GV

Auto Added by WPeMatico

Auto Added by WPeMatico

GPS is one of those science fiction technologies whose use is effortless for the end user and endlessly challenging for the engineers who design it. It’s now at the heart of modern life: everything from Amazon package deliveries to our cars and trucks to our walks through national parks are centered around a pin on a map that monitors us down to a few meters.

Yet, GPS technology is decades old, and it’s going through a much-needed modernization. The U.S., Europe, China, Japan and others have been installing a new generation of GNSS satellites (GNSS is the generic name for GPS, which is the specific name for the U.S. system) that will offer stronger signals in what is known as the L5 band (1176 MHz). That means more accurate map pinpoints compared to the original generation L1 band satellites, particularly in areas where line-of-sight can be obscured, like urban areas. L5 was “designed to meet demanding requirements for safety-of-life transportation and other high-performance applications,” as the U.S. government describes it.

It’s one thing to put satellites into orbit (that’s the easy part!), and another to build power-efficient chips that can scan for these signals and triangulate a coordinate (that’s the hard part!). So far, chipmakers have focused on creating hybrid chips that pull from the L1 and L5 bands simultaneously. For example, Broadcom recently announced the second-generation of its hybrid chip.

OneNav has a totally different opinion on product design, and it placed it right in its name. Eschewing the hybrid chip model of mixing old signals with new, it wants one chip monitoring the singular band of L5 signals to drive cost and power savings for devices. One nav to rule them all, as it were.

The company announced today that it has closed a $21 million Series B round led by Karim Faris at GV, which is solely funded by Alphabet. Other investors included Matthew Howard at Norwest and GSR Ventures, which invested in earlier rounds of the company. All together, OneNav has raised $33 million in capital and was founded about two years ago.

CEO and co-founder Steve Poizner has been in the location business a long time. His previous company, SnapTrack, built out a GPS positioning technology for mobile devices that sold to Qualcomm for $1 billion in stock in March 2000, at the height of the dot-com bubble. His co-founder and CTO at OneNav, Paul McBurney, has similarly spent decades in the GNSS space, most recently at Apple, according to his LinkedIn profile.

OneNav CEO and co-founder Steve Poizner, seen here in 2009. Image Credits: David McNew via Getty Images

They saw an opportunity to build a new navigation company as L5 band satellites have switched on in recent years. As they looked at the market and the L5 tech, they decided they wanted to go further than other companies by eliminating the legacy tech of older GPS technology and moving entirely into the future. By doing that, its design is “half the size of the old system, but much higher reliability and performance,” Poizner said. “We are aiming to get location technology into a much broader number of products.”

He differentiated between upgrading GPS from upgrading wireless signals. “With these L5 satellites, we don’t need the L1 satellites anymore [but] with 5G, you still need 4G,” he said. L5 band GPS does everything that earlier renditions did, but better, whereas with wireless technologies, they often need to complement each other to offer peak performance.

There’s one caveat here: The L5 signal is still considered “pre-operational” by the U.S. government, since the U.S. GPS system only has 16 satellites broadcasting the signal today, and is targeting 24 satellites for full deployment by later in this decade. However, other countries have also deployed L5 GNSS satellites, which means that while it may not be fully operational from the U.S. government’s perspective, it may well be good enough for consumers.

OneNav’s goal according to Poizner is to be “the Arm of the GNSS space.” What he means is that like Arm, which produces the chip designs for nearly all mobile phones globally, OneNav creates comprehensive designs for L5 band GPS chips that can be integrated as a system-on-chip into the products of other manufacturers so that they can “embed a high-performance location engine based on their silicon.”

The company today also announced that its first design customer will be In-Q-Tel, the U.S. intelligence community’s venture capital and business development organization. Poizner said that through In-Q-Tel, “we now have a development contract with a U.S. government agency.” The company is expecting that its customer evaluation units will be completed by the end of this year with the objective of potentially having OneNav’s technology in end-user devices by late 2022.

Location tracking has become a major area of investment for venture capitalists, with companies working on a variety of technologies outside of GPS to offer additional detail and functionality where GPS falls short. Poizner sees these technologies as ultimately complementary to what he and his team are building at OneNav. “The better the GPS, the less pressure on these augmentation systems,” he said, while acknowledging that, “it is the case though that in certain environments [like downtown Manhattan or underground in a subway], you will never get the GPS to work.”

For Poizner, it’s a bit of a return to entrepreneurship. Prior to starting OneNav, he had been heavily involved in California state politics. Several years after the sale of SnapTrack to Qualcomm, he unsuccessfully ran for a seat in the California State Assembly. He later was elected California’s insurance commissioner in 2007 under former Governor Arnold Schwarzenegger. He ran for governor in 2010, losing in the Republican primary against Meg Whitman, who made her name as the longtime head of eBay. He ran for his former seat of California insurance commissioner in 2018, this time as a political independent, but lost.

OneNav is based in Palo Alto and currently has more than 30 employees.

Powered by WPeMatico

Mental health, and how it is getting addressed, has been one of the major leitmotifs of the past year of pandemic living. COVID-19 not only has led to a lot of people getting ill or worse; it has increased isolation, economic uncertainty and led to a lot of other kinds of disappointments, and that all has had a knock-on effect on our collective and individual state of mind.

Today a startup called Headway, which has been working on building a better way for people to attend to themselves — by way of a three-sided marketplace of sorts, by helping a person to find and afford a therapist via a free-to-use portal, by making it possible for those therapists to accept a wider range of insurance plans and by helping those insurance plans facilitate more therapy appointments for their patient networks — is announcing a major round of funding on the heels of strong growth.

