gartner

Auto Added by WPeMatico

Auto Added by WPeMatico

Like countless other industries, mobile phone sales got hit hard in 2020. The industry hit a 10.5% decline for the year, as COVID-19 first decimated the supply and later consumer demand for devices. It was the latest in a rough couple of years for manufacturers, but 2020 hit significantly harder than most.

New numbers from Gartner point to a rebound to pre-2020 levels. The firm is forecasting 1.5 billion devices shipped globally for 2021, amounting to an 11.4% increase across the board. We certainly saw the beginnings of that rebound arrive in Q4 for last year, as declines continued to slow, thanks in no small part to a record quarter for iPhone sales.

That points to the beginnings of a so-called “supercycle” for Apple, which hits a sort of perfect storm. The last few years have seen consumers slow down upgrades, as device prices increased, features were generally less compelling and their existing devices were perfectly fine so as not to warrant a standard two to three year upgrade pattern.

Analysts pointed to 5G as a clear conduit for righting slipping sales numbers early last year, but a global pandemic very much threw a wrench in all of that. If anything, however, the iPhone’s COVID-19-related delay actually contributed to a stellar quarter for the company, both in time for holiday sales and the arrival of multiple vaccines that pointed to some potential return to normalcy.

The long-awaited 5G bump will continue in 2021, according to the new numbers, coupled with a quick push to offer next-gen wireless at an accessible price.

“The growing availability of 5G networks coupled with a higher variety of 5G smartphones starting at $200 will steer demand in mature markets and China,” the firm notes. “Demand in emerging countries will be driven by buyers looking for a smartphone with better specifications and a 5G connectivity as an optional feature. Gartner forecasts sales of 5G smartphones will total 539 million units worldwide in 2021, which will represent 35% of total smartphone sales in that year.”

Powered by WPeMatico

We are now into the all-important holiday sales period, and new numbers from Gartner point to some recovery underway for the smartphone market as vendors roll out a raft of new 5G handsets.

Q3 smartphone figures from the analysts published today showed that smartphone unit sales were 366 million units, a decline of 5.7% globally compared to the same period last year. Yes, it’s a drop; but it is still a clear improvement on the first half of this year, when sales slumped by 20% in each quarter, due largely to the effects of COVID-19 on spending and consumer confidence overall.

That confidence is being further bolstered by some other signals. We are coming out of a relatively strong string of sales days over the Thanksgiving weekend, traditionally the “opening” of the holiday sales cycle. While sales on Thursday and Black Friday were at the lower end of predicted estimates, they still set records over previous years. With a lot of tech like smartphones often bought online, this could point to stronger numbers for smartphone sales as well.

On top of that, last week IDC — which also tracks and analyses smartphones sales — published a report predicting that sales would grow 2.4% in Q4 compared to 2019’s Q4. Its take is that while 5G smartphones will drive buying, prices still need to come down on these newer generation handsets to really see them hit with wider audiences. The average selling price for a 5G-enabled smartphone in 2020 is $611, said IDC, but it thinks that by 2024 that will come down to $453, likely driven by Android-powered handsets, which have collectively dominated smartphone sales for years.

Indeed, in terms of brands, Samsung, with its Android devices, continued to lead the pack in terms of overall units, with 80.8 million units, and a 22% market share. In fact, the Korean handset maker and China’s Xiaomi were the only two in the top five to see growth in their sales in the quarter, respectively at 2.2% and 34.9%. Xiaomi’s numbers were strong enough to see it overtake Apple for the quarter to become the number-three slot in terms of overall sales rankings. Huawei just about held on to number two. See the full chart further down in this story with more detail.

Also worth noting: overall mobile sales — a figure that includes both smartphones and feature phones — were down 8.7% 401 million units. That underscores not just how few feature phones are selling at the moment (smartphones can often even be cheaper to buy, depending on the brands involved or the carrier bundles), but also that those less sophisticated devices are seeing even more sales pressure than more advanced models.

It’s worth remembering that even before the global health pandemic, smartphone sales were facing slowing growth. The reasons: after a period of huge enthusiasm from consumers to pick up devices, many countries reached market penetration. And then, the latest features were too incremental to spur people to sell up and pay a premium on newer models.

