Getty-Images

Auto Added by WPeMatico

Auto Added by WPeMatico

The social video tool Promo.com just raised $16 million in a Series B round led by Getty Images, the company synonymous with stock imagery.

Brands, creators or whoever else might need some quick and dirty video content can search Promo.com for what they need, just like they would use a stock photography service. Getty offers its own library of stock videos as well, but Promo.com provides both the video clips and the tools for non-editors to craft a basic edit with a little bit of customization.

Brands can select an existing professional video clip from a library, plug in their own message and add a logo or custom audio. All that’s left is downloading the customized video and whisking it off to their social channels.

Mizrahi-Tefahot Bank, one of the largest banks in Israel, also participated in the Series B round through debt financing. Promo.com’s existing “strategic partnership” with Getty Images will deepen as part of the deal, giving the former company access to the latter’s expansive existing pool of video clips.

Image Credits: Screenshot/Promo.com

Of course, Promo.com isn’t the only show in town. Video creation platform Biteable raised $7 million of its own in December, and similarly allows companies to make bright, bite-sized video content for social. The super streamlined graphic design platform Canva also supports video editing with its own library of stock images. Vimeo offers its own video template service too, known as Vimeo Create, which grew out of the company’s acquisition of the AI-powered video editor Magisto.

Powered by WPeMatico

My big question for 2021, and the one that is on every startup’s mind, is how will a cataclysmic event such as a global pandemic show up in post-pandemic innovation? I think we’re in the early innings of seeing what “aha moments” have materialized into companies. And we won’t know the pandemic’s true impact on our psyches until the dust settles and we have an opportunity to reflect.

We do know it will be fascinating to watch. In 2020, innovators and investors were forced to stand still, and witness cracks, fractures and rubble in society in a way like never before. It was a humbling year that, for much of the tech community, was mostly spent inside, away and alone.

One reaction I’ve noticed so far — that isn’t necessarily new but comes with new weight — is a rush of innovation that focuses on reducing friction. Take trends like the rise of building in public or the unbundling of venture capital. Or remote work’s shift from enabling communication to now needing to enable passive and active collaboration. Apply the same idea to mental health, education and fitness. Heck, we’re even seeing people take the Y Combinator format and apply it to anything that makes sense, from helping operators turn into investors to helping employees try to turn their side gig into a full-time company.

While these movements didn’t begin because of the coronavirus, they all seem to have a huge, pandemic-sized asterisk next to it.

It would be easy to dismiss these movements as small and inconsequential. But, as my colleague and fellow Equity co-host Danny Crichton pointed out this week, “sometimes the most important changes in venture and startups more generally have come from lowering that last bit of friction to action.”

Lowering friction feels like the mantra with which we all need to enter 2021.

I already have hope that innovation will come from a more diverse set of people, whether it’s in a hacker house for undergraduate women or a student-founded service that matches undergraduate students to nonprofits. So, as we enter the new year — and bear with me here — I urge you to be optimistic.

The last year in tech hasn’t left people exhausted and hopeless, it’s left them energized and ready.

Maze, computer artwork. (Image Credits: Pasieka / Getty Images)

When SAP announced that Qualtrics was getting spun out in July, the full-circle moment made the Equity podcast crew jump to our mics with guesses around why. Now, months later, there’s a new S-1 filing, and more to color in. Alex Wilhelm broke down the Utah-based unicorn’s numbers, noting that it’s the second time Qualtrics has filed.

Will the second time be the charm that Qualtrics needs to actually go public this time around? I’ll let you make the call yourself once you sift through Alex’s analysis of the valuation and financials.

Blackboard Business Strategy Concept. (Image Credits: hanibaram / Getty Images)

If those three words in a single subhed elicit a certain reaction from you, Danny Crichton has a bone to pick with you. He wrote a piece this week about tech’s cynicism around anything new, underscoring how Miami’s future as a tech hub, Substack’s future as a replacement for traditional journalism and Clubhouse’s future as a social media disruptor have come under fire as expected:

The cynicism of immediate perfection is one of the strange dynamics of startups in 2020. There is this expectation that a startup, with one or a few founders and a couple of employees, is somehow going to build a perfect product on day one that mitigates any potential problem even before it becomes one. Maybe these startups are just getting popularized too early, and the people who understand early product are getting subsumed by the wider masses who don’t understand the evolution of products?

Danny’s argument is to give these companies a little more grace to execute on a vision they themselves are not even close to scratching the surface of. When it comes to holding specific decision-makers and businesses to a certain standard, I prefer a more fluid conversation. But I do agree that writing off a business because it hasn’t done everything correctly from the start can hurt progress. It’s easy to be grumpy, but why not choose to be an optimist? Tell me your optimistic bets by responding to this newsletter or tweeting me @nmasc_.

Skyline of downtown Miami, Florida looking toward the Brickell neighborhood on Biscayne Bay. Brickell is one of the largest financial districts in the United States and also has many high-rise residential condominium and apartment towers. (Image Credits: John Coletti / Getty Images)

Speaking of humbling moments and optimism, our own Sarah Perez wrote a piece this week about EarlyBird, an app that lets families and friends gift investments to children. While Acorns and Stash have similar offerings, EarlyBird is bringing a fresh UX play to financial literacy, freedom and education. There’s a ton of work left to be done, hurdles to deal with, and giant unicorns to compete with. EarlyBird, however, is only weeks old, so there’s much to watch out for.

