ggv capital

Auto Added by WPeMatico

Auto Added by WPeMatico

As expected, BigCommerce has filed to go public. The Austin, Texas, based e-commerce company raised over $200 million while private. The company’s IPO filing lists a $100 million placeholder figure for its IPO raise, giving us directional indication that this IPO will be in the lower, and not upper, nine-figure range.

BigCommerce, similar to public market darling Shopify, provides e-commerce services to merchants. Given how enamored public investors are with its Canadian rival, the timing of BigCommerce’s debut is utterly unsurprising and is prima facie intelligent.

Of course, we’ll know more when it prices. Today, however, the timing appears fortuitous.

BigCommerce is a SaaS business, meaning that it sells a digital service for a recurring payment. For more on how it derives revenue from customers, head here. For our purposes what matters is that public investors will classify it along with a very popular — today’s trading notwithstanding — market segment.

Starting with broad strokes, here’s how the company performed in 2019 compared to 2018, and Q1 2020 in contrast to Q1 2019:

BigCommerce didn’t grow too quickly in 2019, but its Q1 2020 expansion pace is much better. BigCommerce will file an S-1/A with more information in Q2 2020, we expect; it can’t go public without sharing more about its recent financial performance.

If the company’s revenue growth acceleration continues in the most recent period — bearing in mind that e-commerce as a segment has proven attractive to many businesses during the COVID-19 pandemic — BigCommerce’s IPO timing would appear even more intelligent than it did at first blush. Investors love growth acceleration.

Moving from revenue growth to revenue quality, BigCommerce’s Q1 2020 gross margins came in at 77.5%, a solid SaaS result. In Q1 2019 its gross margin was 76.8%, a slightly worse figure. Still, improving gross margins are popular as they indicate that future cash flows will grow at a faster clip than revenues, all else held equal.

In 2018 BigCommerce lost $38.9 million on a GAAP basis. Its net loss expanded modestly to $42.6 million in 2020, a larger dollar figure in gross terms, but a slimmer percent of its yearly top line. You can read those results however you’d like. In Q1 2020, however, things got better, as the company’s GAAP net loss fell to $4 million from its year-ago Q1 result of $10.5 million.

The BigCommerce big commerce business is growing more slowly than I had anticipated, but its overall operational health is better than I expected.

A few other notes, before we tear deeper into its S-1 filing tomorrow morning. BigCommerce’s adjusted EBITDA, a metric that gives a distorted, partial view of a company’s profitability, improved along similar lines to its net income, falling from -$9.2 million in Q1 2019 to -$5.7 million in Q1 2020.

The company’s cash flow is, akin to its adjusted EBITDA, worse than its net loss figures would have you guess. BigCommerce’s operating activities consumed $10 million in Q1 2020, an improvement from its Q1 2019 operating cash burn of $11.1 million.

The company is further in debt than many SaaS companies, but not so far as to be a problem. BigCommerce’s long-term debt, net of its current portion, was just over $69 million at the end of Q1 2020. It’s not a nice figure, per se, but it is one small enough that a good IPO haul could sharply reduce while still providing good amounts of working capital for the business.

Investors listed in its IPO document include Revolution, General Catalyst, GGV Capital, and SoftBank.

Powered by WPeMatico

Despite the rapid growth of e-commerce in India, Southeast Asia and other emerging markets, the vast majority of retail transactions there still happen offline in small stores that also serve as neighborhood hubs.

The central role these stores play in their communities led GGV Capital to develop what the firm refers to as its mom-and-pop shop investment thesis. This means backing startups that help small retailers digitize operations, tap into better supply chains and serve as delivery points in markets where logistics and online payment infrastructures are still developing. In turn, GGV’s managing partners believe this will lay the groundwork for stronger e-commerce growth.

Companies that GGV has already invested in under this thesis include B2B e-commerce platform Udaan and Telio, bookkeeping app KhataBook and social commerce startup Shihuituan (also called Nice Tuan) in China.

