EC United States

Auto Added by WPeMatico

Auto Added by WPeMatico

Inflation may or may not prove transitory when it comes to consumer prices, but startup valuations are definitely rising — and noticeably so — in recent quarters.

That’s the obvious takeaway from a recent PitchBook report digging into valuation data from a host of startup funding events in the United States. While the data covers the U.S. startup market, the general trends included are likely global, given that the same venture rush that has pushed record capital into startups in the U.S. is also occurring in markets like India, Latin America, Europe and Africa.

The rapidly appreciating startup price chart is interesting, and we’ll unpack it. But the data also implies a high bar for future IPOs to not only preserve startup equity valuations at their point of exit, but exceed their private-market prices. A changing regulatory environment regarding antitrust could limit large future deals, leaving a host of startups with rich price tags and only one real path to liquidity.

Investors appear to be implicitly betting that the future IPO market will accelerate for a multiyear period at attractive prices.

That situation should be familiar: It’s the unicorn traffic jam that we’ve covered for years, in which the global startup markets create far more startups worth $1 billion and up than the public markets have historically accepted across the transom.

Let’s talk about some big numbers.

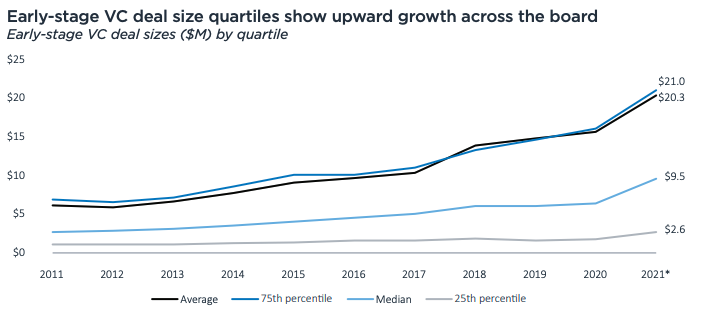

To summarize what PitchBook published: Round sizes are going up as valuations go up, and with the latter rising faster than the former, we’re not seeing investors get more ownership despite them having to spend more for deal access.

In the early-stage market, deal sizes are rising as follows:

Image Credits: PitchBook

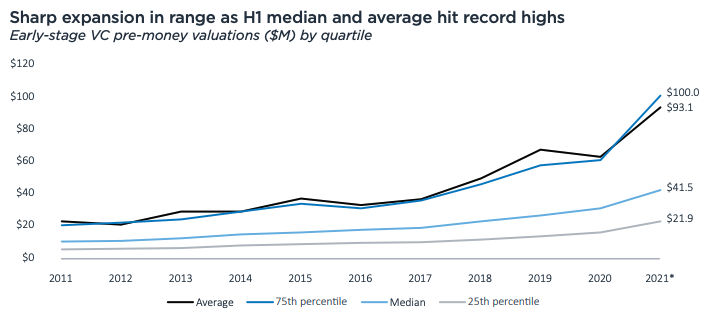

Prices are going up as well, as the following chart shows:

Image Credits: PitchBook

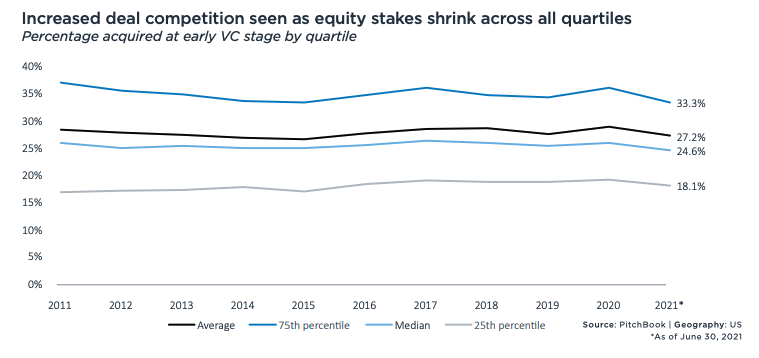

Which leads to the following decline in equity take rates:

Image Credits: PitchBook

Those charts belie somewhat how quickly venture capital is changing. For example, in 2020, the median early-stage value created between rounds was $16 million (or a 54% relative velocity, if you prefer). In 2021 thus far, it’s $39.4 million (120% relative velocity). And that 2020 figure was a prior record. It just got smashed.

