education technology

Auto Added by WPeMatico

Auto Added by WPeMatico

Ironhack, a company offering programming bootcamps across Europe and North and South America, has raised $20 million in its latest round of funding.

The Miami-based company (with locations in Amsterdam, Barcelona, Berlin, Lisbon, Madrid, Mexico City, Miami, Paris and São Paulo) said it will use the money to build out more virtual offerings to complement the company’s campuses.

Over the next five years, 13 million jobs will be added to the tech industry in the U.S., according to Ironhack co-founder Ariel Quiñones. That’s in addition to another 20 million jobs that Quiñones expects to come from the growth of the technology sector in the EU.

Ironhack isn’t the only bootcamp to benefit from this growth. Last year, Lambda School raised $74 million for its coding education program.

Ironhack raised its latest round from Endeavor Catalyst, a fund that invests in entrepreneurs from emerging and underserved markets; Lumos Capital, which was formed by investors with a long history in education technology; Creas Capital, a Spanish impact investment firm; and Brighteye, a European edtech investor.

Prices for the company’s classes vary by country. In the U.S. an Ironhack bootcamp costs $12,000, while that figure is more like $3,000 for classes in Mexico City.

The company offers classes in subjects ranging from web development to UX/UI design, and data analytics to cybersecurity, according to a statement.

“We believe that practical skills training, a supportive global community and career development programs can give everyone, regardless of their education or employment history, the ability to write their stories through technology,” said Quiñones.

Since its launch in 2013, the company has graduated more than 8,000 students, with a job placement rate of 89%, according to data collected as of July 2020. Companies who have employed Ironhack graduates include Capgemini, Siemens and Santander, the company said.

Powered by WPeMatico

School district technology budgets are tight. But Kami CEO and founder Hengjie Wang wanted to make his company’s digital classroom product a go-to tool anyway.

He landed on trying to disrupt the printers.

Wang found that school districts spend an average of $150,000 every year on printed materials. Kami helps teachers digitize worksheets so students can digitally annotate them. Doing the math, Wang says Kami can save districts an estimated $80,000 by getting rid of the need to print handouts every day.

“Districts are apprehensive on paying for tools unless you can also save them money at the same time,” Wang said. With this tactic, the number of school districts using Kami doubled between March and July, going from from 9,987 districts to 17,915 districts. Sales for the startup, which was founded in 2013, grew over 2,000%. Today, Kami is a cash-flow positive business that sells to schools and parents.

When it comes to wide-scale and equitable adoption for edtech startups, success can often hinge on landing contracts that extend to an entire school network. However, budget cuts and red tape have often limited a company’s ability to grow. During the pandemic, consumer edtech startups such as live tutoring or question and answer services have soared now that more kids are learning from home.

However, a second surge in edtech might be upon us. As schools seek to reopen with a hybrid learning solution, Kami and other startups are finding opportunity in one of the hardest institutions to sell to: K-12 school districts.

Powered by WPeMatico

As schools stay closed and summer camp seems more like a germscape than an escape, students are staying at home for the foreseeable future and have shifted learning to their living rooms. Now, Norwegian educational gaming company Kahoot — the popular platform with 1.3 billion active users and over 100 million games (most created by users themselves) — has raised a new round of funding of $28 million to keep up with demand.

The Oslo-based startup, which started to list some of its shares on Oslo’s Merkur Market in October 2019, raised the $28 million in a private placement, and said it also raised a further $62 million in secondary shares. The new equity investment included participation from Northzone, an existing backer of the startup, and CEO Eilert Hanoa. While it’s not a traditional privately held startup in the traditional sense, at the market close today, the company’s valuation was $1.39 billion (or 13.389 billion Norwegian krone).

Existing investors in the company include Disney and Microsoft, and the company has raised $110 million to date.

Kahoot launched in 2013 and got its start and picked up most of its traction in the world of education through its use in schools, where teachers have leaned on it as a way to provide more engaging content to students to complement more traditional (and often drier) curriculum-based lessons. Alongside that, the company has developed a lucrative line of online training for enterprise users as well.

The global health pandemic has changed all of that for Kahoot, as it has for many other companies that built models based on classroom use. In the last few months, the company has boosted its content for home learning, finding an audience of users who are parents and employers looking for ways to keep students and employees more engaged.