In that context, the big hope from the industry has been 5G, which has been marketed by both carriers and handset makers as having more data efficiency and speed than older technologies. Yet when you look at the wider roadmap for 5G, rollout has remained patchy, and consumers by and large are still not fully convinced they need it.

Notably, in this past quarter, there is still some evidence that emerging/developing markets continue to have an impact on growth — in contrast to new features being drivers in penetrated markets.

“Early signs of recovery can be seen in a few markets, including parts of mature Asia/Pacific and Latin America. Near normal conditions in China improved smartphone production to fill in the supply gap in the third quarter which benefited sales to some extent,” said Anshul Gupta, senior research director at Gartner, in a statement. “For the first time this year, smartphone sales to end users in three of the top five markets i.e., India, Indonesia and Brazil increased, growing 9.3%, 8.5% and 3.3%, respectively.”

The more positive Q3 figures coincide with a period this summer that saw new Covid-19 cases slowing down in many places and the relaxation of many restrictions, so now all eyes are on this coming holiday period, at a time when Covid-19 cases have picked up with a vengeance, and with no rollout (yet) of large-scale vaccination or therapeutic programs. That is having an inevitable drag on the economy.

“Consumers are limiting their discretionary spend even as some lockdown conditions have started to improve,” said Gupta of the Q3 numbers. “Global smartphone sales experienced moderate growth from the second quarter of 2020 to the third quarter. This was due to pent-up demand from previous quarters.”

Digging into the numbers, Samsung has held on to its top spot, although its growth was significantly less strong in the quarter. Even with that slump, Samsung is still a long way ahead.

That is in part because number-two Huawei, with 51.8 million units sold, was down by more than 21% since last year. It has been having a hard time in the wake of a public relations crisis after sanctions in the US and UK, due to accusations that its equipment is used by China for spying. (Those UK sanctions, indeed, have been brought up in timing, just as of last night.)

That also led Huawei earlier this month to confirm the long-rumored plan to sell off its Honor smartphone division. That deal will involve selling the division, reportedly valued at around $15 billion, to a consortium of companies.

It will be interesting to see how Apple’s small decline of 0.6% to 40.6 million units to Xiaomi’s 44.4 million, will shift in the next quarter, on the back of the company launching a new raft of iPhone 12 devices.

“Apple sold 40.5 million units in the third quarter of 2020, a decline of 0.6% as compared to 2019,” said Annette Zimmermann, research vice president at Gartner, in a statement. “The slight decrease was mainly due to Apple’s delayed shipment start of its new 2020 iPhone generation, which in previous years would always start mid/end September. This year, the launch event and shipment start began 4 weeks later than usual.”

Oppo, which is still not available through carriers or retail partners in the US, rounded out the top five sellers with just under 30 million phones sold. The fact that it and Xiaomi do so well despite not really having a phone presence in the US is an interesting testament to what kind of role the US plays in the global smartphone market: huge in terms of perception, but perhaps less so when the chips are down.

“Others” — that category that can take in the long tail of players who make phones, continues to be a huge force, accounting for more sales than any one of the top five. That underscores the fragmentation in the Android-based smartphone industry, but all the same, its collective numbers were in decline, a sign that consumers are indeed slowly continuing to consolidate around a smaller group of trusted brands.

| Vendor | 3Q20

Units |

3Q20 Market Share (%) | 3Q19

Units |

3Q19 Market Share (%) | 3Q20-3Q19 Growth (%) |

| Samsung | 80,816.0 | 22.0 | 79,056.7 | 20.3 | 2.2 |

| Huawei | 51,830.9 | 14.1 | 65,822.0 | 16.9 | -21.3 |

| Xiaomi | 44,405.4 | 12.1 | 32,927.9 | 8.5 | 34.9 |

| Apple | 40,598.4 | 11.1 | 40,833.0 | 10.5 | -0.6 |

| OPPO | 29,890.4 | 8.2 | 30,581.4 | 7.9 | -2.3 |

| Others | 119,117.4 | 32.5 | 139,586.7 | 35.9 | -14.7 |

| Total | 366,658.6 | 100.0 | 388,807.7 | 100.0 | -5.7 |

Source: Gartner (November 2020)

Powered by WPeMatico

The last couple of years have been tough on the smartphone industry, as sales plateaued and eventually eroded. But nothing could have prepared manufacturers for 2020. This was supposed to be the year numbers began bouncing back, courtesy of 5G and some radical new designs. But the real figures have been utterly dismal.

