France Newsletter

Auto Added by WPeMatico

Auto Added by WPeMatico

French startup Glose just raised a $3.4 million funding round (€3 million) for its reading app on iPhone, iPad and Android. The company wants to make reading books more social.

If you’re an avid book reader, chances are you always carry a pencil with you to write some notes in the margins. Or maybe you have a tiny notebook with important quotes. But that experience hasn’t worked well with e-books.

Sure, you can highlight text on your e-reader, in the Kindle app and other e-book apps. But it’s hard to do anything with them down the road. Glose wants to leverage your phone to let you do more with the book you’re currently reading.

OneRagTime, Expon Capital, Kima Ventures and Bpifrance participated in today’s funding round, as well as business angels, such as Sébastien Breteau, Patrick Bertrand and Julien Codorniou.

Glose has its own bookstore and lets you read your own DRM-free e-books. The app then keeps you motivated with reading streaks and other gamification aspects. But my favorite feature is that you can highlight text, write annotations and share them with your friends.

When your friends read the same book six months later, they can open the annotations in the margin to see what you wrote. You can follow booklists, create private reading groups and see the progress of your friends; 600,000 people have downloaded the app.

Up next, Glose wants to release a separate service called Glose Education. This version will be tailored for universities and high schools. Teachers will be able to create reading groups, assign homework, write down annotations for the class and more. This seems like a natural use case for a social reading app.

Powered by WPeMatico

French startup Lydia announced a partnership with Banque Casino today for small credit lines. Starting tomorrow, Lydia users in France will be able to borrow as much as €1,000 in just a few seconds.

While Lydia started as a peer-to-peer money transferring app, fintech startups always end up offering credit at some point. It’s hard to make money without offering some form of credit.

Banque Casino is a subsidiary of Casino and Crédit Mutuel. As the name suggests, it’s a bank that can issue credit lines. Lydia has developed a seamless integration with Banque Casino so you can instantly get money from Banque Casino.

The credit feature lets you borrow between €100 and €1,000 and reimburse that credit line over three months. If you’re eligible, you’ll instantly see how much you’ll end up paying after three months.

But the most interesting feature is that you can either get your money instantly on your Lydia account for a fee, or you can wait a couple of weeks to wave this fee.

Combining instant credit with instant spending is key to this feature. Lydia lets you instantly spend money on your Lydia account on e-commerce websites that support Lydia, using Lydia’s debit card, or using a virtual card in Apple Pay, Google Pay or Samsung Pay. And if Lydia wants to replace cash, it needs to be as quick as giving a money bill to someone.

Lydia currently has 1.5 million users; 3,500 people open a Lydia account every day. The company recently released two insurance products for your mobile devices, as well.