The company says that in the last 12 months it had active users in 200 countries, with more than 50% of K-12 students using Kahoot in a school year in that footprint. On top of that, it is also used in some 87% of “top 500” universities around the world, and that 97% of Fortune 500 companies are also using it, although it doesn’t discuss what kind of penetration it has in that segment.

It seems that the coronavirus outbreak has not impacted business as much as it has in some sectors. According to the midyear report it released earlier this week, Q2 revenue is expected to be $9 million, 290% growth compared to last year and 40% growth compared to the previous quarter, and for the full year 2020, it expects revenue between $32 million and $38 million, with a full IPO expected for 2021.

As it has been doing even prior to the coronavirus outbreak, Kahoot has also continued to invest in inorganic growth to fuel its expansion. In May, it acquired math app maker DragonBox for $18 million in cash and shares. The company also runs an accelerator, Kahoot Ignite, to spur more development on its platform.

However, Hanoa said that Kahoot is shifting its focus to now also work with more mature edtech businesses.

“When we started out, we were primarily receiving requests on early stage products,” he said. “Now we have the opportunity to consider mature services for either integration or corporation. It’s a different focus.”

Update: A previous version of this story said that DragonBox was acquired in March. It was acquired in May. The story has been updated to reflect this change.

Powered by WPeMatico

The American South may not be the first region that comes to mind when you hear the phrase “hotbed of tech entrepreneurship,” but, slightly misguided perceptions aside, it’s home to a diverse and growing collection of startups.

Here, we’re going to take a deep dive into the startup funding data for the region.

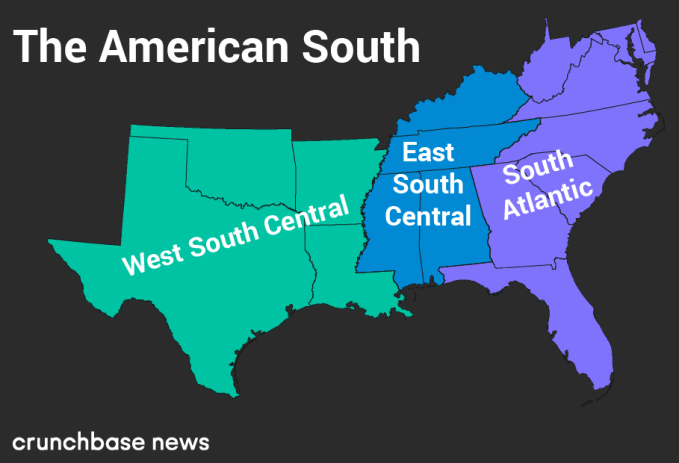

Just like it’s a common pastime for many city dwellers to argue about the precise boundaries of neighborhoods, there’s often some disagreement about the exact contours of the U.S.’s various regions. To quash rabble-rousing from the get-go, we’re using the U.S. Census Bureau’s definition of “the South” on its official map of the United States. Below, we display a map of the states we’re going to look at today.

Much like barbecue, the South is not a monolithic concept. So to incorporate some regional flavor into the following analysis, we’re also going to use the same regional divisions that the U.S. Census Bureau uses.

By doing this, we’ll be able to get a better idea of the relative contribution states from each sub-region make to startup activity in the South overall.

