EC Market Map

Auto Added by WPeMatico

Auto Added by WPeMatico

The pandemic has highlighted some of the brightest spots — and greatest areas of need — in America’s healthcare system. On one hand, we’ve witnessed the vibrancy of America’s innovation engine, with notable contributions by U.S.-based scientists and companies for vaccines and treatments.

On the other hand, the pandemic has highlighted both the distribution challenges and cost inefficiencies of the healthcare system, which now accounts for nearly a fifth of our GDP — far more than any other country — yet lags many other developed nations in clinical outcomes.

Many of these challenges stem from a lack of alignment between payment and incentive models, as well as an overreliance on hospitals as centers for care delivery. A third of healthcare costs are incurred at hospitals, though at-home models can be more effective and affordable. Furthermore, most providers rely on fee for service instead of preventive care arrangements.

These factors combine to make care in this country reactive, transactional and inefficient. We can improve both outcomes and costs by moving care from the hospital back to the place it started — at home.

Right now in-home care accounts for only 3% of the healthcare market. We predict that it will grow to 10% or more within the next decade.

In-home care is nothing new. In the 1930s, over 40% of physician-patient encounters took place in the home, but by the 1980s, that figure dropped to under 1%, driven by changes in health economics and technologies that led to today’s hospital-dominant model of care.

That 50-year shift consolidated costs, centralized access to specialized diagnostics and treatments, and created centers of excellence. It also created a transition from proactive to reactive care, eliminating the longitudinal relationship between patient and provider. In today’s system, patients are often diagnosed by and receive treatment from individual doctors who do not consult one another. These highly siloed treatments often take place only after the patient needs emergency care. This creates higher costs — and worse outcomes.

That’s where in-home care can help. Right now in-home care accounts for only 3% of the healthcare market. We predict that it will grow to 10% or more within the next decade. This growth will improve the patient experience, achieve better clinical outcomes and reduce healthcare costs.

To make these improvements, in-home healthcare strategies will need to leverage next-generation technology and value-based care strategies. Fortunately, the window of opportunity for change is open right now.

Over the last few years, five significant innovations have created new incentives to drive dramatic changes in the way care is delivered.

Powered by WPeMatico

The pandemic has been extremely painful for many. But as lockdowns lifted and people began resuming their outdoor hobbies, mobile-first businesses have seen growth accelerate as consumers turned to digital tools to improve their time outdoors.

The Dyrt, for example, is the top camping app on the Apple and Google Play App Stores. The app sits at the confluence of two trends: An increased interest in outdoor recreation and travel, and an explosion in consumer subscription software (CSS).

The Dyrt launched its premium offering in 2019, The Dyrt PRO, in time to take advantage of the rising number of Americans making the great outdoors part of their lifestyle. A year later, it had a new subscriber every two minutes paying for features like offline maps and detailed camping information.

CSS businesses at the forefront of outdoor activities have closed major deals in recent years such as hunting app OnX (Summit Partners), hiking app Alltrails (Spectrum Equity), Surfline (The Chernin Group) and mountain bike leader Pinkbike (Outside Media). Companies like Netflix and Spotify have trained consumers to pay monthly or annual fees for software that enhances their lives, creating a business model investors view as reliable and poised for growth.

I think of different outdoor activities almost like individual genres on Netflix. Dominating camping or surfing might be like capturing the streaming market for comedy or horror.

Fitness and the outdoor passion space is one of the most exciting CSS categories in a growing landscape that includes everything from family planning/management services to entertainment and education. I believe CSS is still in the early stages of its growth — perhaps where B2B SaaS was a decade ago.

So what sets apart the great CSS businesses from the good ones?

The beauty of the CSS model is the complete alignment between the business and its customers. CSS companies don’t have to please advertisers, and they can design purely for their users.

This dynamic is particularly powerful for CSS companies in the outdoors space, which make your favorite outdoor activity better with performance analytics and enhanced information such as maps, reviews, air quality reports and fire warnings. Consumers are happy to spend money on the activities and hobbies they enjoy, and CSS companies are able to make pleasing those consumers their top priority.

