fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

Fintech startup Revolut has been teasing Asian market expansions for more than a year, but it sounds like it might finally happen. The company has secured licenses to operate in Singapore and Japan. It now expects to launch its service in Q1 2019.

In Singapore, the company was granted a Remittance License by the Monetary Authority and a Stored Value Facility approval — these two things combined let Revolut users hold money as well as send and spend money. In Japan, the company has been authorized to operate by Japan’s Finance Service Agency.

According to Revolut, those approvals are enough to launch the service in those countries. But not all features will make their way to Singapore and Japan. Regulation varies from one country to another, so the company might not be able to provide the same limits and feature set everywhere.

At launch, Revolut will focus on the electronic wallet and the payment card. You won’t be able to buy cryptocurrencies, create business accounts and more. Limits should be more or less the same in local currency equivalent.

In Japan, Revolut says it has already signed deals with Rakuten, Sompo Japan Insurance (SJNK) and Toppan. It sounds like there will be new insurance products, special card designs and more.

Revolut plans to open its APAC office in Singapore. Let’s see if Revolut ends up convincing expats to sign up or if they can have a real impact outside of Europe.

And if you’re a potential user in the U.S. or Canada, you’ll have to wait a bit more. Revolut says there will be more news in the coming weeks.

Powered by WPeMatico

Earlier this year, Rebecca Liebman impressed a panel of high-profile investors, including Ashton Kutcher and Salesforce chief executive Marc Benioff, at a SXSW pitch competition. She won and Benioff wrote her a check for $200,000 on the spot.

Today, she’s announcing that her educational fintech startup LearnLux has closed a $2 million seed round from Kutcher’s investment firm Sound Ventures, Benioff, Underscore VC and former Wealthfront CEO Adam Nash. LearnLux operates under a SaaS model, partnering with businesses to offer access to its digital financial wellness product, which helps employees make important financial decisions.

The Boston-based startup was founded by Liebman, 25, and her brother, Michael Liebman, 22, in 2015.

“He was coding from his dorm room when we were first building the product,” Rebecca said. “We’ve had a really interesting experience from a young age. I was working at a lab at MIT with brilliant Ph.D. students and no one could figure out how to open a retirement account. Michael was working at a bank with people who studied finance who still couldn’t figure out how to open a retirement account.” LearnLux provides interactive learning tools and educational content created in-house to guide workers through their 401k, health savings accounts or stock options, for example. Rebecca says they’ve signed on 10 customers since launching in September.

LearnLux provides interactive learning tools and educational content created in-house to guide workers through their 401k, health savings accounts or stock options, for example. Rebecca says they’ve signed on 10 customers since launching in September.

“There are all these financial decisions you have to make and we allow you to have an interactive experience online where you can play out what those decisions will look like,” she said.

“Finance has been made to confuse people. We had to figure out how to break it down and explain it in a way that makes sense … Whatever kind of learner you are, you will understand more about your financial decisions with [LearnLux.]”

Powered by WPeMatico

French startup Qonto has raised a $23 million funding round for its fintech product. The company is trying to make business banking cheaper, faster and more efficient.

Existing investors Valar Ventures and Alven are once again leading the round. The European Investment Bank Group is also participating.

If you are running a small company or work as a freelancer, Qonto wants to replace your professional bank account. When you sign up, you get a French IBAN, one or multiple debit cards and the ability to send and receive money.

And then, it works pretty much like any challenger bank. You can create virtual cards, order more cards for your team, get real time notifications and freeze cards. This is a breath of fresh air compared to traditional business banks and their time-consuming processes.

You can then sync your transactions with accounting and invoicing services, and grant access to your accountant. Premium plans let you select multiple administrators and create a validation workflow to approve expensive transfers for instance.

With today’s funding round, the company plans to double the size of the team and create its own payment infrastructure. Qonto currently relies heavily on Treezor for the back end. The startup also plans to expand to Germany, Italy and Spain in 2019.

Qonto now has 90 employees and 25,000 clients. The company has managed $2 billion in total transaction volume so far. The fact that the same VC funds keep investing more money into Qonto is a great vote of confidence.

