Health

Auto Added by WPeMatico

Auto Added by WPeMatico

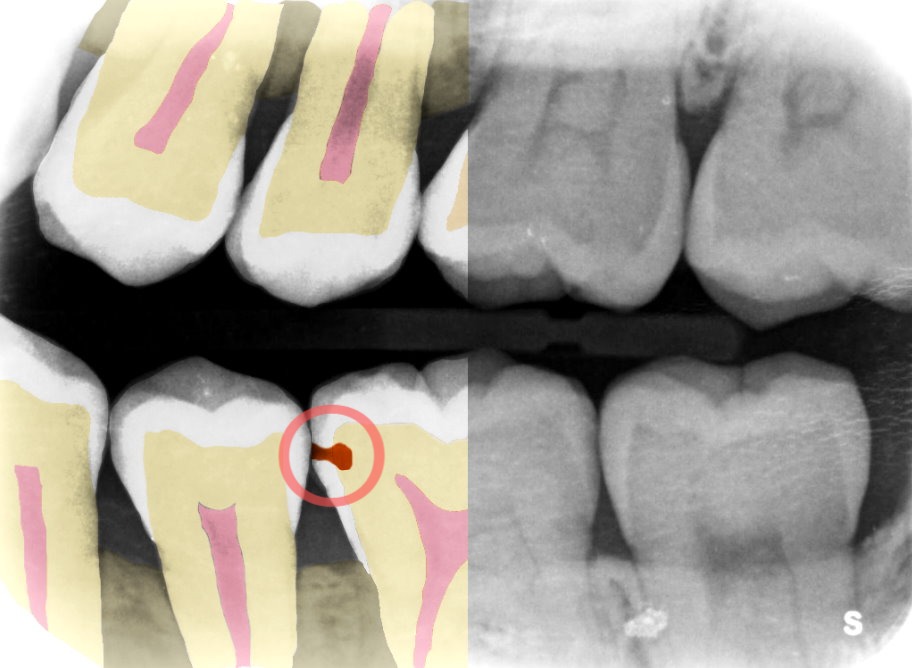

Like other areas of healthcare, the dental industry is steadily embracing technology. But while much of it is in the orthodontic realm, other startups, like Adra, are bringing artificial intelligence into a dentist’s day-to-day workflow, particularly in finding cavities, of what will be a $435.08 billion global dental services market this year.

The Singapore-based company was founded in 2021, but was an idea that started last year. Co-founder Hamed Fesharaki has been a dentist for over a decade and owns two clinics in Singapore.

He said dentists learn to read X-rays in dental school, but it can take a few years to get good at it. Dentists also often have just minutes to read them as they hop between patients.

As a result, dentists end up misdiagnosing cavities up to 40% of the time, co-founder Yasaman Nematbakhsh said. Her background is in imaging, where she developed an artificial intelligence machine identifying hard-to-see cancers, something Fesharaki thought could also be applied to dental medicine.

Providing the perspective of a more experienced dentist, Adra’s intent is to make every dentist “a super dentist,” Fesharaki told TechCrunch. Its software detects cavities and other dental problems on dental X-rays faster and 25% more accurately, so that clinics can use that time to better serve patients and increase revenue.

Example of Adra’s software. Image Credits: Adra

“We are coming from the eye of an experienced dentist to help illustrate the problems by turning the X-rays into images to better understand what to look for,” he added. “Ultimately, the dentist has the final say, but we bring the experience element to help them compare and give them suggestions.”

By quickly pointing out the problem and the extent of it, dentists can decide in what way they want to treat it — for example, do a filling, a fluoride treatment or wait.

Along with third co-founder Shifeng Chen, the company is finishing up its time in Y Combinator’s summer cohort and has raised $250,000 so far. Fesharaki intends to do more formalized seed fundraising and wants to bring on more engineers to tackle user experience and add more features.

The company has a few clinics doing pilots and wants to attract more as it moves toward a U.S. Food and Drug Administration clearance. Fesharaki expects it to take six to nine months to receive the clearance, and then Adra will be able to hit the market in late 2022 or early 2023.

Powered by WPeMatico

Poland-based health tech AI startup Cardiomatics has announced a $3.2 million seed raise to expand use of its electrocardiogram (ECG) reading automation technology.

The round is led by Central and Eastern European VC Kaya, with Nina Capital, Nova Capital and Innovation Nest also participating.

