Extra Crunch

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to our $100 million annual recurring revenue (ARR) series, in which we take irregular looks at companies that have reached material scale while still private. The goal of our project is simple: uncovering companies of real worth beyond how they are valued by private investors.

The Exchange is a daily look at startups and the private markets for Extra Crunch subscribers; use code EXCHANGE to get full access and take 25% off your subscription.

It’s all well and good to get a $1 billion valuation, call yourself a unicorn and march around like you invented the internet. But reaching material revenue scale means that, unlike some highly valued companies, you’re actually hard to kill. (And more valuable, and more likely to go public, we reckon.)

Before we dive into today’s new companies, keep in mind that we’ve expanded the type of company that can make it into the $100M ARR club to include companies that reach a $100 million annual run rate pace. Why? Because we don’t only want to collect SaaS companies, and if we could go back in time we’d probably draw a different box around the companies we are tracking.

Before we dive into today’s new companies, keep in mind that we’ve expanded the type of company that can make it into the $100M ARR club to include companies that reach a $100 million annual run rate pace. Why? Because we don’t only want to collect SaaS companies, and if we could go back in time we’d probably draw a different box around the companies we are tracking.

If you need to catch up, you can find the two most recent entries in the series here and here. For everyone who’s current, today we are adding Snow Software, A Cloud Guru, Zeta Global and Upgrade to the club. Let’s go!

Just this week, Snow Software announced that it has crossed the $100 million ARR mark, according to a release shared with TechCrunch. The Swedish software asset management company has raised a few private rounds, including a $120 million private equity round in 2017. But, unlike many American companies that make this list, we don’t have a historical record of needing extensive private capital to scale.

Powered by WPeMatico

It’s the summer of 1858. London. The River Thames is overflowing with the smell of human and industrial waste. The exceptionally hot summer months have exacerbated the problem. But this did not just happen overnight. Failure to upkeep an aging sewer system and a growing population that used it contributed to a powder keg of effluent, bringing about cholera outbreaks and shrouding the city in a smell that would not go away.

To this day, Londoners still speak of the Great Stink. Recurring cholera infections led to the dawn of the field of epidemiology, a subject in which we have all recently become amateur enthusiasts.

Fast forward to 2020 and you’ll see that modern software pipelines face a similar “Great Stink” due, in no small part, to the vast adoption of continuous integration (CI), the practice of merging all developers’ working copies into a shared mainline several times a day, and continuous delivery (CD), the ability to get changes of all types — including new features, configuration changes, bug fixes and experiments — into production, or into the hands of users, safely and quickly in a sustainable way.

While contemporary software failures won’t spread disease or emit the rancid smells of the past, they certainly reek of devastation, rendering billions of dollars lost and millions of developer hours wasted each year.

This kind of waste is antithetical to the intent of CI/CD. Everyone is employing CI/CD to accelerate software delivery; yet the ever-growing backlog of intermittent and sporadic test failures is doing the exact opposite. It’s become a growing sludge that is constantly being fed with failures faster than can be resolved. This backlog must be cleared to get CI/CD pipelines back to their full capabilities.

What value is there in a system that, in an effort to accelerate software delivery, knowingly leaves a backlog of bugs that does the exact opposite? We did not arrive at these practices by accident, and its practitioners are neither lazy nor incompetent so; how did we get here and what can we do to temper modern software development’s Great Stink?

Powered by WPeMatico

Most people would agree that a chief revenue officer is a pretty significant hire, but I have yet to meet mine in person. Right now, our only face-to-face interaction is over video. In fact, that’s how our relationship began — like many business leaders during this pandemic, I had to hire Todd through a series of video calls.

The pandemic has caused me to question and reevaluate many of my own assumptions. This not only led me to hire our CRO remotely, but it is ultimately why I also decided to allow employees to work from home until 2021.

While it’s tempting to call this a pivot, those who have worked with me would probably describe it more accurately as a flip-flop. I used to believe that you could build an in-person culture or a remote work culture, but that a hybrid of the two was destined to fail.

The realities of COVID-19 have not just changed my outlook, but transformed the way I think about how work should get done —and how leaders need to show up for their team, even if they can’t “show up” in any physical sense.

Before the pandemic, the debate over remote work revolved around its perceived impact on productivity, collaboration, employee engagement and culture.

Powered by WPeMatico

The first wave of AR startups offering smart glasses is now over, with a few exceptions.

Google acquired North this week for an undisclosed sum. The Canadian company had raised nearly $200 million, but the release of its Focals 2.0 smart glasses has been cancelled, a bittersweet end for its soft landing.

Many AR startups before North made huge promises and raised huge amounts of capital before flaring out in a similarly dramatic fashion.

The technology was almost there in a lot of cases, but the real issue was that the stakes to beat the major players to market were so high that many entrants pushed out boring, general consumer products. In a race to be everything for everybody, the industry relied on nascent developer platforms to do the dirty work of building their early use cases, which contributed heavily to nonexistent user adoption.

A key error of this batch was thinking that an AR glasses company was hardware-first, when the reality is that the missing value is almost entirely centered on missing first-party software experiences. To succeed, the next generation of consumer AR glasses will have to nail this.