VP Caleb Frankel, now EarlyBird COO, explained the early inspiration:

“This all started with a problem I experienced years ago when my beautiful baby niece was born. I found myself head over heels and spending hundreds and hundreds of dollars on just the most ridiculous stuff — pretty much just junk gifts,” he says. “I wanted to have a larger impact in her life and something that she could really use when she grew up.”

Image Credits: oxygen (opens in a new window) / Getty Images

Attending CES 2021? TechCrunch wants to meet your startup

Gift Guide: Last-minute subscriptions to keep the gifts going all year

Seen on Extra Crunch

How artificial intelligence will be used in 2021

On the diversity front, 2020 may prove a tipping point

The 2020 boom in climate tech SPACs

2021 will be a calmer year for semiconductors and chips (except for Intel)

Understanding Europe’s big push to rewrite the digital rulebook

Seen on TechCrunch

China lays out ‘rectification’ plan for Jack Ma’s fintech empire Ant

NSO used real people’s location data to pitch its contact-tracing tech, researchers say

India’s slow 2020 told through dollars and cents

An earnest review of a robotic cat pillow

The Equity pod put together a 2021 predictions episode (with Chris Gates, our producer, making a guest appearance on the mic as well!). We talk about IPO candidates, San Francisco and the future of drugs.

2020 brought several million downloads to the podcast, and we’re super thankful to all of y’ all for tuning in. This year will be even bigger, better and, hey, maybe we’ll even get to make fun of each other in person too.

Till next week,

Natasha Mascarenhas

Powered by WPeMatico

Like any successful founder, Andrew Grauer had bright, long-term ambitions for Course Hero from the moment he launched it in 2006.

He started the business to create a place where students could ask questions and get answers similar to Chegg, which launched 15 months before Course Hero . But as he slowly built it, he was tempted by a larger question: “What would a university look like if it was built by the internet?”

And so, the Redwood City-based startup itched at that nebulous goal throughout the years. Course Hero tested and failed products: free curated e-courses, in-person tutoring and teacher advice and ratings.

Clarity only came when Grauer realized that the core goal Course Hero launched with — giving students a place to ask and answer questions — wasn’t simply one product that should be fit into a broader suite of services. Instead, it was a thesis around which to build products. So, the startup began looking for different ways and formats to organize knowledge and questions and answers.

“That was a breakthrough insight,” Grauer said. The startup stopped launching other business verticals and decided to stick to Q&A as its core — and only — business. It sells Netflix -like subscriptions to students looking for access to learning and teaching content. Teachers and publishers can put course-specific study content on the platform.

Image Credits: Getty Images/manopjk

In 2020, Course Hero is a profitable business with annual run revenue upward of $100 million.

Today, Course Hero tells TechCrunch that it has raised a new tranche of capital in a Series B extension round of $70 million. The round is now totaling $80 million, bringing Course Hero’s total known venture capital to date to $95 million.

Its $80 million Series B round is one of the largest U.S. funding deals of 2020, and brings Course Hero’s valuation to $1.1 billion.

From a high level, the new raise is not surprising. Other edtech companies have also recently added on more capital to their balance sheets to meet remote learning demand amid the coronavirus pandemic.

But in Course Hero’s case, the new capital comes as a stark contrast to how the business functioned before 2020. After launching, the startup waited eight years to raise a $15 million Series A. Now, after going another nearly six years without raising venture capital, Course Hero has closed two rounds in this year alone.

Grauer tells TechCrunch that the capital will be used for operations, product innovation and feature development. It also plans to use the capital for future acquisitions (in 2012, Course Hero bought an in-person tutoring business).

Course Hero’s change of heart with venture capital boils down to the company meeting new scale demands. Last year, it passed 1 million subscribers on the platform. Now, it is eyeing “many millions” of students, the co-founder says.

Paraphrasing Bill Gates, Grauer said, “We do overestimate what we can do in just three years. And we dramatically underestimate what we can do closer to 10 years.”

Any edtech company that raises money off of current momentum in remote education will have to face the reality of what it is like to grow when remote learning is no longer a necessity. In other words, when the coronavirus pandemic ends, will these same platforms still find surges in usage?

“That’s the risk and reward of raising capital,” Grauer said. He added that “if you raise too much money early on, you can get misaligned expectations based on different time horizons set up by different terms of incoming shareholders or investors.”

Course Hero sees tailwinds in a dynamic that has been brewing since before the pandemic and will likely grow during and after: the growth of “nontraditional students” enrolling in and participating in higher education. Grauer noted that more than 40% of students work 30 hours or more per week. Over a quarter of students are parents, and of that quarter, over 70% are single moms.

“Because that’s the reality, and because we can make an affordable subscription and the economics can work, Course Hero is aligned to serving the majority, the real majority, and that’s the beauty of opportunity,” he said. There is a freemium model, but on an annual plan, a subscription costs $9.95 per month. On a monthly plan, a subscription costs $39.99 per month.

