health insurance

Auto Added by WPeMatico

Auto Added by WPeMatico

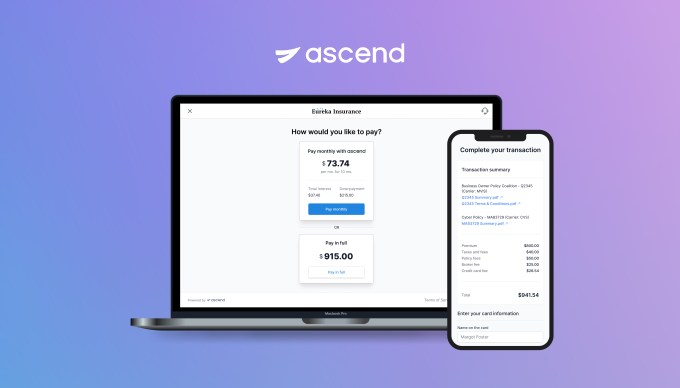

Ascend on Wednesday announced a $5.5 million seed round to further its insurance payments platform that combines financing, collections and payables.

First Round Capital led the round and was joined by Susa Ventures, FirstMark Capital, Box Group and a group of angel investors, including Coalition CEO Joshua Motta, Newfront Insurance executives Spike Lipkin and Gordon Wintrob, Vouch Insurance CEO Sam Hodges, Layr Insurance CEO Phillip Naples, Anzen Insurance CEO Max Bruner, Counterpart Insurance CEO Tanner Hackett, former Bunker Insurance CEO Chad Nitschke, SageSure executive Paul VanderMarck, Instacart co-founders Max Mullen and Brandon Leonardo and Houseparty co-founder Ben Rubin.

This is the first funding for the company that is live in 20 states. It developed payments APIs to automate end-to-end insurance payments and to offer a buy now, pay later financing option for distribution of commissions and carrier payables, something co-founder and co-CEO Andrew Wynn, said was rather unique to commercial insurance.

Wynn started the company in January 2021 with his co-founder Praveen Chekuri after working together at Instacart. They originally started Sheltr, which connected customers with trained maintenance professionals and was acquired by Hippo in 2019. While working with insurance companies they recognized how fast the insurance industry was modernizing, yet insurance sellers still struggled with customer experiences due to outdated payments processes. They started Ascend to solve that payments pain point.

The insurance industry is largely still operating on pen-and-paper — some 600 million paper checks are processed each year, Wynn said. He referred to insurance as a “spaghetti web of money movement” where payments can take up to 100 days to get to the insurance carrier from the customer as it makes its way through intermediaries. In addition, one of the only ways insurance companies can make a profit is by taking those hundreds of millions of dollars in payments and investing it.

Home and auto insurance can be broken up into payments, but the commercial side is not as customer friendly, Wynn said. Insurance is often paid in one lump sum annually, though, paying tens of thousands of dollars in one payment is not something every business customer can manage. Ascend is offering point-of-sale financing to enable insurance brokers to break up those commercial payments into monthly installments.

“Insurance carriers continue to focus on annual payments because they don’t have a choice,” he added. “They want all of their money up front so they can invest it. Our platform not only reduces the friction with payments by enabling customers to pay how they want to pay, but also helps carriers sell more insurance.”

Ascend app

Startups like Ascend aiming to disrupt the insurance industry are also attracting venture capital, with recent examples including Vouch and Marshmallow, which raised close to $100 million, while Insurify raised $100 million.

Wynn sees other companies doing verticalized payment software for other industries, like healthcare insurance, which he says is a “good sign for where the market is going.” This is where Wynn believes Ascend is competing, though some incumbents are offering premium financing, but not in the digital way Ascend is.

He intends to deploy the new funds into product development, go-to-market initiatives and new hires for its locations in New York and Palo Alto. He said the raise attracted a group of angel investors in the industry, who were looking for a product like this to help them sell more insurance versus building it from scratch.

Having only been around eight months, it is a bit early for Ascend to have some growth to discuss, but Wynn said the company signed its first customer in July and six more in the past month. The customers are big digital insurance brokerages and represent, together, $2.5 billion in premiums. He also expects to get licensed to operate as a full payment in processors in all states so the company can be in all 50 states by the end of the year.

