financial planning

Auto Added by WPeMatico

Auto Added by WPeMatico

Pry Financials wants to make startup finances approachable for its entire team, not just the people in charge of its accounting spreadsheets. The Y Combinator alum announced today it has raised $4.2 million from Global Founders Capital, Pioneer Fund, NOMO VC, Liquid2 and Hyphen Capital.

Launched in March, Pry now has more than 200 customers and claims it has grown 35% month-over-month since YC’s Demo Day. It was founded by Alex Sailer, Tiffany Wong, Hayden Jensen and Andy Su.

Before starting Pry, Su was co-founder of InDinero, another YC alum that started as a “Mint for small businesses” before pivoting to a full-service accounting company. InDinero launched while he was still a student at UC Berkeley, and Su eventually became responsible for its financial planning.

Pry Financials’ team. Image Credits: Pry Financials

He told TechCrunch that most startups can’t afford accounting software like Workday Adaptive Planning. Instead, they sometimes work with outsourced CFO services, but mostly rely on spreadsheets for everything: three-way forecasts, predicting runway, hiring and contractor budgets and investor updates.

“I was the chief technical officer and over the years, I also took on the finance function, so it was kind of a dual CTO/CFO role. This was 2010 through 2020 and as technology grew, the engineering and product teams got all sorts of new tools every six months or so, whereas the finance team was just stuck in Excel,” he said.

Started as a side project while Su was still at InDinero, Pry starts at just $50 a month and replaces those spreadsheets with easy-to-understand dashboards for accounting, financial planning and scenario modeling. The dashboards connect to QuickBooks, Xero or bank accounts, so numbers are continuously updated.

Pry’s clients typically start using it after they raise seed funding, because “for most first-time founders, that’s the most amount of money you have ever received, so you need to spend more time managing it and reviewing it every month. And you’re spending a lot of time on payroll each month,” Su said. Second-time founders, meanwhile, sign up for Pry because they are sick of Excel spreadsheets.

“Reviewing a spreadsheet is mind-numbingly hard,” said Su. “If you see a number that’s off, you get this weird formula if you didn’t do it yourself. Then you basically have to write a long email to the financial analyst who wrote it and hope that they get back to you before closing time.” For founders who need to update lenders or investors every month, this means a lot of work.