According to new numbers out of Gartner, worldwide sales dropped 20.4% for the second quarter. The numbers are in keeping with the drops seen in Q1. The culprit is, of course, COVID-19. Global lockdowns and slowed economies have led to further decreasing interest in smartphones. As many users have shifted disposable income to upgrading their home offices, they’ve understandably deprioritized mobile devices, accelerating recent trends.

Samsung was the hardest hit of the top five, dropping a massive 27.1% year-over-year. “Demand for its flagship S Series smartphones did little to revive its smartphone sales globally,” Gartner Senior Research Director Anshul Gupta said in a release tied to the news. The company is no doubt banking on the recent Galaxy Note 20 launch to help reverse course.

Samsung’s decline puts it in a virtual tie with Huawei for first place, with the two companies accounting for 18.6% and 18.4% of the overall market, respectively. While Huawei sales actually decided 6.8% overall, its figures were still strong enough to see an increase in the overall market share for the quarter. The company also saw a rise in sales of 27.4% between Q1 and Q2. Apple, meanwhile, experienced a slight y-o-y dip of 0.4% — a relatively strong showing, all things considered.

In terms of markets, China dipped 7% for the quarter. India, meanwhile, saw the largest drop — down 46%, courtesy of lockdown protocols.

Powered by WPeMatico

More dismal numbers confirm what we already knew: Q1 2020 was real rough for an already struggling smartphone category. Gartner’s latest report puts the global market at a 20.2% slide versus the same time last year, thanks in large part to fallout from the COVID-19 pandemic.

Every single one of the global top-five manufactures saw large declines for the quarter, save for Xiaomi, which saw a slight uptick of 1.4%. The Chinese handset maker got a surprise bump, courtesy of international sales. Samsung and Huawei and Oppo all saw double-digit drop-offs at 22.7%, 27.3% and 19.1%, while Apple declined 8.2%. Other companies combined for a sizable 24.2% loss for Q1.

The reasons are ones we’ve gone over several times before, nearly all pertaining to the global pandemic. Chief among them are global stay at home orders and general economic uncertainly. Issues with the global supply chain have no doubt been a factor, as well, as Asia was the first to get hit with the virus.

All of this comes in addition to an already plateauing/declining smartphone market. Analysts had expected that the arrival of 5G would help stem the tide a bit — but, well, some stuff happened in there. Notably, Apple’s slide wasn’t as bad as it might have been thanks to a strong start to the year.

“If COVID-19 did not happen, the vendor would have likely seen its iPhone sales reached record level in the quarter. Supply chain disruptions and declining consumer spending put a halt to this positive trend in February,” Gartner’s Annette Zimmermann said in a release. “Apple’s ability to serve clients via its online stores and its production returning to near normal levels at the end of March helped recover some of the early positive momentum.”

Overall, I suspect that recovery won’t be instantaneous for the market. The future of COVID-19 still feels largely uncertain as countries have begun the process of reopening, and a pricey investment still may not be in the cards for many who are struggling to make ends meet.

Powered by WPeMatico

Last year saw global smartphone sales decline for the first time since analysts started tracking such things. In Gartner’s case, that comprises a full 11 years, as figures dropped 2% for 2019. Following on last week’s global device forecast, the firm is drilling down on smartphone figures with some slightly rosier results.

According to the new numbers from the firm, global smartphone rates are expected to reverse course slightly for 2020, with a predicted 3% bump in worldwide sales. It’s a minor success, but after a few years of stagnation and then decline, a small victory is a victory no less.

I won’t dig too far into why numbers have been falling lately (I’d direct you here instead), but 2020 is expected to be the first year the move to 5G will finally see some real, tangible payoff for manufacturers. Apple, of course, is expected to get into the game at the end of the year, with the next iPhone, while a new batch of Qualcomm chips are helping to make cheaper 5G devices a reality.