The ultimate goal of the company is not to replace brokers, but to offer them the technology to be more efficient with their operations, Wynn said.

“Brokers are here to stay,” he added. “What will happen is that brokers who are tech-enabled will be able to serve customers nationally and run their business, collect payments, finance premiums and reduce backend operation friction.”

Bill Trenchard, partner at First Round Capital, met Wynn while he was still with Sheltr. He believes insurtech and fintech are following a similar story arc where disruptive companies are going to market with lower friction and better products and, being digital-first, are able to meet customers where they are.

By moving digital payments over to insurance, Ascend and others will lead the market, which is so big that there will be many opportunities for companies to be successful. The global commercial insurance market was valued at $692.33 billion in 2020, and expected to top $1 trillion by 2028.

Like other firms, First Round looks for team, product and market when it evaluates a potential investment and Trenchard said Ascend checked off those boxes. Not only did he like how quickly the team was moving to create momentum around themselves in terms of securing early pilots with customers, but also getting well known digital-first companies on board.

“The magic is in how to automate the underwriting, how to create a data moat and be a first mover — if you can do all three, that is great,” Trenchard said. “Instant approvals and using data to do a better job than others is a key advantage and is going to change how insurance is bought and sold.”

Powered by WPeMatico

Catch is working to make sure that every gig worker has the health and retirement benefits they need.

The company, which is in the midst of moving its headquarters to New York, sells health insurance, retirement savings plans and tax withholding directly to freelancers, contractors or anyone uncovered.

It is now armed with a fresh round of $12 million in Series A funding, led by Crosslink, with participation from earlier investors Khosla Ventures, NYCA Partners, Kindred Ventures and Urban Innovation Fund, to support more distribution partnerships and its relocation from Boston.

Co-founders Kristen Anderson and Andrew Ambrosino started Catch in 2019 and raised $6.1 million previously, giving it a total of $18.1 million in funding.

It took the Catch team of 15 nearly two years to get approvals to sell its platform in 38 states on the federal marketplace. Anderson boasts that only eight companies have been able to do this, and three of them — Catch included — are approved to sell benefits to consumers.

“More companies are not offering healthcare, while more people are joining the creator and gig economies, which means more people are not following an employer-led model,” Anderson told TechCrunch.

The age of an average Catch customer is 32, and in addition to current offerings, they were asking the company to help them set up income sources, like setting aside money for taxes, retirement and medical leave without having to actively save.

When the global pandemic hit, many of Catch’s customers saw their income collapse 40% overall across industries, as workers like hairstylists and cooks had income go down to zero in some cases.

It was then that Anderson and Ambrosino began looking at partnership distribution and developed a network of platforms, business facilitation tools, gig marketplaces and payroll companies that were interested in offering Catch. The company intends to use some of the funding to increase its headcount to service those partnerships and go after more, Anderson said.

Catch is one startup providing insurance products, and many of its competitors do a single offering and do it well, like Starship does with health savings accounts, Anderson said. Catch is taking a different approach by offering a platform experience, but going deep on the process, she added. She likens it to Gusto, which provides cloud-based payroll, benefits and human resource management for businesses, in that Catch is an end-to-end experience, but with a focus on an individual person.

Over the past year, the company’s user base tripled, driven by people taking on second jobs and through a partnership with DoorDash. Platform users are also holding onto five times their usual balances, a result of setting more goals and needing to save more, Anderson said. Retirement investments and health insurance have grown similarly.

Going forward, Anderson is already thinking about a Series B, but that won’t come for another couple of years, she said. The company is looking into its own HSA product as well as disability insurance and other products to further differentiate it from other startups, for example, Spot, Super.mx and Even, all of which raised venture capital this month to provide benefits.

Catch would also like to serve a broader audience than just those on the federal marketplace. The co-founders are working on how to do this — Anderson mentioned there are some “nefarious companies out there” offering medical benefits at rates that can seem too good to be true, but when the customer reads the fine print, they discover that certain medical conditions are not covered.

