economy

Auto Added by WPeMatico

Auto Added by WPeMatico

Lana, a new startup based in Madrid, is looking to be the next big thing in Latin American fintech.

Founded by serial entrepreneur Pablo Muniz, whose last business was backed by one of Spain’s largest financial services institutions, BBVA, Lana is looking to be the all-in-one financial services provider for Latin America’s gig economy workers.

Muniz’s last company, Denizen, was designed to provide expats in foreign and domestic markets with the financial services they would need as they began their new lives in a different country. While the target customer for Lana may not be the same middle to upper-middle-class international traveler that he had previously hoped to serve, the challenges gig economy workers face in Latin America are much the same.

Muniz actually had two revelations from his work at Denizen. The first — he would never try to launch a fintech company in conjunction with a big bank. And the second was that fintechs or neobanks that focus on a very niche segment will be successful — so long as they can find the right niche.

The biggest niche that Muniz saw that was underserved was actually in the gig economy space in Latin America. “I knew several people who worked at gig economy companies and I knew that their businesses were booming and the industry was growing,” he said. “[But] I was concerned about the inequalities.”

Workers in gig economy marketplaces in Latin America often don’t have bank accounts and are paid through the apps on which they list their services in siloed wallets that are exclusive to that particular app. What Lana is hoping to do is become the wallet of wallets for all of the different companies on which laborers list their services. Frequently, drivers will work for Uber or Cabify and deliver food for Rappi. Those workers have wallets for each service.

(Photo by Cris Faga/Pacific Press/LightRocket via Getty Images)

Lana wants to unify all of those disparate wallets into a single account that would operate like a payment account. These accounts can be opened at local merchant shops and, once opened, workers will have access to a debit card that they can use at other locations.

The Lana service also has a bill pay feature that it’s rolling out to users, in the first evolution of the product into a marketplace for financial services that would appeal to gig workers, Muniz said.

“We want to become that account in which they receive funds,” he said. “We are still iterating the value proposition to gig economy companies.”

Working with companies like Cabify, and other, undisclosed companies, Lana has plans to roll out in Mexico, Chile, Peru and, eventually, Colombia and Argentina.

Eventually, Lana hopes to move beyond basic banking services like deposits and payments and into credit services. Already hundreds of customers are using the company’s service through the distribution partnership with Cabify, which ran the initial pilot to determine the viability of the company’s offering.

“The idea of creating Lana was initially tested as an internal project at Cabify,” Muniz wrote in an email. “Soon Cabify and some potential investors saw that Lana could have a greater impact as an independent company, being able to serve gig economy workers from any industry and decided to start over a new entrepreneurial project.”

Through those connections with Cabify, Lana was able to bring in other investors like the Silicon Valley-based investment firm Base 10.

“One of the things we’ve been interested in is in inclusion generally and in fintech specifically,” said Adeyemi Ajao, the firm’s co-founder. “We had gotten very close to investing in a couple of fintech companies in Latin America and that is because the opportunity is huge. There are several million people going from unbanked to banked in the region.”

Along with a few other investors, Base 10 put in $12.5 million to finance Lana as it looks to expand. It’s a market that has few real competitors. Nubank, Latin America’s biggest fintech company, is offering credit services across the continent, but most of their end users already have an established financial history.

“Most of their end users are not unbanked,” said Ajao. “With Lana it is truly gig workers… They can start by being a wallet of wallets and then give customers products that help them finance their cars or their scooters.”

The ultimate idea is to get workers paid faster and provide a window into their financial history that can give them more opportunities at other gig economy companies, said Ajao. “The vision would be that someone can plug in their financial information for services. If they’re working for Rappi and have never been an Uber driver and they want to be an Uber driver, Lana can use their financial history with Rappi to offer a loan on a car,” he said.

That financial history is completely inaccessible to a traditional bank, and those established financial services don’t care about the history built in wallets that they can’t control or track. “Today if you’ve been a gig worker and you go to a bank, that’s worth nothing,” said Ajao.