The seed raise also includes a $1 million non-equity grant from the Polish National Centre of Research and Development.

The 2017-founded startup sells a cloud tool to speed up diagnosis and drive efficiency for cardiologists, clinicians and other healthcare professionals to interpret ECGs — automating the detection and analysis of some 20 heart abnormalities and disorders with the software generating reports on scans in minutes, faster than a trained human specialist would be able to work.

Cardiomatics touts its tech as helping to democratize access to healthcare — saying the tool enables cardiologists to optimise their workflow so they can see and treat more patients. It also says it allows GPs and smaller practices to offer ECG analysis to patients without needing to refer them to specialist hospitals.

The AI tool has analyzed more than 3 million hours of ECG signals commercially to date, per the startup, which says its software is being used by more than 700 customers in 10+ countries, including Switzerland, Denmark, Germany and Poland.

The software is able to integrate with more than 25 ECG monitoring devices at this stage, and it touts offering a modern cloud software interface as a differentiator versus legacy medical software.

Asked how the accuracy of its AI’s ECG readings has been validated, the startup told us: “The data set that we use to develop algorithms contains more than 10 billion heartbeats from approximately 100,000 patients and is systematically growing. The majority of the data-sets we have built ourselves, the rest are publicly available databases.

“Ninety percent of the data is used as a training set, and 10% for algorithm validation and testing. According to the data-centric AI we attach great importance to the test sets to be sure that they contain the best possible representation of signals from our clients. We check the accuracy of the algorithms in experimental work during the continuous development of both algorithms and data with a frequency of once a month. Our clients check it everyday in clinical practice.”

Cardiomatics said it will use the seed funding to invest in product development, expand its business activities in existing markets and gear up to launch into new markets.

“Proceeds from the round will be used to support fast-paced expansion plans across Europe, including scaling up our market-leading AI technology and ensuring physicians have the best experience. We prepare the product to launch into new markets too. Our future plans include obtaining FDA certification and entering the US market,” it added.

The AI tool received European medical device certification in 2018 — although it’s worth noting that the European Union’s regulatory regime for medical devices and AI is continuing to evolve, with an update to the bloc’s Medical Devices Directive (now known as the EU Medical Device Regulation) coming into application earlier this year (May).

A new risk-based framework for applications of AI — aka the Artificial Intelligence Act — is also incoming and will likely expand compliance demands on AI health tech tools like Cardiomatics, introducing requirements such as demonstrating safety, reliability and a lack of bias in automated results.

Asked about the regulatory landscape it said: “When we launched in 2018 we were one of the first AI-based solutions approved as medical device in Europe. To stay in front of the pace we carefully observe the situation in Europe and the process of legislating a risk-based framework for regulating applications of AI. We also monitor draft regulations and requirements that may be introduced soon. In case of introducing new standards and requirements for artificial intelligence, we will immediately undertake their implementation in the company’s and product operations, as well as extending the documentation and algorithms validation with the necessary evidence for the reliability and safety of our product.”

However it also conceded that objectively measuring efficacy of ECG reading algorithms is a challenge.

“An objective assessment of the effectiveness of algorithms can be very challenging,” it told TechCrunch. “Most often it is performed on a narrow set of data from a specific group of patients, registered with only one device. We receive signals from various groups of patients, coming from different recorders. We are working on this method of assessing effectiveness. Our algorithms, which would allow them to reliably evaluate their performance regardless of various factors accompanying the study, including the recording device or the social group on which it would be tested.”

“When analysis is performed by a physician, ECG interpretation is a function of experience, rules and art. When a human interprets an ECG, they see a curve. It works on a visual layer. An algorithm sees a stream of numbers instead of a picture, so the task becomes a mathematical problem. But, ultimately, you cannot build effective algorithms without knowledge of the domain,” it added. “This knowledge and the experience of our medical team are a piece of art in Cardiomatics. We shouldn’t forget that algorithms are also trained on the data generated by cardiologists. There is a strong correlation between the experience of medical professionals and machine learning.”

Powered by WPeMatico

Coming off a $1.5 million seed round in June, bttn. announced Thursday that it secured another $5 million extension, led by FUSE, to the round to give it a $26.5 million post-money valuation.