“We are looking at how to put the right thing in there because it does get confusing,” Anderson added. “Young people have cheaper options, which means they need to make sure they know what they are getting.”

Powered by WPeMatico

The global pandemic highlighted inefficiencies and inconsistencies in healthcare systems around the world. Even co-founders Mayank Banerjee, Matilde Giglio and Alessandro Ialongo say nowhere is this more evident than in India, especially after the COVID death toll reached 4 million this week.

The Bangalore-based company received a fresh cash infusion of $5 million in seed funding in a round led by Khosla Ventures, with participation from Founders Fund, Lachy Groom and a group of individuals including Palo Alto Networks CEO Nikesh Arora, CRED CEO Kunal Shah, Zerodha founder Nithin Kamath and DST Global partner Tom Stafford.

Even, a healthcare membership company, aims to cover what most insurance companies in the country don’t, including making going to a primary care doctor as easy and accessible as it is in other countries.

Banerjee grew up in India and said the country is similar to the United States in that it has government-run and private hospitals. Where the two differ is that private health insurance is a relatively new concept for India, he told TechCrunch. He estimates that less than 5% of people have it, and even though people are paying for the insurance, it mainly covers accidents and emergencies.

This means that routine primary care consultations, testings and scans outside of that are not covered. And, the policies are so confusing that many people don’t realize they are not covered until it is too late. That has led to people asking doctors to admit them into the hospital so their bills will be covered, Ialongo added.

Banerjee and Giglio were running another startup together when they began to see how complicated health insurance policies were. About 50 million Indians fall below the poverty line each year, and many become unable to pay their healthcare bills, Banerjee said.

They began researching the insurance industry and talking with hospital executives about claims. They found that one of the biggest issues was incentive misalignment — hospitals overcharged and overtreated patients. Instead, Even is taking a similar approach to Kaiser Permanente in that the company will act as a service provider, and therefore, can drive down the cost of care.

Even became operational in February and launched in June. It is gearing up to launch in the fourth quarter of this year with more than 5,000 people on the waitlist so far. Its health membership product will cost around $200 per year for a person aged 18 to 35 and covers everything: unlimited consultations with primary care doctors, diagnostics and scans. The membership will also follow as the person ages, Ialongo said.

The founders intend to use the new funding to build out their operational team, product and integration with hospitals. They are already working with 100 hospitals and secured a partnership with Narayana Hospital to deliver more than 2,000 COVID vaccinations so far, and more in a second round.

“It is going to take a while to scale,” Banerjee said. “For us, in theory, as we get better pricing, we will end up being cheaper than others. We have goals to cover the people the government cannot and find ways to reduce the statistics.”

Powered by WPeMatico

Super.mx, an insurtech startup based in Mexico City, has raised $7.2 million in a Series A round led by ALLVP.

Co-founded in 2019 by a trio of former insurance industry executives, Super.mx’s self-proclaimed mission is to design insurance for “the emerging Latin American middle class,” according to CEO Sebastian Villarreal.

“That means insurance that is easy to buy – it can be bought on a cell phone in minutes – and that pays quickly with no adjusters,” he said. The company has built its offering with proprietary models that are used both on the underwriting side to predict risk and on the claims side to make payments automatically.

Goodwater Capital, Kairos Angels and Bridge Partners also participated in the Series A round in addition to angels such as Joe Schmidt IV, vice president of business development at insurtech Ethos and former investor at Accel and Kyle Nakatsuji, founder and CEO of auto insurance startup Clearcover (and also a former VC). Better Tomorrow Ventures led Super.mx’s $2.4 million seed round, which also saw capital from 500 Startups Mexico, Village Global, Anthemis and Broadhaven Ventures, among others.

Unlike most insurtech startups in Latin America, Villarreal emphasizes that Super.mx is neither an aggregator nor a carrier. Instead, it’s an MGA, or managing general agent.

“This lets us have a ‘best of both worlds’ approach,” Villarreal said. “We handle the entire user experience just like a direct to consumer carrier, but with the breadth of product choice offered by an aggregator.”

That product choice includes property, natural disasters and life insurance. The company soon plans to expand to also offer health insurance.