The startup has raised $70 million, money that it will be using to continue expanding its platform with more partnerships, more hiring for its team (it wants to have 300 people this year) and opening in new regions, aiming to be nationwide this year in the U.S. This round, a Series B, has a number of big names attached to it: It is being led by Andreessen Horowitz, with Thrive, GV and Accel also participating. (The latter three are repeat investors: Thrive and GV led its Series A, while Accel led its seed.) This Series B is coming in at a $750 million valuation.

The rapid pace of funding, the backers and that valuation all underscore the timeliness of the concept, and also the traction that Headway is getting for its approach.

When we last covered Headway — it raised $26 million just last November, six months ago — it said it had registered some 1,800 therapists on its platform in the New York metro area, where it is based. Now that number is up to more than 3,000 with its network now covering not just NYC, but also New Jersey, Florida, North Carolina, Texas, Georgia, Michigan, Virginia, Washington, Illinois and Colorado. It has more than 2,000 patients joining the platform each month and has so far helped facilitate 300,000 appointments, with a current average of 30,000 appointments each month. Revenues have in the last year, meanwhile, grown nine-fold.

The approach that Headway is taking — creating not just a vertical search portal for therapists, but building a back-end system to help those therapists grow their business by making it easier for them to accept insurance coverage — comes directly out of the experiences faced by one of the startup’s co-founders.

Andrew Adams, the CEO of Headway, told me last year he came up with the idea after he moved to New York from California several years ago to take a job. In seeking a therapist, he found most unwilling to accept his insurance plan as payment, making getting therapy unaffordable.

This is a very typical problem, he said. Some 70% of therapists do not accept insurance today because it’s too complicated for them to integrate, since about 85% of all therapists happen to be solo practitioners. So something that should be accessible to everyone becomes something typically only used by those who can afford it, or have entered into social care programs that might provide it. But that leaves a massive gap in the middle.

“This is the defining problem in the space,” he said at the time. “Health insurance is built around a medical world dominated by billers and admins, but therapists are small practitioners and don’t have the bandwidth to handle that, so they don’t. So we thought if we could make it easier for them to, they would, and they have.”

And indeed, if you are needing to see a therapist, the very last thing you need or want to be doing is spending your time trying to work out the economics of doing so: You need to be focused on finding someone you feel you can talk to; someone who can help you.

The problem is a huge one. In the U.S. alone it’s estimated that there are some 82 million people who have treatable health conditions. Headway was founded on the premise that most of them currently do not seek that treatment because of cost or accessibility.

A lot of therapy has traditionally been about seeing people in person — and arguably the fact that we’ve had so much reduced contact with people has contributed to mental health issues this past year — but in the event, Headway has definitely adapted to the current climate.

The company says that some 89% of its appointments at the moment are being carried out remotely. This is down from 97% at the peak of the pandemic in the U.S., and has been slowly starting to taper off, the company said. Some of the increased volume, meanwhile, is a direct result of therapists working remotely — they can fit more people in to a daily schedule as a result.

In terms of insurers, the company currently works with Aetna, Cigna, United Healthcare, Oscar and Oxford and says the list will be growing. One interesting detail is that Headway has not only built out a bigger funnel for these insurers in terms of the practitioners they work with and individuals who can subsequently use insurance to pay for therapy, but conversely has served to be a conduit for those insurance groups in bringing more patients through to those therapists, who are now a part of their networks, by way of Headway’s platform.

Headway says that using its system can help a patient get an appointment within five days, versus the the 30-day average you typically face when using an insurance directory.

It’s the kind of scale and “software eating the world” efficiency that has attracted Andreessen Horowitz to backing companies before, with the added detail of this being particularly relevant to the time we are living in.

“By getting the mental health provider community on the same page with insurance companies for the first time, Headway unlocks affordable mental healthcare for millions of Americans,” said Scott Kupor, managing partner at Andreessen Horowitz. “We’re incredibly excited to work alongside the Headway team.” Kupor is also joining Headway’s board with this round.

Cherry Miao, a former partner at Accel and Headway’s lead seed investor, is also joining as head of Finance & Data.

“I’ve been fortunate to work with some of the world’s most influential startups, and know that being part of Headway’s meaningful mission, robust business model, and incredibly talented team is a once-in-a-lifetime opportunity,” she said. “I’m thrilled to be helping rebuild America’s mental healthcare system for access and affordability.”

Powered by WPeMatico

Non-fungible tokens have been around for two years, but these NFTs, one-of-one digital items on the Ethereum and other blockchains, are suddenly becoming a more popular way to collect visual art, primarily, whether it’s an animated cat or an NBA clip or virtual furniture.

“Suddenly” is hardly an overstatement. According to the outlet Cointelegraph, during the second half of last year, $9 million worth of NFT goods sold to buyers; during one 24-hour window earlier this week, $60 million worth of digital goods were sold.

What’s going on? A thorough New York Times piece on the trend earlier this week likely fueled new interest, along with a separate piece in Esquire about the artist Beeple, a Wisconsin dad whose digital drawings, which he has created every single day for the last 13 years, began selling like hotcakes in December. If you evidence of a tipping point (and it’s amply available), the work of Beeple, whose real name is Mike Winkelmann, was just made available through Christie’s. It’s the venerable auction house’s first sale of exclusively digital work.

