exit

Auto Added by WPeMatico

Auto Added by WPeMatico

PagerDuty debuted on the New York Stock Exchange today, and as we type, shares of the nine-year-old, San Francisco-based incident response software company are trading at nearly $39.

That’s up more than 60 percent above their IPO range of $24 per share, which was itself adjusted from the range of $21 to $23 that had been expected earlier and gives the company a valuation of close to $3 billion. That’s an awful lot for a company whose software helps technical teams at 11,000 companies spot problems with applications and respond to incidents. Though it’s growing quickly — revenue was up 48 percent last year — it still pulled in just $117.8 million in 2018. Meanwhile, its net loss widened last year, to $40.7 million from $38.1 million in 2017.

Certainly, its performance has to make the company’s investors — who last assigned the company a valuation of $1.3 billion back in September — very happy. Some of the VCs poised to win big if PagerDuty’s shares continue flying high include Andreessen Horowitz, which owned 18.4 percent of PagerDuty’s shares sailing into the IPO; Accel, which owned 12.3 percent; and Bessemer, which owned 12.2 percent. Other winners include Baseline Ventures (6.7 percent) and Harrison Metal (5.3 percent).

It’s also exciting for CEO Jennifer Tejada, a proven operator who was brought in to lead PagerDuty in 2016 and now becomes part of a small — but growing — club of women CEOs to take their tech companies public, including Katrina Lake of Stitch Fix and Julia Hartz of Eventbrite.

We talked with Tejada earlier today about the company’s big day. In addition to crediting company co-founders (and shareholders) Andrew Miklas and Baskar Puvanathasan, both of whom have since left the company, Tejada thanked PagerDuty co-founder Alex Solomon, who remains the company’s CTO. She also told us a little bit about what today has been like, and how the IPO changes things — and doesn’t. Our chat has been edited for length.

TC: First and foremost, how are you feeling?

JT: It’s been an incredible day. It’s been an incredible several months. You have to enjoy it when it’s going well.

TC: How does the vision for the company change now that it’s public? Have you been thinking ahead to possible acquisitions?

JT: The vision doesn’t change. We intend to do exactly what we’ve been doing, which is to provide the best real-time operations platform available to companies as they undergo digital transformation to meet the growing demands of their customers. We think we’re [facing] an early and very large opportunity that will be available to us for a long time. So our job continues to be to build great products, stay close to our customers, expand regionally and continue doing what has allowed us to be a successful private company.

TC: You and I had talked about the challenges of retaining employees in San Francisco when we sat down together in November. It’s a battle for every local company. How do you keep employees beyond the lock-up period? How do you ensure they stay focused on performance and not your share price?

JT: I think that mindset of, ‘It’s all over when you go public,’ is kind of a Silicon Valley fable. If you look at the most successful SaaS companies on the planet, they’ve gained 10x, 20x, 30x their value post their IPO. I also think what employees look for ahead of their financial success is career success. Am I being developed and recognized and can I build my career at this company? And we’ve worked really hard to create those career opportunities for our employees who [I think see, as I do] the IPO like a racing boat pushing off the dock, across the starting line, and into the open ocean, where the next adventure awaits.

In the meantime, we’ve already lessened our reliance on [overheated job markets] by opening offices in Toronto and Atlanta and Seattle and London and Sydney, even while we’re still hiring in San Francisco and Seattle.

TC: Obviously, Lyft’s shares have been up and down, owing to short sellers. Have you been monitoring short interest? Are you at all concerned about investors driving the price sky high, then selling it on the way down?

JT: I haven’t even looked at the stock price in the last several hours . . . There are a lot of things outside of my control, and the free market is one of them.

TC: PagerDuty is rare in that is doesn’t have a dual-class structure, which can greatly empower leaders over everyone else associated with a company. Presumably, this is a great relief to your investors; I just wonder whether it was ever a consideration?

JT: I’m a little bit of a traditionalist. I’ve been around long enough to know how checks and balances work, and a single-class structure made sense for PagerDuty. Also, dual-class structures tend to emerge more when you have deeply involved founders, and though Alex is still very much a part of the business, PagerDuty’s other two founders have worked outside of the business for some time.

TC: You have plenty of operating experience, including previously running Keynote Systems, but you’ve never taken a company public. Were there ways in which you found the roadshow experience surprising?

JT: I was surprised by how fun it was! [Laughs.] When you have a great story, and a great partner helping you tell it — in my case that’s [PagerDuty CFO] Howard Wilson, who I’ve worked with for 10 years — it’s great. We had a great reception from investors. I loved our IPO team; our Top were both led by women and whenever I had a question, they [had the answer]. I also had this cocoon of experience surrounding me thanks to our board. If anyone tells you that [in this position] they are super comfortable, they’re either lying or [clueless] but I was very lucky. I also have a whole bunch of buddies who are CEOs [and other executives] in SaaS and I’ve been shaking them down for advice for months, so I felt well-prepared.

TC: What was some of the advice you received from those friends about how your life is about to change?

JT: Some of it was about the need to keep people focused and not get distracted, to remind everyone that this is a milestone, not the goal. [Some centered on] surrounding yourself with a great team and the importance of great investor relations, a function you don’t have as a private company but that can create huge value and provide support and understanding of the market.

One CEO said to just make sure you keep having fun, to try and stay “you,” to find joy in the same things as before. There will be stressful moments and tough questions — that’s true of any company that’s scaling — but I heard a lot of advice about just taking care of myself, including on the roadshow. In fact, there were a lot of really supportive notes and private tweets that, in a job that can feel lonely, made me feel not alone, and I’m very appreciative of that.

TC: People call IPOs just another funding event, but that’s kind of baloney, isn’t it? If you had to list the most meaningful moments in your life on a scale from 1 to 10, 1 being the most important, where might today fall? Would today be up there on that list?

JT: When I think of most meaningful moments, I think of the day my daughter was born, and my wedding. Another day that was very meaningful to me was when I approved our pledge to donate one percent [of PagerDuty’s equity, one percent of its product and one percent of employees’ time] to social impact. We did it a lot later in the game than some companies; our equity was already valuable. But we knew that it was going to create meaningful impact over time.

But yes, it is a gratifying day, especially for the co-founders who were pulling the idea together for PagerDuty a couple of years before they even launched it, and for employees who’ve been with the company for nearly as long and who turned down safer and higher-paying jobs along the way. Seeing their joy today — that is a memory that will be in my top 10 for sure.

Powered by WPeMatico

Extra Crunch offers members the opportunity to tune into conference calls led and moderated by the TechCrunch writers you read every day. This week, TechCrunch’s Kirsten Korosec and Kate Clark led a deep-dive discussion into Lyft’s IPO and the outlook for the business going forward.

After skyrocketing nearly 10% on its first day hitting the public markets, Lyft stock has faded back down towards its IPO price as some investors grow more concerned over the company’s path to profitability (or lack thereof) and the long-term fundamentals of the business. But Lyft’s public listing is bigger than just the latest in increasingly common unicorn IPOs. As the first public “transportation-as-a-service” company, Lyft offers the first inside glimpse into the business model and its economics, and its development may ultimately act as the canary in the coal mine for the future of transportation.

“Lyft, hasn’t just survived, they’ve grown. 18.6 million people took at least one ride in the last quarter of 2018. That’s up from 16.6 million in late-2016. That illustrates the growth that the company has had. They’ve also said that they have 39% share of the ride-sharing market in the US. That’s up from 22% in 2016.

To me, the big question is let’s say they had Uber’s share, which is 66%, would they be able to make a profit? Is that the determination? And I’m not convinced that it is, which is why all these other aspects of the transportation-as-a-service business model [micromobility, AVs, etc.] are going to be really important.”

Image via Getty Images / Mario Tama

Kirsten and Kate dive deeper into what the market response to Lyft means for Uber and the timeline for its impending IPO. The two also elaborate on their skepticism of ride-hailing economics and debate which innovative transportation model will ultimately drive the path to profitability for Lyft, Uber and others.

For access to the full transcription and the call audio, and for the opportunity to participate in future conference calls, become a member of Extra Crunch. Learn more and try it for free.

