enterprise software

Auto Added by WPeMatico

Auto Added by WPeMatico

While the technology and business world worked towards the weekend, developer operations (DevOps) firm GitLab filed to go public. Before we get into our time off, we need to pause, digest the company’s S-1 filing, and come to some early conclusions.

GitLab competes with GitHub, which Microsoft purchased for $7.5 billion back in 2018.

The company is notable for its long-held, remote-first stance, and for being more public with its metrics than most unicorns — for some time, GitLab had a November 18, 2020 IPO target in its public plans, to pick an example. We also knew when it crossed the $100 million recurring revenue threshold.

Considering GitLab’s more recent results, a narrowing operating loss in the last two quarters is good news for the company.

The company’s IPO has therefore been long expected. In its last primary transaction, GitLab raised $286 million at a post-money valuation of $2.75 billion, per Pitchbook data. The same information source also notes that GitLab executed a secondary transaction earlier this year worth $195 million, which gave the company a $6 billion valuation.

Let’s parse GitLab’s growth rate, its final pre-IPO scale, its SaaS metrics, and then ask if we think it can surpass its most recent private-market price. Sound good? Let’s rock.

GitLab intends to list on the Nasdaq under the symbol “GTLB.” Its IPO filing lists a placeholder $100 million raise estimate, though that figure will change when the company sets an initial price range for its shares. Its fiscal year ends January 31, meaning that its quarters are offset from traditional calendar periods by a single month.

Let’s start with the big numbers.

In its fiscal year ended January 2020, GitLab posted revenues of $81.2 million, gross profit of $71.9 million, an operating loss of $128.4 million, and a modestly greater net loss of $130.7 million.

And in the year ended January 31, 2021, GitLab’s revenue rose roughly 87% to $152.2 million from a year earlier. The company’s gross profit rose around 86% to $133.7 million, and operating loss widened nearly 67% to $213.9 million. Its net loss totaled $192.2 million.

This paints a picture of a SaaS company growing quickly at scale, with essentially flat gross margins (88%). Growth has not been inexpensive either — GitLab spent more on sales and marketing than it generated in gross profit in the past two fiscal years.

Powered by WPeMatico

I’ve met hundreds of founders over the years, and most, particularly early-stage founders, share one common go-to-market gripe: Pricing.

For enterprise software, traditional pricing methods like per-seat models are often easier to figure out for products that are hyperspecific, especially those used by people in essentially the same way, such as Zoom or Slack. However, it’s a different ballgame for startups that offer services or products that are more complex.

Most startups struggle with a per-seat model because their products, unlike Zoom and Slack, are used in a litany of ways. Salesforce, for example, employs regular seat licenses and admin licenses — customers can opt for lower pricing for solutions that have low-usage parts — while other products are priced based on negotiation as part of annual renewals.

You may have a strong champion in a CIO you’re selling to or a very friendly person handling procurement, but it won’t matter if the pricing can’t be easily explained and understood. Complicated or unclear pricing adds more friction.

Early pricing discussions should center around the buyer’s perspective and the value the product creates for them. It’s important for founders to think about the output and the outcome, and a number they can reasonably defend to customers moving forward. Of course, self-evaluation is hard, especially when you’re asking someone else to pay you for something you’ve created.

This process will take time, so here are three tips to smoothen the ride.

Pricing is not a fixed exercise. The enterprise software business involves a lot of intangible aspects, and a software product’s perceived value, quality, and user experience can be highly variable.

The pricing journey is long and, despite what some founders might think, jumping headfirst into customer acquisition isn’t the first stop. Instead, step one is making sure you have a fully fledged product.

If you’re a late-seed or Series A company, you’re focused on landing those first 10-20 customers and racking up some wins to showcase in your investor and board deck. But when you grow your organization to the point where the CEO isn’t the only person selling, you’ll want to have your go-to-market position figured out.

Many startups fall into the trap of thinking: “We need to figure out what pricing looks like, so let’s ask 50 hypothetical customers how much they would pay for a solution like ours.” I don’t agree with this approach, because the product hasn’t been finalized yet. You haven’t figured out product-market fit or product messaging and you want to spend a lot of time and energy on pricing? Sure, revenue is important, but you should focus on finding the path to accruing revenue versus finding a strict pricing model.

Powered by WPeMatico

Software billing startup Octane announced Tuesday that it raised $2 million on a post-money valuation of $10 million to advance its pay-as-you-go billing software.