It’s not an opportunity the company hopes to expand into, it’s a reality of its diverse customer base. An internal data analytics survey of Course Hero shows that 58% of students that subscribe work at least part time. Over 25% of subscribers are 35 years old or older, and 22% of subscribers are parents.

Looking ahead, Course Hero hopes to continue to broaden its multisided marketplace.

In July, the business announced it is launching Educator Exchange, which allows college faculty to make money by uploading study materials for fellow teachers or students.

The “direct-to-faculty” relationship could pacify earlier tensions between the platform and teachers by giving the latter a way to monetize on how Course Hero “open sources” creative content on the point of copyright infringement.

Grauer compares Course Hero’s long-term vision to that of Google Maps, in that the platform can make recommendations of content based on other people’s usage.

But we’re not talking recommendations for the closest gas station. Based on how a user learns, Course Hero can recommend a specific professor who has a specific syllabus on a topic in which the user is interested.

“We’ve seen that specificity level differentiates us from others,” he said. “It helps students when they’re doing their real work, that one homework, that studying for one test. And I think that’s where the magic is for us.”

Powered by WPeMatico

Apple’s promise of high-quality video “shot on iPhone” is getting another real-world stress test, as late-night TV host Conan O’Brien announced on Wednesday he will return to doing full shows that will be shot using Apple’s mobile device. On Monday, March 30, new episodes of O’Brien’s show “Conan” will air on TBS, with production staff working from home, video that’s shot on iPhone and interviews filmed over video chat.

The news was first reported by Variety and confirmed by O’Brien in the form of a tweet, where he jokes the experience “will not be pretty.”

I am going back on the air Monday, March 30th. All my staff will work from home, I will shoot at home using an iPhone, and my guests will Skype. This will not be pretty, but feel free to laugh at our attempt. Stay safe.

— Conan O’Brien (@ConanOBrien) March 19, 2020

The move to shoot shows remotely is an interesting attempt at restarting daily TV production at a time when everyone’s been ordered to work from home.

Typically, late-night shows are put on with a sizable crew of writers and producers and filmed in front of a live audience. With the CDC advising people to stay at home and gather in groups of no more than 10 due to the threat of the coronavirus outbreak, TV production industry-wide is being shut down.

Until now, that also included all major late-night productions, like Stephen Colbert, Jimmy Fallon, Jimmy Kimmel and James Corden .

O’Brien’s team consists of 75 people and, like others, it went on hiatus in order to protect staff safety. But during the shut down, O’Brien continued to film short videos, which led the team to this idea of doing a full show, but in a different format.

“Conan” isn’t the only show trying to work around the shutdown. Jimmy Fallon has been filming YouTube videos that are incorporated into the evening’s rerun of the “Tonight Show.” Colbert has been filming a new monologue for “The Late Show” reruns. And Kimmel has been sharing his own “#minilogue” on social media.

However, “Conan” is promising full episodes, not just new segments.

“The quality of my work will not go down because technically that’s not possible,” O’Brien said in a statement shared by Variety.

Image credit: Kevin Mazur/Getty Images for WarnerMedia

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about how SoftBank is screwing up. Before that, I noted All Raise’s expansion, Uber the TV show and the unicorn from down under.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

Uber Head of Payments Peter Hazlehurst addresses the audience during an Uber products launch event in San Francisco, California, on September 26, 2019. (Photo by Philip Pacheco / AFP) (Photo credit should read PHILIP PACHECO/AFP/Getty Images)

The sheer number of startup players moving into banking services is staggering,” writes my Crunchbase News friends in a piece titled “Why Is Every Startup A Bank These Days.”

I’ve been asking myself the same question this year, as financial services business like Brex, Chime, Robinhood, Wealthfront, Betterment and more raise big rounds to build upstart digital banks. North of $13 billion venture capital dollars have been invested in U.S. fintech companies so far in 2019, up from $12 billion invested in 2018.

This week, one of the largest companies to ever emerge from the Silicon Valley tech ecosystem, Uber, introduced its team focused on developing new financial products and technologies. In a vacuum, a multibillion-dollar public company with more than 22,000 employees launching one new team is not big news. Considering investment and innovation in fintech this year, Uber’s now well-documented struggles to reach profitability and the company’s hiring efforts in New York, a hotbed for financial aficionados, the “Uber Money” team could indicate much larger fintech ambitions for the ride-hailing giant.

As it stands, the Uber Money team will be focused on developing real-time earnings for drivers accessed through the Uber debit account and debit card, which will itself see new features, like 3% or more cash back on gas. Uber Wallet, a digital wallet where drivers can more easily track their earnings, will launch in the coming weeks too, writes Peter Hazlehurst, the head of Uber Money.

This is hardly Uber’s first major foray into financial services. The company’s greatest feature has always been its frictionless payments capabilities that encourage riders and eaters to make purchases without thinking. Uber’s even launched its own consumer credit card to get riders cash back on rides. It’s no secret the company has larger goals in the fintech sphere, and with 100 million “monthly active platform consumers” via Uber, Uber Eats and more, a dedicated path toward new and better financial products may not only lead to happier, more loyal drivers but a company that’s actually, one day, able to post a profit.

