General Catalyst

Auto Added by WPeMatico

Auto Added by WPeMatico

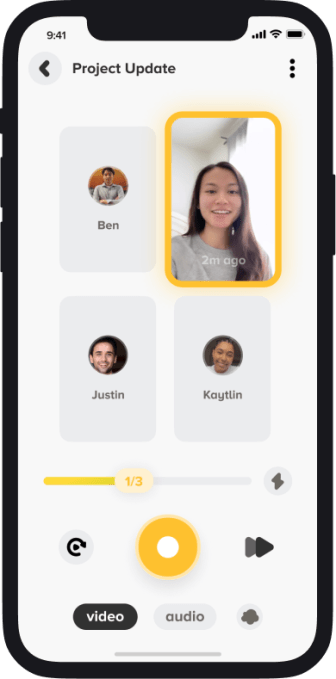

A new startup called Popcorn wants to make work communication more fun and personal by offering a way for users to record short video messages, or “pops,” that can be used for any number of purposes in place of longer emails, texts, Slack messages or Zoom calls. While there are plenty of other places to record short-form video these days, most of these exist in the social media space, which isn’t appropriate for a work environment. Nor does it make sense to send a video you’ve recorded on your phone as an email attachment, when you really just want to check in with a colleague or say hello.

Popcorn, on the other hand, lets you create the short video and then send a URL to that video anywhere you would want to add a personal touch to your message.

For example, you could use Popcorn in a business networking scenario, where you’re trying to connect with someone in your industry for the first time — aka “cold outreach.” Instead of just blasting them a message on LinkedIn, you could also paste in the Popcorn URL to introduce yourself in a more natural, friendly fashion. You also could use Popcorn with your team at work for things like daily check-ins, sharing progress on an ongoing project or to greet new hires, among other things.

Image Credits: Popcorn

Videos themselves can be up to 60 seconds in length — a time limit designed to keep Popcorn users from rambling. Users also can opt to record audio only if they don’t want to appear on video. And you can increase the playback speed if you’re in a hurry. Users who want to receive “pops” could also advertise their “popcode” (e.g. try mine at U8696).

The idea to bring short-form video to the workplace comes from Popcorn co-founder and CEO Justin Spraggins, whose background is in building consumer apps. One of his first apps to gain traction back in 2014 was a Tinder-meets-Instagram experience called Looksee that allowed users to connect around shared photos. A couple years later, he co-founded a social calling app called Unmute, a Clubhouse precursor of sorts. He then went on to co-found 9 Count, a consumer app development shop which launched more social apps like BFF (previously Wink) and Juju.

9 Count’s lead engineer, Ben Hochberg, is now also a co-founder on Popcorn (or rather, Snack Break, Inc. as the legal entity is called). They began their work on Popcorn in 2020, just after the start of the COVID-19 pandemic. But the rapid shift to remote work in the days that followed could now help Popcorn gain traction among distributed teams. Today’s remote workers may never again return to in-person meetings at the office, but they’re also growing tired of long days stuck in Zoom meetings.

With Popcorn, the goal is to make work communication fun, personal and bite-sized, Spraggins says. “[We want to] bring all the stuff we’re really passionate about in consumer social into work, which I think is really important for us now,” he explains.

“You work with these people, but how do you — without scheduling a Zoom — how do you bring the ‘human’ to it?,” Spraggins says. “I’m really excited about making work products feel more social, more like Snapchat than utility tools.”

There is a lot Popcorn would still need to figure out to truly make a business-oriented social app work, including adding enhanced security, limiting spam, offering some sort of reporting flow for bad actors, and more. It will also eventually need to land on a successful revenue model.

Currently, Popcorn is a free download on iPhone, iPad and Mac, and offers a Slack integration so you can send video messages to co-workers directly in the communication software you already use to catch up and stay in touch. The app today is fairly simple, but the company plans to enhance its short videos over time using AR frames that let users showcase their personalities.

The startup raised a $400,000 pre-seed round from General Catalyst (Niko Bonatsos) and Dream Machine (Alexia Bonatsos, previously editor-in-chief at TechCrunch.) Spraggins says the company will be looking to raise a seed round in the fall to help with hires, including in the AR space.

