Extra Crunch

Auto Added by WPeMatico

Auto Added by WPeMatico

With more than 1,200 employees distributed across over 65 countries and a valuation of nearly $3 billion, GitLab is one of the world’s most successful fully remote startups.

Describing it as a textbook example of a remote company would be redundant, because the company actually wrote a textbook about it.

I recently had a chance to talk to GitLab’s head of Remote, Darren Murph, who filled me in on how they get stuff done, his advice for all the companies that had to suddenly shift to remote work and why GitLab gets rid of all its Slack messages after 90 days. (Fun fact: Darren wrote for TechCrunch’s corporate cousin Engadget in a past life, where he earned a Guinness World Record for writing an absolutely ridiculous number of posts.)

Darren and I chatted for quite a while, so I’ve split the transcript into two parts for easier reading. Part two coming tomorrow!

TechCrunch: So your official title is “Head of Remote.” What does that entail?

Darren Murph: It’s three things.

It’s telling our remote story to the world, it’s making sure that people who join the company acclimate to working in an all-remote setting and it’s building out the educational piece. The “all-remote” section of our handbook has dozens of guides on how we do everything remotely, from async, to meetings, to hiring and compensation, and I’m the author of all of that.

We do that to better the world; we put it all out there, it’s open source. We want other companies to read it, implement it and use it. We never saw COVID coming, but I kind of knew that down the road [this handbook] would be necessary. Thankfully, I started working on it in advance. Now that the world needs it… it’s been crazy. We packaged up our best thinking in that remote playbook, and it’s just been off the charts with companies downloading it. It’s been wild.

Why did GitLab go remote in the first place?

It was remote by default. The first three people to join the company were in three different countries… so the only way to do it was through the internet.

The one brief moment in time where there was a co-located wrinkle to the company… they’d moved to California for Y Combinator. I think there was like nine or 10 people at the time. Of course, coming out of Y Combinator, at the time, you just get an office — it’s just what you did.

I think that lasted about three days. Then people just stopped showing up.

[Laughs]

But work kept getting done! Because even in the office they were just communicating on… whatever it was at the time. It probably wasn’t Slack, I don’t think Slack existed.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

“Dear Sophie” columns are accessible for Extra Crunch subscribers; use promo code ALCORN to purchase a one or two-year subscription for 50% off.

Dear Sophie:

Fallout from COVID-19 is forcing our startup to downsize. What legal requirements do we need to consider if we’re laying off foreign-born employees or scaling back their hours?

— HR Manager in San Mateo

Dear HR Manager:

Thank you for your question; a lot of people are going through the same thing. Keep in mind that terminating an employee that your company sponsored for a visa or green card can have ramifications for future hiring.

Powered by WPeMatico

One vote.

That’s all it needed for a bipartisan Senate amendment to pass that would have stopped federal authorities from further accessing millions of Americans’ browsing records. But it didn’t. One Republican was in quarantine, another was AWOL. Two Democratic senators — including former presidential hopeful Bernie Sanders — were nowhere to be seen and neither returned a request for comment.

It was one of several amendments offered up in the effort to reform and reauthorize the Foreign Intelligence Surveillance Act, the basis of U.S. spying laws. The law, signed in 1978, put restrictions on who intelligence agencies could target with their vast listening and collection stations. But after the Edward Snowden revelations in 2013, lawmakers champed at the bit to change the system to better protect Americans, who are largely protected from the spies within its borders.

One privacy-focused amendment, brought by Sens. Mike Lee and Patrick Leahy, passed — permits for more independent oversight to the secretive and typically one-sided Washington, D.C. court that authorizes government surveillance programs, the Foreign Intelligence Surveillance Court. That amendment all but guarantees the bill will bounce back to the House for further scrutiny.

Here’s more from the week.

A feature-length profile in Wired magazine looks at the life of Marcus Hutchins, one of the heroes who helped stop the world’s biggest cyberattack three years to the day.

The profile — a 14,000-word cover story — examines his part in halting the spread of the global WannaCry ransomware attack and how his early days led him into a criminal world that prompted him to plead guilty to felony hacking charges. Thanks in part to his efforts in saving the internet, he was sentenced to time served and walked free.

Powered by WPeMatico

The COVID-19 pandemic has wiped out the spring seasons for professional sports and associated revenue for TV networks, but esports is filling part of that void.

Gaming companies behind titles licensed by each major league are the winners in this unexpected shift; Electronic Arts (EA) is first among them with FIFA, Madden NFL, NBA Live and NHL in its EA Sports portfolio and more than 100 esports events planned for 2020. The way EA, networks and sports leagues are responding to production challenges in this crisis will reshape the esports market going forward.

Millions of people sheltering in place has created a breakout opportunity for esports broadcasting:

In late March, 900,000 viewers tuned into Fox Sports for Nascar’s iRacing series, with 1.1 million watching in early April; the network has also broadcast Madden NFL tournaments with NFL commentators and athletes. ESPN is televising NBA players facing off against each other in NBA 2K (by Take-Two Interactive) and pro drivers (and other pro athletes like Manchester City striker Sergio Aguero) are racing each other in Codemasters’ F1 2019 game. ESPN has broadcast competitive play of non-sports games with League of Legends (by Riot Games) and Apex Legends (by EA) tournaments.

