edtech

Auto Added by WPeMatico

Auto Added by WPeMatico

If you’re trying to develop fluency in a non-native tongue, language immersion is a crucial part of the learning process. Surrounding yourself with native speakers helps with pronunciation, context building, and most of all, confidence.

But what if you’re an eight-year-old kid in Spain learning English and can’t swing a solo trip to the United States for the summer?

Novakid, founded by Maxim Azarov, wants to be your next best option. The San Francisco-based edtech startup offers virtual-only, English language immersion for kids between the ages of four through 12, by combining a mix of different services from live tutors to gamification.

After closing its $4.25 million Series A round last December, Novakid announced today that it is back with a $35 million Series B financing, led by Owl Ventures and Goodwater Capital. Existing investors also participated in the round, including PortfoLion, LearnStart, TMT Investments, Xploration Capital, LETA Capital and BonAngels.

The startup is raising capital in response to an active start to its year. The company’s active client base grew 350% year over year, currently at over 50,000 paying students. The money will be used to get more students into its universe of tools, as well as help Novakid expand into international markets with high populations of speakers who want to learn English.

The company’s suite of services are built around two principles: First, that it can immerse early-age learners into the world of English at scale, and second, that it can actually be fun to use.

When a user signs up, they are first connected to one of Novakid’s 2,000 live tutors for their first class. Tutors must be native English speakers with a B.A. degree or higher, as well as an international teaching certificate such as DELTA, CELTA, TESOL or TEFL.

“One of the things that is really important, even psychologically, is to start listening to the language, start interacting with a live person, and remove being afraid of not understanding something,” Azarov said. The company wants to recreate the conditions of how a kid likely learned their first language.

In the class, the tutors only speak English, and users are encouraged to do the same to slowly build and mistake their way into confidence. While the live, video-based classes are a key part of Novakid’s product, Azarov said it was important that his company “was not just giving you access to a teacher” as its main value proposition.

“Most of the competitors are taking teachers and making them available remotely so you don’t have to travel and you have a bigger selection,” he said. But if you look at the industry in the bigger picture, guys like Oxford, Cambridge, Pearson who provide content for the language learning industry, their product basically sucks. It’s really bad.” So, Novakid puts most of its energy into rebuilding a curriculum that works with better design, and includes games.

Gamified content lives both in and out of classes. Within the classroom, a teacher may take a student on a VR-enhanced tour through famous landmarks and museums to practice vocabulary. Self-paced content could look like a multiplayer “battle” between two students answering questions within a certain time period to get a better score. Novakid has an entire team dedicated to game design and development.

Students are clicking in. Novakid users spend two-thirds of their time on the website with tutors, and one-third with self-paced content that the company built in-house. The company wants to switch those concentrations because more students are spending time with the asynchronous content around grammar and vocabulary, and teachers are reserved for more complex information like speaking and conversation.

Part of the difficulty of scaling up a language learning business is that users need to stay motivated. Gamification helps with engagement, but Novakid’s clientele of children could also be fast to churn compared to adult learners, simply due to priorities. Azarov said that he sees how some would view selling exclusively to children as a disadvantage, but he views their focus as differentiation.

“You get better brand equity when you’re more focused,” he said. “The way kids learn language is vastly different from the way adults learn language, and I don’t think the general players who do ‘everything from everybody’ will be able to do [the former] as well as we are.” Duolingo recently launched Duolingo ABC, a free English literacy app with hundreds of short-form exercises. While the now-public company has strong branding, Novakid’s strategy differs by adding in more services around live learning and speaking.

So far, the company has proven that its strategy is sticking. Its revenue in 2020 was $9 million, and in 2021 it is expected to hit between $36 million to $45 million in revenue. It declined to disclose the specifics around diversity of the team, but plans to kick off a quite intensive recruiting spree going forward. Azarov plans to add 200 people to his 300-person company in the next six months.

Powered by WPeMatico

Duolingo landed onto the public markets this week, rallying excitement and attention for the edtech sector and its founder cohort. The language learning business’ stock price soared when it began to trade, even after the unicorn raised its IPO price range, and priced above the raised interval.

Duolingo’s IPO proves that public market investors can see the long-term value in a mission-driven, technology-powered education concern; the company’s IPO carries extra weight considering the historically few edtech companies that have listed.

Duolingo’s IPO proves that public market investors can see the long-term value in a mission-driven, technology-powered education concern; the company’s IPO carries extra weight considering the historically few edtech companies that have listed.

