fundraising

Auto Added by WPeMatico

Auto Added by WPeMatico

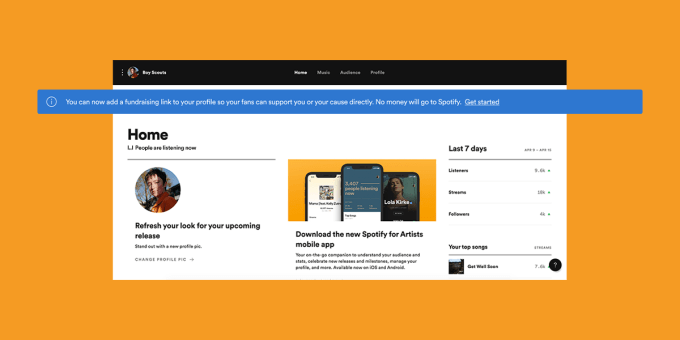

Last month, Spotify announced that as part of its coronavirus relief efforts it would soon add new fundraising features for artists on its platform. Today, the company is following through with the launch of “Artist Fundraising Pick,” a feature that allows artists to fundraise for themselves, their crews, or one of the verified music relief initiatives Spotify has already vetted through the Spotify COVID-19 Music Relief project.

At launch, Spotify is working with a small group of fundraising partners to make the donation process easier, including Cash App, GoFundMe, and PayPal.me.

Cash App is currently Spotify’s preferred method, as it has also established a $1 million relief effort for artists. When Spotify artists choose their “$cashtag” as their Artist Fundraising Pick and secure at least one donation of any size, they’ll receive an additional $100 in their account from Cash App up until a collective total of $1 million has been contributed. This works for artists in the U.S. and U.K., but Spotify users worldwide can donate through Cash App.

To use the new fundraising tools, artists (or Spotify for Artists admin users) will go to their Artist dashboard and click “Get started” on the banner at the top to submit their Fundraising Pick. This is a similar process as to how artists choose which track they want to display on their profile.

Once live, fans can donate to the cause through the artist’s profile. In addition to Cash App, PayPal is broadly available and GoFundMe is available in 19 markets.

If the artist chooses to raise for a music relief organization, they can select from those associated with Spotify’s existing charity project, which launched last month in partnership with MusiCares, PRS Foundation, and Help Musicians. It has now expanded to include a wider range of participating organizations, including several local options, and is continuing to grow.

At launch, a handful of artists already have the new feature live, including Tyrese Pope and Boy Scouts who are fundraising through Cash App; Marshmello who is fundraising for MusiCares; and Benjamin Ingrosso who is fundraising for Musikerforbundet.

Spotify says it moved to quickly launch this feature because it believed it was in a unique position to help artists raise money from a global network of fans. However, it cautions that it’s never built a fundraising feature like this before, and considers this a “first version.” Over time, the feature will likely evolve and update based on artist feedback.

“This is an incredibly difficult time for many Spotify users and people around the world — and there are many worthy causes to support at this time,” the company wrote in an announcement. “With this feature, we simply hope to enable those who have the interest and means to support artists in this time of great need, and to create another opportunity for our COVID-19 Music Relief partners to find the financial support they need to continue working in music and lift our industry,” it said.

Powered by WPeMatico

As silently and swiftly as it has devastated families and communities around the world, COVID-19 has also left many startups gasping for air. Emerging companies with strong 2020 revenue forecasts have seen their high-confidence plans reduced by 60%-80% in a matter of days. Even in the best of times, startups must reach value-unlocking milestones to successfully raise new capital. But today, a globally synchronized halt to business activity has made irrelevant normal benchmarks for financing rounds.

Obtaining payroll support from the recently enacted special government programs for small businesses will not resolve the cascading problems startups are grappling with, regardless of whether or not they are VC-backed.

Product development roadmaps in many innovation-driven industries are changing in ways that may permanently alter a company’s future strategic direction. Merger and acquisition discussions are being shelved. Normal financing rounds, in process and contemplated, are contracting or being abandoned altogether. Many venture funds, including corporate venture programs, have unilaterally “taken a pause” to reevaluate the radically changing landscape for their early-stage company portfolios.

I last experienced this phenomenon in the aftermath of the Great Technology Bubble: 2002-2003. And all signs show that we are at the beginning of a new round of punitive “incentives” for venture investors to keep their companies alive.