The Seattle-based company was founded in March 2021 by JT Garwood and Jack Miller after seeing the challenges medical organizations had during the global pandemic to not only find supplies, but also get fair prices for them.

“We went into this building on the pain points customers had dealing with a system that is so archaic and outdated — most were still faxing in order forms and keeping closets full of supplies, but not knowing what was there,” Garwood, CEO, told TechCrunch.

Bttn. is going after the U.S. wholesale medical supply market, which is predicted to be valued at $243.3 billion by the end of 2021, according to IBISWorld. The company created a business-to-business e-commerce platform with a variety of high-quality medical supplies, saving customers an average of between 20% and 40%, while providing a better ordering and shipping experience, Garwood said.

It now boasts more than 300 customers, including individual practices and surgical centers, and multiple government contracts. It is also currently the preferred supplier for over 17 healthcare associations across the country, Garwood said. In addition to expanding into dental supplies, bttn. is also attracting customers like senior living facilities and home and hospice care.

Garwood intends to use the funds to expand bttn.’s technology, sales and operations teams, and increase its partnerships. The company is also adding new features like a portal to track shipments more easily, better order automation and improve the ability to control when supplies will get to them.

Bttn. is also analyzing more of the data coming in from its marketplace to recognize where the trends are coming from, including hospitalization rates, to share with customers. For example, if hospitals are overcrowded, supply shortages will follow, Garwood said.

“The medical supply industry was built on inequity, and we have a sense of duty to build a product that enables a better future for our customers,” he added. “We can proactively let customers know that spikes are expected, provide them with correct information and give that power back to the consumers and healthcare providers in ways they never had before.”

Whereas bttn.’s first seed round was “about pouring gas on the fire,” partnering with FUSE this time around was an easy decision for Garwood, who said the firm is bringing new assets to the table.

Brendan Wales, general partner at FUSE, said via email that his firm backs promising entrepreneurs building businesses in the Pacific Northwest and discovered bttn. before they announced any funding.

He said there is massive consumerization of healthcare, most evident on the patient side for years, but now becoming so on the provider side. Medical office employees are looking for the same type of customer experience they get from online businesses they frequently shop at, and bttn. “has a relentless drive to provide the same type of experiences and interactions to health providers.”

“We fell in love with the idea of providing a transparent and delightful customer experience to health providers, something that has been sorely lacking,” Wales added. “That, tied in with a young and ambitious team, made it so that our entire partnership worked tirelessly to partner with them.”

Powered by WPeMatico

When you enter the health tech industry as a new startup, an advisory board is a crucial foundational step. A board can guide you through industry-specific nuances, help you make important decisions and prove your legitimacy to investors looking for a strong industry background.

An advisory board will be able to give you strategic insights about both your company and the wider healthcare and technology industries.

In my experience of raising capital, the unpredictable financial situation at the beginning of the pandemic meant we nearly lost our $2 million round, but came through with a committed $250,000, which we used to bring in about $500,000 in revenue.

Something that helped this process was building our advisory board and starting small — we didn’t go for all of healthcare but instead focused on two healthcare verticals. This allowed us to prove our concept, build case studies and win contracts with specific teams in our customers’ companies.

It pays off to stay focused and prove your worth so that your advisory board members can champion you in niche markets, with the potential to expand in the future. For this reason, it’s important to identify the main intention behind your board, and exactly who should be on it.

Three to five people is an ideal starting point for an advisory board, depending on the size and stage of your company. In health tech, you need more than just the healthcare perspective — you also need the insight of those who have already grown technology companies, perhaps outside of the industry. Our company’s board is an even split of two healthcare and two technology advisers, and, ideally, you want to find a fifth who is well versed in both industries.

It pays off to stay focused and prove your worth so that your advisory board members can champion you in niche markets, with the potential to expand in the future.

An M.D., a Ph.D. from a respected institution or a thought leader in your relevant field of healthcare is the most important asset to an advisory board. These are the highly decorated physicians who have strong connections and act as a reference for their peers.

They provide instant credibility for your company, help you get into the minds of both patients and healthcare providers, and can outline how various health systems work.

Powered by WPeMatico

In “Macbeth,” Shakespeare described sleep as the “chief nourisher in life’s feast.” But like his titular character, many adults aren’t sleeping well. Revery wants to help with an app that combines cognitive behavioral therapy (CBT) for insomnia with mobile gaming concepts.

