EC Food Climate and Sustainability

Auto Added by WPeMatico

Auto Added by WPeMatico

We have been raised to believe in recycling, but it has mostly been a sham — only 9% of all plastic waste produced in 2018 was recycled. The beauty industry produces over 120 billion units of packaging every year, little of which is recycled. Globally, an estimated 92 million tons of textile waste ends up in landfills.

Reducing waste is key to meeting environmental milestones, and some retail firms have narrowed in on a unique approach to minimize what their customers throw away: personalization. Accurate personalization can guide consumers to the right products, reducing waste while increasing conversion and loyalty.

Reducing waste is key to meeting environmental milestones, and some retail firms have narrowed in on a unique approach to minimize what their customers throw away: personalization.

For big brands and retailers, personalization is expected to be the top category for tech investment this year. Moreover, personalization holds high appeal, with 80% of survey respondents indicating they are more likely to do business with a company if it offers personalized experiences and 90% indicating that they find personalization appealing, according to a survey by Epsilon.

Startups that deliver sustainable personalization solutions that also improve business for retailers and brands fall into three categories:

Faces are easy to map, since it’s not difficult to virtually place a lipstick color on a face, but using AR and AI to recommend skin-tone-matching makeup products has been challenging for many AR virtual try-on companies. “I’ve been searching for an intuitive foundation-shade-finder tool since launching Cult Beauty in 2008, and nothing has lived up to the experience of having a professional match you in daylight until I discovered MIME,” says Alexia Inge, founder of Cult Beauty. “There are so many variables like light, skin tones, prevalent undertones, device, screen, OS, formula density, formula oxidation, as well as preferences for coverage levels, finish, brand and skin type,” she says.

MIME founder and CEO Christopher Merkle said, “Virtual try-on has exploded in the past few years, but for color cosmetics, the technology doesn’t help solve the primary customer pain point: shade matching. From day one, I decided to focus our company’s R&D efforts exclusively on color accuracy. I want to make sure that when the consumer receives their foundation or concealer in the mail, it’s the perfect shade once applied to their skin.”

MIME’s Shade Finder AI allows consumers to take a photo of themselves, answer a few questions, then get matched with a makeup color that pairs with their skin tone. MIME helps retailers and brands increase their online and in-store purchase conversion by up to five times. More than 22% of beauty returns are due to poor customer color purchases, but Merkle says MIME can get returns as low as 0.1%.

Powered by WPeMatico

China’s e-commerce and industrial ecosystem is as different from the Western world as its culture. The country took decades to earn its reputation as the Factory of the World, but it now boasts a supply chain and manufacturing ability that few countries can match.

Creative use of the country’s networked manufacturing and logistics hubs make mass production both cheap and easy. Clothing, electronics, toys, automobiles, musical instruments, furniture — you name it and you’ll find a manufacturer in China who can turn your intangible concept into mass-manufacturable reality in mere days. And they’ll do it for cheaper than anywhere else in the world.

It was just a matter of time until an intrepid Chinese entrepreneur with a tech background decided to take on Coca-Cola and PepsiCo.

China is also home to one of the world’s largest e-commerce and tech ecosystems. Hundreds of startups dot the landscape, and the amount of money being raised and spent on innovating around the country’s industrial heft is mind-boggling.

So it was just a matter of time until an intrepid Chinese entrepreneur with a tech background decided to take on Coca-Cola and PepsiCo. The tech revolution hasn’t yet affected the bottled beverage industry quite as much as it has others. Incumbent giants therefore could lose a sizable chunk of market share if a company could just manage to weave together China’s manufacturing proficiency and agility with the modern tech startup philosophy of “moving fast and breaking stuff.”

Genki Forest, a Chinese direct-to-consumer (D2C) bottled beverage startup, is one such contender. A philosophy centered around iteration informed by data, quick turnarounds and a laser focus on taking advantage of China’s huge e-commerce ecosystem has helped this company’s revenues rise rapidly since it started five years ago. Its sugar-free sodas, milk teas and energy drinks sell in 40 countries and generated revenue of about $450 million in 2020. The company aims to reach $1.2 billion this year.

If anything, Genki Forest’s valuation has shot up even faster. It recently completed its fourth VC round that values it at a whopping $6 billion, triple the price it fetched a year earlier, and it has so far raised at least half a billion dollars.