Several of my current portfolio companies have recently proposed “emergency bridge” convertible note financings of between $5 million and $15 million, each featuring a painful feature for non-participants: multiple liquidation preferences benefiting only the new money above 3x, with discounts greater than 20% on conversion in a new equity financing. Of course, these financings are open to both existing and new investors. But the likelihood of another round is actually diminished by this type of structure.

Powered by WPeMatico

Marty Pichinson gets called a lot of things: Silicon Valley’s undertaker, its terminator, a grave digger. These aren’t meant as slights; Pichinson is the founder of Sherwood Partners, a restructuring firm that Bay Area venture firms frequently turn to when they need someone to help sell off the assets of startups they have funded. The idea is to return at least some money to the company’s creditors and, if anything is left, to the VCs, too.

We last checked in with Pichinson almost exactly three years ago when the startup world was humming along. Even then, because of the sheer number of companies that get funded — and thus the number of startups that invariably don’t make it — Sherwood Partners was helping to wind down two to four companies a week.

Now, as he told us in conversation last week, it’s winding down two to three companies every day.

So who is shutting down, how does it all work and what can VCs expect to get in terms of a return in the age of the coronavirus?

Right now, Pichinson says the shutdowns are across verticals and across stages. “We’re in companies that raised $10 million to $25 million, to companies that raised up to $1.5 billion. It doesn’t matter what size they are; when they come to us, they’re all broke. If we’re closing it down to clean up and monetize what we can, they are basically in the same position, whether they raised $20 million or they were once a billion-dollar business.”

Powered by WPeMatico

When Rebecca Minkoff first moved to New York City, the then-18-year-old was making $4.75 an hour.

“I just kept working for this designer and someone was telling me what to do every day. I just didn’t like that. And I thought if I’m going to work as hard, it’s going to be for myself and I want to call my own shots,” she said. “I didn’t want to be told what to do, frankly.”

Self-employment for Minkoff turned out just fine; in 2001, she redesigned the iconic “I Love New York” shirt and it appeared on The Tonight Show. After a shout-out from Jay Leno, Minkoff spent the next eight months making T-shirts on the floor of her apartment and quit her job to start designing full time.

We caught up with Minkoff to learn more about how she grew her brand into a global fashion company with the help of her brother, her problem with the unicorn mentality and why she thinks the “invisible barrier” is the future of retail tech.

This interview was edited for brevity and clarity.

TechCrunch: What gave you the energy and drive to become an entrepreneur?

Rebecca Minkoff: Long story. My mom would sell these cast covers, like decorative covers for people with broken arms at the flea market. And I was like, I am going to have a booth here. So I made all these tie-dye shirts and no one bought anything but it was just this idea of like, I can make something I can sell. My mom always taught that. When I wanted a dress, she taught me how to sew a dress instead of buying the dress. And so, I just got this bug for creating things out of nothing.

The constant thread was, “I’m not going to pay for this. You’re going to learn how to do it.”

Powered by WPeMatico

As the venture landscape adjusts to the COVID-19 pandemic and seismic shifts in public markets, early-stage VCs are reassessing which bets they’re making, along with questions they’re asking of founders who are exploring bleeding-edge technology.

Anorak’s Greg Castle

Anorak Ventures is a small seed-investment firm that bets on emerging tech like AR/VR, machine learning and robotics. I recently hopped on a Zoom call with founder Greg Castle to talk about what he’s seen recently in seed investing and how the sector is responding to the crisis. Castle was an early investor in Oculus; his other bets at Anorak include Against Gravity, 6D.ai and Anduril.

Our conversation has been edited for length and clarity.

TechCrunch: Has this pandemic affected the types of companies that you’re looking at?

Greg Castle: From my experience as an investor thus far, being reactive as an investor and looking at “hot” areas has a lot of pitfalls to be mindful of. I think a lot of the areas that excite me as an investor could benefit from what’s going on here, those areas including robotics, automation, immersive entertainment and immersive computing.

Just generally, do you feel like a recession is likely to negatively impact emerging tech more so than other areas?

Powered by WPeMatico

Yesterday, I had the pleasure of hopping on Zoom with betaworks’ John Borthwick and Matt Hartman to discuss the tech world’s adaptation to this new locked-down world, the future of new media and answer questions from the audience.

We discussed whether new media companies can raise capital right now, and touched on emerging trends around audio, voice, AR, live events, travel-related companies and many other topics.

It was a delight, and I’m excited to do more of these in the future.