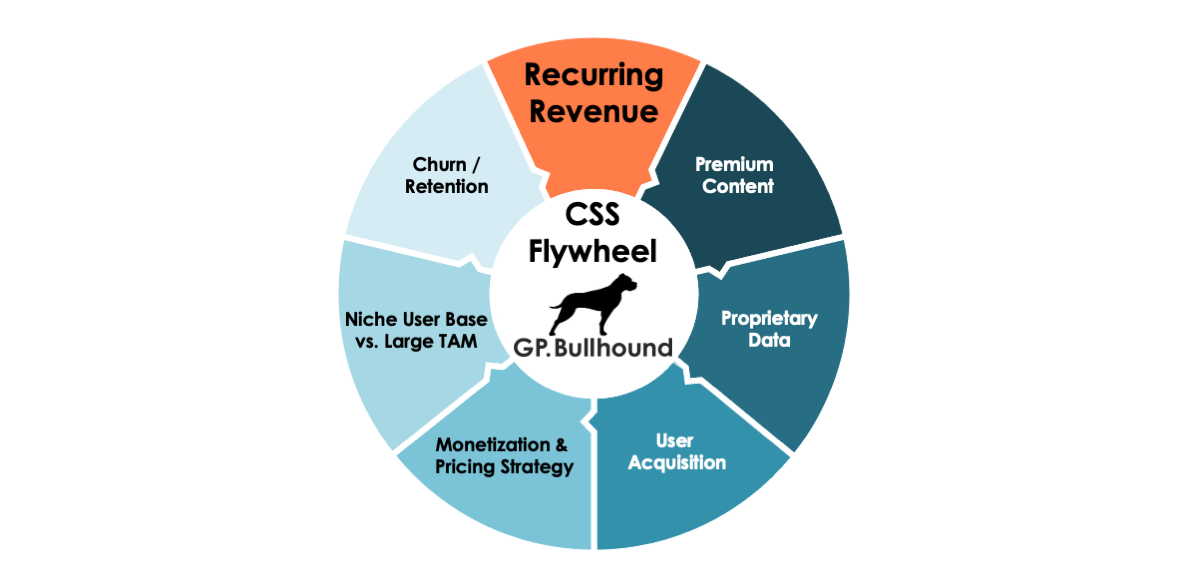

The result is what I call the CSS flywheel, in which a quality CSS product attracts and retains loyal users. Those users contribute their data through posts, photos and reviews, which creates a better product that further attracts new users, and so on.

The CSS flywheel shows the cycle that results when a quality CSS product attracts and retains loyal users. Image Credits: GP Bullhound

When companies get this flywheel right, it’s incredibly appealing to investors, because of the advantages of scale in CSS. Each niche will probably be dominated by one or two players, and a given niche can have tens of millions of consumers.

Powered by WPeMatico

Telemedicine, in its original form of the phone call, has been around for decades. For people in remote or rural areas without easy access to in-person care, consulting a doctor over the phone has often been the go-to approach. But for a large swath of the world used to taking half a day off work just for a 15-30 minute doctor’s appointment, it may seem like telemedicine was invented only last year. That’s mostly because it wasn’t until 2020 that telemedicine, in its myriad forms, debuted into the mainstream consciousness.

It’s impossible to predict how healthcare institutions will operate post-pandemic, but with so many people now accustomed to telemedicine, startups that provide services around virtual care continue to be poised for success.

Telemedicine has faced an uphill battle to become more relevant in the U.S., with challenges such as meeting HIPPA compliance requirements and insurance companies unwilling to pay for virtual visits. But when COVID-19 began raging across the globe and people had to stay home, both the insurance and healthcare industries were forced to adapt.