It’s striking how closely Genki Forest’s operations resemble that of a tech startup. So we thought we should take a closer look and see what this company’s graph can tell us about the new wave of Chinese D2C entrepreneurship looking to take over the globe.

The bottled beverage industry wasn’t what Genki Forest’s founder, Binsen Tang, initially set out to tackle. His first startup was a successful casual, mostly mobile gaming outfit known as ELEX Technology. It was nowhere near record-breaking, though — some 50 million users logged on to a few popular games in over 40 countries worldwide, including one of the first versions of Happy Farm, a predecessor to Zynga’s Farmville. But Tang wasn’t satisfied and eventually sold ELEX Technology to a publicly listed company for about $400 million in 2014.

Tang would walk away with a few important lessons. He’d learned by now that Chinese products were already competitive globally, whether people realized it or not, and that and geographic arbitrage was real, Happy Farm being the perfect example of this. Lastly, he now knew that it was far more important to choose the right “racetrack” (as Chinese investors and entrepreneurs like to put it) than to have a great product.

Picking the right race to win was perhaps the most important takeaway. It’s also an idea that sets Chinese entrepreneurs apart from their Western counterparts — the most worthwhile endeavors are in identifying the largest and most rewarding market at hand, regardless of one’s previous expertise. It was what led Zhang Yiming to create ByteDance, and Lei Jun to found Xiaomi.

That very philosophy led Tang to build Genki Forest. After selling ELEX Technology, Tang didn’t go back to the business that netted him his first pot of gold. As much as he had benefited from the rise of the mobile internet, he thought there was a far bigger opportunity building a consumer brand and applying the lessons he learned from programming to the manufacture of tangible products.

He soon set up his own investment fund, Challenjers Capital, convinced that the next big tech opportunity in China was in tech’s application to everyday consumer products. He soon began to invest in everything from ramen and hotpots to bottled beverages.

China’s quickly expanding e-commerce ecosystem and the plethora of D2C businesses flourishing on Alibaba and JD.com would also influence his decision to sell directly to his target audience rather than take the traditional route. But to truly understand his motivations, we need to take a look at the extremely unique D2C environment in China and how it has changed over the years.

“China doesn’t need any more good platforms,” Tang told his team in an internal email in 2015, “but it does need good products.” Tang was talking about how the age of building infrastructure for e-commerce in China was largely over; it was now time to create brands that could take advantage of the advanced distribution network that had been laid out.

Other investors noticed as well. Albus Yu, principal at China Growth Capital, told me that his fund had stopped making investments in independent consumer-facing platforms or marketplaces for a while. “2014 might have been the last year it was economically feasible to start such a business due to the soaring cost of acquiring customers and the strength of incumbents,” he said.

Indeed, 2015 was the year when CACs began to exceed or at least rival ARPUs for Alibaba and JD.com.

In China, that distribution network was present across the digital and physical worlds. Online, there was immense market power concentrated in the hands of just two players: Alibaba and JD.com, which used to have, and still maintain, 80% or above in market share.

In fact, the dominance of Alibaba, in particular, was so overwhelming that for years, VCs invested not in D2C, but in “Taobao brands,” since that was the only channel one needed to conquer in order to make it.

Customer acquisition was therefore straightforward — throw everything into advertising on Alibaba’s Tmall platform, especially during its annual flagship shopping festival, Singles’ Day. Even today, garnering a top spot in one of the category leaderboards remains a surefire way to build brand awareness, investor interest, as well as sales records.

Physically, the Chinese market also differs greatly from much of the developed West. Years of heavy investment in logistics by the private sector, accelerated by government support and infrastructure buildout, means that delivery costs have come down significantly over the years, even dipping below $0.40 per package wholesale as of this year. Innovations such as return insurance have also sped up customer adoption.

By 2016, China was shipping 30 billion packages a year, already accounting for 44% of global shipments. That number has been doubling every three years and is expected to exceed 100 billion this year. And the low cost of delivery is one of the biggest reasons for China’s outsized e-commerce market — the largest globally and estimated to reach $2.8 trillion in 2021, more than triple that of the No. 2, the U.S.

Express parcels sit stacked at a logistic base of e-commerce giant Suning before the 618 Shopping Festival. Image Credits: VCG

Present-day China also presents another edge: Proximity to an advanced, flexible manufacturing network and supply chain for the vast majority of consumer products, and the ability to outsource almost everything to them.

