Education

Auto Added by WPeMatico

Auto Added by WPeMatico

With the pandemic wreaking havoc amongst early years education amid school lockdowns, it’s no wonder edtech startups have piled into the space. But it has also served to highlight the abysmal nature of early years teaching: Some 40 million teachers across the globe are leaving the sector, according to the World Bank. Of the 1.5 billion primary-age children, only a few can access high-quality education, and approximately 58 million primary-age children are out of education, most of whom are girls.

So the opportunity to make a difference, using online teaching, in these very young years, is great, because classes sizes can be reduced online, and the quality of teaching improved.

This is the idea behind bina, which bills itself as a “digital primary education ecosystem”. It has now raised $1.4 million to aim at the education of 4- to 12-year-olds.

The funding round was led by Taizo Son, one of Japan’s billionaires. Other investors and advisors include Jutta Steiner, founder at Parity Technologies, the company behind Polkadot decentralized protocol, and Lord Jim Knight, ex-Minister of Education (U.K.).

Bina’s “schtick” is that it has very small online class sizes of six students (3x smaller than the OECD average).

It also boasts of “adaptive learning paths” that cover international standards; teachers with a minimum of eight years of digital teaching experience; and data-driven decision making for its pedagogical approach.

Noam Gerstein, bina’s CEO and founder said: “I’ve interviewed students, teachers and parents globally for years, and it is clear a new systemic design is needed. With our founding families, we are building a world in which every child has access to quality education, educators’ skills are valued and continuously developed, and parents don’t need to choose between their work and family life.”

He says it also grants pupils company shares (RSUs) as they grow with the school. Currently available to English-speaking students in the CET time zone, the bina School is planning a SaaS product for governments, NGOs and school systems.

“We right now compete against companies like Outschool, Pearson’s online Academy, Primer and Prisma,” he told me over a call. “So these are the big names of the last year for the first phase. But the strategy is that we’re building it in two phases. The first phase is actually building a school that we operate as a ‘lab’ school. And the second phase is what we call ‘bina as a service’. So it’s a SaaS ‘school as a service’. The idea is that we offer collaboration with NGOs and governments, doing accreditation and training and licencing of the product. So for that second part we’re actually competing against the big accreditation system.”

Powered by WPeMatico

If you’re trying to develop fluency in a non-native tongue, language immersion is a crucial part of the learning process. Surrounding yourself with native speakers helps with pronunciation, context building, and most of all, confidence.

But what if you’re an eight-year-old kid in Spain learning English and can’t swing a solo trip to the United States for the summer?

Novakid, founded by Maxim Azarov, wants to be your next best option. The San Francisco-based edtech startup offers virtual-only, English language immersion for kids between the ages of four through 12, by combining a mix of different services from live tutors to gamification.

After closing its $4.25 million Series A round last December, Novakid announced today that it is back with a $35 million Series B financing, led by Owl Ventures and Goodwater Capital. Existing investors also participated in the round, including PortfoLion, LearnStart, TMT Investments, Xploration Capital, LETA Capital and BonAngels.

The startup is raising capital in response to an active start to its year. The company’s active client base grew 350% year over year, currently at over 50,000 paying students. The money will be used to get more students into its universe of tools, as well as help Novakid expand into international markets with high populations of speakers who want to learn English.

The company’s suite of services are built around two principles: First, that it can immerse early-age learners into the world of English at scale, and second, that it can actually be fun to use.

When a user signs up, they are first connected to one of Novakid’s 2,000 live tutors for their first class. Tutors must be native English speakers with a B.A. degree or higher, as well as an international teaching certificate such as DELTA, CELTA, TESOL or TEFL.

“One of the things that is really important, even psychologically, is to start listening to the language, start interacting with a live person, and remove being afraid of not understanding something,” Azarov said. The company wants to recreate the conditions of how a kid likely learned their first language.

