Federal government

Auto Added by WPeMatico

Auto Added by WPeMatico

The increasing regulation of ESG (environmental, social, governance) disclosure reporting may have started in the public markets, but will almost certainly have downstream effects for private market actors — for founders, companies and investors.

Since his confirmation as the chair of the U.S. Securities and Exchange Commission in April, Gary Gensler has made reforming ESG disclosures concerning climate change risk and human capital a top priority. The SEC’s regulatory agenda confirms as much. And Gensler is not alone in his focus on ESG at the federal level.

President Joe Biden issued an executive order encouraging regulators to assess climate-related financial risk. At the end of March, Treasury Secretary Janet Yellen wrote on Twitter that “our future livelihoods … depend on the financial sector to build a more sustainable and resilient economy.” Congress is considering measures that would require increased ESG disclosures, including the Improving Corporate Governance Through Diversity Act, the Diversity and Inclusion Data Accountability and Transparency Act and the Climate Risk Disclosure Act.

This renewed federal focus on ESG issues will bolster the SEC’s effort to create disclosure practices for public companies and mutual funds. Regardless of whether these federal policies around ESG come to pass, they reflect a momentum that will almost certainly impact private markets:

In his confirmation hearing before the Senate in early March, Gensler said, “Markets — and technology — are always changing. Our rules have to change along with them.”

The federal government is moving to increase regulation around ESG disclosure requirements with the goals of establishing greater transparency and metrics for public companies.

The federal government is moving to increase regulation around ESG disclosure requirements with the goals of establishing greater transparency and metrics for public companies. These requirements are a response to the changing markets — demands from consumers, scrutiny from investors and a general insistence for higher corporate standards from society at large.

Private markets aren’t immune to these forces. Already, three-quarters of investors in a 2020 survey said it was very important to measure the success of sustainability initiatives, but they also said there’s been a lack of clarity on how to define and measure outcomes.

To be sure, private markets are not headed toward full-scale adoption of ESG regulations. They will not be subject to the same reporting or disclosures framework as their public counterparts. Not today, and possibly not for some time.

But we may begin to see private investors, funds and companies adapting to get ahead of ESG regulation and position themselves to effectively operate in a new — albeit adjacent — regulatory environment. In their case, the rules may not change — but the game could.

Powered by WPeMatico

Bipartisanship has long been out of fashion, but one common pursuit among Democrats and Republicans in Washington has been placing Big Tech companies under a microscope.

Congressional committees have held scores of hearings, lawsuits have been filed and legislation has been introduced to regulate privacy and data collection. The knock-on effect of these reforms for young companies and their venture investors is unclear. But one aspect of increased antitrust scrutiny — restrictions on acquisitions — would have a significant negative effect on our entrepreneurial ecosystem, and policymakers should approach these changes with caution.

For VC-backed companies, there are effectively three outcomes: standalone company (often via an IPO), merger or acquisition, or bankruptcy. Despite best efforts, company failure is the most common outcome — more than 90% of startups fail. Fortunately, the success stories are often companies with a big impact, like Moderna and Zoom, which helped the world in the pandemic.

Acquisitions contribute to the health of the startup ecosystem, as entrepreneurs who realize liquidity through the sale of their company regularly go on to found innovative new companies and often invest in other startups as angel investors or venture capitalists.

Entrepreneurs are optimists by nature, and so when the company journey begins, there is great hope of one day creating a standalone public company. However, in most cases, an IPO is not possible. The reality is that entrepreneurship is incredibly hard, and the journey from infancy to public company is one that relatively few companies achieve.

Silicon Valley Bank’s 2020 Global Startup Outlook puts it this way: “[T]he fact is most entrepreneurs never expect to reach a public market exit.” Accordingly, 58% of startups expect to be acquired. NVCA-Pitchbook data on acquisitions and IPOs back up the sentiment of founders when it comes to likely exit opportunities. In 2020, there was an approximately 10:1 ratio of acquisitions of VC-backed companies to IPOs, with 1,042 venture-backed companies acquired and 103 entering the public markets.

Some might argue that acquisitions are more dominant today because of the anti-competitive motivations of current tech incumbents. But as Patricia Nakache of Trinity Ventures said in testimony before the Senate Judiciary Committee: “[Acquisitions have] been commonplace in the U.S. since before the dawn of the modern venture capital industry.” In fact, today we are witnessing fewer acquisitions relative to IPOs than in years past, as the average acquisition-to-IPO ratio since 2004 is approximately 15:1. This is happening against a backdrop of challenges in taking small-cap companies public that has reduced the number of companies in the public markets today.

