Groupon

Auto Added by WPeMatico

Auto Added by WPeMatico

Weezy — an on-demand supermarket that delivers groceries in as fast as 15 minutes — has raised $20 million in a Series A funding led by New York-based venture capital fund Left Lane Capital. Also participating were U.K.-based fund DN Capital, earlier investors Heartcore Capital and angel investors, notably Chris Muhr, the Groupon founder.

Although the company hasn’t made mention of a later U.S. launch, the presence of U.S. investors would tend to suggest that. Weezy is reminiscent of Kozmo, the on-demand groceries business from the dot-com boom of the late ’90s. However, it differs from Postmates in that it doesn’t do pickups.

The cash injection will be used to expand its grocery delivery service across London and the broader UK, and open two fulfillment centers across London. Some 40 more U.K. sites are planned by the end of 2021 and it plans to add 50 new employees in the next four months.

Launched in July 2020, Weezy uses its own delivery people on pedal cycles or electric mopeds to deliver goods in less than 15 minutes on average. As well as working with wholesalers, it also sources groceries from independent bakers, butchers and markets.

It has pushed at an open door during the pandemic. In Q2 2020, half a million new shoppers joined the grocery delivery sector, which is now worth £14.3 billion in the U.K., according to research.

Kristof Van Beveren, co-founder and CEO of Weezy, said in a statement: “People are no longer happy to wait around for deliveries, and there is strong demand for a more efficient service.”

Weezy’s co-founders are Kristof Van Beveren and Alec Dent. Van Beveren is formerly from the consumer goods world at Procter & Gamble and McKinsey & Company, while Dent headed up operations at U.K. startup Drover and business development at BlaBlaCar.

Harley Miller, managing partner, Left Lane Capital, commented: “Weezy’s founding team have the right balance of drive, experience and temperament to lead in e-commerce innovation and convenience within the UK grocery market and beyond.”

Nenad Marovac, founder and managing partner, DN Capital, said: “Even before the pandemic, interest in online grocery shopping was on the rise. The first time I ordered from Weezy, my delivery arrived in seven minutes and I was hooked.”

Powered by WPeMatico

Adam Neumann, the co-founder and chief executive of the international real estate co-working startup WeWork has reportedly cashed out of more than $700 million from his company ahead of its initial public offering.

The size and timing of the payouts, made through a mix of stock sales and loans secured by his equity in the company, is unusual, considering that founders typically wait until after a company holds its public offering to liquidate their holdings.

Despite the loans and sales of stock, first reported by The Wall Street Journal, Neumann remains the single largest shareholder in the company.

According to the Journal’s reporting, Neumann has already set up a family office to invest the proceeds and begun to hire financial professionals to run it.

He’s also made significant investments in real estate in New York and San Francisco, including four homes in the greater New York metropolitan area, and a $21 million, 13,000-square-foot house in the Bay Area, complete with a guitar-shaped room (I guess a fiddle would be too on the nose). In all, Neumann reportedly spent $80 million on real estate.

Neumann has also invested in commercial real estate (the kind that WeWork leases to provide work space with more flexible leases for companies and entrepreneurs), including properties in San Jose, Calif. and New York. Indeed, four of Neumann’s properties are leased to WeWork — to the tune of several million dollars in rent. According to the Journal, Neumann will transfer those property holdings to a WeWork-controlled fund.

The WeWork chief executive has also invested in startups in recent years. He’s got an equity stake in seven companies: Hometalk, Intercure, EquityBee, Selina, Tunity, Feature.fm and Pins, according to CrunchBase.

The rewards that Neumann is reaping from the loans and stock sales are among the highest recorded by a private company executive. In recent years, Evan Spiegel sold $8 million in stock and borrowed $20 million from Snap before its 2017 public offering, and Slack Technologies chief executive Stewart Butterfield sold $3.2 million of stock before Slack’s public offering in June.