Powered by WPeMatico

Ken Babcock and his co-founders, Dan Giovacchini and Brian Shultz, were in the midst of Harvard Business School in March 2020 when they felt the call to start Tango, a Chrome extension that auto-captures workflow best practices so that teams can learn from their top performers.

“This window of opportunity was driven by the pandemic as we saw a lot of companies become distributed and go remote,” CEO Babcock told TechCrunch. “Team leaders were remotely onboarding people, for perhaps the first time, and accelerating ramp times. There was no longer the opportunity to tap on people’s shoulders in the office, so much of the training was left to people’s own devices.”

They dropped out of their program to start Los Angeles-based Tango, and today, announced a $5.7 million seed round for its workflow intelligence platform. Wing Venture Capital led the round and was joined by General Catalyst, Global Silicon Valley, Outsiders Fund and Red Sea Ventures. A group of angel investors also joined, including former Yelp executive Michael Stoppelman, former Uber head of data Jai Ranganathan, KeepTruckin CEO Shoaib Makani and Awesome People Ventures’ Julia Lipton.

Tango is designed to help employees, particularly in customer success and sales enablement, get back as much as 20% of their workweek spent searching for that one piece of information or tracking down the right colleague to assist with a task. Its technology creates tutorials by recording a users’ workflow — actions, links to pages, URLs and screenshots — and turns that into step-by-step documentation with a video.

Previously the co-founders bootstrapped the company, and decided to go after seed funding to expand the product and growth teams and invest in product development so that Tango could take a product-led growth strategy, Babcock said. The team now has 13 employees.

Since starting last year, Tango has secured 10 pilots to figure out the data and capabilities before it is set to launch publicly in September. Babcock said the company will always have a free version of the product, as well as premium and enterprise versions that will unlock additional capabilities.

“The big thing is around integrations and meeting people where the consumer content is,” Babcock added. “We are reducing that burden of creating documentation, and for companies that already have Wikis or other materials, learning how to inject ourselves into those systems.”

Zach DeWitt, partner at Wing Venture Capital, said he met the company three years ago through a mutual friend.

His firm invests in early-stage, business-to-business startups unlocking a novel data set. In Tango’s case, the company was creating a new data set for the enterprise and business, where users can analyze workflow.

With the average tech company using 150 SaaS apps, up from 20 a decade ago, there are permutations about which app to use, how to use them, what happens if the user gets stuck and what if none of the data is being captured, Dewitt said. Tango works in the background and captures workflow, which is the foundation to the business’ success.

“I was blown away by the approach,” he added. “You have to meet people where they get stuck and even anticipate where they get stuck so you can serve the Tango tutorial to get unstuck. It can also change the company’s culture when it rewards people to share knowledge. The whole idea is beneficial to multiple parties: to those who are getting stuck and to new hires. That is powerful.”

Powered by WPeMatico

Edtech startup Microverse has tapped new venture funding in its quest to help train students across the globe to code through its online school that requires zero upfront cost, instead relying on an income-share agreement that kicks in when students find a job.

The startup tells TechCrunch it has closed a $12.5 million Series A led by Northzone with additional participation from General Catalyst, All Iron Ventures and a host of angel investors. We last covered the company after it had closed a bout of seed funding from General Catalyst and Y Combinator; this latest round brings the startup’s total funding to just under $16 million.

The company’s vision has seen added pandemic-era traction as larger tech companies have embraced remote work that spans geographic boundaries and time zones. Microverse has now brought English-speaking students from over 188 countries through its program.

Since we last chatted, CEO Ariel Camus says the startup has landed some 300 early graduates in positions at tech companies including Microsoft, VMWare and Huawei. The company says its has above a 95% employment rate for its students within six months of graduation so far, pushing past one of the bigger issues that income-share-agreement-based schools have had stateside — getting graduates employed.

Microverse does have notably less generous terms than counterparts like Lambda School when it comes to when students begin loan repayment, the terms of both are actually quite different, as noted in my previous article:

While Lambda School’s ISA terms require students to pay 17% of their monthly salary for 24 months once they begin earning above $50,000 annually — up to a maximum of $30,000, Microverse requires that graduates pay 15% of their salary once they begin making more than just $1,000 per month, though there is no cap on time, so students continue payments until they have repaid $15,000 in full. In both startups’ cases, students only repay if they are employed in a field related to what they studied, but with Microverse, ISAs never expire, so if you ever enter a job adjacent to your area of study, you are on the hook for repayments. Lambda School’s ISA taps out after five years of deferred repayments.