The original equipment manufacturers of years past have long since evolved into original design manufacturers. An expected consequence of being “the Factory of the World” for so many years, making goods for some of the best brands in the world, is that some of the knowledge was bound to transfer.

It may be difficult for outsiders to understand just how strong China’s networked manufacturing hubs are these days. What used to take weeks now takes mere days, the lead times shortened drastically by software, robots and other advancements. For example, Chinese cross-border ultra-fast-fashion company Shein has compressed design-to-ship timelines to as little as seven days.

And it’s definitely not just for making crop tops. The turnaround can be astonishingly fast even when manufacturing completely unfamiliar goods, such as when electric vehicle maker BYD turned its factory into the world’s largest face mask plant in just two weeks when the COVID-19 pandemic struck last year.

Companies leverage this manufacturing flexibility and agility for more than just speed. Chinese cosmetics upstart Perfect Diary uses it to launch twice as many SKUs as foreign competitors. In addition, the quick turnaround allows agile brands to take advantage of that most ephemeral of IP, memes.

It’s not to say that the Chinese supply chain is inaccessible to foreign entrepreneurs. Best-selling mattress maker Zinus, for example, is founded by a South Korean, but its products are manufactured in China and sold mostly on Amazon to U.S. customers.

It’s just that very few non-Chinese companies have figured out how to tap as deeply into the supply chain as this new crop of Chinese D2C brands, which can require years of working not just alongside but physically inside the factories, building trust and know-how. Shein, for example, watches carefully what other brands are making by staying close to the factories.

Before global sensations such as TikTok weakened the mantra, “copy to China” used to be a dominant characterization of Chinese startups. In December 2015, when Tang registered the Genki Forest trademark, that was still very much a relevant strategy.