Founded in March 2021, Revery is currently in beta stealth mode and plans to launch its app in the United States later this year. The company announced today it has raised $2 million, led by Sequoia Capital India’s Surge program. Participants included GGV Capital, Pascal Capital, zVentures (Razer’s corporate venture arm) and angel investors like MyFitnessPal co-founder Albert Lee; gaming entrepreneur Juha Paananen; CRED founder Kunal Shah; Mobile Premier League founder Sai Srinivas; Carolin Krenzer; and Josh Lee.

Lee, a mutual friend, first introduced Revery’s founders, Tammie Siew and Khoa Tran, to one another. Before launching the startup, Siew worked at Sequoia Capital India, Boston Consulting Group and CRED, while Tran was a former product manager at Google.

Revery plans to focus on other mental health issues in the future, but it’s starting with sleep because “it has such a strong correlation with mental health and we’re leveraging protocols, cognitive behavioral therapy for insomnia, that’s robust and have been tried and tested for 30 years,” Siew told TechCrunch. “That is the first indication, but the goal is to build multiple games for other wellness indications as well.”

A study by research firm Infinium found that about 30% to 45% of adults in the world experience insomnia, a problem exacerbated by the COVID-19 pandemic. Chronic lack of sleep is linked to a host of health issues, including high blood pressure, strokes, depression and lowered immunity.

For Revery’s team, which also includes former Zynga and King lead game designer Kriti Sawa and software engineer Stephanie Wong, their focus on sleep is personal.

Revery’s team on a Zoom call

“Everyone on our team has a deeply personal connection to the mission, because everyone on our team has experienced, or had a family member or friends go through challenges in mental health,” said Siew. “They’ve seen how late intervention creates consequences that could have been avoided if they had gotten help earlier.”

When Tran was 15, he was diagnosed with hypertension and several other health conditions that needed medication. It wasn’t until he was 26 that Tran found out that sleep apnea was at the root of his medical issues. After getting surgery, Tran’s blood pressure became normal and many of his other conditions also improved.

“When I finally got treatment for my sleep disorder, only then did I realize the impact of sleep on mental health,” Tran said. “For me, I was really lucky that a doctor caught my sleep disorder and super lucky to have the time and resources to get treatment. For many people, it’s incredibly inaccessible.”

Revery’s medical advisory team includes the doctor who performed Tran’s surgery, Stanford Sleep Surgery Fellowship director Dr. Stanley Liu; Stanford professor and behavioral sleep medicine expert Dr. Fiona Barwick; and Dr. Ryan Kelly, a clinical psychologist who researches how video games can be used in therapy.

When people think of sleeping apps, ones that focus on meditation (Calm and Headspace, for example) or soothing noises usually come to mind. The Revery team isn’t sharing a lot of details about its app before launch, but says it draws from casual mobile games, which are designed to get people to return for short play sessions over a long period of time. The goal is to use gamification to make CBT practices interactive and fun, so it becomes part of users’ daily routines.

“That’s the same kind of gameplay that Zynga and King have used, which is why Kriti’s experience is super helpful,” said Siew. Casual games revolve around rewarding people for small actions, and for the Revery app, that means positive reinforcement for habits that contribute to better sleep. For example, it will reward people for putting down their phones.

“I think a lot of people have the misconception that solving sleep is only at the time you fall asleep. They don’t realize that sleep is impacted by what you do throughout the day,” Siew said. “A big part is also what are your thoughts, behavior and the other things that you do, so in order to effectively and sustainably improve sleep, we also have to change your thoughts and behaviors outside of the time you’re trying to fall asleep.”

In a statement, GGV Capital managing director Jenny Lee said, “We are excited about the growing mental wellness market, and believe that Revery’s unique mobile game-based approach has the opportunity to create immense impact. We are happy to back such a mission-driven team in this space.”

Powered by WPeMatico

Pet pharmacy Mixlab has developed a digital platform enabling veterinarians to prescribe medications and have them delivered — sometimes on the same day — to pet parents.

The New York-based company raised a $20 million Series A in a round of funding led by Sonoma Brands and including Global Founders Capital, Monogram Capital, Lakehouse Ventures and Brand Foundry. The new investment gives Mixlab total funding of $30 million, said Fred Dijols, co-founder and CEO of Mixlab.