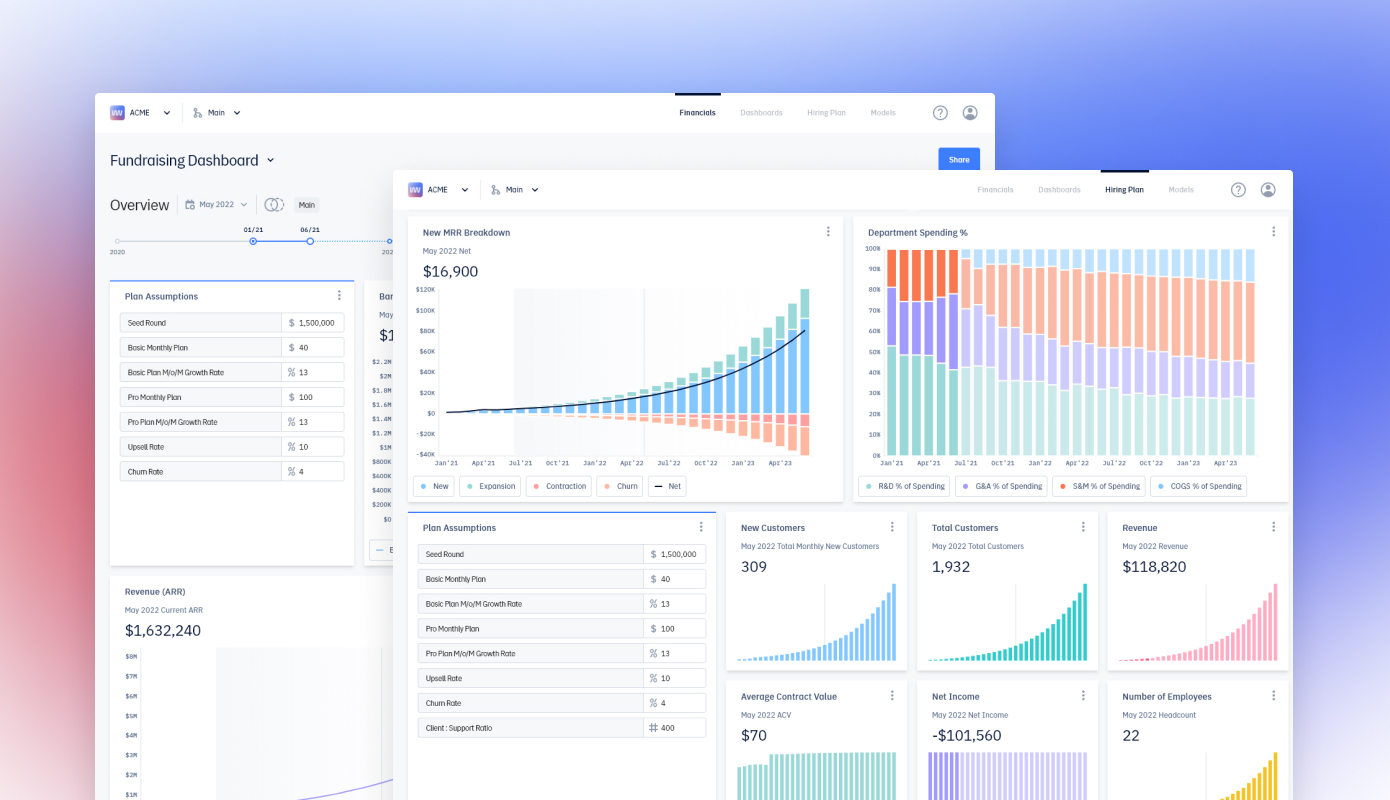

Pry makes the process more efficient by turning three-way reports — combinations of balance sheets, profit and loss statements and cashflow — into Financial Report dashboards, and then adding features like hiring plans, financial modeling and scenario planning.

The scenario planning feature serves as a sandbox, giving startup teams and their investors a way to predict how different situations will impact finances: for example, how much runway they have if they raise a certain amount of funding or adjust product pricing.

Fundraising dashboards created with Pry Financials. Image credits: Pry Financials

“We’re improving upon and trying to make decisions about the company in a collaborative way. The analogy we have is Git branching, where you have your main plan, and want to try something like a new revenue model or acquiring a business, but don’t want to mess with your current strategy,” said Su. “What you can do is create a completely new branch with, say, a new pricing strategy. You can make all the changes you want and then switch back to your old branch without worrying about overriding or conflicting with it.”

Those speculative branches are also continuously updated with the company’s most recent bank account and payroll information, so founders don’t need to recreate them from scratch if they want to revisit a potential scenario later.

Pry plans to build more complex predictive tools and also integrate industry standards, like statistic and benchmarks, into templates to help founders understand what targets they should set.

Because Pry is easier to manage than a set of Excel spreadsheets, Su said it’s helped startups spot important things. For example, one founder was able to find a way to save $15,000 by catching a tax issue. Pry also helps everyone at a startup understand its finances’ even if they haven’t worked with accounting spreadsheets before. The platform will add roles and permissions soon, so founders can give or restrict access to different people, like leaders of specific departments.

Su said Pry does not compete with the accounting services many startups rely on until they can hire a head of finance, but makes it easier for startups to collaborate with them since they can share their dashboards.

“Usually early on, you can outsource to a CFO firm. That’s the norm in the business and it works pretty well for most companies. You get a part-time CFO to work really hard for a month and get your fundraising structure done,” said Su, adding “we fit into that ecosystem well.”

Powered by WPeMatico

Family offices have existed since the 1800s, but they’ve never been so manifold as in recent years. According to a 2019 Global Family Office Report by UBS and Campden Wealth, 68% of the 360 family offices surveyed were founded in 2000 or later.

Their rise owes to numerous factors, including the tech startups that mint new centi-millionaires and billionaires each year, along with the increasingly complex choices that people with so much moolah encounter. Think household administration, legal matters, trust and estate management, personal investments, charitable ventures.

Still, family offices tend to cater to people with investable assets of $1 billion or more, according to KPMG. Even multi-family offices, where resources are shared with other families, are more typically targeting people with at least $20 million to invest. That high bar means there are still a lot of people with a lot of resources who need hand-holding.

Enter Harness Wealth, a three-year-old, New York-based outfit that was founded by David Snider and Katie Prentke English to cater to individuals with increasingly complex financial pictures, including following liquidity events. The two understand as well as anyone how one’s vested interests can abruptly change — and how hard these can be to manage when working full-time.

Snider got his start out of school as an associate with Bain & Company and later as an associate with Bain Capital before becoming the first business hire at the real estate company Compass and getting promoted to COO and CFO after the company’s $25 million Series A raise in 2013. That little company grew, of course, and now, less than four months after its late-March IPO, Compass boasts a market cap of nearly $27 billion.

Indeed, over the years, Snider, who rejoined Bain as an executive-in-residence after 4.5 years with Compass, began to see a big opportunity in bringing together the often siloed businesses of tax planning and estate planning and investment planning, including it because “it resonated with me personally. Despite all these great things on my resume, every six months I found something I could or should have been doing differently with my equity.”

