entrepreneurship

Auto Added by WPeMatico

Auto Added by WPeMatico

Although older adults are one of the fastest-growing demographics, they’re quite underserved when it comes to consumer tech.

The global population of people older than 65 will reach 1.5 billion by 2050, and members of this cohort — who are leading longer, active lives — have plenty of money to spend.

Still, most startups persist in releasing products aimed at serving younger users, says Lawrence Kosick, co-founder of GetSetUp, an edtech company that targets 50+ learners.

“If you can provide a valuable, scalable service for the older adult market, there’s a lot of opportunity to drive growth through partnerships,” he notes.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Image Credits: Sukhinder Singh Cassidy

On Thursday, August 19, Managing Editor Danny Crichton will interview Sukhinder Singh Cassidy, author of “Choose Possibility,” on Twitter Spaces at 2 p.m. PDT/5 p.m. EDT/9 p.m. UTC.

Singh Cassidy, founder of premium talent marketplace theBoardlist, will discuss making the leap into entrepreneurship after leaving Google, her time as CEO-in-Residence at venture capital firm Accel Partners and the framework she’s developed for taking career risks.

They’ll take questions from the audience, so please add a reminder to your calendar to join the conversation.

Thanks very much for reading Extra Crunch this week! Have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

I want to extend an offer to an engineer who has been working in the U.S. on an H-1B for almost five years. Her current employer is sponsoring her for an EB-2 green card, and our startup wants to hire her as a senior engineer.

What happens to her green card process? Can we take it over?

— Recruiting in Richmond

Image Credits: Dmitrii_Guzhanin (opens in a new window) / Getty Images

In a candid guest post, Scott Lenet, president of Touchdown Ventures, writes about the cognitive dissonance currently plaguing venture capital.

Yes, there’s an incredible amount of competition for deals, but there’s also a path to bringing soaring startup valuations back to earth.

For example, early investors have an inherent conflict of interest with later participants and many VCs are thirsty “logo hunters” who just want bragging rights.

At some point, “venture capitalists need to stop engaging in self-delusion about why a valuation that is too high might be OK,” writes Lenet.

Image Credits: Getty Images under a GK Hart/Vikki Hart (opens in a new window) license.

Aesop’s fable about the determined tortoise who defeated an arrogant hare has many interpretations, e.g., the value of perseverance, the virtue of taking on bullies, how an outsized ego can undermine natural talent.

In the case of venture capital, the allegory is relevant because a slow, steady and more personal approach generates better outcomes, says Marc Schröder, managing partner of MGV.

“We simply must take the time to get to know founders.”

Image Credits: Getty Images under a jayk7 (opens in a new window) license.

As the pandemic changed consumer behavior and regulations began to reshape digital marketing tools, advertisers are turning to retail media.

Using the reams of data collected at the individual and aggregate level, retail media produce high-margin revenue streams. “And like most things, there is a bad, a good and a much better way of doing things,” advises Cynthia Luo, head of marketing at e-commerce marketing stack Epsilo.

Image Credits: Nigel Sussman (opens in a new window)

“We lied when we said that The Exchange was done covering 2021 venture capital performance,” Anna Heim and Alex Wilhelm admit.

Yesterday, they reviewed a detailed report from NYC-based VC group Work-Bench on the city’s enterprise tech startups.

“New York City’s enterprise footprint is now large enough that it must be considered a leading market for the startup varietal,” Anna and Alex conclude, “making its results a bellwether to some degree.”

“And if New York City is laying the groundwork for a huge wave of unicorn exits in the coming four to eight quarters, we should expect to see something similar in other enterprise markets around the world.”

Image Credits: PM Images (opens in a new window) / Getty Images

Given the rapid pace of digital transformation, nearly every business will eventually migrate some — or most — aspects of their operations to the cloud.

Before making the wholesale shift to digital, companies can start getting comfortable by using disaster recovery as a service (DRaaS). Even a partially managed DRaaS can make an organization more resilient and lighten the load for its IT team.

Plus, it’s also a savvy way for tech leaders to get shot-callers inside their companies to get on board the cloud bandwagon.

Image Credits: PeopleImages (opens in a new window) / Getty Images

“The decisions of government, the broader legal system and its combined level of scrutiny toward a particular subject” can affect market timing and the durability of an idea, Noorjit Sidhu, an early-stage investor at Plug & Play Ventures, writes in a guest column.

There are three areas currently facing regulatory scrutiny that have the potential to “provide outsized returns,” Sidhu writes: taxes, telemedicine and climate.