The founding team brings a variety of insurance experience to the table. Villarreal previously co-founded Chicago-based Kin Insurance (which raised over $150 million in funding from the likes of Flourish Ventures, Commerce Ventures and QED Investors). He was also once head of auto product at Avant, a growth-stage company funded by General Atlantic and Tiger Global, among others.

With over two decades of insurance industry experience, Dario Luna once served as Mexico’s insurance regulator and helped develop Mexico’s disaster risk management strategy. Marco Ahedo has designed parametric insurance products for 19 Caribbean countries. He was also once a solvency expert for life and health insurance lines at MetLife, and has developed financial models for several P&C carriers.

Villarreal lived in the U.S. for a while before deciding to move back to Mexico, which he recognized was home to an “underinsurance problem.”

“That’s actually a very acute problem,” he said. “People in Latin America buy a lot less insurance than they do in the U.S., and people in Mexico, in particular, buy a lot less insurance than they do in other Latin countries.”

Some have blamed the lack of insurance coverage on the country’s culture but Super.mx operates under the belief that this notion is “total BS.”

“It’s not a cultural problem,” Villarreal said. “The problem is that the insurance products that exist in the market just suck. They’re super expensive. They’re really hard to buy, and they pay very little.”

Image Credits: Super.mx

So far, Super.mx has sold “thousands of policies” but is more focused now on increasing the number of products that it’s selling. The company started out by selling earthquake insurance before adding COVID insurance, and more recently, in April, it launched life insurance. Next, it’s going to offer property, renter’s and health insurance.

“It’s really a different strategy than what you would find in the U.S.,” Villarreal said. “In the U.S, when you look at insurtechs, it’s like everyone just does one thing, but here, it’s very different because when someone says ‘I want insurance,’ really what they’re saying is ‘Hey, something happened that makes me nervous that didn’t make me nervous before.’”

That something could be a new child, for example, that prompts a need for life insurance.

“What we’re trying to do is like Lemonade, Roots and Hippo or Kin all rolled into one,” he added. It’s a big, big play.”

Digital adoption in Mexico, and Latin America in general, has increased exponentially in recent years. The bigger hurdle for Super.mx, according to Villarreal, has less to do with technology and more to do with Mexicans getting over what he describes a “deep mistrust” based on bad experiences in the past.

“People are really distrustful and that’s a huge hurdle, but once you show them that you actually are different,” Villarreal told TechCrunch, “that you actually do things in a different way, you get this incredible emotional response.”

Eventually, Super.mx plans to outside of Mexico to other countries in Latin America.

ALLVP’s Federico Antoni said his Mexico City-based firm had been looking for a team building in this space “for years” before investing in Super.mx. The venture firm was impressed with the company’s technical knowledge and industry expertise. It was also drawn to their multi-product approach and “capacity to ship highly complex products to the market quickly” — both of which he believes are “unique” in the region.

Citing statistics from MAPFRE Economics, Antoni pointed out that globally, the insurance market has been growing over the last 10 years. During that time, Latin America expanded faster on average (4.4% vs. 2.4% worldwide), albeit with more volatility. Life insurance has been driving this growth, at 6.1%, over the period.

“Insurtech may be even bigger than fintech. Also, harder,” he told TechCrunch via email. “We knew the team to unlock the market potential would need to be highly competent and highly disruptive.”

Antoni said he is also convinced that Insurtech is the “next frontier” in financial inclusion in Latin America especially as digitization continues to increase.

“Providing risk coverage to individuals and businesses in the region, brings financial stability to families and unlocks economic potential for SMEs,” he said. “Moreover, the insurance incumbents have been unable to address a growing and underserved market.”

Powered by WPeMatico

New media poster child Substack announced today that they’ve added a small community-building consultancy team to its ranks, acquiring the Brooklyn-based startup People & Company.

The small firm has been working with clients to build up their community efforts, and its team will now be tasked with building up some of the newsletter company’s upstart efforts for writers in its network.

In a blog post, Substack co-founder Hamish McKenzie said that the company had previously used the People & Co. team to consult on their fellowship and mentorship programs and that members of the team would now be working on a variety of new efforts, from scaling programs to help writers with legal support and health insurance to community-guided projects like workshops and meetups to help crowdsource insights.