Akash Khanolkar and his co-founders met a decade ago at Carnegie Mellon University and since then went off in different directions. In Khanolkar’s case, he ran a cloud consulting business and saw how fast companies like Datadog and Snowflake were coming to market and dealing with Amazon Web Services.

He found that the commonality in all of those fast-growing companies was billing software using a pay-as-you-go business model versus the traditional flat-rate plans, Khanolkar told TechCrunch.

However, he explained that monitoring consumption means that billing becomes complicated: companies now have to track how customers are using the software per second in order to bill correctly each month.

Seeing the shift toward consumption-based billing, the co-founders came back together in June 2020 to create Octane, a metered billing system that helps vendors create a plan, monitor usage and charge in a similar way to Snowflake and AWS, Khanolkar said.

“We are API-driven, and you as a vendor will send us usage data, and on our end, we store it and then do real-time aggregations so at the end of the month, you can accordingly bill customers,” Khanolkar said. “We have seen contention between engineering and product. Engineers are there to create core plans, so we built a no-code experience for product teams to be able to create new price plans and then perform changes, like adding coupons.”

Within the global cloud billing market, which is expected to reach $6.5 billion by 2025, there are a set of Octane competitors, like Chargebee and Zuora, that Khanolkar said are tackling the subscription management side and succeeding in the past several years. Now there is a usage and consumption-based world coming and a whole new set of software businesses, like Octane, coming in to succeed there.

The new round of funding was led by Basis Set Ventures and included Dropbox co-founder Arash Ferdowsi, Github CTO Jason Warner, Fortress CTO Assunta Gaglione, Scale AI CRO Chetan Chaudhary, former Twilio executive Evan Cummack, Esteban Reyes, Abstraction Capital and Script Capital.

“With the rise of product-led growth and usage-based pricing models, usage-based billing is a critical and foundational piece of infrastructure that has been simply missing,” said Chang Xu, partner at Basis Set Ventures, via email. “At the same time, it’s something that every department cares about as it’s your revenue. Many later-stage companies we talk to that have built this in-house talk about the ongoing maintenance costs and wishes that there is a vendor they can outsource it to.”

We are super impressed with the Octane team with their dedication to building a best-in-class and robust usage-based billing solution. They’ve validated this opportunity by talking to lots of engineering teams so they can solve for all the edge cases, which is important in something as mission critical as billing. We are convinced that Octane will become an inevitable part of the tech infrastructure.”

The new funding will go primarily toward hiring engineers, as well as product, marketing and sales staff. Octane currently has seven employees, and Khanolkar expects to be around 10 by the end of the year.

The company is working with a large range of companies, primarily focused on infrastructure and the depth gauge industries. Octane is also seeing some unique use cases emerge, like a construction company using the usage meter to track the hours an employee works and companies in electric charging using the meter for those purposes.

“We didn’t envision construction guys using it, but in theory, it could be used by any company that tracks time — even legal,” Khanolkar added.

He declined to speak about the company’s revenue, but did say it now had two to three years of runway.

Up next, the company plans to roll out new features like price experimentation based on usage to help customers better make decisions on how to price their software, another problem Khanolkar sees happening. It will build ways that customers can try different plans against usage data to validate which one works the best.

“We are still in the early innings of consumption-based models, but we see more end users opting to go with an enterprise that wants to let them try out the software and then pay as they go,” he added.

Powered by WPeMatico

The pandemic was a catalyst for showing companies looking to cut costs just how much they were spending on their software tools. New York-based Tropic’s platform not only uncovers those savings, but also brings a click-and-approve approach to buying software. Today, the company announced a $25 million Series A round of funding.

Canaan Partners led the round, with participation from Founder Collective and Mo Koyfman’s new fund, Shine. It gives Tropic $27.1 million in total funding since the company emerged from stealth in 2020, CEO David Campbell told TechCrunch.

Prior to founding the company with Justin Etkin, Campbell was in technology and sales roles, selling software contracts of every size, and realized how complex and rigid the contracts were getting as companies grew larger and the lack of price transparency increased. The complexity of some contracts can cause companies to overpay, even locking companies into payments they can’t afford, Campbell said.

On top of that, more buyers are younger now and their experience with purchasing software is pulling out their phone to download an app, while buying a customer relationship management tool will take six months to buy and cost thousands of dollars.

“Looking at the space, we are in a mirror maze of software, including companies using software to build products that they then sell back to the software companies,” Campbell said. “Companies are only buying software once a year, yet the process can be so complex.”