Prentke English is also like a lot of the clients to which Harness Wealth caters today. After spending more than six years at American Express, she spent two years as the CMO of London-based online investment manager Nutmeg. She left the role to start Harness after being introduced to Snider through a mutual friend; in the meantime, Nutmeg was just acquired by JPMorgan Chase.

While there is no shortage of wealth managers to whom such individuals can turn, Harness says it does far more than pair people with the right independent registered investment advisors — which is a key part of its business and part of the secret sauce of its tech platform, it says. It also helps its customers, depending on their needs, connect with a team of pros across an array of verticals — not unlike the access an individual might have if they were to have a family office.

As for how Harness makes money, it shares revenue with the advisers on the platform. Snider says the percentage varies, though it’s an “ongoing revenue share to ensure alignment with our clients.” In other words, he adds, “We only do well if they find long-term success with the advisers on our platform,” versus if Harness merely collected an upfront lead generation fee by pointing new customers to so-so financial planners or tax attorneys.

Ultimately, the company thinks it can replace a lot of the do-it-yourself services available in the market, like Personal Capital and Mint. That confidence is rooted in part in Snider’s experience with Compass, which, in its earlier days, though it could navigate around real estate agents but “found that while people wanted better data insights and a better user interface, they also wanted that coupled with someone who’d had many clients who looked like them,” says Snider.

He adds that Prentke English joined forces with him after discovering that Nutmeg, too, was “running into the limitations of a non-human-powered solution.”

Investors think the thesis makes sense, certainly. Harness just closed on $15 million in Series A funding led by Jackson Square Ventures, a round that brings the company’s total funding to $19 million. (Both new and existing investors include Bain Capital; Torch Capital; Activant; GingerBread Capital; FJ Labs; i2BF Ventures; First Minute Capital; Liquid2 Ventures; Alleycorp, Marc Benioff; Compass founder Ori Allon; and Paul Edgerley, who is the former co-head of Bain Capital Private Equity.

As for what Harness Wealth does with that fresh capital, part of it, interestingly, will be used to develop its own captive business line called Harness Tax. As Snider explains it, more of its clients are finding that tax planning is among their biggest concerns, given all that is happening on the IPO front, with SPACs, with remote work, and also with cryptocurrencies, into which more people are pouring money but around which the tax code has been playing catch-up.

It makes sense, given that tax planning can be time-sensitive and often dictate the overall financial planning strategy. At the same time, it’s fair to wonder whether some of Harness Wealth’s adviser partners will be turned off from working with the outfit if it thinks its partner is evolving into a rival.

Snider insists that Harness Wealth — which currently employs 22 people and is not-yet profitable — has no such designs. “Our goal is only to help people where we can add value, and we saw an opportunity to lean in on tax side.”

Harness has a “a very large population of people who may not understand their tax liabilities” because of the crypto boom in particular, he explains, adding, “We want to make sure we’re front and center” and ready to help as needed.

Powered by WPeMatico

As enterprise startups continue to target interesting gaps in the market, we’re seeing increasingly sophisticated tools getting built for small and medium businesses — traditionally a tricky segment to sell to, too small for large enterprise tools, and too advanced in their needs for consumer products. In the latest development of that trend, an Israeli startup called DataRails has raised $25 million to continue building out a platform that lets SMBs use Excel to run financial planning and analytics like their larger counterparts.

The funding closes out the company’s Series A at $43.5 million, after the company initially raised $18.5 million in April (some at the time reported this as its Series A, but it seems the round had yet to be completed). The full round includes Zeev Ventures, Vertex Ventures Israel and Innovation Endeavors, with Vintage Investment Partners added in this most recent tranche. DataRails is not disclosing its valuation, except to note that it has doubled in the last four months, with hundreds of customers and on target to cross 1,000 this year, with a focus on the North American market. It has raised $55 million in total.

The challenge that DataRails has identified is that on one hand, SMBs have started to adopt a lot more apps, including software delivered as a service, to help them manage their businesses — a trend that has been accelerated in the last year with the pandemic and the knock-on effect that has had for remote working and bringing more virtual elements to replace face-to-face interactions. Those apps can include Salesforce, NetSuite, Sage, SAP, QuickBooks, Zuora, Xero, ADP and more.

But on the other hand, those in the business who manage finances and financial reporting are lacking the tools to look at the data from these different apps in a holistic way. While Excel is a default application for many of them, they are simply reading lots of individual spreadsheets rather than integrated data analytics based on the numbers.

DataRails has built a platform that can read the reported information, which typically already lives in Excel spreadsheets, and automatically translate it into a bigger picture view of the company.

For SMEs, Excel is such a central piece of software, yet such a pain point for its lack of extensibility and function, that this predicament was actually the germination of starting DataRails in the first place,

Didi Gurfinkel, the CEO who co-founded the company with Eyal Cohen (the CPO) said that DataRails initially set out to create a more general-purpose product that could help analyze and visualize anything from Excel.