The startup has made efforts to streamline their online program since launch to ensure that students are being set up to succeed in the full-time, 10-month program. Part of Microverse’s efforts have included condensing lesson segments into shorter time frames to ensure students aren’t starting the program unless they have enough free time to commit. Camus says the startup is receiving thousands of applications per month, of which only a fraction are accepted in an effort to ensure that the small startup isn’t overcommitting itself early on. The startup estimates it will usher 1,000 students through its program this year.

The startup has big plans for the future, including working more closely with tech companies to ensure that students have easier access to job placement once they graduate.

“We have data now that the day we launch a partner program — which we haven’t done yet but we will eventually — it opens up the market by 5x,” Camus tells TechCrunch. “To get 10,000 students per year in a world where 90% of the world’s population doesn’t have access to higher education — it’s not going to be that hard, to be honest, I’m not too worried.”

Powered by WPeMatico

How big is the market in India for a neobank aimed at teenagers? Scores of high-profile investors are backing a startup to find out.

Bangalore-based FamPay said on Wednesday it has raised $38 million in its Series A round led by Elevation Capital. General Catalyst, Rocketship VC, Greenoaks Capital and existing investors Sequoia Capital India, Y Combinator, Global Founders Capital and Venture Highway also participated in the new round, which brings FamPay’s to-date raise to $42.7 million.

TechCrunch reported early this month that FamPay was in talks with Elevation Capital to raise a new round.

Founded by Sambhav Jain and Kush Taneja (pictured above) — both of whom graduated from Indian Institute of Technology, Roorkee in 2019 — FamPay enables teenagers to make online and offline payments.

The thesis behind the startup, said Jain in an interview with TechCrunch, is to provide financial literacy to teenagers, who additionally have limited options to open a bank account in India at a young age. Through gamification, the startup said it’s making lessons about money fun for youngsters.

Unlike in the U.S., where it’s common for teenagers to get jobs at restaurants and other places and understand how to handle money at a young age, a similar tradition doesn’t exist in India.

After gathering the consent from parents, FamPay provides teenagers with an app to make online purchases, as well as plastic cards — the only numberless card of its kind in the country — for offline transactions. Parents credit money to their children’s FamPay accounts and get to keep track of high-ticket spendings.

In other markets, including the U.S., a number of startups including Greenlight, Step and Till Financial are chasing to serve the teenagers, but in India, there currently is no startup looking to solve the financial access problem for teenagers, said Mridul Arora, a partner at Elevation Capital, in an interview with TechCrunch.

It could prove to be a good issue to solve — India has the largest adolescent population in the world.

“If you’re able to serve them at a young age, over a course of time, you stand to become their go-to product for a lot of things,” Arora said. “FamPay is serving a population that is very attractive and at the same time underserved.”

The current offerings of FamPay are just the beginning, said Jain. Eventually the startup wishes to provide a range of services and serve as a neobank for youngsters to retain them with the platform forever, he said, though he didn’t wish to share currently what those services might be.

Image Credits: FamPay

Teens represent the “most tech-savvy generation, as they haven’t seen a world without the internet,” he said. “They adapt to technology faster than any other target audience and their first exposure with the internet comes from the likes of Instagram and Netflix. This leads to higher expectations from the products that they prefer to use. We are unique in approaching banking from a whole new lens with our recipe of community and gamification to match the Gen Z vibe.”

“I don’t look at FamPay just as a payments service. If the team is able to execute this, FamPay can become a very powerful gateway product to teenagers in India and their financial life. It can become a neobank, and it also has the opportunity to do something around social, community and commerce,” said Arora.

During their college life, Jain and Taneja collaborated and built an app and worked at a number of startups, including social network ShareChat, logistics firm Rivigo and video streaming service Hotstar. Jain said their work with startups in the early days paved the idea to explore a future in this ecosystem.

Prior to arriving at FamPay, Jain said the duo had thought about several more ideas for a startup. The early days of FamPay were uniquely challenging to the founders, who had to convince their parents about their decision to do a startup rather than joining firms or startups as had most of their peers from college. Until being selected by Y Combinator, Jain said he didn’t even fully understand a cap table and dilutions.

