Entrepreneur

Auto Added by WPeMatico

Auto Added by WPeMatico

TechCrunch’s Connie Loizos published some interesting stats on seed and Series A financings this week, courtesy of data collected by Wing Venture Capital. In short, seed is the new Series A and Series A is the new Series B. Sure, we’ve been saying that for a while, but Wing has some clean data to back up those claims.

Years ago, a Series A round was roughly $5 million and a startup at that stage wasn’t expected to be generating revenue just yet, something typically expected upon raising a Series B. Now, those rounds have swelled to $15 million, according to deal data from the top 21 VC firms. And VCs are expecting the startups to be making money off their customers.

“Again, for the old gangsters of the industry, that’s a big shift from 2010, when just 15 percent of seed-stage companies that raised Series A rounds were already making some money,” Connie writes.

As for seed, in 2018, the average startup raised a total of $5.6 million prior to raising a Series A, up from $1.3 million in 2010.

Now on to IPO updates, then a closer look at all the companies raising big rounds. Want more TechCrunch newsletters? Sign up here. Contact me at kate.clark@techcrunch.com or @KateClarkTweets.

![]()

Slack: The workplace communication software provider dropped its S-1 on Friday ahead of a direct listing. That’s when companies sell existing shares directly to the market, allowing them to skip the roadshow and minimize the astronomical fees typically associated with an initial public offering. Here’s the TLDR on financials: Slack reported revenues of $400.6 million in the fiscal year ending January 31, 2019, on losses of $138.9 million. That’s compared to a loss of $140.1 million on revenue of $220.5 million for the year before. Slack’s losses are shrinking (slowly), while its revenues expand (quickly). It’s not profitable yet, but is that surprising?

Zoom was the Slack we thought Slack was all along.

— alex (PVD) (@alex) April 26, 2019

Uber: The ride-hail giant is fast approaching its IPO, expected as soon as next week. On Friday, the company established an IPO price range of $44 to $50 per share to raise between $7.9 billion and $9 billion at a valuation of approximately $84 billion, significantly lower than the $100 billion previously reported estimations. The most likely outcome is Uber will price above range and all the latest estimates will be way off course. Best to sit back and see how Uber plays it. Oh, and PayPal said it would make a $500 million investment in the company in a private placement, as part of an extension of the partnership between the two.

There are a lot of fascinating companies raising colossal rounds, so I thought I’d dive a bit deeper than I normally do. Bear with me.

Carbon: The poster child for 3D printing has authorized the sale of $300 million in Series E shares, according to a Delaware stock filing uncovered by PitchBook. If Carbon raises the full amount, it could reach a valuation of $2.5 billion. Using its proprietary Digital Light Synthesis technology, the business has brought 3D-printing technology to manufacturing, building high-tech sports equipment, a line of custom sneakers for Adidas and more. It was valued at $1.7 billion by venture capitalists with a $200 million Series D in 2018.

Canoo: The electric vehicle startup formerly known as Evelozcity is on the hunt for $200 million in new capital. Backed by a clutch of private individuals and family offices from China, Germany and Taiwan, the company is hoping to line up the new capital from some more recognizable names as it finalizes supply deals with vendors, according to reporting from TechCrunch’s Jonathan Shieber. The company intends to make its vehicles available through a subscription-based model and currently has 400 employees. Canoo was founded in 2017 after Stefan Krause, a former executive at BMW and Deutsche Bank, and another former BMW executive, Ulrich Kranz, exited Faraday Future amid that company’s struggles.

Starry: The Boston-based wireless broadband internet startup has authorized the sale of Series D shares worth up to $125 million, according to a Delaware stock filing. If Starry closes the full authorized raise it will hold a post-money valuation of $870 million. A spokesperson for the company confirmed it had already raised new capital, but disputed the numbers. The company has already raised more than $160 million from investors, including FirstMark Capital and IAC. The company most recently closed a $100 million Series C this past July.

Selina & Sonder: The Airbnb competitor Sonder is in the process of closing a financing worth roughly $200 million at a $1 billion valuation, reports The Wall Street Journal. Investors including Greylock Partners, Spark Capital and Structure Capital are likely to participate. Sonder is four years old but didn’t emerge from stealth until 2018. The startup, which turns homes into hotels, quickly attracted more than $100 million in venture funding. Meanwhile, another hospitality business called Selina has raised $100 million at an $850 million valuation. The company, backed by Access Industries, Grupo Wiese and Colony Latam Partners, builds living/co-working/activity spaces across the world for digital nomads.

Fresh funds: Mary Meeker has made history with the close of her new fund, Bond Capital, the largest VC fund founded and led by a female investor to date. Bond has $1.25 billion in committed capital. If you remember, Meeker ditched Kleiner Perkins last fall and brought the firm’s entire growth team with her. Kleiner said it was a peaceful split that would allow the firm to focus more on its early-stage efforts, leaving the growth investing to Bond. Fortune, however, reported this week that a power struggle of sorts between Meeker and Mamoon Hamid, who joined recently to reenergize the early-stage side of things, was a larger cause of her exit.

Plus, SOSV, a multi-stage venture firm that was founded as the personal investment vehicle of entrepreneur Sean O’Sullivan after his company went public in 1994, has raised $218 million for its third fund. The vehicle has a $250 million target that SOSV expects to meet. Already, the fund is substantially larger than the firm’s previous vehicle, which closed with $150 million.

