eCommerce

Auto Added by WPeMatico

Auto Added by WPeMatico

Colombian startup Elenas says it’s helping tens of thousands of women make money by selling products online. And today, it announced that it has raised $6 million in Series A funding.

That’s on top of the $2 million seed round that Elenas announced last fall. Founder and CEO Zach Oschin said that demand continues to grow, particularly with high unemployment levels (particularly among women), while consumers remain nervous about in-person shopping during the pandemic.

“We’ve been able to provide opportunities for tens of thousands of women to earn extra income,” Oschin said.

He suggested that Elenas is essentially a reinvention of the direct sales/catalog sales model that 11 million women participate in across the Latin America. The idea is that independent seller/entrepreneurs (often but not always women) can browse a catalog of products in categories like beauty, personal care and electronics, from more than 250 distributors and brands, all available at a discounted wholesale price. They decide what they want to sell, how much they want to mark the price up and then promote the products on social channels like WhatsApp and Facebook.

Besides its digital focus, Oschin said Elenas is better for the resellers because there’s less risk: “We don’t hold inventory for the company, which is very different than traditional direct sales, and our entrepreneurs don’t ever hold inventory.” Nor do those entrepreneurs need to get involved in things like payment collection or delivery, because Elenas and its distributor partners handle all of that.

“For us, the goal is to provide this backend operating system that gives women everything they need to run their store,” he added.

Elenas offers an automated on-boarding process for the sellers, but Oschin said that within the app, “we do a lot of work to train our sellers how to sell.”

Elenas CEO Zach Oschin. Image Credits: Elenas

The company (which participated in our Latin American Startup Battlefield in 2018) says it’s now paid out more than $7 million to its sellers. It doesn’t limit participation by gender, but Oschin estimated that more than 95% of sellers are women, with 80% of them under the age of 30 and about a third of them without any previous direct sales experience.

The new funding comes from Leo Capital, FJ Labs, Alpha4 Ventures and Meesho. Oschin said the company’s investors have a presence across six different continents, reflecting its international vision. Indeed, one of its next steps is expanding across Latin America, starting with Mexico and then Peru.

“Having seen the meteoric growth of social commerce in India and China we are excited to partner with Elenas as they have demonstrated the right product and operating model for the region,” said Leo Capital co-founder Shwetank Verma in a statement. “The Elenas team has built a solution that’s inclusive, impactful and is well positioned for exponential growth.”

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Another day, another venture-backed IPO filing. Today it’s ThredUp, a used-goods marketplace that is approaching the public markets in the wake of Poshmark’s own strong debut.

Both companies have a related market focus, albeit different approaches to selling used goods. Poshmark allows users to sell clothing items through its app. ThredUp, in contrast, acquires goods from users and sells them itself.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But while Poshmark had profits to brag about in its own IPO filing, ThredUp does not and is also growing more slowly, expanding revenues just 13.6% in 2020. Reading its S-1 filing, it’s clear ThredUp did not have the best 2020, thanks in part to COVID-19.

This morning, let’s get into the numbers posted by the company backed by Trinity Ventures, Redpoint, Highland Capital Partners and Goldman Sachs to decide if it’s just merely to catch Poshmark’s wave, or if its business is a fine machine in its own right.

To understand ThredUp’s business, we have to get into the mechanics of how it sells things. The company has two methods: direct sales and consignment. In the former, ThredUp buys goods and sells them. It then “recognize[s] revenue on a gross basis” and generates gross profit after deducting “inventory cost, inbound shipping and inventory write-downs, as well as outbound shipping, outbound labor and packaging costs.”

That is the model that ThredUp is leaving behind. After shifting to “primarily consignment sales” in 2019, the company’s business has skewed sharply in that direction. Consignment works by having consumers send ThredUp their goods, which it holds, and perhaps sells, remitting to the user a portion of the sale price. The method reduces write-downs and boosts gross margins.