Powered by WPeMatico

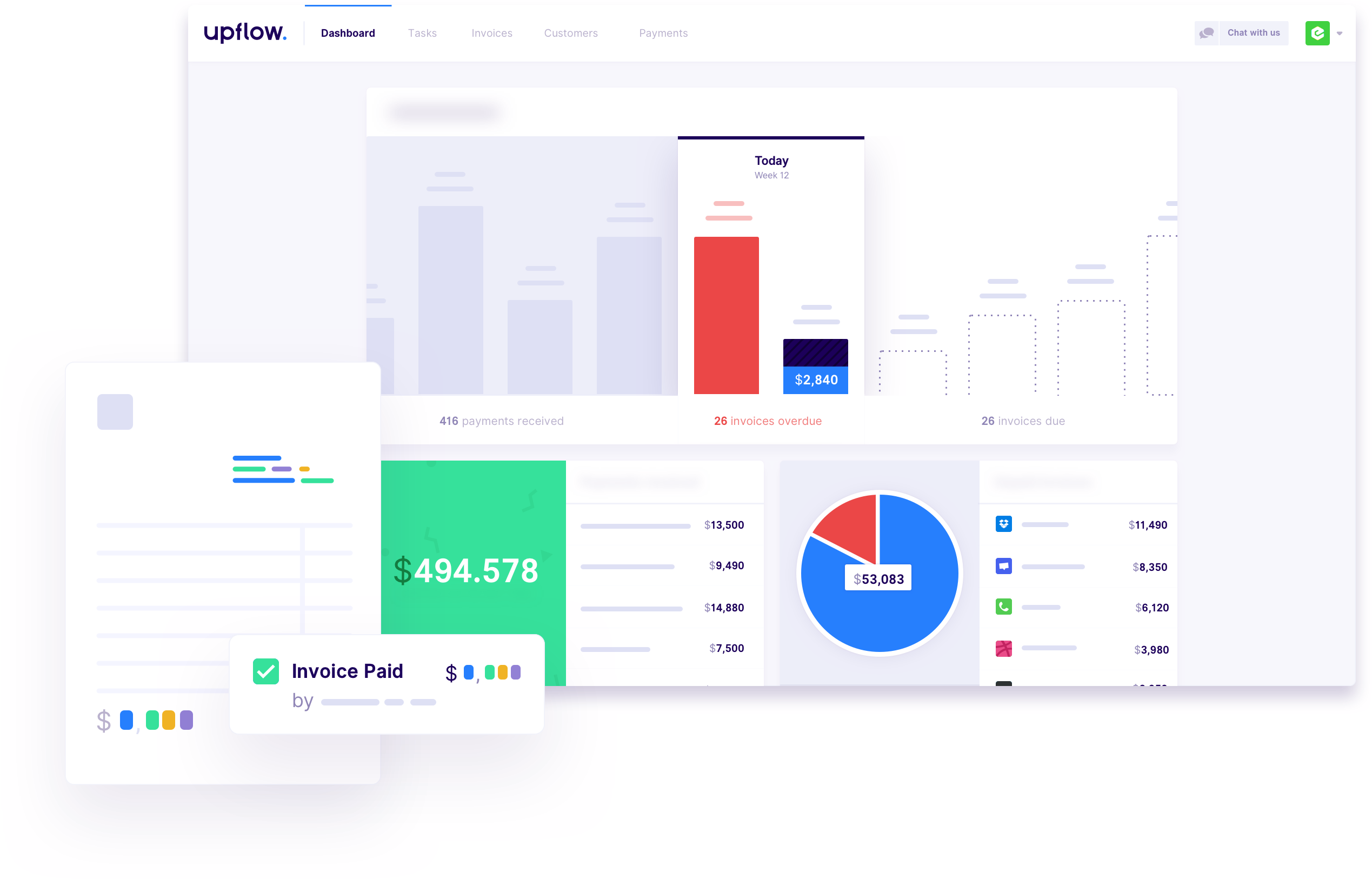

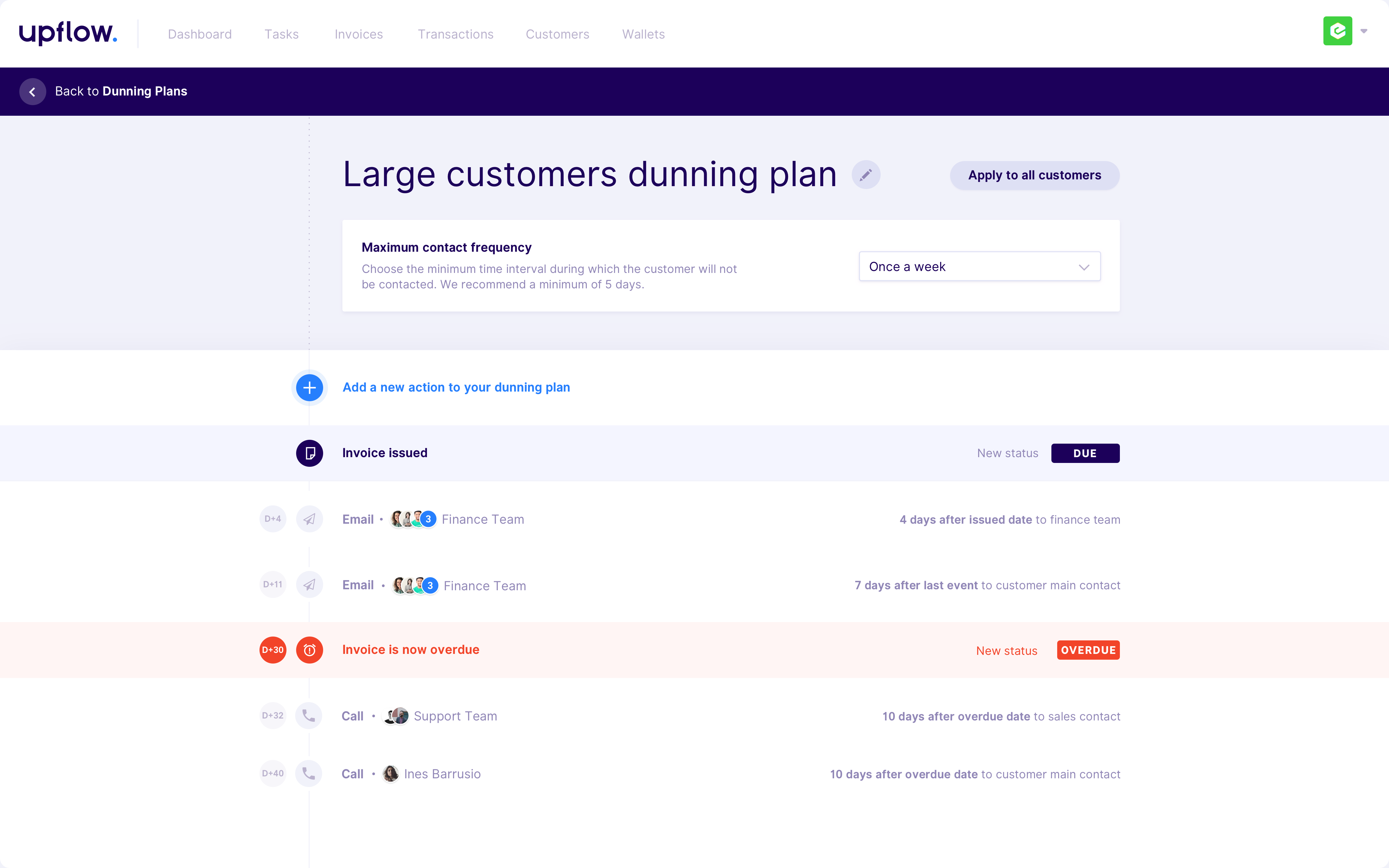

Meet Upflow a French startup that wants to help you deal with your outstanding invoices — the company first started at eFounders. If you’re running a small business, chances are you’re either wasting a ton of time or a ton of money on accounts receivable.

Most companies currently manage invoices using Excel spreadsheets, outdated banking interfaces and unnecessary conversations. Every time somebody signs a deal, they generate an invoice and file it in a spreadsheet somewhere.

Some companies will pay a few days later. But let’s be honest. Too many companies wait 30 days, 40 days or even more before even thinking about paying past due invoices. You end up sending emails, calling your clients and wasting a ton of time just collecting money. You might even feel bad about asking for money even though you already signed a deal.

In France, most companies use bank transfers to pay invoices. But business banking APIs are not there yet. It means that you have to log in to a slow banking website every day to check if somebody paid you. You can then tick a box in an Excel spreadsheet.

If everything I described resonates with you, Upflow wants to manage your invoices for you. It doesn’t replace your bank account, it doesn’t generate invoices for you. It integrates seamlessly with your existing workflow.

After signing up, you can send invoices to your client and cc Upflow in your email thread. Upflow then uses optical character recognition and automatically detects relevant data — the customer name, the amount, the due date, etc.

You can view all your outstanding invoices in Upflow’s interface to see where you stand. The service gives you a list of actionable tasks to get your money. For instance, Upflow tells you if you have overdue payments and tells you to contact your client again.

You can set up different rules depending on your clients. For instance, if you have many small clients, you can automate some of those messages. But if you only work with a handful of clients, you want to make sure that somebody has manually reviewed each message before Upflow sends them.