Powered by WPeMatico

Paidy, a fintech startup that enables Japanese consumers to shop online without using a credit card, announced today that it has raised a $55 million Series C. The round was led by Japanese trade conglomerate Itochu Corporation, with participation from Goldman Sachs.

The Tokyo-based startup says this brings its total funding so far to $80 million, including a $15 million Series B announced two years ago. One notable fact about Paidy’s funding is that it’s raised a sizable amount for Japanese startup, especially one with non-Japanese founders (its CEO and co-founder is Canadian and Goldman Sachs alum Russell Cummer, left in the photo above with CTO and co-founder Lee Smith).

Paidy was launched because even though Japan’s credit card penetration rate is high, their usage rate is relatively low, even for online purchases. Instead, shoppers pay cash on delivery or at convenience stores, which function as combination logistics/payment centers in many Japanese cities.

This is convenient for buyers because they don’t have to enter a credit card online or worry about fraud, but a hassle for businesses that often need to float cash for merchandise that hasn’t been paid for yet or deal with incomplete deliveries.

Paidy makes it possible for people to buy online without creating an account or using their credit cards. Instead, if a merchant uses Paidy, its customers are able to check out by entering their mobile phone numbers and email addresses. Then Paidy authenticates them with a four-digit code sent through SMS or voice. Every month, customers settle their bills, which include all transactions they made using Paidy, at a convenience store or through bank transfers or auto-debits (installment and subscription plans are also available).

The value proposition for businesses is that Paidy can increase their customer base and guarantee they get paid by using machine learning algorithms to underwrite transactions. The company claims that there are now 1.4 million active Paidy accounts, with the ambitious goal of increasing that number to 11 million by 2020 by expanding to bigger merchants and offline transactions.

In a press statement, Cummer said “We are extremely honored that Paidy’s business concept was highly valued by one of Japan’s most prestigious business conglomerates, ITOCHU. Through this tie-up, we expect to launch new merchants in order to deliver Paidy’s frictionless and intuitive financial solution to a much broader audience.”

Powered by WPeMatico

Drip Capital is raising a $20 million funding round from Accel, Wing VC and Sequoia India. The company is helping small exporters in emerging markets access working capital in order to finance big orders.

The startup also participated in Y Combinator back in 2015. Many small companies in emerging markets have to turn down orders because they can’t finance big orders. Even if you found a client in the U.S. or Europe, chances are companies will end up paying for your order a month or two after signing a contract.

If you’re an importer or an exporter, capital is arguably your most valuable resource. You know where to source your products and how to ship many goods. But you still need to buy goods yourself.

And in many emerging markets, you have to pay right away. It creates a sort of capital gap.

At the same time, local banks are often too slow and reject too many credit applications. Drip Capital thinks there’s an opportunity for a tech platform that finances exporters in no time.

The startup is first focusing on India because it meets many of the criteria I listed. This could be particularly useful for small and medium businesses. Large companies don’t necessarily face the same issues as they can access capital more easily.

So far, Drip Capital has funded more than $100 million of trade. After signing up to the platform, you can submit invoices and open a credit line to finance your next orders. Family offices and institutional investors can also invest some money in Drip Capital’s fund and get returns on investment.

This isn’t the only platform that helps you get paid faster. But larger companies tend to do it all and optimize the supply chain for the biggest companies in the world. Drip Capital is focusing on a specific vertical.

With today’s funding round, the company plans to get more customers and expand to other countries.

Powered by WPeMatico

Fintech startup Revolut likes to announce new things all the time. Even though nothing is going live today, it’s interesting to see where the startup is heading. The company is working on a trading platform for traditional shares without any commission.

You’ll find stock from public companies from the U.K. and the U.S., as well as various ETFs and options. In other words, Revolut is going to become the Robinhood of Europe.

While American customers have been using Robinhood for years, the rest of the world has been lagging behind when it comes to stock trading.

You still have to open an account on a painfully slow website and pay a few euros for every transaction. Some companies even ask you to send a letter to create an account. And if you want to buy stock through your existing bank account, it usually costs even more.

