Eric Yuan

Auto Added by WPeMatico

Auto Added by WPeMatico

Maintaining company culture when the majority of staff is working remotely is a challenge for every organization — big and small.

This was an issue, even before COVID. But it’s become an even bigger problem with so many employees working from home. Employers have to be careful that workers don’t feel disconnected and isolated from the rest of the company and that morale stays high.

Enter Workvivo, a Cork, Ireland-based employee experience startup that is backed by Zoom founder Eric Yuan and Tiger Global that has steadily grown over 200% over the past year.

The company works with organizations ranging in size from 100 employees to over 100,000 and boasts more than 500,000 users. According to CEO and co-founder John Goulding, it’s had 100% retention since it launched. Customers include Telus International, Kentech, A+E Networks and Seneca Gaming Corp., among others.

Founded by Goulding and Joe Lennon in 2017, Workvivo launched its employee communication platform in mid-2018 with the goal of helping companies create “an engaging virtual workplace” and replace the outdated intranet.

“We’re not about real time, we’re more asynchronous communication,” Goulding explained. “We have a lot of transactional tools, and typically carry the bigger message about what’s going on in a company and what positive things are happening. We’re more focused on human connection.”

Using Workvivo, companies can provide information like CEO updates, recognition for employees via a social style — “more things that shape the culture so workers can get a real sense of what’s happening in an organization.” It launched podcasts in the second quarter and livestreaming in Q4.

In 2019, Workvivo showed its product to Zoom’s Yuan, who ended up becoming one of the company’s first investors. Then in May of 2020, the company raised $16 million in a Series A funding led by Tiger Global, which is best known for large growth-oriented rounds.

Workvivo, which was built out long before the COVID-19 pandemic, found itself in an opportune place last year. And demand for its offering has reflected that.

“Since COVID hit, growth has accelerated,” Goulding told TechCrunch. “We grew three times in size over where we were before the pandemic started, in terms of revenue, users, customers and employees.”

The SaaS operator’s deals range from $50,000 to close to $1 million a year, he said. Workvivo is Europe-based and operates in 82 countries. But the majority of its customers are located in the U.S. with 80% of its growth coming from the country.

The startup opened an office in San Francisco in early 2020, which it is expanding. Thirty percent of its 65-person team is currently U.S.-based, with some working remotely from other states.

While Workvivo would not reveal hard revenue figures, Goulding only said it’s not seeking additional funding anytime soon considering the company is “in a very strong capital position.”

To tackle the same problem, Microsoft last month launched Viva, its new “employee experience platform,” or, in non-marketing terms, its new take on the intranet sites most large companies tend to offer their employees. With the move, Microsoft is taking on the likes of Facebook’s Workplace platform and Jive in addition to Workvivo.

Despite the increasingly crowded space, Workvivo believes it has an advantage over competitors in that it integrates well with Slack and Zoom.

“We’re sitting alongside Slack and Zoom in the ecosystem,” Goulding said. “There’s Zoom, Slack and us.”

Slack is real-time messaging and what’s happening in the immediate future, and Zoom is real-time video and “about the moment,” he said.

To Goulding, Microsoft’s new offering is unproven yet and a reactionary move.

“It’s obvious there’s a battle to be won for the center of the digital workplace,” he said. “We’re here to capture the heartbeat of an organization, not pulses.”

Powered by WPeMatico

The coronavirus pandemic has bruised and battered many technology startups, but it has also boosted a small few. One such company is Zoom, which has shouldered the task of keeping us connected to one another in the midst of remote work and social distancing.

So, of course, we’re absolutely thrilled to have the chance to chat with Zoom founder and CEO Eric Yuan at Disrupt 2020 online.

Yuan moved to Silicon Valley in 1997 after being rejected for a work visa nine times. He got a job at WebEx and, upon the company’s acquisition by Cisco, became VP of Engineering at the company. He pitched an idea for a mobile-friendly video conferencing system that was rejected by his higher-ups.

And thus, Zoom was born.