“It’s been said that there are decades where nothing happens, and then there are weeks when decades happen,” said StartUp Health co-founders Steven Krein and Unity Stoakes in the company’s 2020 year-end report. That statement couldn’t be truer for telemedicine: Around $3.1 billion in funding flowed into the sector in 2020 — about three times what we saw in 2019, according to the report. A health tech fund and insights company, StartUp Health counts Alphabet, Sequoia and Andreessen Horowitz as some of its co-investors.

Now that people see the benefits and conveniences of “dialing a doc” from the kitchen table, healthcare has changed forever. It’s impossible to predict how healthcare institutions will operate post-pandemic, but with so many people now accustomed to telemedicine, startups that provide services around virtual care continue to be poised for success.

Major players in the field now look at the state of healthcare as, “before COVID and after COVID,” Stoakes told Extra Crunch. “In the post-pandemic world, there’s a significant transformation that’s occurred,” he said. “It’s all accelerated; the customers have shown up. There’s more capital than ever and consumers and physicians have adapted quickly,” he added.

In the U.S., healthcare is first and foremost a business, so while there are treatment approaches that have long been proven to improve patient outcomes, if they didn’t make sense financially, they weren’t instituted at scale. Telemedicine is a great example of this.

A 2017 study by the American Journal of Accountable Care showed that telemedicine can be quite useful for managing healthcare. “The use of telemedicine has been shown to allow for better long-term care management and patient satisfaction; it also offers a new means to locate health information and communicate with practitioners (e.g., via e-mail and interactive chats or video conferences), thereby increasing convenience for the patient and reducing the amount of potential travel required for both physician and patient,” the study reads.

But as we’ve seen, it took a global healthcare emergency to drive widespread adoption of virtual healthcare in the U.S. Now that investors recognize the potential, they are increasingly pouring money into startups that promise to take telemedicine to the next level. Some of the investors backing these newer companies include StartUp Health, Andreessen Horowitz, Sequoia, Alphabet, Kaiser Permanente Ventures, U.S. Venture Partners, Maveron, First Round Capital, DreamIt Ventures, Human Ventures and Tusk Venture Partners.

Powered by WPeMatico

In the early 2000s, Jeff Bezos gave a seminal TED Talk titled “The Electricity Metaphor for the Web’s Future.” In it, he argued that the internet will enable innovation on the same scale that electricity did.

We are at a similar inflection point in healthcare, with the recent movement toward data transparency birthing a new generation of innovation and startups.

Those who follow the space closely may have noticed that there are twin struggles taking place: a push for more transparency on provider and payer data, including anonymous patient data, and another for strict privacy protection for personal patient data. What’s the main difference?

This sector is still somewhat nascent — we are in the first wave of innovation, with much more to come.

Anonymized data is much more freely available, while personal data is being locked even tighter (as it should be) due to regulations like GDPR, CCPA and their equivalents around the world.

The former trend is enabling a host of new vendors and services that will ultimately make healthcare better and more transparent for all of us.

These new companies could not have existed five years ago. The Affordable Care Act was the first step toward making anonymized data more available. It required healthcare institutions (such as hospitals and healthcare systems) to publish data on costs and outcomes. This included the release of detailed data on providers.

Later legislation required biotech and pharma companies to disclose monies paid to research partners. And every physician in the U.S. is now required to be in the National Practitioner Identifier (NPI), a comprehensive public database of providers.

All of this allowed the creation of new types of companies that give both patients and providers more control over their data. Here are some key examples of how.

This is a key capability of patients’ newly found access to health data. Think of how often, as a patient, providers aren’t aware of treatment or a test you’ve had elsewhere. Often you end up repeating a test because a provider doesn’t have a record of a test conducted elsewhere.

Powered by WPeMatico

After years of sustained growth, the pandemic supercharged the outdoor recreation industry. Startups that provide services like camper vans, private campsites and trail-finding apps became relevant to millions of new users when COVID-19 shut down indoor recreation, building on an existing boom in outdoor recreation.

