egnyte

Auto Added by WPeMatico

Auto Added by WPeMatico

Last night Datto priced its IPO at $27 per share, the top end of its range that TechCrunch covered last week. The data and security-focused software company had targeted a $24 to $27 per-share IPO price range, meaning that its final per-share value was at the top of its estimates.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The Datto IPO won’t draw lots of attention; its business is somewhat dull, as selling software to managed service providers rarely excites. But, the public offering matters for a different reason: It gives us a fresh lens into today’s IPO market.

That lens is the perspective of slower, more profitable growth. What is that worth?

The value of quickly growing and unprofitable software and cloud companies is well known. Snowflake made a splash earlier this year on the back of huge growth and enormous losses. Investors ate its shares up, pushing its valuation to towering heights. This year we’ve even seen rapid growth and profits valued by public investors in the form of JFrog’s IPO.

The value of quickly growing and unprofitable software and cloud companies is well known. Snowflake made a splash earlier this year on the back of huge growth and enormous losses. Investors ate its shares up, pushing its valuation to towering heights. This year we’ve even seen rapid growth and profits valued by public investors in the form of JFrog’s IPO.

But slower growth, software margins and profitability? Datto’s financial picture feels somewhat unique among the IPOs that TechCrunch has covered this year.

It’s a similar bet to the one that Egnyte is making; the enterprise software company crested $100 million ARR last year and announced that it grew by around 22% in the first half of 2020. And, it is profitable on an EBITDA basis. Therefore, the Datto IPO could provide a clue as to whether companies like Egnyte and the rest of the late-stage startup crop should be content to grow more slowly, but with the benefit of actually making money.

Here are the deal’s nuts and bolts:

Powered by WPeMatico

The pandemic has put stress on companies dealing with a workforce that is mostly — and sometimes suddenly — working from home. That has led to rising needs for security and governance tooling, something that Egnyte is looking to meet with new features aimed at helping companies cope with file management during the pandemic.

Egnyte helps customers manage files wherever they live — on premises or in the cloud. Over the years, it has added security and governance tooling to bring collaboration around files together with security and governance on a single platform.

“It’s no surprise that there’s been a rapid shift to remote work, which has I believe led to mass adoption of multiple applications running on multiple clouds, and tied to that has been a nonlinear reaction of exponential growth in data security and governance concerns,” Vineet Jain, co-founder and CEO at Egnyte, explained.

Egnyte’s announcements today are in part a reaction to the changes that COVID has brought, a mix of net-new features and capabilities that were on its road map, but accelerated to meet the needs of the changing technology landscape.

The company is introducing a new feature called Smart Cache to make sure that content (wherever it lives) that an individual user accesses most will be ready whenever they need it.

“Smart Cache uses machine learning to predict the content most likely to be accessed at any given site, so administrators don’t have to anticipate usage patterns. The elegance of the solution lies in that it is invisible to the end users,” Jain said. The end result of this capability could be lower storage and bandwidth costs, because the system can make this content available in an automated way only when it’s needed.

Another new feature is email scanning and governance. As Jain points out, email is often a company’s largest data store, but it’s also a conduit for phishing attacks and malware. So Egnyte is introducing an email governance tool that keeps an eye on this content, scanning it for known malware and ransomware and blocking files from being put into distribution when it identifies something that could be harmful.

As companies move more files around it’s important that security and governance policies travel with the document, so that policies can be enforced on the file wherever it goes. This was true before COVID-19, but has only become more true as more folks work from home.

Finally, Egnyte is using machine learning for auto-classification of documents to apply policies to documents without humans having to touch them. By identifying the document type automatically, whether it has personally identifying information or it’s a budget or planning document, Egnyte can help customers auto-classify and apply policies about viewing and sharing to protect sensitive materials.

Egnyte is reacting to the market needs as it makes changes to the platform. While the pandemic has pushed this along, these are features that companies with documents spread out across various locations can benefit from regardless of the times.

The company is over $100 million ARR today, and grew 22% in the first half of 2020. Whether the company can accelerate that growth rate in H2 2020 is not yet clear. Regardless, Egnyte is a budding IPO candidate for 2021 if market conditions hold.