By default, you write your emails in Upflow so that your other team members can see what happened. You can browse invoices by client to see if somebody has multiple unpaid invoices. Upflow lets you assign actions to a particular team member if they’re more familiar with this specific client.

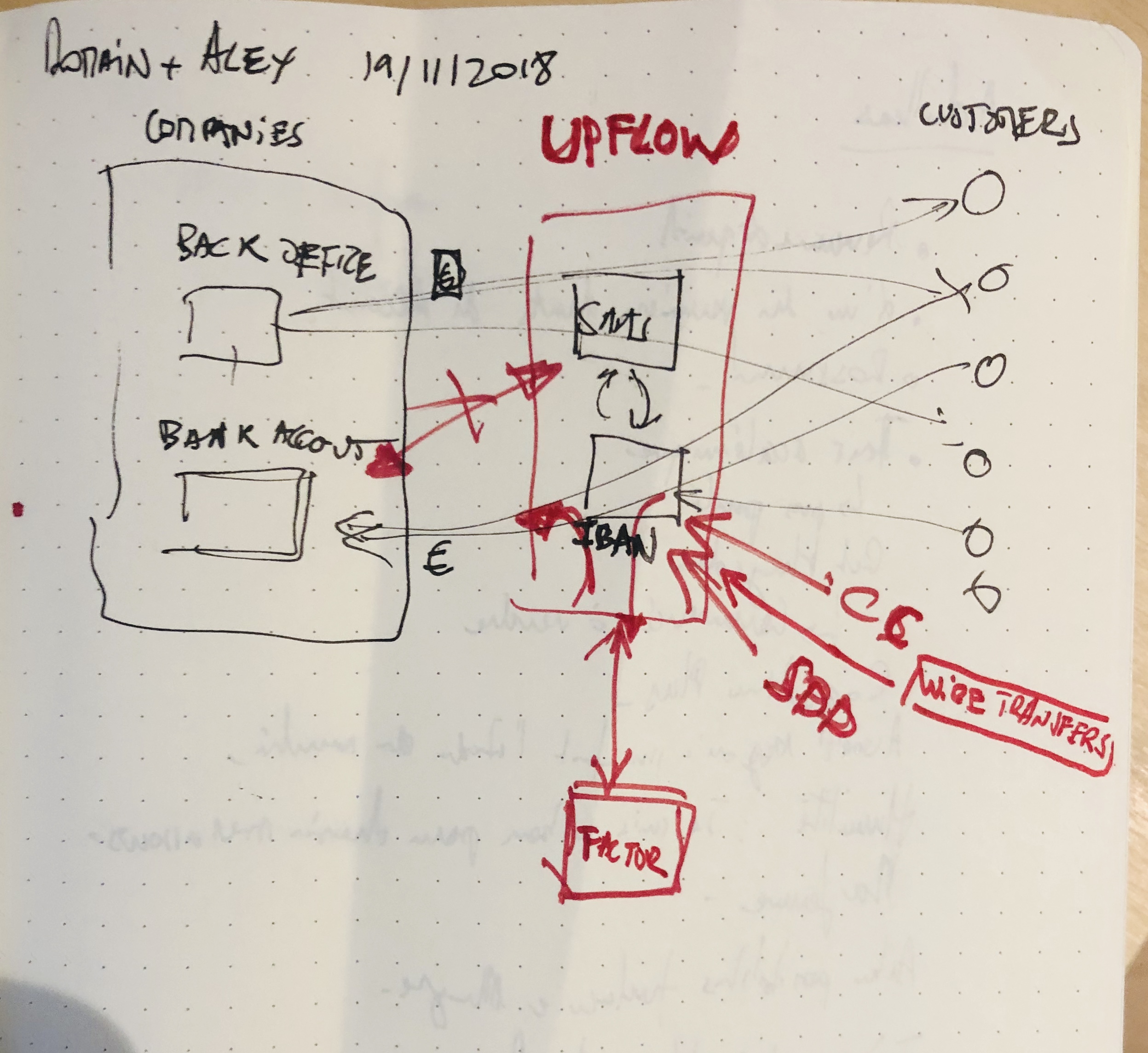

But all of this is just one part of the product. Upflow also generates banking information with the help of Treezor. This way, you can put your Upflow banking information on your invoices.