In the class, the tutors only speak English, and users are encouraged to do the same to slowly build and mistake their way into confidence. While the live, video-based classes are a key part of Novakid’s product, Azarov said it was important that his company “was not just giving you access to a teacher” as its main value proposition.

“Most of the competitors are taking teachers and making them available remotely so you don’t have to travel and you have a bigger selection,” he said. But if you look at the industry in the bigger picture, guys like Oxford, Cambridge, Pearson who provide content for the language learning industry, their product basically sucks. It’s really bad.” So, Novakid puts most of its energy into rebuilding a curriculum that works with better design, and includes games.

Gamified content lives both in and out of classes. Within the classroom, a teacher may take a student on a VR-enhanced tour through famous landmarks and museums to practice vocabulary. Self-paced content could look like a multiplayer “battle” between two students answering questions within a certain time period to get a better score. Novakid has an entire team dedicated to game design and development.

Students are clicking in. Novakid users spend two-thirds of their time on the website with tutors, and one-third with self-paced content that the company built in-house. The company wants to switch those concentrations because more students are spending time with the asynchronous content around grammar and vocabulary, and teachers are reserved for more complex information like speaking and conversation.

Part of the difficulty of scaling up a language learning business is that users need to stay motivated. Gamification helps with engagement, but Novakid’s clientele of children could also be fast to churn compared to adult learners, simply due to priorities. Azarov said that he sees how some would view selling exclusively to children as a disadvantage, but he views their focus as differentiation.

“You get better brand equity when you’re more focused,” he said. “The way kids learn language is vastly different from the way adults learn language, and I don’t think the general players who do ‘everything from everybody’ will be able to do [the former] as well as we are.” Duolingo recently launched Duolingo ABC, a free English literacy app with hundreds of short-form exercises. While the now-public company has strong branding, Novakid’s strategy differs by adding in more services around live learning and speaking.

So far, the company has proven that its strategy is sticking. Its revenue in 2020 was $9 million, and in 2021 it is expected to hit between $36 million to $45 million in revenue. It declined to disclose the specifics around diversity of the team, but plans to kick off a quite intensive recruiting spree going forward. Azarov plans to add 200 people to his 300-person company in the next six months.

Powered by WPeMatico

Duolingo landed onto the public markets this week, rallying excitement and attention for the edtech sector and its founder cohort. The language learning business’ stock price soared when it began to trade, even after the unicorn raised its IPO price range, and priced above the raised interval.

Duolingo’s IPO proves that public market investors can see the long-term value in a mission-driven, technology-powered education concern; the company’s IPO carries extra weight considering the historically few edtech companies that have listed.

Duolingo’s IPO proves that public market investors can see the long-term value in a mission-driven, technology-powered education concern; the company’s IPO carries extra weight considering the historically few edtech companies that have listed.

For those that want the entire story of Duolingo, from origin to messy monetization to historical IPO, check out our EC-1. It has dozens of interviews from executives, investors, linguists and competitors.

For today, though, we have fresh additions. We sat down with Duolingo CEO Luis von Ahn earlier in the week to discuss not only his company’s IPO, but also what impact the listing may have on startups. Duolingo’s IPO can be looked at as a case study into consumer startups, mission-driven companies that monetize a small base of users, or education companies that recently hit scale. Paraphrasing from von Ahn, Duolingo doesn’t see itself as just an edtech company with fresh branding. Instead, it believes its growth comes from being an engineering-first startup.

Selling motivation, it seems, versus selling the fluency in a language is a proposition that international consumers are willing to pay for, and an idea that investors think can continue to scale to software-like margins.

Duolingo has gone through three distinct phases: Growth, in which it prioritized getting as many users as it could to its app; monetization, in which it introduced a subscription tier for survival; and now, education, in which it is focusing on tacking on more sophisticated, smarter technology to its service.