Image Credits: ODG

Powered by WPeMatico

Last week, we discussed the possibility that Dell could be exploring a sale of VMware as a way to deal with its hefty debt load, a weight that continues to linger since its $67 billion acquisition of EMC in 2016. VMware was the most valuable asset in the EMC family of companies, and it remains central to Dell’s hybrid cloud strategy today.

As CNBC pointed out last week, VMware is a far more valuable company than Dell itself, with a market cap of almost $62 billion. Dell, on the other hand, has a market cap of around $39 billion.

How is Dell, which owns 81% of VMware, worth less than the company it controls? We believe it’s related to that debt, and if we’re right, Dell could unlock lots of its own value by reducing its indebtedness. In that light, the sale, partial or otherwise, of VMware starts to look like a no-brainer from a financial perspective.

At the end of its most recent quarter, Dell had $8.4 billion in short-term debt and long-term debts totaling $48.4 billion. That’s a lot, but Dell has the ability to pay down a significant portion of that by leveraging the value locked inside its stake in VMware.

Nothing is ever as simple as it seems. As Holger Mueller from Constellation Research pointed out in our article last week, VMware is the one piece of the Dell family that is really continuing to innovate. Meanwhile, Dell and EMC are stuck in hardware hell at a time when companies are moving faster than ever expected to the cloud due to the pandemic.

Dell is essentially being handicapped by a core business that involves selling computers, storage and the like to in-house data centers. While it’s also looking to modernize that approach by trying to be the hybrid link between on-premise and the cloud, the economy is also working against it. The pandemic has made the difficult prospect of large enterprise selling even more challenging without large conferences, golf outings and business lunches to grease the skids of commerce.

Powered by WPeMatico

While many investors say sheltering in place has broadened their appetite for funding companies located outside major hubs, one firm is doubling down on backing startups in America’s heartland.

Launched in 2016 by Brett Brohl, The Syndicate Fund rebranded to Bread & Butter Ventures earlier this month (a reference to one of Minnesota’s many nicknames). Along with the rebrand, longtime Google executive and Revolution partner Mary Grove joined the team as a general partner and Stephanie Rich came aboard as head of platform.

The growth of the Twin Cities’ startup ecosystem is precisely why The Syndicate Fund rebranded. The firm, which has $10 million in assets under management, will invest in three of Minneapolis’ biggest strengths: agriculture and food, health care and enterprise software.

Agtech interest spans the entire spectrum from farming to restaurants and grocery stores. The firm is also interested in the “messy middle” of supply chain and logistics around food, said Brohl and is interested in a mix of software, hardware and biosciences. Within health care, the firm evaluates solutions focused on prevention versus treatment, female health startups working on maternal health and fertility and software focused on the aging population and millennials.

It’s also looking at enterprise software that can serve large businesses and scale efficiently.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

“Dear Sophie” columns are accessible for Extra Crunch subscribers; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie:

What is going on with recent USCIS furloughs and Trump’s H-1B ban?

I handle recruitment for several tech companies. Is immigration happening? Who can I hire?

—Frustrated in Fremont

Dear Fremont:

Immigration is still possible and I will explain how below. The administration continues to miss the mark with immigration policy. Trump’s U.S. unemployment “solution” of cutting off the stream of global talent to the U.S. is short-sighted. The administration is shooting America in the foot by walling off the promise of post-COVID economic revitalization and job-creation for Americans through the talent of immigrant entrepreneurs, investors and talent.

USCIS just provided a 30-day furlough notice to more than 70% of its employees. Reporters have been reaching out to me every day requesting stories of affected immigrants and HR professionals; please sign up to share your immigration story with journalists.