Zoom launched in 2011 and quickly became one of the biggest teleconferencing platforms in the world, competing with the likes of Google and Cisco. The company has investors like Emergence, Horizon Ventures and Sequoia, and ultimately filed to go public in 2019.

With some of the most reliable video conferencing software on the market, a tiered pricing structure that’s friendly to average users and massive enterprises alike, and a lively ecosystem of apps and bots on the Zoom App Marketplace, Zoom was well poised to be a public company. In fact, Zoom popped 81% in its first day of trading on the Nasdaq, garnering a valuation of $16 billion at the time.

But few could have prepared the company for the explosive growth it would see in 2020.

The coronavirus pandemic necessitated access to reliable and user-friendly video conferencing software for everyone, not just companies moving to remote work. People used Zoom for family dinners, cocktail hours with friends, first dates and religious gatherings.

In fact, Zoom reported 300 million daily active participants in April.

But that growth led to increased scrutiny of the business and the product. The company was beset by security issues and had to pause product innovation to focus its energy on resolving those issues.

We’ll talk to Yuan about the growing pains the company went through, his plans for Zoom’s future, the acceleration in changing user behavior and more.

It’ll be a conversation you won’t want to miss.

Disrupt 2020 runs from September 14 to September 18, and the show will be completely virtual. That means it’s easier than ever to attend and engage with the show. There are just a few Digital Pro Passes left at the $245 price — once they are gone, prices will increase. Discounts are available for current students and nonprofit/government employees. Or if you are a founder, you can exhibit at your virtual booth for $445 and be able to generate leads even before the event kicks off. Get your tickets today.

Powered by WPeMatico

In the old days of enterprise software, when companies like IBM, Oracle and Microsoft ruled the roost, there was a tendency to shop from a single vendor. You bought the whole stack, which made life easier for IT — even if it didn’t always work out so well for end users, who were stuck using software that was designed with administrators in mind.

Once Software-as-a-Service (SaaS) came along, IT no longer had complete control over software choices. The companies that dominated the market began to stumble — although Microsoft later found its way — and a new generation of SaaS vendors developed.

As that happened, users saw a way to pick and choose software that worked best for them, as they were no longer bound to clunky enterprise software; they wanted tools at work that worked as well as the ones they used in the consumer space at home.

Through freemium models and low-cost subscriptions, individual employees and teams started selecting their own tools, and a new way of buying software began to take hold. Instead of buying software from a single shop, consumers could buy the best tool for the job. This in turn, led to wider adoption, as these small groups of users led the way to more lucrative enterprise deals.

The philosophical change has worked well for enterprise startups. The new world means a well-executed idea can beat an incumbent with a similar product. Just ask companies like Slack, Zoom and Box, which have shown what’s possible when you put users first.

Powered by WPeMatico

Brianne Kimmel had no trouble transitioning from angel investor to general partner.

Initially setting out to garner $3 million in capital commitments, Kimmel, in just two weeks’ time, closed on $5 million for her debut venture capital fund Work Life Ventures. The enterprise SaaS-focused vehicle boasts an impressive roster of limited partners, too, including the likes of Zoom chief executive officer Eric Yuan, InVision CEO Clark Valberg, Twitch co-founder Kevin Lin, Cameo CEO Steven Galanis, Andreessen Horowitz general partners Marc Andreessen and Chris Dixon, Initialized Capital GP Garry Tan and fund-of-funds Slow Ventures, Felicis Ventures and NFX.

At the helm of the new fund, Kimmel joins a small group of solo female general partners: Dream Machine’s Alexia Bonatsos is targeting $25 million for her first fund; Day One Ventures’ Masha Drokova raised $20 million for her debut effort last year; and Sarah Cone launched Social Impact Capital, a fund specializing in impact investing, in 2016, among others.

Meanwhile, venture capital fundraising is poised to reach all-time highs in 2019. In the first half of the year, a total of $20.6 billion in new capital was introduced to the startup market across more than 100 funds.

For most, the process of raising a successful venture fund can be daunting and difficult. For well-connected and established investors in the Bay Area, like Kimmel, raising a fund can be relatively seamless. Given the speed and ease of fund one in Kimmel’s case, she plans to raise her second fund with a $25 million target in as little as 12 months.