Image Credits: Nigel Sussman (opens in a new window)

“China’s technology scene has been in the news for all the wrong reasons in recent months,” Anna Heim and Alex Wilhelm write about the Chinese government’s crackdown on a host of technology companies.

“The result of the government fusillade against some of the best-known companies in China was falling share prices,” they write.

But has it affected the venture capital market? SoftBank this week said it would pause investments in China, but the numbers through Q2 indicate China is steadier than Alex and Anna expected.

Image Credits: Westend61 (opens in a new window) / Getty Images under a license.

If you’re a startup founder, odds are, at some point, you’ll raise a Series A (and B and C and D, hopefully), perform a strategic acquisition, and maybe even sell your company.

When those things occur, you’ll need to know how to do a quality of earnings (QofE) to maximize value, Pierre-Alexandre Heurtebize, investment and M&A director at HoriZen Capital, writes in a guest column.

He walks through a framework for thinking and organizing a QofE for “every M&A and private equity transition you may be part of.”

Image Credits: Getty Images under a akinbostanci (opens in a new window) license.

“What was once solely an internal project at Google has since been open-sourced and has become one of the most talked about technologies in software development and operations,” Ben Ofiri, the co-founder and CEO of the Kubernetes troubleshooting platform Komodor, writes of Kubernetes, which he calls “the new Linux.”

“This technology isn’t going anywhere, so any platform or tooling that helps make it more secure, simple to use and easy to troubleshoot will be well appreciated by the software development community.”

Powered by WPeMatico

The technology industry is often thought of as being the domain of the young and the new. We see an emphasis on young founders (“40 Under 40”), innovative ideas and disruptive challenges to legacy brands, incumbent companies and “old” ways of thinking.

But one of the things I’ve learned on my journey in co-founding my latest startup is that technology should be enabling and accessible to all, and nowhere is this more critical than for empowering our older adults.

Older adults are one of the most underrepresented audiences for new technology products and platforms. There is a massive opportunity to provide products and services that will make life better for today’s seniors and future generations of older adults to come. Founders in every space, from edtech to healthcare, from financial services to robotics, can make a bigger impact if we recognize the opportunity of being of service to older adults.

One of the best strategies for tech companies that want to serve the older adult market is to focus your value proposition on empowering older adults.

Older adults often get overlooked by tech companies. In fairness, it can be hard (and insensitive and uninspiring) to market products and services as being “for old people,” because people in this group don’t tend to think of themselves as “old.”

One of the best strategies for tech companies that want to serve the older adult market is to focus your value proposition on empowering older adults. Don’t make a product “for old people” — make a product that helps older adults lead a healthier, more active, more connected life.

Whether it’s the education tech space, financial services, health tech, consumer products or other innovative digital services for seniors, tech companies have big opportunities to empower older adults.

We are seeing some great examples, including:

Older adults have so much to offer. Instead of approaching this market as a “problem” to be solved, startups should engage with older adults as an active, curious, ready-to-learn group of people who are eager to be empowered.

It often seems like so many consumer-facing apps today are created for younger people. But there’s a big disconnect between where so much of the tech industry’s attention and investment is going and the spending power and lifestyle preferences of today’s older adults.

Older adults are the most underserved demographic for the tech world. They’re also one of the fastest-growing age cohorts. The number of people worldwide who are 65 and older is expected to grow from 524 million in 2010 to 1.5 billion in 2050.

The “silver economy,” driven by the spending power of older adults, is expected to grow into the 2030s because the senior population is the wealthiest age group and their numbers are growing 3.2% per year (compared with 0.8% for the overall population).

Powered by WPeMatico

Many VCs tout their mentorship and hands-on approach to founders, especially those who run early-stage startups. But in the recent era of lightning-fast rounds closing at sky-high valuations, the cap tables of early-stage startups are becoming increasingly crowded.

This isn’t to say that the value VCs bring has diminished. If anything, it’s quite the opposite — this new dynamic is forcing founders to be extremely selective about exactly who is sitting around their mentorship table. It’s simply not possible to have numerous deep and meaningful relationships to extract maximum value at the early stage from seasoned investors.

Founders should definitely pursue big rounds at sky-high valuations, but it’s important that they recognize how important it is to manage who they allow into their mentorship circles. Initially, founders should make sure their first layer consists of the real “doers” — usually angels and early venture investors who founders meet with weekly (or more frequently) to help solve some of the most granular problems.

Everything from hiring to operational hurdles all the way to deeper, more personal challenges like balancing family life with a rapidly growing startup.