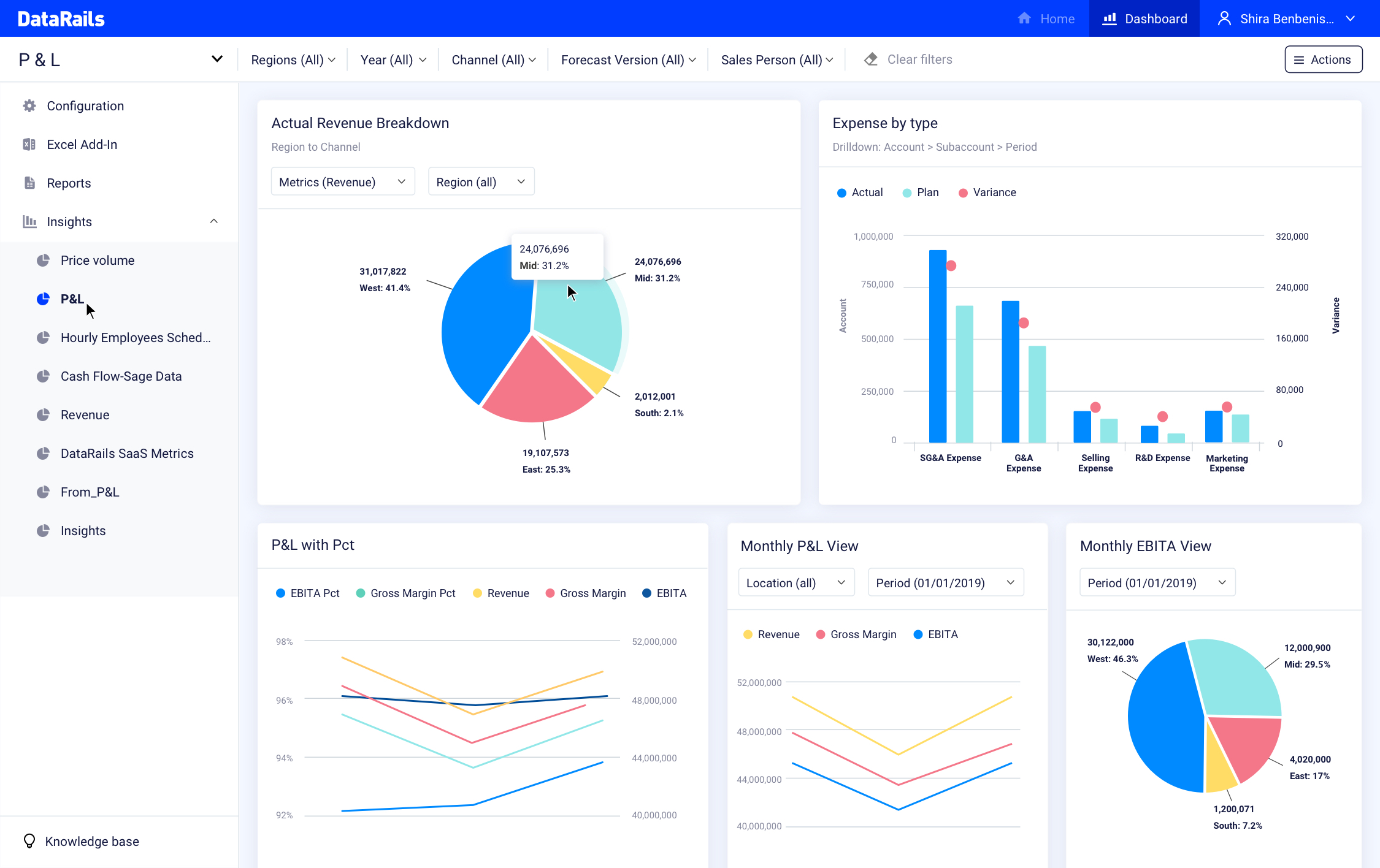

Image: DataRails

“We started the company with a vision to save the world from Excel spreadsheets,” he said, by taking them and helping to connect the data contained within them to a structured database. “The core of our technology knows how to take unstructured data and map that to a central database.” Before 2020, DataRails (which was founded in 2015) applied this to a variety of areas with a focus on banks, insurance companies, compliance and data integrity.

Over time, it could see a very specific application emerging, specifically for SMEs: providing a platform for FP&A (financial planning and analytics), which didn’t really have a solution to address it at the time. “So we enabled that to beat the market.”

“They’re already investing so much time and money in their software, but they still don’t have analytics and insight,” said Gurfinkel.

That turned out to be fortunate timing, since “digital transformation” and getting more out of one’s data was really starting to get traction in the world of business, specifically in the world of SMEs, and CFOs and other people who oversaw finances were already looking for something like this.