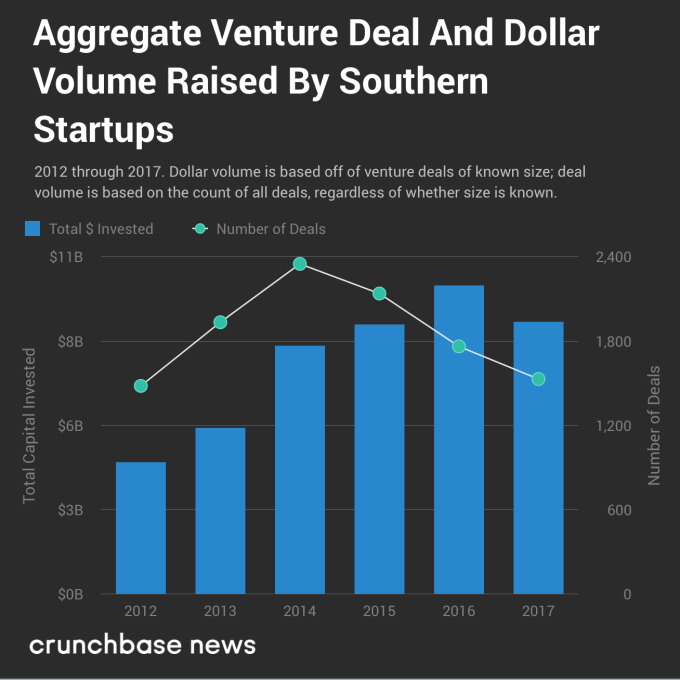

As is the case with most of the country, the South appears to be experiencing a shift in startup funding as we move toward the latter half of a bull run in entrepreneurial activity. The chart below shows a divergence in overall deal and dollar volume over time.

Much like in the rest of the U.S., reported deal and dollar volume are heading in different directions. Part of this may be due to reporting delays — it can sometimes take a few years for seed and early-stage rounds to get added to databases like Crunchbase’s . Nonetheless, there is a slow and generally upward creep in round sizes at most stages of funding. And that’s not just a Southern thing; it’s a country-wide trend.

Let’s disaggregate these figures a bit. We’ll start with deal counts and move on to dollar volume from there.

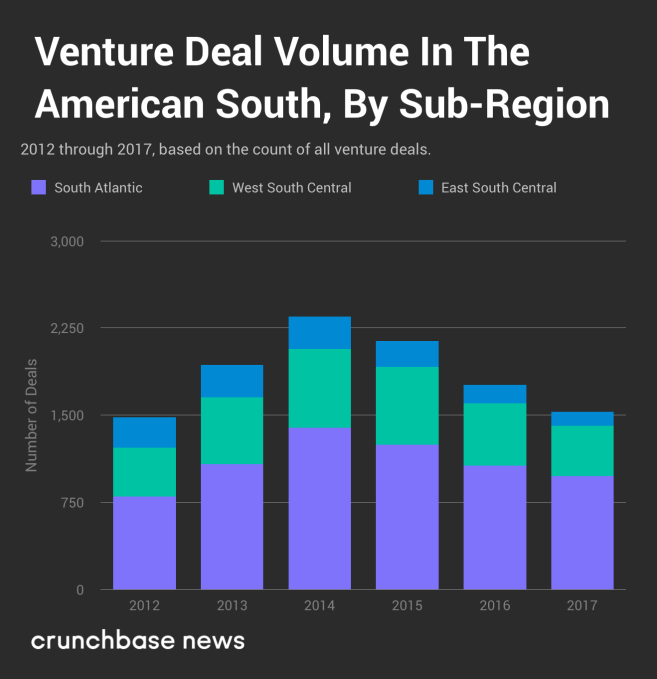

In the chart below, you’ll see venture deal volume broken out by sub-region.

Over the past several years, reported venture deal volume has been on the downswing. From a local maximum in 2014 through the end of 2017, it’s down almost 35 percent overall. But that’s not the whole picture. The relative share of deal volume has changed, as well.

Although it’s not immediately clear just by looking at the chart above, startups in the South Atlantic sub-region have accounted for an increasingly large share of the funding rounds. For example, in 2012, South Atlantic startups attracted 54 percent of the deal volume. In 2017, that grows to 64 percent. Startups in the West South Central sub-region have pretty consistently pulled in between 28 and 30 percent of the deals, so where’s the loss coming from? Startups headquartered in Kentucky, Tennessee, Mississippi and Alabama pulled in just 8 percent of deals in 2017, compared to 18 percent in 2012.