He credited entrepreneurs such as Kunal Shah (founder of CRED) and Amrish Rau (CEO of Pine Labs) for being generous with their time and guidance. They also wrote some of the earliest checks to the startup.

The startup, which has amassed over 2 million registered users, plans to deploy the fresh capital to expand its user base and product offerings, and hire engineers. It is also looking for people to join its leadership team, said Jain.

Powered by WPeMatico

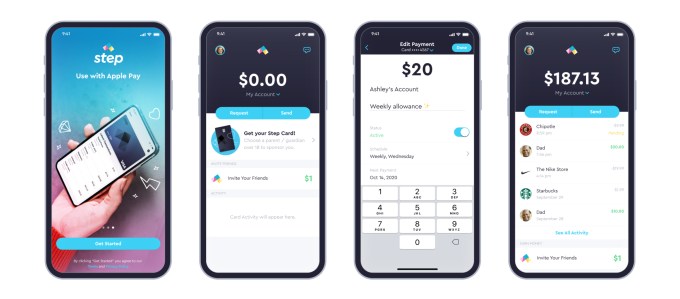

Step, the digital banking service aimed at teens and endorsed by TikTok star Charli D’Amelio, announced this morning the close of a $100 million round of Series C funding after growing to more than 1.5 million users just six months after launch. The new round, led by General Catalyst, comes shortly after Step’s $50 million Series B, announced at the end of last year after the startup hit half a million users in only two months post-launch.

The new round also includes participation from Step’s existing investors, Coatue, Stripe, Charli D’Amelio, The Chainsmokers, Will Smith and Jeffrey Katzenberg, and brings on newcomer Franklin Templeton, signaling a plan to move into investments is on the horizon. It also includes actor and musician Jared Leto. Step is also formally announcing NBA All-Star Stephen Curry as an investor, which had not previously been disclosed, as well as former Square executives Sarah Friar, Jacqueline Reses and Gokul Rajaram.

As a result of the fundraise, Kyle Doherty of General Catalyst is joining Step’s board. To date, Step has raised more than $175 million.

Image Credits: Step

According to CEO CJ MacDonald, Step hasn’t yet spent the money from its Series B, but believes the additional funds can help the startup grow more quickly.

“We’ve signed up more than a million and a half accounts in the first six months. We’re signing up 10,000 accounts-plus a day, and there’s just a lot of things that we want to do to bring this to millions and millions of households to help educate the next generation be smarter with money,” he says. At the time of the Series B, for comparison, Step said it was adding around 7,000 to 10,000 accounts per day.

“Honestly we don’t need the capital,” MacDonald added. “It’s just we think speed to market is really key and we think we can accelerate our growth and invest in infrastructure.”

The company is also planning to hire across operations, engineering, product and design, to double its now 65-person team over the next year.

Step today competes in a crowded market of mobile banking services aimed at a younger demographic, but it’s one of very few that targets teenagers ages 13 to 18. Through Step’s app, teens gain access to an FDIC-insured bank account without fees and a secured Visa card that helps them establish credit before they turn 18. The app also offers Venmo-like functionality for sending money to friends.

Image Credits: Step

Step’s growth so far has benefitted from a combination of factors, including word-of-mouth, use of social media and its popular referral program, which has paid out a few dollars per new sign-up. Step has also leveraged its partnerships with social media influencers like D’Amelio and Josh Richards, as well as celebs like Step investor Justin Timberlake.

The company believes the Curry announcement may also help to raise awareness about the banking app. As a father of three, if Curry talks about introducing Step to his own children, people will take notice.

While the additional funds are focused on driving growth, Step is also thinking about its future as its existing users begin to age up. The company plans to enter into the credit and lending market, as well as introduce investments at some point in the future. The Franklin Templeton investment could be useful here, MacDonald notes.

“Franklin [Templeton is] obviously, one of the largest financial institutions in the world. And, as we start thinking about investments and the journey of the customer, to have a great brand like Franklin Templeton that’s invested in this round — I think it’s just a testament to where they see the world going,” he says.

Step’s fundraise falls on the same day that competitor Current and Greenlight, both which focus on families, also raised new rounds.