For those of you who missed the Zoom, here’s a rundown of what we discussed (audio embed below).

Powered by WPeMatico

No one wants to prepare for their fundraising round to fail. Many founders spend months (or even years) getting their businesses to a point where they’re ready to pitch investors. But there are times when, no matter how hard you try, you’re just not going to be able to close a deal.

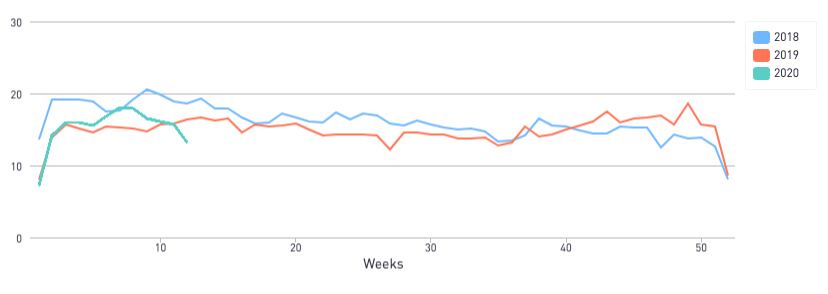

With the current COVID-19 pandemic, the entire VC community is in a state of uncertainty, and there is no clear answer when it comes to the question, “can I still raise funds for my company?” However, there’s hope for early-stage startups. We used the 2020 DocSend Startup Index to track Pitch Deck Interest among investors and found that last week, despite seismic changes across the country, pitch deck interest has only been 11.6% lower than the same week in 2019 so far.

We will be monitoring the Pitch Deck Interest Metric in the coming weeks, but if you’re an early-stage startup and you were planning to raise, there is still opportunity to come away with a term sheet. But if things don’t go as planned, how do you know if it’s time to give up or if you just need to push through?

According to recent DocSend data, you’ll know pretty quickly if it’s time to call it quits. While the average founder who was successful in fundraising contacted 63 investors during their process, startups that weren’t able to raise funds stopped at 27. Why stop? Because the founder listened to the feedback they were getting. If you hear the same concern or piece of feedback twice you should take it to heart, but if you hear it three times you probably need to stop and rethink things.

The Pitch Deck Interest Metric declined 11.6% compared to the same week in 2019

According to our study on the fundraising process of pre-seed startups, founders who were unsuccessful in raising had just nine meetings. That should give you enough feedback to know if you have a deal breaker in your deck.

But negative feedback doesn’t mean all is lost. In fact, of startups studied in the 2020 DocSend Startup Index, 86% reported that they were going to try to fundraise again after addressing the feedback they’d received.

Powered by WPeMatico

Many founders will have kicked off the new year with a new fundraising round. According to the data we shared last year, March, October and November were the months when VCs were reviewing the most decks.

But the COVID-19 pandemic has ground to a halt many industries, and there are even warnings that this will affect the next two quarters in regards to fundraising.

We’ve reviewed the data in our 2020 DocSend Startup Index and we’ve begun tracking the Pitch Deck Interest Metric. With San Francisco under a shelter-in-place order and many VCs scrambling to adjust their processes to an all-remote world, we saw pitch deck interest drop 11.6% when compared to the same week in 2019. While there has been a drop in interest so far, there is still a lot of activity, and VCs seem to still be reading pitch decks.

We will be monitoring the Pitch Deck Interest Metric in the coming weeks, but if you’re an early-stage startup and are in the middle of your fundraise, or are about to fundraise, there are some things you can do to help insure your startup is ready for funding before you meet with any (more) investors.

The Pitch Deck Interest Metric declined 11.6% compared to the same week in 2019

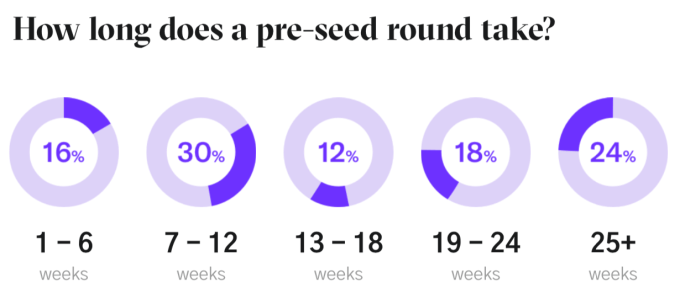

If you were about to kick off a fundraising round, you should have been prepared to contact 50 or more investors, have 20-30 meetings and spend somewhere around 20 weeks before you signed your term sheet. That’s a lot of time and energy to invest, especially when the economy is poised for a downturn and you’re most likely needed in other parts of your business.