The only liquidation of stock and other payouts that have been disclosed that come close to Neumann’s payouts are the $300 million that Groupn co-founder Eric Lefkofsky sold before his company’s IPO and the over $100 million that Mark Pincus took off the table ahead of Zynga’s offering.

WeWork declined to comment for this article.

Powered by WPeMatico

Hot startup Superhuman has been getting some backlash, as often happens when someone notices the precise methodology that a startup is using to enable a core feature. We’re well into stage 2 now when, inevitably, the backlash itself gets backlash.

The nut of it is that people have been exposed to the idea that Superhuman tracks email you send and receive and gives you tools to help you manage it. They do it on your behalf, but without the permission of the recipient.

You can read a review of the service by Lucas Matney, who spent six months with it, here on TC.

The best thing about all of this defense against the backlash chatter coming in is that the backlash itself is really not specious at all. People are literally just pointing out what they do, which is track email. And it provides real, genuine value.

This isn’t a new idea. It’s done by every marketing platform worth a darn that uses email. Every single email that comes in from a BRAND has some sort of this stuff happening. As do all websites (including this one). People are just not used to it being applied to a consumer product as intimate as personal email, and that sort of in-your-face use of commerce-grade tracking is perking up ears.

A few years back a startup founder with a suite of productivity apps (not Superhuman) asked me about this cool new feature they were planning on shipping: email tracking for senders, built right in. Read receipts and action items and all kinds of cool-sounding stuff to make your life easier. He was asking what I thought of it, and whether Apple would have an issue with it if they shipped it on the store.

I told him it sounded like a great idea, but that I would be very cautions of actually rolling it out because it was impossible to get verification from the other side before you began tracking them. There was no opt-in.

I advised him to look at the way Apple handles it, where email tracking happens outside the body of the email in a sort of passive radar fashion. Instead of active “pings” using tracking pixels or other image-hosting tricks, you’re getting a lighter client-side data set to work from. It’s opt in on your side, and doesn’t extend to them.

I warned on it for the same reason that I opt out of services that route my work email through their own servers, I choose not to employ any tracking apps and set up my emails not to auto-display images. It’s not because I don’t want actionable insights, it’s because I am unable to obtain the permission of the people I send it to to begin tracking them.

Yeah, for sure, they’re already tracked 10 ways to Sunday by every spam email from Groupon to The Gap, but this is coming from me, an individual. It’s different, in my opinion, which is why people are reacting the way they are.

Flash forward and now we’ve got a very well-capitalized startup with this at the core of their business. It seems like the founders have thought a lot about this and have decided that this tracking is good and defensible. So it shouldn’t be a shock when it comes time to defend those choices.

If you’re a founder, I think that’s a core lesson: always be willing to die on whatever hill you’re building.

I don’t think that the chatter about the tracking feature of Superhuman is a case of people turning on a startup that has become successful. Superhuman is very new, but very buzzy. And, as I said above, the backlash mostly consists of people highlighting their marquee features in detail. I’d bet a lot of people became even more interested in what it’s doing reading the various and sundry tweets and posts about it, including a Big Profile post in the NYT that kicked off this latest round of discussion.

We’ve been covering Superhuman for a few years now, including detailed explanations of what they want to accomplish and what the origins of the product and team are. That’s pretty much our job — to make sure we see this stuff years before anyone else. (We even covered the last startup to use the name Superhuman for a productivity app.)

The tracking has come up in our stories, but I think that people are just more willing to be skeptical of this stuff given the way that the last couple of years have gone. This is something that we have found happening with a lot of privacy issues recently.

In fact, the most astute criticism of the way Superhuman uses tracking came in a post by designer Mike Davidson, who has spent a lot of time working on large systems that have dangerous, as well as exciting, potential. And that post is anything but a “drive-by” on the model. It’s a thoughtful critique that actually offers some possible solutions.

I do think they are trying to solve a real problem. But there are clearly components of the way that they implemented their key feature that have potential for abuse.

