Finance

Auto Added by WPeMatico

Auto Added by WPeMatico

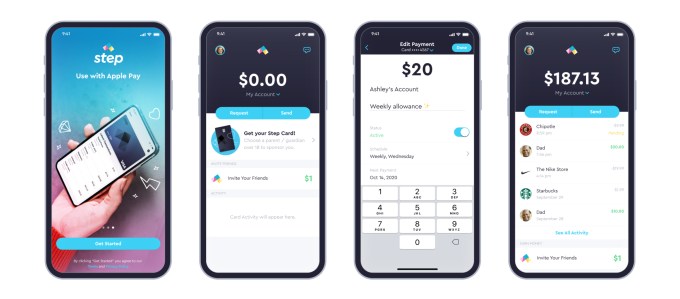

Step, the digital banking service aimed at teens and endorsed by TikTok star Charli D’Amelio, announced this morning the close of a $100 million round of Series C funding after growing to more than 1.5 million users just six months after launch. The new round, led by General Catalyst, comes shortly after Step’s $50 million Series B, announced at the end of last year after the startup hit half a million users in only two months post-launch.

The new round also includes participation from Step’s existing investors, Coatue, Stripe, Charli D’Amelio, The Chainsmokers, Will Smith and Jeffrey Katzenberg, and brings on newcomer Franklin Templeton, signaling a plan to move into investments is on the horizon. It also includes actor and musician Jared Leto. Step is also formally announcing NBA All-Star Stephen Curry as an investor, which had not previously been disclosed, as well as former Square executives Sarah Friar, Jacqueline Reses and Gokul Rajaram.

As a result of the fundraise, Kyle Doherty of General Catalyst is joining Step’s board. To date, Step has raised more than $175 million.

Image Credits: Step

According to CEO CJ MacDonald, Step hasn’t yet spent the money from its Series B, but believes the additional funds can help the startup grow more quickly.

“We’ve signed up more than a million and a half accounts in the first six months. We’re signing up 10,000 accounts-plus a day, and there’s just a lot of things that we want to do to bring this to millions and millions of households to help educate the next generation be smarter with money,” he says. At the time of the Series B, for comparison, Step said it was adding around 7,000 to 10,000 accounts per day.

“Honestly we don’t need the capital,” MacDonald added. “It’s just we think speed to market is really key and we think we can accelerate our growth and invest in infrastructure.”

The company is also planning to hire across operations, engineering, product and design, to double its now 65-person team over the next year.

Step today competes in a crowded market of mobile banking services aimed at a younger demographic, but it’s one of very few that targets teenagers ages 13 to 18. Through Step’s app, teens gain access to an FDIC-insured bank account without fees and a secured Visa card that helps them establish credit before they turn 18. The app also offers Venmo-like functionality for sending money to friends.

Image Credits: Step

Step’s growth so far has benefitted from a combination of factors, including word-of-mouth, use of social media and its popular referral program, which has paid out a few dollars per new sign-up. Step has also leveraged its partnerships with social media influencers like D’Amelio and Josh Richards, as well as celebs like Step investor Justin Timberlake.

The company believes the Curry announcement may also help to raise awareness about the banking app. As a father of three, if Curry talks about introducing Step to his own children, people will take notice.

While the additional funds are focused on driving growth, Step is also thinking about its future as its existing users begin to age up. The company plans to enter into the credit and lending market, as well as introduce investments at some point in the future. The Franklin Templeton investment could be useful here, MacDonald notes.

“Franklin [Templeton is] obviously, one of the largest financial institutions in the world. And, as we start thinking about investments and the journey of the customer, to have a great brand like Franklin Templeton that’s invested in this round — I think it’s just a testament to where they see the world going,” he says.

Step’s fundraise falls on the same day that competitor Current and Greenlight, both which focus on families, also raised new rounds.

Powered by WPeMatico

U.S.-based challenger bank Current, which has now grown to nearly 3 million users, announced this morning it has raised a $220 million round of Series D funding, led by new investor Andreessen Horowitz (a16z). The funding swiftly follows Current’s $131 million Series C at the end of last year, at which point the company had doubled its user base over just six months to more than 2 million users.

As a result of the new round, the fintech company has roughly tripled its valuation in five months, to $2.2 billion.

Other participants in the round include returning investors Tiger Global Management, TQ Ventures (the fund managed by media executive Scooter Braun), Avenir, Sapphire Ventures, Foundation Capital, Wellington Management and EXPA. David George, who led the round with a16z, will become a Current board member.

Current began its life as a teen debit card controlled by parents, but later expanded to offer personal checking accounts powered by the same underlying banking technology. Like a range of modern-day “neobanks,” or digital banks, the Current app offers a baseline of standard features like free overdrafts, no minimum balance requirements, faster direct deposits, instant spending notifications, banking insights, free ATMs, check deposits using your phone’s camera and more. It also last year launched a points rewards program in an effort to better differentiate its service from the growing number of competitors and became one of the first banks to transfer the early round of stimulus payments during the pandemic.

These days, Current is partnering with creators, like the recently announced MrBeast (aka Jimmy Donaldson), who said last week on his YouTube channel that he will personally send $1 to the first 100,000 people who sign up using his Creator code. MrBeast is also an investor.

Like other fintechs in its same space, Current has benefitted from the younger generation’s adoption of mobile banking apps instead of larger, traditional banks, which they feel don’t serve their interests. Its average customer age is 27, for example. Digital banks can keep costs down by not having to pay for the overhead of brick-and-mortar locations, allowing them to roll out benefits like reduced or zero account fees and other consumer-friendly protections.