This circle is where the real mentorship happens, where founders can be open and vulnerable. For obvious reasons, this circle has to be small, and usually consist of two to six people at most. Anything more simply becomes unwieldy and leaves founders spending more time managing these relationships than actually building their company.

How founders manage their VC circles can mean the difference in success or failure for a thousand different reasons.

The second layer should consist of the “quarterly crowd” of investors. These aren’t necessarily people who are uninterested or unwilling to participate in the nitty gritty of running the company, but this circle tends to consist of VCs who make dozens of investments per year. They, like their founders, aren’t capable of managing 50 relationships on a weekly basis, so their touch points on company issues tend to move slower or less frequently.

Powered by WPeMatico

In a company’s early days, the difference between C-level executives and the rest of the organization is simple — employees can walk away from a failure, but the leaders cannot. Under these conditions, certain kinds of people thrive in leadership roles and can take a company from ideation to production.

While there’s no magic formula for what works and what doesn’t, successful startups share common traits in terms of the way their foundational leadership teams are built.

We’ve all experienced what it looks like on the negative end of the spectrum — people making points simply to hear their own voice, leaders competing for credit and clashing agendas. When people would rather be heard than contribute, the output suffers. Members of a healthy leadership team are unafraid to let others have the limelight, because they trust the mission and the culture they’ve built together.

An honest self-assessment is necessary and this is something that only exceptional and selfless founders are capable of.

We are all imperfect human beings, founders included. There are always going to be moments that leaders can’t predict, and mistakes come with the territory. The right leadership team should be able to mitigate the unexpected, and sometimes make the future easier to predict. Putting the right people in the right roles early on can be the difference between success and failure — and that starts at the top.

Investors love founder-CEOs, and founders are often fantastic candidates for this role. But not everyone can do it well, and more importantly, not everyone wants to.

Startup founders should ask themselves a few questions before they lose sleep over the prospect of handing over the reigns:

An honest self-assessment is necessary and this is something that only exceptional and selfless founders are capable of. In many cases, founders decide they need outside help to fill the role. While a CEO may not be your first hire — or even one of the first five — the person you choose will ultimately occupy your organization’s most critical leadership role, so choose wisely.

What to look for: Ambitious vision grounded in execution reality. Your CEO should have hands-on experience that allows them to see around corners, predict pitfalls and identify opportunities.

What to watch out for: Leaders who lack respect for the founding vision or the ability to hire and balance an executive team quickly. A good CEO should be able to manage short-term cash flow and go-to-market needs without compromising the true north, while building a foundation and culture for the long term.

Powered by WPeMatico

I was four years old when my dad first showed me a computer. I immediately asked him if we could take it apart to see how it worked. I was hooked.

When I learned that Windows and Mac were based in the United States, I was 10. Since then, I’ve wanted to come here to launch my own tech business.

What I didn’t realize back then was that the first half of that dream — coming to the U.S. — would provide me with essential training for realizing the second half — launching a business.

As it turns out, the behaviors, attitude and mindset required to traverse the U.S. immigration system are many of the same ones required to navigate the uncertain waters of entrepreneurship.

The behaviors, attitude and mindset required to traverse the U.S. immigration system are many of the same ones required to navigate the uncertain waters of entrepreneurship.

In 2019, I launched Preflight, which makes smart and fast no-code test automation software for web applications. One big reason the business currently exists is that, in my journey to getting asylee status in the United States, I became really good at three things: accepting uncertainty, building resilience and maintaining a positive mental attitude.

I needed them all to get Preflight off the ground.

I had my first shot at making my longtime dream a reality when I was applying to college as an undergraduate. I figured if I could go to school in the United States, I could find a way to stay and start a business.

After doing some research, though, I realized that U.S. colleges were too expensive.

But I figured getting out of Turkey, my home country, would be a start. I looked around for affordable schools and saw that France had good options. So I went to France.

Unfortunately, even after three attempts, I wasn’t able to get a student visa. So I headed back to Turkey and went to college there. After graduation, I knew I had a second shot at the U.S.: a master’s degree. I applied to computer science programs and got accepted — a huge win!

I first arrived in Georgia, where I got my TOEFL certification, then enrolled at Tennessee State University, where I got a teaching assistantship.

Keep in mind, to do all this, I had to have the right visas. I needed a student visa for my master’s degree, but if I wanted to work after graduation, I’d need a work visa.

The thing is, though, I didn’t want to work at a “job.” I wanted to start my own business, which requires a different type of visa altogether.