If you’ve already started your round and are wondering if you should push through, I’ve written a piece on knowing when to quit and recalibrate versus when to push through (Extra Crunch membership required).

Many factors play into navigating a successful fundraising round, and the expectations of investors are constantly changing — specifically when it comes to the pre-seed round.

Investors are now looking for market-ready products and want to see pitch decks that feature the content they’re expecting. We expect to see this focus intensify over the coming months as VCs have more time to spend not just to review pitch decks, but on due diligence for companies in which they plan to invest. Our new report outlines advice for pre-seed startups that are looking to adjust their fundraising strategy.

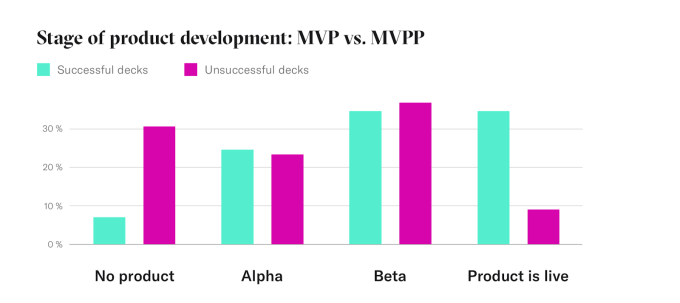

Our analysis reveals a shift in the level of readiness required by institutional investment to receive pre-seed funding. In the past, pre-seed startups could get by with just an MVPP (Minimum Viable PowerPoint). But now, investors are placing their bets on pre-seed startups that have already entered the market and developed an alpha, beta or shipping product.

In fact, 92% of companies with successful pitch decks had either an alpha, beta or shipping product, where only 68% of companies with unsuccessful pitch decks presented the same type of product readiness.

As the economy moves closer to a downturn we can expect VCs to be more cautious with their investments. The current data already shows a preference for companies that have live products; it’s worth the time and effort to be product-ready coming into a pre-seed round or if you’re a startup ready to tackle the round again with a fresh perspective.

That said, even if you do have an MVP, rethinking your pitch deck may be something else to consider. Here’s a good test. Using your pitch deck, spend three to four minutes (that’s all the time you’ll get from a VC) to pitch your business to a friend or family member who knows nothing about your business. Afterward, ask them for a one-sentence description of your company. If they’re not clearly describing what your company does and the problem it’s trying to solve, you probably need to rethink your pitch deck.

According to our recent report, a “less is more” attitude toward creating a compelling pitch deck for meetings could mean more success in pre-seed fundraising.

Your pitch deck will be your main calling card right now. As community events are being replaced with online gatherings during the COVID-19 pandemic, we can expect to see less one-to-one engagement at these events. So pitching a VC in person is not likely to happen anytime soon. Whether you’re sending them a cold email, or getting a warm intro from a portfolio company, you’re going to need to lead with your pitch deck.

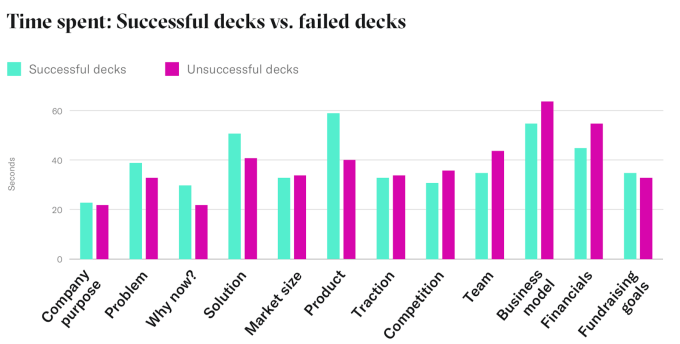

Despite the product taking a more prominent role in the fundraising round, the pitch deck is still a focal point and should be tailored to tell your story in the most effective way, as investors are spending less time evaluating them. On average, investors are spending just 3 minutes and 21 seconds on the pitch deck and the average deck is just 20 slides.

If you are in the process of reevaluating your pitch deck, it could be helpful to make sure your slides feature the right content in the right order. Investors spend nearly 50% more time on the product slides in successful pitch decks and over 18% longer on the business model in unsuccessful pitch decks. Additionally, investors spent more time on solution slides in successful decks than unsuccessful decks.