Revolut promises that you won’t pay any commission when you buy or sell shares. The company plans to make money on margin trading, securities lending and interest on cash. Unfortunately, Revolut didn’t say when the feature would launch.

Premium subscribers will be able to test the feature first. Eventually, you’ll also get additional perks if you’re a premium subscriber. Trading will be available to all Revolut users in Europe and future markets. The company plans to launch in the U.S., Canada, Singapore, Hong Kong, Australia and New Zealand in the coming months.

Revolut’s premium subscription is becoming a sort of Amazon Prime for financial products. You pay £6.99/€7.99 per month and you get unlimited foreign exchange transactions, travel insurance, access to new features and more.

It’s clear that Revolut plans on making predictable revenue on this premium subscription. And maybe the trading platform will make more people subscribe to Revolut Premium.

Additionally, Revolut now officially has 2 million users. It’s funny to see that Revolut is announcing this new milestone just days after N26 announced a million users. Interestingly, Revolut has 900,000 users in the U.K., where N26 has yet to launch.

Powered by WPeMatico

French startup Lendix has raised a new funding round of $37 million (€32 million). With this new influx of cash, the startup has one goal in mind. It wants to become the leading lending marketplace of Continental Europe.

Idinvest and Allianz are leading the round, with CIR SpA (De Benedetti’s holding firm) also participating. Existing investors Partech, CNP Assurances, Decaux Frères Investissements and Matmut are also participating once again.

As of today, people living in France, Spain and Italy can sign up to lend money to companies established in those three countries. But the startup is already working hard to expand to the Netherlands and Germany before the end of the year. Next year, Lendix plans to operate in 7 countries.

And it seems like it’s becoming easier to launch new markets. There are now quite a few users and institutional investors on the platform. Lendix doesn’t need to attract Dutch users to start lending to Dutch companies. French, Italian and Spanish users are already willing to put some money in Dutch companies. It’s a true European user base because everybody uses the same currency.

With today’s funding round, it’s going to be easier to launch in Germany. “When you want to open in Germany — and that is our current plan — it’s harder to recruit if you don’t have a German brand name behind you,” co-founder and CEO Olivier Goy told me.

That’s why Allianz is going to be more than just a financial backer. For instance, the insurance company is going to promote Lendix to its corporate clients so that they think about Lendix if they need to borrow some money.

It’s another proof that Lendix doesn’t want to be a French company that operates in other countries. The company also has opened an office in Madrid and another one in Milan with local teams.

Lendix is still a drop in the bucket compared to traditional bank loans. But the company wants to differentiate its product offering from regular banks as much as possible.

Right now, when a company requests a loan, the company’s algorithms are going to work on a basic credit scoring. After that, somebody calls the company to ask a few questions. The Lendix team can focus on more specific information.

“We also have developed a tool called Iris,” CTO Benjamin Netter told me. “It is going to become the biggest intelligence database for European companies.”

France is leading the way when it comes to open data. You can now access the registry of commerce, the identification number database and important incorporation events. But it’s a mess if you want to access this data. There are different file formats, and the same database uses different fields depending on the region of France.

Lendix has been parsing all this data to turn it into an actionable database. This way, Lendix can get a clear overview of companies that apply for a loan.

The company doesn’t plan to stop there. You could use Iris to detect some fraud patterns. For instance, a person could keep incorporating new companies and shutting them down quickly.

Eventually, you could reach out to companies before they need to apply for a loan. Netter mentioned a restaurant called Street Bangkok. They’ve opened three restaurants over the past six months. It’s clear that they might need some money at some point to invest in new restaurants. Lendix Iris could spot those patterns.

Lendix is still nowhere near as big as Funding Circle. But the company thinks there’s enough room for multiple players in this space. Both can grow at the same time by competing with traditional banks.

And it starts by being faster than a traditional bank. Companies get a rate within 48 hours. “Our goal is that you should be able to get a rate within half a day,” Goy said. Banks will have a hard time giving you an answer so quickly.

Disclosure: I share a personal connection with an executive at CNP Assurances.