Oh, and there was another factor at play: I was enrolled at Tennessee State from 2014 to 2016, during the lead-up to the election of Donald Trump. So in addition to trying to figure out which visa I could reasonably get, I had to deal with the fact that the rules for visas could all change in the coming months.

These experiences are similar to what many founders deal with every day in the process of launching and running a business.

We don’t know if our products will work or if they’ll find a market. We don’t know how changing regulations might affect what we’re doing. We have no idea when something like a pandemic will pull the rug out from everything we’ve built.

But we keep going anyway. In my experience, the most successful founders are the ones who don’t wait for all the pieces to fall into place — they know that will never happen. They’re the ones who do the best they can with what they have. They trust that they’ll be able to adapt and adjust when things inevitably change.

Which brings me to my next lesson.

Hearing “no” isn’t fun, especially when that “no” is about something you’ve wanted for more than a decade.

I experienced a lot of “no”s in my immigration journey, as one visa attempt after another failed. If I’d let any one of those failures stop me, I wouldn’t be where I am today — working at my own startup in the U.S.

The lesson I learned was to hear “no” as “not yet.” It’s been invaluable to me in my journey to becoming a founder.

For example: In 2014, while I was in graduate school, I learned about Y Combinator and decided that I wanted to be a part of it. Throughout grad school, I applied and got rejected three times.

The clock was ticking on my student visa, so I decided to shift my tactics. I applied to jobs at companies that were Y Combinator graduates to see what I could learn.

In 2016, I got hired at ShipBob, a Chicago-based company that was in Y Combinator’s Summer 2014 batch. I joined the team as its first full-time developer and the first one based in the States. From there, things changed dramatically.

For starters, I learned a lot. In my time with ShipBob — just two and a half years — we grew from 10 people to more than 400. I built two apps and applied to Y Combinator twice more and got rejected both times.

But in my work growing and leading a team of developers, I saw a need for a product that didn’t yet exist: a smart, fast, no-code test automation tool.

My team was spending way too much time building tests for ShipBob’s latest updates to make sure existing functionalities worked when we deployed. But when the code changed too quickly, our tests were outdated. It was incredibly frustrating.

Then we hired two quality assurance engineers and it took them four months to get 10% automated test coverage.

These problems led me to an aha moment: I could build a company to address this. A tool that is fast in test creation and can adapt to the UI changes.

That company is Preflight, and it’s the one that finally got me admitted to Y Combinator in the Winter 2019 batch. I was ecstatic when I heard that we’d been accepted. But then I realized that I couldn’t actually work on Preflight full time with my current visa status — at least, if I wanted to one day make a salary, I couldn’t.

And that brings me to my next point.

My professional life wasn’t the only thing that changed dramatically while I was at ShipBob. My immigration status also evolved.

ShipBob applied for and got me an H-1B visa, which made me eligible to work in the U.S.

But when I got accepted to Y Combinator on my sixth application, I knew I needed an alternative: If I left ShipBob to run Preflight, I would lose my H-1B and my ability to work in the U.S.

This kind of conundrum is all too familiar to most startup founders: There’s no new opportunity without a new challenge to accompany it.

So I did what any founder would do: I focused on the positive (I’d gotten into YC!) and dedicated myself to figuring out a different way to stay in the country.

First, I tried to apply for the EB-1 visa, but the required documentation was too burdensome. I don’t think any founder could prepare for that application without several months of preparation.

Then I tried the O-1. No luck.

So I asked ShipBob if I could take an unpaid sabbatical, which would let me keep my H-1B status while I attended Y Combinator and worked on Preflight. They agreed. My brothers, who had both moved to Chicago and started working at ShipBob (you’re welcome, guys!) agreed to support me (thanks, guys!).

Finally, I had a solution that worked — but only for the time being. If Preflight was successful, I’d have to find a different way to stay in the country.

Transferring my H-1B to Preflight wouldn’t work, in part because it would require me to yield 70% to 80% ownership to my co-founder and agree that he could fire me at any time.

But there was another option I’d been reluctant to lean on: asylee status. In 2016, there was an attempted coup in Turkey (that’s the official story, anyway). I won’t get into the political details, but my family and I were supporters of the movement blamed for the attempt. As a result, we were at risk of imprisonment if we stayed in Turkey — and eligible for asylum status in the U.S.

I applied, but hoped that I’d land a work visa in the meantime, partly because asylum status can take years to get approved and partly because there was no telling whether the current administration would change the rules to make me ineligible before my status came through.