Startups like Outdoorsy, AllTrails, Cabana, Hipcamp, Kibbo and Lowergear Outdoors have seen significant growth, but to keep it going, consumers who discovered a fondness for the great outdoors during the pandemic must turn it into a lifelong interest.

Outdoorsy, AllTrails, Cabana, Hipcamp, Kibbo and Lowergear Outdoors have seen significant growth, but to keep it going, consumers who discovered a fondness for the great outdoors during the pandemic must turn it into a lifelong interest.

Social media, increased environmentalism and high urbanization were already fueling a boom in popularity. There was a 72% increase in people who camp more than three times a year between 2014 and 2019, mostly spurred by young millennials, young families with kids and nonwhite participants.

But 2020 was a different animal: After months of shelter-in-place orders, widespread shutdowns and physical distancing, outdoors became the only location for safe socializing. In South Dakota, the Lewis and Clark Recreation Area saw a 59% increase in visitors from 2019 to 2020. In the pandemic year, consumers spent $887 billion on outdoor recreation according to the Outdoor Industry Association, more than pharmaceuticals and fuel combined.

And it’s going to continue to grow. Hiking equipment alone is supposed to reach a $7.4 billion market size by 2027, a 6.3% compound annual growth rate. Camping and caravanning is having an even more drastic moment. Without international travel, vacations shifted from flights to exotic resorts to domestic road trips, self-contained rentals and camping. In 2020, the market for camping and caravanning was almost $40 billion and is predicted to rise 13% to just over $45 billion this year.

After the initial and extreme drop-off in engagement early as national parks closed, private camping sites shut down and domestic travel ceased, many outdoor startups have had a breakout year. Outdoorsy, the peer-to-peer camper van rental marketplace, said it saw 44% of all bookings in the company’s history in 2020.

Campsite booking platform Hipcamp said it sent three times as much money to landowners in 2020 as compared to 2019. And it’s not just experienced outdoor veterans taking advantage of the work-from-home lifestyle: in 2020, Cabana, a camper van rental startup, said 70% of its customers had never rented a camper van or an RV before and another 26% had only done it once.

But a report commissioned by the Outdoor Industry Association showed that the most popular outdoor activities were ones that people could do close to home, not the traveling kind Hipcamp, Cabana and Outdoorsy traffic in. The three most popular outdoor activities for newbies: walking, running and bicycling.

But the pandemic did create a small boost for camping, climbing, backpacking and kayaking; fueled by an increase in women, younger, more ethnically diverse, urban and slightly less wealthy people pushing into the outdoors. This class of outdoor startups will need to engage the new demographic shift to capitalize on the pandemic’s outdoor boom because, according to the report, a quarter of those who started new outdoor activities during the pandemic don’t plan on continuing once it’s over.

But getting into the outdoors can be overwhelming: there’s gear to buy, skills to learn, exploring unfamiliar areas and the added stressor of safety. Outdoor startups are working to lower the barrier to entry to help grow their businesses.

“I think anytime you have like 2,000 articles with two dozen tips on how to use a product, that tells me that it is really, really too hard to use,” said Cabana founder Scott Kubly. “To me, that says there’s nothing but friction in this process. If you want to build something that’s mainstream, you need to make it super consistent and really easy to use.”

Kubly said only half a percent of the U.S. population takes a rental van or RV trip each year. Planning an outdoor adventure can be time-consuming — choosing a location, finding an open campsite, planning meals and water, and figuring out dump stations for trash or septic. That planning is multiplied tenfold if you are going for a road trip or backpacking and need to find new places every other night.

Powered by WPeMatico

More than half a decade ago, my Battery Ventures partner Neeraj Agrawal penned a widely read post offering advice for enterprise-software companies hoping to reach $100 million in annual recurring revenue.

His playbook, dubbed “T2D3” — for “triple, triple, double, double, double,” referring to the stages at which a software company’s revenue should multiply — helped many high-growth startups index their growth. It also highlighted the broader explosion in industry value creation stemming from the transition of on-premise software to the cloud.