Powered by WPeMatico

Merico, a startup that gives companies deeper insights into their developers’ productivity and code quality, today announced that it has raised a $4.1 million seed round led by GGV Capital, with participation from Legend Star and previous investor Polychain Capital. The company was originally funded by the open source-centric firm OSS Capital.

Merico head of business development Maxim Wheatley tells me that the company plans to use the new funding to enhance and expand its existing technology and marketing efforts. As a remote-first startup, Merico already has team members in the U.S., Brazil, France, Canada, India and China.

“In keeping with our roots and mission in open source, we will be focusing some of these new resources to engage more collaboratively with open-source foundations, contributors and maintainers,” he added.

The idea behind Merico was born out of two key observations, Wheatley said. First of all, the team wanted to create a better way to analyze developer productivity and the quality of the code they generate. Some companies still simply use the number of lines of code generated by a developer to allocate bonuses for their teams, for example, which isn’t a great metric by any means. In addition, the team also wanted to find ways to better allocate income and recognition to the community members of open-source projects based on the quality of their contributions.

The company’s tool is systems agnostic because it bases its analysis on the codebase and workflow tools instead of looking at lines of codes or commit counts, for example.

“Merico evaluates the actual code, in addition to related processes, and places productivity in the context of quality and impact,” said Merico CTO Hezheng Yin . “In this process, we evaluate impact leveraging dependency relationships and examine fundamental indicators of quality including bug density, redundancy, modularity, test-coverage, documentation-coverage, code-smell and more. By compiling these signals into a single point of truth, Merico can determine the quality and the productivity of a developer or a team in a manner that more accurately reflects the nature of the work.”

As of now, Merico supports code written in Java, JavaScript (Vue.js and React.js), TypeScript, Go, C, C++, Ruby and Python, with support for other languages coming later.

“Merico’s technology delivers the most advanced code analytics that we’ve seen on the market,” said GGV’s Jenny Lee . “With the Merico team, we saw an opportunity to empower the organizations of tomorrow with insight. In this era of remote transformation, there’s never been a more critical time to bring this visibility to the enterprise and to open source; we can’t wait to see how this technology drives innovation in both technology and management.”

Powered by WPeMatico

I’ve been following consumer audio electronics company Nura with great interest for a few years now — the Melbourne-based startup was one of the first companies I met with after starting with TechCrunch. At the time, its first prototype was a big mess of circuits and wires — the sort of thing you could never imagine shrunk down into a reasonably sized consumer device.

Nura managed, of course. And the final product looked and sounded great; hell, even the box was nice. If I’m lucky, I see a consumer hardware product once or twice a year that seems reasonably capable of disrupting an industry, and Nura’s custom sound profiles fit that bill. But the company was unique for another reason. A graduate of the HAX accelerator, the startup announced NuraNow roughly this time last year.

Hardware as a service (HaaS) has been a popular concept in the IT/enterprise space for some time, but it’s still fairly uncommon in the consumer category. For one thing: A hardware subscription presents a new paradigm for thinking about purchases. That is a big lift in a country like the U.S., which spent years weaning consumers off contract-based smartphones.

That Nura jumped at the chance shouldn’t be a big surprise. Backers HAX/SOSV have been proponents of the model for some time now. I’ve visited their Shenzhen offices a few times, and the topic of HaaS always seems to come up.

In a recent email exchange, General Partner Duncan Turner described HaaS as “a great way to keep in contact with your customers and up-sell them on new features. Most importantly, for startups, recurring revenue is critical for scaling a business with venture capital (and will help appeal to a broad set of investors). HaaS often has a low churn (as easier to put onto long-term contracts).”

Powered by WPeMatico

Now that I’ve offered an overview to help you think through where concentrated stock sits in your overall plan, let’s take a closer look at why selling can be challenging for some.

In the following section, I reveal the facts of the concentrated stock “get rich” myths that reside in the minds of many first-time concentrated stock owners, and I show why it is prudent to consider greater diversification.