“The desire for the fund is to take a step back and imagine how do we build great consumer experiences in the workplace,” Kimmel tells TechCrunch.

Kimmel has been an active angel investor for years, sourcing top enterprise deals via SaaS School, an invite-only workshop she created to educate early-stage SaaS founders on SaaS growth, monetization, sales and customer success. Prior to launching SaaS School, which will continue to run twice a year, Kimmel led go-to-market strategy at Zendesk, where she built the Zendesk for Startups program.

View this post on Instagram

available offline #google #remote

A post shared by Work Life Ventures (@worklifevc) on

“You start by advising, then you start with very small angel checks,” Kimmel explains. “I reached this inflection point and it felt like a great moment to raise my own fund. I had friends like Ryan Hoover, who started Weekend Fund focused on consumer, and Alexia is one of my friends as well and I saw what she was doing with Dream Machine, which is also consumer. It felt like it was the right time to come out with a SaaS-focused fund.”

Emerging from stealth today, Work Life Ventures will invest up to $150,000 per company. To date, Kimmel has backed three companies with capital from the fund: Tandem, Dover and Command E. The first, Tandem, was amongst the most coveted deals in Y Combinator’s latest batch of companies. The startup graduated from the accelerator with millions from Andreessen Horowitz at a valuation north of $30 million.

Dover, another recent YC alum, provides recruitment software and is said to be backed by Founders Fund in addition to Work Life. Command E, currently in beta, is a tool that facilities search across multiple desktop applications. Kimmel is also an angel investor in Webflow, Girlboss, TechCrunch Disrupt 2018 Startup Battlefield winner Forethought, Voyage and others.

Work Life is betting on the consumerization of the enterprise, or the idea that the next best companies for modern workers will be consumer-friendly tools. In her pitch deck to LPs, she cites the success of Superhuman and Notion, a well-designed email tool and a note-taking app, respectively, as examples of the heightened demand for digestible, easy-to-use B2B products.

“The next generation of applications for the workplace sees people spinning out of Uber, Coinbase and Airbnb,” Kimmel said. “They’ve faced these challenges inside their highly efficient tech company so we are seeing more consumer product builders deeply passionate about the enterprise space.”

But Kimmel doesn’t want to bury her thesis in jargon, she says, so you won’t find any B2B lingo on Work Life’s website or Instagram.

She’s focusing her efforts on a more important issue often vacant from conversations surrounding investment in the future of work: diversity & inclusion.

Kimmel meets with every new female hire of her portfolio companies. Though it’s “increasingly non-scalable,” she admits, it’s part of a greater effort to ensure her companies are thoughtful about D&I from the beginning: “Because I have a very focused fund, it’s about maintaining this community and ensuring that people feel like their voices are heard,” she said.

“I want to be mindful that I am a female GP and I feel [proud] to have that title.”

Powered by WPeMatico

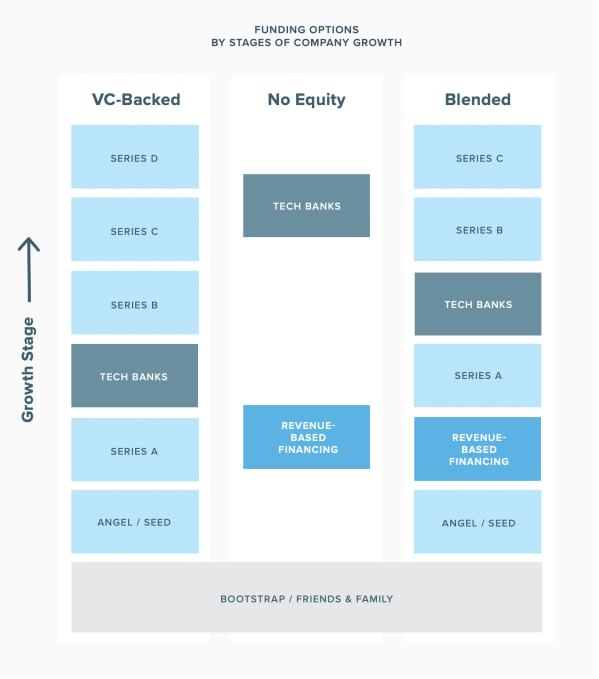

Revenue-based financing is on the rise, at least according to Lighter Capital, a firm that doles out entrepreneur-friendly debt capital.