Consignment sales at ThredUp “recognize revenue net of seller payouts,” deducting “outbound shipping, outbound labor and packaging costs” to reach gross profit results.

The revenue-mix focus change can be seen in how ThredUp generated gross profit in 2018, 2019 and 2020. In those years, consignment gross profit came to 38%, 67% and 81% of total gross profit. ThredUp’s business today is effectively a large, digital consignment effort.

What impact has that shift had on the company’s financial health? Let’s find out.

ThredUp posted $129.6 million in 2018 revenue, a figure that grew to $163.8 million in 2019 and $186 million in 2020. The company’s growth slowed from 26.4% in 2019 to 13.6% in 2020, a sharp deceleration. But at the same time, the portion of ThredUp revenues that came from consignment sales grew to 74% from 60%. Did that change have a material impact on the company’s gross margins, thus rendering its slow growth more palatable?

Not really. The company’s gross margins came to 68.7% in 2019 and 68.9% in 2020. That’s about as flat as Texas. And notably the number stayed flat despite the company noting that consignment revenues had stronger gross margins in 2019 and 2020 (77% and 75%, respectively) than its other model (57% and 51%, respectively).

Powered by WPeMatico

Tens of millions of people each year purchase a second-hand smartphone in India, the world’s second-largest market. Phone makers and giant online sellers such as Amazon and Flipkart are aware of it, but it’s too much of a hassle for them to inspect, repair and resell used phones. But these firms also know that customers are more likely to buy a smartphone if they are offered the ability to trade-in their existing handsets.

A startup that is helping these firms tackle this challenge said on Thursday it has raised $15 million in a new financing round. New York-based Olympus Capital Asia made the investment through Asia Environmental Partners, a fund dedicated to the environmental sector. The five-year-old startup, which counts Blume Ventures among its early investors, has raised $42 million to date.

Cashify operates an eponymous platform — both online and physical stores and kiosks — for users to sell and buy used smartphones, tablets, smartwatches, laptops, desktops and gaming consoles. But 90% of its business today surrounds the smartphone category, explained Mandeep Manocha, founder and chief executive of Cashify, in an interview with TechCrunch.

“For consumers, our proposition is that we make it easy for you to sell your devices. You come to our site or app, answer questions to objectively evaluate the condition of your device, and we give you an estimate of how much your gadget is worth,” he said. “If you like the price, we pick it up from your doorstep and give you instant cash.”

A few years ago, I wrote about the struggle e-commerce firms face globally in handling returned items. There are many liability challenges — such as having to ensure that the innards in a returned smartphone haven’t been tempered with — as well as overhead costs in reversing an order.

Manocha said that phone makers and e-commerce firms have found better ways to handle returned items in recent years, but they still lose a significant amount of money on them. These challenges have created a big opportunity for startups such as Cashify.

In fact, Cashify says it’s the market leader in its category in India. The startup has partnerships with “nearly every OEM,” including Apple, Samsung, OnePlus, Oppo, Xiaomi, Vivo and HP. “If you walk into an Apple store today, they use our platform.” For consumers in India, if they opted for the trade-in program, Apple.com also uses Cashify’s trading platform, he said.

The startup also works with top e-commerce firms in India — Amazon, Flipkart and Paytm Mall. The firms use Cashify’s trading and exchange software, and also rely on the startup for liquidation of devices. The startup then repairs these gadgets and sells the refurbished units to customers.

“Essentially, whether you come directly to us, or go to popular e-commerce firms or phone OEMs, we are handling the majority of the trading,” he said. Even if a customer trades in the device to OEMs, or e-commerce firms, these companies sell the device to players like Cashify, which serves over 2 million customers in more than 1,500 cities.

The startup plans to deploy part of the fresh capital to expand its presence in the offline market. Manocha said Cashify currently has dozens of offline stores and kiosks at shopping malls across the country and it has already proven immensely effective in brand awareness among customers.