The typical DataRails customer might be as small as a business of 50 people, or as big as 1,000 employees, a size of business that is too small for enterprise solutions, “which can cost tens of thousands of dollars to implement and use,” added Cohen, among other challenges. But as with so many of the apps that are being built today to address those using Excel, the idea with DataRails is low-code or even more specifically no-code, which means “no IT in the loop,” he said.

“That’s why we are so successful,” he said. “We are crossing the barrier and making our solution easy to use.”

The company doesn’t have a huge number of competitors today, either, although companies like Cube (which also recently raised some money) are among them. And others like Stripe, while currently not focusing on FP&A, have most definitely been expanding the tools that it is providing to businesses as part of their bigger play to manage payments and subsequently other processes related to financial activity, so perhaps it, or others like it, might at some point become competitors in this space as well.

In the meantime, Gurfinkel said that other areas that DataRails is likely to expand to cover alongside FP&A include HR, inventory and “planning for anything,” any process that you have running in Excel. Another interesting turn would be how and if DataRails decides to look beyond Excel at other spreadsheets, or bypass spreadsheets altogether.

The scope of the opportunity — in the U.S. alone there are more than 30 million small businesses — is what’s attracting the investment here.

“We’re thrilled to reinvest in DataRails and continue working with the team to help them navigate their recent explosive and rapid growth,” said Yanai Oron, general partner at Vertex Ventures, in a statement. “With innovative yet accessible technology and a tremendous untapped market opportunity, DataRails is primed to scale and become the leading FP&A solution for SMEs everywhere.”

“Businesses are constantly about to start, in the midst of, or have just finished a round of financial reporting — it’s a never-ending cycle,” added Oren Zeev, founding partner at Zeev Ventures. “But with DataRails, FP&A can be simple, streamlined, and effective, and that’s a vision we’ll back again and again.”

Powered by WPeMatico

Few people are more knowledgable on the topic of how founders should manage their finances than Alexa von Tobel. She is a certified financial planner, started her own company in the midst of the recession (which happened to be a wildly successful personal finance startup that sold for hundreds of millions of dollars) and is now a VC who invests and advises founders.

At Early Stage 2021, she gave a presentation on how founders should think about managing their own wealth. Startup founders can often put all their money into their venture and end up paying more attention to the finances of their company than their own bank account.

Von Tobel outlined the various steps you can take to stay out of debt, build credit and accumulate wealth through investments to ensure you have financial peace of mind as you take on the most stressful venture of your life: Starting a company.

The first step in getting organized and being proactive is often taking inventory. Von Tobel believes that knowing your numbers and getting organized digitally is the first step to having financial peace of mind.

Know all your numbers. Know your net worth. What are your assets? What’s your debt? What does your total financial picture look like? Get everything online. You should have all the mobile apps downloaded so that, in minutes, you can actually see your full financial life. And keep it simple. Fewer accounts are better. I always tell people, if you have seven credit cards, plus three savings accounts, that’s a lot. You’re never going to be as good at managing your finances. Simplify your accounts. (Time stamp — 2:50)

Powered by WPeMatico

Digital transformation is the name of the game these days, and companies that are enabling businesses to take a leap into the future, by helping them tackle their most complex operations, are reaping the rewards. In the latest development, OneStream, a startup that provides a toolkit of services to enterprises to help them run financial operations (for example, reporting, planning, tax and more), has raised $200 million in primary equity. The funding values OneStream at $6 billion.

D1 Capital Partners led the financing, with participation from Tiger Global and Investment Group of Santa Barbara (IGSB), the company said. Tiger Global and D1 appear to share at least one common backer, Tiger Management, which may be one reason why you see them together in many big deals.

The company plans to use the funding to continue building out the tools that it provides to customers, and to keep up with demand for its services as more customers replace legacy applications and very basic, spreadsheet-based operations.

“We remain sharply focused on delivering innovative planning, reporting and analysis solutions designed to help our customers succeed for today’s fast-paced and increasingly complex business environment,” said Tom Shea, CEO of OneStream Software, in a statement. “The valuation we received is great recognition of the value our employees and stakeholders have helped to create, as well as the exciting opportunities ahead for OneStream.”

To put these large numbers into some context, OneStream was valued at $1 billion only two years ago, when KKR took a majority stake in the company worth more than $500 million. The company’s CFO, Bill Koefoed, has confirmed to us that KKR will continue to be “substantially OneStream’s largest shareholder and remains a very supportive investor”. The company meanwhile appears to be holding off any plans for going public for the time being — despite some possible hints that it was considering that move.

“OneStream is currently focused on delivering 100% customer access, continuing to grow the business and creating value for stakeholders,” Koefoed said. “IPO is a potential exit and OneStream is preparing to be a public company. However, there is no specific timeline.”