Keep reading to learn more about the benefits of diversification, discover how much company stock is likely too much to hold, and the options you have when it comes to diversifying strategically.

There are several hard facts to keep in mind in contemplating maintaining a concentrated position:

The odds of any new IPO being among the top 4% is just slightly better than hitting your lucky number on the roulette wheel. But is your investment portfolio success and the odds of achieving your long-term financial goals something you want to spin the wheel on?

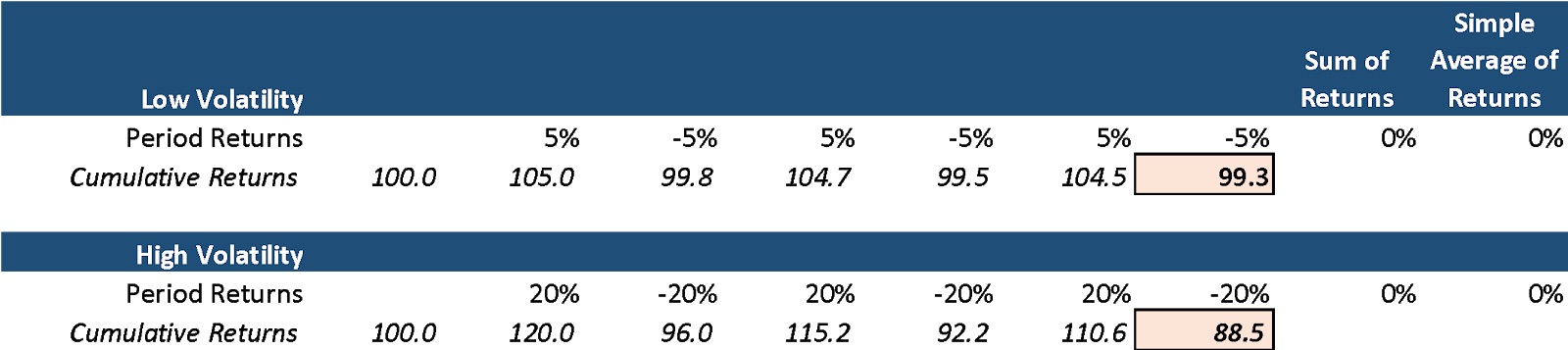

Excess volatility can harm returns. Note the example below that shows the comparison between a low-volatility diversified portfolio versus a high-volatility concentrated portfolio. Despite the same simple average return, the low-volatility portfolio below materially outperforms the high-volatility portfolio.

Image Credits: Peyton Carr

Beyond the math, unexpected spikes in volatility can cause significant price declines. Volatility increases the chances that an investor reacts emotionally and makes a poor investment decision. I’ll cover the behavioral finance aspect of this later. Lowering your portfolio volatility can be as simple as increasing your portfolio diversification.

The Russell 3000, an index representing the 3,000 largest U.S.-based publicly traded companies, has lower volatility when compared against 95%+ of all single stocks. So, how much return do you give up for having lower volatility?

According to Northern Trust Research, the 5.96% annualized average return of the Russell 3000 is 0.73% more than the 5.23% return of the median stock. Additionally, owning the Russell 3000, rather than a single stock, eliminates the likelihood of catastrophic loss scenarios — more than 20% of shares averaged a loss of more than 10% per year over a 20-year time frame.

If this establishes that the avoidance of overly concentrated portfolios is important, how much stock is too much? And at what price should you sell?

We consider any stock position or exposure greater than 10% of a portfolio to be a concentrated position. There is no hard number, but the appropriate level of concentration is dependent on several factors, such as your liquidity needs, overall portfolio value, the appetite for risk and the longer-term financial plan. However, above 10% and the returns and volatility of that single position can begin to dominate the portfolio, exposing you to high degrees of portfolio volatility.

The company “stock” in your portfolio often is only a fraction of your overall financial exposure to your company. Think about your other sources of possible exposure such as restricted stock, RSUs, options, employee stock purchase programs, 401k, other equity compensation plans, as well as your current and future salary stream tied to the company’s success. In most cases, the prudent path to achieving your financial goals involves a well-diversified portfolio.