Acquisitions contribute to the health of the startup ecosystem, as entrepreneurs who realize liquidity through the sale of their company regularly go on to found innovative new companies and often invest in other startups as angel investors or venture capitalists.

Furthermore, acquisitions help power the returns of VC funds, thereby allowing VCs to raise new funds and invest in the next generation of entrepreneurs. This “recycling effect” is one of the key drivers of dynamism in our economy and should not be slowed down.

Despite the importance of acquisitions, antitrust reform has included significant changes to how acquisitions are assessed by the federal government. The two most prominent examples in this space are Sen. Amy Klobuchar’s Competition and Antitrust Law Enforcement Reform Act (CALERA) and Sen. Josh Hawley’s Trust-Busting for the Twenty-First Century Act.

These bills are likely a reaction to findings that incumbents have acted like Pac-Man, gobbling up would-be competitors before they become a competitive problem. But both proposals would ultimately harm startup activity and competition rather than propel it.

A common thread between these proposals is to restrict acquisitions by companies valued at more than $100 billion. Hawley’s bill would impose an outright ban on acquisitions by companies of that market cap that “lessen competition in any way.”

Klobuchar’s bill would shift the burden of proof to parties to an acquisition, a major change because the U.S. government bears the burden currently. This means if the government challenges an acquisition in federal court, the parties to the acquisition must demonstrate it does not “create an appreciable risk of materially lessening competition.” If that standard is not met, the acquisition could be blocked.

Both proposals have negative ramifications for venture-backed companies.

First, consider the scope of the proposals: A $100 billion company is indeed a large one, but setting the threshold there captures far more than the large tech companies that have been hauled before Congress for antitrust hearings. Globally, about 150 companies are valued at $100 billion or more, and the U.S. is home to more than 80 of those companies. That exposes acquirers as wide-ranging as Estee Lauder, John Deere, Starbucks and Thermo Fisher Scientific. If you are struggling to recall those companies being under the antitrust spotlight, then you are not alone.

Second, the legal standards imposed by these new bills are daunting. Klobuchar’s proposal leaves startups scratching their heads on where the line is on which acquisitions are tolerated, while Hawley’s bill throws up a misguided red light for vast amounts of acquisitions. These two standards are particularly vexing since acquirers are generally looking for acquirees that complement their existing business. In addition, many of the most acquisitive companies are multifaceted ones that presumably compete with an array of other companies in some way.

Ultimately, the bills from Klobuchar and Hawley would disrupt an important part of our nation’s startup ecosystem. Acquisitions act like grease to help keep the wheels moving by injecting liquidity into the system so participants can move on to create new and hopefully better companies for our country. Those wheels should not be slowed down when the country needs all the entrepreneurship it can muster.

Powered by WPeMatico

As President-elect Joe Biden readies his transition team and sets the agenda for his first 100 days in office, startups can expect to see some movement on long-stalled infrastructure initiatives that could mean big boosts to their business.

Infrastructure is high on the list of priorities of the incoming Biden Administration as the former vice president hopes to make good on his campaign promise to “build back better.”

American infrastructure has been crumbling for decades without significant investment from the federal government, and much of what will be replaced will also be upgraded with new technology, according to people familiar with the Biden plan.

That means tech companies focused on next-generation telecommunications and utility infrastructure, transportation, housing and construction tech around energy efficiency could see new dollars pour in over the next four years.

“Infrastructure and build out of the clean energy economy … doesn’t necessarily mean large wind or large solar projects. It could mean advanced metering … it can be new engine technologies,” said Dan Goldman, a managing partner at Clean Energy Ventures. “We think that that can be a huge opportunity for job creation … not only putting people back to work but putting people back to work in high quality jobs.”

And there’s a willingness to encourage these infrastructure projects in less partisan ways in states like Massachusetts, Virginia and Florida, which are actively building out electric vehicle infrastructure and renewable energy projects, Goldman said.

While the federal government will ultimately be distributing the cash, startups can expect to see the spending actually come from municipalities and state governments, which often have a better understanding of local needs and where the money should go.

The electrification of everything — a component of any zero-carbon movement — requires significant upgrades to existing power infrastructure. That means everything from systems management technologies to distribution facilities to ways to store power that can be moved on to the grid.

“Without that infrastructure investment it gets quite challenging,” said Abe Yokell, a co-founder and managing partner of Congruent Ventures.

He pointed to large-scale energy storage technologies as one solution, but management systems for utilities will be another area of interest.

