fenwick & west

Auto Added by WPeMatico

Auto Added by WPeMatico

On Tuesday, the Open Cap Table Coalition announced its launch through an inaugural Medium post. The goal of this project is to standardize startup capitalization table data as well as make it far more accessible, transparent and portable.

For those unfamiliar with a cap table, it’s a list of who owns your company’s securities, which includes your company shares, options and more. A clear and simple cap table should quickly indicate who owns what and how much of it they own. For a variety of reasons (sometimes inexperience or bad advice) too many equity holders often find companies’ capitalization information to be opaque and not easily accessible.

This is particularly important for the small percentage of startups that survive in the long term, as growth makes for far more complicated cap tables.

A critical part of good startup hygiene is to always have a clean and updated cap table. Since there is no set format and cap tables are generally not out in the open, they are often siloed rather than collaborative.

Cap tables are near and dear to me as someone who has advised hundreds of startups over the past two decades as the founder of an accelerator, a venture partner and a senior adviser at a government-funded startup launchpad. I have been on the shareholder side of the equation as well and can assure you that pretty much nothing destroys trust between shareholders and startups quicker than poor communication, especially around issues such as the current status of the cap table.

A critical part of good startup hygiene is to always have a clean and updated cap table.

I really like the idea of a cap table being an open corporate record, because the value proposition to the companies is clear. From the time a startup creates a cap table, it’s prone to inaccuracy, friction and mistakes. What this means in practice is that startups may spend money on cap-table-related issues that they should be spending on other things. From a legal process perspective, the law firm that is brought in to help with these issues has to deal with tedious back-end work, so the legal time isn’t high value for either the startup or the law firm.

The value proposition for equity holders is equally clear. All equity holders have a general and legal interest in a company’s capitalization information. They have the right to this information, which they may need for a variety of reasons (including, if things ever get really bad, an aggrieved shareholder action). So making this information clear and easily accessible is a service to equity holders and can also encourage more investment, especially from less experienced investors.

When I imagine what this project could become in the next couple of years, I think back to late 2013, when Y Combinator announced the SAFE (simple agreement for future equity). I think the SAFE is a good analogy here, as no one knew what it was and people wondered if this was a nice-to-have rather than a must-have for startups. But the end result was a dramatic improvement in the early-stage capital-raising process.

While the coalition’s founders include Morgan Stanley’s Shareworks, LTSE Software and Carta, it’s also heavy on Big Law, with Cooley, Goodwin Procter, Wilson Sonsini Goodrich & Rosati, Orrick, Gunderson Dettmer, Latham & Watkins, and Fenwick & West rounding out the group of 10 founding members.

So what’s the real motivation of seven law firms, which together saw revenue of over $10 billion in 2020 to collaborate on an open cap table product for startups? Deal flow.

Big Law has been trying for a couple of decades to build relationships with startups at the stage where it makes no sense for a startup to be dealing with a massive and expensive law firm. Their efforts to build startup programs have often fallen short and received mixed reviews. They have also been far too heavy on the self-serve and too light on the “we’re going to give you our regular Big Law level of services at a small fraction of the costs just in case you make it big and can one day pay our regular fees.” So these firms are trying to separate themselves from the rest of the Big Law pack by building this entrepreneur-friendly tech.

The coalition has already produced its initial version of the open cap table. The real question is whether this is going to be a big deal, as the SAFE was, or whether it’s going to be a vanity solution in search of a real problem. My best guess is that if this coalition gets all the relationships right, doesn’t get greedy and understands that there is a social good component at play here, this could be, reasonably quickly, as impactful as the SAFE was.

Powered by WPeMatico

After WeWork exploded there was — at least supposedly — a change in sentiment among investors and founders alike. Gone were the days of easy nine-figure rounds, expensive growth, negative unit economics and the rest of the excess that Startupland has enjoyed over the past half-decade.

Inside this purported sentiment shift, I presumed, was a decrease in optimism; surely venture capitalists and entrepreneurs would change their behavior inside this new paradigm?

But by some measures, they haven’t. I expected that startups would achieve more conservative proximate valuations in the post-WeWork world, as their leaders would aim to raise a bit less, and a bit more conservatively, and investors would be less starry-eyed in the prices they were willing to pay for startup equity.

That was all wrong, it turns out. A recent report from Fenwick and West, a legal firm that works with technology companies, paints a picture that is the complete opposite of what we might have anticipated.

Perhaps we shouldn’t be surprised; our recent reporting hardly describes a market in slowdown. Boston is having a good start to the year, for example. SaaS is also looking healthy from a venture capital perspective. Cloud stocks are at all-time highs and One Medical is still defying gravity as a public stock. Whatever lesson WeWork was supposed to teach, it doesn’t appear to have made much impact.

