founders fund

Auto Added by WPeMatico

Auto Added by WPeMatico

Hims, known by many for its phallic New York subway advertisements, has raised an additional $100 million in venture capital funding on a pre-money valuation of $1 billion. The round was first reported by Recode and confirmed to TechCrunch by sources with knowledge of the deal.

A growth-stage investor has led the round, which is ongoing, with participation from existing investors. Our source declined to name the lead investor but did say it was a “super big fund” that isn’t SoftBank and that hasn’t previously invested in Hims.

Hims officially launched just over one year ago and has raised $197 million already, as well as launched a women’s wellness brand, Hers, to go alongside its flagship men’s wellness brand. The business sells sexual wellness products, skin care and hair loss treatments directly to consumers. In addition to erectile dysfunction medication, it offers the birth control pill to customers with prescriptions and Addyi, the only FDA-approved medication for women with hypoactive sexual desire disorder.

According to Recode, Hims spent months negotiating with investors, “with some of them balking at the valuation.” Meanwhile, our source says Hims passed on several viable terms sheets and had plenty of IVP — which led its last round — money in the bank ahead of their latest infusion.

$1 billion, a 2x increase from its previous valuation, is a hefty price tag for such an early-stage digital health startup. Then again, most valuations for venture-backed businesses are foolish.

San Francisco-based Hims is also backed by Forerunner Ventures, Founders Fund, Redpoint Ventures, SV Angel, 8VC, Maverick Capital and more.

Powered by WPeMatico

Postmates, one of the earlier entrants to the billion-dollar food delivery wars, has raised an additional $100 million in equity funding at a $1.85 billion valuation, as first reported by Recode and confirmed to TechCrunch by Postmates. The round comes four months after the eight-year-old startup drove home a $300 million investment that finally knocked it into “unicorn” territory.

New investor BlackRock has joined the funding round alongside Tiger Global, which served as the lead investor of Postmates’ September financing. Led by co-founder and chief executive officer Bastian Lehmann, the company has garnered a total of $681 million in venture capital funding from investors, including Spark Capital, Founders Fund, Uncork Capital and Slow Ventures.

In line with several other tech unicorns, Postmates has begun prep for an initial public offering that could come this year, including tapping JPMorgan to advise the float. As Recode pointed out, the $100 million capital infusion was probably less of a necessary funding event but rather an opportunity for existing investors to liquidate stock ahead of an exit.

Postmates, which completes 3.5 million deliveries per month, reportedly expected to record $400 million in revenue in 2018 on food sales of $1.2 billion. The company has not confirmed that figure nor disclosed any other 2018 revenue numbers. The company currently operates in more than 500 cities, recently tacking on another 100 markets to reach an additional 50 million customers.

It will be interesting to see how Wall Street responds to a Postmates public listing. Though it was an early player in what has become an extremely crowded market, Postmates never emerged as the leader in food delivery. Now, with supergiants like Uber dominating via Uber Eats and SoftBank funneling loads of capital into Postmates competitor DoorDash, it shouldn’t count on an oversubscribed IPO.

Powered by WPeMatico

A slew of venture capitalists known for high-profile exits — Kirsten Green of Forerunner Ventures, Keith Rabois of Khosla Ventures, Alfred Lin of Sequoia Capital and Alex Taussig of Lightspeed Venture Partners — have invested in Faire (formerly known as Indigo Fair), a 2-year-old wholesale marketplace for artisanal products.

A quick glance at Faire suggests it’s a combination of Pinterest and Etsy, complete with trendy, pastel stationery, soap, baby products and more, all made by independent artisans and sold to retailers. Faire has today announced a $100 million fundraise across two financing rounds: a $40 million Series B led by Taussig at Lightspeed and a $60 million Series C led by Y Combinator’s Continuity fund. New investors Founders Fund, the venture firm founded by Peter Thiel, and DST Global also participated. The business has previously brought in a total of $16 million.

The latest financing values Faire at $535 million, according to a source familiar with the deal.

If you’re feeling a little bit of déjà vu, that’s because a similar startup also raised a sizeable round of venture capital funding, announced today. That’s Minted . The 10-year-old company, best known for its wide assortment of wedding invitations and stationery, raised $208 million led by Permira, with participation from T. Rowe Price. Though Minted is first and foremost a consumer-facing marketplace, it plans to double down on its wholesale business with its latest infusion of capital, setting it up to be among Faire’s biggest competitors.

Like Minted, Faire leverages artificial intelligence and predictive analytics to forecast which products will fly off its virtual shelves in order to to source and manage inventory as efficiently as possible. The approach appears to be working; Faire says it has 15,000 retailers actively purchasing from its platform, including Walgreens, Walmart, Sephora and Nordstrom — a 3,140 percent year-over-year increase. It’s completed 2,000 orders to date, garnering $100 million in run rate sales, and has expanded its community of artists 445 percent YoY, to 2,000.

The company, headquartered in San Francisco, with offices in Ontario and Waterloo, was founded by three former Square employees: chief executive officer Max Rhodes, who was product manager on a variety of strategic initiatives, including Square Capital and Square Cash; chief information officer Daniele Perito, who led risk and security for Square Cash; and chief technology officer Marcelo Cortes, a former engineering lead for Square Cash.