For those that want the entire story of Duolingo, from origin to messy monetization to historical IPO, check out our EC-1. It has dozens of interviews from executives, investors, linguists and competitors.

For today, though, we have fresh additions. We sat down with Duolingo CEO Luis von Ahn earlier in the week to discuss not only his company’s IPO, but also what impact the listing may have on startups. Duolingo’s IPO can be looked at as a case study into consumer startups, mission-driven companies that monetize a small base of users, or education companies that recently hit scale. Paraphrasing from von Ahn, Duolingo doesn’t see itself as just an edtech company with fresh branding. Instead, it believes its growth comes from being an engineering-first startup.

Selling motivation, it seems, versus selling the fluency in a language is a proposition that international consumers are willing to pay for, and an idea that investors think can continue to scale to software-like margins.

Duolingo has gone through three distinct phases: Growth, in which it prioritized getting as many users as it could to its app; monetization, in which it introduced a subscription tier for survival; and now, education, in which it is focusing on tacking on more sophisticated, smarter technology to its service.

Powered by WPeMatico

U.S. edtech company Duolingo released a revised IPO price range this morning, boosting its potential per-share value to $100 after initially targeting a range that topped out at $95 per share.

Per the unicorn’s SEC filings, Duolingo is now targeting a $95 to $100 per share IPO price range, up from $85 to $95 per share, or a gain of around 12% at the bottom and 5% at the top.

TechCrunch previously called the Duolingo debut a bellwether of sorts for the larger U.S. edtech ecosystem; if Duolingo can price and trade well, investors in private companies may be more willing to invest, given a more proven and attractive exit market. On the other hand, if Duolingo prices weakly or trades poorly, the company could place a wet blanket atop the startup edtech world.

The fact that Duolingo is raising its IPO price range indicates that we are more likely on the path for a strong offering than a weak one.

For edtech companies that have hit unicorn status — like Masterclass, Course Hero, Quizlet and Outschool — it’s good news. For reference, those companies have raised $461.4 million, $97.4 million, $62 million and $130 million, respectively, per Crunchbase data.

The terms of the company’s IPO have not changed, aside from its proposed price. So, Duolingo is still selling 3.7 million shares in its debut, and some 1.41 million shares will be sold by existing equity holders. The company’s underwriters also reserved their right to buy 765,916 shares of the company’s stock at IPO price in the 30 days following its debut.

At the upper and lower bands of the company’s IPO price, its simple valuation excluding underwriter shares now lands between $3.41 billion and $3.59 billion. Inclusive of its greenshoe offering, those numbers rise to $3.48 billion and $3.67 billion.

Recall that when private, Duolingo’s November 2020 Series H valued the company at just over $2.4 billion. So long as Duolingo prices in its range, it will provide investors with a nice bump in the value of their investment. Duolingo was valued at just $1.6 billion in mid-2020, indicating that it has more than doubled in value since that investment.

Powered by WPeMatico

The Exchange spent a little time on Friday ruminating on the impact of then-rumored regulation in China targeting its edtech sector. News that the Chinese government intended to crack down further on the education technology market hit shares of public, China-based edtech companies. It was a mess.

Then over the weekend, the rumors became reality, and the impact is still being felt today in the global markets.

But there’s more. China is also bringing new regulatory pressure on food-delivery companies and Tencent Music. More precisely, we’ve seen successive market-dynamic-changing moves from the Chinese government in the last few days, coming as 2021 had already proved to be a turbulent environment for China-based technology companies.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Today we have to do a little bit of work to understand precisely what is going on with the various regulatory changes. Why? Because the Chinese venture capital market is a key player in the global venture scene. And Chinese startups have gone public on both Chinese, Hong Kong and U.S. exchanges; there’s a lot of capital tied up in companies impacted today — and possibly tomorrow.

For startups, the regulatory changes aren’t a death blow; indeed, many Chinese tech startups won’t be affected by what we’ve seen thus far. And upstart tech companies in sectors less likely to be targeted by central authorities may become more attractive to investors than they were before the regulatory onslaught kicked off. But on the whole, it feels like the risk profile of doing business in China has risen. That could curb the pace at which capital is invested, cut valuations and lower interest in the Chinese startup market from private-market investors able to invest globally.

Let’s parse what’s changed, examine market reactions and then consider what could be next. We want to better understand today’s Chinese startup market and what its new form could mean for existing players and future performance.

Let’s parse what’s changed, examine market reactions and then consider what could be next. We want to better understand today’s Chinese startup market and what its new form could mean for existing players and future performance.