5G phone sales are expected to have their largest impact in China and the broader Asia/Pacific regions. Those areas are expected to increase at 5.1% and 5.7% in overall sales, year over year, respectively. The Middle East and North Africa region, meanwhile, should get the biggest bump, at 5.9% for the year.

Ultimately, 5G may only be a temporary solution to declining smartphone sales. Without a radical shift in form factor or functionality, it’s hard to imagine smartphone sales seeing a substantial course correction in the coming years.

Powered by WPeMatico

In some corners, the smartphone market is showing its first signs of life in some time.

Recent figures from Canalys indicate a small but notable uptick in the European market as shipments grew 3%, year-over-year in Q3.

The analyst firm put global growth at 1% globally in another recent report. Generally, such numbers wouldn’t warrant much celebration, but the way the market has been going, most manufacturers will take what they can get.

New numbers out this morning from Gartner paint a less rosy picture, with sales numbers declining 0.4%. It’s not a huge discrepancy between shipping and sales figures, but it’s the difference between being in the red and being in the black for the quarter.

Powered by WPeMatico

Stop me if you’ve heard this one before. Smartphone sales are down. Again. After years of growth, the smartphone market’s recent slide has continued into the second quarter of 2019, per numbers from analyst group, Gartner.

At 1.7% year over year, it’s not a huge slice of the overall pie, but it does point to a continued problem for manufacturers, dropping from 374 million to 368 million. The biggest hit continues to be in the high end of the market, as higher prices coupled with longer refresh cycles and fewer compelling features continue to contribute to the decline.

Of the top five markets, only China and Brazil saw growth. At 0.5%, however, China’s slight bump wasn’t enough to turn things around. Interestingly, Gartner notes that some of China’s growth may be due to manufacturers looking to move old flagship stock to make way for 5G models. Additional 5G phones, coupled with more carrier coverage, could drive sales a bit as well in future quarters.

The number two market, India, saw a 2.3% drop y-o-y, as consumer upgrades from feature phones to smartphones began to slow. The firm anticipates that sales will continue to remain slow through the end of 2019.

Apple continued to see declines, though those have slowed compared to the hit it took in the first quarter. Samsung and Huawei, meanwhile, were rare bright spots. Samsung’s growth was led primarily by mid-range and entry-level handsets like its Galaxy A series, while the deferment of Huawei’s U.S. ban helped boost its sale a bit for the quarter.

Powered by WPeMatico

Smartphone sales have continued their global decline. New numbers from Gartner forecast a drop of 2.5% down to 1.5 billion. The biggest hits to the industry are Japan, Western Europe and North America, which saw drops of 6.5, 5.3 and 4.4%, respectively.

It’s all part of a continued trend we’ve highlighted several times before: slowed upgrade cycles, pricier phones, a bad economy. Even the world’s largest smartphone market, China, saw a drop for the year, as it battles its own economic headwinds.

The Huawei ban has also impacted some of the larger numbers, though Huawei itself has continued to grow, thanks to healthy continued adoption in its home market. The company, however, is still suffering from negative connotations abroad, while cutting off access to U.S.-based companies will likely halt things further.

The good news for manufacturers in all this is a rebound set for the second half of next year, driven by 5G. The first handsets have started to arrive this year, with others (including the iPhone) not expected until next. A lot’s going to have to happen for sales to reverse the downward trends — even temporarily. That’s going to take more handsets, wider 5G availability and lower prices, with many topping out well over $1,000 here in the States.

