Fifth Wall Ventures

Auto Added by WPeMatico

Auto Added by WPeMatico

Sometimes the smallest innovations can have the biggest impacts on the world’s efforts to stop global climate change. Arguably, one of the biggest contributors in the fight against climate change to date has been the switch to the humble LED light, which has slashed hundreds of millions of tons of carbon dioxide emissions simply by reducing energy consumption in buildings.

And now firms backed by Robert Downey Jr. and Bill Gates are joining investors like Amazon and iPod inventor Tony Fadell to pour money into a company called Turntide Technologies that believes it has the next great innovation in the world’s efforts to slow global climate change — a better electric motor.

It’s not as flashy as an arc reactor, but like light bulbs, motors are a ubiquitous and wholly unglamorous technology that have been operating basically the same way since the nineteenth century. And, like the light bulb, they’re due for an upgrade.

“Turntide’s technology and approach to restoring our planet will directly reduce energy consumption,” said Steve Levin, the co-founder (along with Downey Jr. ) of FootPrint Coalition.

The operation of buildings is responsible for 40% of CO2 emissions worldwide, Turntide noted in a statement. And, according to the U.S. Department of Energy (DOE), one-third of energy used in commercial buildings is wasted. Smart building technology adds an intelligent layer to eliminate this waste and inefficiency by automatically controlling lighting, air conditioning, heating, ventilation and other essential systems and Turntide’s electric motors can add additional savings.

That’s why investors have put over $100 million into Turntide in just the last six months.

PARIS, FRANCE – JUNE 16: Tony Fadell, inventor of the iPod and founder and former CEO of Nest, attends a conference during Viva Technology at Parc des Expositions Porte de Versailles on June 16, 2017 in Paris, France. Viva Technology is a fair that brings together, for the second year, major groups and startups around all the themes of innovation. (Photo by Christophe Morin/IP3/Getty Images)

The company, led by chief executive and chairman Ryan Morris, is commercializing technology that was developed initially at the Illinois Institute of Technology.

Turntide’s basic innovation is a software-controlled motor, or switch reluctance motor, that uses precise pulses of energy instead of a constant flow of electricity. “In a conventional motor you are continuously driving current into the motor whatever speed you want to run it at,” Morris said. “We’re pulsing in precise amounts of current just at the times when you need the torque… It’s software-defined hardware.”

The technology spent 11 years under development, in part because the computing power didn’t exist to make the system work, according to Morris.

Morris was initially part of an investment firm called Meson Capital that acquired the technology back in 2013, and it was another four years of development before the motors were actually able to function in pilots, he said. The company spent the last three years developing the commercialization strategy and proving the value in its initial market — retrofitting the heating ventilation and cooling systems in buildings that are the main factor in the built environment’s 28% contribution to carbon dioxide emissions that are leading to global climate change.

“Our mission is to replace all of the motors in the world,” Morris said.

He estimates that the technology is applicable to 95% of where electric motors are used today, but the initial focus will be on smart buildings because it’s the easiest place to start and can have some of the largest immediate impact on energy usage.

“The carbon impact of what we’re doing is pretty massive,” Morris told me last year. “The average energy reduction [in buildings] has been a 64% reduction. If we can replace all the motors in buildings in the U.S. that’s the carbon equivalent of adding over 300 million tons of carbon sequestration per year.”

That’s why Downey Jr.’s Footprint Coalition, and Bill Gates’ Breakthrough Energy Ventures and the real estate and construction-focused venture firm Fifth Wall Ventures have joined the Amazon Climate Fund, Tony Fadell’s Future Shape, BMW’s iVentures fund and a host of other investors in backing the company.

The company has raised roughly $180 million in financing, including the disclosure today of an $80 million investment round, which closed in October.

Buildings are clearly the current focus for Turntide, which only yesterday announced the acquisition of a small Santa Barbara, California-based building management software developer called Riptide IO. But there’s also an application in another massive industry — electric vehicles.

“Two years from now we will definitely be in electric vehicles,” Morris said.

“Our technology has huge advantages for the electric vehicle industry. There’s no rare earth minerals. Every EV uses rare earth minerals to get better performance of their electric motors,” he continued. “They’re expensive, destructive to mine and China controls 95% of the global supply chain for them. We do not use any exotic materials, rare earth minerals or magnets… We’re replacing that with very advanced software and computation. It’s the first time Moore’s law applies to the motor.”