Another area that could benefit from reevaluation is the number of investors contacted, meetings held and the number of weeks spent in a funding round. Generally speaking, the average amount of investors contacted for successful fundraising rounds is 56, resulting in 26 meetings. On average, successful pre-seed startups will spend 20.5 weeks on fundraising.

When it comes to fundraising, there are diminishing returns for investor outreach. You shouldn’t need to send your deck to more than 60-70 investors and have more than 20-30 meetings. If you’re doing more than that, the ROI on your time just isn’t worth it. Because the current crisis is affecting VCs’ willingness to invest, you’re better off finding a small list of investors who are active and targeting your pitch to them. If you’ve reached out to more than 70 investors, but you’re still faced with a wall of “nos” you’re better off pausing your fundraising and addressing the feedback you’ve received so far. For more on when you should quit and reevaluate versus push through you can read my article here (Extra Crunch membership required).

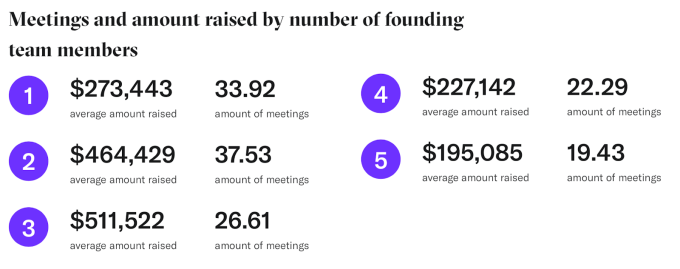

Another area pre-seed startups should evaluate is the number of founders of a company. Our data shows investors still prefer teams of two-three founders, though our data shows that being a solo founder is preferable to having too many founders. For teams of five founders, they averaged earning $195,085 while founding teams of three garnered $511,522.

This may be the right time to find a co-founder. With many people working from home or out of work, this could be the opportunity to take your idea and bring on the technical founder you need. There are online groups and events popping up everywhere in response to social distancing. If you’re worried being a solo founder is going to hold you back, you may want to invest time in those new communities.

For many startups, especially if you are not in Silicon Valley where a substantial amount of funding happens, the process of fundraising can be very opaque. DocSend’s purpose in analyzing this data is to bring some transparency to the process. This in turn provides perspective.

But what founders should do, if they haven’t done so already, is to get some additional perspective. Talk to experts outside your immediate circle of influence. Don’t have a mentor or advisors? Find them. Get a different take on your product idea or the market conditions. Especially now that community events are going virtual, location doesn’t have to hold you back from joining the startup community and finding people to offer feedback on your product or company.

Fundraising is both an art and science. Combining the insights from our data with the benefit of your own community can help you get back on your feet and pitching your company with hopefully a better outcome.

Powered by WPeMatico

Today 500 Startups hosted a virtual demo day for its 26th batch of startups, a group of companies that TechCrunch covered back in February.

500 is not the only accelerator that moved its traditional investor pitch event online; Y Combinator made a similar move after efforts to flatten the spread of COVID-19 required changes that made its traditional demo day setup temporarily impossible.

In addition to hosting a few dozen startup pitches today, 500 also explained changes to its own format and provided notes on the current state of the venture market.

Regarding how 500 Startups is shaking up how it handles its accelerator, the group intends to pivot to a rolling-admissions setup that will give participants more flexibility; the group will still hold two demo days each year — TechCrunch has more on the changes here.

Regarding the venture market, 500 Startups said venture capital’s investment pace could slow for several months. This seems likely, given how the economy has taken body blows in recent weeks as huge swaths of the world’s economy shut down. What advice did 500 have in the face of the new world? What you’d expect: startups should cut burn and focus on customers.

Got all that? OK, let’s talk about our favorite companies from the current 500 cohort.

Powered by WPeMatico

This week, Extra Crunch hosted a call with General Catalyst managing director Niko Bonatsos to discuss a number of startup topics, including what the novel coronavirus is doing to investing in the Valley, as well as his thoughts on robotics, homeschooling, edtech, SMBs, international investing and what he’s looking to see today in startups. Joining me on the live call was my fellow Equity host Alex Wilhelm and a couple of dozen EC members.

If you missed this conference call for EC members, don’t fret: We’ll have more of these to come in this era of work-from-home. In the meantime, here is a lightly edited transcript, along with a recording of the call if you’d like to listen in.

Powered by WPeMatico