Danny Crichton: Good afternoon and good morning everyone this is Danny Crichton, executive editor of Extra Crunch. Thanks so much for joining us today with TechCrunch reporters Kate and Kirsten.

I’ll start with a quick introduction for our two writers today. We have Kate Clark, our venture capital reporter. Kate has been with us for a while now covering everything in the startup and venture world. She’s also one of the hosts of TechCrunch’s podcast Equity and also writes our Startups Weekly newsletter.

Our other writer today is Kirsten, our intrepid automotive writer covering all things Elon Musk, Tesla, and everything else in the autonomous vehicle space. Kirsten has also been with us for quite some time and also writes a newsletter that she just introduced in the last couple of weeks, around transportation. So with that, I’m going to hand off the conversation to the two of them now.

Kirsten Korosec: Thanks so much Danny. This is Kirsten Korosec here. The newsletter is in a bit of a soft launch but it is being published Fridays and we hope to have an email subscription coming sometime in the future, so just keep an eye out for that.

I should also mention I too have a podcast centered around autonomous vehicles and future transportation called The Autonocast that comes out weekly. Thanks so much for joining the call and just a reminder, we want participation. So at about the halfway point, we’ll turn and open up the line and answer questions. Let’s get started.

Before we dig into all the hot takes out there, I think it’s worth providing a primer of sorts — a general timeline of events. We all probably know Lyft of course and most of us think of 2012 as the launch date when it came to San Francisco, but really Lyft was build out of the service of Zimride. Which is the ride-sharing company that John Zimmer and Logan Green founded in 2007.

A lot of attention has been placed on Lyft in 2018 with what happened in the past year, in the run-up to the IPO. But I think it is worth noting the intense activity and growth that happened between 2014 and 2016. These are critically important years for Lyft, just a frenzy of activity in a period where the company gained ground, investors, and partners.

To showcase the amount of activity that was happening; Lyft had two separate funding rounds, one for $530 million another for $150 million, just two months apart in 2015. You might also recall in early-2016 its partnership with GM and the automakers’ $500 million dollar investment as part of the Series F $1 billion dollar fundraising effort.

That was really interesting because GM’s president at the time Dan Ammann took a seat on the board, which he has since vacated. As Lyft and GM started realizing that they were competitors. Now, Dan is the CEO of GM Cruise which is the self-driving unit of GM.

2017 and 2018 were also big years, as Lyft launched their first international market in Toronto. They made big moves on the autonomous vehicle front, which we’ll talk about today, and in micromobility. Their scooter business launched in Denver in 2018. They bought Motivate, which is the oldest and largest electric bike share company in North America. Then, we finally get to the end of 2018, and this is when Lyft confidentially files a statement with the FDC and we’re off with the races to the IPO.

The last two months or three months is when Lyft unveiled its prospectus, met with investors, priced its IPO and made its public debut. So Kate what are the nuts and bolts of the IPO and what’s happening right now?

Kate Clark: Hi everybody this is Kate. So I’m just going to mention really quickly the timeline these last couple of months in the run-up to Lyft’s highly historical IPO. So going back to December, that’s when Lyft initially filed confidentially to go public. We later find out that they are going public on the NASDAQ when they eventually unveiled their S1 in early March.

This is after Lyft had raised $5 billion in debt and equity funding at a $15 billion dollar valuation, so there are a lot of people paying attention to what was the first ever rideshare IPO. So then in early-March, we’re able to get a closer look at Lyft’s S1, which tells us that the company has $911 million in losses in 2018 and revenues of $2.2 billion. So after calculating and pulling together some data, a lot of people were quick to find out that that means Lyft has some of the largest losses ever for any IPO. But also has some of the largest revenues ever for any pre-IPO company, just following Google and Facebook in that category.

So this is a really interesting IPO for a lot of people given these sky-high losses but also these huge, huge revenues. The next we see Lyft price their IPO between $62 and $68 dollars a share. Some people were quick to say that that was maybe a little underpriced, given that this was a highly anticipated IPO with a ton of demand. So on the second day of Lyft’s roadshow, the process, they say that their IPO is oversubscribed. So demand is apparently huge, their oversubscribed, so they decide we’re going to increase the price of our shares.

Image via GettyImages / maybefalse

So Lyft then says they gonna charge a max of $72 per share and then on the day of their IPO they charge $72 per share, the next day opening at $87 per share. So we see a huge IPO pop that I don’t think was particularly surprising given that they already spoke of this demand, and we had already known that there was a lot of demand on Wall Street. Not just for Lyft but just for unicorn IPO’s of this stature, given that there are so few of these. So Lyft began trading hitting $87 per share though, if you’ve been following the news that’s not were Lyft is today.

Kirsten: Yeah so I was just about to ask — Kate give me the latest numbers, you know a lot of focus is on that opening day but things haven’t exactly sustained. So what’s happened in the past few days?

Kate: Yeah it’s really tough to manage expectations after an IPO. I mean, I think there has been a lot of criticism towards Lyft now and I think it’s trading below its initial share price. So as I mentioned Lyft opened at $87 per share, it priced at $72, but almost immediately they began trading below that $72 price per share. So they closed Tuesday trading at $68.96 per share. Still boasting a market cap larger than $19 billion. So they’re still significantly valued at more than they were as a private company at $15 billion but it doesn’t look good to be trading below a price per share so quickly.

However, it actually did hit its IPO price for just a minute today, so maybe let’s give it a few more hours and see where it closes. It’s possible that it will sort of jump towards that $72, but it’s still trading quite significantly below that $87.

Kirsten: With IPOs like this, and especially such a high profile one, there’s going to be a ton of attention on share price and on volatility. And so I’m wondering, in your view, what did this first week, or first few days of volatility say to you? What does it say about Lyft’s future and, well certainly, its present?

Kate: Yeah. I mean, it’s hard to say. I think a lot of people were questioning if Wall Street was going to be interested in a company like Lyft that’s extremely unprofitable at this time and has years left before it will reach profitability, if indeed it ever reaches profitability.

So at this point you got to wonder, do some of these investors that did buy Lyft right off the bat, were they really long on Lyft? Because it does look like a lot of those investors have already sold their stock and perhaps weren’t as invested in Lyft’s long-term profitability plan, which involves a lot of very iffy things, like the future of autonomous vehicles, which we’ll talk about later in this call. And there’s a lot of uncertainty there.

But with that said, it’s not uncommon for a stock to experience volatility right off the bat, and you can’t assume the future of that stock price just because of some early volatility.

And we gathered some examples of IPOs where there was some early volatility that did not determine the long term future. So Carvana, for example, which is an online used car dealer in the automotive space, and it did experience volatility at first, with the stock sliding in the first few months but ultimately trended upward.

Kate: So Carvana opened at $13.50 a share, falling below its IPO price, so it didn’t even have the IPO pop. And then in 2018, it hit an all-time high of $65 per share. Today, it’s trading around $58 per share, so that’s ultimately a positive story to be told there.

And then another example on the other side of things is Snap, which actually took four months to dip beneath its 2017 IPO price, and we all know Snap has definitely not been a success story and it’s trading well below its offer price. But then finally, Facebook, for example, dropped below its IPO price on its second day of trading and then actually had a rough first year on the stock market before the stock ultimately took off and became a very obvious success.

Kirsten: So, Kate, I’m wondering why you think that there was that initial run up on that first day. Was it excitement? Was there something material that was pushing the price up? What was the cause?

Kate: I think there was a lot of excitement and demand around this IPO because it was very much one-of-a-kind, and there were a lot of investors that it seemed were really long on the possibility of Lyft becoming this hugely profitable company. And I think a lot of that was because in the S1, although you did see these really, really big losses — quite major, just ridiculously huge losses — you did see that they were shrinking over time and that there was definitely a path in which Lyft could take where it would reach profitability, say, in the next five years.

And I think Wall Street was really paying attention to that, and they were not paying attention to some of the other metrics. Now, they’ve taken off their rose-colored glasses and they’re looking at Lyft as a public company, and it’s just a little bit different now that it’s actually completed its debut.