GGV managing partner Hans Tung says the mom-and-pop shop thesis means looking at consumers’ shopping habits across countries and understanding why they are different from a historical and social perspective. During his career, Tung has observed e-commerce develop in markets including the United States, China, Japan, Taiwan, India, Southeast Asia and Latin America. Offline shopping habits, population density, transportation infrastructure and credit card penetration all played a factor in how e-commerce evolved in each of those places.

“You realize e-commerce doesn’t exist in a vacuum. It exists as a substitute for what is happening in the offline world,” he says. “Mobile payment doesn’t happen in a vacuum. It just fulfills the same needs with a different method. It was a substitution for what was happening in the offline world with credit card and debit card penetration.”

Powered by WPeMatico

Airbnb has well and truly disrupted the world of travel accommodation, changing the conversation not just around how people discover and book places to stay, but what they expect when they get there, and what they expect to pay. Today, one of the startups riding that wave is announcing a significant round of funding to fuel its own contribution to the marketplace.

Domio, a startup that designs and then rents out apart-hotels with kitchens and other full-home experiences, has raised $100 million ($50 million in equity and $50 million in debt) to expand its business in the U.S. and globally to 25 markets by next year, up from 12 today. Its target customers are millennials traveling in groups or families swayed by the size and scope of the accommodation — typically five times bigger than the average hotel room — as well as the price, which is on average 25% cheaper than a hotel room.

The Series B, which actually closed in August of this year, was led by GGV Capital, with participation from Eldridge Industries, 3L Capital, Tribeca Venture Partners, SoftBank NY, Tenaya Capital and Upper90. Upper90 also led the debt round, which will be used to lease and set up new properties.

Domio is not disclosing its valuation, but Jay Roberts, the founder and CEO, said in an interview that it’s a “huge upround” and around 50x the valuation it had in its seed round and that the company has tripled its revenues in the last year. Prior to this, Domio had only raised around $17 million, according to data from PitchBook.

For some comparisons, Sonder — another company that rents out serviced apartments to the kind of travelers who have a taste for boutique hotels — earlier this year raised $225 million at a valuation north of $1 billion. Others like Guesty, which are building platforms for others to list and manage their apartments on platforms like Airbnb, recently raised $35 million with a valuation likely in the range of $180 million to $200 million. Airbnb is estimated to be valued around $31 billion.

Domio plays in an interesting corner of the market. For starters, it focuses its accommodations at many of the same demographics as Airbnb. But where Airbnb offers a veritable hodgepodge of rooms and homes — some are people’s homes, some are vacation places, some never had and never will have a private occupant, and across all those the range of quality varies wildly — Domio offers predictability and consistency with its (possibly more anodyne) inventory.

“We are competing with amateur hosts on Airbnb,” said Roberts, who previously worked in real estate investment banking. “This is the next step, a modern brand, the next Marriott but with a more tech-powered brain and operating model.” These are not to be confused with something like Hilton’s Homewood Suites, Roberts stressed to me. He referred to Homewood as “a soulless hotel chain.”

“Domio is the anti-hotel chain,” he added.

Roberts is also quick to describe how Domio is not a real estate company as much as it is a tech-powered business. For starters, it uses quant-style algorithms that it’s built in-house to identify regions where it wants to build out its business, basing it not just on what consumers are searching for, but also weather patterns, economic indicators and other factors. After identifying a city or other location, it works on securing properties.

It typically sets up its accommodations in newer or completely new buildings, where developers — at least up to now — are not usually constructing with short-term rentals in mind. Instead, they are considering an option like Domio as an alternative to selling as condominiums or apartments, something that might come up if they are sensing that there is a softening in the market. “We typically have 75%-78% occupancy,” Roberts said. He added that hotels on average have occupancy rates in the high 60% nationally.

As Domio lengthens its track record — its 12 U.S. markets include Miami, Los Angeles, Philadelphia and Phoenix — Roberts says that they’re getting a more select seat at the table in conversations.

“Investors are starting to go out to buy properties on our behalf and lease them to us,” he said. This gives the startup a much more favorable rate and terms on those deals. “The next step is that Domio will manage these directly.” The most recent property it signed, he noted, includes a Whole Foods at the ground level, and a gym.