“Our mission at Faire is to empower entrepreneurs to chase their dreams,” Rhodes wrote in a blog post this morning. “We believe entrepreneurship is a calling. Starting a business provides a level of autonomy and fulfillment that’s become difficult to find for many elsewhere in the economy. With this in mind, we built Faire to help entrepreneurs on both sides of our marketplace succeed.”

Powered by WPeMatico

Berlin-based Zizoo — a startup which self describes as booking.com for boats — has nabbed a €6.5 million (~$7.4M) Series A to help more millennials find holiday yachts to mess about taking selfies in.

Zizoo says its Series A — which was led by Revo Capital, with participation from new investors including Coparion, Check24 Ventures and PUSH Ventures — was “significantly oversubscribed”.

Existing investors including MairDumont Ventures, aws Founders Fund, Axel Springer Digital Ventures and Russmedia International also participated in the round.

We first came across Zizoo some three years ago when they won our pitching competition in Budapest.

We’re happy to say they’ve come a long way since, with a team that’s now 60-people strong, and business relationships with ~1,500 charter companies — serving up more than 21,000 boats for rent, across 30 countries, via a search and book platform that caters to a full range of “sailing experiences”, from experienced sailor to novice and, on the pricing front, luxury to budget.

Registered users passed the 100,000 mark this year, according to founder and CEO Anna Banicevic. She also tells us that revenue growth has been 2.5x year-on-year for the past three years.

Commenting on the Series A in a statement, Revo Capital’s managing director Cenk Bayrakdar said: “The yacht charter market is one of the most underserved verticals in the travel industry despite its huge potential. We believe in Zizoo’s successful future as a leading SaaS-enabled marketplace.”

The new funds will be put towards growing the business — including by expanding into new markets; plus product development and recruitment across the board.

Zizoo founder and CEO Anna Banicevic at its Berlin offices

“We’re looking to strengthen our presence in the US, where we’ve seen the biggest YoY growth while also expand our inventory in hot locations such as Greece, Spain and the Caribbean,” says Banicevic on market expansion. “We will also be aggressively pushing markets such as France and Spain where consumers show a growing interest in boat holidays.”

Zizoo is intending to hire 40 more employees over the course of the next year — to meet what it dubs “the booming demand for sailing experiences, especially among millennials”.

So why do millennials love boating holidays so much? Zizoo says the 20-40 age range makes up the “majority” of its customer.

Banicevic reckons the answer is they’re after a slice of ‘affordable luxury’.

“After the recent boom of the cruising industry, millennials are well familiar with the concept of holidays at sea. However, sailing holidays (yachting) are much more fitting to the millennial’s strive for independence, adventure and experiences off the beaten path,” she suggests.

“Yachting is a growing trend no longer reserved for the rich and famous — and millennials want a piece of that. On our platform, users can book a boat holiday for as low as £25 per person per night (this is an example of a sailboat in Croatia).”

On the competition front, she says the main competition is the offline sphere (“where 90% of business is conducted by a few large and many small travel agents”).

But a few rival platforms have emerged “in the last few years” — and here she reckons Zizoo has managed to outgrow the startup competition “thanks to our unique vertically integrated business model, offering suppliers a booking management system and making it easy for the user to book a boat holiday”.

Powered by WPeMatico

Local newspapers may be shuttering and people may be consuming most news on social media, but don’t tell Alex Mather that a subscription news publication can’t grow like a unicorn startup. His 2-year-old sports publisher The Athletic has gained over 100,000 paid subscribers (60 percent under age 34) and has a 90 percent retention rate.

Having already raised $30 million in its short life, the company announced a new $40 million Series C yesterday, led by Founders Fund and Bedrock Capital. It reportedly values The Athletic around $200 million.

I interviewed Alex Mather (The Athletic’s CEO) and Eric Stomberg (partner at Bedrock Capital) to understand what’s behind the breakout success, and why they think this publishing startup can scale to become a multi-billion dollar company.

EP: Bedrock makes concentrated, contrarian bets. Explain how The Athletic fits that.

ES: I first met Alex and Adam in 2016 during Y Combinator. The popular view then, as it remains now, was that people just aren’t willing to pay for content online and that to win in media you have to put out a high volume of free articles on social.

The Athletic took the opposite approach. It’s a narrative violation. Everything is part of a paid subscription, with the belief that instead of writers needing to post 3-4 pieces per day, they should focus on deeper stories that add value to paid subscribers over time. That worldview resonated with us. If you can create content at scale that people are willing to pay for, that’s a powerful economic engine.

There’s so much sports coverage already out there, by professionals and amateurs alike, so why are people willing to pay for The Athletic?

AM: While there appears to be an abundance of content, most of it is aggregated, shallow content for a broad audience. We produce fewer stories and target a diehard fan. Our subscribers consistently tell us that no one else produces the same depth on a daily basis.

How did you determine the $60/year price point?

AM: We think of $60/year ($5/month) as less than the average NBA ticket. It’s a meaningful price but not prohibitive, especially when we do discounts in the first year. Like all subscription companies, whether we like it or not, we have to consider how our pricing stacks up against Netflix. For $10/month, you can subscribe to Netflix which is spending $8 billion per year in content.

Is The Athletic profitable?

AM: We expand by launching in local markets. We are in 47 thus far. The operational focus is on building a local team and becoming profitable in each local market. I can tell you that most markets are profitable in the first year — currently all of our markets over one year old are profitable and most of those over 6 months old are profitable.