What exactly is RBF you ask? It’s a relatively new form of funding for tech companies that are posting monthly recurring revenue. Here’s how Lighter Capital, which completed 500 RBF deals in 2018, explains it: “It’s an alternative funding model that mixes some aspects of debt and equity. Most RBF is technically structured as a loan. However, RBF investors’ returns are tied directly to the startup’s performance, which is more like equity.”

Source: Lighter Capital

What’s the appeal? As I said, RBFs are essentially dressed up debt rounds. Founders who opt for RBFs as opposed to venture capital deals hold on to all their equity and they don’t get stuck on the VC hamster wheel, the process in which you are forced to continually accept VC while losing more and more equity as a means of pleasing your investors.

RBFs, however, are better than traditional debt rounds because the investors are more incentivized to help the companies they invest in because they are receiving a certain portion of that business’s monthly revenues, typically 1% to 9%. Eventually, as is explained thoroughly in Lighter Capital’s newest RBF report, monthly payments come to an end, usually 1.3 to 2.5X the amount of the original financing, a multiple referred to as the “cap.” Three to five years down the line, any unpaid amount of said cap is due back to the investor. When all is said in done, ideally, the startup has grown with the support of the capital and hasn’t lost any equity.

At this point, they could opt to raise additional revenue-based capital, they could turn to venture capital or they could tap a tech bank to help them get to the next step. The idea is RBF is easier on the founder and it allows them optionality, something that is often lost when companies turn to VCs.

IPO corner, rapid-fire edition

Slack’s direct listing will be on June 20th. Get excited.

China’s Luckin Coffee raised $650 million in upsized U.S. IPO

Crowdstrike, a cybersecurity unicorn, dropped its S-1.

Freelance marketplace Fiverr has filed to go public on the NYSE.

Plus, I had a long and comprehensive conversation with Zoom CEO Eric Yuan this week about the company’s closely watched IPO. You can read the full transcript here.

Silicon Valley entrepreneur Hosain Rahman, the man behind Jawbone, has managed to raise $65.4 million for his new company, according to an SEC filing. The paperwork, coincidentally or otherwise, was processed while most of the world’s attention was focused on Uber’s IPO. Jawbone, if you remember, produced wireless speakers and Bluetooth earpieces, and went kaput in 2017 after burning up $1 billion in venture funding over the course of 10 years. Ouch.

On the heels of enterprise startup UiPath raising at a $7 billion valuation, the startup’s biggest investor is announcing a new fund to double down on making more investments in Europe. VC firm Accel has closed a $575 million fund — money that it plans to use to back startups in Europe and Israel, investing primarily at the Series A stage in a range of between $5 million and $15 million, reports TechCrunch’s Ingrid Lunden. Plus, take a closer look at Contrary Capital. Part accelerator, part VC fund, Contrary writes small checks to student entrepreneurs and recent college dropouts.

Our paying subscribers are in for a treat this week. Our in-house venture capital expert Danny Crichton wrote down some thoughts on Uber and Lyft’s investment bankers. Here’s a snippet: “Startup CEOs heading to the public markets have a love/hate relationship with their investment bankers. On one hand, they are helpful in introducing a company to a wide range of asset managers who will hopefully hold their company’s stock for the long term, reducing price volatility and by extension, employee churn. On the other hand, they are flagrantly expensive, costing millions of dollars in underwriting fees and related expenses…”

Read the full story here and sign up for Extra Crunch here.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about the notable venture rounds of the week, CrowdStrike’s IPO and more of this week’s headlines.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

Extra Crunch offers members the opportunity to tune into conference calls led and moderated by the TechCrunch writers you read every day. This week, TechCrunch’s Kate Clark sat down with Eric Yuan, the founder and CEO of video communications startup Zoom, to go behind the curtain on the company’s recent IPO process and its path to the public markets.