The growth in valuation, meanwhile, reflects the surge of business that OneStream has seen in the last two years, and in particular in the last 12 months, as companies have been compelled to update their systems to work more efficiently and flexibly amid the COVID-19 pandemic and the impact it has had around in-person interactions. OneStream said annual recurring revenue grew 85% in 2020, with customers growing by 40% to 650 enterprises.

The company’s focus is specifically in the area commonly called corporate performance management (CPM), which includes a number of the financial corporate operations that a company runs behind the scenes to keep its business ticking.

Some of these would have fallen to a range of software providers, and much of the work would have been carried out by way of on-premise solutions, with companies like SAP, Oracle Hyperion and IBM dominating the space with all-in solutions, and others like Anaplan and Blackline providing point solutions addressing specific aspects of those functions.

But as with other areas of enterprise services, the advances of technology and software have created opportunities to take a lot of that functionality into the cloud and to run the processes across a single system to improve analytics and efficiency, and that has provided an opportunity to the likes of OneStream.

The impact of the pandemic should not be underestimated in this trend, and it was one that OneStream was able to nail because its software can be used across disparate teams and can draw a direct line to helping companies manage their finances better. And unlike a lot of tech companies that raise venture funding, one interesting detail with OneStream is that it has extended its customer base well outside the realm of technology companies and other early adopters. Those using its software include the likes of Fruit of the Loom, McCain (the frozen fries king) and AAA, but also Takeaway.com, the Carlyle Group and many others.

“The pandemic accelerated OneStream’s business given that it was a wake-up call for many companies that had not digitally transformed their key finance processes,” said Koefoed. “As a result, we have seen increased demand from companies who were using spreadsheets or legacy CPM applications to manage their financial close, consolidation, reporting, planning and forecasting processes… They are better able to keep their finance teams connected and collaborating while physically dispersed. In addition, we have seen many organizations increasing the frequency of their forecasting and scenario modeling from quarterly or monthly to weekly and daily in some cases, especially during the early days of the pandemic when modeling revenue and cash flow was critical.”

For investors, the interest more specifically was how OneStream managed to add more customers away from competitors in the last year.

“OneStream’s platform delivers exceptional customer value,” said Andrew Wynne, a principal at D1 Capital Partners, in a statement. “Management’s intense focus on customer success has enabled OneStream to capture significant market share from incumbents, while posting strong growth in both revenue and customer acquisition. We believe OneStream has both the vision and product required to be a dominant force in its industry.”

Going forward, it sounds like the company will continue to build on what it has already established. That will include more business into Asia Pacific alongside its current operations in North America and Europe, Koefoed said. It will also use its foothold in finance and providing services to the finance department to make inroads into other areas that link closely to money management: money spending and revenue generation, with tools to plan and operate in areas like HR, IT, sales, marketing, supply chain management “and other areas to ensure alignment and optimal resource allocations,” he added.

Powered by WPeMatico

Companies increasingly recognize that one of the greatest stresses for their employees is financial wellness. Even at innovative tech startups, people typically bump up against the limits of how much they know about wealth management pretty fast.

But providing financial education to a workforce, which has become increasingly common, is largely useless as most employees will tell you. The information can be hard to navigate, and it’s often not personalized in a way that addresses an employee’s circumstance and goals, which change over time depending on whether they are a recent graduate, getting married or even eyeing retirement.

It’s why so many employed people look to outside apps that promise to help them to not only understand their financial picture but actually manage it. It’s also a missed opportunity, according to a growing number of founders who are working to convince employers to move beyond education and instead offering automated financial planning (with a dash of human involvement) as an employee perk.

Their understandable argument: While offering benefits around fertility, family planning, and mental health are wonderful, companies are missing out on the chance to address the very top priority for their employees, which is how to avoid financial trouble.

Origin, a year-old San Francisco-based company led by Matt Watson — whose last company was acquired in December — is among the newest entrants to make the case.

Freshly backed by $12 million in funding led by Felicis Ventures, with participation from General Catalyst, Founders Fund and early Stripe employee Lachy Groom, among others, Origin wants to become the place where employees can track financial milestones, get professional advice from licensed financial planners, and take action, whether it be paying down student debt, building emergency savings or finding the right home and automotive insurance.

Currently staffed by 32 employees, six are financial planners, and they can handle the unique circumstances of “mid thousands of people,” says Watson, who notes that after an employee initially sets up a plan, much can be automated until a life event changes the picture.

“If you use just the tech, you’re only getting limited information,” he says, adding that access to Origin’s planners is “unlimited.”

The company already has 15 customers with between 250 and 5,000 employees, including the social network NextDoor; the cloud communications and collaboration software platform Fuze; and Therabody, whose Theragun therapy tool is used by pro athletes and trainers to pulverize their aching muscles.