To be clear, ratings for these events have varied widely, but networks and game companies are rethinking how esports is broadcast, which will advance its pop-culture appeal.

Esports is a massively popular activity with its own large piece of turf in pop culture, but it hasn’t secured a central role. Research firm Newzoo pegs the global audience of “esports enthusiasts” at 223 million. But unlike soccer and basketball, esports is siloed because it caters to viewers who are generally avid gamers. The action is extremely fast, so commentary by a streamer rarely helps outsiders understand what is going on enough to become engaged.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re digging into SoftBank’s latest earnings slides. Not only do they contain a wealth of updates and other useful information, but some of them are gosh-darn-freaking hilarious. We all deserve a bit of levity after the last few months.

The visual elements we quote below come from SoftBank’s reporting of its own results from its fiscal year ending March 31, 2020. Much of the deck is made up of financial reporting tables and other bits of stuff you don’t want to read. We’ve cut all that out and left the fun parts.

Before we dive in, please note that we are largely giggling at some slide design choices and only somewhat at the results themselves. We are certainly not making fun of people who’ve been impacted by layoffs and other such things that these slides’ results encompass.

But we are going to have some fun with how SoftBank describes how it views the world, because how can we not? Let’s begin.

TechCrunch has a number of folks parsing SoftBank’s deck this morning, looking to do serious work. That’s not our goal. Sure, this post will tell you things like the fact that there are 88 companies in the Vision Fund portfolio, and that when it comes to unrealized gains and losses, the portfolio has seen $13.4 billion in gains and $14.2 billion in losses. $4.9 billion of gains have been realized, mind you, while just $200 million of losses have had the same honor.

And this post will tell you that the “net blended [internal rate of return] for SoftBank Vision Fund investors is -1%.”

Hell, you probably also want to know that Uber was detailed as Vision Fund’s worst-performing public company, generating a $1.46 billion loss for the group. In contrast, Guardant Health is good for a $1.67 billion gain, while 2019 IPO Slack has been good for $605 million in profits. Those were the two best companies in the Vision Fund’s public portfolio.

But what you really want is the good stuff. So, shared by slide number, here you go:

Powered by WPeMatico

E-commerce is taking off faster than ever. In the last couple of weeks, my Twitter timeline has been filled with operators gushing about how the weekends seem like Black Friday, even for non-essential commodities. Change is already here.

As we help thousands of businesses to move online, our platform is now handling Black Friday level traffic every day!

It won’t be long before traffic has doubled or more.

Our merchants aren’t stopping, neither are we. We need

to scale our platform.https://t.co/e2JeyjcEeC pic.twitter.com/6lqSrNUCte

— Jean-Michel Lemieux (@jmwind) April 16, 2020

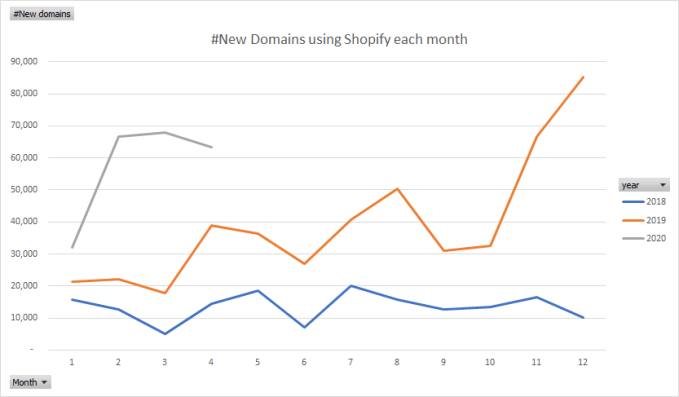

Looking at the above graph in this Tweet from Shopify CTO Jean-Michel Lemieux — and the passing, contextless mention of “Offline2Online” — we got curious.

Beyond just the anecdotal evidence, we looked for signs that tell us e-commerce is being adopted at a faster pace. One way to ascertain that is to look at the historical data of how Shopify has been onboarding merchants for the last two years on a monthly basis, and compare that with what happened this year in Q1.

All of these data points come from PipeCandy’s own data platform that tracks close to 750K+ Shopify merchants with historical data for each:

New domains using Shopify each month

While 2020 started on a faster clip than 2018 and 2019, February and March have seen nothing short of jaw-dropping growth in merchant numbers for Shopify. In those two months alone, Shopify seems to have onboarded more merchants than in the whole of 2018.

The softening you see in April is a result of the lag in the way our systems validate and confirm the data and not a slowdown in Shopify per se. The e-commerce embrace is real.

Powered by WPeMatico

Talk of an economic downturn can be frightening, especially one precipitated by a pervasive health crisis. At times, I’m overwhelmed by the images of countless patients on life-support and the near-endless streams of statistics regurgitating bad news.