The startup also plans to expand outside of India, hire more talent and invest more in getting the word out about its offerings. Manocha said the team is also working on expanding its expertise to more hardware categories such as cameras.

“The management team at Cashify has an excellent track record in building a strong consumer-facing franchise and building relationships with OEMs, e-commerce companies and electronic product retailers to be present across all touch points for the consumer,” said Pankaj Ghai, managing director of Asia Environmental Partners, in a statement.

Powered by WPeMatico

Through all of the last year’s lockdowns, venue closures and other social distancing measures that governments have enacted and people have followed to slow the spread of COVID-19, shopping — and specifically e-commerce — has remained a consistent and hugely important service. It’s not just something that we had to do; it’s been an important lifeline for many of us at a time when so little else has felt normal. Today, one of the startups that saw a big lift in its service as a result of that trend is announcing a major fundraise to fuel its growth.

Wallapop, a virtual marketplace based out of Barcelona, Spain that lets people resell their used items, or sell items like crafts that they make themselves, has raised €157 million ($191 million at current rates), money that it will use to continue growing the infrastructure that underpins its service, so that it can expand the number of people that use it.

Wallapop has confirmed that the funding is coming at a valuation of €690 million ($840 million) — a significant jump on the $570 million valuations sources close to the company gave us in 2016.

The funding is being led by Korelya Capital, a French VC fund backed by Korea’s Naver, with Accel, Insight Partners, 14W, GP Bullhound and Northzone — all previous backers of Wallapop — also participating.

The company currently has 15 million users — about half of Spain’s internet population, CEO Rob Cassedy pointed out to us in an interview earlier today, and has maintained a decent No. 4 ranking among Spain’s shopping apps, according to figures from App Annie.

The startup has also recently been building out shipping services, called Envios, to help people get the items they are selling to the buyers, which has expanded the range from local sales to those that can be made across the country. About 20% of goods go through Envios now, Cassedy said, and the plan is to continue doubling down on that and related services.

Naver itself is a strong player in e-commerce and apps — it’s the company behind Asian messaging giant Line, among other digital properties — and so this is in part a strategic investment. Wallapop will be leaning on Naver and its technology in its own R&D, and on Naver’s side it will give the company a foothold in the European market at a time when it has been sharpening its strategy in e-commerce.

The funding is an interesting turn for a company that has seen some notable fits and starts. Founded in 2013 in Spain, it quickly shot to the top of the charts in a market that has traditionally been slow to embrace e-commerce over more traditional brick-and-mortar retail.

By 2016, Wallapop was merging with a rival, LetGo, as part of a bigger strategy to crack the U.S. market (with more capital in tow).

But by 2018, that plan was quietly shelved, with Wallapop quietly selling its stake in the LetGo venture for $189 million. (LetGo raised $500 million more on its own around that time, but its fate was not to remain independent: it was eventually acquired by yet another competitor in the virtual classifieds space, OfferUp, in 2020, for an undisclosed sum.)

Wallapop has for the last two years focused mainly on growing in Spain rather than running after business further afield, and rather than growing the range of goods that it might sell on its platform — it doesn’t sell food, nor work with retailers in an Amazon-style marketplace play, nor does it have plans to do anything like move into video or selling other kinds of digital services — it has honed in specifically on trying to improve the experience that it does offer to users.

“I spent 12 years at eBay and saw the transition it made to new goods from used goods,” said Cassedy. “Let’s just say it wasn’t the direction I thought we should take for Wallapop. We are laser-focused on unique goods, with the vast majority of that secondhand with some artisan products. It is very different from big box.”

Wallapop’s growth in the past year is the result of some specific trends in the market that were in part fuelled by the COVID-19 pandemic.

People spending more time in their homes have been focused on clearing out space and getting rid of things. Others are keen to buy new items now that they are spending more time at home, but want to spend less on them. In both cases, there has been a push for more sustainability, with people putting less waste into the world by recycling and upcycling goods instead.