A grocery delivery startup crumbles: Honestbee, the online grocery delivery service in Asia, is nearly out of money and trying to offload its business. Despite looking impressive from the outside, the company is currently in crisis mode due to a cash crunch — there’s a lot happening right now. TechCrunch’s Jon Russell dives in deep here.

Extra Crunch: “When it comes to working with journalists, so many people are, frankly, idiots. I have seen reporters yank stories because founders are assholes, play unfairly, or have PR firms that use ridiculous pressure tactics when they have already committed to a story.” Sign up for Extra Crunch for a full list of PR don’ts. Here are some other EC pieces to hit the wire this week:

Equity: If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about Kleiner Perkins, Chinese IPOs and Slack & Uber’s upcoming exits.

Powered by WPeMatico

Sam Altman’s little brother Jack is an entrepreneur, too.

Jack Altman, whose resume includes a stint as vice president of business development at Teespring, has raised $15 million in Series B funding for his startup, Lattice, a modern approach to corporate goal setting. Shasta Ventures led the round, with participation from Thrive Capital, Khosla Ventures and Y Combinator, the latter being the organization his brother led as president until very recently.

Lattice, used by high-growth companies like Reddit, Slack, Coinbase and Glossier, helps human resources professionals develop insights about their teams. Founded in 2015, Altman and Eric Koslow, like most entrepreneurs, developed the idea for Lattice out of their own pain points.

“We realized that with quarterly goal settings, OKRs, we would write them up and get the leadership together and then they would sit on a shelf and nothing would happen,” Altman told TechCrunch.

Lattice, a SaaS business, is a flexible platform that caters to startups and larger businesses’ specific cultures, management practices and varying approaches to employee engagement. The product, inspired by platforms like Gmail and Slack, is designed with consumers in mind. Lattice, the team hopes, has a look and feel that makes incumbent HR platforms feel antiquated.

The product makes it simple for employees and their managers to complete engagement surveys, share feedback, arrange one-on-one meetings and complete comprehensive performance reviews with a larger goal of reworking the company goal-setting process entirely. No more once-yearly check-ins; Lattice enables businesses to check-in with their employees on a weekly basis.

Lattice currently has 1,200 customers, 60 employees and was cash flow break-even for the first time in Q1 2019. With the latest financing, the San Francisco-based startup plans to invest in product development.

“Life is short,” Altman said. “You want to have work that you enjoy and an office that feels good to be at.”

Lattice has previously raised capital from investors including SV Angel, Marc Benioff, Slack Fund and Fuel Capital, Sam Altman, Elad Gil, Alexis Ohanian, Kevin Mahaffey, Daniel Gross and Jake Gibson. Lattice completed the Y Combinator startup accelerator in 2016.

Powered by WPeMatico

Kindbody, a startup that lures millennial women into its pop-up fertility clinics with feminist messaging and attractive branding, has raised a $15 million Series A in a round co-led by RRE Ventures and Perceptive Advisors.

The New York-based company was founded last year by Gina Bartasi, a fertility industry vet who previously launched Progyny, a fertility benefit solution for employers, and FertilityAuthority.com, an information platform and social network for people struggling with fertility.

“We want to increase accessibility,” Bartasi told TechCrunch. “For too long, IVF and fertility treatments were for the 1 percent. We want to make fertility treatment affordable and accessible and available to all regardless of ethnicity and social economic status.”

Kindbody operates a fleet of vans — mobile clinics, rather — where women receive a free blood test for the anti-Müllerian hormone (AMH), which helps assess their ovarian egg reserve but cannot conclusively determine a woman’s fertility. Depending on the results of the test, Kindbody advises women to visit its brick-and-mortar clinic in Manhattan, where they can receive a full fertility assessment for $250. Ultimately, the mobile clinics serve as a marketing strategy for Kindbody’s core service: egg freezing.

Kindbody charges patients $6,000 per egg-freezing cycle, a price that doesn’t include the cost of necessary medications but is still significantly less than market averages.

Bartasi said the mobile clinics have been “wildly popular,” attracting hoards of women to its brick-and-mortar clinic. As a result, Kindbody plans to launch a “fertility bus” this spring, where the company will conduct full fertility assessments, including the test for AMH, a pelvic ultrasound and a full consultation with a fertility specialist.

In other words, Kindbody will offer all components of the egg-freezing process on a bus aside from the actual retrieval, which occurs in Kindbody’s lab. The bus will travel around New York City before heading west to San Francisco, where it plans to park on the campuses of large employers, catering to tech employees curious about their fertility.

“Our mission at Kindbody is to bring care directly to the patient instead of asking the patient to come to visit us and inconvenience them,” Bartasi said.

A sneak peek of Kindbody’s “fertility bus,” which is still in the works

Kindbody, which has raised $22 million to date from Green D Ventures, Trailmix Ventures, Winklevoss Capital, Chelsea Clinton, Clover Health co-founder Vivek Garipalli and others, also provides women support getting pregnant with in vitro fertilisation (IVF) and intrauterine insemination (IUI).

With the latest investment, Kindbody will open a second brick-and-mortar clinic in Manhattan and its first permanent clinic in San Francisco. Additionally, Bartasi says they are in the process of closing an acquisition in Los Angeles that will result in Kindbody’s first permanent clinic in the city. Soon, the company will expand to include mental health, nutrition and gynecological services.