Kirsten: Well, so, I mean, I like to view IPOs often times, and especially in Lyft’s case, as a measure of an investors’ faith in the company’s growth prospects, because this is a company that while it does have quite a bit of revenue, it has significant losses and it’s really planning not just for the present day but for the future. It’s been called a disruptive business for a reason, and it is certainly very forward-looking. So I’m wondering if you think it was a good strategy for Lyft. They wanted to open it up to “the everyman” when they actually went to market. They did a different approach, and do you think this might have had an effect? I mean, it’s very on-brand for them to do this, but I’m wondering if you thought that means that some of the investors aren’t as disciplined.

Kate: Do you mean with the fact they were providing bonuses to their employees and drivers to actually participate in the IPO as well?

Kirsten: Absolutely. That’s actually a really good point that maybe you can elaborate on. Lyft did a little bit of a more open approach for its IPO. Typically IPOs can be closed off to only large, institutional investors. So did this set them up perhaps to have more volatility?

Kate: Yeah, Lyft provided some of their drivers up to, I think, $10,000 to, in theory, actually buy stock in the IPO. Do I think that had a high impact? I don’t know. I think there’s not enough comparison, not enough data to really make a decision or to make a hot take on whether that really was part of the volatility. I think just given the uncertain nature of Lyft’s future and their big losses, I think their volatility was pretty inevitable, and I think people paying attention to this are probably not particularly surprised by how the stock has fared in these first couple days.

And I do want to add there’s this six-month lock-up period for the venture capital funds that own Lyft and as well as their employees, so I think we’re not sure what’s going to happen when that lock-up period ends and those holders can just sell their stock right then or how that will impact the stock price, as well.

Image via TechCrunch/MRD

Kirsten: So something to keep an eye on. It reminds me a lot of a company I write a lot about, which is Tesla, and I’ve been covering them for years. And it’s one of the most volatile stocks, and their investors, they certainly have large, institutional investors, but the number of fanboys that they have with smaller investors, either prop up the share price sometimes or add to that volatility, and I’m kind of really curious to see if that happens with Lyft. If you go to a shareholder meeting at Tesla, for example, it’s filled with people who are passionate about the brand and its CEO, Elon Musk.

And Lyft and possibly Uber, if they end up finally going through with their IPO, you can see that potentially happening because people feel very strongly about the brand and also the service it provides. So I’m curious to see how this all sort of shakes out. And I tend to take the view that I invest personally in mutual funds and things like that. I don’t invest in any of these companies, but the long, patient view tends to be the better one, and trying to catch a falling knife, as investors have told me, is never really a good idea.

So I’m curious to see if investors sort of grow up and learn with Lyft, if they’ll become disciplined and just sort of wait it out and see them play out the growth prospects for the company in the long term. So, we’ve been talking about Lyft and I can’t not talk about Uber as a result. I’m wondering what you think this might mean for Uber. The big story initially was let’s beat Uber to IPO and I’m wondering what this means then. Is this indicative of what Uber is going to experience?

Kate: I think that question is really at the top of everyone’s mind right now, including my own. I will say that I still do think it was highly beneficial for Lyft to get out first. Because imagine if and when Uber does too experience volatility, which it probably will, if it were to have gone first, I think that would have frightened Lyft a lot more than Lyft’s volatility may or may not be frightening Uber. So, with that said, I think I’m of two minds right now with my thoughts on how this impacts Uber’s IPO. I think that if Lyft stock continues to be volatile and perhaps even falls lower than it already has. I do think that there is a chance Uber may ultimately decide to push its IPO back.

I think that for a few reasons, namely being that Uber is not in a huge rush to go public. They do have the ability to wait. They have filed to go public. So it’s likely to happen quite soon, but it may not happen in April as they are reportedly planning to do.

On the other hand, Lyft went public at like a $24 or $25 billion dollar market cap. Whereas Uber is going to debut at maybe a $120 billion dollar initial market cap. So these IPOs, although they are both ride hail IPOs and they are very similar companies in a lot of ways, they’re also very different and Uber is operating on an entirely different scale though it still is unprofitable. And has some of the same issues that, investors are probably noting about Lyft.

I think it’s either going to be that it’s maybe that they do decide to push it back or maybe that Uber is like, well we’re five times larger, six times larger. We have much larger statistics to show to investors. There’s just a chance it could go either way. I wish I had a better, more concrete answer, but I just don’t think we know yet.

Kirsten: Well I’m okay with not taking hot takes just a few days into this IPO. I think this is a good time to open it up to questions. While we wait for a question, I will do one quick follow up with you Kate. What do you think this means for Uber? Will it delay its IPO?

Kate: Right now, no, I don’t think they’re going to. But it’s like I said, it’s tough to say given that it’s only been a few days of Lyfts IPO. But no, I think you’ve got to imagine that they are ready to discuss the possibilities of Lyfts IPO and already planned ahead if there was volatility. They maybe already assumed that would happen, given that that’s not uncommon. So right now I’m going to say no, I don’t think they’re going to delay, but it’s certainly still a possibility.

Kirsten: Okay, great. I think another really interesting piece for Uber was their acquisition of Careem. This is a deal that was made right before their IPO, so it was shifting attention away from Lyft, just for a moment.

Why did Uber do this? Is this not a signal that they’re delaying their IPO? Is this just prepping for it? What are you hearing on it? I’m wondering if this might have just been a strategy to show the world investors, specifically potential shareholders, what the road ahead is going to look like. Or is it some other reason — Is it to justify their really big losses?

Image via Careem / Facebook

Kate: I think it’s the latter two things you said. Just to give some background Uber is paying about $3.1 billion to acquire Careem, which is a Middle Eastern ride-hailing company. So basically just the Uber of the Middle East. Uber does have a history of acquiring, smaller competitors like this in different markets where it’s not active, just as a way for Uber to quickly grow essentially.

So I do think it’s a big deal to make just before going public. So I guess we don’t know if they necessarily will go public in April, but I think it was a move to present to public market investors as a prep for an IPO, to show “we just acquired this company, here’s more evidence of future growth”. Like you mentioned, it’s definitely a justification of those huge losses that we know Uber has.

Kirsten: Thanks for that. Questions?

Caller Question: Hi there, so when we talk about looking ahead and moving towards profitability — what role, if any, do you think the acquisition of a scooter or other mobility companies will have for companies like Lyft and Uber?

Kirsten: That’s a great question. I think it’s going to be a huge piece of both of their businesses. A lot of people describe this as the first ride-hailing IPO. We need to stop calling this a ride-hailing company. These are transportation-as-a-service companies and they’re making money. But generating revenue as opposed to making profit is a totally different thing. When you start talking about ridesharing, it’s a tough business. With those it’s an asset-light business, right? They don’t own the cars and then they technically don’t employ these drivers.

But at the same time, as of 2016 only something like 1% of people in the US were using rideshare. So you see this opportunity, but they’re not pushing forward. There is a ton of car ownership still that’s happening. Yes, sharing has absolutely increased, but 17 million new cars were sold in the US last year. So scooters, bike share and other businesses are going to be key to their paths to profitability because ride-sharing alone is just difficult to make a profit. It’s not difficult to generate revenue. It’s difficult to make a profit on.

And I’m wondering, talking about that road to profitability, I do think it’s worth noting how much they have grown. Lyft, hasn’t just survived, they’ve grown. 18.6 million people took at least one ride in the last quarter of 2018. That’s up from 16.6 million in late 2016, that illustrates the growth that the company has had.

They’ve also said that they have 39% share of the ride-sharing market in the US. That’s up from 22% in 2016. To me, the big question is let’s say they had Uber’s share, which is 66%, would they be able to make a profit? Is that the determination? And I’m not convinced that it is, which is why all these other aspects of the transportation-as-a-service business model are going to be really important.

Kate: I think what you pointed out is important, about Lyft and Uber both becoming transportation businesses, not ride-hailing companies and I think their long-term visions involve scooters, bikes, autonomous vehicles, all sorts of different models of transportation beyond just car sharing.

Kirsten: I hate to be wishy-washy here and say, I don’t know, but I do really think that it’s going to come down to a variety of items all coming together. It’s just not going to be enough for Lyft to scale up its ride-hailing business. And I should point out that Uber should be treated in some ways the same way, but there are some distinct differences. But it’s important for us to think of Lyft as a transportation-as-a-service business. I mean they say in their prospectus that transportation is a massive market opportunity. The hard part of course is turning that into a profit. There might be opportunity there.