Powered by WPeMatico

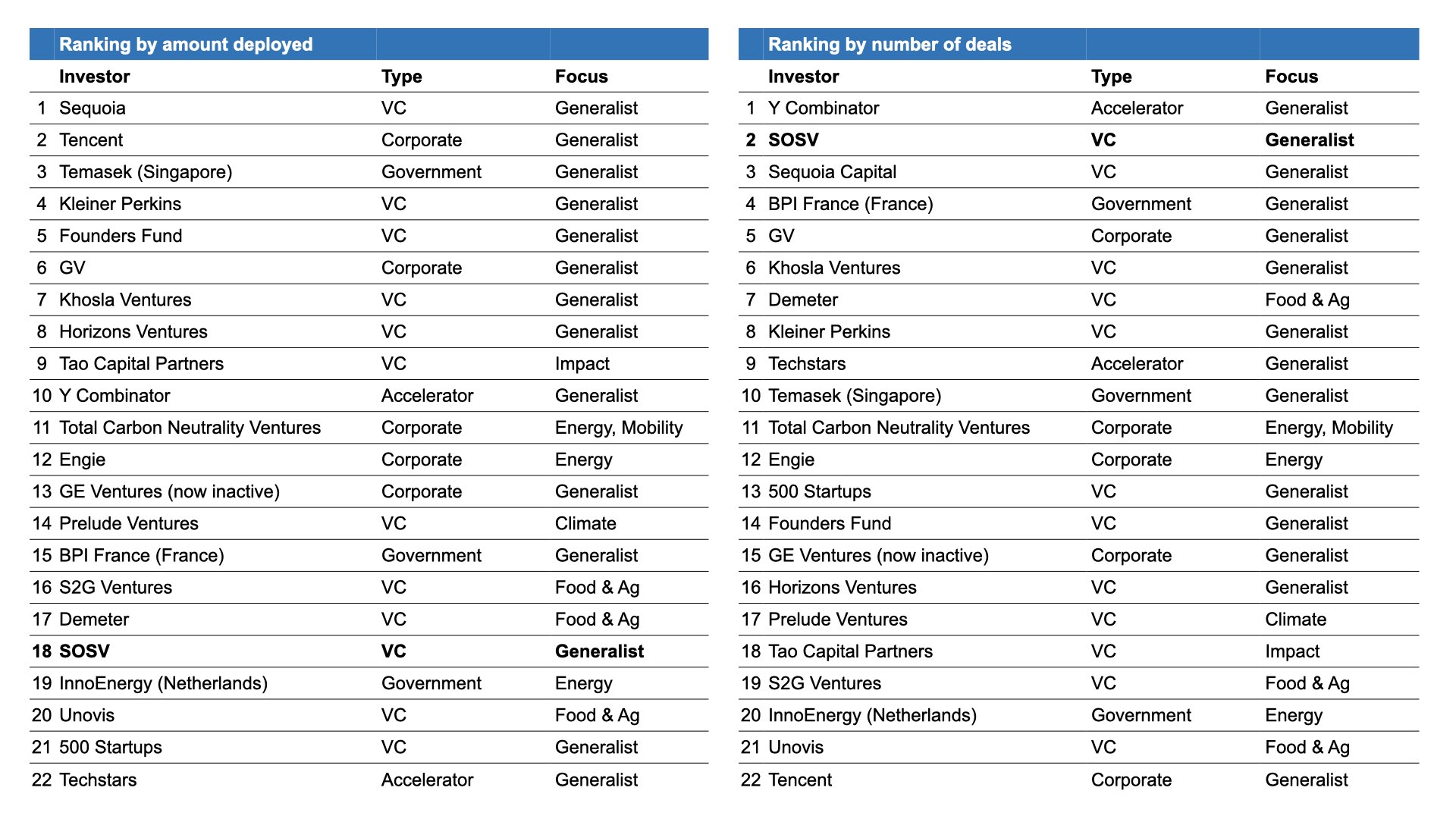

On Earth Day, April 22, SOSV published the SOSV Climate Tech 100, a list of the best startups that we’ve supported from their earliest stages to address climate change. There are always valuable insights embedded in a list like the 100. A TechCrunch story captured the investment perspective, and an SOSV post went deeper into the companies’ category breakdown and founder profiles.

But what can founders learn from the list about climate tech investors? In other words, who invested in the Climate Tech 100? We dug into the “who’s who” of the list, which had more than 500 investors, and here’s what we found.

If you think 500 investors in 100 companies is a lot of investors, you’re right. There are clearly a lot of investors interested in climate tech, and most are generalists just testing the waters. For the Climate Tech 100, about 10% of investors put their money in more than one startup and only seven (less than 2%) wrote a check to four or more. These included Blue Horizon, CPT Capital, EF, Fifty Years, Hemisphere Ventures and Horizons Ventures.

That pattern tracks well with data from PwC, which found that 2,700 unique investors had backed 1,200 startups in its State of Climate Tech 2020 report covering the 2013-2019 period. The report found that only 10 firms out of 2,700 made four or more climate tech deals per year, on average, over the 2013-2019 period. The most active firms are listed in the table below.

Image Credits: PwC, 2020; additional research by SOSV

Capital deployed in climate tech grew at five times the venture capital overall growth rate over the 2013-2019 period.

There is reason to believe that the fragmentation will diminish with the launch of more funds focused on climate tech. Four funds worth more than a billion dollars each have launched since 2020 that fit the description (see chart below).

It’s also encouraging to see that capital deployed in climate tech grew at five times the venture capital overall growth rate over the 2013-2019 period.

Even so, climate tech still only represented 6% of total venture capital deployed in 2019, so there is plenty of room to grow.

Powered by WPeMatico

Almost two centuries ago, gold prospectors in California set off one of the greatest rushes for wealth in history. Proponents of socially conscious investing claim fund managers will start a similar stampede when they discover that environmental, social and governance (ESG) insights can yield treasure in the form of alternative data that promise big payoffs — if only they knew how to mine it.

First, let’s be clear: ESG is not on the fringe.

There may be some truth to that line of thinking if you take some of the rhetoric and advertising out of the equation.

First, let’s be clear: ESG is not on the fringe. The European Union has implemented new financial regulations via the Sustainable Finance Disclosure Regulation (SFDR). These improve ESG disclosures and considerations and help to direct capital toward products and companies that benefit people and the planet. As we write, the U.S. Securities and Exchange Commission is also considering drafting and implementation of ESG-related regulations.

Whether enacted or currently under consideration, these rules encourage fund managers to integrate sustainability risks into their business processes, report on them publicly, stamp out greenwashing, and promote transparency and knowledge among investors. Accordingly, it will become easier to compare firms’ sustainability efforts, too, allowing stakeholders from all corners to make more informed decisions.

Incorporating ESG factors into investment strategies is not new, of course. The world’s largest asset managers have been practicing it for years. According to the Governance & Accountability Institute, 90% of companies listed on the S&P 500 now produce sustainability reports, an increase of 70 percentage points from more than a decade ago.