Powered by WPeMatico

Entrepreneurs have it rough in Africa, India, Pakistan — places where VC cash doesn’t fall from the sky and necessary infrastructure like reliable banking and broadband can be hard to come by. But companies grow and thrive nevertheless in these rugged environments, and DFS Lab is an incubator focused on connecting them with the resources they need to go global.

The company was founded, and funded, on the back of a $4.8 million grant from the Gates Foundation, which of course is deeply concerned with tech-based solutions for well-being all over the world. Its name, Digital Financial Services Lab, indicates its area of focus: fintech. And anyone can tell you that sub-Saharan Africa is one of the most interesting places in the world for that.

This week DFS Lab is announcing a handful of new investments — modest ones on the scale companies are used to in Silicon Valley, but the money is only a small part of the equation. Investment comes at the end of a longer process, the most valuable of which may be the week-long sprint DFS Lab does on the ground, helping solidify ideas into products, or niche products into products at scale.

The relative lack of VCs and angel investors puts early-stage companies at risk and can discourage the most motivated entrepreneur, so the program is aimed at getting them over the hump and connected to a network of peers.

The latest round puts a total of $200,000 into four startups, each touching on a different aspect of a region or vertical’s financial needs. All, however, are largely driven by the massive growth of mobile money in Africa over the last decade and the more recent, ongoing transition to modern smartphones and the app/data landscape familiar to the U.S. and Europe.

The fourth company is choosing to remain in stealth mode for now, but you see the general theme here.

For one reason or another there are major gaps in everyday services that many of us take for granted — the ability to prove one’s identity, for example, is critical but commonly absent. I talked with Paul Damalie, founder of a DFS-funded company called Inclusive that helps address that particular shortcoming.

Basic ID verification can be difficult when you remove many of the things we take for granted. So when, for example, someone wanted to get a loan, a savings account, or some other basic financial service, “Originally you’d have to literally walk into the bank to do it,” Damalie said. Needless to say that isn’t always convenient, and banks as well as users want better options.

“We’ve been collecting existing databases and building a layer of rich access around it,” he continued. “Now we can use facial recognition to check those details. Once you have the ID, you need to check it with the government records” — which Inclusive also does. A range of other data creates a confidence score in the person’s identity, helping avoid identity fraud.

Another opportunity arises not from these gaps but from the unique ways in which the African ecosystem has evolved. USSD, which I mentioned before, is probably unknown to many of our readers — it certainly was to me. But it’s become a standard tool used regularly by millions for important tasks in Africa; if you want to work in that market, you have to deal with USSD one way or another.

Another opportunity arises not from these gaps but from the unique ways in which the African ecosystem has evolved. USSD, which I mentioned before, is probably unknown to many of our readers — it certainly was to me. But it’s become a standard tool used regularly by millions for important tasks in Africa; if you want to work in that market, you have to deal with USSD one way or another.

The problem is that, as you might guess from Nala trying to deprecate it, USSD is a technology dating back to the ’90s, a text-based interface that’s rudimentary but, much like SMS, universally accepted and intelligible. The importance of cross-platform compatibility in mobile markets as fragmented as these can’t be overstated.

So bridging the gap between USSD and a “traditional” (as we might call it) payment app is a unique opportunity, and one a company called Hover (also in the DFS Lab portfolio) is addressing. Its tech acts as a sort of translation layer between USSD and smartphone app interfaces, allowing for modern app design but also deep back-compatibility. It’s an opportunity specific to this time and this area of the world, but nevertheless one that may end up touching millions.

And from the narrowness of its vision that DFS Lab derives its effectiveness.

“They’re one of the most specialized accelerators in the world,” said Damalie. “It goes beyond just funding — it involves having the right kind of network: access to partners, data, sources across the continent. They had context-relevant fellows, people who had very specific challenges.”

“The grant was useful and let us build a proof of concept, and of course the Gates Foundation gives us credibility. But they were taking bets on us as individuals.”