Having started in venture at the beginning of two recessions, I’ve seen how the startup industry functions during economic trouble. My second day of work at Charles River Ventures was September 11th, 2001. My first project, analyzing the VC industry, propelled the firm to return more than 60% of its fund to investors, going from a $1.2 billion fund to $450 million. In May 2008, Mike Maples and I founded Floodgate in the midst of the Great Recession. We learned that great founders won’t wait for a better economic moment to start a company.

While we are currently embroiled in personal and professional circumstances unimaginable even three months ago, these very challenges will form the basis of incredibly innovative ideas. In order for the world to move forward, we need our greatest minds to imagine a brighter future and create solutions to make it a reality.

When I analyze our society and novel health situation, one thing is certain: COVID-19 is a paradigm-shifting event, creating massively accelerated social and economic change.

Our current situation is unique. It’s not merely a cyclical economic event, nor is it a standalone health crisis. What we are experiencing is not just an inflection point: it’s a societal phase-change unlike anything we have ever seen. We face an epic choice of how we move forward, and the decisions we make today will shape an entire generation.

Here’s why: COVID-19 is prompting us to reset many of our most fundamental behaviors. These changes are impacting our financial system, with effects visible throughout our homes, businesses and even the concept of “workplace” itself.

As a global pandemic, the virus itself has spread to nearly every country in the world.

Between February 20 and March 26, 100% of the world’s 20 largest economies implemented government-mandated social distancing. Globally, the number of scheduled airline flights is down 64%. In some countries, like Spain and Germany, flight numbers are down by more than 90%.

Since the timeline for lifting government restrictions is unclear — and even then, scientists are uncertain how the virus will spread — the question lingers: How long will this go on?

COVID-19’s impact is uncertain, long-term and potentially undulating, affecting every facet of our lives. You can’t simply wait it out with the expectation that industries will rebound. In 2001, September 11 felt pervasive, but its economic impact ultimately stemmed from just one single incident and the resulting fear… and that one single incident still cost more than three trillion dollars. How much larger will COVID-19 be?

Powered by WPeMatico

Welcome back to This Week in Apps, the Extra Crunch series that recaps the latest OS news, the applications they support and the money that flows through it all.

The app industry is as hot as ever, with a record 204 billion downloads and $120 billion in consumer spending in 2019. People are now spending 3 hours and 40 minutes per day using apps, rivaling TV. Apps aren’t just a way to pass idle hours — they’re a big business. In 2019, mobile-first companies had a combined $544 billion valuation, 6.5x higher than those without a mobile focus.

In this Extra Crunch series, we help you keep up with the latest news from the world of apps, delivered on a weekly basis.

This week we’re continuing to look at how the coronavirus outbreak is impacting the world of mobile applications, including the latest news about COVID-19 apps, Facebook and Houseparty’s battle to dominate the online hangout, the game that everyone’s playing during quarantine, and more. We also look at the new allegations against TikTok, the demise of a popular “Lite” app, new apps offering parental controls, Telegram killing its crypto plans and many other stories, including a hefty load of funding and M&A.

Powered by WPeMatico

“In general, the consumer has proven to be more resilient than I would have thought,” said Kirsten Green, founder of Forerunner Ventures, which has investments in breakout D2C stars like Glossier, Hims and Bonobos.

She joined us for an Extra Crunch Live conversation to help us better understand buying habits in the COVID-19 era. With tens of millions out of work and uncertainty all around, people are spending less, but Green showed up with a healthy dose of optimism — while acknowledging that her worst-case scenario planning was wrong.

Take a cautious approach, be prepared to make hard decisions, but be thoughtful about that. Don’t just make a knee jerk-reaction, which is “this is the apocalypse, we all need 36 months of runway, fire half your staff and go to the bunker.” I think the biggest opportunity for companies right now in many ways is to create value by demonstrating their flexibility.

Powered by WPeMatico

On May 21 at 3pm ET/12pm PT, we’re hosting an Extra Crunch Live session with Steve Case and Clara Sieg of Revolution.

This chat is the latest in our growing series featuring notable investors, entrepreneurs and technologists. Previously, TechCrunch editorial staff sat down (virtually, of course) with Cowboy Ventures’ Aileen Lee and Ted Wang, Sequoia’s Roelof Botha and Mark Cuban, to name a few.

There’s a lot to talk about with Case and Sieg, and Extra Crunch members are encouraged to come with their own set of questions to ask these renowned investors. Revolution is known for its wide range of investments, inside and out of the Valley, so we’re curious how the firm is addressing the COVID-19 crisis.

Steve Case was a co-founder of AOL and led the company as it became the internet giant of the ’90s — and did so outside of Silicon Valley. Because of this, he’s long been a champion of startups from other regions. Yet the firm still has a presence in Silicon Valley, and Clara Sieg has run that effort since 2012 after joining in 2010.

We’re curious how Case, Sieg and other partners are advising startups to weather this storm. With investments throughout the country, Revolution is in a unique position to have a holistic perspective on how the COVID-19 crisis is affecting startups.

Are they still funding startups right now? What metrics are they looking for? What regions of the country do they see less effected than others and which are hardest hit?

We have questions and we hope they have answers.

Extra Crunch members can ask their own questions directly in the Zoom Q&A. So come prepared! You can find the full information for the chat below. See you there!

Powered by WPeMatico