Dijols and Stella Kim, chief experience officer, co-founded Mixlab in 2017 to provide a better pharmacy experience, with the veterinarian at the center.

Dijols’ background is in medical devices as well as healthcare investment banking, where he became interested in the pharmacy industry, following TruePill and PillPack, which he told TechCrunch were “creating a modern pharmacy model.”

As more pharmacy experiences revolved around at-home delivery, he found the veterinary side of pharmacy was not keeping up. He met Kim, a user experience expert, whose family owns a pharmacy, and wanted to bring technology into the industry.

“The pharmacy industry is changing a lot, and technology allows us to personalize the care and experience for the veterinarian, pet parent and the pet,” Kim said. “Customer service is important in healthcare as is dignity and empathy. We kept that in mind when starting Mixlab. Many companies use technology to remove the human element, but we use it to elevate it.”

Mixlab’s technology includes a digital service for veterinarians to streamline their daily medication workflow and gives them back time to spend with patient care. The platform manages the home delivery of medications across branded, generic and over-the-counter medications, as well as reduces a clinic’s on-site pharmacy inventories. Veterinarians can write prescriptions in seconds and track medication progress and therapy compliance.

The company also operates its own compound pharmacy where it specializes in making medications on-demand that are flavored and dosed.

On the pet parent side, they no longer have to wait up to a week for medications nor have to drive over to the clinic to pick them up. Medications come in a personalized care package that includes a note from the pharmacist, clear and easy-to-read instructions and a new toy.

Over the past year, adoptions of pets spiked as more people were at home, also leading to an increase in vet visits. This also caused the global pet care industry to boom, and it is now projected to reach $343 billion by 2030, when it had been valued at $208 billion in 2020.

Pet parents are also spending more on their pets, and a Morgan Stanley report showed that they see pets as part of their family, and as a result, 37% of people said they would take on debt to pay for a pet’s medical expenses, while 29% would put a pet’s needs before their own.

To meet the increased demand in veterinary care, the company will use the new funding to improve its technology and expand into more locations where it can provide same-day delivery. Currently it is shipping to 47 states and Dijols expects to be completely national by the end of the year. He also expects to hire more people on both the sales team and in executive leadership positions.

The company is already operating in New York and Los Angeles and growing 3x year over year, though Dijols admits operating during the pandemic was a bit challenging due to “a massive surge of orders” that came in as veterinarians had to shut down their offices.

As part of the investment, Keith Levy, operating partner at Sonoma Brands and former president of pet food manufacturer Royal Canin USA, will join Mixlab’s board of directors. Sonoma Brands is focused on growth sectors of the consumer economy, and pets was one of the areas that investors were interested in.

Over time, Sonoma found that within the veterinary community, there was space for a lot of players. However, veterinarians want to home in on one company they trust, and Mixlab fit that description for many because they were getting medication out faster, Levy said.

“What Mixlab is doing isn’t completely unique, but they are doing it better,” he added. “When we looked at their customer service metrics, we saw they had a good reputation and were relentlessly focused on providing a better experience.”

Powered by WPeMatico

Catch is working to make sure that every gig worker has the health and retirement benefits they need.

The company, which is in the midst of moving its headquarters to New York, sells health insurance, retirement savings plans and tax withholding directly to freelancers, contractors or anyone uncovered.

It is now armed with a fresh round of $12 million in Series A funding, led by Crosslink, with participation from earlier investors Khosla Ventures, NYCA Partners, Kindred Ventures and Urban Innovation Fund, to support more distribution partnerships and its relocation from Boston.

Co-founders Kristen Anderson and Andrew Ambrosino started Catch in 2019 and raised $6.1 million previously, giving it a total of $18.1 million in funding.

It took the Catch team of 15 nearly two years to get approvals to sell its platform in 38 states on the federal marketplace. Anderson boasts that only eight companies have been able to do this, and three of them — Catch included — are approved to sell benefits to consumers.

“More companies are not offering healthcare, while more people are joining the creator and gig economies, which means more people are not following an employer-led model,” Anderson told TechCrunch.

The age of an average Catch customer is 32, and in addition to current offerings, they were asking the company to help them set up income sources, like setting aside money for taxes, retirement and medical leave without having to actively save.

When the global pandemic hit, many of Catch’s customers saw their income collapse 40% overall across industries, as workers like hairstylists and cooks had income go down to zero in some cases.