“These people are the best in the world at what they do, and now they’re not only working for Substack, but they’re also working for you,” McKenzie wrote.

Beyond Substack, previous partners with People & Company include Porsche AG, Nike and Surfrider.

Substack has been blazing ahead in recent months, adding new partners and raising cash as it aims to bring on more and more subscribers to its network. The firm shared back in late March that it had raised a $65 million round at a reported valuation around $650 million, according to earlier reporting by Axios.

Powered by WPeMatico

Late Friday, Oscar Health filed to go public, adding another company to today’s burgeoning IPO market. The New York-based health insurance unicorn has raised well north of $1 billion during its life, making its public debut a critical event for a host of investors.

Oscar Health lists a placeholder raise value of $100 million in its IPO filing, providing only directional guidance that its public offering will raise nine figures of capital.

Both Oscar and the high-profile SPAC for Clover Medical will prove to be a test for the venture capital industry’s faith in their ability to disrupt traditional healthcare companies.

The eight-year-old company, launched to capitalize on the sweeping health insurance reforms passed under the administration of President Barack Obama offers insurance products to individuals, families and small businesses. The company claimed 529,000 “members” as of January 31, 2021. Oscar Health touts that number as indicative of its success, with its growth since January 31 2017 “representing a compound annual growth rate, or CAGR, of 59%.”

However, while Oscar has shown a strong ability to raise private funds and scale the revenues of its neoinsurance business, like many insurance-focused startups that TechCrunch has covered in recent years, it’s a deeply unprofitable enterprise.

To understand Oscar Health we have to dig a bit into insurance terminology, but it’ll be as painless as we can manage. So, how did the company perform in 2020? Here are its 2020 metrics, and their 2019 comps:

Let’s walk through the numbers together. Oscar Health did a great job raising its total premium volume in 2020, or, in simpler terms, it sold way more insurance last year than it did in 2019. But it also ceded a lot more premium to reinsurance companies in 2020 than it did in 2019. So what? Ceding premiums is contra-revenue, but can serve to boost overall insurance margins.

As we can see in the net premium earned line, Oscar’s totals fell in 2020 compared to 2019 thanks to greatly expanded premium ceding. Indeed, its total revenue fell in 2020 compared to 2019 thanks to that effort. But the premium ceding seems to be working for the company, as its total insurance costs (our addition of its claims line item and “other insurance costs” category) fell from 2020 to 2019, despite selling far more insurance last year.

Sadly, all that work did not mean that the company’s total operating expenses fell. They did not, rising 16% or so in 2020 compared to 2019. And as we all know, more operating costs and fewer revenues mean that operating losses rose, and they did.

Oscar Health’s net losses track closely to its operating losses, so we spared you more data. Now to better understand the basic economics of Oscar Health’s insurance business, let’s get our hands dirty.

Powered by WPeMatico

French startup Alan is building health insurance products. And 100,000 people are now covered through Alan . I caught up with the company’s co-founder and CEO Jean-Charles Samuelian-Werve so that he could give us an update on the product.

Alan has obtained its own health insurance license and is a proper insurance company. It doesn’t partner with existing insurance companies. The company primarily sells its insurance product to other companies.

In France, employees are covered by both the national healthcare system and private insurance companies. So Alan convinces other companies to use its product for all employees.

Over the years, Alan has diversified its offering with high-end coverage, partnerships with CNP Assurances, Livi and Petit Bambou, and a focus on new verticals, such as companies in the hospitality industry or retired individuals.

“We’ve kept shipping, and I even think that our pace has increased. We’ve released some exciting stuff in recent months, for our members, for companies and for us internally,” Samuelian-Werve told me.

The biggest change isn’t visible to the end user. The company has built a service that lets them generate a new insurance package on demand. It uses historical data to figure out pricing on the fly. And it opens up some market opportunities as big companies want a custom insurance product depending on their needs.

The biggest Alan customer is a company with 1,000 to 1,500 employees. But the startup is currently selling its product to bigger companies. The idea is that companies with more than 100 employees can get a custom insurance package.