Powered by WPeMatico

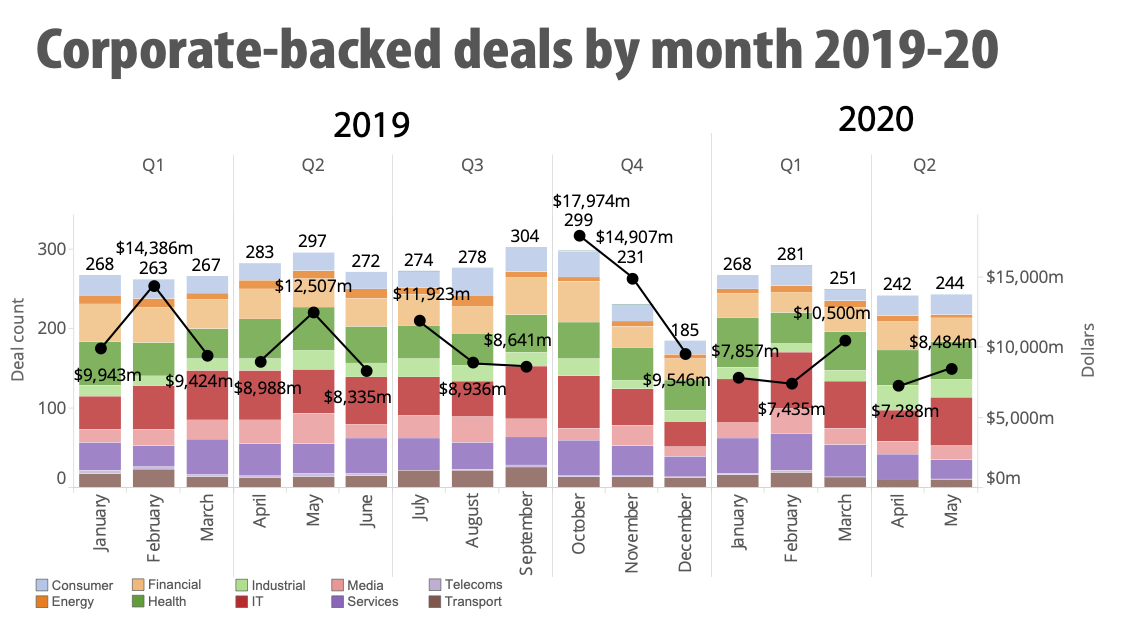

When the going gets tough, it’s common for some corporate VCs to head for the hills.

Today, it’s a narrative that’s emerging again amid the COVID-19 crisis. Global corporate venture deals fell from a total of 580 in April/May of 2019 to 486 in the same period this year, according to Global Corporate Venturing.

However, institutional VC deals are also headed for a decline, with PitchBook anticipating a drop in transaction volume over the next several quarters, as well as a downturn in valuations.

Image Credits: Global Corporate Venturing

It remains to be seen how it will play out this time, but I believe corporate venture capital (CVC) will not only stick around, but also be a vital part of the innovation ecosystem going forward.

I know that Merck Global Health Innovation Fund (MGHIF) remains fully committed to “doing” venture. Now, more than ever, health innovation is vital. Second, we understand that many of today’s most successful companies were funded in times of uncertainty. In fact, to put our money where our mouth is, we’ve recently completed two spinouts, three follow-on investments, and two new deals in 2020 — all since COVID hit. We intend to increase that pace going forward in 2020 and beyond.

It hasn’t been easy. It’s hard to do venture when you can’t venture out into the world, meet founders and do diligence the way we did in the past. But it is possible, if you do some innovating of your own and set up a smoothly functioning system to do CVC virtually.

Here’s how we’ve done it.

Powered by WPeMatico

In the two years since Jeff Semenchuk took the reins in the newly created position of chief innovation officer for Blue Shield of California, the nonprofit health insurer with $20 billion in revenues has stepped up its investments in startup companies.

As one of California’s largest insurance providers with more than four million members, Blue Shield plays an outsized role in technology adoption among physicians, hospital networks and patients. With that in mind, and with the acceleration of entrepreneurial activity around the multitrillion health care market, Semenchuk was brought on board after serving as chief executive of Yaro (now Virgin Plus) and CIO of Hyatt Hotels and co-founder of Citi Ventures.

Semenchuk said he sees Blue Shield as working to create a new health care system: “It’s not to perpetuate the health care system we have today.” Increasingly, startups have a role to play in that revisioning of health care services in America, according to Semenchuk.

“What I would say has happened over the last two years is that we have really focused on transformational innovation,” he added.

Investing in those transformational technologies involves taking cash directly from Blue Shield’s balance sheet for investments. The company doesn’t operate a corporate venture capital fund in the traditional sense, instead making strategic investments under the auspices of Semenchuk or Chief Financial Officer Sandra Clarke.*

Powered by WPeMatico

If you have bought a house in the last decade, you likely started the process online. Perhaps you browsed for your future dream home on a website like Zillow or Realtor, and you may have been surprised by how quickly things moved from seeing a property to making an offer.

When you reached the closing stage, however, things slowed to a crawl. Some of those roadblocks were anticipated, such as the process of getting a mortgage, but one likely wasn’t: the tedious and time-consuming process of obtaining title insurance — that is, insurance that protects your claim to home ownership should any claims arise against it after sale.

For a product that is all but required to purchase a home, title insurance isn’t something many people know about until they have to pay for it and then wait up to two months to get.

Now, finally, a handful of startups are taking on the title insurance industry, hoping to make the process of buying a policy easier, cheaper and more transparent. These startups, including Spruce, States Title, JetClosing, Qualia, Modus and Endpoint, enable part or all of the title insurance buying process. Whether these startups can finally topple the title insurance monopoly remains to be seen, but they are already causing cracks in the system.

To that end, we’ve outlined what’s broken about today’s title industry; recent developments in technology and government that are priming the industry for change; and a synthesis of some key trends we’ve observed in the space, as entrepreneurs begin to capitalize on a tipping point in a century-old, $14 billion business.

To understand how startups are beginning to challenge title insurance incumbents, we need to first understand what title insurance is and what title companies do.

Title insurance is unique from other types of insurance, which require ongoing payments and protect a buyer against future incidents. Instead, title insurance is a one-time payment that protects a buyer from what has already happened — namely errors in the public record, liens against the property, claims of inheritance and fraud. When you buy a home, title insurance companies research your property’s history, contained in public archives, to make sure no such claims are attached to it, then correct any issues before granting a title insurance policy.

Powered by WPeMatico