Since hitting the trading desks just a few weeks ago, Zoom stock is up over 30%. But the Zoom’s path to becoming a Silicon Valley and Wall Street darling was anything but easy. Eric tells Kate how the company’s early focus on profitability, which is now helping drive the stock’s strong performance out of the gate, actually made it difficult to get VC money early on, and the company’s consistent focus on user experience led to organic growth across different customer bases.

Eric: I experienced the year 2000 dot com crash and the 2008 financial crisis, and it almost wiped out the company. I only got seed money from my friends, and also one or two VCs like AME Cloud Ventures and Qualcomm Ventures.

nd all other institutional VCs had no interest to invest in us. I was very paranoid and always thought “wow, we are not going to survive next week because we cannot raise the capital. And on the way, I thought we have to look into our own destiny. We wanted to be cash flow positive. We wanted to be profitable.

nd so by doing that, people thought I wasn’t as wise, because we’d probably be sacrificing growth, right? And a lot of other companies, they did very well and were not profitable because they focused on growth. And in the future they could be very, very profitable.

Eric and Kate also dive deeper into Zoom’s founding and Eric’s initial decision to leave WebEx to work on a better video communication solution. Eric also offers his take on what the future of video conferencing may look like in the next five to 10 years and gives advice to founders looking to build the next great company.

For access to the full transcription and the call audio, and for the opportunity to participate in future conference calls, become a member of Extra Crunch. Learn more and try it for free.

Kate Clark: Well thanks for joining us Eric.

Eric Yuan: No problem, no problem.

Kate: Super excited to chat about Zoom’s historic IPO. Before we jump into questions, I’m just going to review some of the key events leading up to the IPO, just to give some context to any of the listeners on the call.

Powered by WPeMatico

When Zoom hit the public markets Thursday, its IPO pop, a whopping 81 percent, floored everyone, including its own chief executive officer, Eric Yuan.

Yuan became a billionaire this week when his video conferencing business went public. He told Bloomberg that he actually wished his stock hadn’t soared quite so high. I’m guessing his modesty and laser focus attracted Wall Street to his stock; well, that, and the fact that his business is actually profitable. He is, this week proved, not your average tech CEO.

I chatted with him briefly on listing day. Here’s what he had to say.

“I think the future is so bright and the stock price will follow our execution. Our philosophy remains the same even now that we’ve become a public company. The philosophy, first of all, is you have to focus on execution, but how do you do that? For me as a CEO, my number one role is to make sure Zoom customers are happy. Our market is growing and if our customers are happy they are going to pay for our service. I don’t think anything will change after the IPO. We will probably have a much better brand because we are a public company now, it’s a new milestone.”

“The dream is coming true,” he added.

For the most part, it sounded like Yuan just wants to get back to work.

Want more TechCrunch newsletters? Sign up here. Otherwise, on to other news…

You thought I was done with IPO talk? No, definitely not:

While I’m on the subject of Uber, the company’s autonomous vehicles unit did, in fact, raise $1 billion, a piece of news that had been previously reported but was confirmed this week. With funding from Toyota, Denso and SoftBank’s Vision Fund, Uber will spin-out its self-driving car unit, called Uber’s Advanced Technologies Group. The deal values ATG at $7.25 billion.

The TechCrunch staff traveled to Berkeley this week for a day-long conference on robotics and artificial intelligence. The highlight? Boston Dynamics CEO Marc Raibert debuted the production version of their buzzworthy electric robot. As we noted last year, the company plans to produce around 100 models of the robot in 2019. Raibert said the company is aiming to start production in July or August. There are robots coming off the assembly line now, but they are betas being used for testing, and the company is still doing redesigns. Pricing details will be announced this summer.

#TCRobotics pic.twitter.com/Vf4kUWH0fR

— Lucas Matney (@lucasmtny) April 19, 2019

Digital health investment is down

Despite notable rounds for digital health businesses like Ro, known for its direct-to-consumer erectile dysfunction medications, investment in the digital health space is actually down, reports TechCrunch’s Jonathan Shieber. Venture investors, private equity and corporations funneled $2 billion into digital health startups in the first quarter of 2019, down 19 percent from the nearly $2.5 billion invested a year ago. There were also 38 fewer deals done in the first quarter this year than last year, when investors backed 187 early-stage digital health companies, according to data from Mercom Capital Group.