The edtech clampdown did not start last week. China’s edtech sector started to rack up penalties and fines in June, which led to what the Asia Times called “warning bells” in the sector. From there, things went from penalties to punishing regulatory changes.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and me here.

Ever wake up to just a massive wall of news? That was us this morning, so we had to pick and choose. But since this show is about getting you caught up, we decided to focus on the largest, broadest new information that we could:

All that, and we had a good time! Hugs and love from the Equity crew — chat Wednesday!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

News that China’s government may force domestic tutoring-focused companies to go nonprofit is taking a huge bite out of the value of several technology companies. Bloomberg notes that the value of companies like New Oriental Education & Technology Group and TAL Education are tumbling in light of the news, which would constitute merely the latest salvo against tech companies in the autocratic country.

New Oriental’s Hong Kong-listed shares fell 44.22% in after-hours trading after the nonprofit news broke, while NYSE-shares of TAL are off an even sharper 51.75% in pre-market trading. With Yahoo Finance listing a roughly $13.8 billion market cap for TAL ahead of its impending declines at the market open, billions of equity value are about to get deleted. The list goes on: China Online Education Group is off 39.97% in after-hours trading, for example.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

A new decision by China’s government to exert more control over a sector of its domestic economy should not surprise. And we shouldn’t be shocked that online tutoring is in the country’s targets; today’s news is a follow-up to prior regulatory action in the sector from earlier in the year.

As China has become synonymous with edtech startups in recent years, the news impacts more than just public companies. The expected rules change may also hit a host of private, venture-backed companies.

As China has become synonymous with edtech startups in recent years, the news impacts more than just public companies. The expected rules change may also hit a host of private, venture-backed companies.

For example, what will happen to Yuanfudao? The company was valued at $15.5 billion last year, offering what TechCrunch described as “live tutoring, an online Q&A arm and a math-problem-checking arm.” Will the company see its wings clipped?

Or how about Zuoyebang, which raised $1.6 billion in a single round last year? TechCrunch wrote that Zuoyebang offers “online courses, live lessons and homework help for kindergarten to 12th grade students.” Is it in trouble as well?

All this comes on the same day that shares in Zomato began to float, with the Indian online food delivery company seeing its shares close up nearly 65% in their first day’s trading. TechCrunch has viewed the Zomato IPO as a possible bellwether for the larger Indian startup market, and the results augur well for other growth-focused, loss-making unicorns in the country.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

We were a smaller team this week, with Natasha and Alex together with Chris to sort through yet another summer frenzy of a week.

This time around we actually recorded live on Twitter Spaces, which was a first for the podcast. If you missed it, it’s probably because we didn’t promote the taping since it was just an experiment. Good news, though, is that it went well, and we’re going to do some more live tapings of the show with the entire crew on the mics. Make sure to follow the show on the Big Tweet to ensure that you can come hang with us next week. We’ll also do some Q&A at the end, if we’re in good moods.

Until then, let’s live in the present. Here’s what we got into in today’s show:

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Danny, Natasha, and Alex were on deck this week, with Grace on the recording and edit. But, if you want to hear more about Robinhood, this is not the episode for you. If you want to learn more about the consumer fintech company’s IPO filing this is the episode you want. Basically, Robinhood filed after we had wrapped taping, so we had to do a special pod for the news.

So, this is the everything-but-Robinhood episode. And here’s what’s inside of it:

A four-episode week! With only Grace handling production! She’s amazing.

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday morning at 7:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Last week was a good one for edtech in Europe.