Current today continues to offer teen banking, in a challenge to mobile banking app Step, which has also leveraged social media influencers to get the word out with a younger demographic. But Step today is appealing to the 13 to 18-year-old crowd directly, offering banking services and a secured card. Current, meanwhile, targets its service to the parents.

Its teen account costs $36 per year, while personal checking is available both as a free and premium ($4.99/mo) service. The company in the past has said its primary focus is the more than 130 million Americans who live paycheck to paycheck. This continues to be its main drive today, though the mission may attract a broader slice of the American population over time.

“We are still focused on onboarding people to the financial system, making sure that everyone has access to everything, and then democratizing — or going out and getting that value — in this new world that’s being rewritten and bringing it back to as many people as possible,” says Current CEO and founder Stuart Sopp. “Now, in that increase of scope and time. I think we’re going to pick up more and more people.”

Current says the new funds will be used to grow the company and its member base as it expands it range of banking products. One key area of new investment will be cryptocurrency, it says, which will involve a partnership and an educational component to help Current’s users better understand the crypto market.

As it turns out, Sopp’s background includes crypto, in addition to Wall Street trading. In fact, an early version of Current designed by Sopp and CTO Trevor Marshall involved crypto.

“A little-known fact is that Current started with Bitcoin wallet addresses and Ripple gateways,” he says. But the team realized the technology was a little too nascent at the time, and moved to mobile banking. “We have this background, and this knowledge of how it all works. Now do we need to build it ourselves? No, I don’t think we need to build it all ourselves. There’s lots of good companies out there,” he says.

Crypto fits into Current’s vision of democratizing access to financial systems to those in the U.S. who are today underserved by traditional banking and investing products and services.

“There’s a ton of value being created [in crypto] and we want to make sure we have this nexus of providing safe, and trustworthy financial services in that world, as well as what we already exist in,” notes Sopp. “And then, lending, credit cards,” he adds, noting how important these moves are “done safely, in a respectful way for our demographic — because traditionally most of our members have a FICO score of 650.”

In addition, Current will use the new funds for hiring across all roles, including marketing, product, engineering, finance, customer success, fraud and risk, and, of course, crypto. The company today has 100 employees, and plans to grow to around 200 or 300 in the next 18 months.

Current’s fundraise remarkably falls on the same day that competitor Step and Greenlight, both which focus on families, also raised new rounds.

“This new generation of customers doesn’t want to bank in physical branches,” said a16z’s David George, in a statement. “We believe there will be a shift in the next 10 years to mobile and consumer-focused banking services powered by innovation in technology, and with Current’s exceptional growth over the past year, they’ve clearly demonstrated they’re at the forefront of this trend. Their product is among the best in the market, and they have proven an ability to reach customers who previously were unserved or underserved by traditional banks,” he said.

Powered by WPeMatico

Origin stories are satisfying because we already know the hero will overcome the odds — and in doing so, they’ll reveal their core strengths.

This week, we published a four-part series about how Klaviyo co-founders Andrew Bialecki and Ed Hallen bootstrapped their startup into an e-commerce marketing automation platform now valued at $4.15 billion.

Neither founder was bitten by a radioactive spider or received a serum that enhanced their entrepreneurial skills; instead, they focused on outreach to prospective customers to find out what they were willing to pay for and largely ignored the competition.

“Bootstrapping Klaviyo, it came out of this: ‘Hey, if we are super disciplined about finding a problem that someone will pay us to solve, we have a real company,’” said Hallen.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Even though millions of us respond every day to the personalized, automated emails sent through its platform, Klaviyo still isn’t a well-known brand. Our ongoing series of EC-1s offers entrepreneurs real insight into growing and scaling successful companies, but they’re also extremely useful for consumers who want to understand how the internet really works.

Thanks very much for reading Extra Crunch; I hope you have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Nigel Sussman

Image Credits: slowcentury (opens in a new window) / Getty Images

Several micromobility companies once operated in my city, but consolidation has reduced that to a small handful.

Now that many consumers are buying their own e-bikes and e-scooters, shared dockless micromobility “just hasn’t proven itself to be a profitable line of business,” Puneeth Meruva, an associate at Trucks Venture Capital, told TechCrunch.

There’s only one dockless electric moped provider in my town, so price is no longer a consideration. Instead, my first priority is to find a vehicle with the best-charged battery. (San Francisco has a lot of hills, and you never know where the day might take you.)

Larger players like Lime and Bird have vertically integrated tech stacks for fleet management features like this, but there are also opportunities for startups — imagine a “phantom scooter” that drives itself to a neighborhood with high demand or a moped that alerts drivers if there’s traffic ahead.

This in-depth industry analysis shows how increased regulation on the local level and changing consumer habits are pushing micromobility providers to adapt and innovate.

“Whether you want to stack regulatory compliance on the vehicles, do safety features like ADAS or add mapping content, you kind of need this platform where you can actively develop and launch new apps on the vehicle without having to bring it back to the factory,” Meruva said.

Image Credits: TechCrunch/Bryce Durbin

If the definition of insanity is doing the same thing over and over and expecting a different outcome, then one might say the cybersecurity industry is insane.

Criminals continue to innovate with highly sophisticated attack methods, but many security organizations still use the same technological approaches they did 10 years ago. The world has changed, but cybersecurity hasn’t kept pace.

Image Credits: ra2studio (opens in a new window) / Getty Images

By 2025, 463 exabytes of data will be created each day, according to some estimates. It’s now easier than ever to translate physical and digital actions into data, and businesses of all types have raced to amass as much data as possible in order to gain a competitive edge.