Facts aside, maintaining a concentrated position in your company stock is far more tempting than taking a more measured approach. Token examples like Zuckerberg and Bezos tend to outshine the dull rationale of reality, and it’s hard to argue against the possibility of becoming fabulously wealthy by betting on yourself. In other words, your emotions can get the best of you.

But your goals — not your emotions — should be driving your investment strategy and decisions regarding your stock. Your investment portfolio and the company stock(s) within it should be used as tools to achieve those goals.

So first, we’ll take a deep dive into the behavioral psychology that influences our decision-making.

Despite all the evidence, sometimes that little voice remains.

“I want to hold the stock.”

Why is it so hard to shake? This is a natural human tendency. I get it. We have a strong impetus to rationalize our biases and not believe we are vulnerable to being influenced by them.

Becoming attached to your company is common, since after all, that stock has made you, or has the potential of making you wealthy. More often than not, selling and diversifying is the tough, but more rational decision.

Numerous studies have furnished insights into the correlation between investing and psychology. Many unrecognized psychological barriers and behavioral biases can influence you to hold concentrated stock even when the data shows that you should not.

Understanding these biases can be helpful when deciding what to do with your stock. These behavioral biases are hard to spot and even harder to overcome. However, awareness is the first step. Here are a few more common behavioral biases, see if any apply to you:

Familiarity bias: Familiarity is likely why so many founders are willing to hold concentrated positions in their own company’s stock. It is easy to confuse the familiarity with your own company with the safety in the stock. In the stock market, familiarity and safety are not always related. A great (safe) company sometimes can have a dangerously overvalued stock price, and terrible companies sometimes have terrifically undervalued stock prices. It’s not just about the quality of the company but the relationship between the quality of a company and its stock price that dictates whether a stock is likely to perform well in the future.

Another way this manifests is when a founder has less experience with stock market investing and has only owned their company stock. They may think the market has more risk than their company when in actuality, it is usually safer than holding just their individual position.

Overconfidence: Every investor is exhibiting overconfidence when they hold an overly concentrated position in an individual stock. Founders are likely to believe in their company; after all, it already achieved enough success to IPO. This confidence can be misplaced in the stock. Founders often are reluctant to sell their stock if it has been going up since they believe it will continue to go up. If the stock has sold off, the opposite is true, and they are convinced it will recover. Often, it is challenging for founders to be objective when they are so close to the company. They commonly believe that they have unique information and know the “true” value of the stock.

Anchoring: Some investors will anchor their beliefs to something they experienced in the past. If the price of the concentrated stock is down, investors may anchor their belief that the stock is worth its recent previous higher value and be unwilling to sell. This previous value of the stock is not an indicator of its real value. The real value is the current price where buyers and sellers exchange the stock while incorporating all presently available information.

Endowment effect: Many investors tend to place a higher value on an asset they currently own than if they did not own it at all. It makes it harder to sell. An excellent way to check for the endowment effect is to ask yourself: “If I did not own these shares, would I purchase them today at this price?” If you are not willing to purchase the shares at this price today, it likely means you are only holding onto the shares because of the endowment effect.

A fun spin on this is to look into the IKEA effect study, which demonstrates that people assign more value to something that they made than it is potentially worth.

When framed this way, investors can make more intentional decisions on whether to continue holding concentrated stock or selling. At times, these biases are hard to spot, which is why having a second person, a co-pilot, or an advisor, is helpful.

Congratulations to those of you with a concentrated stock position in your company; it is hard-earned and likely represents a material wealth. Understand, there is no “right” answer when it comes to managing concentrated stock. Each situation is unique, so it is essential to speak with a professional about options specific to your situation.

It starts with having a financial plan, complete with specific investment goals that you want to achieve. Once you have a clear picture of what you want to accomplish, you can look at the facts in a new light and gain a deeper appreciation for the dangers of holding a concentrated position in company stock versus the benefits of diversification, considering all of the implications and opportunities involved in rational decision-making and investment behavior.