Although DFS Lab has heretofore been funded by the Gates infusion, that well will run dry soon. Jake Kendall, DFS Lab’s executive director, indicated that the plan is to move towards a more traditional investor fund. They already focus on profitability and the potential for growth to the continental stage or beyond; this isn’t a charity but tactical investment in such a way that social good is a necessary byproduct.

“The best way to have a global impact is to be self-sustaining,” he said.

Powered by WPeMatico

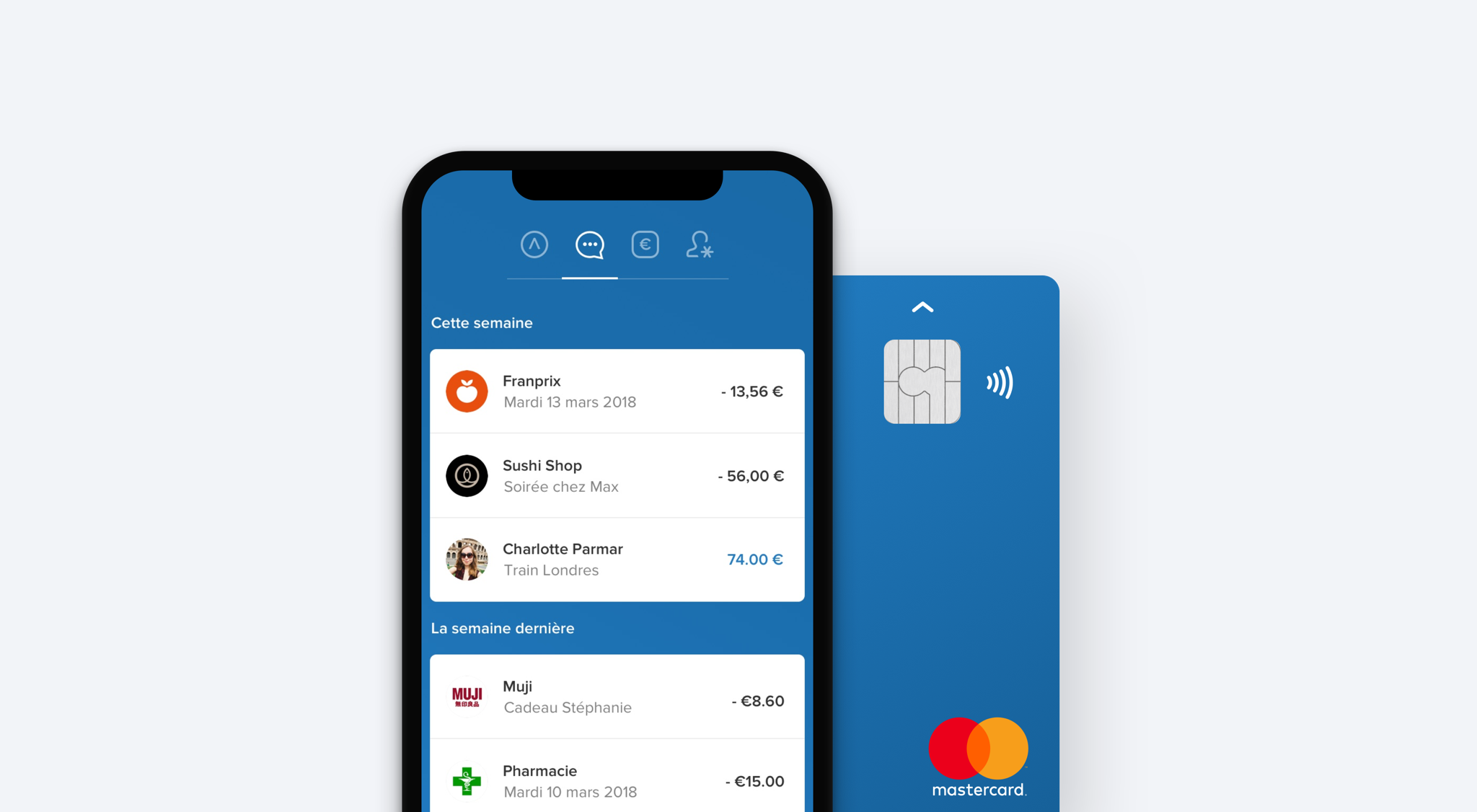

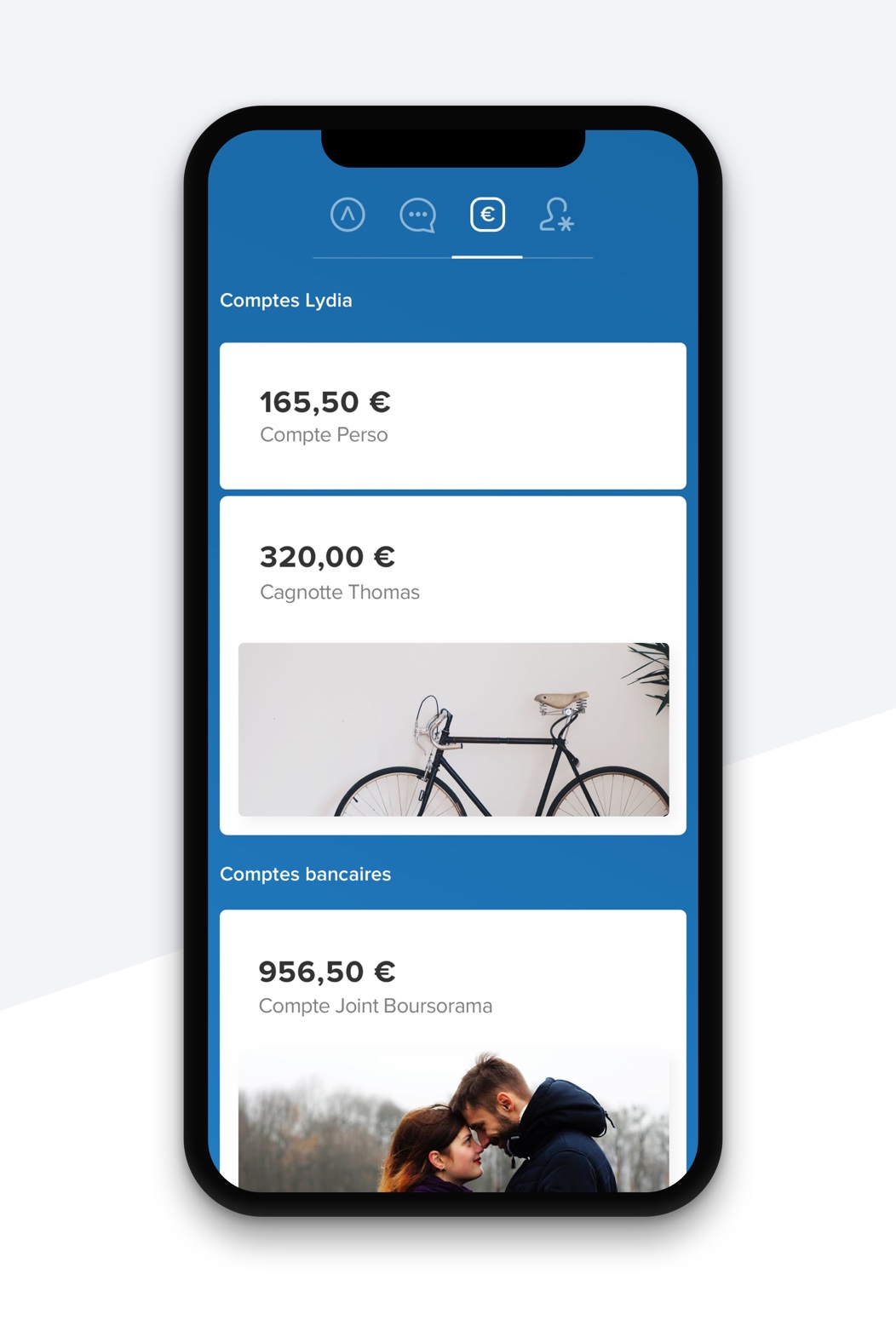

French startup Lydia announces two new things today. First, the company is launching a financial hub with multiple new products. Second, Lydia is announcing a new premium subscription to access those new features.