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, legal, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included in each for audience questions and discussion.

Powered by WPeMatico

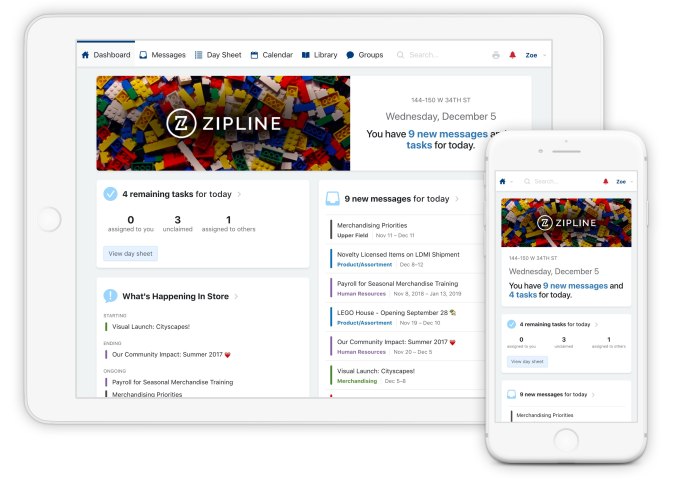

When I first wrote about Retail Zipline in 2019, the startup was focused on building a communication platform that would help corporate decision-makers in retail communicate with individual stores. As you’d probably guess, the startup saw some changes in 2020.

“When COVID first hit, you might think a company that’s primarily focused on retail would be in trouble,” said co-founder and CTO Jeremy Baker. “But it turns out that a product that helps retailers communicate critical information when everything is changing is no longer a nice to have.”

In other words, where Retail Zipline might previously have been used for coordinating sales and promotions, it suddenly became a channel for managing things like health and safety protocols and communicating about furloughs and closures.

Co-founder and CEO Melissa Wong said the platform supports both engagement (a company executives sending a message to retail associates) and execution (translating a broader corporate strategy into an in-store experience). While you might think that execution was the only thing that mattered in the middle of a pandemic, Wong argued that the engagement side was also essential, particularly when employees felt they were putting themselves at risk.

“The engagement part means that we can explain to a retail employee what we’re doing to protect you during this crisis, and your role as part of this company and this brand,” she said.

Image Credits: Retail Zipline

She added that the company has doubled its customer baes during the pandemic and seen revenue increase 2.5x. Retailers using the platform include Sephora, AEO, L.L.Bean, Gap, Hy-Vee, Lush Cosmetics, BevMo, LL Flooring, Cole Haan, The LEGO Group, TOMS and Torrid.

The pandemic also spurred dramatic growth in e-commerce, but Wong (who previously worked on the corporate side of Gap and Old Navy) suggested that this won’t eliminate the need for physical stores. Instead, it just means they’ll have to live up to the long-standing “omni-channel promise,” where they serve as both a store and a distribution center for online orders.

“Retail will become more complex,” she said. “We will enable them to meet those complexities.”

Today, Retail Zipline is announcing that it has raised $30 million in Series B funding. The round was led by real estate-focused firm Fifth Wall, with partner Dan Wenhold joining the board of directors. Emergence Capital, Ridge Ventures, Hillsven Capital, Veeva co-founder Matt Wallach and the Fisher Family Fund also participated.

The company has now raised more than $39 million, according to Crunchbase.

In a blog post, Fifth Wall wrote:

The Fifth Wall network is rich with opportunities for Zipline to explore potential partnerships among our retail-focused partners and portfolio companies. However, we believe retail to be just the beginning for Zipline as we envision the product appealing to many Built World industries. The opportunity for Zipline within real estate could lie with organizations whose HQ office must communicate daily with field operations workers, such as more traditional brokers with a geographic focus (e.g., CBRE, Cushman & Wakefield), leasing agents within multifamily and SFR (e.g., Equity Residential, Greystar), or construction site workers.