Most individuals understand they can simply and directly sell their equity, but there are a variety of other strategies. Some of these opportunities may be far better at minimizing taxes or better at achieving the desired risk or return profile. Some might wonder what the best timing is to sell. I will cover these topics in the final article of the series.

Powered by WPeMatico

Customer engagement company Freshworks today announced that it has acquired Flint, an IT orchestration and cloud management platform based in India. The acquisition will help Freshworks strengthen its Freshservice IT support service by bringing a number of new automation tools to it. Maybe just as importantly, though, it will also bolster Freshworks’ ambitions around cloud management.

Freshworks CPO Prakash Ramamurthy, who joined the company last October, told me that while the company was already looking at expanding its IT services (ITSM) and operations management (ITOM) capabilities before the COVID-19 pandemic hit, having those capabilities has now become even more important, given that a lot of these teams are now working remotely.

“If you take ITSM, we allow for customers to create their own workflow for service catalog items and so on and so forth, but we found that there’s a lot of things which were repetitive tasks,” Ramamurthy said. “For example, I lost my password or new employee onboarding, where you need to auto-provision them in the same set of accounts. Flint had integrated with Freshservice to help automate and orchestrate some of these routine tasks and a lot of customers were using it and there’s a lot of interest in it.”

He noted that while the company was already seeing increased demand for these tools earlier in the year, the pandemic made that need even more obvious. And given that pressing need, Freshworks decided that it would be far easier to acquire an existing company than to build its own solution.

“Even in early January, we felt this was a space where we had to have a time-to-market advantage,” he said. “So acquiring and aggressively integrating it into our product lines seemed to be the most optimal thing to do than take our time to build it — and we are super fortunate that we placed the right bet because of what has happened since then.”

The acquisition helps Freshworks build out some of its existing services, but Ramamurthy also stressed that it will really help the company build out its operations management capabilities to go from alert management to also automatically solving common IT issues. “We feel there’s natural synergy and [Flint’s] orchestration solution and their connectors come in super handy because they have connectors to all the modern SaaS applications and the top five cloud providers and so on.”

But Flint’s technology will also help Freshworks build out its ability to help its users manage workloads across multiple clouds, an area where it is going to compete with a number of startups and incumbents. Since the company decided that it wants to play in this field, an acquisition also made a lot of sense given how long it would take to build out expertise in this area, too.

“Cloud management is a natural progression for our product line,” Ramamurthy noted. “As more and more customers have a multi-cloud strategy, we want to give them a single pane of glass for all the work workloads they’re running. And if they wanted to do cost optimization, if you want to build on top of that, we need the basic plumbing to be able to do discovery, which is kind of foundational for that.”

Freshworks will integrate Flint’s tools into Freshservice and likely offer it as part of its existing tiered pricing structure, with service orchestration likely being the first new capability it will offer.

Powered by WPeMatico

Over the past two decades, the venture capital industry has exploded beyond anyone’s wildest imaginations.

What began as a sleepy industry in Boston and Menlo Park has now expanded to dozens of cities the world over. The National Venture Capital Association estimates that VCs deployed more than $130 billion in 2018 and 2019, and thousands of new investors have joined the ranks in recent years to find the next great startups.

All that activity, though, poses a dilemma for founders: Who actively writes checks? Who is a leader in a specific market or vertical? Who has the conviction to underwrite pathbreaking investments? Who, ultimately, do you want to have by your side for the next decade as your startup grows?

There are lists that rank VCs by their exit returns. There are lists that rank young VCs by their potential. There are lists of VCs who claim investment interest in various sectors. There are lists that try to ferret out deal volume, impact and other quantitative metrics. There are internal lists at accelerators that share collective wisdom between founders.

Who actively writes checks? Who is a leader in a specific market or vertical? Who has the conviction to underwrite pathbreaking investments? Who, ultimately, do you want to have by your side for the next decade as your startup grows?