To better understand the market and why it’s blowing up in real time, we talked this week with David Pakman, a former internet entrepreneur who joined the venture firm Venrock a dozen years ago and began tracking Bitcoin soon after, even mining the cryptocurrency at his Bay Area home beginning in 2015. (“People would come over and see racks of computers, and it was like, ‘It’s sort of hard to explain.’”)

Perhaps it’s no surprise that he also became convinced early on of the promise of NFTs, persuading Venrock to lead the $15 million Series A round for a young startup, Dapper Labs, when its primary offering was CryptoKitties, limited-edition digital cats that can be bought and bred with cryptocurrency.

While the concept baffled some at the time, Pakman has long seen the day when Dapper’s offerings will be far more extensive, and indeed, a recent Dapper deal with the NBA to sell collectible highlight clips has already attracted so much interest in Dapper that it is reportedly right now raising $250 million in new funding at a post-money valuation of $2 billion. While Pakman declined to confirm or correct that figure, but he did answer our other questions in a chat that’s been edited here for length and clarity.

TC: David, dumb things down for us. Why is the world so gung-ho about NFTs right now?

DP: One of the biggest problems with crypto — the reason it scares so many people — is it uses all these really esoteric terms to explain very basic concepts, so let’s just keep it really simple. About 40% of humans collect things — baseball cards, shoes, artwork, wine. And there’s a whole bunch of psychological reasons why. Some people have a need to complete a set. Some people do it for investment reasons. Some people want an heirloom to pass down. But we could only collect things in the real world because digital collectibles were too easy to copy.

Then the blockchain came around and [it allowed us to] make digital collectibles immutable, with a record of who owns what that you can’t really copy. You can screenshot it, but you don’t really own the digital collectible, and you won’t be able to do anything with that screenshot. You won’t be able to to sell it or trade it. The proof is in the blockchain. So I was a believer that crypto-based collectibles could be really big and actually could be the thing that takes crypto mainstream and gets the normals into participating in crypto — and that’s exactly what’s happening now.

TC: You mentioned a lot of reasons that people collect items, but one you didn’t mention is status. Assuming that’s your motivation, how do you show off what you’ve amassed online?

DP: You’re right that one of the other reasons why we collect is to show it off status, but I would actually argue it’s much easier to show off our collections in the digital world. If I’m a car collector, the only way you’re going to see my cars is to come over to the garage. Only a certain number of people can do that. But online, we can display our digital collections. NBA Top Shop, for example, makes it very easy for you to show off your moments. Everyone has a page and there’s an app that’s coming and you can just show it off to anyone in your app, and you can post it to your social networks. And it’s actually really easy to show off how big or exciting your collection is.

TC: It was back in October that Dapper rolled out these video moments, which you buy almost like a Pokemon set in that you’re buying a pack and know you’ll get something “good” but don’t know what. But while almost half it sales have come in through the last week. Why?

DP: There’s only about maybe 30,000 or 40,000 people playing right now. It’s growing 50% or 100% a day. But the growth has been completely organic. The game is actually still in beta, so we haven’t been doing any marketing other than posting some stuff on Twitter. There hasn’t been attempt to market this and get a lot of players [talking about it] because we’re still working the bugs out, and there are a lot of bugs still to be worked out.

But a couple NBA players have seen this and gotten excited about their own moments [on social media]. And there’s maybe a little bit of machismo going on where, ‘Hey, I want my moment to trade for a higher price.’ But I also think it’s the normals who are playing this. All you need to play is a credit card, and something like 65% of the people playing have never owned or traded in crypto before. So I think the thesis that crypto collectibles could be the thing that brings mainstream users into crypto is playing out before our eyes.

TC: How does Dapper get paid?

DP: We get 5% of secondary sales and 100% minus the cost of the transaction on primary sales. Of course, we have a relationship with the NBA, which collects some of that, too. But that’s the basic economics of how the system works.

TC: Does the NBA have a minimum that it has to be paid every year, and then above and beyond that it receives a cut of the action?

DP: I don’t think the company has gone public with the exact economic terms of their relationships with the NBA and the Players Association. But obviously the NBA is the IP owner, and the teams and the players have economic participation in this, which is good, because they’re the ones that are creating the intellectual property here.

But a lot of the appreciation of these moments — if you get one in a pack and you sell it for a higher price — 95% of that appreciation goes to the owner. So it’s very similar to baseball cards, but now IP owners can participate through the life of the product in the downstream economic activity of their intellectual property, which I think is super appealing whether you’re the NBA or someone like Disney, who’s been in the IP licensing business for decades.

And it’s not just major IP where this NFT space is happening. It’s individual creators, musicians, digital artists who could create a piece of digital art, make only five copies of it, and auction it off. They too can collect a little bit each time their works sell in the future.

TC: Regarding NBA Top Shot specifically, prices range massively in terms of what people are paying for the same limited-edition clip. Why?

DP: There are two reasons. One is that like scarce items, lower numbers are worth more than higher numbers, so if there’s a very particular LeBron moment, and they made 500 [copies] of them, and I own number one, and you own number 399, the marketplace is ascribing a higher value to the lower numbers, which is very typical of limited-edition collector pieces. It’s sort of a funny concept. But it is a very human concept.

The other thing is that over time there has been more and more demand to get into this game, so people are willing to pay higher and higher prices. That’s why there’s been a lot of price appreciation for these moments over time.

TC: You mentioned that some of the esoteric language around crypto scares people, but so does the fact that 20% of the world’s bitcoin is permanently inaccessible to its owners, including because of forgotten passwords. Is that a risk with these digital items, which you are essentially storing in a digital locker or wallet?