At the same time, Facebook hasn’t really made big inroads in the country with its Marketplace, and Amazon has also not appeared as a threat to Wallapop, Cassedy noted.

All of these have had a huge impact on Wallapop’s business, but it wasn’t always this way. Cassedy said that the first lockdown in Spain saw business plummet, as people were restricted to leave their homes.

“It was a roller coaster for us,” he said. “We entered the year with incredible momentum, very strong.”

He noted that the drop started in March, when “not only did it become not okay to leave the house and trade locally but the post office stopped delivering parcels. Our business went off a cliff in March and April.”

Then when the restrictions were lifted in May, things started to bounce back more than ever before, nearly overnight, he said. “The economic uncertainty caused people to seek out more value, better deals, spending less money, and yes they were clearing out closets. We saw numbers bounce back 40-50% growth year-on-year in June.”

The big question was whether that growth was a blip or there to say. He said it has continued into 2021 so far. “It’s a validation of what we see as long-term trends driving the business.”

“The global demand for C2C and resale platforms is growing with renewed commitment in sustainable consumption, especially by younger millennials and Gen Z,” noted Seong-sook Han, CEO of Naver Corp., in a statement. “We agree with Wallapop’s philosophy of conscious consumption and are enthused to support their growth with our technology and develop international synergies.”

“Our economies are switching towards a more sustainable development model; after investing in Vestiaire Collective last year, wallapop is Korelya’s second investment in the circular economy, while COVID-19 is only strengthening that trend. It is Korelya’s mission to back tomorrow’s European tech champions and we believe that NAVER has a proven tech and product edge that will help the company reinforce its leading position in Europe,” added Fleur Pellerin, CEO of Korelya Capital.

Powered by WPeMatico

BigCommerce has partnered with Walmart to allow its customers to sell on the Bentonville, Arkansas-based retailer’s e-commerce marketplace, it announced this morning. Shares of Austin-based BigCommerce rose sharply in pre-market trading after the news, gaining around 10% before the bell.

Walmart, best-known for in-person shopping, has proven an e-commerce success story in recent years. For example, in its most recent quarter while Walmart as a whole grew 7.3%, its e-commerce sales advanced 69%.

BigCommerce has also reported strong growth in recent quarters, supported in part by partnerships similar to the one that it announced today. The e-commerce SaaS provider rolled out an integration with Wish last year, for example.

In a call concerning its earnings, which were announced before the Walmart news was announced, BigCommerce CEO Brent Bellm told TechCrunch that his company had been impressed with customer uptake of the Wish integration. Regarding the Walmart partnership, in a second interview Bellm told TechCrunch that it was overdue on the BigCommerce side; given the historical success of the Wish deal, it will be curious to dig into how many of the e-commerce platform’s customers opt to sell on Walmart, and how quickly they do so.

TechCrunch also spoke with Walmart exec Jeff Clementz about the arrangement. He stressed Walmart’s online customer monthly-actives — 120 million, per his company — and the breadth of their demand; BigCommerce customers selling on Walmart could expand its product diversity, helping the traditionally physical retailer possible continue its rapid growth.

The two companies are incentivizing adoption of the deal amongst BigCommerce customers by waiving certain fees for a month for retailers that sign up to sell on Walmart; Clementz described it as the first time that his company had offered a “new-seller discount.”

TechCrunch has had its eye on BigCommerce for some quarters now, thanks in part to its 2020 IPO. But the company is also interesting as its regular earnings results provide a lens into the world of e-commerce growth amongst independent digital retailers. Shopify, a chief BigCommerce rival, provides a similar view into the e-commerce world.

Shopify previously integrated with Walmart in the middle of 2020.

Looking ahead, it will be interesting to see if the Walmart partnership helps BigCommerce continue its improving revenue growth. The company is in a market share race with Shopify. But while BigCommerce’s rival has posted impressive growth from its integrated solutions, like its payments service, the Austin-based company stresses what it calls a more open model. Shopify charges many customers a percentage of their transaction volume for using a third-party payment solution over its own, for example, which Bellm described as a “tax” during an interview.