Tropic’s SaaS procurement model gathers the whole process under one platform. Unlike some competitors’ approaches, it takes on the heavy lifting so when companies have to buy or renew a contract, users can access Tropic’s one-click purchasing service to outsource the transaction. After the contracts are signed, its platform manages the technology and ensures financing is in order. This approach saves companies 23%, on average, on the software purchases, which Campbell said “moves the needle” for many companies where software is the No. 1 cost after salary.

In recent years, cloud software has become a fast-growing spend category across most businesses. Campbell said the average company can have more than 100 software contracts, while that jumps to over 500 for enterprise organizations. Meanwhile, global spend on enterprise software is forecasted to reach $599 billion by the end of 2021, a 13.2% increase over the previous year, according to Statista.

In the last 12 months, the company added over 60 customers, counting Qualtrics, Vimeo, Zapier and Intercom, surpassed $250 million in managed spend and processed transactions for over 1,200 vendors. The company is seeing 100% quarter over quarter growth, and in the last quarter, doubled its annual recurring revenue, Campbell said.

Tropic will use the funding for R & D and to deepen integrations with existing procurement tools in the cloud software ecosystem. Over the past year, the company’s headcount has grown to 50 and Campbell has “aggressive hiring plans between now and the rest of the year” focused on the tech side with engineering and product management.

Hootan Rashidifard, principal from Canaan Partners, said his firm was tracking the software procurement sector and learned about Tropic through Founder Collective, which led the company’s seed round.

“We’re seeing software and financial services converge and Tropic sits squarely at the intersection of both in a category with massive tailwinds,” Rashidifard said via email. “Software is accelerating the share of expenses while also penetrating every part of an organization, and software purchasing is becoming more decentralized. Tropic’s platform is in a fragmented market with high payment volume, which is ripe for layering on all kinds of adjacent services.”

Powered by WPeMatico

Another week, another unicorn IPO. This time, Sprinklr is taking on the public markets.

The New York-based software company works in what it describes as the customer experience market. After attracting over $400 million in capital while private, its impending debut will not only provide key returns to a host of venture capitalists but also more evidence that New York’s startup scene has reached maturity. (More evidence here.)

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Sprinklr last raised a $200 million round at a $2.7 billion valuation in September 2020. That round, as TechCrunch reported, also included a host of secondary shares and $150 million in convertible notes. Inclusive of the latter instrument, Sprinklr’s total capital raised to date soars above the $500 million mark.

Temasek Holdings, Battery Ventures, ICONIQ Capital, Intel Capital and others have plugged funds into Sprinklr during its startup days.

Temasek Holdings, Battery Ventures, ICONIQ Capital, Intel Capital and others have plugged funds into Sprinklr during its startup days.

Sure, Robinhood didn’t file last week as many folks hoped, but the Sprinklr IPO ensures that we’ll have more than just SPACs to chat about in the coming days. But one thing at a time. Let’s discuss what Sprinklr does for a living.

Sprinklr’s IPO filing and corporate website suffer from a slight case of corporate speak, so we have some work to do this morning to determine what the company does. Here’s what the company says about itself in its filing:

Sprinklr empowers the world’s largest and most loved brands to make their customers happier.

We do this with a new category of enterprise software — Unified Customer Experience Management, or Unified-CXM — that enables every customer-facing function across the front office, from Customer Care to Marketing, to collaborate across internal silos, communicate across digital channels, and leverage a complete suite of modern capabilities to deliver better, more human customer experiences at scale — all on one unified, AI-powered platform.

Not very clear, yeah? Don’t worry, I’ve got you. Here’s what the company actually does:

Powered by WPeMatico

Hot off the heels of our look into Marqeta’s IPO filing and dives into SPACs for Bright Machines and Bird, we’re parsing the WalkMe IPO filing. Later this week, Squarespace will direct list and we’ll see IPOs from Oatly and Procore. It’s a super busy time for public debuts of all sorts.

Given how hectic the IPO market is, we’re going to skip our usual throat clearing and dig into WalkMe’s IPO document. As always, we’ll start with a brief overview of its product and then move into discussing its financial performance.

Image Credits: Alex Wilhelm

WalkMe is the second Israel-based technology company to file to go public this week: No-code startup Monday.com is also pursuing an American IPO.

Alright! Into the breach.

WalkMe’s software provides visual overlays on websites that help users navigate the product in question. I base that explanation on my time at Crunchbase, which was a customer during at least part of my time there. WalkMe is popular with marketing teams who want to introduce users to a new or refreshed experience.