So there’s this asset-light business that they have right now, which is the ride-hailing, but then they are making acquisitions in the micromobility space and that is going to become more capital intensive. And that’s going to force them to change their business. And then there’s the autonomous vehicle piece. And then finally, I actually think that one of the pieces of their S1 that has really not received much attention at all is what they’re pursuing in terms of public transportation. And they have said that they, and Uber, intend on being a piece of the public transit ecosystem.

Now that doesn’t mean that they’re going to necessarily be operating buses, but there are people that I’ve talked to in the industry who actually feel like, in Uber’s case, they want to control every mode of transportation. For Lyft, I see them seeing more of the opportunity financially with the data piece and becoming more of a platform and becoming that one-stop shop where you use an app to figure out if you want to use the scooter or a bike, or ride-hailing or buy that ticket for the L in Chicago or the Bart System.

So I really think that the public transit piece often gets ignored and cities are having so much more control now and weighing in. We see this in New York City with congestion pricing. It’s going to force Lyft and Uber to take advantage of these opportunities and use their platform in a way that perhaps accelerates faster than they had intended.

Kate: I’m very interested in the public transportation element, but I’m also very skeptical of the scooters and bikes in the future for Lyft, I think, given the unit economics, I certainly wouldn’t rely on them to be Lyft’s path to profitability. I think autonomous vehicles are a much more interesting path towards profitability. So a lot of companies, Uber, Lyft, Waymo and more are focusing on autonomous vehicles and their development, whether that be with hardware or software. How does Lyft’s strategy with autonomous vehicles differentiate from some of their competitors or does it does differentiate?

Kirsten: It does differentiate, and the funny thing is, is that so you don’t see micromobility necessarily as the oath to profitability and are interested in AVs and I write about AVs, but I see that AVs as a harder path to profitability in a way because of the nuts and bolts that it takes to develop them.

So just to weigh in really quickly on the micromobility piece and then I’ll move on to AVs; To show the opportunity but also the volatility in a real-world example for micromobility, I was in Austin for South by Southwest, I think you were there too, and you probably saw scooters everywhere, right? 18 months ago there were no scooters or bike share in the city. Then bike share came first.

Image via Flickr / Austin Transportation / https://www.flickr.com/photos/austinmobility/41536051644/in/album-72157669223418248/

And I was talking to that mayor of Austin and one of the folks from Spin, which is a Ford owned business, and they told me something that was really remarkable that I hadn’t thought about, which was that scooters were disrupting the bike share business. So bikes share came in and then scooters came in and all of a sudden they’re pulling bikes off the streets because no one was using them or were not using them at the same level as scooters.

Lyft is going to go through these same exact growing pains and people are figuring out what works. And as you mentioned, the unit economics are an issue, the wear and tear on the scooters alone is driving up costs and driving down revenues certainly, but pretty much making it very difficult to make a profit on it.

But that’s a near term business, right? So it’s at least generating revenue right now. On the other hand, you have this other piece, which is the AV piece. Lyft is doing some really interesting things on the AV piece — they kind of have a two-prong approach.

So they basically created a ton of partnerships to use their platform. So this started a couple of years ago and companies like Aptiv, drive.ai, even Waymo and nuTtonomy, which Aptiv just recently bought about a year ago and GM, and Lyft basically allows developers to use their platform and connect to their autonomous vehicle and offer these rides.

And the best example of this, if you’ve been to CES or if you have been to Las Vegas I should say more specifically, is this partnership that Lyft has with Aptiv — and Aptiv as a tier one supplier, they used to be called Delphi, they spun out, they bought nuTonomy, and they’re Aptiv now. And this is taking Aptiv automated BMW, which are on the Lyft network. If you hail a ride, you might be asked if you want a self-driving car, or “are you okay with a self-driving car?” And they have a safety driver, no humans have been pulled away from it yet. But they provided about 35,000 rides since I want to say January 2018.

Then they’re also doing Level 5, a dedicated self-driving vehicle division that launched in 2017. And here they’re basically creating an open self-driving system or open SDS. On top of that, they have partnered with Magna, an auto parts producer, to develop these self-driving systems that can be manufactured at scale.

And so you just see a rush of partnerships and sort of dual approaches and all of that costs a lot of money. And I can’t emphasize the amount of money that it costs or will cost to develop these systems and deploy them commercially. And I hear from other companies figures like $5 billion to get self-driving vehicles. So developing the full stack, doing fleet management, maintenance, all of that — that’s a lot of money. And, I’m not sure where Lyft, will get that capital, will they get it from the open market or will they have to go and ask for more capital.

Kate: So when do you think then that Lyft will be able to commercialize autonomous vehicles?

Kirsten: The timeline? So depending on who you talk to, you can hear from any of these developers between five years and 30 years. I think it’s important to talk about language and how we talk about autonomous vehicles. So to be clear, there is currently not a single commercial autonomous vehicle deployment where a human being or safety driver has been pulled away from the wheel. It just doesn’t exist.

There are plenty of pilots and Waymo is probably considered the leader in that list, though it is a bit of a confusing one for me because they have so many partnerships and they’ve become competitors to some of those partnerships. The analogy I use is “Survivor,” the reality show. Everyone wants to make these alliances so they don’t get voted off the island.

And now we’re at that point where autonomous vehicle development has entered what we call the trough of disillusionment, which is heads down, “let’s get away from the hype, let’s do the hard work.” And I think we’re going to see a lot of those partnerships and headwinds really come up in the next year, 18 months. So to put a target date on Lyft, it’s really going to depend on which one of those partnerships really play out and are real. I think the one with Aptiv seems the most real to me based on what I know the company is doing and I can see them doing a lot more pilots in the next 18 months.

Does that mean commercial deployment without a human safety driver behind the wheel? I’m not sure I can see a lot more these pilots with a human safety driver expanding beyond Las Vegas. I see pilots happening absolutely in the next year to 18 months. The issue is going to be when is that human safety driver going to be pulled out and with which partner.

Kate: So should we open it up to questions again?

Caller Question: Hi, I was just wondering how we should think about the regulatory risks that might exist as these companies expand to new cities, new markets, or even the public transport use case you mentioned. Thanks.

Kirsten: The regulatory piece is an interesting one. Let’s talk about ride-hailing first. We’ve already seen the regulatory environment, in cities, push back against companies like Uber and Lyft. I think the congestion pricing model that just launched in New York City is going to be one to watch and could be something that will put pressure on, on businesses like Lyft.

Kate: I agree and just to speak, quickly on the scooters; I think the narrative around scooters has been pretty dominated by how cities have forced them out or cities push these strict regulatory barriers on them. And I think that’s still playing out very much. There are even some scooter providers that have had to pull out of cities that they worked very hard to get into in the first place. So I think that has slowed down some of the growth there. And given that Lyft has micromobility as such a key part of their road to profitability, I think that’s partially why I am a little bit skeptical of how that’s gonna play out.

Kirsten: One thing we’ve found, and something to consider for Uber as well, in the future, if any of these AV developers end up, filing for IPOs on their own — there’s been chit chat about Waymo someday doing that or GM cruise someday— the implications for all of these companies and their relationship with cities should not be ignored or undervalued.

And I think you see a bit of that playing out with the present day track we have, which is the ride-hailing scooters and bike share cities and transit agencies or the DOT of different counties finding that they are in a more powerful position than they’ve ever been before. And they are exerting that power.

And so you will see instances like Los Angeles where they have put forth a mandatory data sharing component if you want to operate in their city. This raises some privacy concerns by the way, but it also adds another cost to a company or certainly forces them to look at their business a little bit differently.

Then you start talking about AVs and where are they will operate, how they will operate, where are they will park, what type of vehicle will be allowed in the urban center. In places like Europe, there are strict emissions rules, so that’s going to go to an AV or hybrid profile. And it’s important to think about what that regulatory framework might be and acknowledge the fact that it’s really a mishmash.

There are voluntary guidelines on the federal level right now, but there were no mandates. And so it’s really left up to the cities, counties and states to decide how an AV might be deployed. It’s going to mean probably more lobbyists in DC working with federal folks to ensure that their business doesn’t get hamstrung as a result as well as more of a presence in those cities and states and counties.