Powered by WPeMatico

Titan, a startup that is building a retail investment management platform aimed at millennials, has closed on $12.5 million in a Series A round led by VC heavyweight General Catalyst.

A bevy of other investors put money in the round, including Sound Ventures (actor Ashton Kutcher and Guy Oseary’s VC firm), Scribble VC, BoxGroup, Y Combinator, South Park Commons, Instagram founder Mike Krieger, Lee Fixel and others.

Titan is hoping to build on the momentum it saw in 2020, during which it grew revenue, customers and assets under management by 600%, “with effectively no marketing budget, according to co-founder Joe Percoco. The New York-based company says it’s approaching $500 million in assets under management and was cash flow positive last year.

Percoco met co-CEO Clay Gardner while the pair were at the Wharton School of the University of Pennsylvania.

“We came from two different backgrounds with respect to investing,” Percoco recalled. “He was the type that bought his first shares of stock at the ages of 11 and 12. I’m the exact opposite and couldn’t invest myself until after Goldman Sachs, where I went to work after Penn.”

Because the duo both worked in the industry, they found that friends and family were always asking them how they should manage their capital.

“We were sending them to ETFs and mutual funds in our day jobs,” Percoco said. “But we realized they did not have the same access to investing that the wealthier did.”

Frustrated with only helping the rich get richer, the pair founded Titan in 2017 with the goal of disrupting what they viewed as “an archaic industry. They’ve since built an operating system aimed at giving “everyday investors access to the types of investment products and experiences that they’ve historically been locked out of.” Or, as they describe, it a mobile version of what investment giants Fidelity and BlackRock created decades ago.

Titan’s capital management platform is designed for both accredited and unaccredited investors. The company says it provides access to services that would historically require a $1 million minimum, such as direct portfolio manager access. It charges a fee amounting to just 1% of assets, compared to the 2% – and in some cases 20% of profits – that legacy players charge.

“We believe Fidelity 2.0 will be direct-to-consumer with no walls and no black boxes,” Percoco said.

(For the unacquainted, according to Investopedia, black box accounting is the deliberate use of complex bookkeeping methodologies to make interpreting financial statements challenging and time-consuming.)

Its simplicity sets it apart. Titan chooses stocks via its “proprietary and discretionary” research process based on the principals’ previous experience.

The startup currently offers two stock-focused strategies on its platform,

One of those strategies, called Flagship, is focused on large cap growth. The other, called Opportunities, focuses on smaller, under-the-radar companies.

Titan’s core customer is the young professional in the 25-35 age range.

“They’re already investing money somewhere, even if not that much of their money,” Gardner said. “But they’re well attuned to the reasons they should be… And, most asset management products remain in the Stone Age, offering 90-page prospectuses and black-box client experiences.”

As former TC editor Josh Constine explained when the company raised a $2.5 million seed round in October 2018, Titan differs from Robinhood or E*Trade, where users essentially are left to fend for themselves. But clients also have some control, unlike passive options such as Wealthfront and Betterment.

Looking ahead, Titan plans to use its new capital to scale its engineering and investment team, as well as make “significant investments” in product, marketing and operations. It also plans to launch several investment products across a variety of asset classes.

“Many legacy players are hungry to have an OS to serve more folks they historically could not,” Percoco said. “We’re getting inbounds from legacy players in the space seeking to manage capital for new generations and realizing it will shift to mobile operating systems like Titan’s. Eventually, we can enable them to build their own investment products on Titan.”

Katherine Boyle, partner at General Catalyst and Titan board member, said she was struck by Percoco and Gardner’s “deep empathy” for investors who are often overlooked — such as millennials and new investors “who have cash sitting in their checking accounts and want expert management but don’t know where to go.”

“They don’t want to be stock pickers but they don’t want a set-it-and-forget-it product,” Boyle said. “There’s another level of sophistication with actively managed products where the best managers are making investment decisions on behalf of those who can afford it. But there’s no reason why retail investors should be excluded from this model.”

She thinks Titan can capitalize on what she believes is millennials’ “deep lack of trust” in legacy institutions.

“We need new institutions like Titan to combat this lack of trust,” Boyle said. “And these new institutions need to have incentives that are aligned with their clients, not with hedge funds or banks.”