Using technology to identify where to grow is not the only area where tech plays a role. Roberts said that the company is now working on an app — yet to be released — that will be the epicenter of how guests interact to book places and manage their experience once there.

“Everything you can do by speaking to a human in a traditional hotel you will be able to do with the Domio app,” he said. That will include ordering room service, getting more towels, booking experiences and getting restaurant recommendations. “You can book your Uber through the Domio app, or sync your Spotify account to play music in the apartment.

Ans there are plans to extend the retail experience using the app. Roberts says it will be a “shoppable” experience where, if you like a sofa or piece of art in the place where you’re staying, you can order it for your own home. You can even order the same wallpaper that’s been designed to decorate Domio apartments.

Although Airbnb has grown to be nearly as ubiquitous as hotels (and perhaps even more prominent, depending on who you are talking to), the wider travel and accommodation market is still ripe for the taking, estimated to reach $171 billion by 2023 and the highest growth sector in the travel industry.

“Airbnb has taught us that hotels are not the only place to stay,” said Hans Tung, GGV’s managing partner. “Domio is capitalizing on the global shift in short-term travel and the consumer demand for branded experiences. From my travels around the world, there is a large, underserved audience — millennials, families, business teams — who prefer the combined benefits of an apartment and hotel in a single branded experience.”

I mentioned to Roberts that the leasing model reminded me a little of WeWork, which itself does not own the property it curates and turns into office space for its tenants. (The SoftBank investor connection is interesting in that regard.) Roberts was very quick to say that it’s not the same kind of business, even if both are based around leased property re-rented out to tenants.

“One of the things we liked about Domio is that is very capital-efficient,” said Tung, “focusing on the model and payback period. The short-term nature of customer stays and the combination of experience/price required to maintain loyal customers are natural enforcers of efficient unit economics.”

“For GGV, Domio stands out in two ways,” he continued. “First, CEO Jay Roberts and the Domio team’s emphasis on execution is impressive, with expansion into 12 cities in just three years. They have the right combination of vision, speed and agility. Domio’s model can readily tap into the global opportunity as they have ambition to scale to new markets. The global travel and tourism spend is $2.8 trillion with 5 billion annual tourists. Global travelers like having the flexibility and convenience of both an apartment and hotel — with Domio they can have both.”

Powered by WPeMatico

Chinese autonomous air mobility company EHang has filed with the SEC the paperwork required to go public in the U.S. on the Nasdaq exchange, with a $100 million initial public offering. The company, which has been flying demonstration flights with passengers on board for a while now, is gearing up to launch its first commercial service in Guangzhou after getting approval from local and national regulators to deploy its drones in the area.

At launch, EHang will be using its two-seater vertical take-off and landing craft (VTOL), which has room for two passengers on board. EHang doesn’t just build the aircraft, though — its goal is to build full, multi-aircraft (as many as “thousands,” according to Forbes) autonomous transportation networks that it hopes will serve to alleviate and avoid congested ground traffic. Guangzhou, with an estimated population of more than 13 million, suffers from considerable traffic.

EHang is also building out logistics and cargo transportation capabilities as well as passenger services. The company believes it can offer short, designated cross-city transportation that can cut down on time by as much as 40 to 60%, and once it achieves scale, it also says that costs have the potential to be reduced by as much as 50%.

Founded in 2014, EHang last announced funding in 2015, when it raised $42 million in a Series B round led by GP Capital, with GGV Capital, ZhenFund, Lebox Capital, OFC and PreAngel also participating.

Powered by WPeMatico

Even as tens of millions of Indians have come online for the first time in recent years, most businesses in the nation remain offline. They continue to rely on long notebooks to keep a log of their financial transactions. A nine-month old startup which is digitizing the bookkeeping and allowing merchants to accept online payments just raised a significant amount of capital.

Khatabook, a Bangalore-based startup, said on Tuesday it has raised $25 million in a new financing round. The Series A round for the startup was funded by GGV Capital, Partners of DST Global, RTP Ventures, Sequoia India, Tencent, and Y Combinator. A clutch of high-profile angel investors including Amrish Rau, Anand Chandrasekharan, Deep Nishar, Gokul Rajaram, Jitendra Gupta, Kunal Bahl, and Kunal Shah also participated in the round. The startup has raised $29 million to date.