When a customer pays you, Upflow automatically matches invoices with incoming payments. This feature alone lets you save a ton of time. The startup transfers money back to your company’s bank account every day.

Upflow co-founder and CEO Alexandre Louisy drew me the following chart when we met. It’s probably easier to understand after reading my explanations:

In other words, Upflow has created a brick that sits between your company’s back office and your customers. Eventually, you could imagine more services built on top of this brick as Upflow is learning many things on your company.

According to Louisy, small and medium companies really need this kind of product — and not necessarily tech companies. Those companies don’t have a lot of money on their bank accounts, don’t have a big staff and need to save as much time as possible.

Now let’s see if it’s easy to sell a software-as-a-service solution to a family business that has been around for decades.

Powered by WPeMatico

French crowd-lending platform October (formerly known as Lendix), wants to educate more people about new ways to borrow money. That’s why the company is launching a project called Grandir Ensemble (grow together).

11 big companies are borrowing €100,000 each on October at a 2.5 percent interest rate. October users will be able to lend as little as €20 to one of these companies.

If you look at the list of companies, all those names will sound familiar to French readers and beyond. Most of them are public companies, most of them are originally from France — AccorHotels, Adecco Group, Allianz France, Arkéa, Edenred, Engie, Iliad, JCDecaux, Suez, Unibail-Rodamco-Westfield and Webhelp.

According to October, annual revenue of those companies ranges from €1.8 billion to €122 billion, with Allianz generating more revenue than anyone else.

At a press conference, October co-founder and CEO Olivier Goy explained the idea behind this project. Those credit lines won’t change anything for big public companies. But many of those companies work with small and medium companies.

Today’s partners will be able to refer small companies. October will wave the application fees for those companies up to €11 million in loans.

Thanks to this vote of confidence, you could imagine small companies applying to October because a big company they trust has done it before.

France’s Economy Minister Bruno Le Maire recorded a video message for the press conference, saying that he supports October and today’s campaign.

One of October’s key advantages compared to borrowing money from the bank is that it’s much faster. You can apply to a credit line and get an answer just a few days later. This is quite useful if you need to move quickly to launch a new product, open a new office and more.

October currently operates in France, Spain, Italy and soon the Netherlands. I already covered the company in depth back in June if you want to read more.

Powered by WPeMatico

Meet Bubble a bootstrapped startup that has been building a powerful service that lets you create a web application even if you don’t know how to code. Many small and big companies rely on Bubble for their website.

I have to say I was quite skeptical when I first heard about Bubble. Many startups have already tried to make coding as easy as playing with Lego bricks. But it’s always frustratingly limited.

Bubble is more powerful than your average website building service. It recreates all the major pillars of web programming in a visual interface.

It starts with a design tab. You start with a blank canvas and you can create web pages by dragging and dropping visual elements on the screen. You can put elements wherever you want, resize maps, text boxes, images and more. You can click on the preview button to see the development version of your time whenever your want.

In the second tab, you can create the logic behind your site. It works a bit like Automator on the Mac. You add blocks to create a chronological action. You can set some conditions within each block.

In the third tab, you can interact with your database. For instance, you can create a sign up page and store profile information in the database. At any time, you can import and export data.

There are hundreds of plugins that let you accept payments with Stripe, embed a TypeForm, use Intercom for customer support via chat, use Mixpanel, etc. You can also use your Bubble data outside of Bubble. For instance, you can build an iPhone app that relies on your Bubble database.

Many small companies started using Bubble, and it’s been working fine for some of them. For instance, Plato uses Bubble for all its back office. Qoins and Meetaway run on Bubble. Dividend Finance raised $365 million and uses Bubble.

The startup takes care of hosting your application for you. Every time you resize your instance as your application gets bigger, you pay more.

Even though the company never raised any money, it already generates $115,000 in monthly recurring revenue. Bubble is still a small startup, which can be scary for bigger customers. But the company wants to improve the product so that customers don’t see the limitations of Bubble. Now, the challenge is to grow faster than customers’ needs.