However, in our collective infatuation with data (and obtaining more of it), what’s often overlooked is the role that storytelling plays in extracting real value from data.

The reality is that data by itself is insufficient to really influence human behavior. Whether the goal is to improve a business’ bottom line or convince people to stay home amid a pandemic, it’s the narrative that compels action, not the numbers alone.

As more data is collected and analyzed, communication and storytelling will become even more integral in the data science discipline because of their role in separating the signal from the noise.

Image Credits: Raquel Segato/EyeEm (opens in a new window) / Getty Images

We all need to be taking precautionary measures, not just in light of COVID, but to ensure our firms can continue to thrive when faced with unexpected tragedy.

So ask yourself this question: “What would happen if I or my partner(s) checked into the hospital tomorrow and had no phone and/or was too sick to call anyone, and that went on for two or three weeks (or longer)?”

If the answer is “I’m really not sure,” then you don’t have a business continuity plan.

Image Credits: rubberball (opens in a new window) / Getty Images

After years of sustained growth, the pandemic supercharged the outdoor recreation industry. Startups that provide services like camper vans, private campsites and trail-finding apps became relevant to millions of new users when COVID-19 shut down indoor recreation, building on an existing boom in outdoor recreation.

Startups like Outdoorsy, AllTrails, Cabana, Hipcamp, Kibbo and Lowergear Outdoors have seen significant growth, but to keep it going, consumers who discovered a fondness for the great outdoors during the pandemic must turn it into a lifelong interest.

Image Credits: MaboHH / Getty Images

Dell last week agreed to spin out VMware in exchange for a huge one-time dividend, a five-year commercial partnership agreement, lots of stock for existing Dell shareholders and Michael Dell retaining his role as chairman of its board.

So, where does the deal leave VMware in terms of independence and in terms of Dell influence?

Image Credits: Westend61 (opens in a new window) / Getty Images

Many emerging and mature organizations survive or die based on their ability to scale. Scale quicker. Scale cheaper. Scale right.

Typically the IT team bears that burden — on top of countless other demands. IT teams move mountains for their organizations while scaling the tech platform as fast as possible, putting out the latest infrastructure fire and responding to countless day-to-day requests.

The most helpful gift any chief information officer or chief technology officer can give their IT teams is more time. Many people think that means adding another team member. But it could be as simple as introducing a low-code integration platform.

Image Credits: Nigel Sussman (opens in a new window)

A stunning first quarter in venture capital funding was not restricted to the United States; Europe also had one hell of a start to the year.

The venture capital world kicked off its 2021 European investing cycle with enough activity to set the continent on the path that would crush yearly records.

Inside the data, there’s lots to unpack, including which sectors of European startups stood out in terms of capital raised, rising seed and late-stage deals, and dollar volume. We’ll also need to discuss exits — the Deliveroo IPO and its various woes was not the only transaction from the period worth understanding.

We’ll keep in mind that all venture capital data lags reality somewhat, as many deals from a particular period are not disclosed or discovered until long after they actually occurred.

In this case, it makes the numbers all the more impressive.

Image Credits: Zastrozhnov (opens in a new window) / Getty Images

Robotic process automation unicorn UiPath went public this week, concentrating our focus on its value.

UiPath raised its last private round when the markets were most interested in public offerings and is now going public in a slightly altered climate.

In numerical terms, UiPath raised its IPO range from $43 to $50 per share to $52 to $54 per share. That’s a 21% jump in the value of the lower end of its range and an 8% gain to the value of the upper end of its per-share IPO price interval.

UiPath is also selling more shares than before, which should make its total valuation slightly larger at the top end than a mere 8% gain. So let’s go through the math one more time.

Image Credits: Nigel Sussman (opens in a new window)

The investment landscape for insurtech startups is off to a hot start in Q2 2021. Since the end of the first quarter, we’ve seen several players in the broad startup category announce new capital.

But, as anyone who’s familiar with startups that offer insurance-related products and services knows, the sector is enough of a mixed bag that one needs to segment down to get clarity on how constituent companies are performing.

Let’s discuss insurtech’s 2020 as a whole, peek at some preliminary 2021 venture data and then dive deep into what we’ve collected regarding growth among insurtech marketplace players.

Covering longitudinal progress of specific startup categories is one of our favorite things to do. So, please, walk with us!

Image Credits: Kehan Chen / Getty Images

Research papers come out far too frequently for anyone to read them all. That’s especially true in the field of machine learning, which now affects (and produces papers in) practically every industry and company.

This column aims to collect some of the most relevant recent discoveries and papers — particularly in, but not limited to, artificial intelligence — and explain why they matter.

This week, we dove into “introspective failure prediction,” using ML to identify dangerous moles, and spotting cows from space.

Image Credits: Gearstd (opens in a new window) / Getty Images

With strict privacy laws such as GDPR and CCPA already listing big-ticket penalties — and a growing number of countries following suit — businesses have little option but to comply.

It’s not just bigger, established businesses offering privacy and compliance tech; brand-new startups are filling in the gaps in this emerging and growing space.

Privacy isn’t dead, as many would have you believe. New regulations, stricter cross-border data transfer rules and increasing calls for data sovereignty have helped the privacy startup space grow thanks to an uptick in investor support.

This is how we got here, and where investors are spending.

Image Credits: Nigel Sussman (opens in a new window)

UiPath is not worth $36 billion, as we might have expected, but at a figure below $30 billion.