Early Stage is the premiere ‘how-to’ event for startup entrepreneurs and investors. You’ll hear first-hand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company-building: Fundraising, recruiting, sales, legal, PR, marketing and brand building. Each session also has audience participation built-in – there’s ample time included in each for audience questions and discussion.

Powered by WPeMatico

Recharge, a startup that tried convincing hotels to let its customers rent their rooms by the hour and even minute, has revamped and rebranded. Now Globe, the company is hoping to convince guests to sign up for short stays instead in people’s homes so that they can kick back between other commitments, and, if the host allows it, to shower and nap.

It’s at once crazy sounding and intriguing, which is perhaps why the popular accelerator program Y Combinator accepted the company into its most recent class of companies. (It shows off its newest batch of startups next week.) YC was famously early to spy the opportunity that Airbnb could chase, after all. The question is whether Globe, which likens itself to an Airbnb for day breaks, will have anywhere near the same appeal.

Its proposition is certainly similar. Home owner or renter wrings out some extra income by renting out all or part of their home, except that unlike with Airbnb, where the minimum stay is at least one night, with Globe, a host rents out his or her space for smaller increments of time.

In a world where the economic divide continues to grow between the haves and have-nots, it’s easy to see the logic in maximizing an underutilized asset — even one’s living room — in order to live more comfortably. It’s especially easy to see the logic in prohibitively expensive cities like San Francisco and New York.

At the same time, letting in a stranger — even a “businessperson” — for a shorter period of time is not going to be a no-brainer for many people who might otherwise rent their home while away for a weekend. And on the other side of the marketplace, getting enough hosts with nice enough places to become hosts is a high hurdle for Globe to surmount. After all, if someone is looking for an alternative to Starbucks for a few hours, and that individual has to take some form of transportation to get to a host’s couch that may or may not be as nice as pictured, that individual may well go the coffee shop route instead. (The company is also up against startups like Breather that offer hourly or daily “space as a service.”)

Founder Manny Bamfo appreciates the challenge, he says. In fact, after running Recharge for a couple of years, he’s gotten well-acquainted with adversity.

Though he says that Recharge wound up seeing $4 million in revenue from its hotel partners, renting rooms to Recharge customers “wasn’t their number one priority, and that made it hard to provide a consistent experience for our customers.” Bamfo suggests their “unionized cleaning labor” wasn’t excited at the prospect of cleaning rooms more frequently than once daily, either, which is partly why Recharge decided to relaunch as a home-sharing service instead.

It’s not just a branding exercise. Along with the new name, Globe is starting from scratch with a new cap table, though Bamfo says Globe opened up a small round for previous investors that was “oversubscribed instantly.” Recharge had raised $10 million from investors. (One of these backers was Binary Capital, which has since evolved into little more than a tangle of lawsuits. Another backer was the real estate-focused firm Fifth Wall Ventures, which maintains a small stake in the new company, says Bamfo.)

In the meantime, Globe is looking to “do a proper seed round at [YC’s] Demo Day.” And it’s busy spreading the word in an effort to build up its burgeoning new marketplace of homes and apartments for rent, and advertising a rate of $50 per hour to people who host their entire home by the hour and $25 per hour to those who share less room.

Globe keeps 20% of the fee.

Globe is also promising $1 million in general liability insurance and, for now, guests who have been verified and vetted by Bamfo himself. It’s not a scalable solution, he acknowledges, but at the moment, he says, it’s all about building the right community, and he sounds optimistic, of course, about its odds.

“People view it like selling a lamp on Craigslist. ‘If it’s not much work, and it’s another form of income, I’ll do it,’” he says. The reality are a “lot of people with great jobs living in cities that are very expensive — people who are cops, who are teachers, who aren’t quite making six figures, and any extra income is a godsend.”

It all begs the question of why, if it’s such a big opportunity, Airbnb isn’t already it. Bamfo’s answer is that it’s basic time management, as well as a different market. “For any company to do this well, it has to be their number one priority.” Besides, he adds, Airbnb is “a travel company. We’re localized, with the ability to charge on a minute-by-minute basis. It’s a huge engineering undertaking and, for now, it’s part of our moat, too.”

Powered by WPeMatico

Brick & Mortar Ventures, a young, San Francisco-based venture firm that’s focused on startups innovating in or around architecture, engineering, construction and facilities management, has closed with $97.2 million in capital commitments.