Khatabook operates an eponymous Android app that allows small and medium businesses to keep a log of their financial transactions and accept payments online. The app, which was launched on Google Play Store in December last year, has amassed 5 million merchants from more than 3,000 cities, towns, and villages in India, Ravish Naresh, cofounder and CEO of Khatabook told TechCrunch in an interview this week.

The app, which remains free of charge, was used to process transactions worth more than $3 billion in August, said Naresh. Most merchants in developing markets are not online currently. They continue to rely on logging their financial transactions — credit, for instance — on notebooks. As you can imagine, this methodology is not structured.

Even has Reliance Jio, a telecom operator launched by India’s richest man Mukesh Ambani, upended the Indian market and brought tens of millions of Indians online for the first time in last three years, most businesses in the country are still carrying out their operations without the use of any technology, said Naresh. “Could we build an app that makes it very easy for merchants to digitize their bookkeeping?” he said.

“As soon as we launched the app, we instantly started to go viral,” he said. For several months now, the startup is seeing 20% growth each month, he said. In six months, the app has helped businesses recover $5 billion in previously unpaid credits, Naresh claimed. Without any marketing, the app has also gained a significant number of users in Nepal, Pakistan, and Bangladesh, said Naresh.

“At Khatabook, we have taken early but significant steps towards leveraging this trend to digitize India’s shopkeepers. For most of our merchants, we are the first business software they’ve used in their entire life. And we will continue to build more India-first innovations to further enable the growth of what is still a largely untapped sector,” he said.

In a statement, Hans Tung, Managing Partner of GGV Capital, said, “as a global investor, we seek out founders who understand the local market and respond to growth opportunities with speed and agility – we certainly see this with the Khatabook team.”

Naresh, a cofounder of property startup Housing, said the startup will use the capital to build new features to serve merchants. In next 12 months, Khatabook will aim to add 25 million businesses, he said.

A growing number of startups in India are attempting to help businesses. OkCredit, which raised $67 million last month, serves 5 million merchants. IndiaMART, a 23-year-old B2B firm that went public this year, led a round in a startup called Vyapar last month that is addressing similar problems.

Powered by WPeMatico

Kong, the open core API management and life cycle management company previously known as Mashape, today announced that it has raised a $43 million Series C round led by Index Ventures. Previous investors Andreessen Horowitz and Charles River Ventures (CRV), as well as new investors GGV Capital and World Innovation Lab, also participated. With this round, Kong has now raised a total of $71 million.

The company’s CEO and co-founder Augusto Marietti tells me the company plans to use the funds to build out its service control platform. He likened this service to the “nervous system for an organization’s software architecture.”

Right now, Kong is just offering the first pieces of this, though. One area the company plans to especially focus on is security, in addition to its existing management tools, where Kong plans to add more machine learning capabilities over time, too. “It’s obviously a 10-year journey, but those two things — immunity with security and machine learning with [Kong] Brain — are really a 10-year journey of building an intelligent platform that can manage all the traffic in and out of an organization,” he said.

In addition, the company also plans to invest heavily in its expansion in both Europe and the Asia Pacific market. This also explains the addition of World Innovation Lab as an investor. The firm, after all, focuses heavily on connecting companies in the U.S. with partners in Asia — and especially Japan. As Marietti told me, the company is seeing a lot of demand in Japan and China right now, so it makes sense to capitalize on this, especially as the Chinese market is about to become more easily accessible for foreign companies.

Kong notes that it doubled its headcount in 2018 and now has more than 100 enterprise customers, including Yahoo! Japan, Ferrari, SoulCycle and WeWork.

It’s worth noting that while this is officially a Series C investment, Marietti is thinking of it more like a Series B round, given that the company went through a major pivot when it moved from being Mashape to its focus on Kong, which was already its most popular open-source tool.