Fast forward to today, and many of T2D3’s insights are still relevant. But now it’s time to update T2D3 to account for some of the tectonic changes shaping a broader universe of B2B tech — and pushing companies to grow at rates we’ve never seen before.

One of the biggest factors driving billion-dollar B2Bs is a simple but important shift in how organizations buy enterprise technology today.

I call this new paradigm “billion-dollar B2B.” It refers to the forces shaping a new class of cloud-first, enterprise-tech behemoths with the potential to reach $1 billion in ARR — and achieve market capitalizations in excess of $50 billion or even $100 billion.

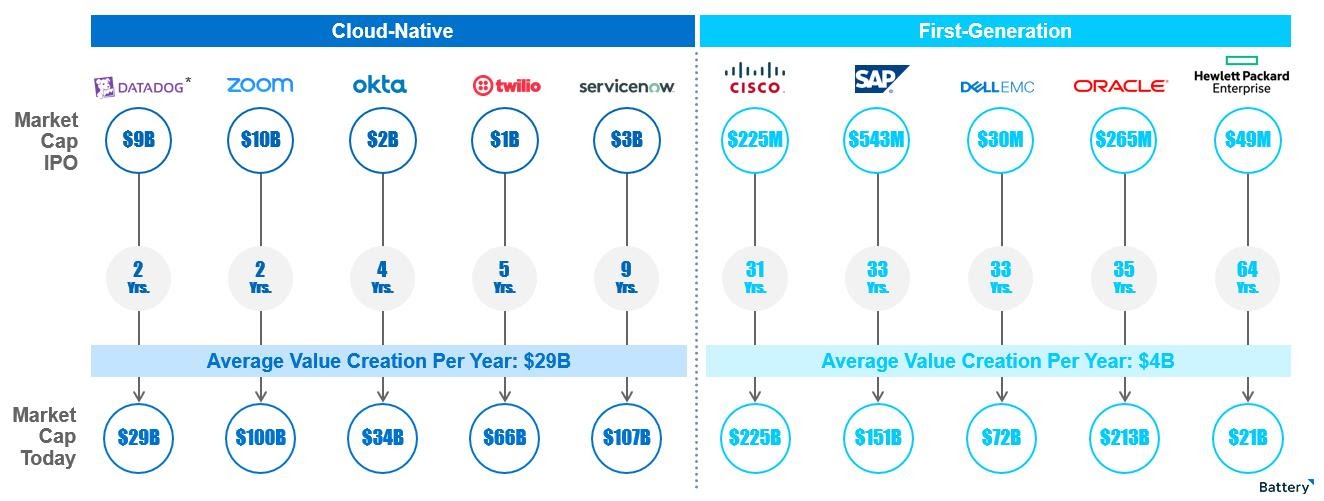

In the past several years, we’ve seen a pioneering group of B2B standouts — Twilio, Shopify, Atlassian, Okta, Coupa*, MongoDB and Zscaler, for example — approach or exceed the $1 billion revenue mark and see their market capitalizations surge 10 times or more from their IPOs to the present day (as of March 31), according to CapIQ data.

More recently, iconic companies like data giant Snowflake and video-conferencing mainstay Zoom came out of the IPO gate at even higher valuations. Zoom, with 2020 revenue of just under $883 million, is now worth close to $100 billion, per CapIQ data.

Image Credits: Battery Ventures via FactSet. Note that market data is current as of April 3, 2021.

In the wings are other B2B super-unicorns like Databricks* and UiPath, which have each raised private financing rounds at valuations of more than $20 billion, per public reports, which is unprecedented in the software industry.

Powered by WPeMatico

In 2019, St. Louis Metro Transit was struggling to keep customers. Uber and Lyft, along with dockless shared bikes and scooters, had flooded streets, causing ridership to fall more than 7% in a single year.

The agency didn’t try to fight for attention. Instead, it embraced its competitors.