Powered by WPeMatico

French startup Lydia is launching an insurance product for your mobile phone. For €4.29 per month ($4.89), you can insure your phone from the Lydia app.

Lydia is one of the most popular peer-to-peer payment apps in Europe, with 1.5 million users. Think about it as a sort of Venmo or Square Cash for Europe. More recently, the company started offering more options to manage your money with a premium subscription and additional features.

While Lydia doesn’t want to replace your bank and insurance company, the company is offering an insurance product for the first time. Lydia is partnering with its investor CNP Assurances — having an insurance company as an investor has a few advantages.

So here’s what you get. You’re instantly covered against cracked screens, liquid damage and accidental damage. There’s no excess, but you’re limited to one claim per year. Phones now cost a small fortune, but you’re limited to €500 ($570) per claim.

Optionally, you can subscribe to a better insurance product for €9.99 per month ($11.39). In addition to phone insurance, your laptop, tablet, Nintendo Switch, Kindle, camera and other electronics are covered. You can make two claims per year and you can get back up to €500 for your phone and €1,800 for other devices. More importantly, you’re also covered against theft.

Many phone carriers sell mobile phone insurance. But they usually cost more than that. In most cases, you also need to subscribe for at least one year. In Lydia’s case, you can cancel your subscription whenever you want in the app.

If that product sounds familiar, it’s because Revolut offers a similar feature (with some drawbacks). You can subscribe to mobile phone insurance from Revolut’s mobile app.

Pricing isn’t as straightforward with Revolut, as Premium subscribers get a discount. For an iPhone X, the insurance product costs as much as €9.58 per month ($10.92) without a Revolut Premium account, or as little as €6.67 per month ($7.60) if you pay upfront and you have a Revolut Premium account.

It’s a 12-month contract with a €125 excess and no theft protection. You also need to start insuring your phone quickly after buying (within six months), otherwise you aren’t covered. Revolut works with Allianz and Simplesurance for this insurance product.

Lydia may have borrowed the idea from Revolut, but I’m not sure why you’d choose Revolut’s insurance product over Lydia’s product.

It’s interesting to see that fintech companies are creating alternative revenue streams with insurance products. Subscribing to an insurance product is quick and painless, as they already manage your money and have your card on file.

Powered by WPeMatico

Language learning company Reverso is launching a new product on the web and mobile. Reverso Synonyms is a thesaurus service that lets you learn new words and improve your vocabulary.

You may have found this feature in the main Reverso translation app already. If you translate a word or a group of words, there’s a tiny “S” button in the corner. It lets you access related words directly from the translation app.

But this was just a soft rollout, as the company is now expanding this feature into a full-fledged service. Reverso Synonyms works with a dozen languages, including English, French, Spanish…

It’s a pretty straightforward product. You can type a word and get a bunch of synonyms. You get examples and you can load the word definition for more details. You can also tap on any word to double-check the meaning.

But the service goes beyond that by offering slang translations and giving you analogies for words with multiple meanings. It also works with expressions of multiple words (“beside the point”). There will be a premium subscription with additional features.

Even more interesting than the product itself, Reverso came up with an interesting way to build a huge database in no time. Given that the company has been working for years on translation dictionaries, the company tapped this data to create a basic version of this new product.

There are 2 billion bilingual dictionary entries in Reverso Context. If two words have the same translation in multiple languages, chances are that they mean the same thing. Of course, this data has been adjusted since then with a refined algorithm and some human curation.

While Google Translate is still quite dominant in the dictionary space, Reverso manages to attract tens of millions of users every month, generating 450 million page views on the web alone. It’s an interesting startup story in a monopolistic space. While translation dictionaries will probably remain Reverso’s main product, it’s good to see some new features.

Powered by WPeMatico

Concord is raising a new $25 million funding round led by Tenaya Capital, with existing investors CRV and Alven also participating. The company is building a platform that makes it easier to manage your contracts all the way from writing them to signing them.