Powered by WPeMatico

For much of the history of enterprise technology, companies tended to buy from a single vendor because it made managing the entire affair much easier while giving them a “single throat to choke” when something went wrong. On the flip side, it also put customers at the mercy of said vendor — and it wasn’t always pretty.

As we move deeper into the cloud model, many IT pros are looking for more flexibility than they had in the past, avoiding the vendor lock-in from the previous generation of enterprise tech, and what being beholden to a single vendor could mean for the bottom line and their own flexibility.

This is something that comes up frequently in discussions about moving workloads from one cloud to another, and is sometimes referred to as a multi-cloud approach. Customers are loath to leave their workloads in the hands of one vendor again and repeat the mistakes of the past. They are looking to have the same flexibility on the infrastructure side that they are getting in the SaaS world, where companies tend to purchase best-of-breed from multiple vendors.

That means, they want the freedom to move workloads between clouds, but that’s not always as easy a prospect as it might seem, and it’s an area where startups could help lead the way.

What’s stopping customers from just moving data and applications between clouds? It turns out that there is a complex interlinking of public cloud APIs that help the applications and data work in tandem. If you want to pull out of one public cloud, it’s not a simple matter of just migrating to the next one.

Powered by WPeMatico

Egnyte announced today it was combining its two main products — Egnyte Protect and Egnyte Connect — into a single platform to help customers manage, govern and secure the data from a single set of tools.

Egynte co-founder and CEO Vineet Jain says that this new single platform approach is being driven chiefly by the sheer volume of data they are seeing from customers, especially as they shift from on-prem to the cloud.

“The underlying pervasive theme is that there’s a rapid acceleration of data going to the cloud, and we’ve seen that in our customers,” Jain told TechCrunch. He says that long-time customers have been shifting from terabytes to petabytes of data, while new customers are starting out with a few hundred terabytes instead of five or ten.

As this has happened, he says customers are asking for a way to deal with this data glut with a single platform because the volume of data makes it too much to handle with separate tools. “Instead of looking at this as separate problems, customers are saying they want a solution that helps address the productivity part at the same time as the security part. That’s because there is more data in the cloud, and concerns around data security and privacy, along with increasing compliance requirements, are driving the need to have it in one unified platform,” he explained.

The company is doing this because managing the data needs to be tied to security and governance policies. “They are not ultimately separate ideas,” Jain says.

Jain says, up until recently, the company saw the data management piece as the way into a customer, and after they had that locked down, they would move to layer on security and compliance as a value-add. Today, partly due to the data glut and partly due to compliance regulations, Jain says, these are no longer separate ideas, and his company has evolved its approach to meet the changing requirements of customers.

Egnyte was founded in 2007 and has raised over $138 million on a $460 million post valuation, according to Pitchbook data. Its most recent round was $75 million led by Goldman Sachs in September, 2018. Egnyte passed the $100 million ARR mark in November.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re adding five names to the $100 million annual recurring revenue (ARR) club and listing all preceding members in a single post. This series, which was a bit of an accident, if I’m being honest, has included more than a dozen companies that have reached $100 million ARR, along with a handful more that are close.

Today we’re adding Seismic, ThoughtSpot, Noom, Riskified and Moveable Ink to the list. As always, we have funding histories, growth metrics and interviews below on the new group. But at this juncture, as we head toward the two-dozen company mark, it’s a good time to ask, what is this list that we’re compiling?

At first, the goal of the jokingly-named “$100 million ARR club” was to highlight companies that were of real scale, an idea designed to gently push back against the “unicorn” moniker. As more and more unicorns were born and the private-capital world became adept at getting startups of all maturity levels over the requisite $1 billion valuation threshold, the term began to feel too diluted to have much signaling value.

While, in contrast, $100 million in ARR felt much more “hard” to the valuation metric’s comparable squishiness. But, since that first post, more and more companies have written in, sharing hard metrics and the series has continued. Perhaps we’re really just compiling an IPO watchlist, a grouping of firms that will probably go (or should go) public in the next 18 months.