“Modern software is now built in the cloud, with applications consuming other applications, service to service,” said Martin Casado, general partner at Andreessen Horowitz . “We’re at the tipping point of enterprise adoption of microservices architectures, and companies are turning to new open-source-based developer tools and platforms to fuel their next wave of innovation. Kong is uniquely suited to help enterprises as they make this shift by supporting an organization’s entire service architecture, from centralized or decentralized, monolith or microservices.”

Powered by WPeMatico

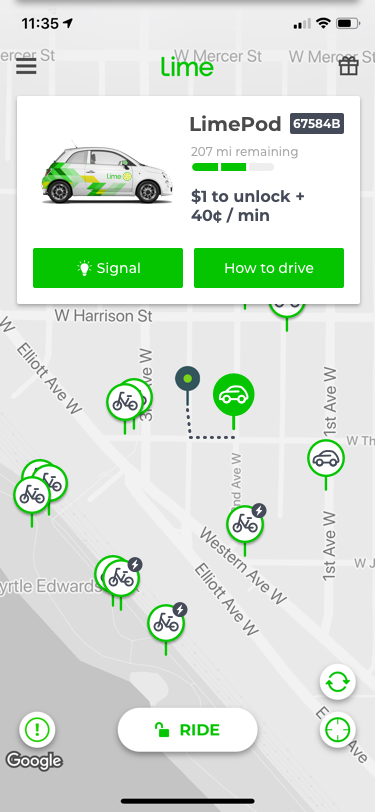

Lime, the well-funded startup known for its fleet of brightly colored dockless bicycles and electric scooters, has a new way for its customers to get around: cars.

Beginning this week, Lime users in Seattle will be able to reserve a “LimePod,” a Lime-branded 2018 Fiat 500, within the Lime mobile app. There will be 50 cars available to start as part of the company’s initial rollout. Lime plans to increase that number at the end of the month.

“LimePods, Lime’s car-sharing product line, a convenient, affordable, weather-resistant mobility solution for communities,” a spokesperson for Lime said in a statement provided to TechCrunch. “The ease of use of finding, unlocking, and paying for cars will be consistent with how riders use Lime scooters and e-bikes today.”

Lime will roll out 50 “LimePods” in Seattle this week.

Rides in the LimePod will cost $1 to unlock the car and 40 cents per minute of use. The company plans to unleash additional shareable cars in California early next year. Its scooters and e-bikes, for reference, are $1 to unlock and 15 cents per minute and regular pedal bikes are $1 to unlock and 5 cents per minute.

Founded in 2017 by Berkeley graduates Toby Sun and Brad Bao, the startup has raised a total of $467 million to date from GV, Andreessen Horowitz, IVP, Section 32, GGV Capital and more. Reports indicate that Lime is on the fundraising circuit now, targeting a $3 billion valuation, or nearly 3x its latest valuation.

LimePods will be available to order in the Lime mobile app.

The company is expanding rapidly, most recently releasing a fleet of e-scooters and bikes in Australia, as well as making notable hires on what seems like a weekly basis. In the last month, Lime has tapped Joe Kraus, a general partner at Alphabet’s venture arm GV and an existing member of the startup’s board of directors, as its first chief operating officer. Before that, it brought on Uber’s former chief business officer David Richter as its first-ever chief business officer and interim chief financial officer.

In July, the company hired Peter Dempster from ReachNow to lead the LimePod initiative out of Seattle.

Powered by WPeMatico

After four months “on the beach,” per his LinkedIn profile, Uber’s former global head of business and corporate development has a new gig. Lime has hired David Richter (pictured) as its first-ever chief business officer and interim chief financial officer.

Based in San Francisco, Richter will be overseeing the bike- and e-scooter-sharing startup’s business operations. Richter spent more than four years at Uber leading the ride-hailing giant’s global business development, corporate development, experiential marketing, autonomous vehicle alliances and brand relevance teams. He left in May after expressing frustrations with a series of departures in his group, according to The Information.

“As Lime continues to grow, David will bring in unparalleled expertise, particularly in the realm of business development and corporate partnerships, as well as in managing our overall business strategy and deal flow,” Lime co-founder and chief executive officer Toby Sun said in a statement. “His leadership experience, coupled with his keen understanding of the fast-moving shared mobility industry will be a huge advantage to our company as we continue to expand our global footprint.”