The TechCrunch team is heading to Berlin again this year for our annual event, TechCrunch Disrupt Berlin, which brings together entrepreneurs and investors from across the globe. We announced the agenda this week, with leading founders including Away’s Jen Rubio and UiPath’s Daniel Dines. Take a look at the full agenda.

I will be there to interview a bunch of venture capitalists, who will give tips on how to raise your first euros. Buy tickets to the event here.

This week on Equity, I was in studio while Alex was remote. We talked about a number of companies and deals, including a new startup taking on Slack, Wag’s woes and a small upstart disrupting the $8 billion nail services industry. Listen to the episode here.

Equity drops every Friday at 6:00 am PT, so subscribe to us on iTunes, Overcast and all the casts.

Powered by WPeMatico

According to Dropbox CEO Drew Houston, 80% of the product’s users rely on it, at least partially, for work.

It makes sense, then, that the company is refocusing to try and cement its spot in the workplace; to shed its image as “just” a file storage company (in a time when just about every big company has its own cloud storage offering) and evolve into something more immutably core to daily operations.

Earlier this week, Dropbox announced that the “new Dropbox” would be rolling out to all users. It takes the simple, shared folders that Dropbox is known for and turns them into what the company calls “Spaces” — little mini collaboration hubs for your team, complete with comment streams, AI for highlighting files you might need mid-meeting, and integrations into things like Slack, Trello and G Suite. With an overhauled interface that brings much of Dropbox’s functionality out of the OS and into its own dedicated app, it’s by far the biggest user-facing change the product has seen since launching 12 years ago.

Shortly after the announcement, I sat down with Dropbox VP of Product Adam Nash and CTO Quentin Clark . We chatted about why the company is changing things up, why they’re building this on top of the existing Dropbox product, and the things they know they just can’t change.

You can find these interviews below, edited for brevity and clarity.

Greg Kumparak: Can you explain the new focus a bit?

Adam Nash: Sure! I think you know this already, but I run products and growth, so I’m gonna have a bit of a product bias to this whole thing. But Dropbox… one of its differentiating characteristics is really that when we built this utility, this “magic folder”, it kind of went everywhere.

Powered by WPeMatico

Today, Peloton is a bonafide success. The company, which sells $2,245 internet-connected exercise bikes, boasts a $4 billion valuation and a cult following.

That hasn’t always been the case. For years, Peloton battled for venture capital investment and struggled to attract buyers. Now that it’s proven the market for tech-enabled home exercise equipment and affiliated subscription products, a whole bunch of startups are chasing down the same customer segment.

Mirror, a New York-based company that sells $1,495 full-length mirrors that double as interactive home gyms, is closing in a round of funding expected to reach $36 million, sources and Delaware stock filings confirm, at a valuation just under $300 million. It’s unclear who has signed on to lead the round; we’ve heard a number of high-profile firms looked at Mirror’s books and passed. The company has previously raised a total of $38 million from Spark Capital, First Round Capital, Lerer Hippeau, BoxGroup and more.

Mirror declined to comment for this story.

Like Peloton, Mirror is sold for a hefty fee with a subscription to the service’s unlimited live and on-demand workouts that comes at an additional cost. The company hasn’t disclosed subscriber numbers, though The New York Times reported in February the business was selling $1 million worth of Mirrors — or some 650 units — per month.

The company has not only benefited from the Peloton effect, but also from a near-immediate interest from celebrities and influencers in its product. Kate Hudson, Alicia Keys, Reese Witherspoon, Jennifer Aniston and Gwyneth Paltrow are among the many celebrities to have publicly boasted about Mirror, undoubtedly boosting sales for the up-and-coming startup.

Venture capitalists were quick to show support for Mirror, too; in fact, the business attracted money at a $200 million valuation prior to launching its first product. Mirror began selling its sleek equipment, dubbed by The New York Times as “The Most Narcissistic Exercise Equipment Ever,” in September.

SAN FRANCISCO, CA – SEPTEMBER 06: Mirror Founder and CEO Brynn Putnam (L) and moderator Lucas Matney speak onstage during Day 2 of TechCrunch Disrupt SF 2018 at Moscone Center on September 6, 2018, in San Francisco, California. (Photo by Steve Jennings/Getty Images for TechCrunch)

The round comes amid a distinct boom in funding for fitness-related startups evidenced not only by Peloton’s mammoth valuation and hyped-over initial public offering expected soon but by the rapid uptick in small upstarts looking to capitalize on rising interest in fitness apps and equipment. In total, VCs bet some $2 billion on U.S. fitness startups in 2018, a record amount of funding for the space. So far this year, nearly $500 million has been allocated to the growing sector, per PitchBook, as entrepreneurs strive to bring the gym into the home.

Tonal, which sells personal exercise equipment that combines on-demand training with smart features, is among a small class of venture-backed fitness companies to have accumulated a large following. The company has raised $91.7 million in equity funding at a valuation of $185 million, according to PitchBook, from investors including L Catterton, Shasta Ventures, Mayfield and Sapphire Sport.