Powered by WPeMatico

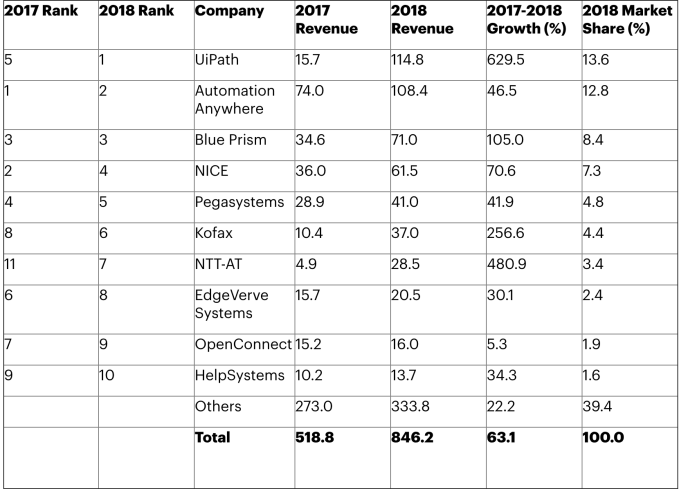

If you asked the average person on the street what Robotic Process Automation is, most probably wouldn’t have a clue. Yet new data from Gartner finds the RPA market grew over 63% last year, making it the fastest growing enterprise software category. It is worth noting, however, that the overall market value of $846.2 million remains rather modest compared to other multi-billion dollar enterprise software categories.

RPA helps companies automate a set of highly manual processes.The beauty of RPA, and why companies like it so much, is that it enables customers to bring a level of automation to legacy processes without having to rip and replace the legacy systems.

As Gartner points out, this plays well in companies with large amounts of legacy infrastructure like banks, insurance companies, telcos and utilities.”The ability to integrate legacy systems is the key driver for RPA projects. By using this technology, organizations can quickly accelerate their digital transformation initiatives, while unlocking the value associated with past technology investments,” Fabrizio Biscotti, research vice president at Gartner said in a statement.

The biggest winner in this rapidly growing market is UIPath, the startup that raised $568 million on a fat $7 billion valuation last year. One reason it’s attracted so much attention is its incredible growth trajectory. Consider that UIPath brought in $15.7 million in revenue in 2017 and increased that by a whopping 629.5% to $114.8 million last year. That kind of growth tends to get you noticed. It was good for 13.6% marketshare and first place, all the way up from fifth place in 2017, according to Gartner.

Another startup nearly as hot as UIPath is Automation Anywhere, which grabbed $300M from SoftBank at a $2.6B valuation last year. The two companies have raised a gaudy $1.5 billion between them with UIPath bringing in an even $1 billion and Automation Anywhere getting $550 million, according to Crunchbase.

Automation Anywhere revenue grew from $74 million to $108.4 million, a growth clip of 46.5%, good for second place and 12.8 percent marketshare. Automation Anywhere was supplanted in first place by UIPath last year.

Blue Prism, which went public in 2016, issued $130 million in stock last year to raise some more funds, probably to help keep up with UIPath and Automation Anywhere. Whatever the reason, it more than doubled its revenue from $34.6 million to $71 million, a healthy growth rate of 105 percent, good for third place with 8.4 percent marketshare.

For now, everyone it seems is winning as the market grows in leaps and bounds. In fact, the growth numbers down the line are impressive with NTT-ATT growing 456% and Kofax growing 256% year over year as two prime examples, but even with those growth numbers, the marketshare begins to fragment into much smaller bites.

While the market is still very much in a development phase, which could account for this level of growth and jockeying for market position, at some point that fragmentation at the bottom of the market might lead to consolidation as companies try to buy additional marketshare.

Powered by WPeMatico

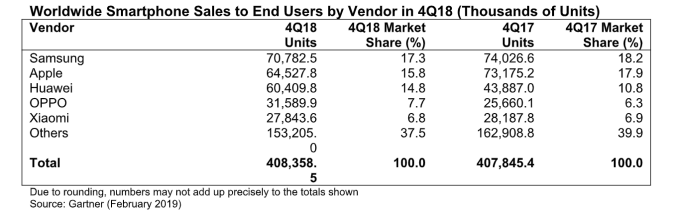

Gartner’s smartphone market share data for the just gone holiday quarter highlights the challenge for device makers going into the world’s biggest mobile trade show, which kicks off in Barcelona next week: The analyst’s data shows global smartphone sales stalled in Q4 2018, with growth of just 0.1 percent over 2017’s holiday quarter, and 408.4 million units shipped.

tl;dr: high-end handset buyers decided not to bother upgrading their shiny slabs of touch-sensitive glass.

Gartner says Apple recorded its worst quarterly decline (11.8 percent) since Q1 2016, though the iPhone maker retained its second place position with 15.8 percent market share behind market leader Samsung (17.3 percent). Last month the company warned investors to expect reduced revenue for its fiscal Q1 — and went on to report iPhone sales down 15 percent year over year.