Metro Transit dropped its internal trip-planning app, which had been developed with the Trapeze Group and directed riders to Transit, a private third-party app that offers mapping and real-time transit data in more than 200 cities. That app also included micromobility and ride-hailing information, allowing customers to not just look up bus schedules, but see how they might get to and from stops — or ignore the bus altogether.

The following year, Metro Transit partnered with mobile ticketing company Masabi and added a payment option on some bus routes. Now, the agency is planning an all-in-one app — via third-party providers Transit and Masabi — where customers could plan and book end-to-end trips across trains, buses, bikes, scooters and taxis.

“What we do best is transporting large volumes of people on vehicles and managing mass transit,” said Metro Transit executive director Jessica Mefford-Miller. “On the software side, there are a lot of players out there doing great stuff that can help us meet our customers where they are and make trip planning as easy as possible.”

St. Louis Metro Transit isn’t an outlier. As transit agencies seek to win back riders, a flurry of platforms — some backed by giants like Uber, Intel and BMW — are offering new technology partnerships. Whether it’s bundling bookings, payments or just trip planning, startups are selling these mobility-as-a-service (MaaS) offerings as a lifeline to make transit agencies the backbone of urban mobility.

Whether it’s bundling bookings, payments or just trip planning, startups are selling mobility-as-a-service (MaaS) offerings as a lifeline to make transit agencies the backbone of urban mobility.

Third-party platforms have become more appealing to transit agencies as they scramble to keep buses, trains and rail full of customers. According to the American Public Transportation Association (APTA), ridership and total miles traveled has declined since 2014, including a 2.5% drop from 2017 to 2018. The COVID-19 pandemic could accelerate this trend as more people continue working from home or shy away from crowding into buses and trains.

“This is like Expedia, the idea of seeing multiple airlines in one place to comparison shop,” said Regina Clewlow, CEO of transportation management firm Populus. “A lot of operators are looking at the question of whether that would give them more rides.”

But that the private growth could come at a cost, potentially injecting private concerns into what should be a public good, Metro Transit’s Mefford-Miller cautioned.

“If we let the market handle this planning on its own, a company might only do it for someone with a digital device or a bank account or only help people who don’t need special accommodation,” Mefford-Miller said. “That’s why we have as an underpinning an equitable and accessible system. It’s the underpinning before we choose any tools we use.”

Amid the swarm of new startups there are a few giants. One of the biggest established players is Cubic Corp., a San Diego-based defense and public transportation company. The firm already controls payments and back-end software for hundreds of transit agencies, including in Chicago, New York and San Francisco, and in January launched a suite of new products under the brand name Umo to expand their offerings.

The package includes a customer-facing multimodal app, a fare collection platform, a contactless payment system, a rewards program, a behind-the-scenes management platform and a MaaS marketplace for public and private offerings. Mick Spiers, general manager of Umo, said the goal is to offer a “connected, integrated journey.”

“We’re uniquely placed as an independent, trusted third party that can be the data broker for a journey focused around the needs of the user,” Spiers added. “The journey we create has no commercial interest for us.”

Powered by WPeMatico

Jim Jackson developed timber and farmland in Eastern Washington, protected from coastal rains by the peaks of the Cascade mountains, building out a clutch of apple farms and other properties on the state’s sunny side for 40 years.

Traditionally, he raised money to expand operations for his farms through his existing network, which meant asking previous investors to pool together and come up with the cash.

But more recently, Jackson turned to a fundraising platform that operates entirely online. Like hundreds of other farmers, he’s using a service called AcreTrader to raise money for agricultural development projects. AcreTrader is one of a growing number of companies revolutionizing the way farm and forestland are acquired, developed and commercialized across the United States.

There’s lots of farmland in the U.S. Bill Gates, Microsoft founder and the world’s third-richest man, is the nation’s largest owner of farmland, holding roughly 242,000 acres. That number seems high until you compare it with the 897.4 million acres of land that are currently arable and used for farming in the U.S.