(Photo by Thearon W. Henderson/Getty Images)

Explain your growth strategy in terms of coverage: Which sports did you start with and at which level (local versus national)?

AM: Direct-to-consumer businesses have to really work to earn their subscribers’ hard-earned money. We have to obsess over where we can be different. In the beginning, that was with hockey and baseball, because those have been de-prioritized by the bigger players. That shifted as we gained more subscribers: we needed to become comprehensive. We hired folks to cover the NBA, to cover the NFL, to cover soccer.

Do subscribers usually come just for one local sport or for the broader bundle?

AM: We’ve built a powerful bundle. A local newspaper has local politics, local restaurants, and then local sports. We have just the sports, but add a national perspective and a nationwide bundle. Most of our subscribers are “super bundlers,” meaning they subscribe to content from multiple cities plus at least one national product and usually a college product that’s not local. We provide all that for significantly less than competitors.

Eric — as a VC looking for multi-billion-dollar exits, how are you analyzing the potential scale of a subscription publication like this? Even most people who are bullish on subscriptions believe it’s a choice of going for a niche audience and staying small.

ES: There are two things we look for in a subscription business: retention and a positive flywheel.

Retention. In any subscription business, the key question is: can they maintain their subscribers over time? Most of them don’t. Spotify does, Netflix does, and The Athletic does as well. The Athletic is off the charts, which sets it up for scale. You want to see deep engagement over a very, very long period of time — years.

A positive flywheel. The more you build your subscriber base, the more you build your revenue base. That allows you to get better content, to hire unique writers, to build greater depth. In doing so, you attract people who weren’t ready to subscribe in the early days but now you have writers they follow and content they want. Technology is important here too: as you build a bigger platform with more content, serving the right content at the right time to each user is a key advantage. When this flywheel is working it’s actually quite hard to put a ceiling on the business.

Most publishers did a so-called “pivot to video” over the last couple of years. You’re anchored in writing. Why not more video at the start?

AM: We’re obsessed with the consumer and all our research in the beginning said that people still like to read books and articles. Advertising with text may not be as good as with video, which may be why so many other companies “pivoted to video,” but we think the written word is still the best way to convey certain types of stories. It’s straightforward, it doesn’t require headphones.

There’s an incredible amount of talent out there that can produce these stories and that has been cast aside by many entities. We saw it as an opportunity to give them great jobs and bring value to our subscribers. That has paid off for us.

What are your plans for video or other content formats in the future?

AM: We raised this Series C with audio and video in mind. We can tell even more stories when we add in audio and video possibilities. Our goal is to serve the subscriber: some love to read, some love to listen, others prefer to watch. We look up to things like The Ringer, Andre the Giant on HBO, VICE News, Gimlet, and The Daily by The New York Times all as incredible storytelling, and we ask ourselves “how can we do sports versions of those?”

Why focus on hiring experienced, full-time writers rather than a stable of contributors or curating from the vast pool of content by fans? Lots of amateurs pay close attention to sports.

AM: What’s really important to us is a growth mentality — that by Day 100 on our team a writer is thinking very differently. We’re providing lots of data, lots of feedback. We invest in great people who will figure this out with us over time. Also, scaling so quickly from 0 to 300 editorial staff was possible because we recruited experienced talent who know what to do already.

We do have about 400 contributors as well. These are folks who may be lawyers or accountants but are passionate about the teams they cover. We are a way for them to reach a premium audience. We can pay them really well and give them world-class editors formerly with Sports Illustrated and ESPN.

How are you acquiring your subscribers?

AM: When we expand into a new market, we gain new subscribers by hiring writers who have a following already and by word of mouth from existing subscribers. Then like any direct-to-consumer brand, we are acquiring subscribers through Google, Facebook and Twitter.

You financially incentivize your writers based on them acquiring new subscribers through their articles or by promoting The Athletic with their followers online. That is very uncommon in publishing. Explain that strategy.

AM: It ties back to our focus on building for the long term and investing in talent that will grow with us. We like to assign incentives that give us the best chance of building a sustainable business and we think about compensation in that way. We give our team equity in the company and for many, we tie a portion of their comp to the performance of their team, sport, city. It’s a great way to share in the responsibility and success of the business.

At the bottom of articles, you ask readers to rate each story as “Meh,” “Solid,” or “Awesome.” I wish every publisher did this. How do you use this data? How do a writer’s scores impact them?

AM: It’s about feedback loops. Our writers gauge feedback when they share on Twitter. This is another data point. It helps paint a more complete picture. NPS alone isn’t enough of course though. We look at whether articles drive new subscribers, drive deep engagement, drive comments, etc. We don’t use pageviews, but we certainly use metrics. Usually, this results in a writer producing very different work on Day 100 than they were on Day 0.

Explain the interaction between subscribers. It’s not unique to have a comments section: there are bad comments sections, good comments sections and comments sections that go unused. At a tactical level, how do you think about building community?

AM: My co-founder and I met at Strava, the social network for endurance athletes. I ran the product team and we were obsessed with community. We see an incredible connection between community engagement and subscriber retention. The question that drives us is how can we connect users in an authentic way, how can we connect users to our staff in an authentic way, how can we connect users to athletes in an authentic way. We’re doing a lot of experimentation here. We have a distinct opportunity because of our paywall: most of the comments on The Athletic are saying substantive things.