But Kate, I’m wondering what is your view from a startup perspective? Do you think of Lyft as a startup anymore are they acting like a startup or are they acting like a company that could handle all of these different complicated, various challenges? I mean, we’ve got pricing pressure, regulatory pressure or you’ve got AV development, opportunities with scooters and all this other stuff. So are they acting like a company that is able to handle this?

Image via Getty Images / Jeff Swensen

Kate: That’s an interesting question. I mean, they’re definitely not a startup anymore by, by anybody’s definition. You maybe could have still used that word, if they were still private, but even then, I know many people would yell at you for using that term for a company worth $15 billion. But now it’s a public company. It’s not a startup. I don’t think they’re acting like a startup, no. I think that they are mature in the way that they’re handling all of these different, so-called paths to profitability.

But we need to wait and see. Let’s see how this year goes, let’s see how they handle all the criticism that they’re going to undoubtedly take from Wall Street or from everyone who’s either interested in buying or just taking a seat and watching how the stock favors and then we’ll know what kind of lessons they took from all those years as a private company. Then we can decide if their behavior is really that of a mature public company.

Kirsten: I do want to make one point that I think is an interesting one on Lyft’s strategy versus Uber is in terms of AVs. Let’s all put a big asterisk that says no, AVs are still a ways out. It is important to note the Lyft and Uber’s strategies for AVs are wildly different and Uber does not take this dual approach. Uber is throwing a ton of capital towards developing their own, self-driving stack and also they’ve done, some acquisitions as well.

They’ve also had quite a bit of trouble. Last year Uber had the first self-driving vehicle fatality that happened in Tempe, Arizona, which looked like it was going to derail their self-driving unit, but it did not. They’re back, testing in a very limited way, but Lyft’s is all about what they call the democratization of autonomous vehicles.

And we can look at that as marketing speech, but I do think that it’s important to look at those words because it shows what their business model is. Their business model is partnerships, alliances, opening up the platform and casting the widest net possible. What I’m very interested to find out is which approach will end up being the winner. It’s going to be a very long game. It’s not going to be anything that’s going to be determined in the next year. I think what Lyft’s proven is that when they look like they’re down and out, they come back.

We’ll see what the better approach is. Do you do everything in-house and launch your own robo-taxi service? Or take capital partners on or do the Lyft approach, with multiple partners? Are partnerships actually too complicated? As someone who covers the startup world, do you have a thought on which one might work or not?

Kate: I have no idea which will work better and I’m sort of excited to see where this all goes, especially as Uber and Lyft are now going to be public.

That’s a good spot to end the call on.

Kirsten: Thanks so much for joining. Thanks again for being Extra Crunch subscribers, we really appreciate it. Bye everyone.

Powered by WPeMatico

Managed by Q, the office management platform based out of New York, has today been acquired by The We Company, formerly known as WeWork.

Financial terms were not disclosed. The WSJ reports that it was a cash and stock deal. Managed by Q, which has 500 employees, will remain as a wholly owned separate entity and CEO Dan Teran will remain following the acquisition to join WeWork leadership.

Upon its latest financing in January, Managed by Q was valued at $249 million, according to PitchBook.

Here’s what Teran had to say in a prepared statement:

We are excited for this incredible opportunity to deepen our commitment to realizing our ambitious vision of building an operating system for the built world. WeWork is uniquely positioned to invest in workplace technology and services, and I look forward to partnering with their team to build more robust products for our clients and create a global platform to help companies push the bounds on our collective potential.

Managed by Q was founded in 2014 with a plan to change the way that offices run. The platform allowed office managers and other decision-makers to handle supply stocking, cleaning, IT support and other non-work related tasks in the office by simply using the Managed by Q dashboard. Managed by Q serves the demand through a combination of in-house operators and third-party vendors and service providers.

Notably, Managed by Q took a different tack than most other logistics companies, employing their operators as W2 workers instead of 1099 contractors. Moreover, Managed by Q offered a stock option plan to operators that gives 5 percent of the company back to those employees.

The company has raised a total of $128.25 million since launch from investors such as GV, RRE and Kapor Capital. Managed by Q currently serves the markets of New York, San Francisco, Los Angeles, Chicago, Boston and Silicon Valley, with plans to aggressively expand following the acquisition, according to the WSJ.

Not only has Managed by Q swiftly matured into a big player in the NY tech scene and Future of Work space, but it has also fostered interesting competition and consolidation within the space. Managed by Q has itself made several acquisitions, including the purchase of NVS (an office space planning and project management service) and Hivy (an internal comms tool to let employees tell office managers what they need).

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Sure, we just aired a new episode, but things keep happening, and after talking about this crop of IPOs for so long, we can’t help ourselves. (You can follow us on Twitter, here and here, by the way, if Equity isn’t enough for you.)

Lyft, as you know, started trading today, closing the loop on a long saga that brought the smaller of the two domestic ride-hailing unicorns to the public markets.

After so much speculation about which of the two would get out the door first, Lyft did, and now we get to see what sort of pricing shenanigans happen next. Does Uber drop rates and punish Lyft? Or does Uber work to cut its losses, lowering its expenses and providing a clearer path toward profitability before its April IPO roadshow kicks off? (Not a path to profitability, mind; Uber and Lyft need to show a path to the direction of profitability first.)

We hit all the bases, going over the company’s pricing path, its varying share figures, final raise metrics and more. If you want the hard stuff, we’ve got a shot for you.

Now that the Lyft IPO has wrapped, we’ll be shifting our focus to Pinterest, Zoom and, of course, Uber. Stay tuned.

OK, now we’re done. Until next Friday. Unless something else happens.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

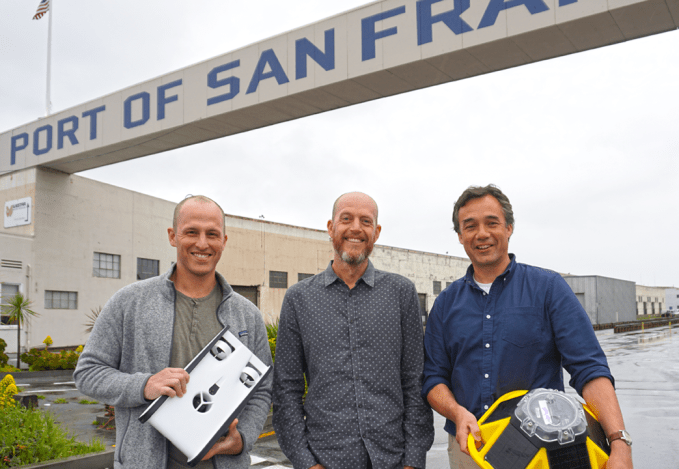

What lies beneath the murky depths? SolarCity co-founder Peter Rive wants to help you and the scientific community find out. He’s just led a $7 million Series A for Sofar Ocean Technologies, a new startup formed from a merger he orchestrated between underwater drone maker OpenROV and sea sensor developer Spoondrift. Together, they’re teaming up their 1080p Trident drone and solar-powered Spotter sensor to let you collect data above and below the surface. They can help you shoot awesome video footage, track waves and weather, spot fishing and diving spots, inspect boats or infrastructure for damage, monitor acquaculture sites or catch smugglers.

Sofar’s Trident drone (left) and Spotter sensor (right)

“Aerial drones give us a different perspective of something we know pretty well. Ocean drones give us a view at something we don’t really know at all,” former Spoondrift and now Sofar CEO Tim Janssen tells me. “The Trident drone was created for field usage by scientists and is now usable by anyone. This is pushing the barrier towards the unknown.”

But while Rive has a soft spot for the ecological potential of DIY ocean exploration, the sea is crowded with competing drones. There are more expensive professional research-focused devices like the Saildrone, DeepTrekker and SeaOtter-2, as well as plenty of consumer-level devices like the $800 Robosea Biki, $1,000 Fathom ONE and $5,000 iBubble. The $1,700 Sofar Trident, which requires a cord to a surface buoy to power its three hours of dive time and two meters per second speed, sits in the middle of the pack, but Sofar co-founder David Lang things Trident can win with simplicity, robustness and durability. The question is whether Sofar can become the DJI of the water, leading the space, or if it will become just another commoditized hardware maker drowning in knock-offs.