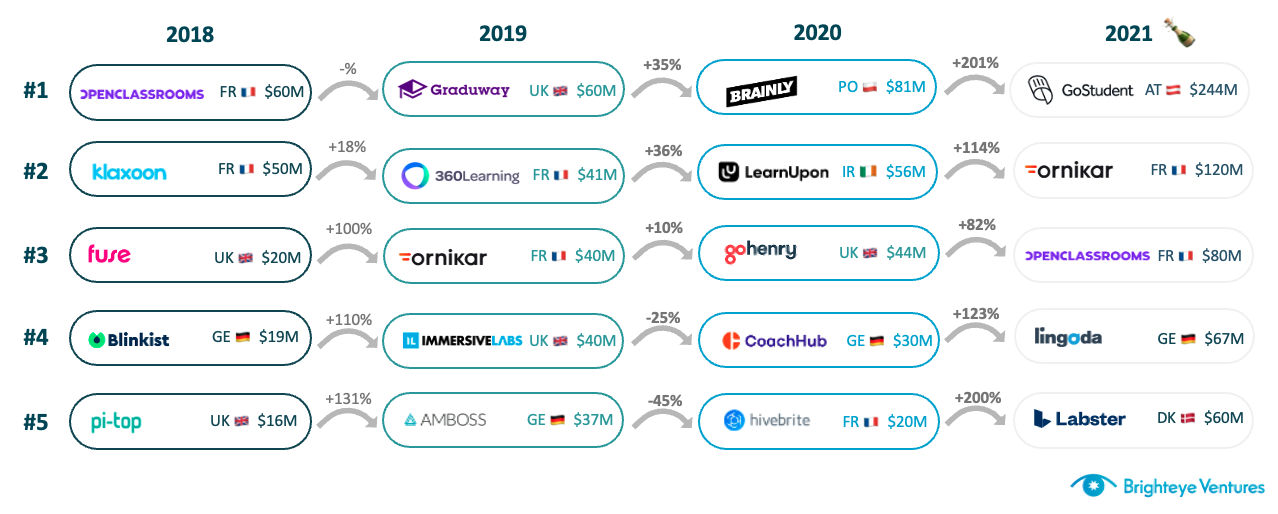

GoStudent became Europe’s first edtech unicorn (IPO’d companies aside), raising its third round in 12 months and the biggest ever in the sector in Europe. Brighteye Ventures’ analysis showed that VC investments in European edtech had breached $1 billion in a calendar year for the first time, even without GoStudent’s mega-round, with six months left to go.

Edtech deal flow in 2021 looks set to match or even outpace 2020 levels, per the report: At $9.4 million, average deal size is triple 2020 levels; seven companies have raised $50 million in five different markets; and the U.K. has more than three times as many deals as the next individual market.

Deal-size progression in edtech over the years. Image Credits: Brighteye Ventures

It’s interesting that we are not seeing enormous increases in deal count. The $1.05-billion mark in the report is spread across 111 transactions — there were 237 in 2020, so we could expect a similar total this year. More funding and stable deal count of course means that we are seeing significant increases in deal size.

It seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

We can draw a few conclusions from this. We can construe that companies created last year and in previous years matured significantly during the pandemic due to increased demand. Moreover, this rapid natural selection process provided insights on verticals and possible winners.

Lastly, it seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

This is contributing to larger early rounds than we have seen in previous years — investors can’t pick the winner, but they can slant the playing field instead. We therefore expect to see a surge in the number of pre-seed, seed and Series A rounds in the second half of 2021, as companies founded during the pandemic begin to raise meaningful funding.

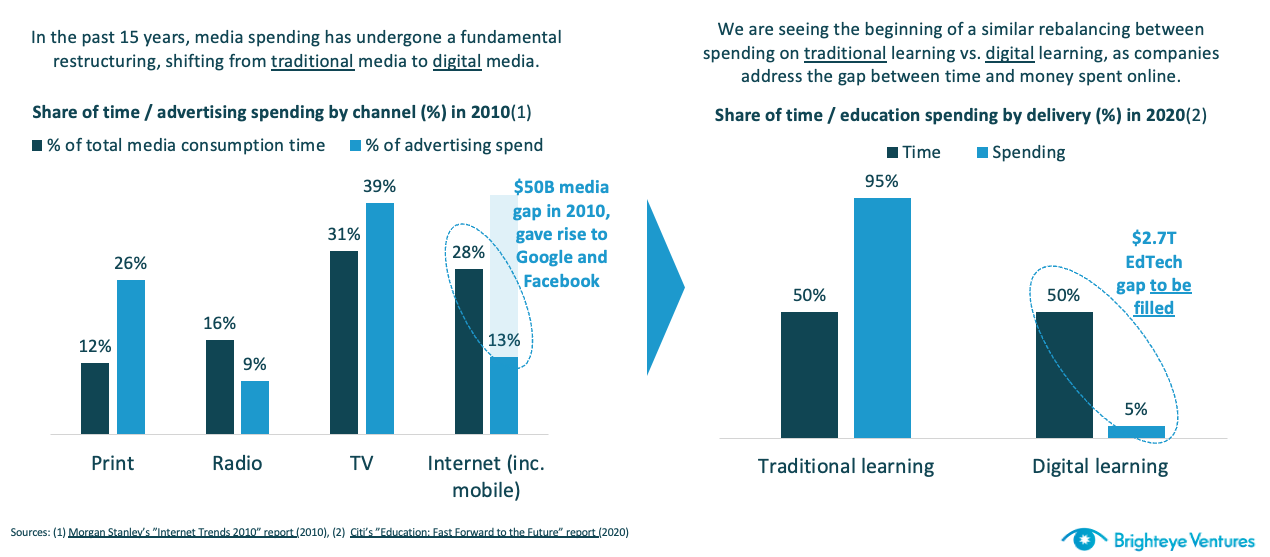

Another reason that edtech is being taken seriously by generalist investors is that the true size of the market (and the extent of digitization to come) is becoming more conceivable.