At $29.1 billion, UiPath has a roughly 35x run-rate multiple. That just about ties it for eighth-best overall. Among all public cloud companies. That means that UiPath is insanely valuable, just not that insanely valuable.

So what went wrong with the company’s final private round? The Exchange’s hunch is that UiPath’s final private investors expected the market to stay as hot as it once was, but it has cooled since the first two months of the year. So, instead of UiPath coming to the market in the expected climate, the company instead had to price where it did because the weather predicted by its final private price had already chilled.

Those investors gambled, in other words, hoping that a last-minute, pre-IPO round could snag them a rapid return on a company going public in a hot market. That didn’t work out.

And how bad is that? Not very! UiPath’s IPO is more a meeting of private-market exuberance and modestly more conservative public markets. It’s nothing to cry about.

Image Credits: d3sign (opens in a new window) / Getty Images

The second half of 2021 will bring incredible growth, the likes of which we haven’t seen in a long time.

Here’s how marketing in tech will shift — and what you need to know to reach more customers and accelerate growth this year.

First and foremost, differentiation is going to be imperative. It’s already hard enough to stand out and get noticed, and it’s about to get much more difficult as new companies emerge and investments and budgets balloon in the latter half of the year.

Additionally, tech companies need to be mindful not to ignore the most important part of the ecosystem: people. Technology will only take you so far, and it’s not going to be enough to survive the competition.

Tactically, the most successful tech companies will embrace video and experimentation in their marketing — two components that will catapult them ahead of the competition.

Ignoring these predictions, backed by empirical evidence, will be detrimental and devastating. Fasten your seatbelts: 2021 is going to be a turbocharged year of growth opportunities for marketing in tech.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

I’m a female entrepreneur who created my first startup a few months ago.

Once my startup gets off the ground — and as COVID-19 gets under control — I’d like to visit the United States to test the market and meet with investors. Which visas would allow me to do that?

—Noteworthy in Nairobi

Despite a somewhat circuitous route, UiPath closed its first day as a public company worth more than it was in its Series F round — when it sold 12,043,202 shares at $62.27576 apiece, per SEC filings. More simply, UiPath closed on Wednesday worth more per-share than it was in February.

How you might value the company, whether you prefer a simple or fully diluted share count, is somewhat immaterial at this juncture. UiPath had a good day.

TechCrunch spoke with UiPath CFO Ashim Gupta, curious about the company’s choice of a traditional IPO, its general avoidance of adjusted metrics in its SEC filings and the IPO market’s current temperature.

Image Credits: Nigel Sussman (opens in a new window)

The global venture capital market had a cracking start to the year. Coming off a 2020 high, VC totals in the United States, in Europe, and among competitive verticals like insurtech and AI are on pace to set new records in 2021.

The rapid-fire deal-making and trend of larger venture checks at higher valuations that The Exchange has tracked for some time require private-market investors to make decisions faster than ever. For venture capitalists, the timeline for reaching conviction around a startup’s thesis and executing due diligence has become compressed.

Some venture capitalists are turning to data to move more quickly. Some are spending more time preparing to be vetted themselves. And some investors are simply doing the work beforehand.

We were tipped off to the concept of pre-diligence during the reporting process for a look into recent fundraising trends in the AI/ML space. Sapphire investor Jai Das, when asked about how he was handling a competitive and swiftly moving market for AI startup investments, said that “most firms are completing their due diligence way before the financing actually happens.”

How does that work in practice?

Image Credits: MartinvBarraud (opens in a new window) / Getty Images

Your clients might not demand 24/7 customer service yet, but they’re certainly hoping for it.

But how can a startup with a lean staff provide round-the-clock customer care? There are several options available, but more than ever, outsourcing is one of them.

When should your startup consider outsourcing its customer care? And what should you look for in a provider?

Here are some insights on what customer care as a service (CCaaS) can do for you, and how fast-growing startups have been leveraging this new class of partners to boost customer satisfaction.

Image Credits: Erik Isakson / Getty Images

Productivity infrastructure is on the rise and will continue to be front and center as companies evaluate what their future of work entails and how to maintain productivity, rapid software development and innovation with distributed teams.

Understanding the benefits, use cases and steps to consider can propel organizations into the next phase of digital transformation.

Image Credits: Klaus Vedfelt (opens in a new window) / Getty Images

The clock begins ticking on a startup the day the doors open. Regardless of a young company’s struggles or success, sooner or later the question of when, how or whether to sell the enterprise presents itself. It’s possibly the biggest question an entrepreneur will face.

For founders who self-funded (bootstrapped) their startup, a boardroom full of additional factors comes into play. Some are the same as for investor-funded firms, but many are unique.

After 18 years of bootstrapping a BI software firm into a business that now serves 28,000 companies and 3 million users in 75 countries, here’s what I’ve learned about myself, my company, about entrepreneurship and about when to grab for that brass ring.

Put happiness at the center of the decision, and let your intuition — the instincts that made you the person you are today — be your guide.

Powered by WPeMatico

Nearly exactly one month ago, digital real estate platform Loft announced it had closed on $425 million in Series D funding led by New York-based D1 Capital Partners. The round included participation from a mix of new and existing investors such as DST, Tiger Global, Andreessen Horowitz, Fifth Wall and QED, among many others.

At the time, Loft was valued at $2.2 billion, a huge jump from its being just near unicorn territory in January 2020. The round marked one of the largest ever for a Brazilian startup.

Now, today, São Paulo-based Loft has announced an extension to that round with the closing of $100 million in additional funding that values the company at $2.9 billion. This means that the 3-year-old startup has increased its valuation by $700 million in a matter of weeks.