In an interview with The Verge last year, Bartasi said she’s taken inspiration from SoulCycle and DryBar, companies whose millennial-focused branding strategies and prolific social media presences have helped them accumulate customers. Kindbody, in that vein, notifies its followers of new pop-up clinics through its Instagram page.

In the article, The Verge called Kindbody “the SoulCycle of fertility” and questioned its branding strategy and its claim that egg freezing “freezes time.” After all, there is limited research confirming the efficacy of egg freezing.

“The technology that allows for egg-freezing has only been widely used in the last five to six years,” Bartasi explained. “The majority of women who froze their eggs haven’t used them yet. It’s not like you freeze your eggs in February and meet Mr. Right in June.”

Though Kindbody touts a mission of providing fertility treatments to the 99 percent, there’s no getting around the sky-high costs of the services, and one might argue that companies like Kindbody are capitalizing off women’s fear of infertility. Providing free AMH tests, which often falsely lead women to believe they aren’t as fertile as they’d hoped, might encourage more women to seek a full-fertility assessment and ultimately, to pay $6,000 to freeze their eggs, when in reality they are just as fertile as the average woman and not the ideal candidate for the difficult and uncomfortable process.

Bartasi said Kindbody makes all the options clear to its patients. She added that when she does hear accusations that services like Kindbody capitalize on fear of infertility, they tend to come from legacy programs and male fertility doctors: “They are a little rattled by some of the new entrants that look like the patients,” she said. “We are women designing for women. For far too long women’s health has been solved for by men.”

Kindbody’s pricing scheme may itself instill fear in incumbent fertility clinics. The startup’s egg-freezing services are much cheaper than market averages; its IVF services, however, are not. Not including the costs of medications necessary to successfully harvest eggs from the ovaries, the average cost of an egg-freezing procedure costs approximately $10,000, compared to Kindbody’s $6,000. Its IVF services are on par with other options in the market, costing $10,000 to $12,000 — not including medications — for one cycle of IVF.

Kindbody is able to charge less for egg freezing because they’ve cut out operational inefficiencies, i.e. they are a tech-enabled platform while many fertility clinics around the U.S. are still handing out hoards of paperwork and using fax machines. Bartasi admits, however, that this means Kindbody is making less money per patient than some of these legacy clinics.

“What is a reasonable profit margin for fertility doctors today?” Bartasi said. “Historically, margins have been very, very high, driven by a high retail price. But are these really high retail prices sustainable long term? If you’re charging 22,000 for IVF, how long is that sustainable? Our profit margins are healthy.”

Bartasi isn’t the only entrepreneur to catch on to the opportunity here, as I’ve noted. A whole bunch of women’s health startups have launched and secured funding recently.

Tia, for example, opened a clinic and launched an app that provides health advice and period tracking for women. Extend Fertility, which like Kindbody, helps women preserve their fertility through egg freezing, banked a $15 million round. And a startup called NextGen Jane, which is trying to detect endometriosis with “smart tampons,” announced a $9 million Series A a few weeks ago.

Powered by WPeMatico

The HBO sci-fi blockbuster Westworld has been an inspiring look into what humanlike robots can do for us in the meatspace. While current technologies are not quite advanced enough to make Westworld a reality, startups are attempting to replicate the sort of human-robot interaction it presents in virtual space.

Rct studio, which just graduated from Y Combinator and ranked among TechCrunch’s nine favorite picks from the batch, is one of them. The “Westworld” in the TV series, a far-future theme park staffed by highly convincing androids, lets visitors live out their heroic and sadistic fantasies free of consequences.

There are a few reasons why rct studio, which is keeping mum about the meaning of its deliberately lower-cased name for later revelation, is going for the computer-generated world. Besides the technical challenge, playing a fictional universe out virtually does away the geographic constraint. The Westworld experience, in contrast, happens within a confined, meticulously built park.

“Westworld is built in a physical world. I think in this age and time, that’s not what we want to get into,” Xinjie Ma, who heads up marketing for rct, told TechCrunch. “Doing it in the physical environment is too hard, but we can build a virtual world that’s completely under control.”

Rct studio wants to build the Westworld experience in virtual worlds. / Image: rct studio

The startup appears suitable to undertake the task. The eight-people team is led by Cheng Lyu, the 29-year-old entrepreneur who goes by Jesse and helped Baidu build up its smart speaker unit from scratch after the Chinese search giant acquired his voice startup Raven in 2017. Along with several of Raven’s core members, Lyu left Baidu in 2018 to start rct.

“We appreciate a lot the support and opportunities given by Baidu and during the years we have grown up dramatically,” said Ma, who previously oversaw marketing at Raven.

Immersive films, or games, depending on how one wants to classify the emerging field, are already available with pre-written scripts for users to pick from. Rct wants to take the experience to the next level by recruiting artificial intelligence for screenwriting.

At the center of the project is the company’s proprietary engine, Morpheus. Rct feeds it mountains of data based on human-written storylines so the characters it powers know how to adapt to situations in real time. When the codes are sophisticated enough, rct hopes the engine can self-learn and formulate its own ideas.

“It takes an enormous amount of time and effort for humans to come up with a story logic. With machines, we can quickly produce an infinite number of narrative choices,” said Ma.

To venture through rct’s immersive worlds, users wear a virtual reality headset and control their simulated self via voice. The choice of audio came as a natural step given the team’s experience with natural language processing, but the startup also welcomes the chance to develop new devices for more lifelike journeys.