“Merchant Solutions” revenue at Shopify, which it generates “principally” from “payment processing fees from Shopify Payments,” grew 116% in 2020 to a little over $2 billion.

So with BigCommerce collecting a partnership with Walmart to match Shopify’s own, we’re seeing not merely two e-commerce platforms go toe-to-toe on providing their customers with as much market access as they can, but two different business philosophies compete. Akin to Microsoft Teams and Slack, it’s a competition to spectate.

Powered by WPeMatico

This morning Shippo, a software company that provides shipping-related services to e-commerce companies, announced a new $45 million investment. The new capital values the startup at $495 million. TechCrunch is calling the new funding a Series D as it is a priced round that followed its Series C; the company did not award the round a moniker.

Shippo’s 2020 Series C, a $30 million transaction that was announced last April, valued the company at around $220 million. D1 Capital led both Shippo’s Series C and D rounds, implying that it was content to pay around twice as much for the company’s equity in 2021 than it was in 2020. (Recall that investors doubling-down on previous bets as lead investor in successive rounds is no longer considered to be a negative signal concerning startup quality, but a positive indicator.)

Why raise more money so soon after its last round? According to Shippo CEO and founder Laura Behrens Wu, her company made material progress on customer acquisition and partnerships last year. That led to a decision around the time of Shippo’s Q4 board meeting with her investors that it was a good time to put more capital into the company.

In a sense the timing is reasonable. As Shippo scales its customer base, it can negotiate better shipping deals with various providers, which, in turn, help it continue to attract new customers. Behrens Wu noted in an interview with TechCrunch that when her company was helping its early customers ship just a few packages, shipping companies it supports on its platform didn’t want to meet with the startup. Now armed with more volume, Shippo can recycle customer demand into partner leverage, improving its total customer offering.

Behrens Wu said that Shippo had secured such a partnership with UPS before it raised its new round.

Turning to growth, Shippo doubled its platform spend, or “GPV” last year. GPV is the company’s acronym for gross postage volume. It roughly tracks with revenue, TechCrunch confirmed. So Shippo likely doubled its top-line last year. That’s good. Shippo wants to do that again this year, Behrens Wu told TechCrunch. The startup will also double its headcount this year, adding around 150 people.

Now flush with more capital, what’s next for Shippo? Per its CEO, the startup wants to invest more in platforms (where Shippo is baked into a marketplace, for example), international expansion (Shippo only does a “little bit” of international shipping, per Behrens Wu), and double-down on what it considers its core customer base.

TechCrunch was curious about how broad Shippo might take its product from its original home in shipping labels. The startup said that there’s lots of room in the journey of a package, from pre-purchase on, where her company might expand into. However, Behrens Wu cautioned that such a broadening of product work is not an immediate focus at her company.

Let’s see how long the current e-commerce boom lasts and how far this new capital can take Shippo. If it doubles in size again this year we’ll have to start its IPO countdown sometime in mid-2022.

Powered by WPeMatico

If we are not careful, every entry of this column could consist of SPAC news.

Special purpose acquisition companies, or blank-check companies, whatever you prefer to call them, are enormous business today. But they aren’t the only thing going on, and we’ll get to other things shortly. Consider this an apology for having written about SPACs twice in two days.

Yesterday, we considered the rise of the VC-led SPAC and whether venture capital groups that offer seed-through-SPAC money will wind up with advantage in the market over firms that specialize on any particular startup stage. Sticking to the blank-check theme, this morning we’re looking into two SPAC-led deals, namely those involving Rover and MoneyLion.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

We’re doubling up to prevent more SPAC-related posts. And we’ve selected Rover because Chewy, another pet-themed entity, is an already-public company. As both were venture-backed, we may be able to contrast their trading performance post-debut. Sadly, Chewy is focused on pet e-commerce while Rover is more centered around pet services, but they may prove close enough for some loose comparisons.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup, one that TechCrunch has covered extensively. If its SPAC-assisted vault into the public markets goes well, it could smooth the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised capital.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup, one that TechCrunch has covered extensively. If its SPAC-assisted vault into the public markets goes well, it could smooth the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised capital.