It is, and I do find it a bit amusing that I have to say this in twenty-nineteen, OK for people to want to discuss this and to examine the trade offs in a product that makes other people’s privacy choices for them. This isn’t backlash, this is discussion, and it’s good.

One of the reasons that we’ve gotten to a place where large platforms have been able to be mis-used to manipulate audiences at scale is that not enough people were listening to the conversations that were had about these possibilities early enough.

In context, it is very hard to argue that a genuine moment of thoughtfulness about any startup that has traction, raises significant capital and is aiming to have the most users possible see the world from its point of view is a bad thing.

Powered by WPeMatico

When serial entrepreneur Eric Lefkofsky grows a company, he puts the pedal to the metal. When in 2011 his last company, the Chicago-based coupons site Groupon, raised $950 million from investors, it was the largest amount raised by a startup, ever. It was just over three years old at the time, and it went public later that same year.

Lefkofsky seems to be stealing a page from the same playbook for his newest company, Tempus. The Chicago-based genomic testing and data analysis company was founded a little more than three years ago, yet it has already hired nearly 700 employees and raised more than $500 million — including through a new $200 million round that values the company at $3.1 billion.

According to the Chicago Tribune, that new valuation makes it — as Groupon once was — one of Chicago’s most highly valued privately held companies.

So why all the fuss? As the Tribune explains it, Tempus has built a platform to collect, structure and analyze the clinical data that’s often unorganized in electronic medical record systems. The company also generates genomic data by sequencing patient DNA and other information in its lab.

The goal is to help doctors create customized treatments for each individual patient, Lefkofsky tells the paper.

So far, it has partnered with numerous cancer treatment centers that are apparently giving Tempus human data from which to learn. Tempus is also generating data “in vitro,” as is another company we featured recently called Insitro, a drug development startup founded by famed AI researcher Daphne Koller. With Insitro, it is working on a liver disease treatment owing to a tie-up with Gilead, which has amassed related human data over the years from which Insitro can use to learn. As a complementary data source, Insitro, like Tempus, is trying to learn what the disease does in a “dish,” then determine if it can use what it observes using machine learning to predict what it sees in people.

Tempus hasn’t come up with any cancer-related cures yet, but Lefkofsky already says that Tempus wants to expand into diabetes and depression, too.

In the meantime, he tells Crain’s Chicago Business that Tempus is already generating “significant” revenue. “Our oldest partners, have, in most cases, now expanded to different subgroups (of cancer). What we’re doing is working.”

Investors in the latest round include Baillie Gifford; Revolution Growth; New Enterprise Associates; funds and accounts managed by T. Rowe Price; Novo Holdings; and the investment management company Franklin Templeton.

Powered by WPeMatico

As we swing into the summer tourist season, a company poised to capitalise on that has raised a huge round of funding. GetYourGuide — a Berlin startup that has built a popular marketplace for people to discover and book sightseeing tours, tickets for attractions and other experiences around the world — is today announcing that it has picked up $484 million, a Series E round of funding that will catapult its valuation above the $1 billion mark.

The funding is a milestone for a couple of reasons. GetYourGuide says it is the highest-ever round of funding for a company in the area of “travel experiences” (tours and other activities) — a market estimated to be worth $150 billion this year and rising to $183 billion in 2020. And this Series E is also one of the biggest-ever growth rounds for any European startup, period.

The company has now sold 25 million tickets for tours, attractions and other experiences, with a current catalog of some 50,000 experiences on offer. That’s a sign of strong growth: in 2017 it sold 10 million tickets, and its last reported catalog number was 35,000. It will be using the funding to build more of its own “Originals” tour experiences — which have now passed the 40,000 tickets sold mark — as well as to build up more activities in Asia and the U.S., two fast-growing markets for the startup.