For the customer, pricing remains transparent as Alan shows you how much it costs to cover your medical needs depending on what you’re asking for. Alan adds a membership fee on top of that to access the platform and related services.

Alan is also introducing a new messaging feature. You can start a text discussion with a doctor whenever you have a question about your health — it’s included in your insurance package. Alan doesn’t want to replace your general practitioner. But having a doctor that you can text is always helpful when you’re not sure what to do next.

On the other side of the screen, there are actual doctors answering your questions. “We’ve hired a full-time doctor and we’re working with a bit under 10 doctors on a part-time basis,” Samuelian-Werve told me.

Alan’s app has been redesigned with a bigger emphasis on your health instead of your insurance. The company shows you all your interactions with health professionals. You can add documents and notes to consolidate information in the same place.

It sounds a bit like France’s DMP, which acts as a personal repository for all your health-related documents. And Alan doesn’t want to replace the public initiative. The startup would like to take advantage of the service to upload and download data at some point down the road.

If you give your consent, Alan can also proactively nudge you about your health. For instance, given your child’s age, Alan can notify you when they’re supposed to get vaccinated. Or if you haven’t been to the dentist in a year, Alan can tell you that it’s time to get a routine checkup.

Finally, the company has improved efficiency when it comes to reimbursements. “Seventy-four percent of reimbursements are issued within an hour. And we’re using instant transfers to send money to your bank account,” Samuelian-Werve told me.

As you can see, Alan is releasing incremental updates. They slowly add up and change the product. In the coming years, the company plans to offer its product in multiple European countries.

Powered by WPeMatico

The Miami-based startup Papa has raised an additional $18 million as it looks to expand its business connecting elderly Americans and families with physical and virtual companions, which the company calls “pals.”

The company’s services are already available in 17 states and Papa is going to expand to another four states in the next few months, according to chief executive Andrew Parker.

Parker launched the business after reaching out on Facebook to find someone who could serve as a pal for his own grandfather in Florida.

After realizing that there was a need among elderly residents across the state for companionship and assistance that differed from the kind of in-person care that would typically be provided by a caregiver, Parker launched the service. The kinds of companionship Papa’s employees offer range from helping with everyday tasks — including transportation, light household chores, advising with health benefits and doctor’s appointments, and grocery delivery — to just conversation.

With the social isolation brought on by responses to the COVID-19 pandemic there are even more reasons for the company’s service, Parker said. Roughly half of adults consider themselves lonely, and social isolation increases the risk of death by 29%, according to statistics provided by the company.

“We created Papa with the singular goal of supporting older adults and their families throughout the aging journey,” said Parker, in a statement. “The COVID-19 pandemic has unfortunately only intensified circumstances leading to loneliness and isolation, and we’re honored to be able to offer solutions to help families during this difficult time.”

Papa’s pals go through a stringent vetting process, according to Parker, and only about 8% of all applicants become pals.

These pals get paid an hourly rate of around $15 per hour and have the opportunity to receive bonuses and other incentives, and are now available for virtual and in-person sessions with the older adults they’re matched with.

“We have about 20,000 potential Papa pals apply a month,” said Parker. In the company’s early days it only accepted college students to work as pals, but now the company is accepting a broader range of potential employees, with assistants ranging from 18 to 45 years old. The average age, Parker said, is 29.

Papa monitors and manages all virtual interactions between the company’s employees and their charges, flagging issues that may be raised in discussions, like depression and potential problems getting access to food or medications. The monitoring is designed to ensure that meal plans, therapists or medication can be made available to the company’s charges, said Parker.

Now that there’s $18 million more in financing for the company to work with, thanks to new lead investor Comcast Ventures and other backers — including Canaan, Initialized Capital, Sound Ventures, Pivotal Ventures, the founders of Flatiron Health and their investment group Operator Partners, along with Behance founder, Scott Belsky — Papa is focused on developing new products and expanding the scope of its services.

The company has raised $31 million to date and expects to be operating in all 50 states by January 2021. The company’s companion services are available to members through health plans and as an employer benefit.