From left: Peter Rive (chairman of Sofar), David Lang (co-founder of OpenROV) and Tim Janssen (co-founder and CEO of Sofar)

Spoondrift launched in 2016 and raised $350,000 to build affordable ocean sensors that can produce climate-tracking data. “These buoys (Spotters) are surprisingly easy to deploy, very light and easy to handle, and can be lowered in the water by hand using a line. As a result, you can deploy them in almost any kind of conditions,” says Dr. Aitana Forcén-Vázquez of MetOcean Solutions.

OpenROV (it stands for Remotely Operated Vehicle) started seven years ago and raised $1.3 million in funding from True Ventures and National Geographic, which was also one of its biggest Trident buyers. “Everyone who has a boat should have an underwater drone for hull inspection. Any dock should have its own weather station with wind and weather sensors,” Sofar’s new chairman Rive declares.

Spotter could unlock data about the ocean at scale

Sofar will need to scale to accomplish Rive’s mission to get enough sensors in the sea to give us more data on the progress of climate change and other ecological issues. “We know very little about our oceans since we have so little data, because putting systems in the ocean is extremely expensive. It can cost millions for sensors and for boats,” he tells me. We gave everyone GPS sensors and cameras and got better maps. The ability to put low-cost sensors on citizens’ rooftops unlocked tons of weather forecasting data. That’s more feasible with Spotter, which costs $4,900 compared to $100,000 for some sea sensors.

Sofar hardware owners do not have to share data back to the startup, but Rive says many customers are eager to. They’ve requested better data portability so they can share with fellow researchers. The startup believes it can find ways to monetize that data in the future, which is partly what attracted the funding from Rive and fellow investors True Ventures and David Sacks’ Craft Ventures. The funding will build up that data business and also help Sofar develop safeguards to make sure its Trident drones don’t go where they shouldn’t. That’s obviously important, given London’s Gatwick airport shutdown due to a trespassing drone.

Spotter can relay weather conditions and other climate data to your phone

“The ultimate mission of the company is to connect humanity to the ocean as we’re mostly conservationists at heart,” Rive concludes. “As more commercialization and business opportunities arise, we’ll have to have conversations about whether those are directly benefiting the ocean. It will be important to have our moral compass facing in the right direction to protect the earth.”

Powered by WPeMatico

In Silicon Valley, investors don’t expect their portfolio companies to be profitable. “Blitzscaling: The Lightning-Fast Path to Building Massively Valuable Companies,” a bible for founders, instead calls for heavy spending on growth to scale in an Amazon -like fashion.

As for Wall Street, it’s shown an affinity for stock in Jeff Bezos’ business, despite the many years it spent navigating a path to profitability, as well as other money-losing endeavors. Why? Because it too is far less concerned with profitability than market opportunity.

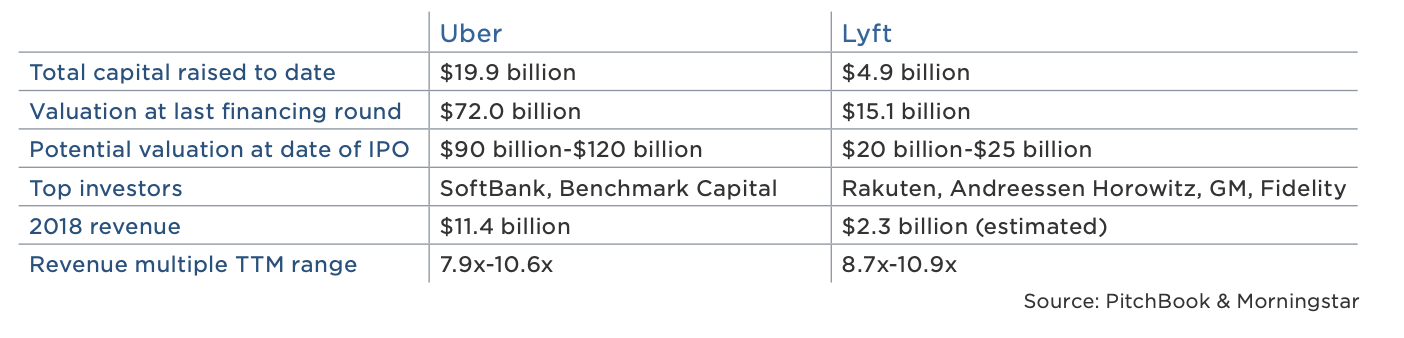

Lyft, a ride-hailing company expected to go public this week, is not profitable. It posted losses of $911 million in 2018, a statistic that will make it the biggest loser amongst U.S. startups to have gone public, according to data collected by The Wall Street Journal. On the other hand, Lyft’s $2.2 billion in 2018 revenue places it atop the list of largest annual revenues for a pre-IPO business, trailing behind only Facebook and Google in that category.

Wall Street, in short, is betting on Lyft’s revenue growth, assuming it will narrow its loses and reach profitability… eventually.

Lyft, losses notwithstanding, is growing rapidly and Wall Street is paying attention. On the second day of its road show, reports emerged that its IPO was already oversubscribed. As a result, Lyft is said to have upped the cost of its stock, with new plans to raise more than $2 billion at a valuation upwards of $25 billion. That represents a revenue multiple of more than 11x, a step up multiple of more than 1.6x from its most recent private valuation of $15.1 billion and, of course, Wall Street’s insatiable desire for unicorns, profitable or not.

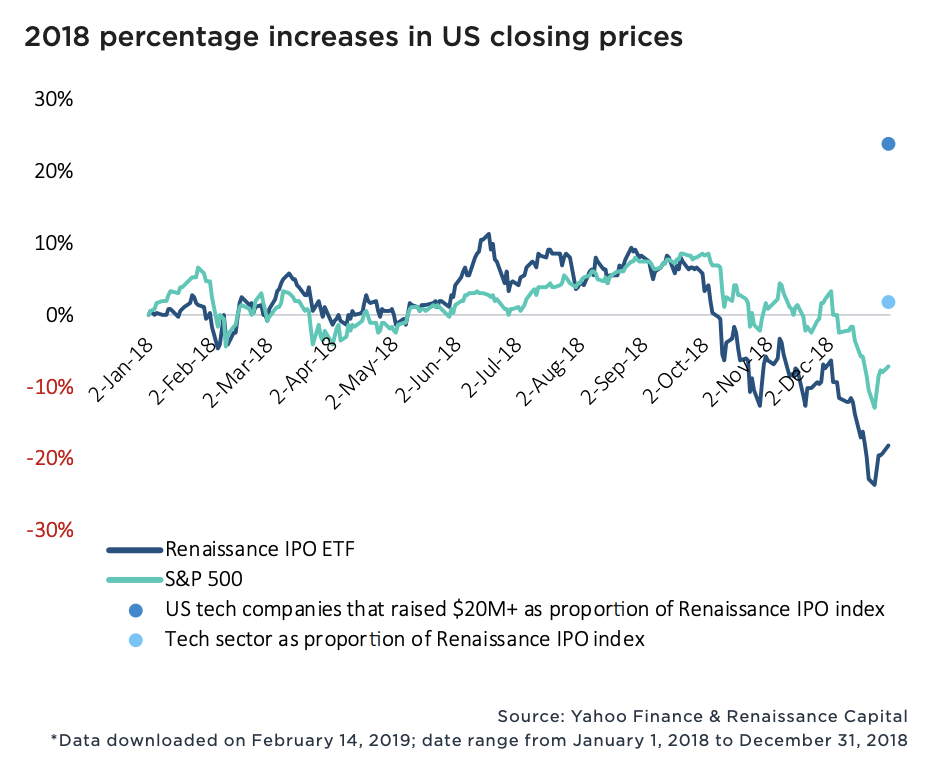

New data from PitchBook exploring the performance of billion-dollar-plus VC exits confirms Wall Street’s leniency toward unprofitable tech companies. Sixty-four percent of the 100+ companies valued at more than $1 billion to complete a VC-backed IPO since 2010 were unprofitable, and in 2018, money-losing startups actually fared better on the stock exchange than money-earning businesses. Moreover, U.S. tech companies that had raised more than $20 million traded up nearly 25 percent of 2018, while the S&P 500 technology sector posted flat returns.