DP: It’s a complex topic, but I will say that Dapper has tried to build this in a way where that won’t happen, where there’s effectively some type of password recovery process for people who are storing their moments in Dapper’s wallet.

You will be able to take your moments away from Dapper’s account and put it into other accounts, where you may be on your own in terms of password recovery.

TC: Why is it a complex topic?

DP: There are people who believe that even though centralized account storage is convenient for users, it’s somehow can be distrustful — that the company could de-platform you or turn your account off. And in the crypto world, there’s almost a religious ferocity about making sure that no one can de-platform you, that the things that you buy — your cryptocurrencies or your NFTs. Long term, Dapper supports that. You’ll be able to take your moments anywhere you want. But today, our customers don’t have to worry about that I-lost-my-password-and-I’ll-never-get-my-moments-again problem.

Powered by WPeMatico

In 2015, then-Twitter product manager Terri Burns penned a piece about staying optimistic despite the sexism and racism that exists expansively within tech. “America has broke my heart countless times, but I believe that technology can be a tool to mend some of the woes of the world and produce tools to better humanity,” she wrote.

“It’s hard to continue to believe this when the industry holding this power takes so little interest in the basic rights of women and people of color. I actively choose to remain hopeful under the belief that myself and many of the incredible people also working toward equality and justice in technology and in America will make a difference.”

Burns left Twitter in 2017 to join GV, formerly known as Google Ventures. Her hope has now been met with recognition. GV has promoted Terri Burns to partner, making her the first Black woman to hold that role — and the youngest ever. Making history comes with its own set of pressures and spotlight, but Burns seems focused on simply finding a new place to put her optimism and hope: Gen Z.

Read on for a Q&A with Burns about her investment thesis, role change and plans as partner.

TechCrunch: Before you were in venture, you held product roles at Venmo and Twitter. When did you know that computer science was the right field for you?

Terri Burns: I grew up in Southern California, in Long Beach. And I think I’ve always just been a really curious kid. For me, I always spent a ton of time just asking questions and I always liked science. But, I actually did not have any interest in computer science until college.

I went to NYU and I remember thinking my freshman year, major-wise, that I’m not entirely sure what it is that I want to do. By chance, I happened to apply to this program called Google BOLD. It was a week-long program for people that are a little bit too young for a full-time internship. There we just talked about all the opportunities at Google that were not engineering.

It’s funny, I grew up in California, but growing in Long Beach, I didn’t know anything about Silicon Valley whatsoever. College was really the first time I had an introduction to Silicon Valley, to technology, to entrepreneurship, to Google. Even though [Google BOLD] was a nontechnical program, I was “I want to know what this coding thing is about.” So my sophomore year, when I went back to campus, I took my first computer science class. And that was the beginning.

What’s the most effective way to get on your radar without knowing you prior? Any anecdotes for how out of network founders grabbed your attention?

Yes! In fact, I met Suraya Shivji, the CEO of HAGS, through Twitter. I knew people who were buzzing about the company on Twitter, and I proactively reached out to her to do a virtual coffee. Social media, networking events and warm intros are pretty good paths. For what it’s worth, I read every cold email I receive as well; I’m just not able to respond to all of them!

What kind of companies will you always take a meeting with?

Mobile consumer and consumer in general is definitely what my background is in, and so I’ll always have a natural inclination

in consumer. I recognize that that’s broad, but I think software consumer companies are ones that I know and I understand. So that’s something I’m always going to lean into. One of the things that I really love about GV is that we are a generalist firm, which has also been a theme for me personally and something that I definitely want to uphold as an investor. Some other things that I’m interested in [are] fintech on the enterprise side and [ … ] enterprise collaboration tools.

Powered by WPeMatico

One of the more salient trends in the tech world — arguably the engine that propels it — has been the recurring theme of people who hone talents at bigger companies and then strike out on their own to found their own startups.

(Some, like Max Levchin, even hire entrepreneurial types intentionally to help perpetuate this cycle and get more proactive teams in place.)

It turns out that trend doesn’t just apply to companies, but also to the investors who back them. At Disrupt we talked with three venture capitalists who have followed that path: Making their names and cutting their teeth at major firms, and now building their own “startup” funds on their own steam.

On the macro level, the whole world has been living through a challenging time this year. But as we’ve seen time and again the wheels have continued to turn in the tech world.

IPOs are returning, products are being rolled out, people are buying a lot online and using the internet to stay connected, there has been a lot of M&A and promising startups are getting funded.

Indeed, if entrepreneurs and their innovations are the engine of the tech world, money is the fuel, and that is the opportunity that Dayna Grayson (formerly of NEA, now founder at Construct Capital), Renata Quintini (formerly at Lux Capital, now founder at Renegade Partners) and Lo Toney (formerly GV, now founder at Plexo Capital) have zeroed in to address.

Grayson said that part of the reason for striking out to start Construct Capital with co-founder Rachel Holt was what they saw as an opportunity to create a firm that specifically funded startups tackling the industrial sector:

“Half the U.S. economy’s GDP, half the GDP of this country, hasn’t really been digitized,” she said. “[Firms] haven’t been tech enabled. They’ve been way under invested … The time is now to build with early stage entrepreneurs.”

While Construct is focusing on a sector, Renegade was founded to focus on something else: The stage of development for a startup, and specific the Series B, which the firm refers to as “supercritical,” essential in terms of getting team and strategy right after a startup is no longer just starting out, but before and leading to scaled growth.