Powered by WPeMatico

News that China’s government may force domestic tutoring-focused companies to go nonprofit is taking a huge bite out of the value of several technology companies. Bloomberg notes that the value of companies like New Oriental Education & Technology Group and TAL Education are tumbling in light of the news, which would constitute merely the latest salvo against tech companies in the autocratic country.

New Oriental’s Hong Kong-listed shares fell 44.22% in after-hours trading after the nonprofit news broke, while NYSE-shares of TAL are off an even sharper 51.75% in pre-market trading. With Yahoo Finance listing a roughly $13.8 billion market cap for TAL ahead of its impending declines at the market open, billions of equity value are about to get deleted. The list goes on: China Online Education Group is off 39.97% in after-hours trading, for example.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

A new decision by China’s government to exert more control over a sector of its domestic economy should not surprise. And we shouldn’t be shocked that online tutoring is in the country’s targets; today’s news is a follow-up to prior regulatory action in the sector from earlier in the year.

As China has become synonymous with edtech startups in recent years, the news impacts more than just public companies. The expected rules change may also hit a host of private, venture-backed companies.

As China has become synonymous with edtech startups in recent years, the news impacts more than just public companies. The expected rules change may also hit a host of private, venture-backed companies.

For example, what will happen to Yuanfudao? The company was valued at $15.5 billion last year, offering what TechCrunch described as “live tutoring, an online Q&A arm and a math-problem-checking arm.” Will the company see its wings clipped?

Or how about Zuoyebang, which raised $1.6 billion in a single round last year? TechCrunch wrote that Zuoyebang offers “online courses, live lessons and homework help for kindergarten to 12th grade students.” Is it in trouble as well?

All this comes on the same day that shares in Zomato began to float, with the Indian online food delivery company seeing its shares close up nearly 65% in their first day’s trading. TechCrunch has viewed the Zomato IPO as a possible bellwether for the larger Indian startup market, and the results augur well for other growth-focused, loss-making unicorns in the country.

Powered by WPeMatico

French startup PowerZ has raised another $8.3 million (€7 million at today’s exchange rate) including $1.2 million (€1 million) in debt — the rest is a traditional equity round. The company is both an edtech startup and a video game studio with an ambitious goal — it wants to build a game that is as engaging as Minecraft or Fortnite, but with a focus on education.

In February, PowerZ launched the first version of its game on computers. It doesn’t have a lot of content, but the company wanted to start iterating as quickly as possible. Aimed at kids who are six years old and over, PowerZ teleports the player into a fantasy world with cute dragons and magic spells.

“The idea is really to build a sort of Harry Potter,” co-founder and CEO Emmanuel Freund told me. “You have this world that is super nice and very interesting. Like with Hogwarts, you want to come back regularly, and the story will progress over a very long time.”

15,000 children tried out the first chapter. On average, they spent four hours in the game. I asked whether Freund was satisfied with those metrics. He told me he thought his company’s vision was “completely validated.”

Bpifrance Digital Venture, RAISE Ventures and Bayard are investing in today’s round. Existing investors Educapital, Hachette Livres, Pierre Kosciusko-Morizet and Michaël Benabou are also investing once again.

Image Credits: PowerZ

Now, it’s time to add content, expand to other platforms and launch new languages. When it comes to content, the company wants to partner with other game studios. They’re going to create new islands and design games that make you learn new stuff. Zero Games, Opal Games and ArkRep are the first third-party studios to contribute to PowerZ.

When those new chapters are available, kids will be able to practice mental calculation, geometry, vocabulary, foreign languages, sign language, but also astronomy, photography, architecture, sculpture, cooking, wildlife, yoga, etc.

“Basically we want to position ourselves as a publisher,” Freund said. “The only thing we want to keep in-house is the main storyline.”

As for new platforms, PowerZ is launching its game on the iPad this week. The company realized that launching on computers was a mistake. Adults are already using computers or don’t want to leave your kid on the computer. That’s why PowerZ is starting with the iPad and the iPhone will follow suite. In 2022, the company expects to release its game on the Nintendo Switch and potentially other game consoles.