Edtech spending is growing like media spending did in the 2010s. Image Credits: Brighteye Ventures

Powered by WPeMatico

Duolingo filed to go public yesterday, giving the world a deep look inside its business results and how the pandemic impacted the edtech unicorn’s performance. TechCrunch’s initial read of the company’s filing was generally positive, noting that its growth was impressive and its losses modest; Duolingo recently began making money on an adjusted basis.

While the company’s top-level numbers are impressive, we want to go one level deeper to grow our understanding of the company beyond our EC-1.

Duolingo is likely entering a period in which it will have to invest heavily in features like pronunciation, efficacy and new apps — which could come at a steep upfront cost.

First, we’ll explore the growth of Duolingo’s total user base, how much money it makes per active user, and how effectively the company has managed to convert free users to paid products over time. The numbers will set us up to understand what else can be learned about Duolingo’s business beyond our original deep dive into the company’s finances — specifically underscoring the pressure cooker it finds itself in when looking for new revenue sources.

Starting with Duolingo’s growth in total active users, guess how fast they rose from 2019 to 2020. Hold that number in your head.

The actual numbers are as follows: In 2019, Duolingo closed the year with 27.3 million monthly active users (MAUs); it wrapped 2020 with 36.7 million MAUs. That’s a gain of 34%. If we narrow our gaze to Q1 2021 numbers compared to Q1 2020, we can see that Duolingo’s MAUs rose from 33.5 million to 39.9 million, or growth of around 19%.

The bulk of Duolingo’s growth, then, came in early 2020 when we consider its pandemic bump. Put more simply, the company scaled from 27.3 million MAUs at the end of 2019 to 33.5 million MAUs at the end of Q1 2020; from then, the company added 3.2 million more MAUs throughout 2020 and 6.4 million during the next four quarters.

Another lens through which to view the numbers is simply a recognition that first-quarter results at Duolingo appear to be stronger than results in the rest of the year, perhaps due to New Year’s resolutions to learn a new language or brush up on a second language learned in high school.

Next, let’s examine Duolingo’s monetization efforts regarding converting free users to paying users.

Here we can see a very different growth story. While the company’s MAUs rose 34% from 2019 to 2020, the company’s paying users rose from 900,000 at the end of 2019 to 1.6 million at the end of 2020. That is a far sharper gain of 84% on a year-over-year basis.

So, while Duolingo did see material user growth during 2020, it saw turbocharged expansion in the users it was able to shake revenue from. Improved monetization, more than acceleration in user growth, was the pandemic’s effect on Duolingo.

What can we see in the company’s more recent results? From Q1 2020 to Q1 2021, Duolingo’s paid subscribers rose from 1.1 million to 1.8 million, a gain of around 64%. That was a slower pace than the company managed more generally in 2020, which matches Duolingo’s slower revenue growth in Q1 2021 than it recorded in 2020.

The number is still strong, we think. But not as impressive as the more than 100% revenue expansion that the company put on the board last year.

In percentage terms, 3.3% of Duolingo’s MAUs were paid subscribers in 2019. That figure rose to 4.4% in 2020. And in Q1 2021, it reached 4.5%. Duolingo rounds that number to 5% in its S-1, which feels somewhat aggressive to us, given the somewhat modest pace at which the metric is improving. Here’s the wording:

As of March 31, 2021, approximately 5% of our monthly active users were paid subscribers of Duolingo Plus. Our paid subscriber penetration has increased steadily since we launched Duolingo Plus in 2017 and, combined with our user growth, has led to our revenue more than doubling every year since.

A gain of 0.1 percentage point in a quarter is growth, we suppose.

Next, let’s chat about revenue per MAU. To get consistent numbers, we’ll divide quarterly revenues by MAU figures from the same period. So, we’ll compare Q4 2019 revenue at Duolingo with its year-end MAU figure. We’ll do the same for 2020, and for Q1 2021 we’ll use both numbers from that period.

Powered by WPeMatico