Eileen Burbidge, a partner at Passion Capital, in a statement. “We’ve been proud to support the team’s ambitions since the start, and now look forward to its next chapter in Europe as it continues its mission to change the industry for the better.”

Powered by WPeMatico

Tech stocks are getting hammered today, with previously high-flying shares of software companies taking even more damage.

For a sector that has enjoyed a year in the sun, recent trading sessions have punctured a period of market adoration. It is too soon to say that the market is repricing tech stocks, but the selloff has reached the point of materiality and is therefore something we need to note.

As we write, the tech-heavy Nasdaq Composite is off another 1.2% today after previous declines. The now-infamous ARK Innovation ETF is off 6.5% and the list of individual declines worth noting in the tech sector is very long indeed.

The change in sentiment is clear in recent results. Here’s the tech-heavy Nasdaq Composite:

And the damage intensifies if we consider just SaaS and cloud stocks. Here’s the Bessemer cloud index:

In more prosaic terms, the Nasdaq is in a technical correction, while SaaS stocks have reached bear-market territory. That’s quite a turnabout from recent all-time highs for both.

Lost on the TechCrunch editing floor from late yesterday is a post we wrote noting the sharp declines in the value of insurtech stocks ahead of the impending public debut of Hippo, another neo-insurance company. The SPAC-led Hippo flotation will not touch down in a warm market. Instead, its contemporaries look like this today:

The damage is widespread. Hell, recent IPO success-story Snowflake announced yesterday that it grew from revenues of $88 million in its year-ago quarter to $190 million in its most recent. And its stock is off more than 7% today.

We’ll leave it to you whether the changing public valuations are just a blip or a more staid change in the winds. But it does feel different out there.

For startups, this is all somewhat poor news. Valuations for public comps were strong in 2020. To lose that halo in 2021 could crimp late-stage valuations, perhaps even reaching back to Series A and B rounds to limit some upside for growing upstarts. But such an impact will lag the public markets, so don’t expect things to change quite yet.

Still, every private investor has their eye on the exit when it comes to their deals. And if that exit is suddenly shrinking, so too might their interest in paying for quite so great a markup on their next deal.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Natasha and Danny and Alex and Grace were all here to chat through the week’s biggest tech happenings. It was yet another crazy week, but we did our best to get through as much of it as we could. Here’s the rundown, in case you are reading along with us!

And with that we are back on Monday. Have a rocking weekend!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Metromile began trading as a public company yesterday. Its exit from the private market was accelerated by its decision to combine with a special purpose acquisition company, or SPAC.

Such transactions have exploded in popularity in recent years, bridging the gap between a host of richly valued private companies and endless bored capital. SPACs raise cash, go public and then merge with a private entity. The SPAC then dissolves itself into the combined entity, a process that often includes an additional slug of money (PIPE) for good measure.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

SPAC-led debuts can move faster than a traditional IPO, making them attractive to companies in a hurry. And with more visibility into how much capital might be raised than during a traditional public-offering pricing run, they can smooth worries amongst target-companies regarding how much cash they can attract by leaving the private-market fold.

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

But with many more SPACs coming our way, we took Metromile’s debut as a learning moment. To that end, we got on the horn with CEO Dan Preston to chat about what the day meant for his company, and to elicit a note or two on the SPAC process for our own enjoyment.

TechCrunch asked Preston about the SPAC world and how his combination came about. He said his firm started by dipping its toe into the blank-check waters, kicking off with a small set of conversations, chats that quickly gathered traction.

But don’t take that to mean that any company will elicit a similar market response. Preston said SPACs are designed for a specific class of company; namely those that want or need to share a bit more story when they go public. Younger companies, in other words, for whom a traditional S-1 filing might not be provide a sufficient summation of its potential.

Powered by WPeMatico

As we head toward the exits of 2020, we have one more name to add to our roll call of private companies that have reached the $100 million annual recurring revenue (ARR) milestone. Well, one and a half.

But before we get into Nexthink and give Coalition a honorable mention, let’s talk about the startups we’re looking for in 2021.

The $100 million ARR list came together by accident, a quirk of a news cycle that happened to have a few companies reach the threshold when I was in transition back to working at TechCrunch. So, when I got back into our WordPress install, the group of companies that had each recently reached nine-figure revenues was top of mind.