When I got accepted to Y Combinator, my asylum status was pending. When my initial sabbatical from ShipBob ran out, it was still pending. I asked for an extension and got it (thanks, ShipBob!). A few months later, I figured I could not get the visa sorted. I wanted to focus on my business and use asylum-pending status, which would give me work authorization for two years. I was therefore able to work on and take a salary from Preflight.

My asylum was granted early this year, four years after applying. Getting asylee status was a big win because it meant I could realize my dream of running a business in the U.S. So I was, in some ways, at the resolution of my immigration journey — but I was just at the beginning of my journey as a founder.

Right away, I had my first experience applying all the lessons I’d learned in the last six years: We wanted to raise our first funding round. That funding would let me start taking a salary.

All told, we approached more than 100 VCs before we got a yes. But we did get that yes, and we raised a seed round of $1.2 million in September 2019.

It was a big win for Preflight, but it didn’t have the transformational power for the company I’d hoped for. That’s because, after closing our round, we didn’t focus on sales and marketing to the extent that we should have.

After several months of frustrating results, I consulted with my advisers about how to proceed. They offered me insight that seemed obvious once I had it — but that I may not have gotten on my own — which was discussing everything that’s happening internally with the investors. And the outcome was me being the CEO.

In the month and a half after I adjusted course based on my vision, I grew Preflight’s revenue 600% in just about two months.

The whole startup ethos of disrupting what’s not working to improve people’s lives is based on the premise that the world is constantly changing. The global disruption caused by COVID-19 underscored that in a major way.

Founders who accept that change is inevitable and who embrace uncertainty, develop resilience for when things go wrong, and maintain a positive mental attitude about the ups and (especially) the downs of running a startup will be the ones who succeed for the long haul.

I’ve known since I was 10 that I wanted to run a company in the United States. Given the choice, I would have opted for a much smoother road to entrepreneurship. But what I’ve discovered is that the difficult immigration path I had to follow provided exactly the training I needed to succeed in the challenging role of a founder.

Powered by WPeMatico

The startup world can be a rollercoaster. While investment continues to pour in — with both founders and investors looking for the next unicorn — the reality is that 90% of startups fail, with over half of those going under in the first three years.

I’ve founded two companies that I grew and sold (Mezi and Dhingana). I encountered many of the issues that new founders face, learned on the job, and thankfully persevered. Using the knowledge that I acquired in my previous companies, I’ve founded a third — Zeni — to try and help founders make more informed, sustainable financial decisions.

For many founders, a transformative idea and initial outside investment doesn’t translate into understanding the underlying financial complexities of running a business.

Whether you’re just wrapping your seed round, or on to Series B, avoiding these common issues is the best way to ensure that you’re set on solid ground and free to focus on your vision.

Startups go under for a variety of reasons. Some fail to achieve product-market fit in a scalable way. Many others simply run out of money. While the above two reasons are often cited as the two primary reasons for startup failure, they’re also related. If you don’t solve a market problem and don’t generate customers, you’re eventually going to run out of money.

Unfortunately, many of the startups that fail shouldn’t. They’re led by bright entrepreneurs with a great idea. But for many founders, a transformative idea and initial outside investment doesn’t translate into understanding the underlying financial complexities of running a business.

When you break down the various complexities founders face in understanding business finances, there are three primary hurdles they face:

All of the above issues put increased workload and strain on founders, which can lead to burnout. Owners, on average, spend around 40% of their working hours on tasks like hiring, HR and payroll. While hiring is integral to a founders’ day-to-day role, other administrative tasks related to finance, HR and payroll distract founders from focusing on their overall vision and goals.

The good news is that by being aware of the above issues, you can solve them and eliminate the consequences of burnout, distraction and, ultimately, failure. Let’s talk about how.

The financial decision-making and tasks of most startups start and stop with the founder. This means that bookkeeping, bill paying, invoicing, financial projections, employee payments and taxes all run into a bottleneck. Even worse, each of these functions requires another employee, vendor or third-party expert — finance firms, admins, CFOs, CPA firms — each using its own software and applications to accomplish their goals.

Each of these parties is reporting back up to the founder, who is then in charge of making sense of it all and disseminating the information to the entities that need it. This means that not only is everything slower, but often things fall through the cracks, as communication can become a serious issue.

Worse still, this creates cash flow problems, as bills go unpaid, invoices go unsent, and important financial documents are delayed. I’ve seen revenue go unreported and invoices unsent and uncollectable due to the fragmentation-bottleneck system most founders experience.

Powered by WPeMatico

Though 2021 is far from over, it’s already witnessed a record level of venture capital activity in the technology sector. With larger round sizes announced daily, founders may have their pick of term sheets — but they need to think critically and strategically about which firms to add to their cap table.