All are paying $6 per employee per month because it doesn’t matter how much employees are making, says Watson. “The thing about financial stress is that it impacts everyone pretty evenly. The greater your income, the more stuff you buy.”

Considering that employees spend an estimated two to four hours each week dealing with their personal finances, an offering like Origin’s seems like a no-brainer for employers looking to both improve employee productivity and employee retention.

Indeed, the only thing holding back such offerings earlier in time were the kind of open banking APIs that exist today.

Now, the biggest challenge for Origin is to capture employers’ attention ahead of the competition. For example, another startup that’s also developing financial planning services as an employee perk is Northstar, founded by Red Swan Ventures investor Will Peng. More established players like Betterment that have long catered to individual investors are also focusing more on building up ties to employers that can use their offerings as an employee resource.

Either way, the trend is a positive one for employees, who are right now living through an economic roller coaster and could more generally use a lot more help with both staying afloat and saving for the future.

“Everyone struggles with finances,” says Watson, who worked in high-yield credit trading at Citi in New York before moving to San Francisco to start his last company. “I’m supposed to understand this stuff, and it’s complicated for me.”

Powered by WPeMatico

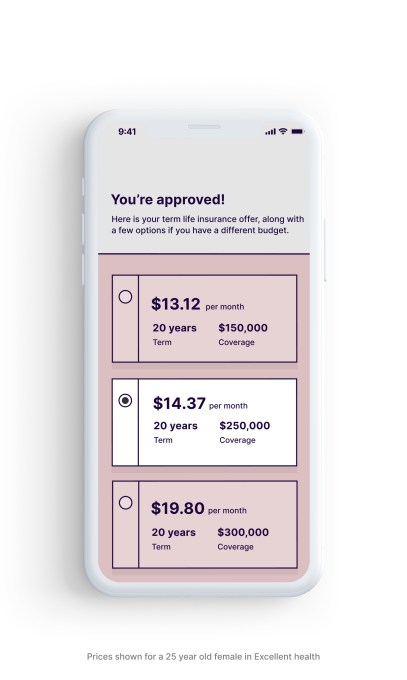

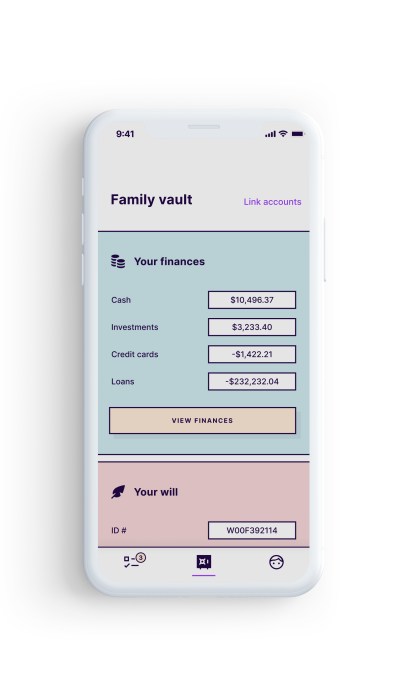

A new app called Fabric aims to make it simpler for parents to plan for their family’s long-term financial well-being. The goal is to offer parents a one-stop-shop that includes the ability to ability for term life insurance from their phone, create a free will in about five minutes, and collaborate with a spouse or partner to organize key financial accounts or other important documents. In addition, parents are able to coordinate with beneficiaries, children’s guardians, attorneys, financial advisors, and others right from the app.

Fabric was originally founded in 2015 by Adam Erlebacher, previously the COO at online bank Simple, and Steven Surgnier, previously the Director of Data at Simple. The company last year raised a $10 million Series A led by Bessemer Venture Partners, after having sold life insurance coverage to thousands of families.

Since launch, Fabric has expanded beyond life insurance to offer other services, like easy will creation and the addition of tools that help families organize their financial and legal information in one place. The idea, the company explained at the time, was to offer today’s busy parents a better alternative to meetings with agents to discuss complicated life insurance products. Instead, the company offers a simple, 10-minute life insurance application and the option to connect with a licensed team if they need additional help, as well as a similarly simplified will creation workflow.

As with the founders’ earlier company, Simple, which offered a better front-end to banking while actual bank accounts were held elsewhere, Fabric’s life insurance policies are issued by “A” rated insurer, Vantis Life, not Fabric itself.

However, until now, Fabric’s suite of services were only available on the web. They’re now offered in an app for added convenience. The app is initially available on iOS with an Android version in the works.

“Money can be especially stressful when you’re trying to build a family and a career,” said Fabric co-founder and CEO Adam Erlebacher. “In one survey by Everyday Health, 52% of respondents said financial issues regularly stress them out, and people between the ages of 38 to 53 were the most stressed out financially. Parents want to have more control over their families’ long-term financial well-being and today’s dusty old products and tools are failing them,” he added.