The PitchBook dataset has other superlatives worth noting. Enterprise-focused seed pre-money valuations hit an average of $11 million in the first half of 2021, an all-time high. Early-stage valuations for enterprise-focused startups also hit fresh records — $92.7 million on average, $43 million median — this year after rising consistently since 2011.

And late-stage valuations for enterprise tech startups have gone vertical (chart on the right):

Powered by WPeMatico

Robinhood priced at $38 per share this week, opened flat and closed its first day’s trading yesterday worth $34.82 per share, or a bit more than 8% underwater. The company posted a mixed picture today, falling early before recovering to breakeven in late-morning trading.

It wasn’t the debut that some expected Robinhood to have.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

To close out the week, we’re not going to noodle on banned Chinese IPOs or do a full-week mega-round discussion. Instead, let’s parse some notes from a chat The Exchange had with Robinhood’s CFO about his company’s IPO and go over a few reasonable guesses as to why we’re not wondering how much money Robinhood left on the table by pricing its public offering lower than it closed on its first day.

Let’s not be dicks about it. The time for Twitter jokes was yesterday. We’ll put our thinking caps on this morning.

Let’s not be dicks about it. The time for Twitter jokes was yesterday. We’ll put our thinking caps on this morning.

Chatting with Robinhood CFO Jason Warnick earlier this week, we wanted to know why this was the right time for Robinhood to go public.

Now, no public company CEO or CFO will come out and directly say that they are going public because they think that they can defend — or extend — their most recent private valuation thanks to current market conditions.

Instead, execs on IPO day tend to deflect the question, pivoting to a well-oiled bon mot about how their public offering is a mere milestone on their company’s long-term trajectory. For some reason in our capitalist society, during an arch-capitalist event, by a for-profit company, leaders find it critical to downplay their IPO’s importance.1

With that in mind, Warnick did not say Robinhood went public because the IPO market has recently rewarded big-brand consumer tech companies like Airbnb and DoorDash with strong debuts. And he didn’t say that with tech shares near all-time highs and a taste for high-growth concerns, the company was likely set to enter a market that would be willing to price it at a valuation that it found attractive.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie,

I handle people ops as a consultant at several different tech startups. Many have employees on OPT or STEM OPT who didn’t get selected in this year’s H-1B lottery.

The companies want to retain these individuals, but they’re running out of options. Some companies will try again in next year’s H-1B lottery, even though they face long odds, particularly if the H-1B lottery becomes a wage-based selection process next year.

Others are looking into O-1A visas, but find that many employees don’t yet have the experience to meet the qualifications. Should we look at Canada?

— Specialist in Silicon Valley

Dear Specialist,

That’s what we’re all about — finding creative immigration solutions to help U.S. employers attract and retain international talent and help international talent reach their dreams of living and working in the United States.

I’ve written a lot on how U.S. tech startups can keep their international team members in the United States. One strategy is to help the startup employees become qualified for O-1As. Another is to obtain unlimited H-1B visas without the lottery through nonprofit programs affiliated with universities. Sometimes candidates return to school for master’s degrees that offer a work option called CPT, or curricular practical training.

Image Credits: Joanna Buniak / Sophie Alcorn (opens in a new window)

But sometimes, companies end up deciding to move some of their international talent to Canada to work remotely. Recently, Marc Pavlopoulos and I discussed how to help U.S. employers and international talent on my podcast. Through his two companies, Syndesus and Path to Canada, Pavlopoulos helps both U.S. tech employers and international tech talent when their employees or they themselves run out of immigration options in the United States. He most often assists U.S. tech employers when their current or prospective employees are not selected in the H-1B lottery.