Powered by WPeMatico

Silicon Valley is in the midst of a health craze, and it is being driven by “Eastern” medicine.

It’s been a record year for US medical investing, but investors in Beijing and Shanghai are now increasingly leading the largest deals for US life science and biotech companies. In fact, Chinese venture firms have invested more this year into life science and biotech in the US than they have back home, providing financing for over 300 US-based companies, per Pitchbook. That’s the story at Viela Bio, a Maryland-based company exploring treatments for inflammation and autoimmune diseases, which raised a $250 million Series A led by three Chinese firms.

Chinese capital’s newfound appetite also flows into the mainland. Business is booming for Chinese medical startups, who are also seeing the strongest year of venture investment ever, with over one hundred companies receiving $4 billion in investment.

As Chinese investors continue to shift their strategies towards life science and biotech, China is emphatically positioning itself to be a leader in medical investing with a growing influence on the world’s future major health institutions.

We like to talk about things we can interact with or be entertained by. And so as nine-figure checks flow in and out of China with stunning regularity, we fixate on the internet giants, the gaming leaders or the latest media platform backed by Tencent or Alibaba.

However, if we follow the money, it’s clear that the top venture firms in China have actually been turning their focus towards the country’s deficient health system.

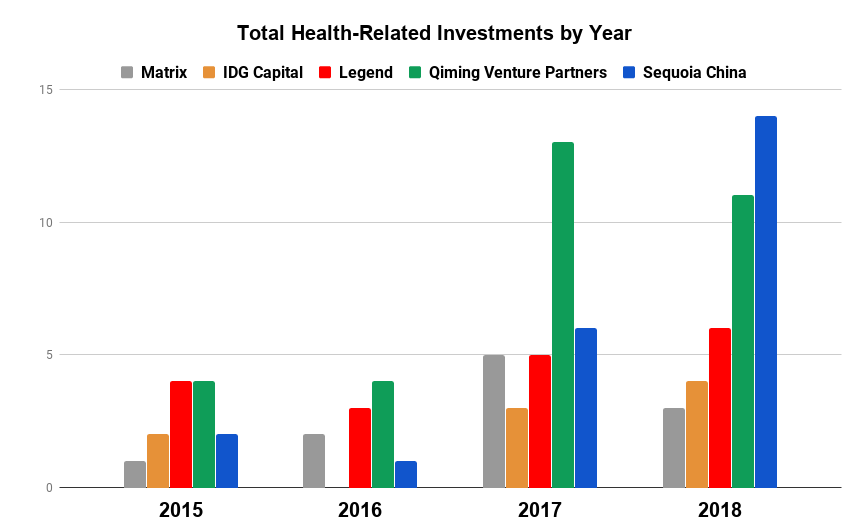

A clear leader in China’s strategy shift has been Sequoia Capital China, one of the country’s most heralded venture firms tied to multiple billion-dollar IPOs just this year.

Historically, Sequoia didn’t have much interest in the medical sector. Health was one of the firm’s smallest investment categories, and it participated in only three health-related deals from 2015-16, making up just 4% of its total investing activity.

Recently, however, life sciences have piqued Sequoia’s fascination, confirms a spokesperson with the firm. Sequoia dove into six health-related deals in 2017 and has already participated in 14 in 2018 so far. The firm now sits among the most active health investors in China and the medical sector has become its second biggest investment area, with life science and biotech companies accounting for nearly 30% of its investing activity in recent years.

Health-related investment data for 2015-18 compiled from Pitchbook, Crunchbase, and SEC Edgar

There’s no shortage of areas in need of transformation within Chinese medical care, and a wide range of strategies are being employed by China’s VCs. While some investors hope to address influenza, others are focused on innovative treatments for hypertension, diabetes and other chronic diseases.

For instance, according to the Chinese Journal of Cancer, in 2015, 36% of world’s lung cancer diagnoses came from China, yet the country’s cancer survival rate was 17% below the global average. Sequoia has set its sights on tackling China’s high rate of cancer and its low survival rate, with roughly 70% of its deals in the past two years focusing on cancer detection and treatment.

That is driven in part by investments like the firm’s $90 million Series A investment into Shanghai-based JW Therapeutics, a company developing innovative immunotherapy cancer treatments. The company is a quintessential example of how Chinese VCs are building the country’s next set of health startups using their international footprints and learnings from across the globe.

Founded as a joint-venture offshoot between US-based Juno Therapeutics and China’s WuXi AppTec, JW benefits from Juno’s experience as a top developer of cancer immunotherapy drugs, as well as WuXi’s expertise as one of the world’s leading contract research organizations, focusing on all aspects of the drug R&D and development cycle.

Specifically, JW is focused on the next-generation of cell-based immunotherapy cancer treatments using chimeric antigen receptor T-cell (CAR-T) technologies. (Yeah…I know…) For the WebMD warriors and the rest of us with a medical background that stopped at tenth-grade chemistry, CAR-T essentially looks to attack cancer cells by utilizing the body’s own immune system.

Past waves of biotech startups often focused on other immunologic treatments that used genetically-modified antibodies created in animals. The antibodies would effectively act as “police,” identifying and attaching to “bad guy” targets in order to turn off or quiet down malignant cells. CAR-T looks instead to modify the body’s native immune cells to attack and kill the bad guys directly.