Baillie Gifford led the Series D-2 round, which also included participation from Tarsadia, Flight Deck, Caffeinated and others. Individuals also put money in the extension, including the founders of Better (Zach Frenkel), GoPuff, Instacart, Kavak and Sweetgreen.

Loft has seen great success in its efforts to serve as a “one-stop shop” for Brazilians to help them manage the home buying and selling process.

Image Credits: Loft

In 2020, Loft saw the number of listings on its site increase “10 to 15 times,” according to co-founder and co-CEO Mate Pencz. Today, the company actively maintains more than 13,000 property listings in approximately 130 regions across São Paulo and Rio de Janeiro, partnering with more than 30,000 brokers. Not only are more people open to transacting digitally, more people are looking to buy versus rent in the country.

“We did more than 6x YoY growth with many thousands of transactions over the course of 2020,” Pencz told TechCrunch at the time of the company’s last raise. “We’re now growing into the many tens of thousands, and soon hundreds of thousands, of active listings.”

The decision to raise more capital so soon was due to a variety of factors. For one, Loft has received “overwhelming investor interest” even after “a very, very oversubscribed main round,” Pencz said.

“We have seen a continued acceleration in our market share growth, especially in São Paulo and Rio de Janeiro, the two markets we currently operate in,” he added. “We saw an opportunity to grow even faster with additional capital.”

Pencz also pointed out that Baillie Gifford has relatively large minimum check size requirements, which led to the extension being conducted at a higher price and increased the total round size “by quite a bit to be able to accommodate them.”

While the company was less forthcoming about its financials as of late, it told me last year that it had notched “over $150 million in annualized revenues in its first full year of operation” via more than 1,000 transactions.

The company’s revenues and GMV (gross merchandise value) “increased significantly” in 2020, according to Pencz, who declined to provide more specifics. He did say those figures are “multiples higher from where they were,” and that Loft has “a very clear horizon to profitability.”

Pencz and Florian Hagenbuch founded Loft in early 2018 and today serve as its co-CEOs. The aim of the platform, in the company’s words, is “bringing Latin American real estate into the e-commerce age by developing online alternatives to analogue legacy processes and leveraging data to create transparency in highly opaque markets.” The U.S. real estate tech company with the closest model to Loft’s is probably Zillow, according to Pencz.

In the United States, prospective buyers and sellers have the benefit of MLSs, which in the words of the National Association of Realtors, are private databases that are created, maintained and paid for by real estate professionals to help their clients buy and sell property. Loft itself spent years and many dollars in creating its own such databases for the Brazilian market. Besides helping people buy and sell homes, it offers services around insurance, renovations and rentals.

In 2020, Loft also entered the mortgage business by acquiring one of the largest mortgage brokerage businesses in Brazil. The startup now ranks among the top-three mortgage originators in the country, according to Pencz. When it comes to helping people apply for mortgages, he likened Loft to U.S.-based Better.com.

This latest financing brings Loft’s total funding raised to an impressive $800 million. Other backers include Brazil’s Canary and a group of high-profile angel investors such as Max Levchin of Affirm and PayPal, Palantir co-founder Joe Lonsdale, Instagram co-founder Mike Krieger and David Vélez, CEO and founder of Brazilian fintech Nubank. In addition, Loft has also raised more than $100 million in debt financing through a series of publicly listed real estate funds.

Loft plans to use its new capital in part to expand across Brazil and eventually in Latin America and beyond. The company is also planning to explore more M&A opportunities.

This article was updated post-publication to reflect accurate investor information.

Powered by WPeMatico

For IBM, much of the last eight years simply posting positive revenue growth was a challenge. In fact, the company had a period between 2013 and 2018 when it experienced an astonishing 22 straight quarters of negative revenue growth. So when Big Blue reported yesterday that revenue was up slightly, I’m sure the company took that as a win. Investors appear to be happy with the results, with the stock up 4.73% this morning as of publication.

Consider that over the last eight quarters encompassing FY2019 and FY2020, the company had only one positive revenue quarter when it was up 0.1% in Q42019. It had had five losing quarters prior to that one. When you look at yesterday’s report in that light, and combine it with growth in the Cloud and Cognitive Services group, it adds up to a decent quarter for IBM, one it badly needed after another negative report in the prior quarter.

Looking back at the January report, the company reported Cloud and Cognitive Services revenues down 4.5% at $6.8 billion, which was a big blow, considering the company has been betting much of its future on those very areas, fueled in large part by the $34 billion Red Hat acquisition in 2018.

Its most recent quarterly report proved much better, with the company reporting Cloud and Cognitive Services revenues of $5.4 billion, up 3.8% YoY. Interestingly quarter-on-quarter revenue for the segment was down, but rose on a year-over-year basis. Perhaps a year-end enterprise revenue push could account for the difference between Q4 2020 and Q1 2021.

At any rate, IBM CEO Arvind Krishna saw today’s report as a positive sign that his attempts to push the company toward a future focused on hybrid computing and AI were starting to take root. He also saw enough in the report to predict some growth this year.

“In our last call, we shared our financial expectations for the year, revenue growth and $11 billion to $12 billion of adjusted free cash flow. While it’s still early in the year and a lot remains to be done, we are confident enough to say that we are on track,” Krishna said in the earnings call with analysts yesterday.

The company has made a number of smaller acquisitions over the last year, including a couple of consulting companies, which should help as they try to work with customers around the transition to hybrid computing and artificial intelligence, both of which tend to require a lot of hand-holding to get done.