While the game is only available in French for now, the startup is also thinking about launching an English version soon.

“The game is completely free right now. We have an idea to monetize it. We’ll copy every other games with in-app purchases for visual items,” Freund said.

When you look further down the roadmap, PowerZ has some radically ambitious goals. Freund believes that educational games will become mainstream really quickly. Many companies don’t want to develop this kind of stuff because screens are bad for kids.

“If we just say that screens are bad, we’ll end up with an Amazon product to learn math. I feel a sense of urgency to develop an educational platform for screens that can scale,” Freund told me.

PowerZ wants to reach hundreds of thousands of children as quickly as possible. And just like Fortnite or Minecraft, the company believes its game can act as a platform for other stuff that can evolve over time.

Powered by WPeMatico

Edtech startup Microverse has tapped new venture funding in its quest to help train students across the globe to code through its online school that requires zero upfront cost, instead relying on an income-share agreement that kicks in when students find a job.

The startup tells TechCrunch it has closed a $12.5 million Series A led by Northzone with additional participation from General Catalyst, All Iron Ventures and a host of angel investors. We last covered the company after it had closed a bout of seed funding from General Catalyst and Y Combinator; this latest round brings the startup’s total funding to just under $16 million.

The company’s vision has seen added pandemic-era traction as larger tech companies have embraced remote work that spans geographic boundaries and time zones. Microverse has now brought English-speaking students from over 188 countries through its program.

Since we last chatted, CEO Ariel Camus says the startup has landed some 300 early graduates in positions at tech companies including Microsoft, VMWare and Huawei. The company says its has above a 95% employment rate for its students within six months of graduation so far, pushing past one of the bigger issues that income-share-agreement-based schools have had stateside — getting graduates employed.

Microverse does have notably less generous terms than counterparts like Lambda School when it comes to when students begin loan repayment, the terms of both are actually quite different, as noted in my previous article:

While Lambda School’s ISA terms require students to pay 17% of their monthly salary for 24 months once they begin earning above $50,000 annually — up to a maximum of $30,000, Microverse requires that graduates pay 15% of their salary once they begin making more than just $1,000 per month, though there is no cap on time, so students continue payments until they have repaid $15,000 in full. In both startups’ cases, students only repay if they are employed in a field related to what they studied, but with Microverse, ISAs never expire, so if you ever enter a job adjacent to your area of study, you are on the hook for repayments. Lambda School’s ISA taps out after five years of deferred repayments.

The startup has made efforts to streamline their online program since launch to ensure that students are being set up to succeed in the full-time, 10-month program. Part of Microverse’s efforts have included condensing lesson segments into shorter time frames to ensure students aren’t starting the program unless they have enough free time to commit. Camus says the startup is receiving thousands of applications per month, of which only a fraction are accepted in an effort to ensure that the small startup isn’t overcommitting itself early on. The startup estimates it will usher 1,000 students through its program this year.

The startup has big plans for the future, including working more closely with tech companies to ensure that students have easier access to job placement once they graduate.

“We have data now that the day we launch a partner program — which we haven’t done yet but we will eventually — it opens up the market by 5x,” Camus tells TechCrunch. “To get 10,000 students per year in a world where 90% of the world’s population doesn’t have access to higher education — it’s not going to be that hard, to be honest, I’m not too worried.”