Those infrastructure initiatives will likely mean good things for battery companies like Form Energy, which signed its first major contract with Great River Energy earlier this year; or Antora and Malta, which store energy as heat; or Quidnet, which has a pumped hydroelectric play for large-scale energy storage by pumping water into the gaps between rocks underground that creates pressure and can force water back up through a generator.

Other large-scale energy storage companies working on developing and installing batteries could benefit as well. That means good things for Tesla, which has a few major battery installs under its belt, and Fluence, which manages and operates big install projects.

Natel Energy, another startup working on energy storage (and generation) using hydropower, could also find its technology in the mix, according to company founder, Gia Schneider.

Schneider sees three potential pitches for her company’s technologies. “Climate change is water change,” she said. “We have a bucket in energy, a bucket of stuff in environmental and a bucket of stuff in working lands.”

Powered by WPeMatico

This week saw protests spread across the world sparked by the murder of George Floyd, an unarmed Black man, killed by a white police officer in Minneapolis last month.

The U.S. hasn’t seen protests like this in a generation, with millions taking to the streets each day to lend their voice and support. But they were met with heavily armored police, drones watching from above, and “covert” surveillance by the federal government.

That’s exactly why cybersecurity and privacy is more important than ever, not least to protect law-abiding protesters demonstrating against police brutality and institutionalized, systemic racism. It’s also prompted those working in cybersecurity — many of which are former law enforcement themselves — to check their own privilege and confront the racism from within their ranks and lend their knowledge to their fellow citizens.

The Justice Department has granted the Drug Enforcement Administration, typically tasked with enforcing federal drug-related laws, the authority to conduct “covert surveillance” on protesters across the U.S., effectively turning the civilian law enforcement division into a domestic intelligence agency.

The DEA is one of the most tech-savvy government agencies in the federal government, with access to “stingray” cell site simulators to track and locate phones, a secret program that allows the agency access to billions of domestic phone records, and facial recognition technology.

Lawmakers decried the Justice Department’s move to allow the DEA to spy on protesters, calling on the government to “immediately rescind” the order, describing it as “antithetical” to Americans’ right to peacefully assembly.

Powered by WPeMatico

There comes a time for many startup companies where they either realize they need to do a nationwide rollout, or they need to actively target buyers in the middle of the country. If you are a startup on either the East or the West Coasts, it’s worth thinking about how this market might present its own set of unique challenges, and how you plan to overcome them.

There are a lot of misconceptions about what some people call “flyover country,” and as a San Francisco native who spent two decades in New York, Washington DC, and Boston before moving to Pittsburgh, I can assure you they are almost all wrong. Without getting into specifics, the reality of “middle America” is that it’s the same as anywhere else.

Income, education, world view, and waistlines are all varied. It’s pretty accurate that San Francisco possesses a culture obsessed with fitness and entrepreneurship, but California isn’t necessarily all like that, and if you think it is, I encourage you to go to Bakersfield, the Central Valley, or Eureka sometime.

In addition, just because the stereotypes are wrong doesn’t mean there’s nothing different about doing business here. As you think about how to conduct your rollout, here are some things you should consider:

As with any market, research is key since it informs every other aspect of the rollout. Start by looking into who your competition is.

Since there are fewer VC-backed startups in middle America, and smaller companies tend to get less press, the research may be harder. However, there are some major universities that are actively putting money into their own Entrepreneurship programs and those spinoffs often do very well.

Powered by WPeMatico

A lot of students attend public universities to lessen the financial burden of higher education. At last tally, tuition and fees at American public colleges and universities averaged around $6,800 a year, per the federal government. That’s far below the $32,600 mean price tag for private, nonprofit institutions.

Yet when it comes to public universities, the old adage “you get what you pay for” clearly does not apply. Leading public research universities in particular have a track record of turning out enviably knowledgeable and successful graduates. That includes a whole lot of funded startup founders.