Chinese VCs are investing in a wide range of innovative life science and biotech startups. (Photo by Eugeneonline via Getty Images)

The international and interdisciplinary pedigree of China’s new medical leaders not only applies to the organizations themselves but also to those running the show.

At the helm of JW sits James Li. In a past life, the co-founder and CEO held stints as an executive heading up operations in China for the world’s biggest biopharmaceutical companies including Amgen and Merck. Li was also once a partner at the Silicon Valley brand-name investor, Kleiner Perkins.

JW embodies the benefits that can come from importing insights and expertise, a practice that will come to define the companies leading the medical future as the country’s smartest capital increasingly finds its way overseas.

Despite heavy investment by China’s leading VCs, Silicon Valley is doubling down in the US health sector. (AFP PHOTO / POOL / JASON LEE)

Innovation in medicine transcends borders. Sickness and death are unfortunately universal, and groundbreaking discoveries in one country can save lives in the rest.

The boom in China’s life science industry has left valuations lofty and cross-border investment and import regulations in China have improved.

As such, Chinese venture firms are now increasingly searching for innovation abroad, looking to capitalize on expanding opportunities in the more mature US medical industry that can offer innovative technologies and advanced processes that can be brought back to the East.

In April, Qiming Venture Partners, another Chinese venture titan, closed a $120 million fund focused on early-stage US healthcare. Qiming has been ramping up its participation in the medical space, investing in 24 companies over the 2017-18 period.

New firms diving into the space hasn’t frightened the Bay Area’s notable investors, who have doubled down in the US medical space alongside their Chinese counterparts.

Partner directories for America’s most influential firms are increasingly populated with former doctors and medically-versed VCs who can find the best medical startups and have a growing influence on the flow of venture dollars in the US.

At the top of the list is Krishna Yeshwant, the GV (formerly Google Ventures) general partner leading the firm’s aggressive push into the medical industry.

Krishna Yeshwant (GV) at TechCrunch Disrupt NY 2017

A doctor by trade, Yeshwant’s interest runs the gamut of the medical spectrum, leading investments focusing on anything from real-time patient care insights to antibody and therapeutic technologies for cancer and neurodegenerative disorders.

Per data from Pitchbook and Crunchbase, Krishna has been GV’s most active partner over the past two years, participating in deals that total over a billion dollars in aggregate funding.

Backed by the efforts of Yeshwant and select others, the medical industry has become one of the most prominent investment areas for Google’s venture capital arm, driving roughly 30% of its investments in 2017 compared to just under 15% in 2015.

GV’s affinity for medical-investing has found renewed life, but life science is also part of the firm’s DNA. Like many brand-name Valley investors, GV founder Bill Maris has long held a passion for the health startups. After leaving GV in 2016, Maris launched his own fund, Section 32, focused specifically on biotech, healthcare and life sciences.

In the same vein, life science and health investing has been part of the lifeblood for some major US funds including Founders Fund, which has consistently dedicated over 25% of its deployed capital to the space since at least 2015.

The tides may be changing, however, as the recent expansion of oversight for the Committee on Foreign Investment in the United States (CFIUS) may severely impact the flow of Chinese capital into areas of the US health sector.

Under its extended purview, CFIUS will review – and possibly block – any investment or transaction involving a foreign entity related to the production, design or testing of technology that falls under a list of 27 critical industries, including biotech research and development.

The true implications of the expanded rules will depend on how aggressively and how often CFIUS exercises its power. But a lengthy review process and the threat of regulatory blocks may significantly increase the burden on Chinese investors, effectively shutting off the Chinese money spigot.

Regardless of CFIUS, while China’s active presence in the US health markets hasn’t deterred Valley mainstays, with a severely broken health system and an improved investment environment backed by government support, China’s commitment to medical innovation is only getting stronger.

Deficiencies in China’s health sector has historically led to troublesome outcomes. Now the government is jump-starting investment through supportive policy. (Photo by Alexander Tessmer / EyeEm via Getty Images)

They say successful startups identify real problems that need solving. Marred with inefficiencies, poor results, and compounding consumer frustration, China’s health industry has many.

Outside of a wealthy few, citizens are forced to make often lengthy treks to overcrowded and understaffed hospitals in urban centers. Reception areas exist only in concept, as any open space is quickly filled by hordes of the concerned, sick, and fearful settling in for wait times that can last multiple days.

If and when patients are finally seen, they are frequently met by overworked or inexperienced medical staff, rushing to get people in and out in hopes of servicing the endless line behind them.

Historically, when patients were diagnosed, treatment options were limited and ineffective, as import laws and affordability issues made many globally approved drugs unavailable.

As one would assume, poor detection and treatment have led to problematic outcomes. Heart disease, stroke, diabetes and chronic lung disease accounts for 80% of deaths in China, according to a recent report from the World Bank.

Recurring issues of misconduct, deception and dishonesty have amplified the population’s mounting frustration.

After past cases of widespread sickness caused by improperly handled vaccinations, China’s vaccine crisis reached a breaking point earlier this year. It was revealed that 250,000 children had been given defective and fallacious rabies vaccinations, a fact that inspectors had discovered months prior and swept under the rug.

Fracturing public trust around medical treatment has serious, potentially destabilizing effects. And with deficiencies permeating nearly all aspects of China’s health and medical infrastructure, there is a gaping set of opportunities for disruptive change.