When it comes to early-stage efforts, there’s no shortage of recent fundraises. Last week, Livekick, which gives customers access to one-on-one personal training and yoga from their home, closed a $3 million seed round led by Firstime VC. Two weeks ago, fitness startup Future secured an $8.5 million round led by Kleiner Perkins’ Mamoon Hamid. For a $150 monthly fee, Future assigns personalized workout plans and a coach who tracks customers’ fitness activity through an Apple Watch. To keep users committed to their workout regimens, Future sends daily text messages with motivational feedback.

The AI-based personal training company Aaptiv, Plankk, which sells live fitness lessons led by Instagram stars, and audio coaching app Eastnine, have also recently launched.

Mirror was founded in late 2016 by Brynn Putnam, an entrepreneur behind Refine Method, a chain of boutique fitness studios located in New York. The former professional dancer spoke to TechCrunch’s Lucas Matney at Disrupt San Francisco in September about the future of the business.

“[We want] to enhance the human touch rather than to replace it,” Putnam said. “Our goal is not to be the next treadmill in your life, our goal is to be the next screen in your home,” Putnam said.

Ultimately, Putnam added, Mirror plans to scale beyond fitness content with potential extensions including physical therapy, fashion, beauty and education.

“We have the ability to create personalized premium content across a wide range of verticals, with fitness being our first vertical,” Putnam said.

Powered by WPeMatico

Amazon and Walmart’s problems in India look set to continue after Narendra Modi, the biggest force to embrace the country’s politics in decades, led his Hindu nationalist Bharatiya Janata Party to a historic landslide re-election on Thursday, reaffirming his popularity in the eyes of the world’s largest democracy.

The re-election, which gives Modi’s government another five years in power, will in many ways chart the path of India’s burgeoning startup ecosystem, as well as the local play of Silicon Valley companies that have grown increasingly wary of recent policy changes.

At stake is also the future of India’s internet, the second largest in the world. With more than 550 million internet users, the nation has emerged as one of the last great growth markets for Silicon Valley companies. Google, Facebook, and Amazon count India as one of their largest and fastest growing markets. And until late 2016, they enjoyed great dynamics with the Indian government.

But in recent years, New Delhi has ordered more internet shutdowns than ever before and puzzled many over crackdowns on sometimes legitimate websites. To top that, the government recently proposed a law that would require any intermediary — telecom operators, messaging apps, and social media services among others — with more than 5 million users to introduce a number of changes to how they operate in the nation. More on this shortly.

Powered by WPeMatico

More than five years ago, Sequoia partner Alfred Lin called Tony Xu, the founder of a small on-demand delivery startup called DoorDash, to say he was passing on the company’s seed round.

This was, of course, before venture capital funding in food delivery startups had taken off. DoorDash, launched out of Xu’s Stanford graduate school dorm room, wasn’t worth Sequoia’s capital — yet.

Today, venture capitalists are valuing the San Francisco-based company at a whopping $12.6 billion with a $600 million Series G. New investors Darsana Capital Partners and Sands Capital participated in the deal, which nearly doubles DoorDash’s previous valuation, alongside existing backers Coatue Management, Dragoneer, DST Global, Sequoia Capital, the SoftBank Vision Fund and Temasek Capital Management.

As for Sequoia’s Alfred Lin, he realized his mistake years ago and jumped in on DoorDash’s 2014 Series A, and has participated in every subsequent round since. DoorDash, a graduate of Y Combinator’s Summer 2013 cohort, is also backed by Kleiner Perkins, CRV and Khosla Ventures, among others. In total, the company has raised $2.5 billion in VC funding, making it one of the most well-capitalized private companies in the U.S.

SoftBank, via its prolific dealmaker Jeffrey Housenbold, was responsible for making DoorDash a unicorn in early 2018. The nearly $100 billion Vision Fund led DoorDash’s $535 million Series D, valuing the business at $1.4 billion. Just three months ago, the SoftBank Vision Fund, DST Global, Coatue Management, GIC, Sequoia and Y Combinator put an additional $400 million in the fast-growing business.

SAN FRANCISCO, CA – SEPTEMBER 05: DoorDash CEO Tony Xu speaks onstage during Day 1 of TechCrunch Disrupt SF 2018 at Moscone Center on September 5, 2018 in San Francisco, California. (Photo by Kimberly White/Getty Images for TechCrunch)

Xu told TechCrunch the company’s Series F was “a reflection of superior performance over the past year.” DoorDash was currently seeing 325% growth year-over-year, he said, pointing to recent data from Second Measure showing the service had overtaken Uber Eats in the U.S., coming in second only to GrubHub.

“I think the numbers speak for themselves,” Xu said at the time. “If you just run the math on DoorDash’s course and speed, we’re on track to be number one.”

At a venture capital-focused summit hosted in April, Xu added that DoorDash was the largest delivery platform in America by “pretty wide margins,” explaining that it was, in fact, growing 4x faster than its next closest peer. In this morning’s announcement, the company added that it’s grown 60% since its late February Series F, with its annualized total sales hitting $7.5 billion in March, an increase of 280% year-over-year.

Still, one wonders what kind of growth metrics DoorDash might be sharing to attract that kind of valuation multiple. The company has yet to disclose revenues and is not yet profitable, but has seen its price tag grow astronomically in just two years. Since March 2018, DoorDash’s valuation has skyrocketed from $1.4 billion to $4 billion with a $250 million Series E to $7.1 billion with a $350 million Series F and, finally, to nearly $13 billion with its Series G.