“Papa is enabling a growing number of older Americans to age at home, while reducing the cost of care for health plans and creating meaningful jobs for companion care professionals,” said Fatima Husain, principal at Comcast Ventures, in a statement. “

Powered by WPeMatico

The coronavirus global health pandemic — and the new emphasis on social distancing to slow down the spread of COVID-19 — has put healthcare and tech services used to enable healthcare remotely under the spotlight. Today a startup that’s building microinsurance and healthcare services specifically targeting emerging markets is announcing a round of funding to meet a surge in demand for its services.

BIMA, a startup that provides life and health insurance policies, along with telemedicine to support the latter, all via a mobile-first platform targeting consumers in emerging markets whose primary entry point to online services is via phones, not computers, is today announcing that it has raised $30 million in funding, a growth round that the Stockholm/London-based startup plans to use to double down on its health services in the wake increased demand around COVID-19.

The company currently provides telemedicine as a service connected to its health insurance, and it has expanded to include health programs for managing illnesses and offering discounts for pharmacies, and the plan seems to be to bring more services into the mix.

This is the same approach we’re seeing from other insurance startups targeting emerging economies, including China’s Waterdrop, which recently raised $230 million. Looking at the network of services Waterdrop is building, including crowdfunding, gives you an idea of what else BIMA might potentially look to add in, too.

The round is being led by a new investor — China’s CreditEase Fintech Investment Fund (CEFIF) — with previous backers LeapFrog Investments and insurance giant Allianz (who were in BIMA’s previous, $97 million round) also participating.

The startup is not disclosing its valuation this time around, but in its previous round the company was valued at $300 million, and it has grown considerably since then.

BIMA has now clocked up 2 million tele-doctor consultations and has some 35 million insurance and health policies on its books, growing its customer base by some 11 million people in the last two years. It’s now active in 10 countries — Ghana, Tanzania and Senegal in Africa; and Bangladesh, Cambodia, Indonesia, Malaysia, Pakistan, Philippines and Sri Lanka across Asia.

At a time when we have seen a number of insure tech startups emerge in the US and Europe — with some, like Lemonade, growing into publicly-listed companies — BIMA is very notable in part because of who it targets.

It’s not higher economic brackets, or necessarily segments with disposable income, or those in developed markets with stable economies. Rather, its focus is, in its words, underserved families that typically live on less than $10 per day and are at high risk of illness or injury, with 75% of its customers accessing insurance services for the very first time, BIMA notes.

“Telemedicine and insurance are needed more than ever and COVID accelerated awareness and acceptance for these types of products amongst emerging consumers and government. They’ve gone from ‘nice to have’ to a necessity,” said Mathilda Strom, who co-founded the company with CEO Gustaf Agartson, in an interview. “Utilisation nearly doubled in our telemedicine services.” BIMA covers COVID and pandemics in general in its policies, she added. “We have paid out COVID-related claims to families of people who suffered or passed away from the illness.”

It’s also working with health authorities that have been overwhelmed in the pandemic. Pakistani government and Indonesian government now use BIMA to off-load their health services by providing teledoctor consultations or doctors chats to customers.

Aiming at developing economies where middle classes are still only materialising, currencies are potentially unstable, and there is still a lack of infrastructure means that BIMA is contending with a combination of factors that makes the bar high for entry, but it’s also potentially more rewarding because of the lack of competition and tapping a demand that is still rapidly growing.

“The onset of COVID-19 has brought home the value of telemedicine, to help prevent the spread of disease, and the importance of insurance, for peace of mind,” said Agartson in a statement.

“Through digital solutions, and a human touch, we’ve been able to serve hard to reach communities with tools and services that bring them a sense of security at such a challenging time. The funds we have raised will allow us to expand our operations and further invest in our product offering that will help us scale quickly to meet the unprecedented demand for our services.”

It’s interesting to see CreditEase, a Chinese investor, as part of this round: the idea of all-in, full service health services companies banked around the insurance proposition has been one cultivated in the Chinese market. But even with the development of HMOs in the US, it’s interesting that there have been relatively few startups around the world trying to develop similar models. BIMA stands out in part because of that.