“We saw through our boards over and over again companies that figured out how to scale their organizations, put in the processes,” said Quintini, who co-founded Renegade with Roseanne Wincek. “On the people side, they actually went further and captured a lot more market cap and market share faster. Once we saw this opportunity, we could not let it go.”

She compares the current imperative to really focus on how to build and scale companies at the “supercritical” stage to the focus on early stage funding that typified an earlier period in the development of the startup ecosystem 15 years ago. “You could get a million dollars and be in business, a lot more people could, and you had less time to figure out what really resonated with customers,” she said. “That really gave rise to today.”

Toney has taken yet another approach, focusing not on sector, nor stage, but using capital to help germinate a whole new demographic of founders, the premise being that funding a more diverse and inclusive mix of founders is not just good for creating a more level playing field, but also for the good of more well-rounded products that speak to a wider population of users.

“I was having a great time at GV, but I just saw this opportunity as being one that was too hard to resist,” said Toney of founding Plexo, which invests not just in startups but in funds that are following a similar investment principle to his. Investing in both funds and founders is something GV did as well, but the added ability to turn that into investing with a social imperative was important. “To have this byproduct of increasing diversity and inclusion in the ecosystem [is something] I’m super passionate about,” he said.

We are living through a time when the tech world seems to be awash in capital. One of the byproducts of having so many successful tech companies has been limited partners rushing in to back more VCs in hopes of also getting some of the spoils: Many firms are closing funds in record times, oversubscribed and that’s having a knock-on effect not just in terms of startups getting funded, but VCs themselves also multiplying with increasing frequency. All three said that the fact that they all identify as more than just “another new VC”, with specific purposes, also makes it easier for them to get themselves noticed to get involved in good deals.

Grayson said that the challenge of starting a firm in the midst of a global pandemic turned out to be a piece of good fortune in disguise in an industry that thrives on the concept of “disruption” (as we at TechCrunch know all too well … ).

“We were really lucky that we started investing in a COVID world,” she said. “So many things have been up ended. And I think, you know, software adoption and technology adoption have been moved up 10-20 years in industry. [And] the way that we work together really has changed.” She also said that they’ve found themselves almost looking for companies “created in a COVID environment,” which indeed would qualify as a battle-tested business model.

In terms of raising funds themselves, Toney also recalled the period when we saw a real surge of VCs emerging to fund companies at the seed stage and the growth of “solo capitalists” around that.

“I think what’s really interesting about solo capitalists is [how] they take their understanding of operations, and a deep network of other technologists, both from big companies as well as entrepreneurs, and … leverage access to all that deal flow by going out and actually raising capital from other sources, whether that be high net worth individuals or family offices or even institutions,” he said.

Powered by WPeMatico

Imagine a model of collaborative research and development among hospitals, pharmaceutical companies, universities and other research institutions where no one shared any actual data.

That’s the dream of the new New York-based startup Owkin, which has raised $25 million in fresh financing from investors, including Bpifrance Large Venture, Cathay Innovation and MACSF (the French Pension Fund for Clinicians), alongside previous investors GV, F-Prime Capital and Eight Roads.

The company’s pitch is that data scientists, clinical doctors, academics and pharmaceutical companies can all log in to the virtual lab that Owkin calls the Owkin Studio.

In that virtual environment, all parties can access anonymized data sets and models exclusively to refine their own research and development and studies to ensure that the most cutting-edge insights into novel biomarkers, mechanisms of action and predictive models inform the work that all of the relevant parties are doing.

The ultimate goal, the company said, is to improve patient outcomes.

In its quest to get more companies and institutions to open up and share information — with the promise that the information can’t be extracted or used in a way that isn’t allowed by the owners of the data — Owkin is replicating work that other companies are pursuing in fields ranging from healthcare to financial services and beyond.

The Israeli company Qedit has developed similar technologies for the financial services industry, and Sympatic, a recent graduate from one of the recent batches of Techstars companies, is working on a similar technology for the healthcare industry.