The funding is being led by SoftBank, via its Vision Fund, with Temasek, Lakestar, Heartcore Capital (formerly Sunstone Capital) and Swisscanto Invest among others also participating. (Swisscanto is part of Zürcher Kantonalbank: GetYourGuide was originally founded in Zurich, where the founders had studied, and it still runs some R&D operations there.) The company has now raised well over $600 million.

It’s notable how SoftBank — which is on the hunt for interesting opportunities to invest its $100 billion superfund — has been stepping up a gear in Germany to tap into some of the bigger tech players that have emerged out of that market, which today is the biggest in Europe. Other big plays have included €460 million into Auto1 and €900 million into payments provider Wirecard. Other companies it has backed, such as hotel company Oyo out of India, are using its funding to break into Europe (and buy German companies in the process).

There had been reports over the last several months that GetYouGuide was in the process of raising anywhere between $300 million and more than $500 million. In late April, we were told by sources that the round hadn’t yet closed, and that numbers published in the media up to then had been inaccurate, even as we nailed down that SoftBank was indeed involved in the round.

The valuation in this round is not being disclosed, but CEO Johannes Reck (who co-founded the app with Martin Sieber, Pascal Mathis, Tobias Rein and Tao Tao) said in an interview with TechCrunch that it was definitely “now a unicorn” — meaning that its valuation had passed the $1 billion mark. For additional context, the rumor last month was that GetYourGuide’s valuation was up to €1.6 billion ($1.78 billion), but I have not been able to get firm confirmation of that number.

GetYourGuide’s growth — and investor interest in it — has closely followed the rise of new platforms like Airbnb that have changed the face of how we travel, and what we do when we get somewhere. We have moved far beyond the days of visiting a travel agent that books everything, from flight to hotel to all your activities, as you sit on the other side of a desk from her or him. Now with the tap of a finger or the click of a mouse, we have thousands of choices.

Within that, GetYourGuide thinks that it has jumped on an interesting opportunity to rethink the activity aspect of tourism. Tour packages and other highly organized travel experiences are often associated with older people, or those with families — essentially people who need more predictability when they are not at home.

Reck noted that the earliest users of GetYourGuide in 2010 were precisely those people — or at least those who were more inclined to use digital platforms to begin with: the demographic, he said, was 40-50 year olds, most likely travelling with family.

That is one thing that has really started to change, in no small part because of GetYourGuide itself. Making the experience of booking experiences mobile-friendly, GetYourGuide has played into the culture of doing and showing, which has propelled the rise of social media.

“They want to do things, to have something to post on Instagram,” he said. The average age of a GetYourGuide user now, he said, is 25-40.

This has even evolved into what GetYourGuide provides to users. “At some point, staff in Asia had the idea of crafting a ‘GetYourGuide Instagram Tour of Bali.’ That really took off, and now this is the number-one tour booked in the region.” It has since expanded the concept to 50 destinations.

Not by coincidence, today the company is also announcing that Ameet Ranadive is joining as the company’s first chief product officer. Ranadive comes from Instagram, where he led the Well-being product team (the company’s health and safety team). He’d also been VP and GM of Revenue Product at Twitter. Nils Chrestin is also coming on as CFO, having recently been at Rocket Internet-incubated Global Fashion Group.

That has also led GetYourGuide to conclude it has a ways to go to continue developing its model and scope further, expanding into longer sightseeing excursions, beyond one or two-hour tours into day trips and even overnight experiences.

As it continues to play around with some of these offerings, it’s also increasingly taking a more direct role in the branding and the provision of the content. Initially, all tickets and tours were posted on GetYourGuide by third parties. Now, GetYourGuide is building more of what Reck calls “Originals” — which it might develop in partnership with others but ultimately handles as its own first-party content. (That Instagram tour was one of those Originals.)