Powered by WPeMatico

University education is getting more expensive, and at the moment it feels a bit like a Petri dish for infections, but the long-term trends continue to show a dramatic growth in the number of people worldwide getting degrees beyond high school, with one big reason for this being that a college degree generally provides better economic security.

But today, a startup that is exploring a different route for those interested in technology and knowledge worker positions — specifically by way of apprenticeships to bring in and train younger people on the job — is announcing a significant round of growth funding to see if it can provide a credible, scalable alternative to that model.

Multiverse, a U.K. startup that works with organizations to develop these apprenticeships, and then helps source promising, diverse candidates to fill those roles, has raised $44 million, funding that it will be using to spearhead a move into the U.S. market after picking up some 300 clients in the U.K. and thousands of apprentices.

The Series B is being led by General Catalyst (which has been especially active this week with U.K. startups: it also led a large round yesterday for Bloom & Wild), with GV (formerly known as Google Ventures), Audacious Ventures, Latitude and SemperVirens also participating. Index Ventures and Lightspeed Venture Partners, which first invested in the company in its $16 million Series A in 2020, also participated.

Valuation is not being disclosed, but for what it’s worth, the round was one that generated a lot of interest. In between getting pitched this story and publishing it, the size of the Series B grew by $8 million (it was originally closed at $36 million). The FT notes that the valuation was around $200 million with this round, but the company says that is “speculation on the FT’s part.”

The company was originally co-founded as WhiteHat and is officially rebranding today. Co-founder Euan Blair (who happens to be the son of the former U.K. Prime Minister Tony Blair and his accomplished barrister wife Cherie Booth Blair) said the name change was because the original name was a reference to how the startup sought to “hack the system for good.”

However, he added, “The scale has become bigger and more evolved.” The new name is to convey that — as in gaming, which is probably the arena where you might have heard this term before — “anything is possible.”

There are “multiple universes” one can inhabit as a post-18 young adult, Blair continued. While it’s been assumed that to get into tech, the obvious route was a two-to-four year (and often more) tour through college or university to pick up a higher education degree, the bet that Multiverse is making here is that apprenticeships can easily, and widely, become another. “We want to build an outstanding alternative to university and college,” he said. These typically last 1.5 years.

The idea of an “outstanding alternative” is especially important when thinking of how to target more marginalized groups and how this ties up with how tech companies are looking to be more diverse in the future, without cutting down on the quality of what people are getting out of the experience, or the resulting talent that is getting recruited.

There’s long been a stigma attached to less prestigious institutions, and putting money or effort into another channel to perpetuate that doesn’t really make sense or point to progress.

Blair said that currently over half of the people making their way through Multiverse are people of color, and 57% are women, and the plan is to build tools to make that an even firmer part of its mission.

The startup sees itself as part tech company and part education enterprise.

It works with tech companies and others to open up opportunities for people who have not had any higher education or any training, where fresh high school graduates can come in, learn the ropes of a job while getting paid and then continue on working their way up the ladder with that knowledge base in place.

Apprenticeships on the platform right now range from data analysts through to exhibition designers, and the idea is that by opening up and targeting the U.S. market, the breadth, number and location of roles will grow.

This is not just a social enterprise: There is actual money in this area. Blair said that prices it charges the companies it works with range by qualification, “but are broadly around the $15,000 mark.” (The individuals applying don’t pay anything, and they will also be paid by the companies providing the apprenticeships.)

On the educational front, Multiverse doesn’t just connect people as a recruiter might: it has a team in place to build out what the “curriculum” might be for a particular apprenticeship, and how to deliver and train people with the requisite skills alongside the practice experience of working, and more.

That latter role, of course, has taken on a more poignant dimension in the last year: Concepts like remote training and virtual mentorship have very much come into their own at a time when offices are largely standing empty to help reduce the spread of COVID-19.

Regardless of what happens in the year ahead — fingers crossed that vaccinations and other efforts will help us collectively move past where we are right now — many believe that the infrastructure that has been put into place to keep working virtually will continue to be used, which bodes well for a company like Multiverse that is building a business around that, both with technology it creates itself and will bring in from third parties and partners.

Indeed, the ecosystem of companies building tools to deliver educational content, provide training and work collaboratively has really boomed in the pandemic, giving companies like Multiverse a large library of options for how to bring people into new work situations. (Google, which is now an investor in Multiverse, is very much one of the makers of such education tools.)