Powered by WPeMatico

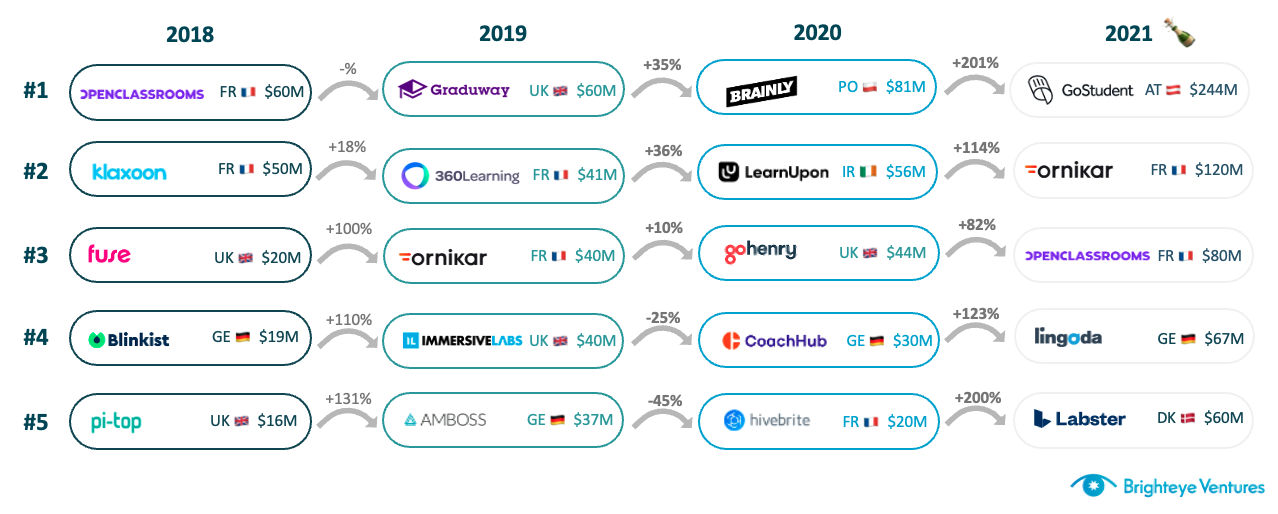

Last week was a good one for edtech in Europe.

GoStudent became Europe’s first edtech unicorn (IPO’d companies aside), raising its third round in 12 months and the biggest ever in the sector in Europe. Brighteye Ventures’ analysis showed that VC investments in European edtech had breached $1 billion in a calendar year for the first time, even without GoStudent’s mega-round, with six months left to go.

Edtech deal flow in 2021 looks set to match or even outpace 2020 levels, per the report: At $9.4 million, average deal size is triple 2020 levels; seven companies have raised $50 million in five different markets; and the U.K. has more than three times as many deals as the next individual market.

Deal-size progression in edtech over the years. Image Credits: Brighteye Ventures

It’s interesting that we are not seeing enormous increases in deal count. The $1.05-billion mark in the report is spread across 111 transactions — there were 237 in 2020, so we could expect a similar total this year. More funding and stable deal count of course means that we are seeing significant increases in deal size.

It seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

We can draw a few conclusions from this. We can construe that companies created last year and in previous years matured significantly during the pandemic due to increased demand. Moreover, this rapid natural selection process provided insights on verticals and possible winners.

Lastly, it seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

This is contributing to larger early rounds than we have seen in previous years — investors can’t pick the winner, but they can slant the playing field instead. We therefore expect to see a surge in the number of pre-seed, seed and Series A rounds in the second half of 2021, as companies founded during the pandemic begin to raise meaningful funding.