It’s worth noting that others are closing in on the same “experiences” model that forms the core of GetYourGuide’s business: Airbnb, to diversify how it makes revenues and to extend its touchpoints with guests beyond basic accommodation bookings, has also started to sell experiences. Meanwhile, daily deals pioneer Groupon has also positioned itself as a destination for purchasing “experiences” as a way to offset declines in other areas of its business. Similarly, travel portals that sell plane tickets regularly default to pushing more activities on you.

Reck pointed out that the area of business where GetYourGuide is active is becoming increasingly attractive to these players as other aspects of the travel industry become increasingly commoditised. Indeed, you can visit dozens of sites to compare pricing on plane tickets, and if you are flexible, pick up even more of a bargain at the last minute. And the rise of multiple Airbnb-style platforms offering private accommodation has made competition among those supplying those platforms — as well as hotels — increasingly fierce.

All of that leaves experiences — for now at least — as the place where these companies can differentiate themselves from the pack. Reck believes that focusing on this, however, means you just do it much better than companies that have added experiences on to a platform that is not a native destination for discovering or buying that kind of content or product. (That doesn’t mean there aren’t others natively tackling “experiences” from the world of startups. Klook is one also funded by SoftBank.)

“Consumers, especially millennials, are spending an increasing portion of their disposable income on travel experiences. We believe GetYourGuide is leading this seismic shift by consolidating the fragmented global supply base of tour operators and modernizing access for travelers globally,” said Ted Fike, partner at SoftBank Investment Advisers, in a statement. “This combination creates powerful network effects for their business that is fueling their strong growth. We are excited to partner with their passionate and talented leadership team.” Fike is joining the board with this round.

Powered by WPeMatico

In Silicon Valley, investors don’t expect their portfolio companies to be profitable. “Blitzscaling: The Lightning-Fast Path to Building Massively Valuable Companies,” a bible for founders, instead calls for heavy spending on growth to scale in an Amazon -like fashion.

As for Wall Street, it’s shown an affinity for stock in Jeff Bezos’ business, despite the many years it spent navigating a path to profitability, as well as other money-losing endeavors. Why? Because it too is far less concerned with profitability than market opportunity.

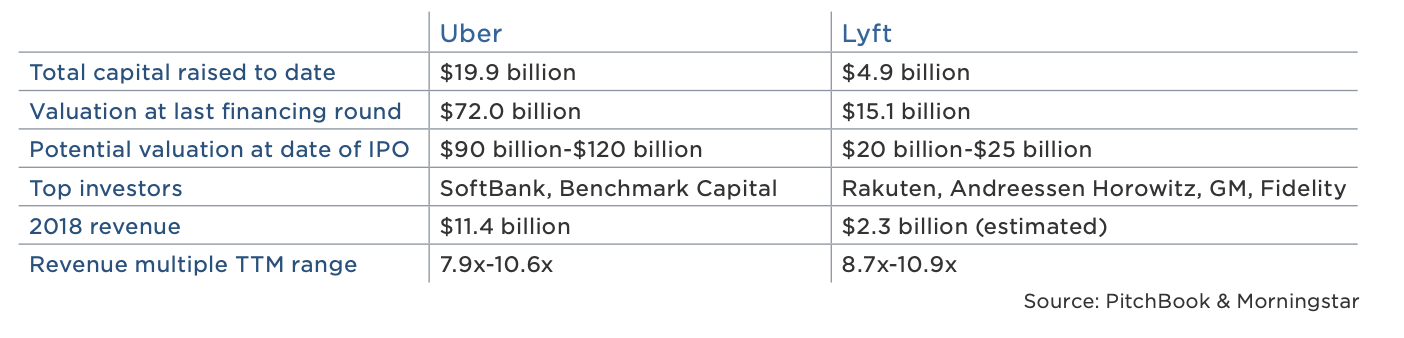

Lyft, a ride-hailing company expected to go public this week, is not profitable. It posted losses of $911 million in 2018, a statistic that will make it the biggest loser amongst U.S. startups to have gone public, according to data collected by The Wall Street Journal. On the other hand, Lyft’s $2.2 billion in 2018 revenue places it atop the list of largest annual revenues for a pre-IPO business, trailing behind only Facebook and Google in that category.