“It’s sort of like how the film Ready Player One built its own gadgets for the virtual world. Or Apple, which designs its own devices to carry out superior software experience,” explained Ma.

On the creative front, rct believes Morpheus could be a productivity tool for filmmakers as it can take a story arc and dissect it into a decision-making tree within seconds. The engine can also render text to 3D images, so when a filmmaker inputs the text “the man throws the cup to the desk behind the sofa,” the computer can instantly produce the corresponding animation.

Investors are buying into rct’s offering. The startup is about to close its Series A funding round just months after banking seed money from Y Combinator and Chinese venture capital firm Skysaga, the startup told TechCrunch.

The company has a few imminent tasks before achieving its Westworld dream. For one, it needs a lot of technical talent to train Morpheus with screenplay data. No one on the team had experience in filmmaking, so it’s on the lookout for a creative head who appreciates AI’s application in films.

Rct studio’s software takes a story arc and dissects it into a decision-making tree within seconds. / Image: rct studio

“Not all filmmakers we approach like what we do, which is understandable because it’s a very mature industry, while others get excited about tech’s possibility,” said Ma.

The startup’s entry into the fictional world was less about a passion for films than an imperative to shake up a traditional space with AI. Smart speakers were its first foray, but making changes to tangible objects that people are already accustomed to proved challenging. There has been some interest in voice-controlled speakers, but they are far from achieving ubiquity. Then movies crossed the team’s mind.

“There are two main routes to make use of AI. One is to target a vertical sector, like cars and speakers, but these things have physical constraints. The other application, like Alpha Go, largely exists in the lab. We wanted something that’s both free of physical limitation and holds commercial potential.”

The Beijing and Los Angeles-based startup isn’t content with just making the software. Eventually, it wants to release its own films. The company has inked a long-term partnership with Future Affairs Administration, a Chinese sci-fi publisher representing about 200 writers, including the Hugo award-winning Cixin Liu. The pair is expected to start co-producing interactive films within a year.

Rct’s path is reminiscent of a giant that precedes it: Pixar Animation Studios . The Chinese company didn’t exactly look to the California-based studio for inspiration, but the analog was a useful shortcut to pitch to investors.

“A confident company doesn’t really draw parallels with others, but we do share similarities to Pixar, which also started as a tech company, publishes its own films, and has built its own engine,” said Ma. “A lot of studios are asking how much we price our engine at, but we are targeting the consumer market. Making our own films carry so many more possibilities than simply selling a piece of software.”

Powered by WPeMatico

When considering the structural impact of technology companies on our economy and society, we tend to focus on questions of scale and monopoly.

It’s true that the FAANG companies and more recent winners (Airbnb, Uber) have surfed a combination of network effects, preferential access to capital and classic efficiencies of scale to generate tremendous value for their shareholders — to the detriment of new entrants who attempt to unseat them.

At their high water mark in mid-2018, FAANG alone made up 11 percent of the total market cap of the S&P 500 and 38 percent of the index’s year-to-date gain, representing a doubling in their influence in only five years. The question of regulating technology companies — to the point of instituting anti-trust actions — has even become a rare point of relative concord between Democrats and Republicans in Congress.

But is the narrative of tech companies in the 2010s only a story of economic consolidation and growing inequality? Many of the most successful B2B startups of the last decade are aligned by a theme that paints a different picture. By transforming the nature of the costs required to start a business, these startups are reducing the influence of capital and leveling the playing field for new entrants to share in the surplus generated by the secular shift to a tech-mediated economy.

Source: Getty Images/MIKIEKWOODS

What do AWS, WeWork, Stord, Gusto

But they are alike in the economic purpose they serve for their customers. Each of these services takes a fixed cost — a bank of servers, a lease, a legal retainer — and transforms it into a variable cost. As a refresher, a fixed cost stays constant regardless of output, and variable costs scale with the output of a business.

When my father started his software consulting business in the early 1990s, I remember the giant boxes of AIX servers that arrived at our apartment, and tagging along to office tours in central New Jersey before he decided to run the company out of our spare bedroom. Back then, starting almost any kind of business was hard because of high fixed costs. Without AWS or WeWork, you shelled out upfront for hardware and a lease.

Access to capital, whether in the form of a bank loan, savings or friends and family was a prerequisite for entrepreneurship.

Today, startups make it possible to start and scale almost any kind of business while incurring few fixed costs. Want to found an e-commerce store? Start with a free Shopify account and dropship your inventory. Want to become a freelance designer? Put a shingle up on Fiverr and meet clients at a Breather you rent by the hour.

Whether software or hardware or labor, building a business is way easier when overhead is transformed into a string of flexible microservices that you only pay for as you grow.

Image courtesy of Getty Images

Taken together, startups that turn fixed costs into variable costs make it less capital-intensive to start a business. This decreases the influence of gatekeepers and aggregators of capital — an impact evident in the way entrepreneurs think about starting businesses today.

It’s no coincidence that the rise of B2B startups fitting this theme has coincided with the bootstrap movement, in which tech entrepreneurs with major ambitions demur from raising venture funding because — well, they don’t need the money anymore.

It has also coincided with a renaissance in freelance entrepreneurship: 56.7 million Americans freelanced in 2018. Beyond the economic benefits of working for yourself — the fastest growing segment of freelancers earns more than $75,000 a year — freelancers can access the lifestyle and health benefits of owning their destiny, which aren’t directly captured but play a role in the economic picture. Indeed, 51 percent of freelancers said no amount of money would lure them into a traditional job, and 64 percent reported feeling healthier and happier.