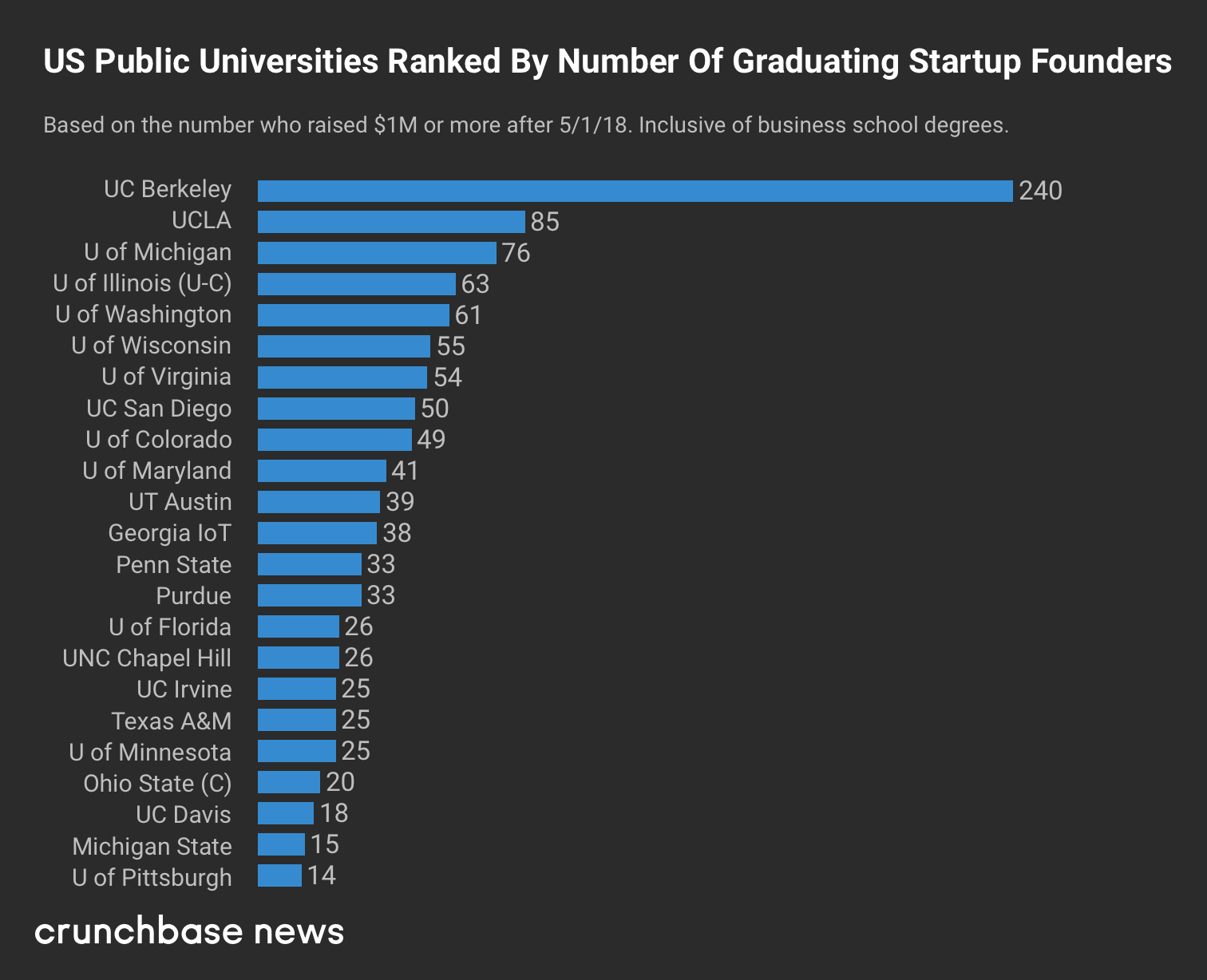

And that leads us to our latest ranking. At Crunchbase News, we’ve been tracking the intersection of alumni affiliation and startup funding for the past few years. In a story published earlier this week, we looked at which U.S. universities graduated the most founders of startups that raised $1 million or more in roughly the past year.

For today’s follow-up, we’re focusing exclusively on public universities. Starting with a list of top-ranking research universities, we looked to see which have graduated the highest number of funded founders.

For the most part, we used the same criteria as the public-and-private list, focusing on startups that raised $1 million or more after May, 2018. The public list, however, does not separate out business school grads.

Without further ado, here’s the list:

Looking at the list above, a few things stand out. First, our top ranker, University of California at Berkeley, is multiples above the rest of the field when it comes to graduating funded founders.

Berkeley is a school that’s generally hard to get into, prominent in STEM and located in the VC-rich San Francisco Bay Area. So seeing it top the list isn’t necessarily surprising. However, the magnitude of its lead — with nearly three times the funded founders of runner-up UCLA — does warrant attention.

Big Midwestern schools also did well, with University of Michigan and University of Illinois, Urbana-Champaign nabbing the third and fourth spots.

More broadly, the list includes schools from all U.S. regions, including the East Coast, West Coast, South, Midwest and Southwest. So no particular region has a lock on graduating funded entrepreneurs. That’s also not surprising. But it’s good to have some more numbers to back up that notion.

Powered by WPeMatico