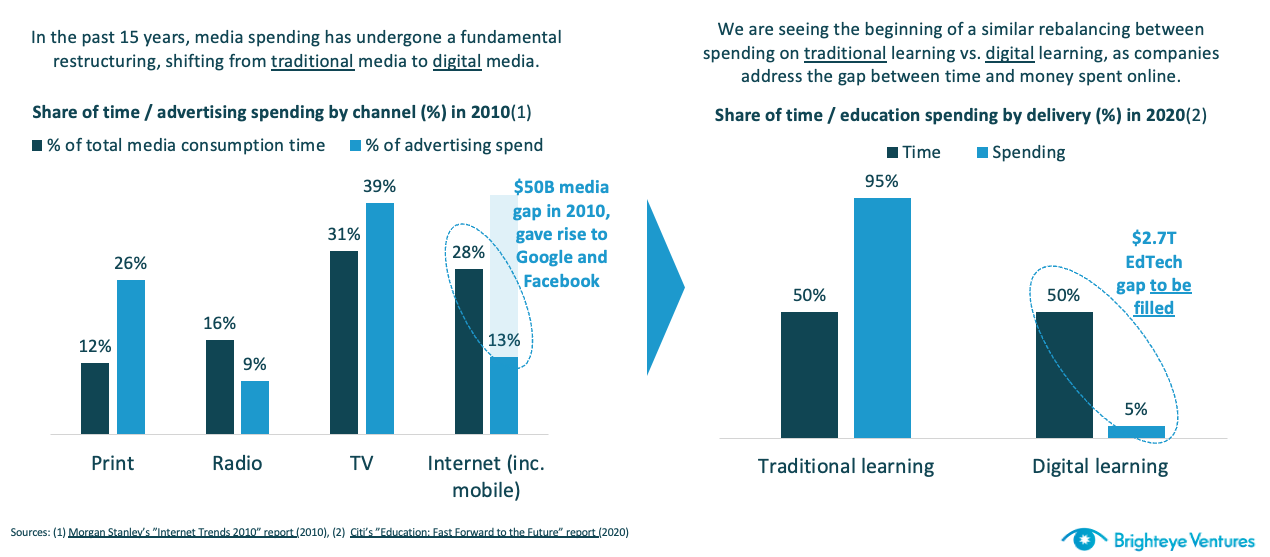

Another reason that edtech is being taken seriously by generalist investors is that the true size of the market (and the extent of digitization to come) is becoming more conceivable.

Edtech spending is growing like media spending did in the 2010s. Image Credits: Brighteye Ventures

Powered by WPeMatico

Most companies don’t announce their first venture investment after almost 20 years in the business, nor do they announce that round is the equivalent of a good startup’s entire private fundraising history. But Articulate, a SaaS training and development platform, is not your typical company and today it announced a whopping $1.5 billion investment on a $3.75 billion valuation.

You can call it Series A if you must label it, but whatever it is, it’s a hefty investment by any measure. General Atlantic led the round with participation from Blackstone Growth and Iconiq Growth. GA claims it’s one of the largest A rounds ever, and I’m willing to bet it’s right.

CEO Adam Schwartz founded the company with his life savings in 2002 and hasn’t taken a dime of outside investment since. “Our software enables organizations to develop, deliver, and analyze online training that is engaging and effective for enterprises and SMBs,” Schwartz explained.

He says that the company started back in 2002 as a plug-in for PowerPoint. Today it is a software service with the goal of helping enable everyone to deliver training, even if they aren’t a training professional. Articulate actually has two main products, one is a set of tools for companies building training that connects to an enterprise learning management system or LMS. The other is aimed at SMBs or departments in an enterprise.

Its approach seems to be working with the company reporting it has 106,000 customers across 161 countries including every single one of the Fortune 100. Schwartz was loath to share any additional metrics, but did say they hope to use this money to grow 10x over the next several years.

Company president Lucy Suros, who has been with the organization for a decade, says even with this success, they see plenty of opportunity for growth and they felt taking this capital now would really enable them to accelerate.

“We are the most dominant player by far in course authoring apps, but when you look at that whole ecosystem and you think about where companies are in transforming from instructor-led training to online training, they’re still really in the early innings so there’s a lot of opportunity,” she said.

Anton Levy, co-president and managing director at General Atlantic, who is leading the investment for the firm, says that this is a “big, bold, incredible business” and that’s why they’re making an investment of this size and scope. “The reason we’re stepping up in such a large way, and what’s such a large check for us, is because of the business they’ve built, the team they’ve built, and frankly the market opportunity that they’re playing in and their ambition,” he said.