When capital plays a reduced role in new business formation, access to capital plays a smaller role in determining who will succeed. More companies are founded, and the economy becomes more likely to birth new Davids that will unseat the Goliaths. Economics 101: lower barriers to entry create markets that converge on perfect competition instead of oligarchic concentration.

Source: Getty Images/ERHUI1979

Variable costs have their downsides. A startup with a relatively higher proportion of fixed costs — the profile of the classic high-tech software business — can achieve higher profit margins as it scales. Compare Microsoft or Google, which pay high fixed costs in the form of salaries and servers but few costs in delivering their services and achieve operating margins of 25-30 percent, to Costco, which takes in more than $100 billion of annual revenue but earns an operating margin in the single digits.

That’s OK. Neither type of cost is “better” or “worse,” but having the option to decide how to structure costs through a company’s life cycle can meaningfully impact an entrepreneur’s ability to execute a business idea.

Founders investigating startup ideas — and politicians debating the impact of technology — would do well to pay attention to how B2B companies have democratized access to entrepreneurship.

Powered by WPeMatico

Taiwanese technology giant Foxconn International is backing Carbon Relay, a Boston-based startup emerging from stealth today that’s harnessing the algorithms used by companies like Facebook and Google for artificial intelligence to curb greenhouse gas emissions in the technology industry’s own backyard — the data center.

Already, the computing demands of the technology industry are responsible for 3 percent of total energy consumption — and the addition of new technologies like Bitcoin to the mix could add another half a percent to that figure within the next few years, according to Carbon Relay’s chief executive, Matt Provo.

That’s $25 billion in spending on energy per year across the industry, Provo says.

A former Apple employee, Provo went to Harvard Business School because he knew he wanted to be an entrepreneur and start his own business — and he wanted that business to solve a meaningful problem, he said.

Variability and dynamic nature of the data center relating to thermodynamics and the makeup of a facility or building is interesting for AI because humans can’t keep up.

“We knew what we wanted to focus on,” said Provo of himself and his two co-founders. “All three of us have an environmental sciences background as well… We were fired up about building something that was true AI that has positive value… the risk associated [with climate change] is going to hit in our lifetime, we were very inspired to build a company whose technology would have an impact on that.”

Carbon Relay’s mission and founding team, including Thibaut Perol and John Platt (two Harvard graduates with doctorates in applied mathematics) was able to attract some big backers.

The company has raised $6 million from industry giants like Foxconn and Boston-based angel investors, including Dr. James Cash — a director on the boards of Walmart, Microsoft, GE and State Street; Black Duck Software founder, Douglas Levin; Karim Lakhani, a director on the Mozilla Corporation board; and Paul Deninger, a director on the board of the building operations management company, Resideo (formerly Honeywell).

Provo and his team didn’t just raise the money to tackle data centers — and Foxconn’s involvement hints at the company’s broader goals. “My vision is that commercial HVAC systems or any machinery that operates in a business would not ship without our intelligence inside of it,” says Provo.

What’s more compelling is that the company’s technology works without exposing the underlying business to significant security risks, Provo says.

“In the end all we’re doing are sending these floats… these values. These values are mathematical directions for the actions that need to be taken,” he says.

Carbon Relay is already profitable, generating $4 million in revenue last year and on track for another year of steady growth, according to Provo.

Carbon Relay offers two products: Optimize and Predict, that gather information from existing HVAC devices and then control those systems continuously and automatically with continuous decision making.

“Each data center is unique and enormously complex, requiring its own approach to managing energy use over time,” said Cash, who’s serving as the company’s chairman. “The Carbon Relay team is comprised of people who are passionate about creating a solution that will adapt to the needs of every large data center, creating a tangible and rapid impact on the way these organizations do business.”

Powered by WPeMatico

Now that “utility” tokens have become a popular and international way to fund major blockchain projects, a pair of investors are creating a new way to turn tokens into true equities. The investors, Jonathan Nelson and Laura Nelson, have created Hack Fund, an early stage investment vehicle that allows startups to launch what amounts to “blockchain stock certificates,” according to Jonathan.

“Our previous business model exchanged equity from startup companies for services, and wrapped that equity into funds that we then sold to investors. These fund investors have included family offices, institutions, and high net worth individuals,” said Jonathan. “However, Hack Fund represents a new business model. Because Hack Fund leverages the blockchain, investors all over the world at all levels can participate in startup investing by trading blockchain stock certificates. Also, its SEC compliant structure means that it is also available to a limited number of accredited investors in the US.”

The team originally created Hackers/Founders, a tech entrepreneur group in Silicon Valley, and they now support 300,000 members in 133 cities and 49 countries. Hack Fund is a vehicle to support some of the startups in the Hackers/Founders network.

“HACK Fund, through its Hackers/Founders heritage, has a large, unique global network,” said Jonathan. “This provides Hack Fund with unparalleled reach and deal flow across the global technology market. There are a few blockchain-based funds, but they are limited themselves to blockchain-only investments. Unlike typical venture funds, HACK Fund will provide quick liquidity for investors, leveraging blockchain technology to make typically illiquid private stocks tradeable.”

The idea behind Hack Fund is quite interesting. In most cases investing in a company leads to up to ten years of waiting for a liquidity event. However, with blockchain-based stock certificates investors can buy shares that can be bought and sold instantly while company performance drives the value up or down. In short, startups become liquid in an instant, which can be a good thing or a bad thing, depending on the founding team.