It was then that Anderson and Ambrosino began looking at partnership distribution and developed a network of platforms, business facilitation tools, gig marketplaces and payroll companies that were interested in offering Catch. The company intends to use some of the funding to increase its headcount to service those partnerships and go after more, Anderson said.

Catch is one startup providing insurance products, and many of its competitors do a single offering and do it well, like Starship does with health savings accounts, Anderson said. Catch is taking a different approach by offering a platform experience, but going deep on the process, she added. She likens it to Gusto, which provides cloud-based payroll, benefits and human resource management for businesses, in that Catch is an end-to-end experience, but with a focus on an individual person.

Over the past year, the company’s user base tripled, driven by people taking on second jobs and through a partnership with DoorDash. Platform users are also holding onto five times their usual balances, a result of setting more goals and needing to save more, Anderson said. Retirement investments and health insurance have grown similarly.

Going forward, Anderson is already thinking about a Series B, but that won’t come for another couple of years, she said. The company is looking into its own HSA product as well as disability insurance and other products to further differentiate it from other startups, for example, Spot, Super.mx and Even, all of which raised venture capital this month to provide benefits.

Catch would also like to serve a broader audience than just those on the federal marketplace. The co-founders are working on how to do this — Anderson mentioned there are some “nefarious companies out there” offering medical benefits at rates that can seem too good to be true, but when the customer reads the fine print, they discover that certain medical conditions are not covered.

“We are looking at how to put the right thing in there because it does get confusing,” Anderson added. “Young people have cheaper options, which means they need to make sure they know what they are getting.”

Powered by WPeMatico

Now that you have that COVID dog, Embark Veterinary wants to help him or her be in your life for a long time by offering DNA testing with the goal of curbing preventable diseases and increasing the lifespan of dogs by three years within the next decade.

The Boston-based dog genetics company raised $75 million in Series B funding in what the company is calling “the biggest Series B for a pet startup to date.” SoftBank Vision Fund 2 was the lead investor and was joined by existing investors F-Prime Capital, SV Angel, Slow Ventures, Freestyle Capital and Third Kind Venture Capital.

The new round boosts Embark’s total funding to $94.3 million since the company was founded in 2015, according to Crunchbase data. It also gives it a post-money valuation of $700 million, Embark founder and CEO Ryan Boyko told TechCrunch.

Boyko has been a dog lover all his life, and also interested in biology and evolution. Dogs, in particular, are fascinating to him because of their variety: they can be bred to be two pounds or 200 pounds, and come in all shapes and sizes. His interest led him to study dogs in order to understand their evolution.

“I began to think about health problems, and honestly, dogs are a better system for using genetics to better their health than humans,” Boyko said. “You can breed them, so genetics has as much power to cause health problems as it can improve quality and life.”

Embark’s dog DNA test retails for $199 and enables dog owners, breeders and veterinarians to personalize care plans based on a dog’s unique genetic profile. It can test for over 350 breeds and 200 genetic health risks, as well as physical traits. Similar to a 23andMe test, test users can learn characteristics about breed, health and ancestry.

For example, the test could show that a healthy dog may have a gene that predisposes them to slipped discs. If the dog has that, then weight management would be an important factor in their care regime, as would not allowing them to jump off the couch. Another common genetic risk is HUU, or Hyperuricosuria, which is elevated levels of uric acid in urine that could lead to bladder stones due to the way dogs process minerals. By changing the dog’s diet, it could reduce the risk for developing the stones, which are painful and expensive to treat, Boyko said.

The test’s technology revolves around proprietary genotyping technology that analyzes more than 200,000 genetic markers, currently two times more information than any other dog DNA test on the market, Boyko said. This gives Embark the world’s largest database of canine health and biological information, enabling the company to provide insights into certain conditions and make new discoveries about health risks, traits and breeds.

Embark aims to become the standard of care for dog owners and vets. It grew 235% between 2019 and 2020 and saw five times the sales over the past two years. To support that growth, the company intends to use the new funding to bring on key hires and expand its database. Boyko anticipates adding more than 100 employees between 2021 and 2022.

Boyko said the opportunity in the pet startup space is huge. Indeed, U.S. spending on pets reached nearly $100 billion in 2020, up from $95.7 billion in 2019, according to the American Pet Products Association.