The $100 million ARR list came together by accident, a quirk of a news cycle that happened to have a few companies reach the threshold when I was in transition back to working at TechCrunch. So, when I got back into our WordPress install, the group of companies that had each recently reached nine-figure revenues was top of mind.

But looking at $100 million ARR companies proved less useful than we might have hoped. Mostly what we managed was to collect a bucket of companies that were about to go public.

That was always a risk. As we wrote at the time:

Perhaps the startup market would do well to celebrate the $50 million ARR mark even more loudly. At $50 million ARR, a startup is scaling to IPO size. That’s the goal, after all.

This is our aim for 2021.

If your startup is approaching the $50 million ARR mark, or the $50 million annual run rate threshold, I want to hear from you. Drop a line if your startup has an annualized run rate between $35 million and $60 million, is privately held, and you are willing to chat about how quickly it is growing. (The Exchange first raised this idea in November.)

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But that’s next year. Today, let’s chat about Nexthink, what the hell “digital employee experience” is and what’s good with cyber insurance and why it’s helping Coalition grow rapidly.

Nexthink is a venture-backed software company with headquarters in Lausanne, Switzerland and Boston. According to PitchBook, Nexthink raised external capital in modest amounts from 2006 until 2014, when the startup picked up a $14.5 million Series D. That round was its first worth more than $10 million.

From there, Nexthink was a venture capital success story, presumably scaling quickly as it raised two larger rounds in 2016 and 2018 worth an estimated $40 million and $85 million, respectively. Nexthink was valued at a little over $558 million (post-money) following its 2018 round.

How did it attract so much external funding? By building digital experience monitoring software. Which, after doing a bit of research this morning, appears to be software aimed at tracking what corporate end users are doing with devices and how well software running on those devices perform.

Powered by WPeMatico

In the wake of insurtech unicorn Root’s IPO, it felt safe to say that the big transactions for the insurance technology startup space were done for the year.

After all, 2020 had been a big one for the broad category, with insurtech marketplaces raising lots, rental insurance startup Lemonade going public, Root itself debuting even more recently on the back of its automotive insurance business, a big round to help Hippo keep building its homeowners company and more.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But yesterday brought with it even more news: Metromile, a startup competing in the auto insurance market, is going public via a blank-check company (SPAC), and Hippo raised a huge, unpriced round.

So let’s talk about why Metromile might be plying the public markets, and why Hippo may have have decided to pick up more cash. Hint: The reasons are related.

So let’s talk about why Metromile might be plying the public markets, and why Hippo may have have decided to pick up more cash. Hint: The reasons are related.

The Lemonade IPO was a key moment for neoinsurance startups, a key part of the broader insurtech space. When the rental insurance provider went public, it helped set the tone for public exit valuations for companies of its type: fast-growing insurance companies with slick consumer brands, improving economics, a tech twist and stiff losses.

For the Roots and Metromiles and Hippos, it was an important moment.

So, when Lemonade raised its IPO range, and then traded sharply higher after its debut, it boded well for its private comps. Not that rental insurance and auto insurance or homeowners insurance are the same thing. They very most decidedly are not, but Lemonade’s IPO demonstrated that private investors were correct to bet generally on the collection of startups, because when they reached IPO-scale, they had something that public investors wanted.

Powered by WPeMatico

This morning Root Insurance, a neoinsurance provider that has attracted ample private capital for its auto-insurance business, is targeting a valuation of as much as $6.34 billion in its pending IPO.

The former startup follows insurtech leader Lemonade to the public markets during a year in which IPOs have been well-received by investors focused more on growth than profitability. In the wake of Lemonade’s strong public offering and rich revenue multiples, it was not impossible to see another, similar startup test the same waters.

Root’s $6.34 billion valuation upper limit at its current price range matches expectations for its bulk. The company is targeting $22 to $25 per share in its debut.

The startup will raise over $500 million from the shares it is selling in its regular offering. Concurrent placements worth $500 million from Dragoneer and Silver Lake raise that figure to north of $1 billion and could help boost general demand for shares in the company. Snowflake’s epic IPO came with similar private placements from well-known investors in what became the transaction of the year.

Will we see Root boost its target? And what does Root’s IPO price range mean for insurtech startups? Let’s dig into the numbers.