Even if you used a service like DocuSign to sign a contract in the past, chances are you or the sender used Microsoft Word to write the contract. It’s fine if you’re the only one working on this contract. But it can quickly become a mess as your legal team gets larger.

“It’s ultimately bringing a B2C experience to a really complex B2B experience,” VP of Marketing Travis Bickham told me.

And one of the company’s main challenge has been to make it convenient for all teams in your organization. If you work in human resources, you’re dealing with HR contracts. If you’re an office manager, you may need to sign a contract to order a new fridge. If you’re on the sales team, you want to make sure your client signs a contract. The procurement team also wants some sort of legal proof from its partners. And the list goes on.

Concord lets you create templates and workflows. For instance, the most basic contracts don’t require the same attention to details. A non-disclosure agreement is pretty standard. You just have to replace some fields and make the person sign it.

You can create an approval process for more complicated contracts. For instance, you can say that the legal team has to approve any sales contract above $100,000.

Concord has also built integrations with third-party tools. For instance, you can generate a contract in Salesforce using Concord’s integration.

There are currently 80 people working for Concord in San Francisco and Paris. With today’s funding round, the company plans to hire more people, get more clients, target bigger companies, etc. Concord currently works with 200,000 companies.

Powered by WPeMatico

French startup Alan wants to be a bit better than your good old health insurance. That’s why the company is trying something new and now covers part of your Petit Bambou subscription.

Petit Bambou is a popular meditation app. It’s a sort of Headspace, but with French content. You download an app, put your earphones, close your eyes and follow the instructions. Meditating ten or twenty minutes every day should help you feel better after a while.

The basic course is free and you need to pay a subscription to access more content. It costs €7 per month or €60 per year.

In France, health insurance companies usually cover your bills when the national healthcare system already pays for part of the bill.

For instance, if you get X-Rays for your arm, the national healthcare system will pay for part of the bill, and your health insurance will cover the rest. Usually, if something is not covered by the national healthcare system, your insurance company won’t cover it either.

But Alan wants to differentiate its offering and add more stuff. The Petit Bambou offering is just a test for now. You can get €25 back if you subscribe for six months or a year. It only works once. But Alan is thinking about turning it into a recurring offer if people like the feature.

Powered by WPeMatico

AI-powered photo management app Zyl is going back to the drawing board with a streamlined, more efficient redesign. The app is now focused on one thing only — resurfacing your old memories.

Taking photos on a smartphone is now a daily habit. But what about looking back at photos you took one year, three years or even eight years ago? It can pile up quite quickly. Zyl thinks there’s emotional value in those long-forgotten photos.

Before this update, Zyl helped you delete duplicates, create smart photo albums based on multiple criteria and collaborate on photo albums. In other words, it was a utility app.

But when the company started talking with some of their users, they realized that one feature stood out and had more value than the rest.

Applying those AI-powered models to your photo library is a great way to find interesting photos. But nobody was really looking at them.

When you open the app, you get a view of your camera roll with your last photos at the bottom. There’s also a big green button at the bottom. When you tap on it, Zyl creates a satisfying animation and unveils an important photo.

If you took multiple photos to capture this moment, the app stitches together those photos and create a GIF. You can then share this Zyl with a friend or family member.

But the true magic happens if you try to get another Zyl. You have to wait 24 hours to unlock another photo. The next day, the app sends you a notification when your photo is ready. You can always open the app again and look at your past Zyls in a new tab with your most important photos.

Unlike Timehop or Facebook’s “On This Day” feature, Zyl doesn’t look at your social media posts and focuses on your camera roll. Zyl isn’t limited to anniversaries either.

Just like before, Zyl respects your privacy and leaves your photos alone. They’re never sent to the company’s server — Zyl uses the same photo database as the native one on your iPhone or Android phone so it doesn’t eat up more storage.

Over time, the app could give you more options by leveraging facial recognition and the intrinsic social graph of your photo library. Maybe you want to see more photos of your brother as his wedding is coming up.

And that notification can be a powerful nudge. I keep opening the app and sharing old photos. Zyl is a good example of the combination of something that you care about combined with an element of surprise.

Powered by WPeMatico