The $12.6 billion valuation makes DoorDash one of the 10 most valuable venture-backed companies in the U.S., surpassing Coinbase, Instacart and even Slack, according to PitchBook.

DoorDash is currently active in more than 4,000 cities in the U.S. and Canada, with hundreds of partners, including both restaurants and supermarkets (Walmart is using DoorDash for grocery deliveries). The company also operates DoorDash Drive, which allows businesses to use the DoorDash network to make their own deliveries.

Powered by WPeMatico

Since the dawn of the internet, the titans of this industry have fought to win the “starting point” — the place that users start their online experiences. In other words, the place where they begin “browsing.” The advent of the dial-up era had America Online mailing a CD to every home in America, which passed the baton to Yahoo’s categorical listings, which was swallowed by Google’s indexing of the world’s information — winning the “starting point” was everything.

As the mobile revolution continues to explode across the world, the battle for the starting point has intensified. For a period of time, people believed it would be the hardware, then it became clear that the software mattered most. Then conversation shifted to a debate between operating systems (Android or iOS) and moved on to social properties and messaging apps, where people were spending most of their time. Today, my belief is we’re hovering somewhere between apps and operating systems. That being said, the interface layer will always be evolving.

The starting point, just like a rocket’s launchpad, is only important because of what comes after. The battle to win that coveted position, although often disguised as many other things, is really a battle to become the starting point of commerce.

Google’s philosophy includes a commitment to get users “off their page” as quickly as possible…to get that user to form a habit and come back to their starting point. The real (yet somewhat veiled) goal, in my opinion, is to get users to search and find the things they want to buy.

Of course, Google “does no evil” while aggregating the world’s information, but they pay their bills by sending purchases to Priceline, Expedia, Amazon and the rest of the digital economy.