Byton loses co-founder and former CEO, reported $500M Series C to close this summer

Lyric raises $160M from VCs, Airbnb

Brex, the credit card for startups, raises $100M debt round

Ro, a D2C online pharmacy, reaches $500M valuation

Logistics startup Zencargo gets $20M to take on the business of freight forwarding

Co-Star raises $5M to bring its astrology app to Android

Y Combinator grad Fuzzbuzz lands $2.7M seed round to deliver fuzzing as a service

Hundreds of billions of dollars in venture capital went into tech startups last year, topping off huge growth this decade. VCs are reviewing more pitch decks than ever, as more people build companies and try to get a slice of the funding opportunities. So how do you do that in such a competitive landscape? Storytelling. Read contributor’s Russ Heddleston’s latest for Extra Crunch: Data tells us that investors love a good story.

Plus: The different playbook of D2C brands

And finally, for the first of a new series on VC-backed exits aptly called The Exit. TechCrunch’s Lucas Matney spoke to Bessemer Venture Partners’ Adam Fisher about Dynamic Yield’s $300M exit to McDonald’s.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about rounds for Brex, Ro and Kindbody, plus special guest Danny Crichton joined us to discuss the latest in the chip and sensor world.

Powered by WPeMatico

Zoom, the only profitable unicorn in line to go public, priced its initial public offering at between $28 and $32 per share Monday morning. The video conferencing business plans to trade on the Nasdaq under the ticker symbol “ZM.”

Zoom, valued at $1 billion in 2017, initially filed to go public in March. According to its amended IPO filing, the company will raise up to $348.1 million by selling 10.9 million Class A shares. The offering will grant Zoom a fully diluted market value of $8.7 billion, a more than 8x increase to its latest private market valuation.

Although the company has garnered praise for its stellar financials — Zoom posted $330 million in revenue in the year ending January 31, 2019, a remarkable 2x increase year-over-year, with a gross profit of $269.5 million — the road to IPO hasn’t been without hiccups.

The company’s founder and chief executive officer Eric Yuan last night published an open letter concerning the conduct of Zoom’s chief financial officer Kelly Steckelberg. According to the letter, Zoom was recently informed by an anonymous source that Steckelberg had an “undisclosed, consensual relationship” during her tenure at a previous employer.

Steckelberg was most recently the CEO of the online dating site Zoosk; before that, she was a senior director in consumer finance at Cisco . The letter does not specify where the relationship took place, when or with whom.

Losing a CFO mere days before an IPO would have been a major loss for Zoom. CFOs often become the face of the IPO, handling the grueling tasks associated with crafting an IPO prospectus, leading the roadshow and more, while also maintaining day-to-day financial operations.

Yuan writes that the Zoom’s board of directors conducted a full investigation into the matter and determined that Steckelberg would stay on as Zoom’s CFO: “Kelly expressed regret for what transpired at her former employer, took ownership for the situation, and made clear to us that she had learned valuable lessons from the experience,” he wrote.

“We appreciated Kelly’s openness and candor during this process,” he continued. “It is clear that this matter related only to circumstances at her former employer. During Kelly’s tenure at Zoom, she has been an incredible contributor, as well as a model steward of our culture, values, and high standards since joining the Company.”

We reached out to Zoosk for comment. Zoom declined to comment further.

Zoom, expected to make the final call on its IPO price next Wednesday, will likely price at the top of the range and see a clean pop on its first day on the markets given its clean track record and positive financials. The business was founded in 2011 by Eric Yuan, an early engineer at WebEx, which sold to Cisco for $3.2 billion in 2007. Before launching Zoom, he spent four years at Cisco as its vice president of engineering.