Let’s dig into our new additions. Then, we’ll list all our prior entrants with links to our preceding coverage in case you are playing catch up. With that, here’s the entire $100 million ARR club a list of companies that we think could go public inside the next six quarters.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re continuing our exploration of companies that have reached material scale, usually viewed through the lens of annual recurring revenue (ARR). We’ve looked at companies that have reached the $100 million ARR mark and a few that haven’t quite yet, but are on the way.

Today, a special entry. We’re looking at a company that isn’t yet at the $100 million ARR mark. It’s 60% of the way there, but with a twist. The company is bootstrapped. Yep, from pre-life as a consultancy that built a product to fit its own needs, Cloudinary is cruising toward nine-figure recurring revenue and an IPO under its own steam.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re adding four new names to the growing $100 million annual recurring revenue (ARR) club. The firms — Sisense, SiteMinder, Monday.com, and Lemonade — add diversity to our current group of yet-private companies which have reached the nine-figure recurring revenue threshold.

Our goal in tracking the companies in this high-flying cohort is to keep tabs on the private firms (often unicorns, it should be said) that could go public if needed. While not every unicorn will or could go public, companies with nine-figure ARR have a clear path to the public markets provided that their economics are in reasonable shape.

And we’ve seen some remarkably efficient companies meet the mark, including Egnyte with just $137.5 million raised, and Braze, with only $175 million on its books. For growth-oriented, venture-backed companies, those are efficient results.

But let’s add a few more members to the club today. Please meet our new centurions, centaurs, or whatever we end up calling them.

Sisense is a business intelligence company that merged with Periscope Data earlier this year. The combined firm has raised just over $200 million, according to Crunchbase, with the lion’s share of that landing in Sisense’s column (about $175 million).

What’s notable about the combination is that the two firms were public about saying that, when brought together, they would have combined ARR of $100 million. That was back in May. Today, Sisense has crested the $100 million mark by itself, according to an interview with TechCrunch. With Periscope added to the mix the company’s total ARR is naturally higher.

Sisense had a few original goals according to CEO Amir Orad, including helping businesses “take complex data and bring it together to get insights.” Its second focus is helping companies “take complex data sets and build [them out] as an analytical application in their products,” he said.

Periscope came into the picture when Orad and the smaller company’s CEO Harry Glaser (now Sisense’s CMO) started talking as friends about their respective markets. According to Orad, Glaser outlined a new sort of organization being built inside some companies that “were not traditional BI teams” or “traditional product teams,” but instead brought together “data engineers and data scientists and very capable individuals who [wanted] to make sense of [the] data sitting in the cloud.” Periscope had built “a very impressive business” supporting those new organizations, with “many hundreds of customers,” Orad said.

That meant that Sisense’s pair of focuses were somewhat two of out three, making the corporate combination an obvious bet.

Regarding what changed as Sisense grew, cresting the $50 million ARR mark and later the $100 million ARR mark, Orad told TechCrunch that what differed was “scale,” saying that at its size “what you do impacts more people, more individuals, more companies, [and] more customers.” (I have interesting notes on how the two companies managed their combination from a culture perspective, let me know if you’d like to read them.)

The first Australian member of the nine-figure ARR club is SiteMinder, which we’re letting in on a technicality; the firm’s ARR figure is in Australian dollars, which works out to around $70 million USD. However, its growth curve appears steep so we’re not too worried about including it a little early from a domestic dollar perspective.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the grey space in between.

Today we’re taking stock of a cohort of special companies: still-private startups that have reached $100 million in annual recurring revenue (ARR). Our goal is to understand which startup companies are actually exceptional. This late in the unicorn era, hundreds of companies around the world have reached a valuation of $1 billion, making the achievement somewhat pedestrian.

Reaching $100 million in ARR, however, still stands out.

We explored the idea earlier this week, citing Asana, Druva and WalkMe as private companies that recently reached $100 million ARR. In addition to that trio, Bill.com and Sprout Social, both of which went public this week, also crossed the nine-figure annual recurring revenue mark in 2019.