“HACK Fund is a publicly traded closed-end fund. The fund’s venture investments are valued on a quarterly basis by an independent third party, audited and posted to the blockchain for all token holders to review. There are no K-1 statements issued, there is no partnership/LLC, rather HACK Fund is an investment company akin to Berkshire Hathaway which invests in the same manner as early-stage venture capital,” said Jonathan.

The $100 million fund raise has already kicked off across Asia, Middle East, Latin America and to a small number of accredited investors in the US. The fund will be rounded out with $2 million from retail investors who will be able to buy some of the tokens on October 29th through BRD wallet.

Powered by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

Sometimes smart contracts can be pretty dumb.

All of the benefits of a cryptographically secured, publicly verified, anonymized transaction system can be erased by errant code, malicious actors or poorly defined parameters of an executable agreement.

Hoping to beat back the tide of bad contracts, bad code and bad actors, Sagewise, a new Los Angeles-based startup, has raised $1.25 million to bring to market a service that basically hits pause on the execution of a contract so it can be arbitrated in the event that something goes wrong.

Co-founded by a longtime lawyer, Amy Wan, whose experience runs the gamut from the U.S. Department of Commerce to serving as counsel for a peer-to-peer real estate investment platform in Los Angeles, and Dan Rice, a longtime entrepreneur working with blockchain, Sagewise works with both Ethereum and the Hedera Hashgraph (a newer distributed ledger technology, which purports to solve some of the issues around transaction processing speed and security which have bedeviled platforms like Ethereum and Bitcoin).

The company’s technology works as a middleware, including an SDK and a contract notification and monitoring service. “The SDK is analogous to an arbitration clause in code form — when the smart contract executes a function, that execution is delayed for a pre-set amount of time (i.e. 24 hours) and users receive a text/email notification regarding the execution,” Wan wrote to me in an email. “If the execution is not the intent of the parties, they can freeze execution of the smart contract, giving them the luxury of time to fix whatever is wrong.”

Sagewise approaches the contract resolution process as a marketplace where priority is given to larger deals. “Once frozen, parties can fix coding bugs, patch up security vulnerabilities, or amend/terminate the smart contract, or self-resolve a dispute. If a dispute cannot be self-resolved, parties then graduate to a dispute resolution marketplace of third party vendors,” Wan writes. “After all, a $5 bar bet would be resolved differently from a $5M enterprise dispute. Thus, we are dispute process agnostic.”

Wavemaker Genesis led the round, which also included strategic investments from affiliates of Ari Paul (Blocktower Capital), Miko Matsumura (Gumi Cryptos), Youbi Capital, Maja Vujinovic (Cipher Principles), Jordan Clifford (Scalar Capital), Terrence Yang (Yang Ventures) and James Sowers.

“Smart contracts are coded by developers and audited by security auditing firms, but the quality of smart contract coding and auditing varies drastically among service providers,” said Wan, the chief executive of Sagewise, in a statement. “Inevitably, this discrepancy becomes the basis for smart contract disputes, which is where Sagewise steps in to provide the infrastructure that allows the blockchain and smart contract industry to achieve transactional confidence.”

In an email, Wan elaborated on the thesis to me, writing that, “smart contracts may have coding errors, security vulnerabilities, or parties may need to amend or terminate their smart contracts due to changing situations.”

Contracts could also be disputed if their execution was triggered accidentally or due to the actions of attackers trying to hack a platform.

“Sagewise seeks to bring transactional confidence into the blockchain industry by building a smart contract safety net where smart contracts do not fulfill the original transactional intent,” Wan wrote.

Powered by WPeMatico

The dream of a startup founder can often be summarized by the following well-intentioned, and mostly delusional, quote: “We’ll raise a few rounds and in a few years we’ll IPO on Nasdaq.”

But a more likely scenario looks something like this:

You invest a few years of hard work to build something of value. One day you receive an acquisition offer out of the blue. You’re elated. And you’re not prepared. You drop everything to focus on this opportunity. Exclusive due diligence starts. Your company is a mess (IP, contracts, burn). Days become weeks; weeks become months. You’ve neglected business and fundraising. You’re running out of money. M&A is now your one and only option. The buyer says they found a bunch of cockroaches in the walls and drops the price. Now what?

Sound unlikely?

This is still a favorable situation: You had an offer! Think about how much time you invested in your various funding rounds. The hundreds of names and Google spreadsheet or Streak-powered quasi-CRM process.

Have you spent even a fraction of that on understanding exit paths? If you’d rather not live the situation described above, read along.