At the same time, venture capital interest in U.S. pet-focused companies, from nutrition to travel to healthcare, grew 29.5% from 2019 and 2020, according to Crunchbase data. In addition to Embark’s funding, 2021 was good to other pet startups as well, including pet insurance company Wagmo, raising $12.5 million, connected pet collar company Fi received $30 million and Rover, which announced plans to go public via SPAC.

Lydia Jett, partner at SoftBank Investment Advisers, told TechCrunch that this was her first pet-based investment, and what Embark is doing brings advances to a category right now where people care about their pets enough that they want to do something that will expand their value of life.

Jett said the management team being dedicated to DNA-based analytics is the future, and Embark is starting this big curve when it comes to pets and the convergence of real emotional ties to pets and the ability to improve their lives.

“This company is a driver of change to happen,” she added. “We are the largest consumer investor in the world, and Embark is very much aligned with what we are seeing across our portfolio that consumers are revisiting priorities and choices. That is a major trend, but still early in the cycle of personalization for their pets.”

Powered by WPeMatico

The global pandemic highlighted inefficiencies and inconsistencies in healthcare systems around the world. Even co-founders Mayank Banerjee, Matilde Giglio and Alessandro Ialongo say nowhere is this more evident than in India, especially after the COVID death toll reached 4 million this week.

The Bangalore-based company received a fresh cash infusion of $5 million in seed funding in a round led by Khosla Ventures, with participation from Founders Fund, Lachy Groom and a group of individuals including Palo Alto Networks CEO Nikesh Arora, CRED CEO Kunal Shah, Zerodha founder Nithin Kamath and DST Global partner Tom Stafford.

Even, a healthcare membership company, aims to cover what most insurance companies in the country don’t, including making going to a primary care doctor as easy and accessible as it is in other countries.

Banerjee grew up in India and said the country is similar to the United States in that it has government-run and private hospitals. Where the two differ is that private health insurance is a relatively new concept for India, he told TechCrunch. He estimates that less than 5% of people have it, and even though people are paying for the insurance, it mainly covers accidents and emergencies.

This means that routine primary care consultations, testings and scans outside of that are not covered. And, the policies are so confusing that many people don’t realize they are not covered until it is too late. That has led to people asking doctors to admit them into the hospital so their bills will be covered, Ialongo added.

Banerjee and Giglio were running another startup together when they began to see how complicated health insurance policies were. About 50 million Indians fall below the poverty line each year, and many become unable to pay their healthcare bills, Banerjee said.

They began researching the insurance industry and talking with hospital executives about claims. They found that one of the biggest issues was incentive misalignment — hospitals overcharged and overtreated patients. Instead, Even is taking a similar approach to Kaiser Permanente in that the company will act as a service provider, and therefore, can drive down the cost of care.

Even became operational in February and launched in June. It is gearing up to launch in the fourth quarter of this year with more than 5,000 people on the waitlist so far. Its health membership product will cost around $200 per year for a person aged 18 to 35 and covers everything: unlimited consultations with primary care doctors, diagnostics and scans. The membership will also follow as the person ages, Ialongo said.

The founders intend to use the new funding to build out their operational team, product and integration with hospitals. They are already working with 100 hospitals and secured a partnership with Narayana Hospital to deliver more than 2,000 COVID vaccinations so far, and more in a second round.

“It is going to take a while to scale,” Banerjee said. “For us, in theory, as we get better pricing, we will end up being cheaper than others. We have goals to cover the people the government cannot and find ways to reduce the statistics.”

Powered by WPeMatico

More than half of the U.S. population has stayed away from considering life insurance because they believe it’s probably too expensive, and the most common way to buy it today is in person. A startup that’s built a platform that aims to break down those conventions and democratize the process by making life insurance (and the benefits of it) more accessible is today announcing significant funding to fuel its rapidly growing business.

Ethos, which uses more than 300,000 data points online to determine a person’s eligibility for life insurance policies, which are offered as either term or whole life packages starting at $8/month, has picked up $100 million from a single investor, SoftBank Vision Fund 2. Peter Colis, Ethos’s CEO and co-founder, said that the funding brings the startup’s valuation to over $2.7 billion.

This is a quick jump for the company: It was only two months ago that Ethos picked up a $200 million equity round at a valuation of just over $2 billion.