We’ve dug into Root’s business a few times now, both before and after it formally filed its IPO documents. This morning we will merge both sets of work, snag a fresh revenue multiple from Lemonade, apply it to Root’s own numbers, observe any valuation deficit and ask ourselves what’s next for the debuting company.

Will we see Root’s IPO price rise? Here’s how to think about the question:

Powered by WPeMatico

During the week’s news cycle one particular bit of reporting slipped under our radar: Root Insurance is tipped by Reuters to be prepping an IPO that could value the neo-insurance provider at around $6 billion.

Coming after two 2020 insurtech IPOs, Root’s steps toward the public markets are not surprising. But they are good news all the same for a number of insurance startups that have raised lots of capital and will eventually need to prepare their own debuts if they don’t find a larger corporate home.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Programming note: The Exchange column is off starting tomorrow through next week. The newsletter will go out as always on Saturdays. I’m taking a week to sit and do nothing.

The Root IPO will also help clarify Lemonade’s own public offering and ensuing valuation. Lemonade’s debut brought a strong price to the rental-focused insurance provider, leading to a more buoyant attitude toward the valuation of its class of startups. More precisely, the public price assigned to Lemonade when it floated was, no bullshit, very bullish.

If Root can repeat the feat it would cast a warm light on the yet-private players in its niche that will have their eyes pinned to the flotation. Names like MetroMile and Hippo could be next if Root’s IPO goes well.

But, first, does Root make sense at a $6 billion valuation? We can do a little digging on that this morning, using Lemonade’s present-day valuation to get a handle on the figure. Let’s go!

Before we get into the numbers, bear in mind that we’re going to compare apples and oranges today, and that we’ll have to use some dated numbers as well. That said, we can still get somewhere about what Root could be worth. So, roll with me but don’t take every number as engraved onto an obelisk.

Back in July of this year, in the wake of the Lemonade IPO and Hippo’s latest funding round, a $150 million investment at a $1.5 billion post-money valuation, we started to do some math. Lemonade’s valuation was much richer than Hippos’ when you look at their multiples, which got us thinking about private and public neo-insurance provider valuations: Why was Lemonade worth so much more than its peers per dollar of written premium?

To better understand the situation, we dug up some 2019 data on the dollar value of gross written premium Hippo and Lemonade wrote and found new valuation multiples for them based on those numbers. Lemonade was worth 28.4x its Q1 annualized gross written premium, while Hippo was worth just 5.6x its own.

Then we also found Root and MetroMile gross written premium numbers for 2019, which allowed us to calculate their own effective valuations (albeit using dated numbers).

As before when we found that Hippo’s private valuation looked light compared to Lemonade’s public valuation when we contrasted their valuation/gross written premium multiple, we discovered that MetroMile and Root also looked cheap. Very cheap.

Powered by WPeMatico

On the heels of Hippo’s funding round and our exploration of how the private markets appear to be more conservative than public investors at the moment, we’re asking a new question: are a bunch of insurtech startups undervalued?

Hippo — an insurtech startup focused on home insurance — put together a $150 million round at a $1.5 billion post-money valuation after growing its gross written premium to $270 million “in the past 12 months.” At that valuation, and at pre-adjustment premium scale, Hippo is super-cheap compared to Lemonade, another venture-backed insurtech startup that just went public.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or receive it for free in your inbox. Sign up for The Exchange newsletter, which drops Saturdays starting July 25.

There’s no need to relitigate Hippo’s valuation and how the private markets have valued the firm. But our work yesterday does give us the chance to do some fun math on other players in the neo-insurance space, namely, Root and MetroMile. Using data accrued from financial filings and valuation data from Pitchbook and Crunchbase, we can grok how much the two firms are worth using Hippo’s and Lemonade’s current premium multiples.

If you aren’t familiar, the cohort of startups we’re looking at have raised well over $1 billion as a group; VCs really believe in them. How they are priced then, and how they exit, will help determine the results of many a venture fund.

If you aren’t familiar, the cohort of startups we’re looking at have raised well over $1 billion as a group; VCs really believe in them. How they are priced then, and how they exit, will help determine the results of many a venture fund.

So, are other players in the startup insurance market cheap at their last private price when compared to Lemonade and Hippo? Did their venture backers overpay? Let’s find out.

Powered by WPeMatico