Lime is said to be completing the fundraising circuit right now, asking investors for a valuation north of $3 billion. The company, which entered the unicorn club in June, has raised a total of $467 million to date from GV, Andreessen Horowitz, IVP, Section 32, GGV Capital and more.

The company is using the buckets of capital to expand beyond bikes and scooters. Last Monday, rumors emerged that it was planning a brick-and-mortar push. The company confirmed that it would indeed build scooter “lifestyle stores” in major U.S. and international markets, starting with Santa Monica, Calif.

The next day on stage at the JD Power Automotive Roundtable, Lime announced its official foray into car-sharing. The company has since applied for a car-sharing permit in Seattle and plans to rent out small electric vehicles, which it’s calling “transit pods,” by the end of the year.

According to Axios, Lime plans to spend $50 million on the pods, which will cost $1 for consumers to start, plus an additional 40 cents per minute.

“You can expect electric vehicles to be an additional micro-mobility option for Lime riders to choose from within the Lime app soon,” a spokesperson for Lime said in a statement provided to TechCrunch. “More details on timing, specs of the vehicle, locations for the first rollout, etc. will be announced in the coming weeks.”

Lime launched in 2017 and has since recorded 11.5 million scooter and bike rides.

Powered by WPeMatico

Roy Raymond opened a little store called Victoria’s Secret, now one of the most popular lingerie businesses in the world, because he was embarrassed to buy lingerie for his wife in department stores.

The brand was founded on the premise that men needed a safe space to buy lingerie for women and women needed a larger variety of sexy, angelic bras and other intimates to wear for men.

But it’s 2018. Women, today, buy lingerie for themselves. They want to be comfortable and functional and beautiful all at the same time.

“[Victoria’s Secret] was always about the angel and the fantasy and a lot of push up and wire so women’s bodies could conform to a marketing campaign,” said Michelle Cordeiro Grant, founder and CEO of direct-to-consumer lingerie startup Lively, and a former Victoria’s Secret senior merchant. “Inspiring women to be Candice Swanepoel is not feasible for most women in the world. I wanted to create a product that is for women and by women.”

Recognizing the gap in the market for bras that don’t stab you with underwire, she built Lively. To date, the company has raised $15 million in venture capital funding, including a $6.5 million Series A investment from GGV Capital, NF Ventures and former Nautica CEO Harvey Sanders announced today.

“Previously, women had two rows of products in their drawer. One row they wanted to be seen in … and the other row was ones that were more basic and comfortable — but no nobody wanted to be seen in them.”

Though she began work on Lively before the #MeToo movement, Cordeiro Grant says it pushed the business forward in a big way. In the last year, the size-inclusive startup has seen 300 percent growth. What began as a direct-to-consumer company selling $35 bras and underwear has expanded to offer swimwear, activewear and loungewear. Physical retail is next.

“Women have been ready for a conversation like ours,” she said.

The startup is using the capital to open brick-and-mortar stores, a trend among other e-commerce businesses. The first of several stores in the pipeline, a 2,700-square-foot location, opened in New York City’s SoHo neighborhood this July. Stores in Chicago, Los Angeles and Dallas are also on the docket, as is a partnership with Nordstrom that will have Lively selling a limited distribution of intimates across 11 stores beginning next week.

Lively competes with several other brands of direct-to-consumer lingerie and activewear, including ThirdLove, AdoreMe, TomboyX and Outdoor Voices.

Powered by WPeMatico

Back in January, we told you about a young, Austin, Tex.-based startup that fights online disinformation for corporate customers. Turns out we weren’t alone in finding it interesting. The now four-year-old, 40-person outfit, New Knowledge, just sealed up $11 million in new funding led by the cross-border venture firm GGV Capital, with participation from Lux Capital. GGV had also participated in the company’s $1.9 million seed round.

We talked yesterday with co-founder and CEO Jonathon Morgan and the company’s director of research, Renee DiResta, to learn more about its work, which appears to be going well. (They say revenue has grown 1,000 percent over last year.) Our conversation, edited for length, follows.