The fund is one in a sea of debut funds that have swung open their doors in recent years, though it’s also interesting for numerous reasons, beginning with its founder, Darren Bechtel, who knows a thing or two about the building industry. He’s a scion of the family that built the 120-year-old, privately held company Bechtel into one of the largest construction and engineering firms in the world. In fact, his brother, Brendan, who was named CEO in 2016, represents the fifth generation of Bechtels to lead the company. (Their sister, Katherine, is a project controls manager with the powerhouse outfit.)

Brick & Mortar’s investors are just as notable. They aren’t the typical pension funds and university endowments that many VCs try hard to lock down. Instead, they comprise a long list of companies that are part of the “construction value chain” and so have an interest in the latest and greatest developments in their respective industries. Among the firm’s backers, for example, is the special materials maker Ardex; the software giant Autodesk; the building materials company CEMEX; Ferguson Ventures, which is the venture arm of a huge U.S distributor of plumbing supplies; FMI, a management consulting company to the engineering and construction industry; Obayashi, a major Japanese construction company; Sidewalk Labs, which is Alphabet’s urban innovation organization; and United Rentals, one of the world’s largest equipment rental companies.

Brick & Mortar isn’t the first venture firm to focus on the so-called built world. Other firms that focus largely, if not exclusively, around the same themes include Fifth Wall Ventures, Navitas Capital, Corigin Ventures, Camber Creek, MetaProp, Starwood Capital and Tamarisc Ventures.

In fact, Darren Bechtel has ties to and is an individual investor in Fifth Wall, an LA-based firm that stormed onto the scene in 2017 with an equally impressive, and very different, roster of limited partners in the real estate industry, from which it has already amassed more than $700 million in capital commitments across two funds.

As Bechtel told us on a call late last week, he was going to go into business with Fifth Wall’s founders initially, but they wanted to raise a lot of money, and Bechtel was thinking more conservatively — for a reason. “I’d done five deals on AngelList with [Fifth Wall co-founder] Brendan [Wallace] and we’d started putting together a pitch deck, and as we were thinking through ideal fund structure and size, Brendan said $500 million and I said $50 million,” says Bechtel.

Wallace was thinking big, says Bechtel, because “hospitality already had some massive players — Airbnb, WeWork. It was a far more mature landscape, and Brendan thought that if we were going to own a category, we needed the capital to secure a leadership position in the right deals.”

Bechtel thinks Wallace was right, too. He says he just came to realize that construction tech — which is what really interested him — was in its own league, and it was in its infancy. Though the construction software company PlanGrid took off like gangbusters — Bechtel wrote the largest check during the company’s seed round — it wasn’t so long ago that “there were great, billion-dollar ideas being formed but the rounds were small and the valuations were small,” says Bechtel. Because the “investment community didn’t understand what it was looking at, I had concerns about our ability to generate returns if we had too large a fund.”

In the end, the friends and former Stanford MBA classmates decided to split their respective focus on real estate and hospitality (Fifth Wall) and the actual construction of buildings (Brick & Mortar), and things seem to have gone well since. As Fifth Wall has gained traction, so too has Brick & Mortar, which is now a couple of years in the making. Indeed, though Bechtel is announcing the close of Brick & Mortar’s first fund today, he already works with two principals and two associates, and they’ve collectively sourced and funded 16 startups to date with capital they’ve been raising from investors along the way.

One of those checks went to Fieldwire, a maker of field management software for construction teams. They’ve also backed Serious Labs, which trains workers how to use heavy equipment and tools via virtual reality software, and Curbio, a real estate technology startup that orchestrates turnkey renovations for home sellers, then gets paid back once the home is sold.

Brick & Mortar even has an exit already, having helped fund the construction software platform BuildingConnected, which sold last December to Autodesk. (Bechtel’s earlier investment in PlanGrid, which also sold to Autodesk last year, was a personal investment, one of roughly 40 he made before setting out to create a traditional venture firm.)

As for whether Brick & Mortar ever hunts for companies that Bechtel — the firm founded by Darren’s great-great-grandfather — might like to acquire or otherwise partner with, Darren is quick to note that the firm is not an investor in his venture fund or any or its portfolio companies, and he doesn’t have his finger on the pulse of what’s happening there.