After we posted that short list, four other companies either just shy of $100 million ARR, or with a little bit more, reached out to TechCrunch, touting their own successes. Given that our point was that companies which reach the revenue threshold million are neat, it’s worth taking a moment to look at the other companies joining the $100 million ARR club.

For extra fun I got on the phone with a number of their CEOs to chat about their progress. We’ll start with a look at a company that is nearly a member of the club, and then talk about a few that recently punched their membership cards.

To be frank, I did not know that GitLab was as large as it is. Backed by more than $400 million in private capital, GitLab competes with the now-purchased GitHub as a developer resource and service. Its backers include Goldman Sachs, ICONIQ, GV, August Capital and Khosla.

GitLab became a unicorn back in September of 2018, when it raised $100 million at a $1 billion post-money valuation. Its more recent $268 million Series E raised this September pushed that valuation to nearly $2.8 billion.

It’s a good company for us to include, as it provides a good example of how far in advance a $1 billion valuation can precede a $100 million ARR business; in GitLab’s case, provided that it grows as expected, its unicorn valuation came nearly 1.5 years before reaching nine-figure ARR.

To understand more about the company’s growth, we caught up with its CEO Sid Sijbrandij (full discussion here), learning that he views the unicorn tag as a way to help a company brand itself, but something that is outside of his company’s control. Revenue, in his view, is “much more within your control.” According to Sijbrandij, GitLab is aiming for $1 billion in revenue in 2023 and has a November, 2020 IPO targeted.

GitLab is sharing its impending ARR milestone as it runs its whole business very transparently (hence why my chat with its CEO was live-streamed, and archived on YouTube). It will be super interesting to see if the company hits the ARR target on time, and then if it can also stick the landing with a Q4 2020 IPO.

Egnyte, a player in the enterprise productivity, storage and security spaces, has kept growing since its $75 million Series E it raised last October.

The company, backed by Goldman Sachs (again), GV (again) and Kleiner Perkins, has raised just $137.5 million to date. Reaching $100 million ARR on that level of funding means that Egnyte has run efficiently as a business. In fact, as TechCrunch has reported, Egnyte has occasionally made money on its path to the public markets.

TechCrunch has spoken to Egnyte’s CEO Vineet Jain a number of times, but it seemed appropriate to get him back on the phone now that his company is nearly ready to go public (at least in terms of size). According to Jain, in fresh data released to Extra Crunch:

Powered by WPeMatico

Egnyte announced today that customers can now store G Suite files inside its storage, security and governance platform. This builds on the support the company previously had for Office 365 documents.

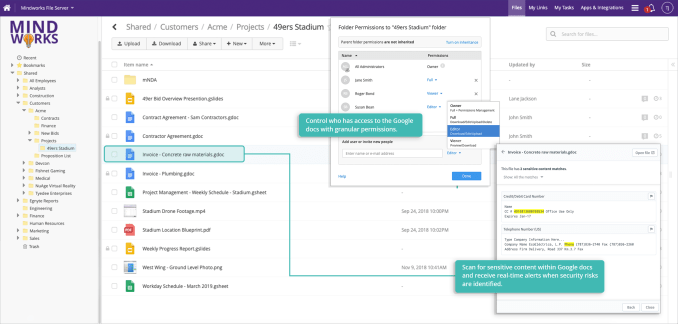

Egnyte CEO and co-founder Vineet Jain says that while many enterprise customers have seen the value of a collaborative office suite like G Suite, they might have stayed away because of compliance concerns (whether that was warranted or not).

He said that Google has been working on an API for some time that allows companies like Egnyte to decouple G Suite documents from Google Drive. Previously, if you wanted to use G Suite, you no choice but to store the documents in Google Drive.

Jain acknowledges that the actual integration is pretty much the same as his competitors because Google determined the features. In fact, Box and Dropbox announced similar capabilities over the last year, but he believes his company has some differentiating features on its platform.