Today the company has 300 employees and they have been working as a remote company long before COVID. With the new capital, that number could triple over the next several years. Suros says that when she started at the company, there were 50 employees, mostly male engineers and she went to work to make it a more diverse work environment.

“We’ve put emphasis and a lot of just structural things in place to ensure that we are bringing more [diverse] people to the table, and then supporting folks once they’re here,” she said. With the new capital, the company announced a lot of new benefits and she said those were developed with the idea of helping break down barriers for under-represented groups in their ranks including covering gender transition-related costs.

She says that one of the benefits of becoming more visible as a company is being able to talk about and their human-centered organization framework, the set of principles the company put in place to define its values. “[We think about] how that can impact the employees and drive human flourishing for its own sake, and that also happens to lead to better business outcomes. But we’re really also interested in it from [the standpoint that] we want to be good and do good in the world and promote human flourishing at work,” she said.

The company seems to have been doing just fine up until now, but with this kind of capital, it aims to take the business to another level, while trying to be good corporate citizens as they do that.

Powered by WPeMatico

Duolingo filed to go public yesterday, giving the world a deep look inside its business results and how the pandemic impacted the edtech unicorn’s performance. TechCrunch’s initial read of the company’s filing was generally positive, noting that its growth was impressive and its losses modest; Duolingo recently began making money on an adjusted basis.

While the company’s top-level numbers are impressive, we want to go one level deeper to grow our understanding of the company beyond our EC-1.

Duolingo is likely entering a period in which it will have to invest heavily in features like pronunciation, efficacy and new apps — which could come at a steep upfront cost.

First, we’ll explore the growth of Duolingo’s total user base, how much money it makes per active user, and how effectively the company has managed to convert free users to paid products over time. The numbers will set us up to understand what else can be learned about Duolingo’s business beyond our original deep dive into the company’s finances — specifically underscoring the pressure cooker it finds itself in when looking for new revenue sources.

Starting with Duolingo’s growth in total active users, guess how fast they rose from 2019 to 2020. Hold that number in your head.

The actual numbers are as follows: In 2019, Duolingo closed the year with 27.3 million monthly active users (MAUs); it wrapped 2020 with 36.7 million MAUs. That’s a gain of 34%. If we narrow our gaze to Q1 2021 numbers compared to Q1 2020, we can see that Duolingo’s MAUs rose from 33.5 million to 39.9 million, or growth of around 19%.

The bulk of Duolingo’s growth, then, came in early 2020 when we consider its pandemic bump. Put more simply, the company scaled from 27.3 million MAUs at the end of 2019 to 33.5 million MAUs at the end of Q1 2020; from then, the company added 3.2 million more MAUs throughout 2020 and 6.4 million during the next four quarters.

Another lens through which to view the numbers is simply a recognition that first-quarter results at Duolingo appear to be stronger than results in the rest of the year, perhaps due to New Year’s resolutions to learn a new language or brush up on a second language learned in high school.

Next, let’s examine Duolingo’s monetization efforts regarding converting free users to paying users.

Here we can see a very different growth story. While the company’s MAUs rose 34% from 2019 to 2020, the company’s paying users rose from 900,000 at the end of 2019 to 1.6 million at the end of 2020. That is a far sharper gain of 84% on a year-over-year basis.

So, while Duolingo did see material user growth during 2020, it saw turbocharged expansion in the users it was able to shake revenue from. Improved monetization, more than acceleration in user growth, was the pandemic’s effect on Duolingo.

What can we see in the company’s more recent results? From Q1 2020 to Q1 2021, Duolingo’s paid subscribers rose from 1.1 million to 1.8 million, a gain of around 64%. That was a slower pace than the company managed more generally in 2020, which matches Duolingo’s slower revenue growth in Q1 2021 than it recorded in 2020.

The number is still strong, we think. But not as impressive as the more than 100% revenue expansion that the company put on the board last year.