Apprenticeships are an interesting area for a startup to tackle. Traditionally, it’s a term that would have been associated mainly with skilled labor positions, rather than “knowledge workers.”

But you can argue that with the bigger swing that the globe has seen away from industrial and towards knowledge economies, there is an argument to be made for building more enterprises and opportunities for an ever wider pool of users, rather than expecting everyone to be shoehorned into the models of the last 50 years. (The latter would essentially imply that college is possibly the only way up.)

You might also be fair to claim that Blair’s connections helped him secure funding and open doors with would-be customers, and that might well be the case, but ultimately the startup will live or die by how well it executes on its premise, whether it finds a good way to connect more people, engage them in opportunities and keep them on board.

This is what really attracted the investors, said Joel Cutler, managing director and co-founder of General Catalyst.

“Euan has a genuine belief that this is important, and when you talk to him, you get a feeling of manifest destiny,” Cutler said in an interview. In response to the question of family connections, he said that this was precisely the kind of issue that the technology industry should be tackling to fight.

“Of all the industries to break the mold of where you went to school, it should be the tech world that will do that, since it is far more of a meritocracy than others. This is the perfect place to start to break that mold,” he said. “Education will be super valuable but apprenticeships will also be important.” He noted that another company that General Catalyst invests in, Guild Education, is addressing similar opportunities, or rather the gaps in current opportunities, for older people.

Powered by WPeMatico

Healthcare startup Color has raised a sizable $167 million in Series D funding round, at a valuation of $1.5 billion post-money, the company announced today. This brings the total raised by Color to $278 million, with its latest large round intended to help it build on a record year of growth in 2020 with even more expansion to help put in place key health infrastructure systems across the U.S. — including those related to the “last mile” delivery of COVID-19 vaccines.

This latest investment into Color was led by General Catalyst, and by funds invested by T. Rowe Price, along with participation from Viking Global investors as well as others. Alongside the funding, the company is also bringing on a number of key senior executives, including Claire Vo (formerly of Optimizely) as chief product officer, Emily Reuter (formerly of Uber, where she played a key role in its IPO process) as VP of Strategy and Operations, and Ashley Chandler (formerly of Stripe) as VP of Marketing.

“I think with the [COVID-19] crisis, it’s really shone the light on that lack of infrastructure. We saw it multiple times, with lab testing, with antigen testing and now with vaccines,” Color CEO and co-founder Othman Laraki told me in an interview. “The model that we’ve been developing, that’s been working really well and we feel like this is the opportunity to really scale it in a very major way. I think literally what’s happening is the building of the public health infrastructure for the country that’s starting off from a technology-first model, as opposed to, what ends up happening in a lot of industries, which is you start off taking your existing logistics and assets, and add technology to them.”

Color’s 2020 was a record year for the company, thanks in part to partnerships like the one it formed with San Francisco to establish testing for healthcare workers and residents. Laraki told me they did about five-fold their prior year’s business, and while the company is already set up to grow on its own sustainably based on the revenue it pulls in from customers, its ambitions and plans for 2021 and beyond made this the right time to help it accelerate further with the addition of more capital.

Laraki described Color’s approach as one that is both cost-efficient for the company, and also significant cost-saving for the healthcare providers it works with. He likens their approach to the shift that happened in retail with the move to online sales — and the contribution of one industry heavyweight in particular.

“At some point, you build Amazon — a technology-first stack that’s optimized around access and scale,” Laraki said. “I think that’s literally what we’re seeing now with healthcare. What’s kind of getting catalyzed right now is we’ve been realizing it applies to the COVID crisis, but also, we started actually working on that for prevention and I think actually it’s going to be applying to a huge surface area in healthcare; basically all the aspects of health that are not acute care where you don’t need to show up in hospital.”

Ultimately, Color’s approach is to rethink healthcare delivery in order to “make it accessible at the edge directly in people’s lives,” with “low transaction costs,” in a way that’s “scalable, [and] doesn’t use a lot of clinical resourcing,” Laraki says. He notes that this is actually very possible once you reasses the problem without relying on a lot of accepted knowledge about the way things are done today, which result in a “heavy stack” versus what you actually need to deliver the desired outcomes.