Let’s explore the Fenwick data and then ask if we can spot anywhere where the markets are behaving like the chastened children that we were told had taken over.

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

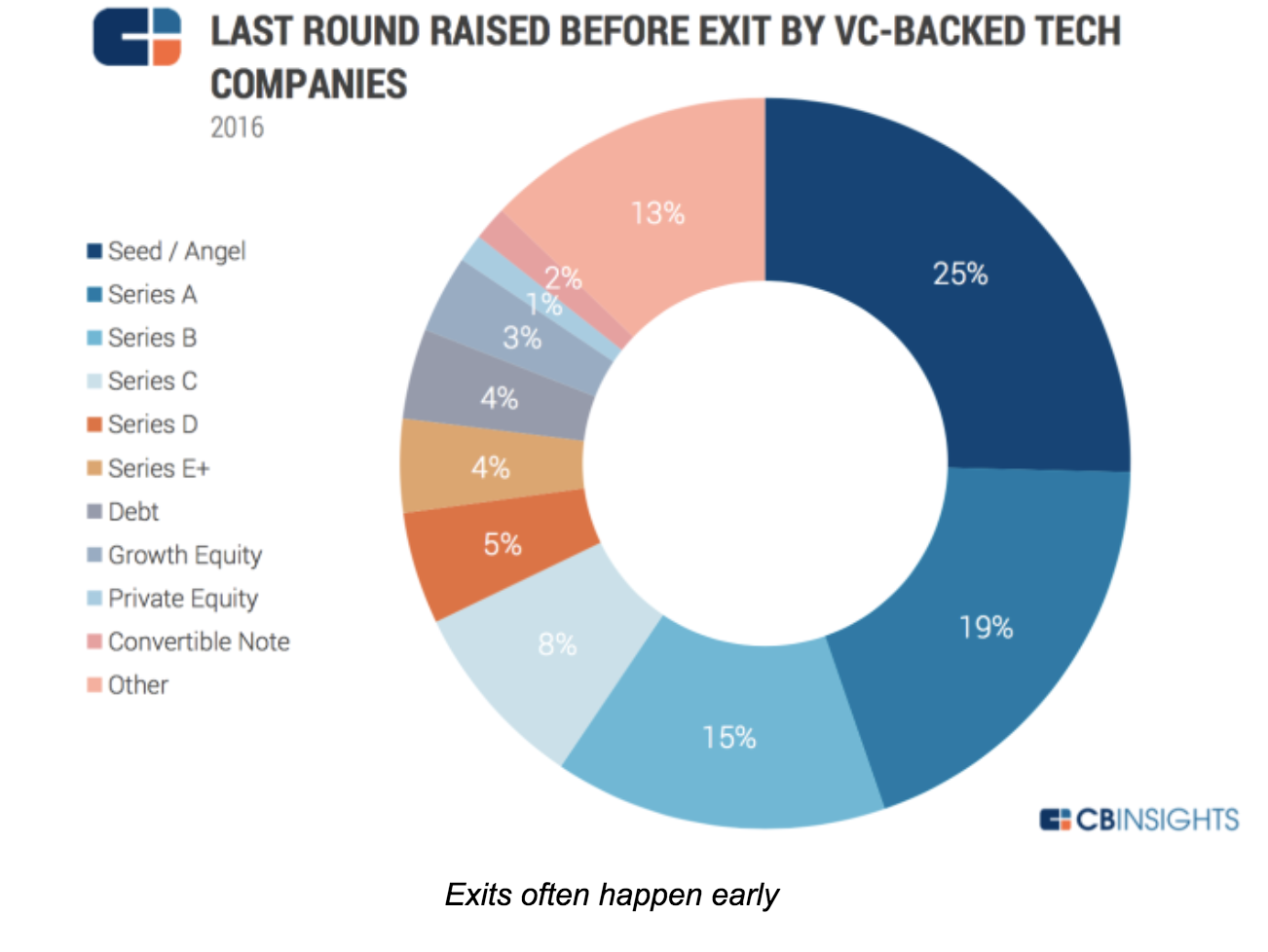

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico

This morning, the law firm Fenwick & West published new findings about all the U.S.-based unicorn financings that took place during the last nine months of 2015. It’s rife with interesting nuggets, but perhaps most fascinating is that in the fourth quarter of last year, half of the 12 rounds it tracked featured valuations in the $1 billion to $1.1 billion range — and with… Read More

This morning, the law firm Fenwick & West published new findings about all the U.S.-based unicorn financings that took place during the last nine months of 2015. It’s rife with interesting nuggets, but perhaps most fascinating is that in the fourth quarter of last year, half of the 12 rounds it tracked featured valuations in the $1 billion to $1.1 billion range — and with… Read More

Powered by WPeMatico