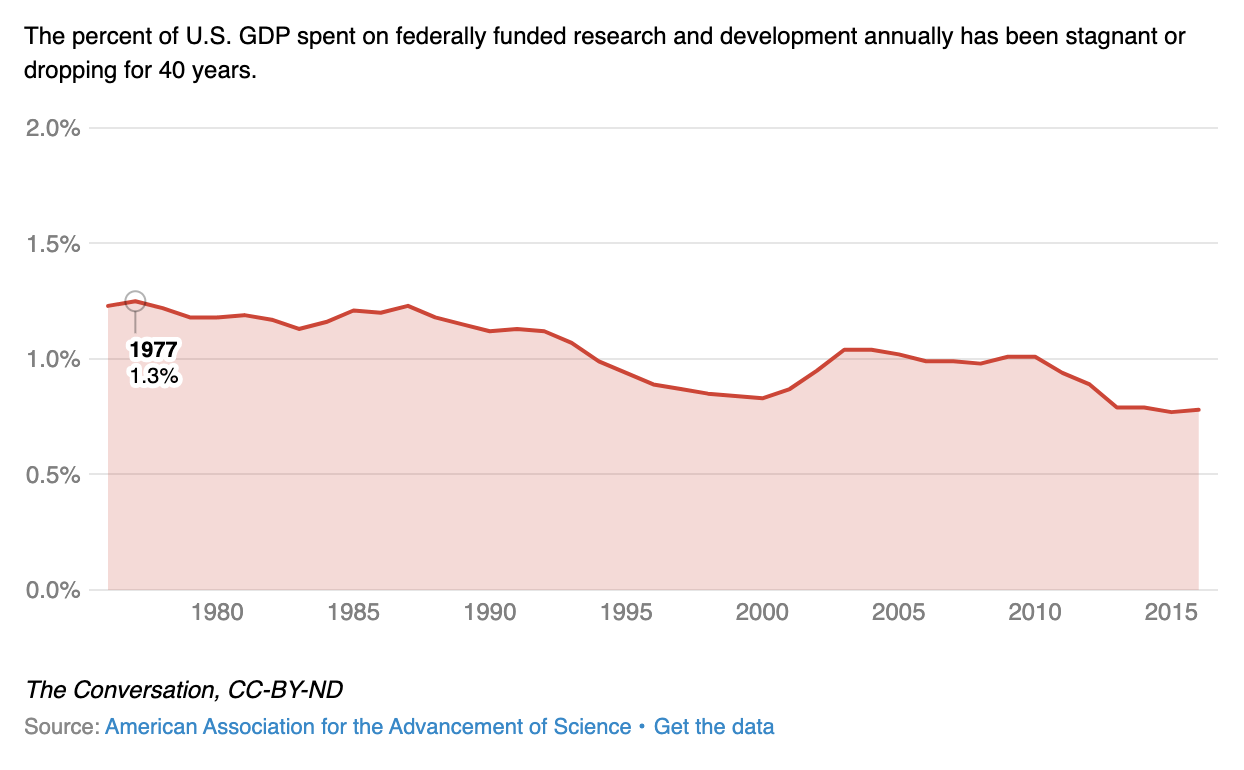

Owkin makes money by enabling remote access to the data sets for pharmaceutical companies and licensing the models developed by universities to those companies. It’s a way for the company to entice researchers to join the platform and provide another revenue stream for research institutions who have seen their funding decline over the last 40 years.

“We have a huge loop of academic universities that have access to the data and are developing algorithms and we share data,” said the company’s chief executive Dr. Thomas Clozel. “At the end what it helps is developing better drugs.”

Declines in federal funding for scientific research since the 1980s (Image courtesy of The Conversation)

The investment from Owkin’s new and existing investors takes the company to $55 million in total capital raised through the extension of its Series A round. In all, the round totaled $52 million, Clozet said.

“We are exactly where we need to be because it’s about privacy and privacy is more important than ever before,” said Clozet.

The COVID-19 epidemic has emphasized the need for closer collaboration among different corporations and research institutions, and that has also increased demand for the company’s technology. “It touches everything… We have access to the right data sets and centers to build the best models for COVID,” said Clozet. “We’re lucky to have the right traction before the COVID happens and we have the right research that has been done.”

In fact, the company has launched the Covid-19 Open AI Consortium (COAI), and is using its platform to advance collaborative research and accelerate clinical development of effective treatments for patients infected with the coronavirus, the company said. All of its findings will be shared with the global medical and scientific communities.

The initial focus on the research is on cardiovascular complications in COVID-19 patients in collaboration with CAPACITY, an international registry working with over 50 centers worldwide, the company said. Other areas of research will include patient outcomes and triage, and the prediction and characterization of immune response, according to Owkin.

“Since we first backed Owkin in 2017, we have been sharing its vision to apply AI to fighting one of the most dreadful diseases on earth: cancer,” said Jacky Abitbol, a partner at Cathay Innovation. “Owkin has risen to become a leader in digital health, we are proud to grow our investment in the company to fuel its ambition to pioneer AI for medical research, while preserving patient-privacy and data security.”

Powered by WPeMatico

Digits, a fintech startup hailing from the same team that built and sold Crashlytics to Twitter, is officially launching today after two years of development. It’s also announcing a $22 million Series B round of funding led by GV, as it makes its public debut.

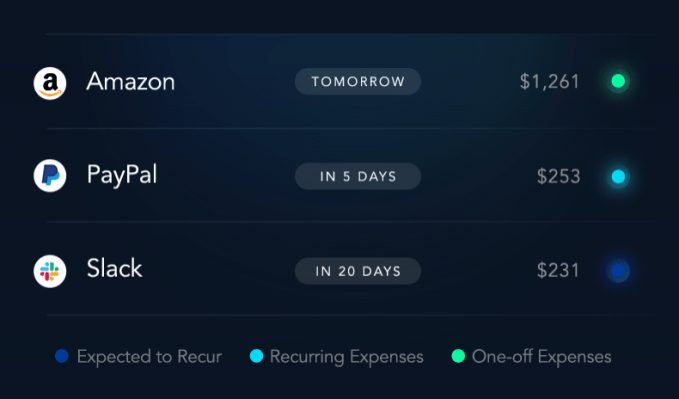

While the company had been fairly quiet about product details while in stealth mode, it’s today unveiling its first product: a visual, machine learning-powered expense monitoring dashboard aimed at startups and small businesses.

The dashboard, called Digits for Expenses, helps business owners track how their company is spending money, by showing things like spend by category, by identifying vendors and recurring expenses and by offering real-time alerts, among other features.

Instead of requiring business owners to make a switch from their existing financial solutions, Digits connects with the accounting software, banks, payroll providers, financial packages, sources of revenue and credit cards the business already uses — like Xero, QuickBooks, NetSuite, Citi, Bank of America or Chase, for example.

Instead of requiring business owners to make a switch from their existing financial solutions, Digits connects with the accounting software, banks, payroll providers, financial packages, sources of revenue and credit cards the business already uses — like Xero, QuickBooks, NetSuite, Citi, Bank of America or Chase, for example.

