EC Southeast Asia & Oceania

Auto Added by WPeMatico

Auto Added by WPeMatico

Southeast Asian tech companies are drawing the attention of investors around the world. In 2020, startups in the region raised over $8.2 billion, about four times more than they did in 2015. This trend continued in 2021, with regional M&A hitting a record high of $124.8 billion in the first half of 2021, up 83% from a year earlier.

This begs the question: Who exactly is investing in Southeast Asia?

Let’s explore the three key types of investors pouring money into and driving the growth of Southeast Asia’s tech ecosystem.

Over 229 family offices have been registered in Singapore since 2020, with total assets under management of an estimated $20 billion.

Southeast Asia has become an attractive market for U.S. and Chinese tech firms. Internet penetration here stands at 70%, higher than the global average, and digital adoption in the region remains nascent — it wasn’t until the pandemic that adoption of digital services such as e-wallets and online shopping took off.

China’s tech giants Tencent and Alibaba were among the first to support early e-commerce growth in Southeast Asia with investments in Sea Limited and Lazada, and have since expanded their footprint into other internet verticals. Alibaba has backed Akulaku, M-Pay (eMonkey), DANA, Wave Money and Mynt (GCash), while Tencent has invested in Voyager Innovations (PayMaya), SHAREit, iflix, Ookbee and Sanook.

U.S. tech firms have also recently entered the scene. In June 2020, Gojek closed a $3 billion Series F round from Google, Facebook, Tencent and Visa. Google, together with Singapore’s Temasek Holdings, invested some $350 million in Tokopedia in October. Meanwhile, Microsoft invested an undisclosed amount in Grab in 2018 and has invested $100 million in Indonesian e-commerce firm Bukalapak.

In Q1 2021, Southeast Asian startups raised $6 billion, according to DealStreetAsia, positioning 2021 as another record year for VC investment in the region.

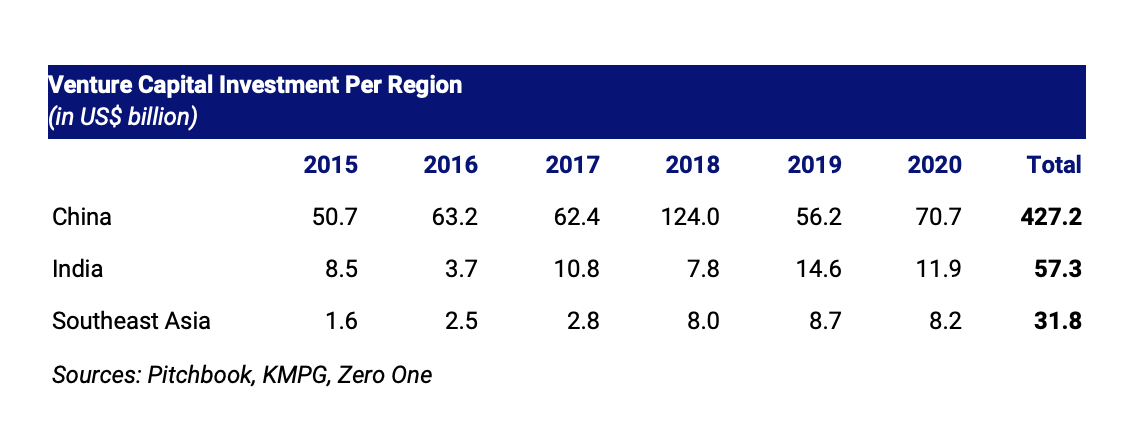

The region is also rising in prominence as a destination for investment capital relative to the rest of Asia. Regional VC investment grew 5.2 times to $8.2 billion in 2020 from $1.6 billion in 2015, as we can see in the table below.

Image Credits: Jungle VC

Southeast Asia also has many opportunities for VC investment relative to its market size. From 2015 to 2020, China saw VC investment of nearly $300 per person; for Southeast Asia — despite a recent investment boom — this metric sits at just $47.50 per person, or just a sixth of that in China. This implies a substantial opportunity for investments to develop the region’s digital economy.

The region’s rising population and growth prospects are higher due to China’s population growth challenges, alongside the latter’s higher digital economy market saturation and maturity.

Powered by WPeMatico

Singapore is home to fewer than six million people, making it one of the smallest ASEAN countries, in terms of population. It is a young country as well — having gained independence in 1963 — and resides in a neighborhood with far larger economies, including China, Indonesia, and Vietnam. When the country first became independent, its mandate was to simply survive rather than thrive.

So how does a country evolve from a position of relative uncertainty, with comparatively few resources, to one that leads the ASEAN region in venture capital investment and has been home to 10 unicorns?

Countries around the world examine Singapore’s ecosystem from a distance, hoping to learn from, and emulate, its story. The World Bank Group recently published a report, The Evolution and State of Singapore’s Start-up Ecosystem, documenting the country’s experience in building its startup ecosystem and the challenges facing it.

This article presents an overview of the report’s key findings and offers a few key recommendations on what other countries can learn from Singapore’s experience, as well as what Singapore itself can do to maintain progress.

As of 2019, Singapore had over $19 billion in PE and VC assets under management, more than twice that of neighboring Indonesia, Philippines, Vietnam, Malaysia, and Thailand combined. In that same year, the country was home to an estimated 3,600 tech startups and nearly 200 different intermediary and supporting organizations (accelerators, co-working spaces, coding academies, etc.) – some which have a multinational presence, such as Blk71, whose Singapore headquarters has been referred to as “the world’s most tightly packed entrepreneurial ecosystem.”

While assessing the size and strength of startup ecosystems is an evolving method, Start-up Genome priced Singapore’s ecosystem at over $25 billion, five times the global median.

Arguably, the most eye-catching hallmark of this ecosystem is its population of current and former unicorns. Collectively, Singapore has been home to ten unicorns, three of which have offered an IPO (Nanofilm, Razer and Sea) and two of which have been acquired – one by giant Alibaba (Lazada) and one by Chinese streaming powerhouse YY (Bigo Live). The remaining five are Trax, Acronis, JustCo, PatSnap, and Grab – the ASEAN region’s largest unicorn to date.

The education sector is also prominent in Singapore’s ecosystem. Universities like the National University of Singapore (NUS) and Nanyang Technological University (NTU) are deeply embedded into this ecosystem, helping with R&D commercialization linkages, incubation, talent/knowledge transfer, and other areas.

Numerous factors have contributed to building Singapore’s startup ecosystem, with government intervention and leadership being the dominant driving forces. The government has spent more than USD60 billion over the past several decades to enhance the country’s R&D infrastructure, create VC funds, and launch accelerators and other support organizations.

Powered by WPeMatico