Wall Street is still adapting to the rapid growth of the tech industry; public markets investors, therefore, are willing to deal with negative to minimal cash flows for, well, a very long time.

There’s no doubt Lyft and its much larger competitor, Uber, will go public at monstrous valuations. The two IPOs, set to create a whole bunch of millionaires and return a number of venture capital funds, will provide Silicon Valley a lesson in Wall Street’s tolerance for outsized exits.

Much like a seed-stage investor must bet on a founder’s vision, Wall Street, given a choice of several unprofitable businesses, has to bet on potential market value. Fortunately, this strategy can work quite well. Take Floodgate, for example. The seed fund invested a small amount of capital in Lyft when it was still a quirky idea for ridesharing called Zimride. Now, it boasts shares worth more than $100 million. I’m sure early shareholders in Amazon — which went public as a money-losing company in 1997 — are pretty happy, too.

Ultimately, Wall Street’s appetite for unicorns like Lyft is a result of the shortage of VC-backed IPOs. In 2006, it was the norm for a company to make its stock market debut at 7.9 years old, per PitchBook. In 2018, companies waited until the ripe age of 10.9 years, causing a significant slowdown in big liquidity events and stock sales.

Fund sizes, however, have grown larger and the proliferation of unicorns continues at unforeseen rates. That may mean, eventually, an influx of publicly shared unicorn stock. If that’s the case, might Wall Street start asking more of these startups? At the very least, public market investors, please don’t be swayed by WeWork‘s eventual stock offering and its “community adjusted EBITDA.” Silicon Valley’s pixie dust can’t be that potent.

Powered by WPeMatico

Social investing and trading platform eToro announced that it has acquired Danish smart contract infrastructure provider Firmo for an undisclosed purchase price.

Firmo’s platform enables exchanges to execute smart financial contracts across various assets, including crypto derivatives, and across all major blockchains. Firmo founder and CEO Dr. Omri Ross described the company’s mission as “…enabl[ing] our users to trade any asset globally with instant settlement by tokenizing assets and executing all essential trade processes on the blockchain.” Firmo’s only disclosed investment, according to data from Pitchbook, came in the form of a modest pre-seed round from the Copenhagen Fintech Lab accelerator.

Firmo’s mission aligns well with that of eToro — which is equal parts trading platform, social network and educational resource for beginner investors — with the company having long communicated hopes of making the capital markets more open, transparent and accessible to all users and across all assets. By gobbling up Firmo, eToro will be able to accelerate its development of offerings for tokenized assets.

The acquisition represents the latest step in eToro’s broader growth plan, which has ramped up as of late. Earlier in March, the company launched a crypto-only version of its platform in the US, as well as a multi-signature digital wallet where users can store, send and receive cryptocurrencies.

The Firmo deal and eToro’s other expansion activities fit squarely into the company’s belief in the tokenization of assets and the immense, sector-defining opportunity that it creates. Etoro believes that asset tokenization and the movement of financial services onto the blockchain are all but inevitable and the company has employed the long-tailed strategy of investing heavily in related blockchain and crypto technologies despite the ongoing crypto winter.

“Blockchain and the tokenization of assets will play a major role in the future of finance,” said eToro co-founder and CEO Yoni Assia. “We believe that in time all investible assets will be tokenized and that we will see the greatest transfer of wealth ever onto the blockchain.” Assia expressed a similar sentiment in a recent conversation with TechCrunch, stating “We think [the tokenization of assets] is a bigger opportunity than the internet…”

After the acquisition, Firmo will operate as an internal R&D arm within eToro focused on developing blockchain-oriented trade execution and the infrastructure behind the digital representation of tokenized assets.

“The Firmo team has done ground-breaking work in developing practical applications for blockchain technology which will facilitate friction-less global trading,” said Assia.

“The adoption of smart contracts on the blockchain increases trust and transparency in financial services. We are incredibly proud and excited that [Firmo] will be joining the eToro family. We believe that together we have a very bright future and look forward to pursuing our shared goal to become the first truly global service provider allowing people to trade, invest and save.”

Powered by WPeMatico

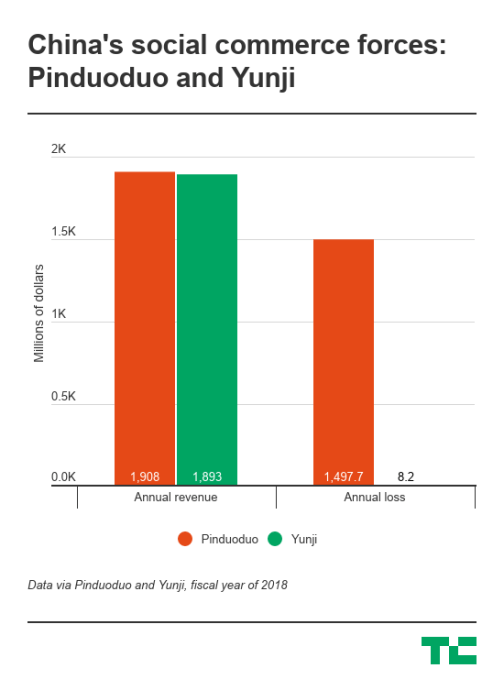

China’s Pinduoduo was all the rage in 2018 as the e-commerce upstart quickly rose to challenge Alibaba and raised $1.63 billion through a Nasdaq listing. Much of its success was attributable to its link to WeChat, China’s messaging leader. Now, another emerging e-commerce player that has leveraged WeChat is gearing up for a listing in the United States.

Yunji, which was founded in 2015 (the same year Pinduoduo launched), is raising up to $200 million according to its prospectus filed with the Securities and Exchange Commission last week. Reuters reported citing sources in September that Yunji planned to raise around $1 billion in the IPO at a valuation of between $7 billion and $10 billion.

Like Pinduoduo, Yunji bills itself as a “social e-commerce” service, which means it takes advantage of social relationships on apps like WeChat to acquire, engage and sell to users. The pair differ, however, in how exactly they make money. Pinduoduo generates the bulk of its revenues — nearly 90 percent in the fourth quarter — from advertising fees collected from merchants. This is akin to Alibaba’s marketplace play of connecting buyers and third-party sellers. Yunji, which was started by e-commerce veteran Xiao Shanglue, focuses on direct sales like Alibaba’s arch-foe JD.com, derived 88 percent of its fourth-quarter revenues from selling to users.

In terms of size, Yunji was about $15 million behind Pinduoduo in revenue last year. It had 23.2 million buyers in 2018, compared to Pinduoduo’s 272.6 million monthly active users. Yunji was, however, much closer to achieving profitability than Pinduoduo, which spent most of its money on sales and marketing. Most of Yunji’s expenses went to fulfillment and logistics.

From inception, Yunji has boasted of its “innovative” membership-based e-commerce model. To join, people typically pay a fee, upon which they gain access to a variety of benefits and discounts as well as the permission to open their own micro-stores. Members then get compensated for successfully selling to others and recruiting new members.

The marketing practice helped Yunji quickly build up a large network of users. As of 2018, Yunji had 7.4 million members who contributed 11.9 percent of its annual revenues and 66.4 percent of annual transactions. But the firm went too far in exploiting the social links it controlled that it started to look like a pyramid scheme, which is banned in China. In 2017, the local government slapped Yunji with a $1.4 million fine for pyramid selling. The firm subsequently apologized and promised to revamp its marketing strategy. For instance, to avoid crossing the red line of awarding salespeople with “material” or “financial” benefits, Yunji resorted to virtual Yun-coins, which are not redeemable for cash and can only be used as coupons for future purchase.

But Yunji is still on the edge. The company warns in its prospectus that China could at any time redefine what constitutes pyramid selling.

“[T]here is no assurance that the competent governmental authorities in China that we communicate with will not change their views, or the other relevant government authorities will share the same view as our PRC legal counsel, or they will find our business model, not in violation of any applicable regulations, given the uncertainties in the interpretation and application of existing PRC laws, regulations and policies relating to our current business model, including, but not limited to, regulations regulating pyramid selling.”