So this is a SPAC post, but as we’ll largely be looking at the financial health of two companies that we’ve heard about for ages and never got to see inside of, I hope you join me all the same.

We’re starting with the Rover investor presentation, before zipping over to MoneyLion’s own.

Rover is merging with Nebula Caravel Acquisition Corp., which is affiliated with True Wind Capital. The deal gives Rover an anticipated market cap of around $1.6 billion, with around $300 million in cash on its books.

So, how attractive is this new unicorn? You can find its investor deck here, if you want to read along as we peek.

First up, the company stresses rising use of digital services in the last year thanks to the pandemic and the fact that pet ownership is growing. Both of which are true. We’ve seen the accelerating digital transformation for both companies and consumers. And if you’ve tried to adopt a pet lately, you’ve seen how few are left waiting for forever homes.

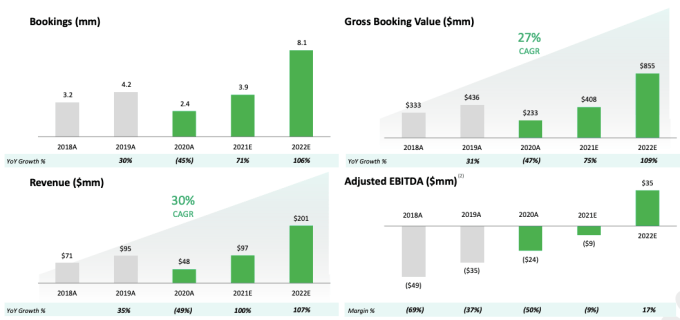

With those things behind it, you might be wondering why Rover is pursuing a SPAC-led debut as well. If its market is hot and it has previously raised venture capital, why not just go public via an IPO? Because 2020 was tough on the company.

Image Credits: Rover

Revenue dipped from $95 million in 2019 to just $48 million last year. Bookings fell from 4.2 million to 2.4 million over the same time frame, leading to gross booking value falling from $436 million in 2019 to $233 million in 2020. Why? Because everyone was stuck at home. With their pets. A situation that limited demand for Rover-delivered pet services.

Powered by WPeMatico

Talkshoplive is a startup that’s worked with stars like Paul McCartney and Garth Brooks, as well as small businesses, to host shopping-focused live videos. Today, it’s announcing that it has raised $3 million in seed funding from Spero Ventures.

CEO Bryan Moore founded the company with his sister Tina in 2018. Moore previously led social media efforts at Twentieth Television (previously known as Twentieth Century Fox) and CBS Television, and he said he was inspired to launch Talkshoplive by the rise of livestreamed shopping experiences in China.

At the same time, Moore said it wasn’t enough to just copy what worked in China: “Small businesses are different here, talent is different, the needs are different.” One of the keys, in his view, is to focus on helping creators and businesses meet their customers where those customers already are — which he also suggested differentiates Talkshoplive from competing services as well.

For one thing, the startup does not require consumers to download any additional apps in order to watch its videos. Instead, it’s created a video player that works on the Talkshoplive website, on the websites of its partners and anywhere else that videos can be embedded. And wherever those videos are played, they also include a one-click buy button.

Moore said Talkshoplive started out with a focus in books and music, working with famous names like Matthew McConaughey, Alicia Keys and Dolly Parton, as well as the aforementioned Brooks and McCartney. For example, Brooks used Talkshoplive to exceed more than 1 million vinyl pre-sales for his “Legacy Collection” box set in 2019.

On the book side, Talkshoplive has worked with publishers including Harper Collins, Penguin Random House, Simon & Schuster and Macmillan. Moore claimed the platform is driving three to nine times the sales an author would see on other e-commerce sites.