The South Korean mobile maker also lost share year over year (declining around 5 percent), with Gartner noting that high-end devices such as the Galaxy S9, S9+ and Note 9 struggled to drive growth, even as Chinese rivals ate into its mid-tier share.

Huawei was one of the Android rivals causing a headache for Samsung. It bucked the declining share trend of major vendors to close the gap on Apple from its third-placed slot — selling more than 60 million smartphones in the holiday quarter and expanding its share from 10.8 percent in Q4 2017 to 14.8 percent.

Gartner has dubbed 2018 “the year of Huawei,” saying it achieved the top growth of the top five global smartphone vendors and grew throughout the year.

This growth was not just in Huawei “strongholds” of China and Europe, but also in Asia/Pacific, Latin America and the Middle East, via continued investment in those regions, the analyst noted. Its expanded mid-tier Honor series helped the company exploit growth opportunities in the second half of the year, “especially in emerging markets.”

By contrast, Apple’s double-digit decline made it the worst performer of the holiday quarter among the top five global smartphone vendors, with Gartner saying iPhone demand weakened in most regions, except North America and mature Asia/Pacific.

It said iPhone sales declined most in Greater China, where it found Apple’s market share dropped to 8.8 percent in Q4 (down from 14.6 percent in the corresponding quarter of 2017). For 2018 as a whole iPhone sales were down 2.7 percent, to just over 209 million units, it added.

“Apple has to deal not only with buyers delaying upgrades as they wait for more innovative smartphones. It also continues to face compelling high-price and midprice smartphone alternatives from Chinese vendors. Both these challenges limit Apple’s unit sales growth prospects,” said Gartner’s Anshul Gupta, senior research director, in a statement.

“Demand for entry-level and midprice smartphones remained strong across markets, but demand for high-end smartphones continued to slow in the fourth quarter of 2018. Slowing incremental innovation at the high end, coupled with price increases, deterred replacement decisions for high-end smartphones,” he added.

Further down the smartphone leaderboard, Chinese OEM, Oppo, grew its global smartphone market share in Q4 to bump Chinese upstart, Xiaomi, and bag fourth place — taking 7.7 percent versus Xiaomi’s 6.8 percent for the holiday quarter.

The latter had a generally flat Q4, with just a slight decline in units shipped, according to Gartner’s data — underlining Xiaomi’s motivations for teasing a dual folding smartphone.

Because, well, with eye-catching innovation stalled among the usual suspects (who’re nonetheless raising high-end handset prices), there’s at least an opportunity for buccaneering underdogs to smash through, grab attention and poach bored consumers.

Or that’s the theory. Consumer interest in “foldables” very much remains to be tested.

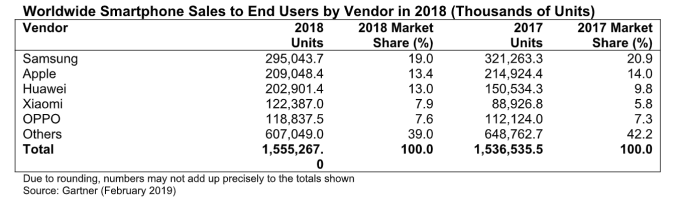

In 2018 as a whole, the analyst says global sales of smartphones to end users grew by 1.2 percent year over year, with 1.6 billion units shipped.

The worst declines of the year were in North America, mature Asia/Pacific and Greater China (6.8 percent, 3.4 percent and 3.0 percent, respectively), it added.

“In mature markets, demand for smartphones largely relies on the appeal of flagship smartphones from the top three brands — Samsung, Apple and Huawei — and two of them recorded declines in 2018,” noted Gupta.

Overall, smartphone market leader Samsung took 19.0 percent market share in 2018, down from 20.9 percent in 2017; second-placed Apple took 13.4 percent (down from 14.0 percent in 2017); third-placed Huawei took 13.0 percent (up from 9.8 percent the year before); while Xiaomi, in fourth, took a 7.9 percent share (up from 5.8 percent); and Oppo came in fifth with 7.6 percent (up from 7.3 percent).

Powered by WPeMatico