“Today, we’re lucky enough to have you here to announce you the biggest thing we’ve done since Lydia’s launch,” co-founder and CEO Cyril Chiche said in a press conference. “We’ve been working on this for a while — and it’s not a challenger bank.”

Lydia is no longer just a peer-to-peer payment app with a few other features. The company says it is now building a meta-banking app, sitting above other financial products. So you’ll find and control a handful of financial products in the Lydia app.

“We didn’t want to stop at aggregating services,” Chiche said. “But we tried to think about people-centric, exclusive features that you can’t find anywhere else.”

![]()

Let’s go through the new features. There’s a new IBAN menu where you can add new recipients using a good old IBAN account. Lydia also asks you if you want to add specific IBANs to your own bank accounts. This way, instead of opening BNP Paribas’ app to copy and paste an IBAN into Société Générale’s app, you can add recipients from Lydia.

And of course, you can also send money to your recipient. You can use money from your Lydia e-wallet or from one of your own bank account. You don’t have to open your banking app anymore. Lydia leverages Budget Insight for this feature.

Lydia also supports recurring transactions. “It’s been the most requested features for multiple years,” co-founder and CTO Antoine Porte said. For instance, you can pay for your share of the internet bill every month using Lydia. The app sends you a notification every month to confirm the transaction.

Finally, there’s a brand new tab to get an overview of multiple accounts. You can see your bank account and Lydia sub-accounts. For instance, if you’re going on vacation with a few friends, you can create a Lydia sub-account and manage all your expenses from Lydia without any fee.

Interestingly, you can create a URL and send it to friends who are not using Lydia. Other users can then pay using your debit card. It feels like a streamlined version of Lydia’s existing money pot feature.

This is a big step for the company as Lydia is launching Lydia Premium for those new features. You can connect to your bank accounts, create recurring payments and sub-accounts for a monthly post. It’ll cost €2.99 per month ($3.69).

Existing features are still free. You can send and receive money in a just a few seconds with a Lydia transaction. You can pay in Franprix stores or on Cdiscount with your Lydia account.

You can try some of the new features with a free account. For instance, you can link one bank account, you can create one recurring payment, you can generate one virtual card, you can create money pots with some fees, etc.

Just like before, you can generate a virtual card for free so that you can pay on the internet or use Apple Pay with it. But if you’re a Lydia Premium subscriber, you’ll be able to generate multiple virtual cards to manage your online subscriptions. For instance, you can stop a subscription by deleting a virtual card or change the payment source for this card.

If you want to get a good old plastic card, you can pay an extra euro. For €3.99 per month ($4.92), you get everything I just described and a MasterCard. When you pay, the card uses your Lydia e-wallet and sends you a notification. You can open the app and choose one of your bank accounts to debit your bank account instantly.

Personal IBAN numbers and direct debits are no longer available for now — you could generate one for free. They’ll be back as part of Lydia Premium with new features as well as shared accounts. You’ll be able to pick a bank account for each transaction. For instance, you can say that you use LCL for your electricity bill and Fortuneo for your taxes. Lydia partners with Treezor for IBANs, virtual and physical cards.

Lydia currently has a little bit over a million registered users. And the startup is currently attracting around 2,000 new users every day. Over 80 percent of this user base has less than 30 years.

Lydia is currently available in France, Ireland, the U.K., Spain and Portugal. The startup also recently raised $16.1 million (€13 million) from CNP Assurances and others.

It’s interesting to see that Lydia isn’t competing head-to-head with challenger banks, such as N26 or Revolut (soon). The company thinks you can provide more value by partnering with multiple companies and building the interface that makes everything work together.

Powered by WPeMatico

Financial services giant Citi reckons fintech startups are missing out on a major opportunity to disrupt institutional banking. Indeed, it’s inviting entrepreneurs to do so.

Financial services giant Citi reckons fintech startups are missing out on a major opportunity to disrupt institutional banking. Indeed, it’s inviting entrepreneurs to do so.