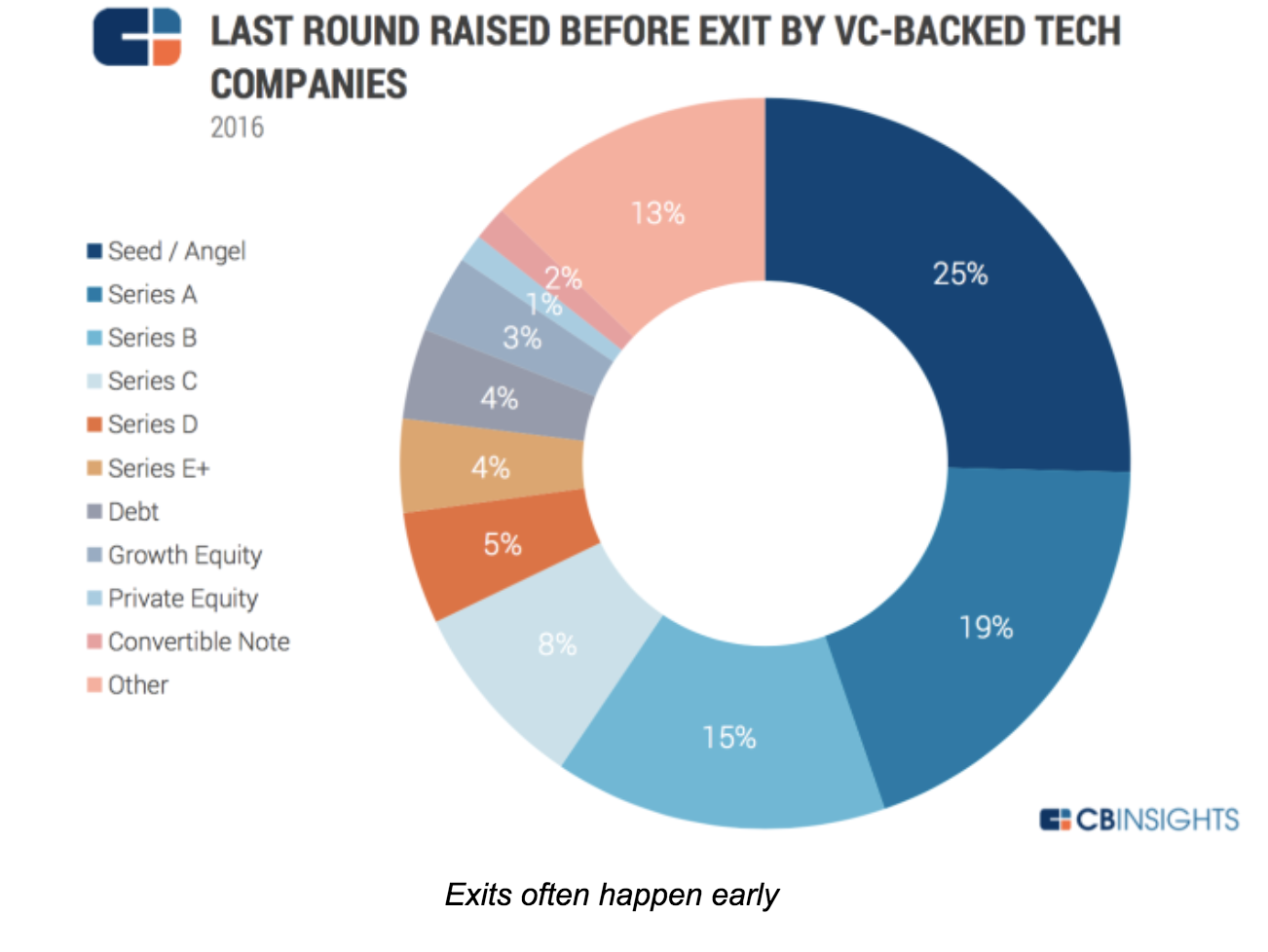

Investors live by exits, but many founders keep dreaming of unicornization and avoid the “E-word” until it’s too late. Yet, in 2016, 97 percent of exits were M&As. And most happened before Series B.

Exits matter because that’s when you, your team and your investors get paid. Oddly enough, and to use a chess metaphor, we hear a lot about the “opening game” (lean startup) and the “mid-game” (growth), but very little about this “end game.”

As a result, founders miss opportunities or leave money on the table. This is a shame. Our fund has more than 700 companies in portfolio. We want the best possible exit for each of them. And fortune favors the prepared! Now, how to get 700 exits (and counting)?

To explore the topic, we organized a series of Master Classes tapping corporate buyers, bankers, investors, lawyers and startup CEOs with M&A or IPO experience in San Francisco. It was a group that included the founders of Guitar Hero — bought by Activision; JUMP Bikes — a SOSV portfolio company bought by Uber, Ubiquisys — bought by Cisco and Withings — bought by Nokia. Each one for hundreds of millions.

Their observations can be summarized below.

“Founders must be aware of what contributes to an exit. This means understanding partnerships and how they are formed in the business space the entrepreneur is working in,” said one Master Class participant.

As founders, you build your product, your company and… optionality. You need to understand the options open to your company, and take steps to enable them.

The most likely one is an acquisition, but there are others like IPO (including small cap), RTO, SBO, LBO, Equity Crowdfunding and even ICO.

“Exit is not a goal per se, but as a CEO it is something you should think about as early in your cycle as possible, while being business-focused,” said the London-based investor Frederic Rombaut, of Seraphim Capital.

Indeed, most participants said that exits should always be on the chief executive’s agenda, no matter how early in the process. “Exits should be on the CEO agenda. Not front and center, but on the agenda. M&A is a by-product of a great business and targeted BD. IPOs are always an option once you’ve built significant cashflow forecasting.”

It’s important to ask questions like: How many “strategic engagements” with potential buyers have you had this month? Is your message and value clear in their eyes? Have you considered an acquisition track in parallel to a fundraise?

It doesn’t stop there:

One thing is sure: The time to exit is not when you’re running out of money.

Unicorn or not, the most likely exit is an acquisition.