In percentage terms, 3.3% of Duolingo’s MAUs were paid subscribers in 2019. That figure rose to 4.4% in 2020. And in Q1 2021, it reached 4.5%. Duolingo rounds that number to 5% in its S-1, which feels somewhat aggressive to us, given the somewhat modest pace at which the metric is improving. Here’s the wording:

As of March 31, 2021, approximately 5% of our monthly active users were paid subscribers of Duolingo Plus. Our paid subscriber penetration has increased steadily since we launched Duolingo Plus in 2017 and, combined with our user growth, has led to our revenue more than doubling every year since.

A gain of 0.1 percentage point in a quarter is growth, we suppose.

Next, let’s chat about revenue per MAU. To get consistent numbers, we’ll divide quarterly revenues by MAU figures from the same period. So, we’ll compare Q4 2019 revenue at Duolingo with its year-end MAU figure. We’ll do the same for 2020, and for Q1 2021 we’ll use both numbers from that period.

Powered by WPeMatico

Last fall, Facebook announced it was opening an office in Lagos, Nigeria, which would provide the company with a hub in the region and the first office on the continent staffed with a team of engineers. We’ve now spotted one of the first products to emerge from this office: an education-focused mobile app called Sabee, which means “to know” in Nigerian Pidgin. The app aims to connect learners and educators in online communities to make educational opportunities more accessible.

The app was briefly published to Google Play by “NPE Team,” the internal R&D group at Facebook, which has typically focused on new social experiences in areas like dating, audio, music, video, messaging and more.

While the learnings from the NPE Team’s apps sometimes inform broader Facebook efforts, the group hasn’t yet produced an app that has graduated to become a standalone Facebook product. Many of its earlier apps have also shut down, including (somewhat sadly), the online zine creator Eg.g, video app Hobbi, calling app CatchUp, friend-finder Bump, podcast community app Venue, and several others.

Sabee, however, represents a new direction for the NPE Team, as it’s not about building yet another social experiment.

Instead, Sabee is tied to Facebook’s larger strategy of focusing more on serving the African continent, starting with Nigeria. This is a strategic move, informed by data that indicates a larger majority of the world’s population will be in urban centers by 2030, and much of that will be on the African continent and throughout the Middle East. By 2100, Africa’s population is expected to have tripled, with Nigeria becoming the second-most populated country in the world, behind China.

Image Credits: Facebook NPE Team

To address the need to connect these regions to the internet, Facebook teamed with telcos on 2Africa, a subsea cable project that aims to serve the over 1 billion people still offline in Africa and the Middle East. These aren’t altruistic investments, of course — Facebook knows its future growth will come from these demographics.

Facebook confirmed its plans for Sabee to TechCrunch after we discovered it, noting it was still a small test for the time being.

“There are 50 million learners, but only 2 million educators in Nigeria,” said Facebook Product Lead, Emeka Okafor. “With this small, early test, we’re hoping to understand how we can help educators build communities that make education available to everyone. We look forward to learning with our early testers, and deciding what to do from there.”

Image Credits: Facebook NPE Team

The disparity between learners and educators in Nigeria greatly impacts women and girls, which is another key focus for Sabee — and the NPE Team’s efforts in the region as a whole. The company also wants to explore how to better serve groups who are often left behind by technology. On this front, Sabee is working to create an experience that works with low connectivity, like 2G.

We understand the app is currently in early alpha testing with fewer than 100 testers who are under NDA agreements with Facebook. It’s not available for anyone else beyond that group at present, but the company hopes to scale Sabee to the next stage before the end of the year.

There is no way to sign up for a Sabee waitlist, and the app is no longer public on Google Play. It was available so briefly that it was never ranked on any charts, app store intelligence firm Sensor Tower confirmed to us.

We should note that “sabee” and “sabi/sabis” have other, less-polite meanings in different languages, per Urban Dictionary. But the team has no plans to change the name for now as it makes sense in the Nigerian market where the app is targeted.

Powered by WPeMatico