Per the company’s F-1 filing, other elements of its service that matter include its onboarding system and what WalkMe calls Workstation, or its “single interface to the applications within an enterprise and simplifies task completion through a natural language conversational interface and automation.” We’re including that last feature because it says “automation,” which, in the wake of the UiPath IPO, is a word worth watching. Investors are.

At a high level, WalkMe is a SaaS business, which means that when we digest its results we are digging into a modern software company. Let’s do just that.

From 2019 to 2020, WalkMe grew its revenues from $105.1 million to $148.3 million, a gain of 41%. In its most recent quarter, the company’s growth rate slowed: From Q1 2020 to Q1 2021, WalkMe’s top line grew 25% from $34.2 million to $42.7 million.

In SaaS terms, WalkMe calculates that its annual recurring revenue, or ARR, grew from $131.2 million at the end of 2019 to $164.3 million in 2020. In more granular terms, the company’s ARR grew from $137.8 million to $177.5 million in the first quarters of 2020, and 2021, respectively.

Powered by WPeMatico

Amount, a company that provides technology to banks and financial institutions, has raised $99 million in a Series D funding round at a valuation of just over $1 billion.

WestCap, a growth equity firm founded by ex-Airbnb and Blackstone CFO Laurence Tosi, led the round. Hanaco Ventures, Goldman Sachs, Invus Opportunities and Barclays Principal Investments also participated.

Notably, the investment comes just over five months after Amount raised $86 million in a Series C round led by Goldman Sachs Growth at a valuation of $686 million. (The original raise was $81 million, but Barclays Principal Investments invested $5 million as part of a second close of the Series C round). And that round came just three months after the Chicago-based startup quietly raised $58 million in a Series B round in March. The latest funding brings Amount’s total capital raised to $243 million since it spun off from Avant — an online lender that has raised over $600 million in equity — in January of 2020.

So, what kind of technology does Amount provide?

In simple terms, Amount’s mission is to help financial institutions “go digital in months — not years” and thus, better compete with fintech rivals. The company formed just before the pandemic hit. But as we have all seen, demand for the type of technology Amount has developed has only increased exponentially this year and last.

CEO Adam Hughes says Amount was spun out of Avant to provide enterprise software built specifically for the banking industry. It partners with banks and financial institutions to “rapidly digitize their financial infrastructure and compete in the retail lending and buy now, pay later sectors,” Hughes told TechCrunch.

Specifically, the 400-person company has built what it describes as “battle-tested” retail banking and point-of-sale technology that it claims accelerates digital transformation for financial institutions. The goal is to give those institutions a way to offer “a secure and seamless digital customer and merchant experience” that leverages Amount’s verification and analytics capabilities.

Image Credits: Amount

HSBC, TD Bank, Regions, Banco Popular and Avant (of course) are among the 10 banks that use Amount’s technology in an effort to simplify their transition to digital financial services. Recently, Barclays US Consumer Bank became one of the first major banks to offer installment point-of-sale options, giving merchants the ability to “white label” POS payments under their own brand (using Amount’s technology).

“The pandemic dramatically accelerated banks’ interest in further digitizing the retail lending experience and offering additional buy now, pay later financing options with the rise of e-commerce,” Hughes, former president and COO at Avant, told TechCrunch. “Banks are facing significant disruption risk from fintech competitors, so an Amount partnership can deliver a world-class digital experience with significant go-to-market advantages.”

Also, he points out, consumers’ digital expectations have changed as a result of the forced digital adoption during the pandemic, with bank branches and stores closing and more banking done and more goods and services being purchased online.

Amount delivers retail banking experiences via a variety of channels and a point-of-sale financing product suite, as well as features such as fraud prevention, verification, decisioning engines and account management.

Overall, Amount clients include financial institutions collectively managing nearly $2 trillion in U.S. assets and servicing more than 50 million U.S. customers, according to the company.

Hughes declined to provide any details regarding the company’s financials, saying only that Amount “performed well” as a standalone company in 2020 and that the company is expecting “significant” year-over-year revenue growth in 2021.

Amount plans to use its new capital to further accelerate R&D by investing in its technology and products. It also will be eyeing some acquisitions.

“We see a lot of interesting technology we could layer onto our platform to unlock new asset classes, and acquisition opportunities that would allow us to bring additional features to our platform,” Hughes told TechCrunch.

Avant itself made its first acquisition earlier this year when it picked up Zero Financial, news that TechCrunch covered here.