As George Patterson, managing director at HSBC in New York said, “Good tech companies are bought, not sold. The question is thus: how to get bought?”

Patterson says it’s important to understand how mergers and acquisitions actually work; how to prepare a startup for an exit; and how to develop a “feel” for the market you’re exiting through and into.

Hearing from corp dev veterans from Cisco, Logitech, Dassault and IBM, a few key ideas emerged:

Motivations vary

It could be from least to most expensive, or as a mix, as listed by Mark Suster, managing partner at Upfront Ventures:

How corporates find you

Corporates find deals via the development of partnerships, investment (CVC), their business units, corp dev research, media and investor connections.

Asked about the best approach, Todd Neville, manager of Corporate Business Development and Strategy at IBM (who gave the most detailed description of the corp dev process), said, “Do something cool to one of the IBM customers. If they rave about even a POC, we’re interested.”

In other words, business development is corporate development.

Get the house in order

Buyers typically want to know three things:

For IP, they will check your contracts (staff and contractors), and run some automated code analysis for proprietary code and open source use. They will evaluate potential IP infringement. No point buying you if you end up costing more in lawsuits!

For your team skills: Sitting down with your engineers will tell them plenty enough without understanding the details of this or that algorithm. The last thing a corporate wants is to be accused of stealing!

Lawyers engaged early can help. The later the clean-up, the more costly and painful.

Develop a feel for your “market”

Develop relationships and create champions within corporates. It will help promote your deal when the time comes, and will let you keep your finger on the pulse of corporate strategy to time your moves.

Do you read the earning calls of Cisco or IBM (or others relevant to you)? This is where strategies are presented. Are your keywords coming up there or in their press releases?

Chris Gilbert, former CEO of Ubiquisys (sold to Cisco for more than $300 million) was very deliberate in planning his exit.

“Selling starts on day one and is a leadership-only function — work out who will be your buyer. Only the CEO can do this. Constantly articulate why a company should buy you,” Gilbert said. Bring clear messages into the acquiring company so it can be presented upwards: give them the presentation you would like them to show their boss! When the time is right, force decisions through competition. If you know they have to buy you, your starting position is strong.”

The dark art of price discovery

There are dozens of formulas (from DCF to comparables) to evaluate a deal — which also means none is “correct.” What matters is: How much would you sell for, and how much is the buyer ready to pay?

Gilbert, at Ubiquisys, described how close interactions with his banker helped drive the price up among the bidders assembled.

Just like buyers, we meet bankers and lawyers too rarely at startup events, but there is much to learn with them. They make deals happen, avoid value erosion and optimize price. They often also make introductions before you engage them, to build goodwill and earn your business.

And if you worry about fees, the right banker handsomely pays for itself by finding more bidders and playing “bad cop” for you, avoiding direct confrontation with your future employer. Do you want a slice of the watermelon or the whole grape?

When asked about what happens after an M&A or IPO, buyers said they generally hoped the founders would stay with them for many years. Often using re-vesting, earn-outs or shares of the acquiring company to incentivize them. Neville, from IBM, mentioned a security company they acquired whose founder is now the head of one of the largest IBM divisions.

In the case of IPOs, supposedly the ultimate “exit,” any block of shares sold by founders would face extreme scrutiny and might cause a price drop.

So who’s exiting during those deals? Investors (and not always).

Eventually, if the average age of a startup at exit is 8-10 years, the active duty period of founders (if not replaced in the meantime) extends even more. Better love the problem you’re solving, and your customers!

Thanks to speakers, participants and supporters of this Master Class series:

London: Frederic Rombaut (Seraphim Capital), Joe Tabberer (FirstBank), Chris Gilbert (Ubiquisys), Jonathan Keeling (Crowdcube), Fred Destin, Tony Fish (AMF Ventures, James Clark (London Stock Exchange), Denise Law (SGCIB).

Paris: Frederic Rombaut (Seraphim Capital), Manuel Gruson (Dassault Systemes), Pierre-Henri Chappaz (Rothschild Global Advisory), Christine Lambert-Goue (All Invest), Olivier Younes (EXPEN), Eric Carreel (Withings), Fabien Bardinet (Balyo), Xavier Lazarus (Elaia Partners), Pierre-Eric Leibovici(Daphni). Jean de La Rochebrochard (Kima Ventures), Jeremy Sartre (SmartAngels), Gwen Regina Tan (Entrepreneur First).

San Francisco: Natasha Ligai (Logitech), Matt Cutler (Cisco),Will Hawthorne, (CODE Advisors), Ryan Rzepecki (JUMP Bikes), Charles Huang (Guitar Hero), Jeff Thomas (Nasdaq), Shahin Farshchi (Lux Capital), Ammar Hanafi (Moment Ventures), Adam J. Epstein (Third Creek Advisors), Nathan Harding (EKSO Bionics), Kate Whitcomb, Anthony Marino and Ethan Haigh (SOSV).

New York: Todd Neville (IBM), George Patterson (HSBC), Ryan Rzepecki (JUMP Bikes), Aaron Kellner (SeedInvest), Jeremy Levine (Bessemer Venture Partners), Taylor Greene (Collaborative Fund), Adam Rothenberg (BoxGroup), Eli Curi (Fenwick & West), Ian Engstrand and Salil Gandhi (Goodwin), Warren Spar(Sparring Partners Capital), Duncan Turner, Vivian Law and Sheng Ge (SOSV).

Powered by WPeMatico