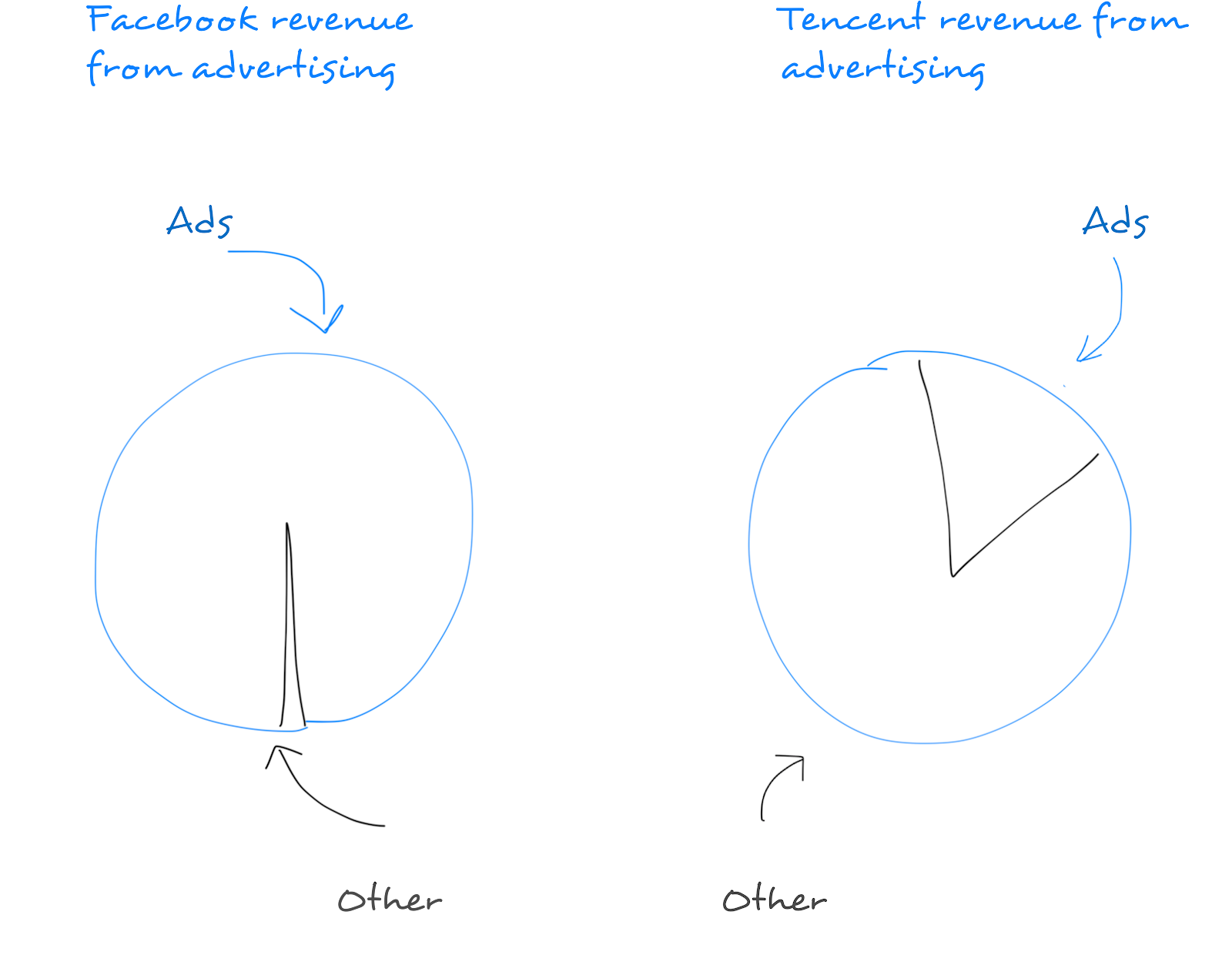

Facebook, on the other hand, has become a starting point through its monopolization of users’ time, attention and data. Through this effort, it’s developed an advertising business that shatters records quarter after quarter.

Google and Facebook, this famed duopoly, represent 89 percent of new advertising spending in 2017. Their dominance is unrivaled… for now.

Change is urgently being demanded by market forces — shifts in consumer habits, intolerable rising costs to advertisers and through a nearly universal dissatisfaction with the advertising models that have dominated (plagued) the U.S. digital economy. All of which is being accelerated by mobile. Terrible experiences for users still persist in our online experiences, deliver low efficacy for advertisers and fraud is rampant. The march away from the glut of advertising excess may be most symbolically seen in the explosion of ad blockers. Further evidence of the “need for a correction of this broken industry” is Oracle’s willingness to pay $850 million for a company that polices ads (probably the best entrepreneurs I know ran this company, so no surprise).

As an entrepreneur, my job is to predict the future. When reflecting on what I’ve learned thus far in my journey, it’s become clear that two truths can guide us in making smarter decisions about our digital future:

Every day, retailers, advertisers, brands and marketers get smarter. This means that every day, they will push the platforms, their partners and the places they rely on for users to be more “performance driven.” More transactional.

Paying for views, bots (Russian or otherwise) or anything other than “dollars” will become less and less popular over time. It’s no secret that Amazon, the world’s most powerful company (imho), relies so heavily on its Associates Program (its home-built partnership and affiliate platform). This channel is the highest performing form of paid acquisition that retailers have, and in fact, it’s rumored that the success of Amazon’s affiliate program led to the development of AWS due to large spikes in partner traffic.

Chinese flag overlooking The Bund, Shanghai, China (Photo: Rolf Bruderer/Getty Images)

When thinking about our digital future, look down and look east. Look down and admire your phone — this will serve as your portal to the digital world for the next decade, and our dependence will only continue to grow. The explosive adoption of this form factor is continuing to outpace any technological trend in history.

Now, look east and recognize that what happens in China will happen here, in the West, eventually. The Chinese market skipped the PC-driven digital revolution — and adopted the digital era via the smartphone. Some really smart investors have built strategies around this thesis and have quietly been reaping rewards due to their clairvoyance.

China has historically been categorized as a market full of knock-offs and copycats — but times have changed. Some of the world’s largest and most innovative companies have come out of China over the past decade. The entrepreneurial work ethic in China (as praised recently by arguably the world’s greatest investor, Michael Moritz), the speed of innovation and the ability to quickly scale and reach meaningful populations have caused Chinese companies to leapfrog the market cap of many of their U.S. counterparts.

The most interesting component of the Chinese digital economy’s growth is that it is fundamentally more “pure” than the U.S. market’s. I say this because the Chinese market is inherently “transactional.” As Andreessen Horowitz writes, WeChat, China’s most valuable company, has become the “starting point” and hub for all user actions. Their revenue diversity is much more “Amazon” than “Google” or “Facebook” — it’s much more pure. They make money off the transactions driven from their platform, and advertising is far less important in their strategy.

The obsession with replicating WeChat took the tech industry by storm two years ago — and for some misplaced reason, everyone thought we needed to build messaging bots to compete.