Wall Street, in short, is betting on Lyft’s revenue growth, assuming it will narrow its loses and reach profitability… eventually.

Lyft, losses notwithstanding, is growing rapidly and Wall Street is paying attention. On the second day of its road show, reports emerged that its IPO was already oversubscribed. As a result, Lyft is said to have upped the cost of its stock, with new plans to raise more than $2 billion at a valuation upwards of $25 billion. That represents a revenue multiple of more than 11x, a step up multiple of more than 1.6x from its most recent private valuation of $15.1 billion and, of course, Wall Street’s insatiable desire for unicorns, profitable or not.

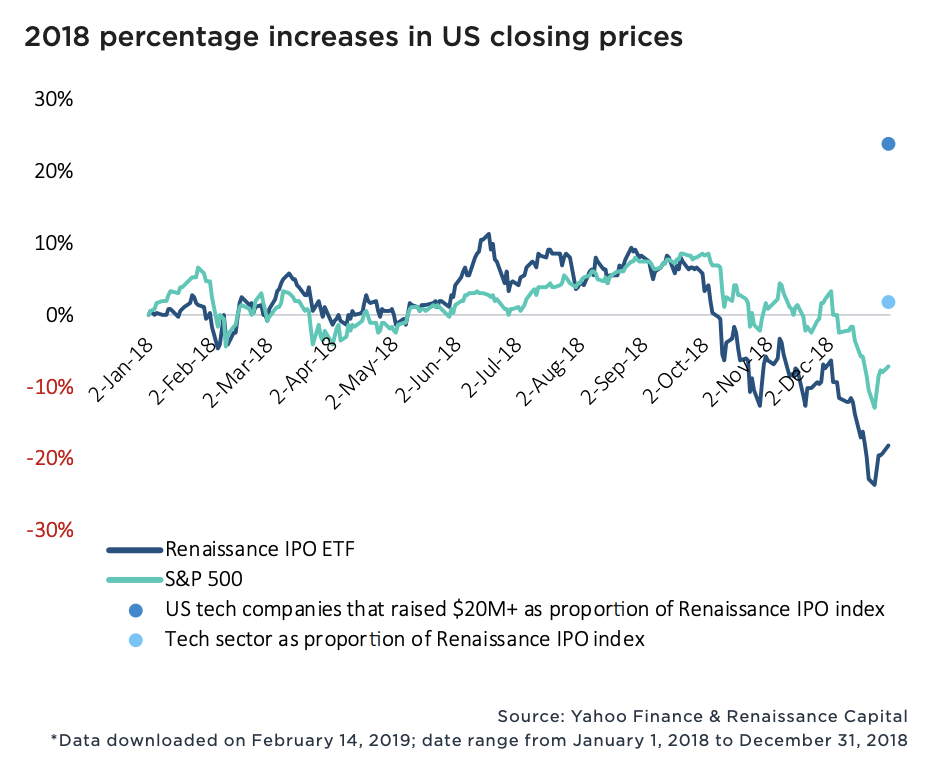

New data from PitchBook exploring the performance of billion-dollar-plus VC exits confirms Wall Street’s leniency toward unprofitable tech companies. Sixty-four percent of the 100+ companies valued at more than $1 billion to complete a VC-backed IPO since 2010 were unprofitable, and in 2018, money-losing startups actually fared better on the stock exchange than money-earning businesses. Moreover, U.S. tech companies that had raised more than $20 million traded up nearly 25 percent of 2018, while the S&P 500 technology sector posted flat returns.

Wall Street is still adapting to the rapid growth of the tech industry; public markets investors, therefore, are willing to deal with negative to minimal cash flows for, well, a very long time.