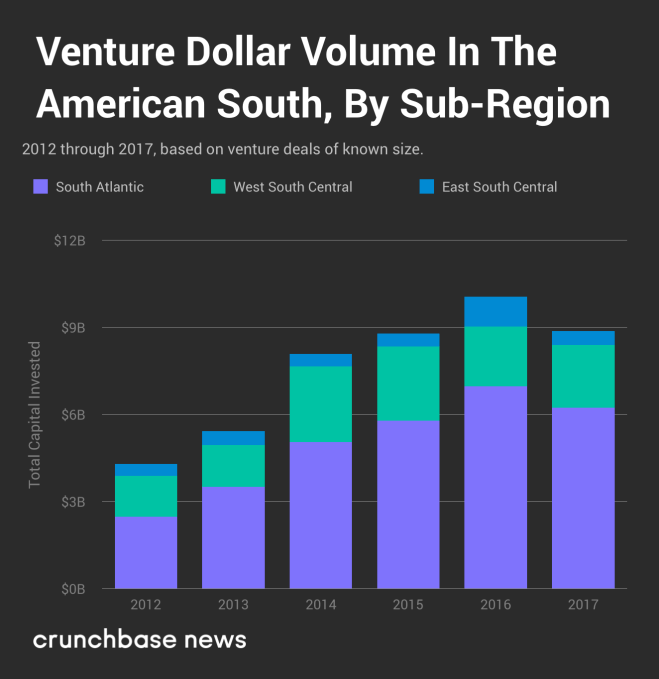

It’s a similar story with dollar volume.

In general, dollar volume follows the same pattern, albeit with a bit more variability. Regardless, startups in the South Atlantic sub-region are hoovering up an ever-larger share of venture dollars, and there’s little to indicate that trend will reverse itself any time soon.

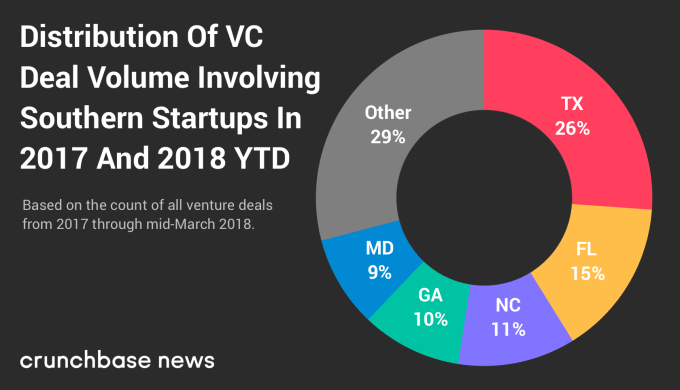

Let’s see which states accounted for most of the deal volume. The chart below shows the geographic distribution of deal-making activity by startups in each Southern state from the beginning of 2017 through time of writing. It should come as no surprise that much of the activity is concentrated in states with higher populations.

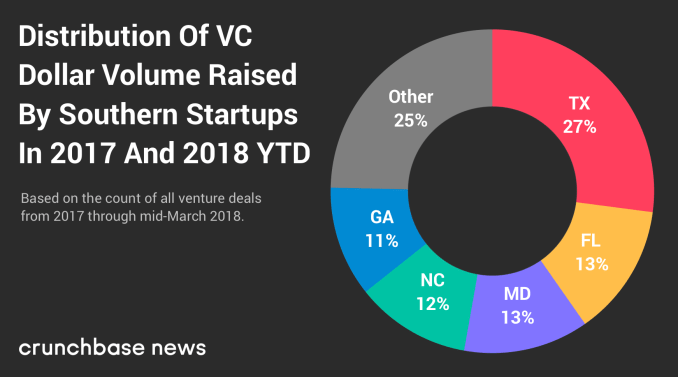

And here’s the distribution of dollar volume among southern states.

Despite some variation in which states are at the top of the ranks, the share of deal and dollar volume raised by startups in the top three states is remarkably similar, coming in at between 52 and 53 percent for both metrics.

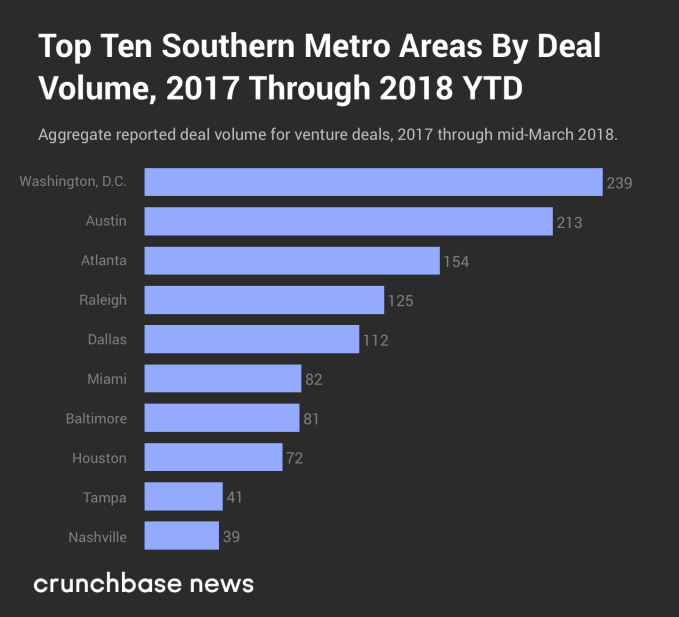

We started by looking at the South as a whole and then drilled into its sub regions and states. But there’s one layer deeper we can go here, and that’s to rank the top startup cities in the South.