Using the Fabric app, parents can take advantage of any of its offerings, including the option to apply for life insurance from the phone and get immediate approval. The app also makes it possible to share the policy information with beneficiaries, so it doesn’t get lost.

Another feature lets you create your will for free, and share that information with key people as well, including the witnesses you need to coordinate with in order to finalize the will, for example. And a spouse can choose to mirror your will, which speeds up the process of creating a second one with the same set of choices.

Fabric also helps to address an issue that often only comes up after it’s too late or in other emergency situations — organizing both parents’ finances in a single place. Many working adults today have not just a bank account, but also have investment accounts, 401Ks, IRAs, and credit cards, or a combination of those. But their partner may not know where to find this information or where the accounts are held.

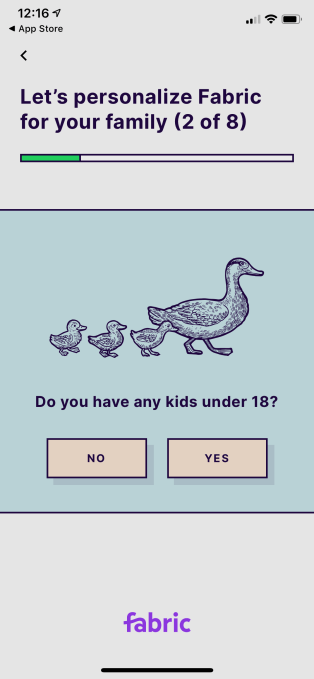

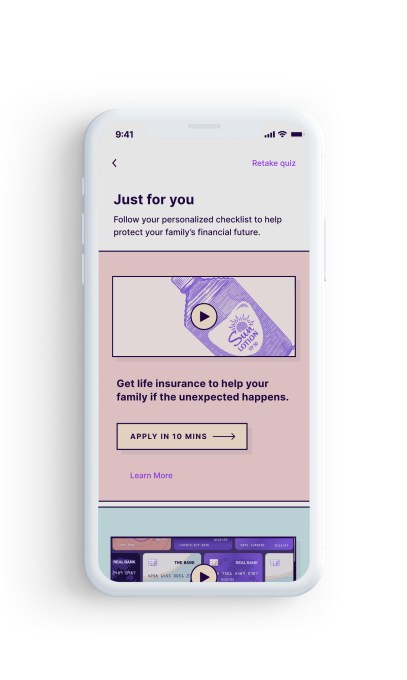

The app, which we put through its paces (but didn’t purchase life insurance through), is very easy to use. It starts off with a short quiz to get a handle on your financial picture. It then delivers you to a personalized homescreen with a checklist of suggestions of what to do next. Naturally, this includes the life insurance application, as this is where Fabric’s revenue lies. And if you’re lacking a will and have other fiances to organize, these are featured, too.

The online forms are easy to fill out, despite the smartphone’s reduced screen space compared with a web browser, and Fabric has taken the time to get the small touches right — like when you enter a phone number, the numeric keypad appears, for example, or the integration of address lookup so you can just tap on the match and have the rest autofill. It also saves your work in progress, so you can finish later in case you get interrupted — as parents often do. And it explains terms, like “executor,” so you know what sort of rights you’re assigning.

Given its focus, Fabric protects user information with bank-grade security, including 256-bit encryption, two-factor authentication, automatic lockouts, biometrics, and other adaptive security features.

Fabric isn’t alone in helping parents and others financially plan wills and more from their iPhone. Other apps exist in this space, including will planning apps from Tomorrow, LegalZoom, Qwill, and others. Plus many insurers offer a mobile experience. Fabric is unique because it puts wills, insurance, and other tools into a single destination, without complicating the user interface.

Fabric’s app is a free download on the App Store.

Powered by WPeMatico

Tidemark, the cloud financial planning platform announced $25 million in additional funding today along with some new growth numbers.

Tidemark, the cloud financial planning platform announced $25 million in additional funding today along with some new growth numbers.

Existing investors Greylock Partners, Andreessen Horowitz, Redpoint Ventures, Tenaya Capital, and Silicon Valley Bank all participated in the round along with new investor, fellow cloud company Workday.

Today’s investment brings the total raised to $100… Read More

Powered by WPeMatico

Tidemark announced the latest update to its cloud financial planning platform today, one that mixes big data from internal and external sources to give customers a way to predict what’s going to happen next, rather than simply report on what’s happened. Tidemark CEO Christian Gheorghe says today, too many companies are looking at their financials and not seeing the whole… Read More

Tidemark announced the latest update to its cloud financial planning platform today, one that mixes big data from internal and external sources to give customers a way to predict what’s going to happen next, rather than simply report on what’s happened. Tidemark CEO Christian Gheorghe says today, too many companies are looking at their financials and not seeing the whole… Read More

Powered by WPeMatico