At the same time, of course, the company is continuing apace with its spin out of the legacy infrastructure services division, which it announced last year. The plan at this point is to rename the company Kyndryl (an unfortunate choice) and complete the spin out by year’s end.

CFO Jim Kavanaugh also sees the modestly positive quarter as something the company can build on. “…in fact we are even more confident in the position we put in place with regards to our two most important measures, one, revenue growth, and second, adjusted free cash flow, which is going to provide the fuel for the investments needed for us to capture that hybrid cloud $1 trillion TAM,” Kavanaugh said in the earnings call with analysts.

All of this is being pushed by Red Hat, which grew revenue 15% in the most recent quarter, something the company is banking will continue to advance it deeper into positive territory throughout the rest of 2021.

Krishna is not looking for booming growth by any means. He just wants growth, and even sustained single-digit top line expansion will make him happy. “Our systems if I take a two-year to three-year view kind of flattish, but in any given year it might increase or decrease but not by a whole lot. It doesn’t impact the top line a lot and that’s how sort of we get to the mid-single-digit sustainably,” Krishna said in the call.

The CEO simply wants to bring some long-term stability back to the company it has been sadly lacking in recent years. Of course, it’s hard to know if this quarter was a temporary upward blip on IBM’s earnings chart, one of those fluctuations up or down he spoke of, or if it is the corner the company has been looking to turn for years. Only time will tell whether IBM can sustain the modest revenue goals Krishna has set for the organization, or if it will fall back into the revenue doldrums that have plagued the company for the last eight years.

Powered by WPeMatico

“Challenger” startups in banking and insurance have upended their industries, and picked up significant business, by building more customer-friendly tools and services — more personalized, easier to access and usually competitively priced — than those typically provided by their bigger, incumbent rivals. Now, a startup out of Romania that is building tools to help the incumbents respond with better services of their own is announcing a significant round of funding as its business grows.

FintechOS, which has built a low-code platform aimed at larger (older) banking and insurance companies to help them build new services and analytics on top of and around their existing infrastructure, has raised €51 million ($61.5 million at today’s rates, but $60 million at the time of the deal closing) in a Series B round of funding.

FintechOS’s opportunity has been to target the wave of incumbents in the insurance and banking industries that have been slowly watching as newer players like Lemonade (in insurance) and a huge plethora of challenger banks (Revolut, N26, Monzo and many others) are swooping in and picking up customers, especially among younger demographics, while they have been unable to respond mostly because their infrastructure is too old and big. Turning a huge ship around, as we have seen, is no small task — a situation that has become only more apparent in the last year of pandemic living and the big shift to digital interactions that resulted from it.

“When we launched FintechOS in 2017, we could already see existing solutions to digital transformation would struggle to deliver tangible results. By contrast, our unique approach has quickly inspired a sea-change in how financial institutions address digitization and engage with their customers,” said Teodor Blidarus, co-founder and CEO at FintechOS, in a statement. “Events over the last year have only increased pressure on our industry to evolve and as a result we’re seeing growing demand for our powerful platforms. Our latest round of funding will help us grow at the pace needed to improve outcomes for financial institutions and their customers globally.”

(It is not the only one. Others out of Europe in the space of bringing new tools to incumbent banks to help them make more modern and competitive products include 10x, Thought Machine, Temenos, Mambu and many more.)

The Series B round of funding is being led by Draper Esprit, with Earlybird, Gapminder Ventures, Launchub and OTB Ventures (which all participated in its Series A in December 2019) also participating. There are other backers in the round that are not being disclosed at this time, the startup added. FintechOS is also not disclosing its valuation. The company, based out of Bucharest, has raised just under $80 million to date.

FintechOS is active today in the U.K. and Europe — where it has been growing at a CAGR of 200% and says its services touch “millions” of people, with some of its key customers including the likes of banking giants Societe Generale and IdeaBank and international insurance brokers Howden. The plan will be to continue investing in those markets, as well as expanding internationally.

And it will be adding more services. Today, the banking platform is designed to help banks launch more retail services for consumers and small and medium business customers, and for insurance companies to build new health, life and general insurance products (there are a lot of synergies in how insurance and financial services companies have been built over the years, and so it’s a natural couplet when it comes to building tools for those industries).

In the financial sector, FintechOS lets banks build in new digital onboarding flows, credit cards and loan products, savings and mortgage products. Insurance products include new approaches to generating and handling quotes, customer onboarding and management and claims automation — which may well bring FintechOS into closer contact and collaboration with the most successful startup to come out of its home country to date, the RPA juggernaut UiPath. In all cases, it helps stitch together data from a bank’s own systems with more modern tooling, and to link that up with yet more modern tools to help process that data more easily.

This is “low code,” but it typically means that the company needs to work with third parties to enable all of this. Partners include the likes of integrators and other global services technicians, such as Microsoft, Deloitte, CapGemini, KPMG and so on. (And the founders of the startup themselves come from consulting backgrounds so they well understand the role these companies play in the process of bringing technology into big businesses.)

FintechOS is tapping into a couple of very big trends that have arguably been the biggest in the financial and related insurance industries.

The first of these is the fact that core services around things like credit/loans, current deposits and savings are not just very complex to build but actually have largely become commoditized — similar to digital payments — and so packaging them up and turning them into services that can be integrated by way of an API makes them more easily accessed without the heavy lifting needed to build them from scratch. This lets companies focus instead on customer service or building more interesting tools around those basic services to customise them (for example AI-based personalization). Disintermediating basic functions from the services built around them is arguably a bigger trend, but it has been especially prevalent in enterprise, which has long been a slow-moving space when it comes to innovation in the back-end, and the front-end.