In response to these issues, China’s government placed more emphasis on the search for medical innovation by rolling out policies that improve the chances of success for health startups, while reducing costs and risk for investors.

Billions of public investment flooded into the life science sector, and easier approval processes for patents, research grants, and generic drugs, suddenly made the prospect of building a life science or biotech company in China less daunting.

For Chinese venture capitalists, on top of financial incentives and a higher-growth local medical sector, loosening of drug import laws opened up opportunities to improve China’s medical system through innovation abroad.

Liquidity has also improved due to swelling global interest in healthcare. Plus, the Hong Kong Stock Exchange recently announced changes to allow the listing of pre-revenue biotech companies.

The changes implemented across China’s major institutions have effectively provided Chinese health investors with a much broader opportunity set, faster growth companies, faster liquidity, and increased certainty, all at lower cost.

However, while the structural and regulatory changes in China’s healthcare system has led to more medical startups with more growth, it hasn’t necessarily driven quality.

US and Western investors haven’t taken the same cross-border approach as their peers in Beijing. From talking with those in the industry, the laxity of the Chinese system, and others, have made many US investors weary of investing in life science companies overseas.

And with the Valley similarly stepping up its focus on startups that sprout from the strong American university system, bubbling valuations have started to raise concern.

But with China dedicating more and more billions across the globe, the country is determined to patch the massive holes in its medical system and establish itself as the next leader in international health innovation.

Powered by WPeMatico

Cargo, the startup that helps ridesharing drivers earn money by bringing the convenience store into their vehicles, has raised $22 million in a Series A round led by Founders Fund.

Additional investment came from Coatue Management, Aquiline Technology Growth and a number of high-profile entertainment, gaming and technology executives that include Zynga founder Mark Pincus, Twitch’s former CSO Colin Carrier, media investor Vivi Nevo, former NBA commissioner David Stern, Def Jam Records CEO Paul Rosenberg, Steve Aoki, Maria Shriver and Patrick and Christina Schwarzenegger.

To date, Cargo has raised $30 million in venture funding. As part of this latest round, Founders Fund partner Cyan Banister is joining the board.

Cargo provides qualified ridesharing drivers with free boxes filled with the kinds of goods you might find in a convenience store, including snacks and phone chargers. Riders can use Cargo’s mobile web menu on their smartphones (without downloading an app) to buy what they need. Cargo has previously partnered with Kellogg’s, Starbucks and Mars Wrigley Confectionery — companies looking for ways to market their goods to consumers.

“In just a few years, ridesharing has evolved from a niche service to an indispensable element of our global transportation system,” Banister said in a statement. “Founders Fund is excited to support Cargo in driving the next evolution: a better on-trip experience for riders and new revenue generating opportunities for drivers.”

The round follows Cargo’s partnership with Uber and an international licensing deal with Grab. The company, which was founded in 2017, has activated more than 12,000 drivers across 10 cities.

Cargo says it will use the capital to scale its business in the U.S. and internationally. It’s also working on new digital services — a development Banister eludes to — that will improve users on-trip experience. The strategic investments from gaming and entertainment executives is designed to help Cargo develop those digital services for riders.

“Our default behavior in an Uber is to shop, play games and listen to music on our phone. Riders have ordered more than two million products and today transact with us every five seconds,” Cargo founder and CEO Jeff Cripe said in a statement. “We brought riders instant commerce, now we’ll help them discover and enjoy games, music, and entertainment on one in-car platform.”

Existing Cargo investors participating in the round include CRCM Ventures, Rosecliff Ventures, Kellogg’s eighteen94 capital, RiverPark Ventures, and former Uber executives including Chief Business Officer Emil Michael, New York City General Manager Josh Mohrer and former West Coast General Manager William Barnes.

Powered by WPeMatico

For people who make investment decisions based on revenues and projected earnings, biotech IPOs are kind of a non-starter. Not only are new market entrants universally unprofitable, most have zero revenue. Going public is mostly a means to raise money for clinical trials, with red ink expected for years to come.

That pattern may be one reason the venture capital press, Crunchbase News included, tends to devote a disproportionately small portion of coverage to biotech IPOs. It’s more exciting to watch a big-name internet company pop in first-day trading or poke fun at an underperforming dud.

But with our fixation on all things tech, we’re missing out on the big picture. There are actually a lot more biotech and healthcare startup IPOs than tech offerings. In the second quarter of this year, for instance, at least 16 U.S. venture-backed biotech and healthcare companies went public, compared to just 11 tech startups. In three of the past four years, bio offerings outnumbered tech IPOs, according to Crunchbase data.

In the following analysis, we attempt to get up to speed on the pace of biotech offerings, assess where we are in the cycle and spotlight some of the rising stars.