So far this year, we’ve seen $292.4 billion in venture financing across the globe, of which $138.9 billion was raised in the United States. Specific to tech companies, the capital is only accelerating: In Q2, founders raised 157% more capital compared to the same period last year, according to the latest data from CB Insights.

It’s not just that more companies are raising money — they are doing so at a higher valuation. Median seed and Series A stage valuations today stand at $12 million and $42 million, respectively, up 20% to 30% from 2020. This can be partly attributed to growing exits/M&A activity in the technology sector, a record number of IPOs and a general bullishness around technology, as well as low interest rates and liquidity in the market.

Good VCs who are aligned with a startup’s vision create more value than the dollars they bring to the table.

At a time when we are witnessing record VC activity, founders would be well served to go back to the basics and focus on the principles of fundraising when determining who sits on their cap table. Here are a few pointers for founders in that direction:

Good VCs who are aligned with a startup’s vision create more value than the dollars they bring to the table. Typically, such value is created across a few distinct functions — product, sales, domain expertise, business development and recruiting, to name a few — based on the background of the partners of the fund and the composition of their limited partners (investors in the venture fund).

Further, the right VC can serve as an authentic, objective sounding board for CEOs, which can be an asset to have as a startup navigates uncertainty and the typical challenges that come with scaling a young company. As founders assess multiple term sheets, it’s worth thinking through whether they should optimize for VCs who offer the highest valuation, or for ones who bring the most value to the table.

Running an efficient fundraising process, in part, entails holding VCs accountable to their own diligence requests. While it is unfortunately common for VCs to request a lot of data upfront, startups should share information after assessing intent and appetite on the investors’ part.

For every additional data request, founders are well within their rights (and should) check with their potential investors on where the process stands and get indicative timelines for moving forward with next steps. Mark Suster said it best: “Data rooms are where fundraising processes go to die.”