The second of these is the big swing toward using no-code and low-code tools to empower more people within organizations to get stuck in when they can see something not working as efficiently as it could, and building the workflows themselves to improve that. This also applies to trying out and testing new products — again something that typically has not been done in financial and insurance services but can now be possible with low-code and no-code tools.

“Not only is our technology helping financial institutions become customer centric, but it’s also helping them provide products and services to more people and businesses,” said Sergiu Negut, the other co-founder who is FintechOS’s CFO and COO, in a separate statement. “With so many markets still underserved, the ability to tailor offerings to a segment of one offers the opportunity to increase financial inclusion and adheres to our ideal that easy access to financial services is essential. We’re delighted to be working with investors who share our views on how fintech should be transforming the financial services industry.”

Notably, Draper Esprit also has backed Thought Machine, another big player in the world of fintech that is taking some of the learnings and models that have helped new entrants disrupt incumbents, and is packaging them up as services for incumbents, too. It takes a different approach to doing this, not using low-code but smart contracts, which could be one reason why the VC doesn’t see the investments as conflict of interest. They are also tackling an enormous market, and so at least for now there is room for them, and many others in the space, such as 10x, Temenos, Mambu, Rapyd and many others.

“When we met Teo and Sergiu, we were immediately convinced of their vision: a data led, end-to-end platform, facilitated with a low-code/no-code infrastructure,” Vinoth Jayakumar, partner at Draper Esprit, said in a statement. “Incumbent financial services firms have cost-to-income ratios up to 90%, so we see a huge and increasing need for infrastructure software that allows digitisation at speed, ease and lower cost. Draper Esprit builds enduring partnerships; with the team at FintechOS we hope to build an enduring fintech company that will dramatically change financial services experiences for people all over the world.”

Powered by WPeMatico

Fintech startup Payhawk has raised a $20 million funding round. QED Investors is leading the round with existing investor Earlybird Digital East also participating. Payhawk is building a unified system to manage all the money that is going in and out.

Essentially, companies switching to Payhawk can replace several services they already use and that didn’t interact well with each other. Payhawk lets you issue corporate cards for your employees, manage invoices and track payments from a single interface.

After signing up, customers get their own banking details with a dedicated IBAN. You can connect with your existing bank account, load funds to your Payhawk account and start using it in multiple ways.

Compared to other companies working on similar products, Payhawk gives each customer their own IBAN, which means they can receive third-party payments.

One of the key features of Payhawk is that customers can issue virtual and physical cards for employees with different rules. You can set up a team budget, configure an approval workflow for large transactions and let Payhawk handle receipt collection from those card transactions.

You can upload invoices to manage them through Payhawk. The startup tries to automatically extract data from those invoices for easier reconciliation. Payhawk also lets you reimburse employees. The service acts as a single source of truth for your company’s spending. Finally, you can connect Payhawk with your existing ERP system.

As a software-as-a-service solution, you pay a monthly subscription fee that will vary depending on optional features and the number of active cards. Clients include LuxAir, Lotto24, Viking Life, ATU, Gtmhub, MacPaw and By Miles. Overall, the startup has 200 clients.

The company has been growing nicely as revenue doubled in Q1 2021. It currently accepts clients in the European Union and the U.K. but it already plans to expand beyond those markets. Up next, Payhawk plans to launch credit cards, more currencies and tighter integration with corporate bank accounts.

Powered by WPeMatico

We’ve all heard the phrase “passive income” to describe how people can make money by owning rental properties. Many Americans would love to passively earn money, but the process of becoming a landlord can be intimidating and complicated.

I mean, how many people have looked back and wished they hadn’t sold a property after seeing its value rise years after selling it?

And those who are already landlords can get overwhelmed by the complexities of managing properties.

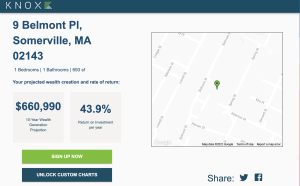

One startup out of Boston, Knox Financial, aims to help people identify and manage residential rentals with its algorithm-based platform, and it’s raised a $10 million Series A to help it further that goal. Boston-based G20 Ventures led the round, which included participation from Greycroft, Pillar VC, 2LVC, and Gaingels.

The investment brings Knox’s total raised since its inception in 2018 to $14.7 million. The company closed on a $3 million seed round in January 2020, led by Greycroft.

Knox co-founder and CEO David Friedman is no stranger to startups. He founded Boston Logic — an integrated marketing platform and online marketing services for real estate offices and agents — in 2004. He sold that company (now under the name Propertybase) to Providence Equity for an undisclosed amount in 2016.

Knox launched its platform in March of 2019, with the goal of offering homeowners who are ready to move “a completely hands-off way” of converting a home they’re moving out of into an investment property. It also claims to help landlords more easily and efficiently manage their rentals.

At the time of its seed round early last year, the company was only operating in the Boston market and had 50 units on its platform. It’s now operating in seven states, has “hundreds” of investment properties on its platform and is overseeing a portfolio of more than $100 million.

So how does it work? Once a property is enrolled on Knox’s “Frictionless Ownership Platform,” the company automates and oversees the property’s finances and taxes, insurance, leasing and legal, tenant and property care, banking and bill pay.

Knox also has developed a rental pricing and projection model for calculating the investment rate of return a property will produce over time.

Image Credits: Knox Financial

“We save investors a lot and almost always make their portfolios more profitable,” Friedman said. “If someone is moving or upsizing, we can turn properties into incredible ROI generators or cash flow.”