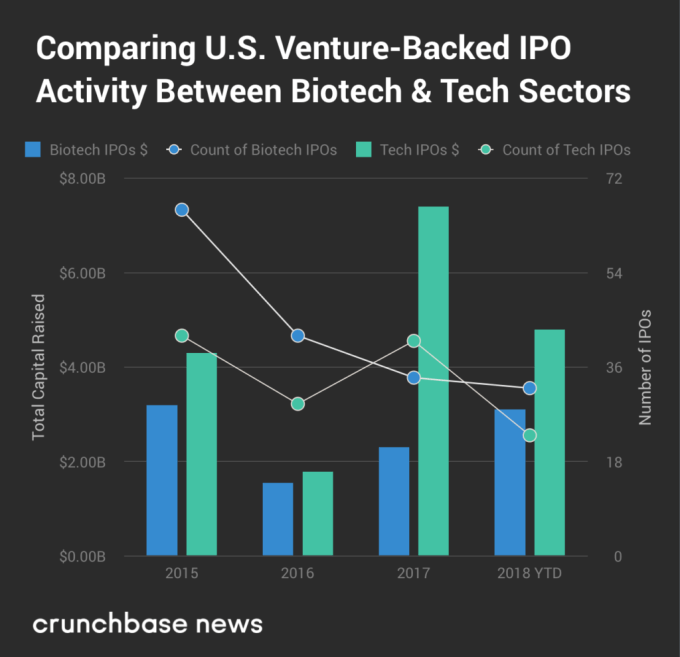

As mentioned above, U.S. bio IPOs outnumber tech offerings in most years. However, the bio cohort raises less total capital, partly because the largest technology IPOs tend to be much bigger than the largest bio IPOs. In the chart below, we compare the two sectors over the past four years.

Globally, the numbers are much higher. Using Crunchbase data, we’ve put together a chart looking at global VC-backed biotech and healthcare IPOs over the past four years. While we’re just over halfway through 2018, biotech and health IPOs have already raised more money than in any of the prior three full calendar years.

It’s pretty clear we’re in an upcycle for all things startup-related. VCs are flush with cash, late-stage rounds are ballooning in size and IPO and M&A action is picking up, too.

So what does that mean for bio IPOs? Is the uptick in the pace and size of offerings mostly a result of bullish market conditions? Or is the current slate of pre-IPO candidates more compelling than in the past?

We turned to Bob Nelsen, co-founder of ARCH Venture Partners, one of the top-performing biotech investors, for his take, which is that it’s a “fundamentals driven, cycle amplified” IPO boomlet.

More companies are launching well-received IPOs because the pace of startup innovation is faster than in the past. Nelson calls it “the result of the previous 30 years of investment and innovation in biotech that has finally led to essentially data-driven innovation.” That’s leading to more curative treatments, disease-modifying therapies and preventative technologies.

Yet we’re also in a bullish segment of the market cycle for biotech. That’s prompting companies that might have stayed private under other conditions to give going public a shot. It’s also providing bigger outcomes for emerging companies that were already on the IPO track.

The latest example of a big outcome IPO is Rubius Therapeutics, which develops drugs based on genetically engineered red blood cells. This week, the five-year-old company raised $241 million at an initial valuation of over $2 billion, making it the largest bio offering of 2018. The Cambridge, Mass. company, which previously raised nearly a quarter-billion-dollars in venture funding, is still in the pre-clinical trial phase.

This year has delivered several other good-sized offerings as well, including drug developers Eidos Therapeutics and Homology Medicines, recently valued around $800 million each, along with Tricida, valued around $1.2 billion. (See the full list of 2018 global bio and health offerings here.)

As for aftermarket performance, that’s been up and down, but includes some big ups. Last year, biotech led the pack for best-performing IPOs on U.S. exchanges. The sector accounted for four of the six top spots, according to Renaissance Capital, led by drug developers AnaptysBio, Argenx and UroGen, along with Calyxt, an agbio startup.

While things are already up, bio VCs, generally an optimistic bunch, see several reasons why bio IPOs could go higher.

Nelson points to what he sees as the lagging pace of in-house innovation at big pharma and biotech players. Increasingly, they need to acquire startups and recently public companies to stay competitive and build out new product pipelines.

There is also tons of fresh capital earmarked for healthcare startups. In the U.S. in 2017, healthcare-focused venture capitalists raised $9.1 billion. That figure was up 26 percent from 2016, per Silicon Valley Bank.

More dollars also are flowing from venture firms that invest in a mix of tech and life sciences through a single fund. That list includes well-established VCs with dry powder to invest, including Polaris Partners, Founders Fund, Kleiner Perkins and Sequoia Capital.

Still, Nelson observes, deep into an IPO bull market, the average quality of offerings does tend to decline. That said, he’s been through similar inflection points in previous cycles and “for the same point in the cycle, the quality is markedly higher.”

Powered by WPeMatico

Going to the dentist can be anxiety-inducing. Unfortunately, it was no different for me last week when I went to discuss Uniform Teeth’s recent $4 million seed funding round from Lerer Hippeau, Refactor Capital, Founder’s Fund and Slow Ventures.

Uniform Teeth is a clear teeth aligner startup that competes with the likes of Invisalign and Smile Direct Club. The startup takes a One Medical-like approach in that it provides real, licensed orthodontists to see you and treat your bite.

“For us, we’re really focused on transforming the orthodontic experience,” Uniform Teeth CEO Meghan Jewitt told me at the startup’s flagship dental office in San Francisco. “There are a lot of health care companies out there that are taking areas that aren’t very customer-centric.”

Jewitt, who spent a couple of years at One Medical as director of operations, pointed to One Medical, Oscar Insurance and 23andMe as examples of companies taking a very customer-centric approach.

“We are really interested in doing the same for the orthodontics space,” she said.

Ahead of the first visit, patients use the Uniform app to take photos of their teeth and their bite. During the initial visit, patients receive a panoramic scan and 3D imaging to confirm what type of work needs to be done.