Another 823 million acres of forests dot the United States, the majority of which are privately owned.

Taken together, that’s a massive amount of real estate with economic potential that’s traditionally been accessible only to the ultrawealthy to acquire and finance for development. Now, startups like AcreTrader and others including Tillable, ($8.3 million) FarmTogether ($3.7 million), and Harvest Returns are bringing marketplace models to the farming world — potentially bringing hundreds of thousands of investable acres to financiers looking to diversify.

Powered by WPeMatico

At Battery, a central part of our consumer investing practice involves tracking the evolution of where and how consumers find and purchase goods and services. From our annual Battery Marketplace Index, we’ve seen seismic shifts in how consumer purchasing behavior has changed over the years, starting with the move to the web and, more recently, to mobile and on-demand via smartphones.

The evolution looks like this in a nutshell: In the early days, listing sites like Craigslist, Angie’s List* and Yelp effectively put the Yellow Pages online — you could find a new restaurant or plumber on the web, but the process of contacting them was largely still offline. As consumers grew more comfortable with the web, marketplaces like eBay, Etsy, Expedia and Wayfair* emerged, enabling historically offline transactions to occur online.

More recently, and spurred in large part by mobile, on-demand use cases, managed marketplaces like Uber, DoorDash, Instacart and StockX* have taken online consumer purchasing a step further. They play a greater role in the operations of the marketplace, from automatically matching demand with supply, to verifying the supply side for quality, to dynamic pricing.

The key purpose of being end-to-end is to deliver an even better value proposition to consumers relative to incumbent alternatives.

Each stage of this evolution unlocked billions of dollars in value, and many of the names listed above remain the largest consumer internet companies today.

At their core, these companies are facilitators, matching consumer demand with existing supply of a product or service. While there is no doubt these companies play a hugely valuable role in our lives, we increasingly believe that simply facilitating a transaction or service isn’t enough. Particularly in industries where supply is scarce, or in old-guard industries where innovation in the underlying product or service is slow, a digitized marketplace — even when managed — can produce underwhelming experiences for consumers.

In these instances, starting from the ground up is what is really required to deliver an optimal consumer experience. Back in 2014, Chris Dixon wrote a bit about this phenomenon in his post on “Full stack startups.” Fast forward several years, and more startups than ever are “full stack” or as we call it, “end-to-end operators.”

These businesses are fundamentally reimagining their product experience by owning the entire value chain, from end to end, thereby creating a step-functionally better experience for consumers. Owning more in the stack of operations gives these companies better control over quality, customer service, delivery, pricing and more — which gives consumers a better, faster and cheaper experience.

It’s worth noting that these end-to-end models typically require more capital to reach scale, as greater upfront investment is necessary to get them off the ground than other, more narrowly focused marketplaces. But in our experience, the additional capital required is often outweighed by the value captured from owning the entire experience.

Many of these businesses have reached meaningful scale across industries:

Image Credits: Battery Ventures (opens in a new window)

All of these companies have recognized they can deliver more value to consumers by “owning” every aspect of the underlying product or service — from the bike to the workout content in Peloton’s case, or the bank account to the credit card in Chime’s case. They have reinvented and reimagined the entire consumer experience, from end to end.

As investors, we’ve had the privilege of meeting with many of these next-generation end-to-end operators over the years and found that those with the greatest success tend to exhibit the five key elements below:

The end-to-end approach makes the most sense when disrupting very large markets. In the graphic above, notice that most of these companies play in the largest, but notoriously archaic industries like banking, insurance, real estate, healthcare, etc. Incumbents in these industries are very large and entrenched, but they are legacy players, making them slow to adopt new technology. For the most part, they have failed to meet the needs of our digital-native, mobile-savvy generation and their experiences lag behind consumer expectations of today (evidenced by low, or sometimes even negative, NPS scores). Rebuilding the experience from the ground up is sometimes the only way to satisfy today’s consumers in these massive markets.

Powered by WPeMatico