In the interest of keeping our rankings fresh and timely, we’re covering activity from the past 15 months or so, from the start of 2017 through mid-March 2018. But before highlighting some of the more notable hubs, let’s take a look at the numbers.

In the chart below, you’ll find the top 10 metropolitan areas where Southern startups closed the most funding rounds.

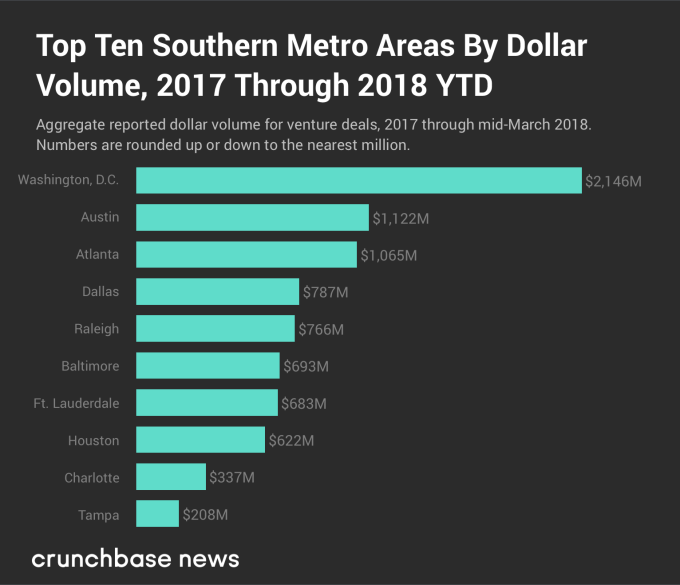

The chart below shows reported dollar volume over the same period of time.

Much like we saw at the state level, the top five startup cities — ranked by both deal and dollar volume — are the same, although there’s some variation between where each one ranks. In order, the D.C., Austin and Atlanta metro areas rank in the top three for each metric, while Dallas and Raleigh, NC switch off between fourth and fifth place.

To be frank, Washington, D.C.’s top-shelf ranking was a bit of a surprise. It may be the fact that Austin, TX plays host to South By Southwest, a somewhat more relaxed culture and/or a preponderance of excellent breakfast taco and barbecue joints, but to many — ourselves included — the city feels like it would have a more active startup scene than the nation’s capital. But that’s not exactly the case. The D.C. metro area had more venture deal and dollar volume than Austin for seven out of the last 10 years, and startups based in the nation’s capital have raised more than twice as much money so far in 2018.

D.C.-area startups have recently raised some notable rounds. Just a couple of weeks prior to the time of writing, Viela Bio raised $250 million in a Series A round (in late February 2018) to continue funding research and testing of its treatments for severe inflammation and autoimmune diseases. And on the later-stage end of things, education technology company Everfi raised $190 million in a Series D round that had participation from Amazon founder and CEO Jeff Bezos, former Alphabet executive Eric Schmidt and Medium CEO Ev Williams. Other D.C. companies, including Mapbox, Upside.com, Afiniti and ThreatQuotient, have all raised late-stage rounds within the past 15 months.

Startup ecosystems in Southern cities may pale in comparison to places like New York and San Francisco, but it wouldn’t be wise to discount the region entirely. A large number of interesting companies call the lower half of the Lower 48 home, and as the cost of living continues to rise on the east and west coasts, don’t be surprised if many current and would-be founders opt to stay down home in the South.

Powered by WPeMatico

What if I told you that you could visit three continents in one day without leaving your office and truly feel like you were there in person? That you could move down a hallway or across a stage, make eye contact and feel, well, more like a human being than just a face on a screen? Read More

What if I told you that you could visit three continents in one day without leaving your office and truly feel like you were there in person? That you could move down a hallway or across a stage, make eye contact and feel, well, more like a human being than just a face on a screen? Read More

Powered by WPeMatico