Powered by WPeMatico

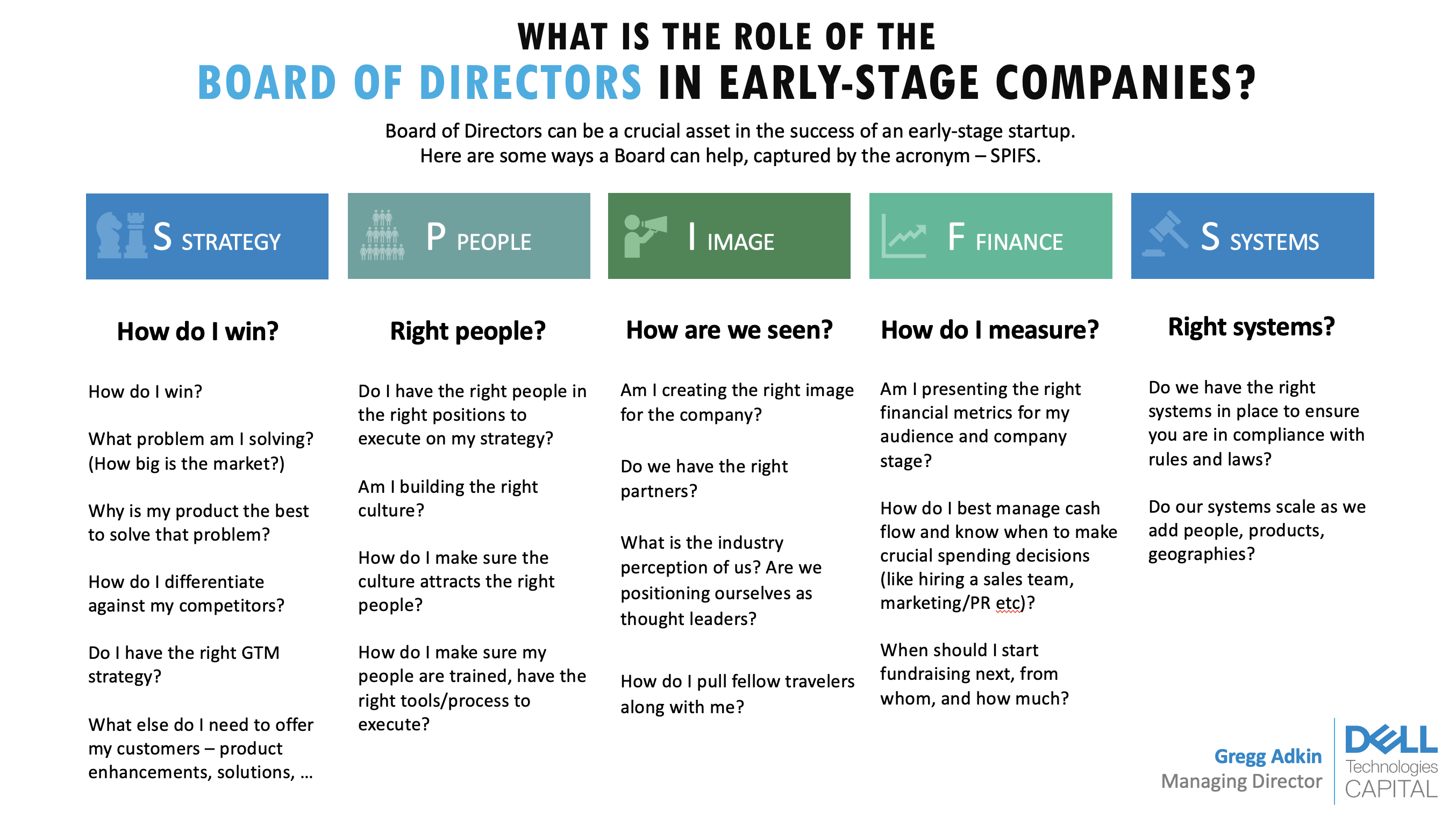

What’s the board’s role in an early-stage startup?

Startup founders frequently ask me about the role of a board of directors. A board can be a crucial asset in an early-stage startup.

Here’s a framework for how it can help drive success at your company: Strategy, People, Image, Finance and Systems for compliance, or “SPIFS.”

The board of directors helps with governance of the company. U.S. law requires that any company have one, though does not require how big it should be. By generic definition, the board of directors consists of elected individuals that represent shareholders. It is the governing body that provides company oversight and helps set business policy and strategy.

On a more practical level and in a startup environment, the board can aid in creating a successful business strategy, putting together the right management team, developing branding, building good financial habits, and avoiding legal and compliance issues. The needs and composition of the board will change depending on the startup’s stage, management and financing history (e.g., if there are preferred shareholders, investors that require a board seat and more).

Investors often ask founders about their board: It says a lot about their character, their judgment and their willingness to be challenged.

Investors often ask founders about their board for two reasons. First, it says a lot about their character, their judgment and their willingness to be challenged. The founder can typically choose who is on their board (through careful selection of investors and advisers) and negotiate a board structure they prefer.

Typically, a healthy board will have a good balance between common shareholders, preferred shareholders and independents. It also helps investors and analysts understand who will ask critical questions and give important advice to the company’s executive management, especially when the going gets tough (it inevitably does!).

After 20 years as a venture capitalist and board member, I boiled down the value of a board into five main pieces under the acronym SPIFS: Strategy, People, Image, Finance and Systems for compliance.

Image Credits: Dell Technologies Capital

Setting business strategy is one of the main ways that the board helps founders, especially if it’s their first time running a business. It is a valuable sounding board for validating that you have taken a sober account of the market and have the right plan to develop your product and acquire customers.

The board should ask these questions when guiding founders through setting strategy:

Powered by WPeMatico

The future of technology is determined by a handful of venture capitalists. The world’s 10 leading venture capital firms have, together, invested over $150 billion in technology startups. The venture capitalists who run these firms decide which startups today will develop the new platforms and technologies that will shape our lives tomorrow.

There is a startling lack of diversity within the venture capital sector. This means that a small group of men — mostly white men — make decisions that affect all of us. Unsurprisingly, they all too often ignore the broader societal and human rights implications of these investment decisions.

We all live in a world shaped by venture capital. As of 2019, 81% of all venture capital funds worldwide are clustered in just a handful of countries, primarily in the U.S., Europe and China, which in turn are shaping the future of technology. If you spend time on Facebook or Twitter, use Google, travel in an Uber or stay in an Airbnb, then you’ve experienced firsthand the impact of venture capital funding.

Venture capital firms, which provide equity financing for early- and growth-stage startups, play a critical gatekeeper role, deciding which new technologies and technology companies will receive funding.

Venture capital firms need to institute human rights due diligence processes that meet the standards set forth in the UN Guiding Principles on Business and Human Rights.

All businesses — including venture capital — have a responsibility to respect human rights. In order to ensure that their investments are not undermining our human rights, it is therefore critical for venture capital firms to conduct due diligence processes before making investments.

Amnesty International recently surveyed the world’s largest venture capital firms and startup accelerators. Of the world’s 10 largest venture capital firms, not a single one had an adequate human rights due diligence process that met the standards set forth in the UN Guiding Principles on Business and Human Rights.