It has now raised $400 million to date and has amassed a very illustrious group of backers. In addition to SoftBank they include General Catalyst, Sequoia Capital, Accel, GV, Jay-Z’s Roc Nation, Glade Brook Capital Partners, Will Smith and Robert Downey Jr.

This latest injection of funding — which will be used to hire more people and continue to expand its product set into adjacent areas of insurance like critical illness coverage — was unsolicited, Colis said, but comes on the heels of very rapid growth.

Ethos — which is sold currently only in the U.S. across 49 states — has seen both revenues and user numbers grow by over 500% compared to a year ago, and it’s on track to issue some $20 billion in life insurance coverage this year. And it is approaching $100 million in annualized growth profit. Ethos itself is not yet profitable, Colis said.

There are a couple of trends going on that speak to a wide opportunity for Ethos at the moment.

The first of these is the current market climate: Globally we are still battling the COVID-19 global health pandemic, and one impact of that — in particular given how COVID-19 has not spared any age group or demographic — has been more awareness of our mortality. That inevitably leads at least some part of the population to considering something like life insurance coverage that might not have thought about it previously.

However, Colis is a little skeptical on the lasting impact of that particular trend. “We saw an initial surge of demand in the COVID period, but then it regressed back to normal,” he said in an interview. Those who were more inclined to think about life insurance around COVID-19 might have come around to considering it regardless: It was being driven, he said, by those with pre-existing health conditions going into the pandemic.

That, interestingly, brings up the second trend, which goes beyond our present circumstances, and Colis believes will have the more lasting impact.

While there have been a number of startups, and even incumbent providers, looking to rethink other areas of insurance such as car, health and property coverage, life insurance has been relatively untouched, especially in some markets like the U.S. Traditionally, someone taking out life insurance goes through a long vetting process, which is not all carried out online and can involve medical examinations and more, and yes, it can be expensive: The stereotype you might best know is that only wealthier people take out life insurance policies.

Much like companies in fintech that have rethought how loan applications (and payback terms) can be rethought and evaluated afresh using big data — pulling in a new range of information to form a picture of the applicant and the likelihood of default or not — Ethos is among the companies that is applying that same concept to a different problem. The end result is a much faster turnaround for applications, a considerably cheaper and more flexible offer (term life insurance lasts only as long as a person pays for it), and generally a lot more accessibility for everyone potentially interested. That pool of data is growing all the time.

“Every month, we get more intelligent,” said Colis.

There is also the matter of what Ethos is actually selling. The company itself is not an insurance provider but an “insuretech” — similar to how neobanks use APIs to integrate banking services that have been built by others, which they then wrap with their own customer service, personalization and more — Ethos integrates with third-party insurance underwriters, providing customer service, more efficient onboarding (no in-person medical exams for example) and personalization (both in packages and pricing) around them. Given how staid and hard it is to get more traditional policies, it’s essentially meant completely open water for Ethos in terms of finding and securing new customers.

Ethos’s rise comes at a time when we are seeing other startups approaching and rethinking life insurance also in the U.S. and further afield. Last week, YuLife in the U.K. raised a big round to further build out its own take on life insurance, which is to sell policies that are linked to an individual’s own health and wellness practices — the idea being that this will make you happier and give more reason to pay for a policy that otherwise feels like some dormant investment; but also that it could help you live longer (Sproutt is another also looking at how to emphasize the “life” aspect of life insurance). Others like DeadHappy and BIMA are, like Ethos, rethinking accessibility of life insurance for a wider set of demographics.

There are some signs that Ethos is catching on with its mission to expand that pool, not just grow business among the kind of users who might have already been considering and would have taken out life insurance policies. The startup said that more than 40% of its new policy holders in the first half of 2021 had incomes of $60,000 or less, and nearly 40% of new policy holders were under the age of 40. The professions of those customers also speak to that democratization: The top five occupations, it said, were homemaker, insurance agent, business owner, teacher and registered nurse.

That traction is likely one reason why SoftBank came knocking.

“Ethos is leveraging data and its vertically integrated tech stack to fundamentally transform life insurance in the U.S.,” said Munish Varma, managing partner at SoftBank Investment Advisers, in a statement. “Through a fast and user-friendly online application process, the company can accurately underwrite and insure a broad segment of customers quickly. We are excited to partner with Peter Colis and the exceptional team at Ethos.”

Powered by WPeMatico