At launch, the list includes more than 9,000 banks, with support for Xero and NetSuite coming soon.

After setup, Digits will then automatically analyze the company’s spend and visualize it, in real time.

While visualizations of data may be reminiscent of personal finance startup Mint, Digits’ web-based solution is more technical in nature and offers an expanded analysis of the data on hand. Plus, as a business solution, it has to offer features like security, permissioning and collaborative workflows, which results in a more sophisticated product.

Digits also uses machine learning technology to predictively categorize transactions as they happen and the software can alert users to anomalies — like suspicious activity or unexpectedly large transactions — in real time. Business owners can use the dashboard to find out things like how quickly expenses are growing, what the cash flow looks like, where costs can be trimmed, what services are being paid for on a recurring basis and more, and can search for transactions.

Digits also uses machine learning technology to predictively categorize transactions as they happen and the software can alert users to anomalies — like suspicious activity or unexpectedly large transactions — in real time. Business owners can use the dashboard to find out things like how quickly expenses are growing, what the cash flow looks like, where costs can be trimmed, what services are being paid for on a recurring basis and more, and can search for transactions.

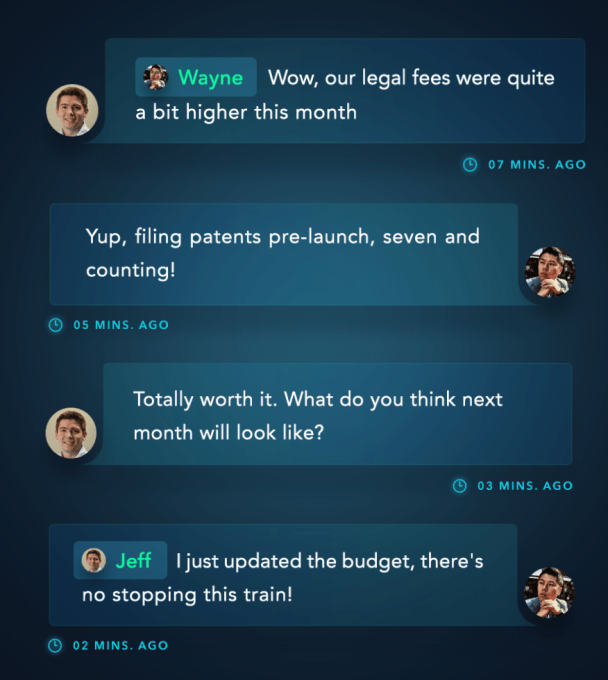

The software also supports the ability to comment on transactions, loop in a colleague to ask for clarification about a charge and upload missing receipts. Everything uses HTTPS along with TLS and certificates so data is encrypted between Digit’s services and at rest.

The original idea for Digits came from a problem that co-founders Wayne Chang and Jeff Seibert faced themselves when building Crashlytics. As they explained previously, their focus as entrepreneurs was on solving technical challenges, not on the operational side of running a business.

Many entrepreneurs also find themselves in this same space. They’re trying to solve a problem or crack a tough engineering puzzle, but instead have to redirect their time and resources to spreadsheets, financial reports, transaction records and other paperwork required to actually run the business.

“Startups and small businesses today simply don’t have the resources to manage their finances internally. Most of them still settle for spreadsheets, and the lucky ones work on an hourly basis with external accountants,” explains Seibert. “As a result, their accounting itself is seen as a cost-center, and they pay for little beyond the basic monthly financial statements — Profit & Loss, Balance Sheet, etc. By the time those statements are delivered — weeks after the end of each month — they’re already out of date,” he said.

That means things businesses need — like updates, one-off reports and new budgets — can require additional costs and longer wait times, so they get skipped.

The COVID-19 pandemic has put even more pressure on small businesses, many of which are now struggling to even survive. As a result, Digits has decided to launch the product for free to those who sign up — not a free trial, but actually free. It plans to later charge for additional products and paid upgrades to support its own business.

Digits is able to make this offer because of its now-expanded venture funding.

Already, the company had raised $10.5 million in Series A funding in a round led by Benchmark. That round had included a sizable 72 angel investors as well, including founders and CEOs from companies like Box, GitHub, Tinder, Twitch, StitchFix, SoFi and several others — entrepreneurs with an understanding of the problems Digits is aiming to solve.

Today, Digits is announcing an additional $22 million led by Jessica Verrilli at GV, who also now joins Digits’ board alongside Benchmark’s Peter Fenton. (Benchmark also participated in the new round).

“Jeff and Wayne are masterful at creating intuitive, high-utility products from complicated data,” said Verrilli about the GV investment. “I saw this up close with Crashlytics and Twitter, and I’m thrilled to partner with them on Digits as they reimagine financial software for startups,” she added.

The startup, now a team of 18 and hiring, was already offering its software solution to a group of customers ahead of today’s public launch, who effectively operated as beta testers allowing Digits to refine its product. Digits isn’t able to share its customer names, for the most part. However, it noted that Coda was one of early adopters and provided valuable feedback.

It also has over 10,000 companies who joined its waitlist over the past two years who are now being let in.

At the time of its Series A, Digits saw more than $1.5 billion in transaction value flowing across its production systems. That number has since grown to $8 billion.

The software is free starting today for U.S.-based small businesses. The company plans to add support for international markets later this year.

Powered by WPeMatico

A startup that has framed itself as an Instagram for websites is now squaring up against Shopify as it nabs new funding from Google’s venture capital arm.