At the same time, he emphasized that the startup is also working with more than 3,500 small businesses, and he said that when a small business owner is broadcasting on Talkshoplive, “You’re creating your own microfandom by being able to tell the story … You’re making yourself a brand story, even as a small business.”

He added, “When you’re able to help people move $25,000 in a show — for a small business, that’s a huge deal.”

In this sense, Moore said he sees Talkshoplive as a continuation of his previous work in social media, all connected by the question, “How are you creating human connection in a digital landscape?” The “ultimate goal,” he added, is to turn the platform into a “digital Main Street” for businesses everywhere.

More recently, Talkshoplive has been moving into other categories like food and beauty, and Moore said he’s excited to work with Spero founding partner Shripriya Mahesh (previously an executive at eBay and First Look Media) to “continually evolve our product and create these tools that help us scale faster — and also help benefit these businesses.”

“From the moment we met the Talkshoplive team, we were impressed with their focus on enabling SMB’s with a new, creative, innovative way to build their businesses,” Mahesh said in a statement. “Talkshoplive also innovates on the marketplace model with a way for buyers to truly engage with the sellers, get to know them, and experience shopping in a whole new way. We are incredibly excited by the community that is taking shape at Talkshoplive and are thrilled to be working with Bryan, Tina, and the TSL team as they grow their community and the marketplace.”

Powered by WPeMatico

A new breed of startups is acquiring and growing small but promising third-party merchants, and building out their own economies of scale.

And while there are a number of such startups based in the U.S. and Europe, none had emerged in the Latin American market. Until now.

Valoreo, a Mexico City-based acquirer of e-commerce businesses, announced Tuesday that it has raised $50 million of equity and debt financing in a seed funding round.

The dollar amount is large for a seed round by any standards, but most certainly ranks among the highest ever raised by a Latin American startup — further evidence of increased investor interest in the region’s burgeoning venture scene.

Upper90, FJ Labs, Angel Ventures, Presight Capital and a slew of angel investors participated in the round. Those angels included David Geisen, head of Mercado Libre Mexico; BEA Systems’ co-founder Alfred Chuang; and Tushar Ahluwalia, founder of Razor Group, a European marketplace aggregator, among others.

Founded in late 2020, Valoreo aims to invest in, operate and scale e-commerce brands as part of its self-described mission “to bring better products at more affordable prices” to the Latin American consumer.

“We were substantially oversubscribed and were therefore able to select investors that not only provide capital, but also additional know-how in key areas,” said co-founder Alex Gruell.

Valoreo joins the growing number of startups focused on rolling up e-commerce brands.

The company’s model is similar to that of Thrasio — which just raised another $750 million –– and Perch in the U.S. But Valoreo says its approach has been tailored to “the specific needs of the Latin American market and is specifically focused on the Latin American end customer.”

Another new company in the space called Branded recently launched its own roll-up business on $150 million in funding. Others in the space include Berlin Brands Group, SellerX, Heyday and Heroes.

But as my colleague Ingrid Lunden points out, “the feverish pace of fundraising in the area of FBA roll-ups feels very much like a bubble in the market — not least because none of these still-young companies have yet to prove that the strategy to buy up and consolidate these sellers is a useful and profitable one.”

Valoreo (which the company says is an extension of the Spanish word “valor,” meaning to add value), acquires merchants that operate their own brands and primarily sell on online marketplaces such as Mercado Libre, Amazon and Linio. The company targets brands that offer “category-leading products” and which it believes have “significant growth potential.” It also develops brands in-house to offer a broader selection of products to the end customer.

Like Thrasio, Valoreo says it’s able to help entrepreneurs who may lack the resources and access to capital to take their businesses to the next level.

Co-founder and co-CEO Stefan Florea says the company takes less than five weeks typically from its initial contact with a seller to a final payout.