All those lists and rankings have an important function to serve, but for all the compilations of investors out there, we couldn’t find a single one that publicly answered a simple yet vital question: Who are the VC investors who are leaders in specific verticals who should be a founder’s first stop during a fundraise?

Today’s venture industry is made up of thousands of investors with varying specialties, and far too many passive investors that are willing to participate in rounds but don’t actively participate in deals unless other investors have committed. Many don’t actively push to get deals done or don’t actively lead the charge to build a syndicate of investors.

With all that in mind, we’re excited to launch a new initiative that we hope will help answer those questions and help founders find that first check — The TechCrunch List.

![]()

Over the next few weeks, we’re going to be collecting data around which individual investors are actually willing to write the proverbial “first check” into a startup’s fundraising round and help catalyze deals for founders — whether it be seed, Series A or otherwise (i.e. out of your Series A investors, the first person who was willing to write the check and get the ball rolling with other investors). Once we’ve collected, cleaned and analyzed the data, we’ll publish lists of the most recommended “first check” investors across different verticals, investment stages and geographies, so founders can see which investors are potentially the best fit for their company.

Founders are used to being specialized; after all, they have to live and breathe their startups every single day. So it can be jarring to start talking to generalist investors who know little about a category and ask shallow questions only to render a judgment with irrelevant advice. One of the greatest impetuses for us to put together The TechCrunch List is that like founders, we also struggle to cut through the noise around the interests of individual VCs.

We’d argue that’s close to impossible. There is more spend on technology than ever before in history. Verticals are getting more competitive — market maps that used to have 10 to 50 companies have expanded to hundreds. The only way to compete today is to specialize, and that has never been more true for VCs.

In all, The TechCrunch List will publish the most recommended “first check” writers across 22 different categories, ranging from D2C & e-commerce brands to space, and everything in between. Through some data analysis around total investments in each space, we believe our 22 categories should cover the entirety or majority of the venture activity today.

To make this project a success and create a useful resource for founders, we need your help. We want to hear from company builders and we want to hear from them directly.

To make this project a success and create a useful resource for founders, we need your help. We want to hear from company builders and we want to hear from them directly. We will be collecting endorsements submitted by founders through the form linked here.

Through the form, founders will be asked to submit their name, their startup, the stage of company, the name of the one “first check” investor they want to endorse and a couple of minor logistical items. We are asking founders here for their on-the-record endorsement. We ask that you limit your recommendations to one (1) person per fundraise round.

While many investors may have helped you in your journey, we are specifically interested in the person who most helped you get a round underway and closed. The one who catalyzed your round. The one who guided you through the fundraise process. The one investor you would ultimately recommend to other founders who are trying to find their VC champion.

Our main goal is to help founders, dreamers and company builders find investors who will invest in them today, and with your help, we think we can. The TechCrunch List is not meant to identify every possible investor under the sun who might make an investment within a space, nor just the big household-name VCs whose reputations can sometimes seem more linked to their follower counts on Twitter as opposed to their bold term sheets.

Our hope is that this can be a go-to resource for founders looking to fundraise going forward, and with that in mind, we are very determined to improve the glaring representation gaps in the venture industry. It’s no secret that the world of VC still looks like a country-club membership roster, dominated by white men with strong opinions and loud voices. Looking at the data, it’s clear that there are groups that are particularly underrepresented, with only a small portion of the industry made up of Black, Latinx and female investors, for example.

We want to amplify these voices and we want to hear particularly from founders of color, female founders and other underrepresented groups. We also want to make sure our recommended investor lists are sufficiently representative and highlight underrepresented investors who might not have had equal opportunities in the past.

We want to help builders wade through the BS politics and fundraising annoyances that founders complain to us about on a daily basis, and help them identify qualified leads that are actually active, engaged and specialized and are the best fit to help founders raise money and grow now.

Thank you for your support. We’re excited to build The TechCrunch List with you — and for you.

Powered by WPeMatico

The venture capital industry is less transparent today than at any time in recent memory.