Through Syndesus, a Canada-based remote employer — also known as a professional employment organization (PEO) — Pavlopoulos helps U.S. employers retain international tech workers who either no longer have visa or green card options that will enable them to remain in the United States or those who were born in India and are fed up by the decades-long wait for a U.S. green card. U.S. employers that don’t have an office in Canada can relocate these workers to Canada with the help of Syndesus, which employs these tech workers on behalf of the U.S. company, sponsoring them for a Canadian Global Talent Stream work visa.

Syndesus also helps U.S. tech startups without a presence in Canada find Canadian tech workers and employ them on the startup’s behalf. As an employer of record, Syndesus handles payroll, HR, healthcare, stock options and any issues related to Canadian employment law.

Pavlopoulos’ other company, Path to Canada, currently focuses on connecting international engineers and other tech talent working in the U.S. — including those whose OPT or STEM OPT has run out — who cannot remain in the U.S. find employment in Canada, either at a Canadian company or at the Canadian office of a U.S. company. These employees get a Global Talent Stream work visa and eventually permanent residence in Canada. Pavlopoulos intends to expand Path to Canada to help tech talent from around the world live and work in Canada.

Powered by WPeMatico

Jen Young and Jeff Cavins were sitting in a beige conference room at a downtown Vancouver hotel, wasting away under fluorescent lights, an endless PowerPoint and a pair of sad Styrofoam cups of coffee between them. Young was there on a marketing contract. Cavins was a board member. They shared one of those looks that only couples can understand. It said: There’s got to be something better than this.

With 40 years of running technology companies under Cavins’ belt and a successful ad agency career under Young’s, the two decided to craft a business around their shared passion of being out in nature. When they realized there are more than 20 million recreational vehicles all across the U.S., most of which are used only a handful of days, they saw an opportunity. They asked themselves: How do we create memorable outdoor experiences and make them available to everybody?

For seven months, the couple traveled across the U.S. to do market research on travelers and RV owners to form the basis of their company.

The sharing economy of Uber, Lyft and Airbnb had already laid the groundwork. Why not open it up to RVs?

In 2014, Young and Cavins invested their life savings into Outdoorsy, sold their homes and jumped into an Airstream Eddie Bauer trailer. For seven months, the couple traveled across the U.S. to do market research on travelers and RV owners to form the basis of their company.

In June, Outdoorsy raised $90 million in a Series D led by ADAR1 Partners, as well as an additional $30 million in debt financing from Pacific Western Bank. The money will be used in large part to accelerate the growth of Outdoorsy’s insurtech business, Roamly. In the same month, the company announced a partnership with glamping company Collective Retreats to expand its outdoor offerings.

The following interview, part of an ongoing series with founders who are building transportation companies, has been edited for length and clarity.

You’ve taken a personal approach to your business, spending months in the research phase actually living in an RV and interviewing RV owners and their families around the country. How do you think that’s shaped your business?

Jen Young: When we lived on the road, we had to experience that customer experience every day for hundreds of days. So this is where we were able to pick up and identify what the biggest pain points were on the renter and the owner side and start tackling those first.

For example, we understood what was most important from an insurance perspective because we could hear the voices of renters and owners — they consider these things their babies in many cases.

The owners that are more entrepreneurial-minded, they consider them more of a business asset, but both of them want to know, “What am I going to get for liability insurance? Comp and collision? Interior damage?” The detailed list of those things became the beginning of the product roadmap, as well as itemizing what things have to occur for a good guest experience.

In what ways have you had to pivot your model based on how people have used your platform?

Cavins: One of the things we learned is most renters don’t want to drive these things, so owners started to do delivery, which became very popular on our platform. Sixty percent of all owners now will just deliver and set up for you so you can arrive at your campsite and everything’s just done. Your chairs are out, your barbecue is out, your awning is out and maybe a bottle of champagne in your fridge for you.

When Jen and I were traveling last year, we saw that most of the American landscape of campgrounds and campsites were overbooked. People couldn’t get their reservations closed the way that you would expect in a world of technologically evolved industries, and we thought there had to be something better in terms of the customer experience for camping, which really catalyzed our investment in glamping company Collective Retreats.