TC: A lot of people associate coordinated manipulation by bad actors online with trying to disrupt elections here in the U.S. or with pro-government agendas elsewhere, but you’re working with companies that are also battling online propaganda. Who are some of them?

JM: Election interference is just the tip of the iceberg in terms of social media manipulation. Our customers are a little sensitive about being identified, but they are Fortune 100 companies in the entertainment industry, as well as consumer brands. We also have national security customers, though most of our business comes from the private sector.

TC: Renee, just a few weeks ago, you testified before the Senate Intelligence Committee about how social media platforms have enabled foreign-influence operations against the United States. What was that like?

RD: It was a great opportunity to educate the public on what happens and to speak directly to the senators about the need for government to be more proactive and to establish a deterrent strategy because [these disinformation campaigns] aren’t impacting just our elections but our society and American industry.

TC: How do companies typically get caught up in these similar practices?

JM: It’s pretty typical for consumer-facing brands, because they are so high-profile, to get involved in quasi-political conversations, whether or not they like it. Communities that know how to game the system will come after them over a pro-immigration stance for example. They mobilize and use the same black market social media content providers, the same tools and tactics that are used by Russia and Iran and other bad actors.

TC: In other words, this is about ideology, not financial gain.

JM: Where we see this more for financial gain is when it involves state intelligence agencies trying to undermine companies where they have nationalized an industry that competes with U.S. institutions like oil and gas and agriculture companies. You can see this is the promotion of anti-GMO narratives, for example. Agricultural tech in the U.S. is a big business, and on the fringes, there’s some debate about whether GMOs are safe to eat, even though the scientific community is clear that they’re completely safe.

Meanwhile, there are documented examples of groups aligned with Russian intelligence using purchased social media to circulate conspiracy theories and manipulate the public conversation about GMOs. They find a grain of truth in a scientific article, then misrepresent the findings through quasi-legitimate outlets, Facebook pages and Twitter accounts that are in turn amplified by social media automation.

TC: So you’re selling software-as-a-service that does what exactly?

JM: We have a SaaS product and a team of analysts who come out of the intelligence community and who help customers understand threats to their brand. It’s an AI-driven system that detects subtle social signs of manipulation across accounts. We then help the companies understand who is targeting them, why, and what they can do about it.

TC: Which is what?

JM: First, they can’t be blindsided. Many can’t tell the difference between real and manufactured public outcry, so they don’t even know about it when it’s happening. But there’s a pretty predictable set of tactics that are used to create false public perception. They plant a seed with accounts they control directly that can look quasi-legitimate. Then they amplify it via paid automation, and they target specific individuals who may have an interest in what they have to say. The thinking is that if they can manipulate these microinfluencers, they’ll amplify the message by sharing it with their followers. By then, you can’t put the cat back in the bag. You need to identify [these campaigns] when they’ve lit the match, but haven’t yet started a fire.

At the early stage, we can provide information to social media platforms to determine if what’s going on is acceptable within their policies. Longer term, we’re trying to find consensus between governments and also social media platforms themselves over what is and what isn’t acceptable — what’s aggressive conversation on these platforms and what’s out of bounds.

TC: How can you work with them when they can’t even decide on their own policies?

JM: First, different platforms are used for different reasons. You see peer-to-peer disinformation, where a small group of accounts drives a malicious narrative on Facebook, which can be problematic at the very local level. Twitter is the platform where media gets its pulse on what’s happening, so attacks launched on Twitter are much more likely to be made into mainstream opinion. There are also a lot of disinformation campaigns on Reddit, but those conversations are less likely to be elevated into a topic on CNN, even while they can shape the opinions of large numbers of avid users. Then there are the off-brand platforms like 4chan, where a lot of these campaigns are born. They are all susceptible in different ways.

The platforms have been very receptive. They take these campaigns much more seriously than when they first began looking at election integrity. But platforms are increasingly evolving from more open to more closed spaces, whether it’s WhatsApp groups or private Discord channels or private Facebook channels, and that’s making it harder for the platforms to observe. It’s also making it harder for outsiders who are interested in how these campaigns evolve.

Powered by WPeMatico