Some of Yunji’s more notable investors include China’s CDH Investments and Huaxing Growth Capital, China Renaissance’s subsidiary focusing on high-growth startups.

Powered by WPeMatico

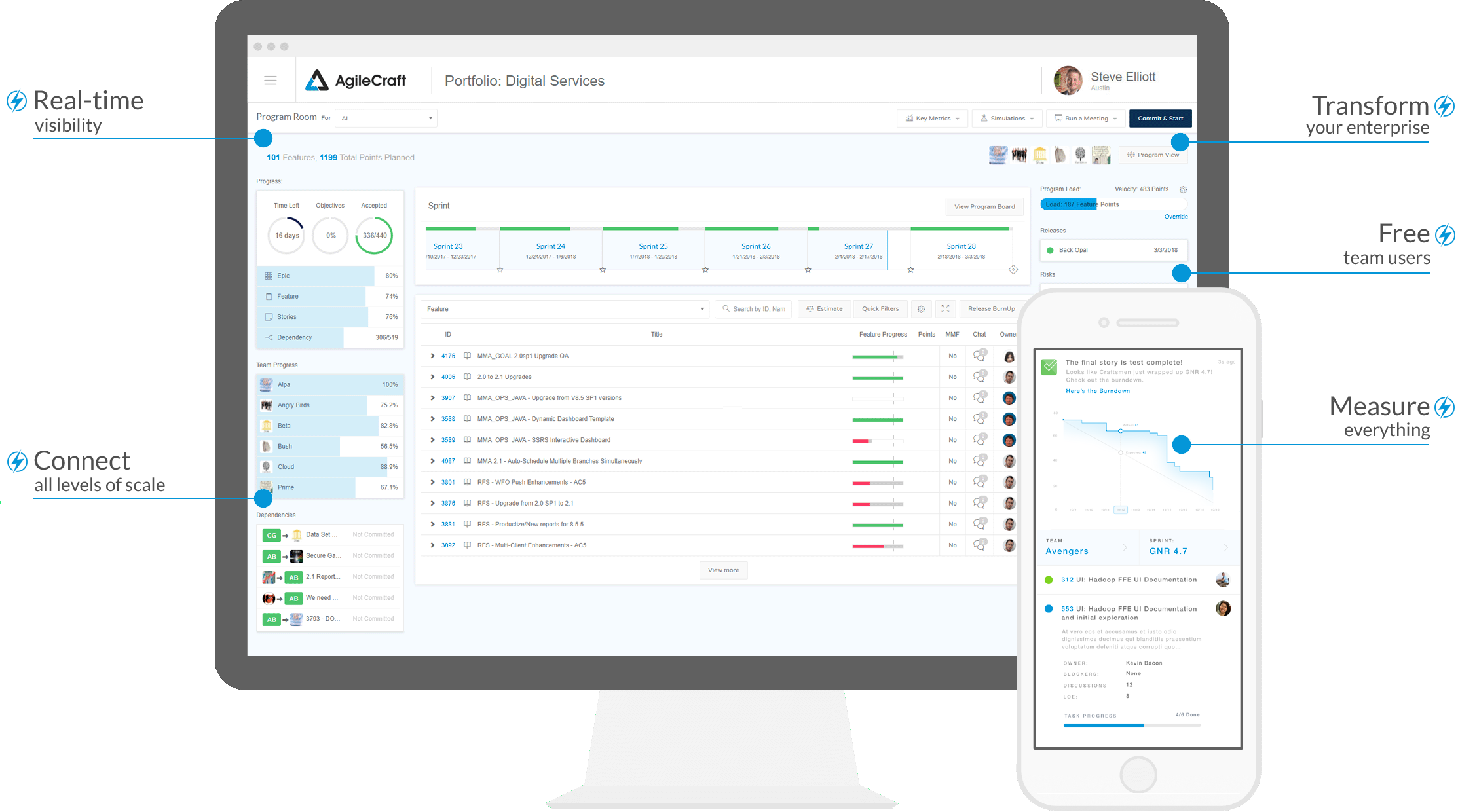

Atlassian today announced that it has acquired AgileCraft, a service that aims to help enterprises plan their strategic projects and workstreams. The service provides business leaders with additional insights into the current status of technical projects and gives them insights into the bottlenecks, risks and dependencies of these projects. Indeed, the focus of AgileCraft is less on technical teams than on the business teams that support them and help them manage the digital transformation of their businesses.

The price total of the acquisition is about $166 million, with $154 million in cash and the remainder in restricted shares.

“Many leaders are still making mission-critical decisions using their instincts and best guesses instead of data,” said Scott Farquhar, Atlassian’s co-founder and co-CEO, in today’s announcement. “As Atlassian tools spread through organizations, technology leaders need better visibility into work performed by their teams. With AgileCraft joining Atlassian, we believe we’re the best company to help executives align the work across their organization – providing an all-encompassing view that connects strategy, work, and outcomes.”

As the name implies, AgileCraft focuses on the Agile methodology, though it also offers a bit of flexibility there with support for frameworks like SAFe, LeSS and Spotify. It supports pulling in data from tools like Atlassian’s Jira, but also Microsoft’s Team Foundation Server, IBM’s RTC and other services.

Atlassian will continue to operate AgileCraft, which had raised about $10.1 million before the acquisition as a standalone service. “We will continue to focus relentlessly on our customers’ success,” writes AgileCraft’s founder and CEO Steve Elliott. “We remain dedicated to pioneering enterprise agility and are thrilled to team up with the outstanding people at Atlassian to help our customers thrive.”

Over the years, Atlassian started embracing users and use cases for its tools that go beyond its core tools for developers. Jira and Confluence are the prime examples for this. Today’s acquisition continues this trend in that AgileCraft aims to bring to the rest of the company many of the methodologies that tech teams use.

“One of the critical roles we play for lots of organizations is in helping drive this kind of digital transformation where we’re really empowering the teams that are building and developing the kind of technology that moves our customers forward,” Atlassian president Jay Simons told me. “AgileCraft basically complements all of that by extending visibility into what teams are using Atlassian products to do up into key stakeholders and leaders in the business that are trying to manage better visibility at a portfolio or program level.”

Simons also stressed that AgileCraft already has very strong integrations into the existing Atlassian tools — and indeed, that was one of the main drivers of the acquisition. He noted that the company plans to improve those and think about additional patterns. “We’ll continue doing what we’re doing,” he said.

Simons also noted that he expects that a lot of Jira customers will now look at AgileCraft as an additional tool in helping the businesses manage their business’s digital transformation.

Atlassian doesn’t typically make a lot of acquisitions. Its pace is close to about one major buy per year. Last year, the company picked up OpsGenie for $295 million. In 2017, it acquired Trello for $425 million, the company’s biggest acquisition to date. Other major products the company has acquired include StatusPage, BlueJimp, HipChat and Bitbucket (all the way back in 2010).

Powered by WPeMatico

During its earnings report yesterday afternoon, Okta announced it intends to acquire Azuqua, a Seattle, Wash. workflow automation startup, for $52.5 million.

In a blog post announcing the news, Okta co-founder and COO Frederic Kerrest saw the combining of the two companies as a way to move smoothly between applications in a complex workflow without having to constantly present your credentials.

“With Okta and Azuqua, IT teams will be able to use pre-built connectors and logic to create streamlined identity processes and increase operational speed. And, product teams will be able to embed this technology in their own applications alongside Okta’s core authentication and user management technology to build…integrated customer experiences,” Kerrest wrote.

In a modern enterprise, people and work are constantly shifting and moving between applications and services and combining automation software with identity and access management could offer a seamless way to move between them.

This represents Okta’s largest acquisition to-date and follows Stormpath almost exactly two years ago and ScaleFT last July. Taken together, you can see a company that is trying to become a more comprehensive identity platform.

Azuqua, which has raised $16 million since it launched in 2013, appears to have given investors a pretty decent return. When the deal closes, Okta intends to move the Azuqua team to its Bellevue offices, increasing its presence in the Northwest. Okta’s headquarters are in San Francisco. Azuqua customers include Airbnb, McDonald’s, VMware and HubSpot,

Okta was founded in 2009 and raised over $229 million before going public April, 2017.

Powered by WPeMatico