“We are very impressed by BIMA’s innovative integration of micro insurance and tele-doctor services, which provide critical coverage to meet large unmet demand in emerging markets, and whose value is accentuated further by the current pandemic,” said Dennis Cong, managing partner at CEFIF, in a statement. “We are very happy to have the opportunity to join this meaningful journey, along with the established leading shareholders, and support the company to grow its business and expand its leadership position in its served markets.”

“The market that BIMA is serving is vast and demand for health services is tremendous,” added Stewart Langdon, a partner at LeapFrog Investments. “BIMA’s unique digital capabilities empower emerging market consumers to access many health and insurance services on a single, easy to use platform. That includes protection for millions of first-time buyers of insurance who would otherwise remain unprotected and at risk.”

“We are happy to continue our partnership with BIMA and jointly deliver telemedicine and remote healthcare services in developing markets,” said Nazim Cetin, CEO at Allianz X, in a statement. “We believe the demand for these services will continue to increase and want to manifest BIMA’s leading position in the market by providing support with our experience and network.”

Powered by WPeMatico

Telehealth, or remote, tech-enabled healthcare, has existed for years in primary medical care through companies like Teladoc (NYSE: TDOC), Doctors on Demand and MDLIVE.

In recent years, the application of telehealth had rapidly expanded to address specific chronic and behavioral health issues like mental health, weight loss and nutrition, addiction, diabetes and hypertension, etc. These are real and oftentimes very severe issues faced by people all over the world, yet until now have seen little to no use of technology in providing care.

We believe behavioral health is particularly suited to benefit from the digitization trends COVID-19 has accelerated. Previously, we’ve written about the pandemic’s impact on online learning and education, both for K-12 students and adult learners. But behavioral health is another area impacted by the fundamental change in consumers’ behavior today. Below are four reasons we think the time is now for behavioral health startups — followed by five key factors we think characterize successful companies in this area.

Traditional behavioral healthcare is cost-prohibitive for most people. In-person therapy costs $100+ per session in the U.S., and many mental health and substance-use providers don’t accept insurance because they don’t get paid enough by insurers.

By contrast, telehealth reduces overhead costs and scales more effectively. Leveraging technology, providers can treat more patients in less time with almost zero marginal costs. Mobile-based communications enable asynchronous care that further helps providers scale. Access to digital content gives patients on-going support without the need for a human on the other side. This is particularly useful in treating behavioral health issues where ongoing support and motivation may be necessary.

Globally, we face an extreme shortage of behavioral health providers. For example, the United States has fewer than 30,000 licensed psychiatrists (translating to <1 for every 10,000 people). Outside of big cities, the problem gets worse: ~50-60% of nonmetro counties have no psychologists or psychiatrists at all.

Even when providers are available, wait times for appointments are notoriously long. This is a huge issue when behavioral health conditions often require timely intervention.

We are seeing new platforms build large networks of certified coaches, licensed psychologists and psychiatrists, and other providers, aggregating supply in what has historically been a scarce and a highly fragmented provider population.

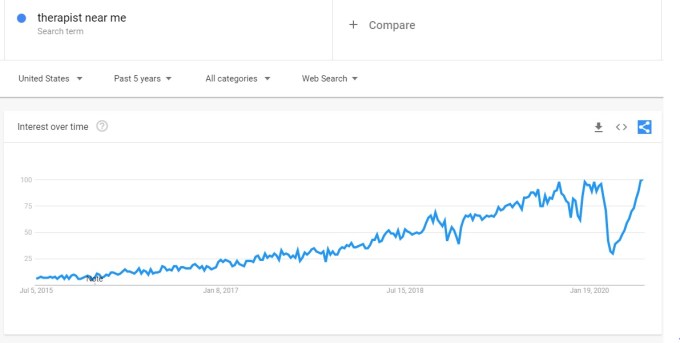

We believe the stigma associated with mental illness and other behavioral health conditions is dissipating. More and more public figures are speaking out about their struggle with anxiety, depression, addiction and other behavioral health issues. Our zeitgeist is shifting fast, and there’s an all-time high in people seeking help as the Google Trends data below demonstrates.

Image Credits: Google

Note: The anomalous dip in March/April ’20 was driven by mandatory shelter-in-place due to COVID-19.

Powered by WPeMatico