Then, the acquired and developed brands are integrated into the company’s consolidated holding. By tapping its team of “specialists” in areas such as digital marketing and supply chain management, it claims to be able to help these brands “reach new heights” while giving the entrepreneurs behind the companies “an attractive exit,” or partial exit in some cases.

“We have different structures, always taking into account the personal objectives of the seller,” Stefan Florea added.

Generally Valoreo acquires the majority of the business, with the purchase price typically being a combination of an upfront cash payment and a profit share component so sellers can still earn money.

Looking ahead, Valoreo plans to use its new capital mostly to acquire and develop “interesting” brands, as well as build out its current team of 10 while expanding its infrastructure and operations.

The company is currently focused on the Mexican and Brazilian markets, but is planning its expansion into other Latin American countries where it has strong local support systems, such as Colombia, according to co-founder Martin Florea.

“Our mission is to be a pan-Latin American player providing value to the entire region,” Martin Florea said. “Latin America in general and Mexico in particular are in a distinct situation which provides phenomenal opportunities for e-commerce merchants on the one hand but also presents particular challenges on the other hand.”

Those challenges, according to Martin Florea, include limited access to growth capital, a lack of specialized expertise in certain areas (such as supply chain management), limited opportunities to sell their business and pursue new ventures, as well as operational burdens and the lack of capacities to expand into new countries and marketplaces.

Valoreo emphasizes it is not out to compete with Mercado Libre, Amazon and other regional marketplaces but instead wants to partner with them.

“Without these platforms, this opportunity would not exist,” Martin Florea said.

Hernán Fernández, founder and managing partner of Angel Ventures, believes Valoreo “will add a lot of value” to the Latin American e-commerce landscape, which is experiencing both market growth and the fragmentation of the seller space.

Jüsto co-founder and CEO (and Valoreo investor) Ricardo Weder notes that the e-commerce market is at an inflection point in Latin America. According to eMarketer, the region was the fastest-growing e-commerce market in the world in 2020, with 37% year over year growth. However, it is a much more fragmented and crowded market compared to other regions, such as the United States.

This, Valoreo believes, provides an opportunity for consolidation.

“There are still many consumers that are not aware of the great variety of outstanding local brands that sell innovative products on marketplaces online,” Stefan Florea said. “In the U.S. or Europe e-commerce is the new way of shopping, offering an even greater range of products and brands than offline shopping. We firmly believe it will not take long until end-customers in Mexico and across Latin America discover all the benefits that e-commerce offers.”

Powered by WPeMatico

French startup Lengow has a new landlord as Marlin Equity Partners has acquired a majority stake in the company. Lengow operates a software-as-a-service platform to optimize e-commerce listings. Terms of the deal are undisclosed.

In particular, many sellers now list their items on multiple e-commerce websites at once. For instance, a company could have its own e-commerce website and also sell products on Amazon, eBay, etc. And you may have noticed the same third-party sellers on different marketplaces.

Manually listing items across multiple e-commerce platforms would be extremely tedious. Behind the scenes, Lengow tries to automate as many steps as possible. First, you can import your products by connecting Lengow with your product information management system (PIM) or your e-commerce back end — it can run on Akeneo, Shopify, Magento, WooCommerce, etc.

You can then publish your products on multiple sales channels at once. It can be a marketplace, a price comparison website, a social network or an adtech platform. Examples include Amazon, Google Shopping, Criteo, Instagram, etc.

Lengow also helps you track orders, create rules when you’re running low on stock and manage your advertising strategy. Essentially, it’s the glue that makes all the moving parts of e-commerce stick together. There are 4,600 merchants using Lengow globally.

Marlin describes the deal as a growth investment. The firm plans to increase the value of Lengow in the coming years as it hasn’t reached its full potential yet. “We are looking forward to leveraging our operational and financial resources to support Lengow’s growth trajectory and continued international expansion,” Marlin principal Roland Pezzutto said in a statement.

Powered by WPeMatico