For all the talk about expanding access and improving its sordid record on diversity, in reality, it has never been harder for founders to figure out who can even write a check to their startups in the first place.

When I first returned to TechCrunch after my second stint in venture capital, my first piece was entitled “The loss of first check investors.” While working in the venture capital industry, it was maddening to see — particularly at the pre-seed and seed stages — how few investors were really willing to go out on a limb and invest in founders before another VC had committed a check.

It’s only gotten worse in the past two years since that article, and the complexity comes from a number of different places. As our investigation showed more than a year ago, fewer and fewer venture rounds are being announced through SEC Form D filings.

There are almost no publicly accountable datasets left indicating who is writing checks in the venture industry and which companies are receiving those checks. While stealthiness is valid in the early days of a startup, the excuse wears thin after years.

Powered by WPeMatico

Akron, Ohio, the hometown of LeBron James; the seat of the U.S. tire industry; the 127 largest city in the U.S.; and the home of America’s first toy company, is now the latest site of a global experiment in whether cities can use behavioral economics to help foster good citizenship.

Thanks to the work of the city’s deputy mayor for integrated development, James Hardy, Akron is the first city to roll out services from an Israeli-based company called Colu. A startup backed by just over $20 million in financing from American and Israeli investors, the company has developed an app-based rewards service that cities can roll out to provide perks to users.

In Akron’s case, the initiative rewards points for shopping at local businesses that can be redeemed for discounts at those stores. The initial effort, which includes a platform for businesses to market directly to the app’s users, focuses on businesses owned by women and minorities (a response to the movement for racial justice that has sprung up in the wake of the murder of George Floyd in Minneapolis).

Akron is the first city of what Colu founder Amos Meiri expects to be a nationwide rollout throughout the U.S. The company already has managed to ink another agreement with the city of Chula Vista, Calif.

Colu, which has raised its capital from investors associated with blockchain technologies like Barry Silbert’s Digital Currency Group; the Boston-based venture capital firm, Spark Capital; New York’s Box Group and the Israeli corporate conglomerate, IDB Group, has deep ties to the cryptocurrency world of alternative financial instruments through Meiri.

One of the original architects of the Color coin blockchain experiment, Meiri’s work with Colu is in some ways an extension of that effort to create new kinds of economies powered by alternative financial mechanisms.

Meiri said cities typically pay for Colu out of their marketing budgets as a new way to communicate and attempt to influence civic behavior.

For Akron’s government officials, the company’s services are a way to boost locally owned businesses that have been hit hard by the state’s attempts to contain the COVID-19 outbreak.

“Our locally owned small businesses are facing enormous challenges and we need out-of-the-box ideas that safely connect them to consumers and turn local spending into a source of pride for residents,” said Akron Mayor Dan Horrigan, in a statement. “Our partnership with Colu will enable the city to reward customers for shopping local, improving revenues for our small businesses while helping folks stretch their dollars.”

Earlier work with the municipal government in Tel Aviv promoted sustainable business practice and encouraged businesses to do more to manage their waste and carbon footprint by introducing a “green label.” Businesses that followed the city’s guidelines were given the label and shoppers were encouraged to frequent those merchants.

Colu envisions itself as more than just a marketing and rewards platform for businesses. The company hopes it can draw users into a kind of social networking platform for civic engagement where users can share their own stories about city-life and their interactions with local business owners and the community.

In some ways, it’s a kinder, gentler version of China’s social credit scoring system, which is also designed to influence civic behavior. In this formulation, there’s a rewards system, but no mechanisms to punish citizens for bad behavior.

“Akron has a long history of innovation within our economy — this initiative draws on that legacy,” said Deputy Mayor Hardy, in a statement. “By putting the future of Akron’s locally owned small businesses in the palm of our citizens’ hands, we hope to make it easy for consumers to keep their money local and continue to strengthen our incredible community.”