“I honestly would be hard pressed to tell you this is different than what Box or Dropbox is doing, but when you look at the overall context of what we’re doing…I think our advanced governance features are a game changer,” Jain told TechCrunch.

What that means is that G Suite customers can open a document and get the same editing experience as they would get were they inside Google Drive, while getting all the compliance capabilities built into Egnyte via Egnyte Protect. What’s more, they can store the files wherever they like, whether that’s in Egnyte itself, an on-premises file store or any cloud storage option that Egnyte supports, for that matter.

G Suite documents stored on the Egnyte platform

Long before it was commonplace, Egnyte tried to differentiate itself from a crowded market by being a hybrid play where files can live on-premises or in the cloud. It’s a common way of looking at cloud strategy now, but it wasn’t always the case.

Jain has always emphasized a disciplined approach to growing the company, and it has grown to 15,000 customers and 600 employees over 11 years in business. He won’t share exact revenue, but says the company is generating “multi-millions in revenue” each month.

He has been talking about an IPO for some time, and that remains a goal for the company. In a recent letter to employees that Egnyte shared with TechCrunch, Jain put it this way. “Our leadership team, including our board members, have always looked forward to an IPO as an interim milestone — and that has not changed. However, we now believe this company has the ability to not only be a unicorn but to be a multi-billion dollar company in the long-term. This is a mindset that we all need to have moving forward,” he wrote.

Egnyte was founded in 2007 and has raised more than $137 million, according to Crunchbase data.

Powered by WPeMatico

Egnyte launched in 2007 just two years after Box, but unlike its enterprise counterpart, which went all-cloud and raised hundreds of millions of dollars, Egnyte saw a different path with a slow and steady growth strategy and a hybrid niche, recognizing that companies were going to keep some content in the cloud and some on prem. Up until today it had raised a rather modest $62.5 million, and hadn’t taken a dime since 2013, but that all changed when the company announced a whopping $75 million investment.

The entire round came from a single investor, Goldman Sachs’ Private Capital Investing arm, a part of Goldman’s Special Situations group. Holger Staude, vice president of Goldman Sachs Private Capital Investing will join Egnyte’s board under the terms of the deal. He says Goldman liked what it saw, a steady company poised for bigger growth with the right influx of capital. In fact, the company has had more than eight straight quarters of growth and have been cash flow positive since Q4 in 2016.

“We were impressed by the strong management team and the company’s fiscal discipline, having grown their top line rapidly without requiring significant outside capital for the past several years. They have created a strong business model that we believe can be replicated with success at a much larger scale,” Staude explained.

Company CEO Vineet Jain helped start the company as a way to store and share files in a business context, but over the years, he has built that into a platform that includes security and governance components. Jain also saw a market poised for growth with companies moving increasing amounts of data to the cloud. He felt the time was right to take on more significant outside investment. He said his first step was to build a list of investors, but Goldman shined through, he said.

“Goldman had reached out to us before we even started the fundraising process. There was inbound interest. They were more aggressive compared to others. Given there was prior conversations, the path to closing was shorter,” he said.

He wouldn’t discuss a specific valuation, but did say they have grown 6x since the 2013 round and he got what he described as “a decent valuation.” As for an IPO, he predicted this would be the final round before the company eventually goes public. “This is our last fund raise. At this level of funding, we have more than enough funding to support a growth trajectory to IPO,” he said.

Philosophically, Jain has always believed that it wasn’t necessary to hit the gas until he felt the market was really there. “I started off from a point of view to say, keep building a phenomenal product. Keep focusing on a post sales experience, which is phenomenal to the end user. Everything else will happen. So this is where we are,” he said.

Jain indicated the round isn’t about taking on money for money’s sake. He believes that this is going to fuel a huge growth stage for the company. He doesn’t plan to focus these new resources strictly on the sales and marketing department, as you might expect. He wants to scale every department in the company including engineering, posts-sales and customer success.

Today the company has 450 employees and more than 14,000 customers across a range of sizes and sectors including Nasdaq, Thoma Bravo, AppDynamics and Red Bull. The deal closed at the end of last month.

Powered by WPeMatico