Unfortunately, this is true of the broader venture capital sector as well. Overall, of the 50 VC firms and three startup accelerators analyzed by Amnesty International, we found that almost all of them lacked adequate human rights due diligence policies and processes.

This failure to carry out adequate due diligence means that a vast majority of VC firms are failing in their responsibility to respect human rights.

This almost complete lack of respect for human rights among the world’s largest venture capital firms has three key impacts. First, and most immediately, it means that venture capital firms invest in companies whose products and services have been implicated in ongoing human rights abuses, such as companies that provide support to the Chinese government’s repression of the Uyghur population in Xinjiang and across China.

Second, it means that venture capital firms continue to fund companies whose business models have a significant negative impact on human rights, including our privacy and labor rights. For instance, leading venture capital firms continue to support companies that rely on app-based or “gig” workers, who often face exploitative or otherwise abusive work conditions, as well as companies whose “surveillance capitalism” business model undermines our right to privacy.

Third, the lack of human rights due diligence by venture capital firms dramatically increases the risk that they fund new and “frontier” technologies without ensuring that adequate human rights safeguards are in place.

For instance, the application of increasingly powerful artificial intelligence/machine learning (AI/ML) tools across a wide variety of sectors risks amplifying existing societal biases and discrimination. Seemingly objective algorithms can be biased by reliance on incomplete or unrepresentative training data, and/or by replicating the unconscious bias of those who developed the algorithms.

This is a critical blind spot, especially as VC-funded startups seek to disrupt such fundamental parts of our lives as education, finance and health.

The negative impacts of the VC firms’ lack of human rights due diligence — especially regarding issues like algorithmic bias — are magnified by these firms’ own lack of gender and racial diversity. For instance, women comprise only 23% of venture capital investment professionals (i.e., those involved in deciding which startups to fund).

The numbers are even worse when it comes to racial diversity — just 4% of investment professionals at VC firms in the U.S. are Latinx, and only 4% are Black. Groups like Blck VC, Diversity VC and digitalundivided have been calling attention to this issue for years, but venture capitalists have been slow to respond so far.

This lack of diversity is mirrored in the gender and racial composition of founders who receive VC funding. In 2018, all-female founding teams received just 2.2% of all U.S.-based venture funding. At the same time, Black and Latinx founders received less than 2.3% of all U.S.-based venture capital funding in 2019.

With power comes responsibility. Venture capital firms need to institute human rights due diligence processes that meet the standards set forth in the UN Guiding Principles on Business and Human Rights.

Further, they should provide support to their portfolio companies to ensure that they comply with human rights standards. Venture capital firms should also publicly commit to hiring more diverse teams, especially in investment-related positions. Finally, they should publicly commit to funding more diverse startup founders as part of their flagship funds.

VC firms have a responsibility to ensure that their investments are not causing harm. A responsibility that they have, to date, largely ignored.

Powered by WPeMatico

On Sunday Square announced it was gobbling up Afterpay in a deal worth $29 billion at the time of announcement. Alex followed up yesterday with more details on why the deal made sense for Square and Afterpay over here, but we wanted to ask some notable VCs what it means for the startup market.

For context, the Square deal follows a ton of money and interest flowing into the BNPL market. Just this year, VCs have invested in companies like Alma ($59.4 million, January 2021), Scalapay ($48 million, January 2021), Wisetack ($19 million, February 2021), Zilch ($80 million, April 2021) and Dividio ($30 million, June 2021).

Most of the investors we reached out to were generally bullish on the Square and Afterpay integration, but they were less excited about opportunities for other consumer BNPL businesses to emerge.

Then there’s Klarna, which raised $639 million at a post-money valuation of $45.6 billion in June, after raising $1 billion in March at a post-money valuation of $31 billion.

There’s also interest from some major public companies. After a slow start, PayPal is aggressively pushing BNPL services with merchants that offer it as a payment option. And there are reports that Apple is building its own BNPL offering through Apple Pay.

We reached out to Commerce Ventures founder and GP Dan Rosen, Better Tomorrow Ventures founding partner Jake Gibson, Fika Ventures partner TX Zhuo, and Matthew Harris of Bain Capital Ventures to see what they thought of the deal, as well as what it might mean for the opportunity for other BNPL companies and startups.

The main takeaways? “Buy now, pay later” may be effective at driving retail conversion, but scale matters and long-term margins look slim for BNPL startups.

Now, let’s hear from the venture community.

Why is the BNPL market so hot?

Powered by WPeMatico