The company’s revenue model is simple.

“When a dollar of rent moves through our system, we keep a dime,” Friedman told TechCrunch. “We align our interests with our customers. If there’s no rent coming in, we’re not making money. Or if a tenant doesn’t pay rent, we don’t make money.”

Knox plans to use its new capital to continue expanding geographically and getting the word out to more people.

“We want to become the de facto platform for real estate investment acquisition and ownership,” Friedman said. “And we have to be coast to coast to really do that for everybody. So, we’re still very early in our growth trajectory.”

Bob Hower, co-founder and partner of G20 Ventures, shared that weeks after his college graduation, he had bought a fixer upper with his mother’s help. A week after finishing renovations, he put the house on the market. Over the subsequent five months, he gradually reduced the price as the market softened, and eventually the property sold at a small profit.

“That house now is worth a multiple of what I paid for it,” Hower recalls. “In hindsight, the mistake I made was deciding to sell the house at all.”

That experience helped Hower appreciate what he describes as a “clarity of thinking” in Knox’s business model.

“Had Knox existed decades ago, I’d likely still have that fixer-upper I bought after college,” he said. “Investing platforms such as Betterment have collapsed multiple advising and optimization activities into a simple single-sign-on service, and Knox is the first company to apply this type model to residential real estate investing.”

Powered by WPeMatico

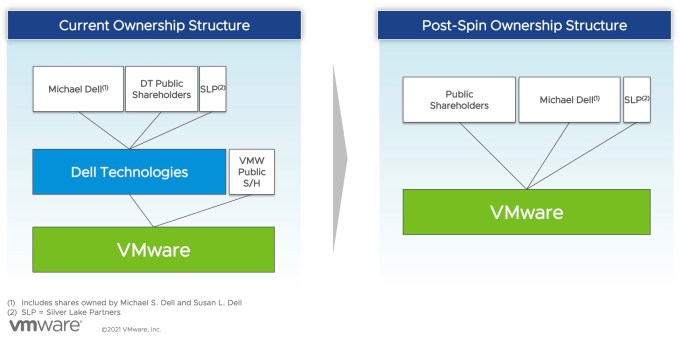

TechCrunch has spilled much digital ink tracking the fate of VMware since it was brought to Dell’s orbit thanks to the latter company’s epic purchase of EMC in 2016 for $58 billion. That transaction saddled the well-known Texas tech company with heavy debts. Because the deal left VMware a public company, albeit one controlled by Dell, how it might be used to pay down some of its parent company’s arrears was a constant question.

Dell made its move earlier this week, agreeing to spin out VMware in exchange for a huge one-time dividend, a five-year commercial partnership agreement, lots of stock for existing Dell shareholders and Michael Dell retaining his role as chairman of its board.

So, where does the deal leave VMware in terms of independence, and in terms of Dell influence? Dell no longer will hold formal control over VMware as part of the deal, though its shareholders will retain a large stake in the virtualization giant. And with Michael Dell staying on VMware’s board, it will retain influence.

Here’s how VMware described it to shareholders in a presentation this week. The graphic shows that under the new agreement, VMware is no longer a subsidiary of Dell and will now be an independent company.

Image Credits: VMware

But with VMware tipped to become independent once again, it could become something of a takeover target. When Dell controlled VMware thanks to majority ownership, a hostile takeover felt out of the question. Now, VMware is a more possible target to the right company with the right offer — provided that the Dell spinout works as planned.

Buying VMware would be an expensive effort, however. It’s worth around $67 billion today. Presuming a large premium would be needed to take this particular technology chess piece off the competitive board, it could cost $100 billion or more to snag VMware from the public markets.

So VMware will soon be more free to pursue a transaction that might be favorable to its shareholders — which will still include every Dell shareholder, because they are receiving stock in VMware as part of its spinout — without worrying about its parent company simply saying no.

Powered by WPeMatico

When Dell announced it was spinning out VMware yesterday, the move itself wasn’t surprising; there had been public speculation for some time. But Dell could have gone a number of ways in this deal, despite its choice to spin VMware out as a separate company with a constituent dividend instead of an outright sale.

The dividend route, which involves a payment to shareholders between $11.5 billion and $12 billion, has the advantage of being tax-free (or at least that’s what Dell hopes as it petitions the IRS). For Dell, which owns 81% of VMware, the dividend translates to somewhere between $9.3 billion and $9.7 billion in cash, which the company plans to use to pay down a portion of the huge debt it still holds from its $58 billion EMC purchase in 2016.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned.

VMware was the crown jewel in that transaction, giving Dell an inroad to the cloud it had lacked prior to the deal. For context, VMware popularized the notion of the virtual machine, a concept that led to the development of cloud computing as we know it today. It has since expanded much more broadly beyond that, giving Dell a solid foothold in cloud native computing.

Dell hopes to have its cake and eat it too with this deal: It generates a large slug of cash to use for personal debt relief while securing a five-year commercial deal that should keep the two companies closely aligned. Dell CEO Michael Dell will remain chairman of the VMware board, which should help smooth the post-spinout relationship.

But could Dell have extracted more cash out of the deal?

Patrick Moorhead, principal analyst at Moor Insights and Strategies, says that beyond the cash transaction, the deal provides a way for the companies to continue working closely together with the least amount of disruption.

“In the end, this move is more about maximizing the Dell and VMware stock price [in a way that] doesn’t impact customers, ISVs or the channel. Wall Street wasn’t valuing the two companies together nearly as [strongly] as I believe it will as separate entities,” Moorhead said.

Powered by WPeMatico