There’s no doubt Lyft and its much larger competitor, Uber, will go public at monstrous valuations. The two IPOs, set to create a whole bunch of millionaires and return a number of venture capital funds, will provide Silicon Valley a lesson in Wall Street’s tolerance for outsized exits.

Much like a seed-stage investor must bet on a founder’s vision, Wall Street, given a choice of several unprofitable businesses, has to bet on potential market value. Fortunately, this strategy can work quite well. Take Floodgate, for example. The seed fund invested a small amount of capital in Lyft when it was still a quirky idea for ridesharing called Zimride. Now, it boasts shares worth more than $100 million. I’m sure early shareholders in Amazon — which went public as a money-losing company in 1997 — are pretty happy, too.

Ultimately, Wall Street’s appetite for unicorns like Lyft is a result of the shortage of VC-backed IPOs. In 2006, it was the norm for a company to make its stock market debut at 7.9 years old, per PitchBook. In 2018, companies waited until the ripe age of 10.9 years, causing a significant slowdown in big liquidity events and stock sales.

Fund sizes, however, have grown larger and the proliferation of unicorns continues at unforeseen rates. That may mean, eventually, an influx of publicly shared unicorn stock. If that’s the case, might Wall Street start asking more of these startups? At the very least, public market investors, please don’t be swayed by WeWork‘s eventual stock offering and its “community adjusted EBITDA.” Silicon Valley’s pixie dust can’t be that potent.

Powered by WPeMatico

The founders of PayPal and its employees have produced many highly successful companies over the years. Often referred to as the “PayPal Mafia” because they’ve had such an impact on the startup ecosystem, this serial entrepreneur success story is reminiscent of a similar phenomenon taking place in Latin America. The story starts with another U.S. company, Groupon. Read More

The founders of PayPal and its employees have produced many highly successful companies over the years. Often referred to as the “PayPal Mafia” because they’ve had such an impact on the startup ecosystem, this serial entrepreneur success story is reminiscent of a similar phenomenon taking place in Latin America. The story starts with another U.S. company, Groupon. Read More

Powered by WPeMatico

The rise was like a tech startup fairytale. Within three years of founding, this unicorn company had raised more than $1 billion in venture capital — closing an astonishing $950 million in its final private round at a nearly $5 billion valuation. Revenue growth was skyrocketing from $30 million in year two to $713 million in year three and a run-rate of $2.6 billion in year four. Read More

The rise was like a tech startup fairytale. Within three years of founding, this unicorn company had raised more than $1 billion in venture capital — closing an astonishing $950 million in its final private round at a nearly $5 billion valuation. Revenue growth was skyrocketing from $30 million in year two to $713 million in year three and a run-rate of $2.6 billion in year four. Read More

Powered by WPeMatico

It’s a tough world out there for on-demand startups — confusion around the W2 versus 1099 conversation, tough margins and customer service are but a few of the initial obstacles for these companies. Add in the necessity of huge amounts of up-front capital and it’s an uphill battle at best. But trust me, the on-demand economy will survive and eventually prevail, and 2016… Read More

It’s a tough world out there for on-demand startups — confusion around the W2 versus 1099 conversation, tough margins and customer service are but a few of the initial obstacles for these companies. Add in the necessity of huge amounts of up-front capital and it’s an uphill battle at best. But trust me, the on-demand economy will survive and eventually prevail, and 2016… Read More

Powered by WPeMatico

After seeing big and small competitors collapsing or withdrawing altogether from the race, Groupon still enjoys an undisputed leadership in the deal space. However, with slow growth in North America, and no growth at all in the international markets, the once fastest-growing company in history is having a hard time meeting the growth expectations of public markets. Read More

After seeing big and small competitors collapsing or withdrawing altogether from the race, Groupon still enjoys an undisputed leadership in the deal space. However, with slow growth in North America, and no growth at all in the international markets, the once fastest-growing company in history is having a hard time meeting the growth expectations of public markets. Read More

Powered by WPeMatico