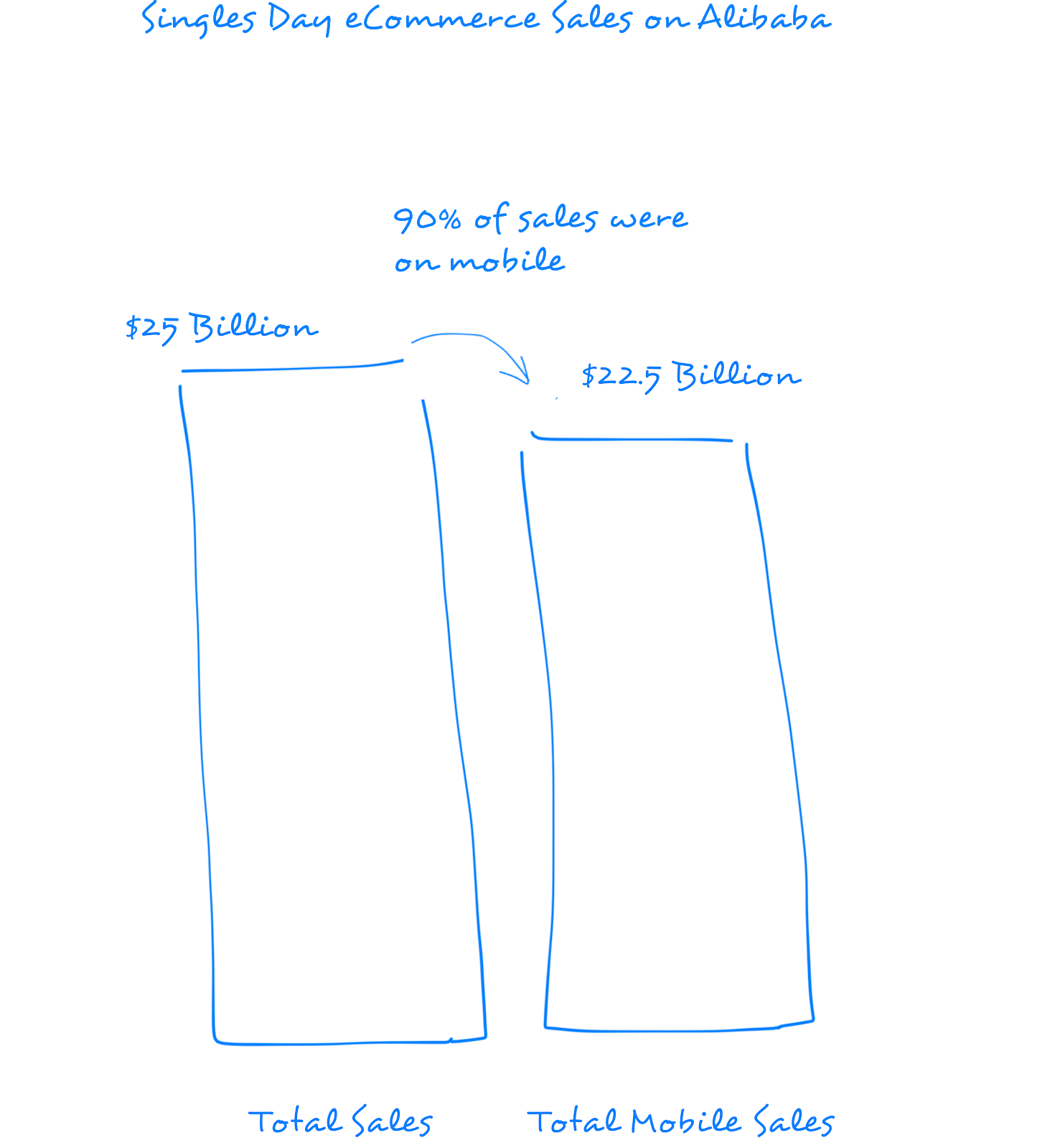

What shouldn’t be lost is our obsession with the purity and power of the business models being created in China. The fabric that binds the Chinese digital economy and has fostered its seemingly boundless growth is the magic combination of commerce and mobile. Singles Day, the Chinese version of Black Friday, drove $25 billion in sales on Alibaba — 90 percent of which were on mobile.

The lesson we’ve learned thus far in both the U.S. and in China is that “consumers spending money” creates the most durable consumer businesses. Google, putting aside all its moonshots and heroic mission statements, is a “starting point” powered by a shopping engine. If you disagree, look at where their revenue comes from…

Google’s recent announcement of Shopping Actions and their movement to a “pay per transaction model” signals a turning point that could forever change the landscape of the digital economy.

Google’s multi-front battle against Apple, Facebook and Amazon is weighted. Amazon is the most threatening. It’s the most durable business of the four — and its model is unbounded on two fronts that almost everyone I know would bet their future on, 1) people buying more online, where Amazon makes a disproportionate amount of every dollar spent, and 2) companies needing more cloud computing power (more servers), where Amazon makes a disproportionate amount of every dollar spent.

To add insult to injury, Amazon is threatening Google by becoming a starting point itself — 55 percent of product searches now originate at Amazon, up from 30 percent just a year ago.

Google, recognizing consumer behavior was changing in mobile (less searching) and the inferiority of their model when compared to the durability and growth prospects of Amazon, needed to respond. Google needed a model that supported boundless growth and one that created a “win-win” for its advertising partners — one that resembled Amazon’s relationship with its merchants — not one that continued to increase costs to retailers while capitalizing on their monopolization of search traffic.

Google knows that with its position as the starting point — with Google.com, Google Apps and Android — it has to become a part of the transaction to prevail in the long term. With users in mobile demanding fewer ads and more utility (demanding experiences that look and feel a lot more like what has prevailed in China), Google has every reason in the world to look down and to look east — to become a part of the transaction — to take its piece.

A collision course for Google and the retailers it relies upon for revenue was on the horizon. Search activity per user was declining in mobile and user acquisition costs were growing quarter over quarter. Businesses are repeatedly failing to compete with Amazon, and unless Google could create an economically viable growth model for retailers, no one would stand a chance against the commerce juggernaut — not the retailers nor Google itself.

As I’ve believed for a long time, becoming a part of the transaction is the most favorable business model for all parties; sources of traffic make money when retailers sell things, and, most importantly, this only happens when users find the things they want.

Shopping Actions is Google’s first ambitious step to satisfy all three parties — businesses and business models all over the world will feel this impact.

Good work, Sundar.

Powered by WPeMatico