Kevin Marcus, partner at WestCap, said his firm invested in Amount based on the belief that banks and other financial institutions have “a point-in-time opportunity to democratize access to traditional financial products by accelerating modernization efforts.”

“Amount is the market leader in powering that change,” he said. “Through its best-in-class products, Amount enables financial institutions to enhance and elevate the banking experience for their end customers and maintain a key competitive advantage in the marketplace.”

Powered by WPeMatico

If businesses are going to meet their increasingly aggressive targets for reducing the greenhouse gas emissions associated with their operations, they’re going to have to have an accurate picture of just what those emissions look like. To get that picture, companies are increasingly turning to businesses like Sweep, which announced its commercial launch today.

The Parisian company boasts a founding team with an impeccable pedigree in enterprise software. Co-founders Rachel Delacour and Nicolas Raspal were the co-founders of BIME Analytics, which was acquired by Zendesk. And together with Zendesk colleagues Raphael Güller and Yannick Chaze, and the founder of the Net Zero Initiative, Renaud Bettin, they’ve created a software toolkit that gives companies a visually elegant view into not just a company’s own carbon emissions, but those of their suppliers as well.

It’s the background of the team that first attracted investors like Pia d’Iribarne, co-founder and managing partner, New Wave, which made their first climate-focused investment into the software developer.

“We decided to invest before we even closed the fund,” d’Iribarne said of the investment in Sweep. “We officially invested in December or January.”

New Wave wasn’t the only investor wowed by the company’s prospects. The new European climate-focused investment firm 2050, and La Famiglia, a fund with strong ties to big European industrial companies, also participated alongside several undisclosed angel investors from the Bay Area. In all Sweep raked in $5 million for its product before it had even launched a beta.

Sweep offers users the ability to visualize each location of a company’s business by brand, location, product or division and see how those different granular operations contribute to a company’s overall carbon footprint. Users can also link those nodes to external suppliers and distributors to share carbon data.

The effects of climate change are increasing, and companies across industries are motivated to do their part. But today’s carbon reduction efforts are being stalled by complex tools and resources that can’t match the urgency of the threat. By putting automation, connectivity and collaboration at the heart of the platform, Sweep is the first to offer companies an efficient mechanism to tackle their indirect Scope 3 emissions, and turn net zero from a buzzword into a reality.

Like the other companies that have come on the market with carbon monitoring and management solutions, Sweep also offers the ability to finance offset projects directly from its platform. And, like those other companies, Sweep’s offsets are primarily in the forestry space.

“Around the world, companies are under pressure from customers, investors and regulators to take action to reduce their emissions,” said Pia d’Iribarne in a statement. “As a result, we’re seeing unprecedented growth in the climate technology market and we expect it to continue to explode. What used to be an issue confined to a company’s sustainability team is now a front-and-center business objective that has the commitment of the CEO. We invested in Sweep because of their world-class expertise in sustainability and their success in developing state-of-the-art, end-to-end SaaS platforms. It’s the right team and the right product at the right time.”