Zoom has raised $145 million to date from investors, including Emergence Capital, which owns a 12.2 percent pre-IPO stake; Sequoia Capital (11.1 percent pre-IPO stake); Digital Mobile Venture (8.5 percent), a fund affiliated with former Zoom board member Samuel Chen; and Bucantini Enterprises Limited (5.9 percent), a fund owned by Li Ka-shing, a Chinese billionaire and among the richest people in the world.

Morgan Stanley, JP Morgan and Goldman Sachs are leading its offering.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

What a Friday. This afternoon (mere hours after we released our regularly scheduled episode no less!), both Pinterest and Zoom dropped their public S-1 filings. So we rolled up our proverbial sleeves and ran through the numbers. If you want to follow along, the Pinterest S-1 is here, and the Zoom document is here.

Got it? Great. Pinterest’s long-awaited IPO filing paints a picture of a company cutting its losses while expanding its revenue. That’s the correct direction for both its top and bottom lines.

As Kate points out, it’s not in the same league as Lyft when it comes to scale, but it’s still quite large.

More than big enough to go public, whether it’s big enough to meet, let alone surpass its final private valuation ($12.3 billion) isn’t clear yet. Peeking through the numbers, Pinterest has been improving margins and accelerating growth, a surprisingly winsome brace of metrics for the decacorn.

Pinterest has raised a boatload of venture capital, about $1.5 billion since it was founded in 2010. Its IPO filing lists both early and late-stage investors, like Bessemer Venture Partners, FirstMark Capital, Andreessen Horowitz, Fidelity and Valiant Capital Partners as key stakeholders. Interestingly, it doesn’t state the percent ownership of each of these entities, which isn’t something we’ve ever seen before.

Next, Zoom’s S-1 filing was more dark horse entrance than Katy Perry album drop, but the firm has a history of rapid growth (over 100 percent, yearly) and more recently, profit. Yes, the enterprise-facing video conferencing unicorn actually makes money!

In 2019, the year in which the market is bated on Uber’s debut, profit almost feels out of place. We know Zoom’s CEO Eric Yuan, which helps. As Kate explains, this isn’t his first time as a founder. Nor is it his first major success. Yuan sold his last company, WebEx, for $3.2 billion to Cisco years ago then vowed never to sell Zoom (he wasn’t thrilled with how that WebEx acquisition turned out).

Should we have been that surprised to see a VC-backed tech company post a profit — no. But that tells you a little something about this bubble we live in, doesn’t it?

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

The video conferencing company Zoom is aiming to file a public S-1 by the end of March, according to a new report in Business Insider that adds the company could go public as soon as April.

Business Insider reported last month that Zoom had filed confidentially with the SEC to go public, just months after Reuters reported that the San Jose, Calif.-based company had chosen investment bank Morgan Stanley to lead its eventual IPO.

We’ve reached out to the company for comment.

Zoom was valued at $1 billion when it raised its last funding in 2017 in the form of a $100 million check from Sequoia Capital. Reuters sources have said they expect the company to be valued at several billion dollars at the IPO.

The company, founded in 2011, has raised $145 million altogether, including from Emergence Capital and Horizons Ventures. Its earliest backers include Qualcomm Ventures, Yahoo founder Jerry Yang, WebEx founder Subrah Iyar and former Cisco SVP Dan Scheinman, who has been an active angel investor for years.

We had a chance to sit down with CEO Eric Yuan last year at a small industry event hosted by the venture firm NextWorld Capital. He talked about coming to the United States as a student from China and applying for a U.S. visa nine times over the course of two years before finally receiving it and arriving in Silicon Valley in 1997. We also talked about his experience as the 10th employee of WebEx, and his frustration that the company’s code remained stubbornly unchanged after it was sold for $3.2 billion to Cisco in 2007.

He wasn’t alone, clearly. When Yuan struck out on his own to found Zoom, fully 45 employees from WebEx joined him, a decision for which they’re likely thankful now. Financial rewards aside, Yuan was ranked at the top of Glassdoor’s annual list of best-rated CEOs last year.

We’ll be able to take a deeper dive into the health of Zoom once its reported S-1 is made public. In the meantime, you can check out our chat here.

Powered by WPeMatico