Laraki doesn’t think the problem is easy to solve — on the contrary, he acknowledges that 2021 is likely to be even more difficult and challenging than 2020 in many ways for the healthcare industry, and we’ve already begun to see evidence of that in the many challenges already faced by vaccine distribution and delivery in its initial rollout. But he’s optimistic about Color’s ability to help address those challenges, and to build out a “last mile” delivery system for crucial care that expands accessibility, while also making sure things are done right.

“When you take a step back, doing COVID testing or COVID vaccinations … those are not complex procedures at all — they’re extremely simple procedures,” he said. “What’s hard is doing them massive scale and with a very low transaction cost to the individual and to the system. And that’s a very different tooling.”

Powered by WPeMatico

General Catalyst has made early bets on some of the biggest companies in tech today, including Airbnb, Lemonade and Warby Parker.

We sat down with Katherine Boyle and Peter Boyce, who co-lead the firm’s seed-stage investments, to discuss what they look for in founders, which sectors they’re most excited about and how business has changed in the wake of the COVID-19 pandemic.

This conversation is part of our broader Extra Crunch Live series, where we sit down with VCs and founders to discuss startup core competencies and get advice. We’ve spoken to folks like Aileen Lee, Mark Cuban, Roelof Botha, Charles Hudson and many, others. You can browse the full library of episodes here.

Check out our full conversation with Boyce and Boyle in the YouTube video below, or skim the text for the highlights.

Katherine Boyle: I look for what I would call this obsessive trait, where they are learning more about the regulatory complications, where they are constantly trying to figure out how to solve a problem.

I’d say that the common theme among the founders that I support are that they have this sort of obsessive gene or personality, where they will go deeper and deeper and deeper. When we invest in these companies, it becomes very clear that they often have sort of a contrarian view of the industry. Maybe they are not industry-native. They come at it from a different perspective of problem solving. They’ve had to defend that thesis for a very, very long time in front of a variety of different customers and different people. In some ways, that makes them much stronger in terms of the way they approach problems.

Peter Boyce: I think the first would be being magnetic for talent. It ends up influencing the speed of learning and development. Really incredible founding teams that can be magnetic for talent and learning just kind of spirals out of control in really good ways over time. I really look for the speed and the sources of learning. And can folks be really intentional? Can they get the right set of advisors and teammates around them?

The second would be the personal connection to the problem space. It’s like there’s this kind of deep-seated source of energy and fuel that actually isn’t going to run out. Catherine and I’ve been lucky to work across a number of different particular thematic areas, but the thing they have in common is just this personal connection to how and why their business needs to exist. Because I just think that that fuel doesn’t run out, you know what I mean? Like, that’s renewable.

Boyle: If you’re someone who’s comfortable presenting on Zoom, making connections on Zoom, or using Signal and using Twitter and being very online, then I 100% think that you can make investments, build community and build connections through digital worlds and digital platforms. If you really like that in-person connectivity, then you might consider staying in a tech hub, or you might consider sort of these distanced walks until things go back to normal.

Powered by WPeMatico

Cityblock Health, a company that provides healthcare services to low-income communities, is now commanding a high-priced valuation of over $1 billion after venture capitalists poured $160 million into the company.

The round was led by new investor General Catalyst with participation from crossover investor Wellington Management and support from major existing investors, including Kinnevik AB, Maverick Ventures, Thrive Capital, Redpoint Ventures and more, according to a statement from the company.

Cityblock works with community caregivers to work with residents to provide primary care, behavioral health and other services to address social determinants of health, in person and… increasingly… through virtual consultations.

The company first spun out of Alphabet’s Sidewalk Labs in 2017 and initially partnered with EmblemHealth. By relying primarily on licensed clinical social workers, community health partners and a network of specialized practice clinicians and doctors to provide basic primary care and supporting health services, Cityblock believes it can drive down the costs of healthcare.

Some 70,000 patients use Cityblock services in four major U.S. cities, the company said.

To date, Cityblock has raised $300 million.

The company said in a statement that the new funding will be used to support Cityblock’s national expansion in caring for Medicaid and dually-eligible communities, to attract and onboard talent across its product, engineering, data science, clinical and business operations, to launch new service lines and to continue investing in its proprietary technology platform, Commons.

Powered by WPeMatico