Powered by WPeMatico

Duolingo filed to go public yesterday, giving the world a deep look inside its business results and how the pandemic impacted the edtech unicorn’s performance. TechCrunch’s initial read of the company’s filing was generally positive, noting that its growth was impressive and its losses modest; Duolingo recently began making money on an adjusted basis.

While the company’s top-level numbers are impressive, we want to go one level deeper to grow our understanding of the company beyond our EC-1.

Duolingo is likely entering a period in which it will have to invest heavily in features like pronunciation, efficacy and new apps — which could come at a steep upfront cost.

First, we’ll explore the growth of Duolingo’s total user base, how much money it makes per active user, and how effectively the company has managed to convert free users to paid products over time. The numbers will set us up to understand what else can be learned about Duolingo’s business beyond our original deep dive into the company’s finances — specifically underscoring the pressure cooker it finds itself in when looking for new revenue sources.

Starting with Duolingo’s growth in total active users, guess how fast they rose from 2019 to 2020. Hold that number in your head.

The actual numbers are as follows: In 2019, Duolingo closed the year with 27.3 million monthly active users (MAUs); it wrapped 2020 with 36.7 million MAUs. That’s a gain of 34%. If we narrow our gaze to Q1 2021 numbers compared to Q1 2020, we can see that Duolingo’s MAUs rose from 33.5 million to 39.9 million, or growth of around 19%.

The bulk of Duolingo’s growth, then, came in early 2020 when we consider its pandemic bump. Put more simply, the company scaled from 27.3 million MAUs at the end of 2019 to 33.5 million MAUs at the end of Q1 2020; from then, the company added 3.2 million more MAUs throughout 2020 and 6.4 million during the next four quarters.

Another lens through which to view the numbers is simply a recognition that first-quarter results at Duolingo appear to be stronger than results in the rest of the year, perhaps due to New Year’s resolutions to learn a new language or brush up on a second language learned in high school.

Next, let’s examine Duolingo’s monetization efforts regarding converting free users to paying users.

Here we can see a very different growth story. While the company’s MAUs rose 34% from 2019 to 2020, the company’s paying users rose from 900,000 at the end of 2019 to 1.6 million at the end of 2020. That is a far sharper gain of 84% on a year-over-year basis.

So, while Duolingo did see material user growth during 2020, it saw turbocharged expansion in the users it was able to shake revenue from. Improved monetization, more than acceleration in user growth, was the pandemic’s effect on Duolingo.

What can we see in the company’s more recent results? From Q1 2020 to Q1 2021, Duolingo’s paid subscribers rose from 1.1 million to 1.8 million, a gain of around 64%. That was a slower pace than the company managed more generally in 2020, which matches Duolingo’s slower revenue growth in Q1 2021 than it recorded in 2020.

The number is still strong, we think. But not as impressive as the more than 100% revenue expansion that the company put on the board last year.

In percentage terms, 3.3% of Duolingo’s MAUs were paid subscribers in 2019. That figure rose to 4.4% in 2020. And in Q1 2021, it reached 4.5%. Duolingo rounds that number to 5% in its S-1, which feels somewhat aggressive to us, given the somewhat modest pace at which the metric is improving. Here’s the wording:

As of March 31, 2021, approximately 5% of our monthly active users were paid subscribers of Duolingo Plus. Our paid subscriber penetration has increased steadily since we launched Duolingo Plus in 2017 and, combined with our user growth, has led to our revenue more than doubling every year since.

A gain of 0.1 percentage point in a quarter is growth, we suppose.

Next, let’s chat about revenue per MAU. To get consistent numbers, we’ll divide quarterly revenues by MAU figures from the same period. So, we’ll compare Q4 2019 revenue at Duolingo with its year-end MAU figure. We’ll do the same for 2020, and for Q1 2021 we’ll use both numbers from that period.

Powered by WPeMatico