Powered by WPeMatico

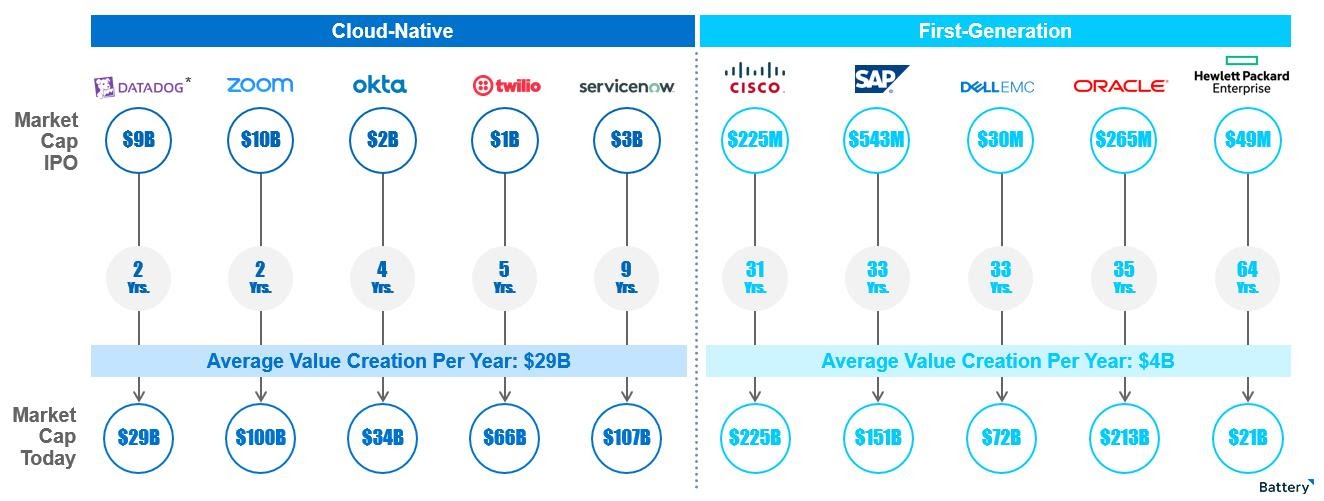

More than half a decade ago, my Battery Ventures partner Neeraj Agrawal penned a widely read post offering advice for enterprise-software companies hoping to reach $100 million in annual recurring revenue.

His playbook, dubbed “T2D3” — for “triple, triple, double, double, double,” referring to the stages at which a software company’s revenue should multiply — helped many high-growth startups index their growth. It also highlighted the broader explosion in industry value creation stemming from the transition of on-premise software to the cloud.

Fast forward to today, and many of T2D3’s insights are still relevant. But now it’s time to update T2D3 to account for some of the tectonic changes shaping a broader universe of B2B tech — and pushing companies to grow at rates we’ve never seen before.

One of the biggest factors driving billion-dollar B2Bs is a simple but important shift in how organizations buy enterprise technology today.

I call this new paradigm “billion-dollar B2B.” It refers to the forces shaping a new class of cloud-first, enterprise-tech behemoths with the potential to reach $1 billion in ARR — and achieve market capitalizations in excess of $50 billion or even $100 billion.

In the past several years, we’ve seen a pioneering group of B2B standouts — Twilio, Shopify, Atlassian, Okta, Coupa*, MongoDB and Zscaler, for example — approach or exceed the $1 billion revenue mark and see their market capitalizations surge 10 times or more from their IPOs to the present day (as of March 31), according to CapIQ data.

More recently, iconic companies like data giant Snowflake and video-conferencing mainstay Zoom came out of the IPO gate at even higher valuations. Zoom, with 2020 revenue of just under $883 million, is now worth close to $100 billion, per CapIQ data.

Image Credits: Battery Ventures via FactSet. Note that market data is current as of April 3, 2021.

In the wings are other B2B super-unicorns like Databricks* and UiPath, which have each raised private financing rounds at valuations of more than $20 billion, per public reports, which is unprecedented in the software industry.

Powered by WPeMatico

The world of enterprise software and cybersecurity has taken multiple body blows since COVID-19 demolished the in-person office, flinging employees across the world and forcing companies to adapt to an all-remote productivity model. The shift has required companies to rethink not only collaboration software, but also the infrastructure that powers it and the best way to protect assets once their security perimeters have been destroyed.

The pandemic has also dramatically increased the usage of digital services, forcing cloud providers to keep up with crushing demands for performance and reliability.

In short — it’s never been a better time to be an enterprise investor (or, possibly, a founder).

So I’m excited to announce our next guest in our Extra Crunch Live interview series: Asheem Chandna from Greylock, one of the top enterprise investors of the past two decades who has worked with multiple important founding teams from whiteboard to IPO. We’re scheduled for Thursday, November 5 at noon PST/3 p.m. EST/8 p.m. GMT (check that daylight savings time math!)

Login details are below the fold for EC members, and if you don’t have an Extra Crunch membership, click through to sign up.

For nearly two decades, Asheem Chandna has invested in enterprise and security startups at Greylock, with massive investment wins in Palo Alto Networks, AppDynamics and Sumo Logic. These days, he continues to invest in cybersecurity with companies like Awake Security and Abnormal Security, data platforms like Rubrik and Delphix, and the stealthy search engine company Neeva. As a leading early-stage investor and mentor in the space, he’s seen a multitude of companies transition from inception to product-market fit to IPO.

We’ll talk about what all the turbulence in enterprise means for the future of startups in the space, how cybersecurity is evolving given the new threat landscape and also discuss a bit about how the public markets and their aggressive multiples for Silicon Valley enterprise startups is changing the strategy of venture capitalists. Plus, we’ll talk about company building, developing founders as leaders and more.

Join us next week with Asheem on Thursday, November 5 at noon PST/3 p.m. EST/8 p.m. GMT. Login details and calendar invite are below.

Powered by WPeMatico