Brooklyn-based Universe has just closed a $10 million Series A from GV. The funding round was well in the works before the COVID-19 pandemic took hold stateside; nevertheless, CEO Joseph Cohen definitely sounded relieved to have everything signed.

“Hopefully, it’ll take some weight off their shoulders that may have been there otherwise,” said GV general partner M.G. Siegler, who led the deal and is taking a seat on their board.

When the team launched out of YC two years ago, the initial aim was to be the go-to short link for young people and creatives to stick in their Instagram bios. The mobile app allowed users to create very basic landing pages, allowing them to type up some text, toss up photos and arrange their creation across a couple of web pages.

As the startup matures and looks to home in on a more robust business model, they’re now looking to build an incredibly low-friction commerce platform. Users can add a shopping “block” to their site, add a photo, description and price and then start accepting orders.

“We’ve gone from a landing page builder to a full-fledged website builder,” Cohen told TechCrunch in an interview.

Universe is going after what Cohen calls “very small businesses.” This could be an artist selling prints, a yoga instructor charging for Zoom classes or one of their latest customers, a farmer selling live bait. “These are people who don’t work at desks,” Cohen says.

Shopify has been one of the biggest tech success stories of the past several years, but Cohen sees weaknesses for Universe to capitalize on. Shopify is “complex and not mobile-first,” he says. Universe not only doesn’t require a developer to implement, it doesn’t seem to require someone that’s particularly tech-savvy.

The price of simplicity for the end user is a hefty cut for Universe. At launch, the company isn’t taking a percentage for the first $1,000 of a customer’s revenue, but will take a 10% slice thereafter, a number that’s notably multiples higher than the rates of competitors.

Cohen acknowledges that if a business succeeds, this can be a significant expense for them, one that might push them to another platform. He say that he wants to figure out a model that can help his startup “grow and scale” with their customers, but he didn’t offer up any details on what that might look like.

The team is still working with free and paid “pro” tiers that offer advanced features like analytics. Commerce features will be available for both tiers.

Universe has raised $17 million to date. Other investors include Javelin Venture Partners, General Catalyst and Greylock Partners.

We chatted with GV’s M.G. Siegler about closing this deal and how his role as an investor has shifted since the current crisis took hold. You can read that interview on Extra Crunch.

Powered by WPeMatico

The coronavirus pandemic has pushed entrepreneurs and investors into unknown territory.

Google’s GV just led a $10 million investment in Universe, a low-friction website builder that’s venturing into the world of commerce.

The investment was in the works before COVID-19 hit America in force, but things were finalized for the Brooklyn startup in late March. I chatted with M.G. Siegler, the general partner at GV (and former TechCrunch writer) who led the deal, about how the crisis was affecting his investment work and how he was balancing portfolio work with sourcing new deals.

This interview has edited for length and clarity.

TechCrunch: This deal sounds like it was in the works before pandemic concerns really hit America, but when you saw this situation arise, did it change your thinking about this deal at all?

M.G. Siegler: The reality is we’re still going to be continuing to look for interesting opportunities to invest in. History has shown that even during great financial turmoil, many companies are still being built, although it’s certainly not easy for anyone, given that we’re all stuck inside and trying to make things work. I think Universe is in an interesting spot; they have a tool that can potentially help some of these struggling businesses move online quicker and create commerce opportunities that they really need to think about given the current realities.

So there’s no thought that we shouldn’t do something just because of the current macro environment if we’re really passionate about it to begin with. Obviously, there’s varying degrees of that for different sectors, but I do think that Universe had been in a great position before this situation, and it seems like they have different opportunities now.

Powered by WPeMatico

SpinLaunch, a company that aims to turn the launch industry on its head with a wild new concept for getting to orbit, has raised a $35M round B to continue its quest. The team has yet to demonstrate their kinetic launch system, but this year will be the year that changes, they claim.

TechCrunch first reported on SpinLaunch’s ambitious plans in 2018, when the company raised its previous $35 million, which combined with $10M it raised prior to that and today’s round comes to a total of $80M. With that kind of money you might actually be able to build a space catapult.

The basic idea behind SpinLaunch’s approach is to get a craft out of the atmosphere using a “rotational acceleration method” that brings a craft to escape velocity without any rockets. While the company has been extremely tight-lipped about the details, one imagines a sort of giant rail gun curled into a spiral, from which payloads will emerge into the atmosphere at several thousand miles per hour — weather be damned.

Naturally there is no shortage of objections to this method, the most obvious of which is that going from an evacuated tube into the atmosphere at those speeds might be like firing the payload into a brick wall. It’s doubtful that SpinLaunch would have proceeded this far if it did not have a mitigation for this (such as the needle-like appearance of the concept craft) and other potential problems, but the secretive company has revealed little.

The time for broader publicity may soon be at hand, however: the funds will be used to build out its new headquarter and R&D facility in Long Beach, but also to complete its flight test facility at Spaceport America in New Mexico.

“Later this year, we aim to change the history of space launch with the completion of our first flight test mass accelerator at Spaceport America,” said founder and CEO Jonathan Yaney in a press release announcing the funding.

Lowering the cost of launch has been the focus of some of the most successful space startups out there, and SpinLaunch aims to leapfrog their cost savings by offering orbital access for under $500,000. First commercial launch is targeted for 2022, assuming the upcoming tests go well.

The funding round was led by previous investors Airbus Ventures, GV, and KPCB, as well as Catapult Ventures, Lauder Partners, John Doerr and Byers Family.

Powered by WPeMatico