Powered by WPeMatico

Due to COVID-19, business continuity has been put to the test for many companies in the manufacturing, agriculture, transport, hospitality, energy and retail sectors. Cost reduction is the primary focus of companies in these sectors due to massive losses in revenue caused by this pandemic. The other side of the crisis is, however, significantly different.

Companies in industries such as medical, government and financial services, as well as cloud-native tech startups that are providing essential services, have experienced a considerable increase in their operational demands — leading to rising operational costs. Irrespective of the industry your company belongs to, and whether your company is experiencing reduced or increased operations, cost optimization is a reality for all companies to ensure a sustained existence.

One of the most reliable measures for cost optimization at this stage is to leverage elastic services designed to grow or shrink according to demand, such as cloud and managed services. A modern product with a cloud-native architecture can auto-scale cloud consumption to mitigate lost operational demand. What may not have been obvious to startup leaders is a strategy often employed by incumbent, mature enterprises — achieving cost optimization by leveraging managed services providers (MSPs). MSPs enable organizations to repurpose full-time staff members from impacted operations to more strategic product lines or initiatives.

Powered by WPeMatico

RudderStack, a startup that offers an open-source alternative to customer data management platforms like Segment, today announced that it has raised a $5 million seed round led by S28 Capital. Salil Deshpande of Uncorrelated Ventures and Mesosphere/D2iQ co-founder Florian Leibert (through 468 Capital) also participated in this round.

In addition, the company also today announced that it has acquired Blendo, an integration platform that helps businesses transform and move data from their data sources to databases.

Like its larger competitors, RudderStack helps businesses consolidate all of their customer data, which is now typically generated and managed in multiple places — and then extract value from this more holistic view. The company was founded by Soumyadeb Mitra, who has a Ph.D. in database systems and worked on similar problems previously when he was at 8×8 after his previous startup, MairinaIQ, was acquired by that company.

Mitra argues that RudderStack is different from its competitors thanks to its focus on developers, its privacy and security options and its focus on being a data warehouse first, without creating yet another data silo.

“Our competitors provide tools for analytics, audience segmentation, etc. on top of the data they keep,” he said. “That works well if you are a small startup, but larger enterprises have a ton of other data sources — at 8×8 we had our own internal billing system, for example — and you want to combine this internal data with the event stream data — that you collect via RudderStack or competitors — to create a 360-degree view of the customer and act on that. This becomes very difficult with the SaaS-hosted data model of our competitors — you won’t be sending all your internal data to these cloud vendors.”

Part of its appeal, of course, is the open-source nature of RudderStack, whose GitHub repository now has more than 1,700 stars for the main RudderStack server. Mitra credits getting on the front page of HackerNews for its first sale. On that day, it received over 500 GitHub stars, a few thousand clones and a lot of signups for its hosted app. “One of those signups turned out to be our first paid customer. They were already a competitor’s customer, but it wasn’t scaling up so were looking to build something in-house. That’s when they found us and started working with us,” he said.

Because it is open source, companies can run RudderStack anyway they want, but like most similar open-source companies, RudderStack offers multiple hosting options itself, too, that include cloud hosting, starting at $2,000 per month, with unlimited sources and destination.

Current users include IFTTT, Mattermost, MarineTraffic, Torpedo and Wynn Las Vegas.

As for the Blendo acquisition, it’s worth noting that the company only raised a small amount of money in its seed round. The two companies did not disclose the price of the acquisition.

“With Blendo, I had the opportunity to be part of a great team that executed on the vision of turning any company into a data-driven organization,” said Blendo founder Kostas Pardalis, who has joined RudderStack as head of Growth. “We’ve combined the talented Blendo and RudderStack teams together with the technology that both companies have created, at a time when the customer data market is ripe for the next wave of innovation. I’m excited to help drive RudderStack forward.”

Mitra tells me that RudderStack acquired Blendo instead of building its own version of this technology because “it is not a trivial technology to build — cloud sources are really complicated and have weird schemas and API challenges and it would have taken us a lot of time to figure it out. There are independent large companies doing the ETL piece.”

Powered by WPeMatico