“I don’t work at Bechtel or pretend to know what their intentions are, though my brother is CEO, so you could say I know a guy there.”

More, he notes, he doesn’t think it would make sense to fund a company that “a user would want to acquire. If one user buys [a startup’s tools] because they want exclusivity, they’re limiting the exit value of that company.” To underscore his point, he notes that “Bechtel does around $30 billion a year, but the construction market is an $11 trillion market.” In the end, he says, it’s “better to have a preferred relationship. Maybe you get the next year’s model released early; maybe you get custom colors.” But if you’ve developed a winning product, you want to make it accessible to everyone. “You benefit the most by having a technology adopted by the whole industry.”

Above, the Brick & Mortar Ventures team. From left to right: Austin Yount, senior associate; Alice Leung, associate; Curtis Rodgers, principal; Darren Bechtel, general partner; and Kaustubh Pandya, principal.

Powered by WPeMatico

Heyday, a startup aiming to make facials more affordable and personalized, announced today that it has raised $8 million in Series A funding.

I first wrote about the company a year ago, when it raised its $3 million seed round. At the time, co-founder and CEO Adam Ross said his goal was to offer something that sits between expensive, high-end facials and “random little places that are generally cheap in a bad way.” (Heyday pricing starts at $65 for a 30-minute session.)

The company currently operates six brick-and-mortar locations — it started in New York City but recently opened its first Los Angeles store. At the same time, Ross said the website was recently redesigned to offer a more “frictionless” booking experience, and the company also says it can use its “Facial Record” of customers to personalize the treatment and products.

Moving forward, the goal is to both open new physical locations (particularly in LA), but also to continue investing in the technology.

“It’s not an either/or — we see mutual growth and expansion across both channels,” Ross said. “The physical footprint is always going to be a key pillar of our brand strategy, but to win and service customers’ needs in this space, you need to be online.”

Ross also suggested that Heyday is changing the way customers look at facials. For one thing, 30 percent of its customers say they’ve never had a facial before. In addition, Ross said they’re starting to see facials not as an occasional luxury, but as a regular part of their wellness routine: “Most of our clients think about us like an Equinox membership.” And they should, he argued, especially since “your skin is your largest organ.”

The new funding was led by Fifth Wall Ventures, with participation from Lerer Hippeau, Brainchild Funding, M3 Ventures and CircleUp. Fifth Wall partner Kevin Campos is joining Heyday’s board of directors.

“We are in the midst of a significant shift in the retail industry, where marquee brands are moving from digitally native to an omnichannel model,” Campos said in the funding announcement. “We believe the team at Heyday is offering the best experience across both digital and physical touchpoints, and we are thrilled to partner with them to help navigate this complex process and position them for success.”

Powered by WPeMatico

SEC chairman Jay Clayton made clear today that his agency, along with the Commodity Futures Trading Commission, remains acutely concerned about initial coin offerings and crytocurrency trades. In fact, toward that end, they’re now looking for more expansive powers when it comes to protecting customers on cryptocurrency exchanges from fraud.

SEC chairman Jay Clayton made clear today that his agency, along with the Commodity Futures Trading Commission, remains acutely concerned about initial coin offerings and crytocurrency trades. In fact, toward that end, they’re now looking for more expansive powers when it comes to protecting customers on cryptocurrency exchanges from fraud.

“When you have an unregulated… Read More

Powered by WPeMatico

Eden, the office management and tech support platform, has today closed $10 million in Series A funding led by Spectrum 28, with participation from Fifth Wall Ventures, Bessemer Venture Partners, Y Combinator Continuity Fund, Canvas Ventures, Comcast Ventures, Eniac Ventures and other existing investors. Eden started out as a tech support service for both businesses and consumers. The… Read More

Eden, the office management and tech support platform, has today closed $10 million in Series A funding led by Spectrum 28, with participation from Fifth Wall Ventures, Bessemer Venture Partners, Y Combinator Continuity Fund, Canvas Ventures, Comcast Ventures, Eniac Ventures and other existing investors. Eden started out as a tech support service for both businesses and consumers. The… Read More

Powered by WPeMatico