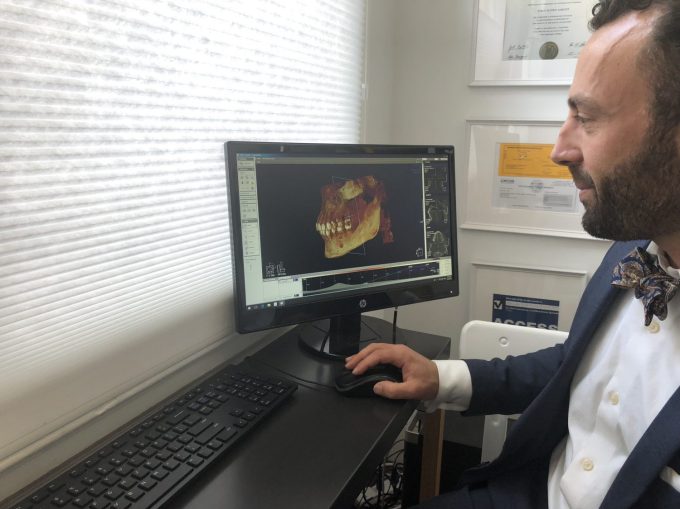

Last week during my visit, Jewitt and Uniform Teeth co-founder Dr. Kjeld Aamodt showed me the technology Uniform uses for its patient evaluations.

In the GIF above, you can see I received a 3D panoramic X-ray. The process took about 10 seconds and it’s about the same exposure to X-rays as a flight from San Francisco to Los Angeles, Dr. Aamodt said.

“With that information, we’re able to see the health of your roots, your teeth, the bone, your jaw joints, check for anything that could get worse during treatment,” Dr. Aamodt said.

Below, you can see the 3D scan.

Next is looking in-between the teeth. From here, the idea is to get a much more holistic view, Dr. Aamodt said. This is where things got interesting.

If you look at the bottom left of the photo, under my back bottom tooth, you can see a dark circle below the tooth. Dr. Aamodt gently pointed that out to me.

“That tells me there’s bacteria living inside of your jaw,” he explained. “A lot of people have this. It’s pretty common so don’t beat yourself up for it.”

This is when he told me I’d likely need to get a root canal to get rid of it. Mild panic ensued.

Dr. Aamodt went on to explain that, if I were a patient of his looking to get my teeth straightened, he would recommend that I first get the root canal before any teeth movement. That’s because, he explained, moving teeth at that point could potentially result in further infection.

“The concern about that is when we move a tooth with that, the infection will get worse and you could risk losing that tooth,” he told me.

Although I was freaking out internally, I continued to move ahead with the process. Next up was the 3D scan, which results in something fancy called a 3D Cone Beam Computed Tomography. This, Dr. Aamodt said, is what really sets Uniform Teeth apart in precision tooth movement.

This process takes the place of dental impressions, which are made by biting into a tray with gooey material. I didn’t feel like getting my bottom teeth scanned, but below is what the top looks like.

At this point Uniform Teeth would share its recommendations with the patient. My personal recommendation was to go see my dentist and, if I’m interested in straightening my teeth, come back once my roots are in a healthy enough state.

From there, I’d receive a custom treatment plan that combines the X-ray plus 3D scan to predict how my teeth will move. After receiving the clear aligners in a couple of weeks, I’d check in with Dr. Aamodt every week via the mobile app. If something were to come up, I could always set up an in-person appointment. Most people average about two to three visits in total, Jewitt said. All of that would add up to about $3,500.

The reason Uniform Teeth requires in-office visits is because 75 percent or more of the cases require additional procedures. For example, some people require small, tooth-colored attachments to be placed onto the clear aligners. Those attachments can help move teeth in a more advanced way, Dr. Aamodt said.

“If you don’t have these, then you can tip some teeth but you can’t do all of the things to help improve the bite, to create a really lasting, beautiful, healthy smile,” he explained.

Uniform Teeth currently treats patients in San Francisco, but intends to open additional offices nationwide next year. As the company expands, the plan is to bring on board more full-time orthodontists.

“Right now, we’re an employment-based model and we’d really like to continue that because it allows us to control the experience and deliver a really high-quality service,” Jewitt said.

A lot of companies say they care about the customer when, in reality, they just care about making money. But I genuinely believe Uniform Teeth does care. After I left with my tail between my legs that day, I called my dentist to set up an appointment. The following day, my dentist confirmed what Dr. Aamodt found and proceeded to set me up to get a root canal. A few days later, Dr. Aamodt checked in with me via the mobile app to ask me how I was doing and to make sure I was getting it treated. I was pleased to let him know, as Olivia Pope likes to say, “It’s handled.”

Powered by WPeMatico

HQ is redefining mobile, creating through its twice-daily trivia games a sense of urgency that pierces the monotony of our social feeds. Now it’s raised a big round of funding to turn its scrappy operation into the Jeopardy from tomorrow. But just like its 12-round games, we’ve got 12 questions (and some answers) for HQ. Read More

HQ is redefining mobile, creating through its twice-daily trivia games a sense of urgency that pierces the monotony of our social feeds. Now it’s raised a big round of funding to turn its scrappy operation into the Jeopardy from tomorrow. But just like its 12-round games, we’ve got 12 questions (and some answers) for HQ. Read More

Powered by WPeMatico