Yet some are still groaning about adopting an ESG investing mindset; they see ESG as a nuisance that detracts from their mission of earning high returns. But could this mindset mean they are missing important opportunities?

Waiting for new mandatory ESG reporting and compliance framework standards in the U.S. puts Americas-focused managers at a significant disadvantage. Fund managers can start gaining insights today from alternative data originating in ESG-related data stemming from climate change, natural disasters, harassment and discrimination lawsuits, and other events and information that can be mined.

Powered by WPeMatico

On a recent morning in downtown Shenzhen, Lingyu queued up to order her go-to McMuffin. As she waited in line with other commuters, the 50-year-old accountant noticed the new vegetarian options on the menu and decided to try the imitation spam and scrambled egg burger.

“I’ve never had fake meat,” she said of the burger — one of five new breakfast items that McDonald’s introduced last week in three major Chinese cities featuring luncheon meat substitutes produced by Green Monday.

Although some investors worry the sudden boom of meat-substitute startups could turn into a bubble, others believe the market is far from saturated.

Lingyu, who works in her family business in Shenzhen, is exactly the type of Chinese customer that imitation meat companies want to attract beyond the young, trendy, eco-conscious urbanites. Her yuan means potentially more to meat replacement companies because it advances their business and climate agendas both. Eating less meat is one of the simplest ways to reduce an individual’s carbon footprint and help fight climate change.

McDonald’s hopes that its pea- and soy-based, zero-cholesterol, luncheon meat substitutes will carve out a piece of China’s massive dining market. Longtime rival KFC, and local competitor Dicos introduced their own plant-based products last year. Partnering with fast food chains is a smart move for companies that want to promote alternative protein to the masses, because these products are often pricey and are usually aimed at wealthy urbanites.

2020 could well have been the dawn of alternative protein in China. More than 10 startups raised capital to make plant-based protein for a country with increasing meat demand. Of these, Starfield, Hey Maet, Vesta and Haofood have been around for about a year; ZhenMeat was founded three years ago; and the aforementioned Green Monday is a nine-year-old Hong Kong firm pushing into mainland China. The competition intensified further last year when American incumbents Beyond Meat and Eat Just entered China.

Although some investors worry the sudden boom of meat-substitute startups could turn into a bubble, others believe the market is far from saturated.

“Think about how much meat China consumes a year,” said an investor in a Chinese soy protein startup who requested anonymity. “Even if alternative protein replaces 0.01% of the consumption, it could be a market worth tens of billions of dollars.”

In many ways, China is the ideal testbed for alternative protein. The country has a long history of imitation meat rooted in Buddhist vegetarianism and an expanding middle class that is increasingly health-conscious and willing to experiment. The country also has a grip on the global supply chain for plant-based protein, which could give domestic startups an edge over foreign rivals.

“I believe, in five years, China will see a raft of domestic plant-based protein companies that could be on par with industry leaders from Europe and North America,” said Xie Zihan, who founded Vesta to develop soy-based meat suitable for Chinese cuisine.

Hey Maet’s imitation meat dumplings. Image Credits: Hey Maet

Lily Chen, a manager at the Chinese arm of alternative protein investor Lever VC, outlines three categories of meat analog companies in China: Western giants such as Beyond Meat and Eat Just; local players; and conglomerates such as Unilever and Nestlé that are developing vegan meat product lines as a defense strategy. Lever VC invested in Beyond Meat, Impossible Foods and Memphis Meats.

“They all have their product differentiation, but the industry is still very early stage,” said Chen.

Powered by WPeMatico

Cities traditionally have been bustling hubs where people live, work and play. When the pandemic hit, some people fled major metropolitan markets for smaller towns — raising questions about the future validity of cities. It’s true that we’re still months away from broader reopenings and herd immunity via current vaccination efforts.

However, those who predicted that COVID-19 would destroy major urban communities might want to stop shorting the resilience of these municipalities and start going long on what the post-pandemic future looks like.

Those who predicted that COVID-19 would destroy major urban communities might want to stop shorting the resilience of these municipalities and start going long on what the post-pandemic future looks like.

U.N. forecasts show that by 2030, two-thirds of the world’s population will reside in cities, communities that are the epicenters of culture, innovation, wealth, education and tourism, to mention just a few benefits. They are not only worth saving — they’re also ripe for rebirth, precisely why many municipal leaders in the U.S. anticipate the Biden administration will allocate substantial monetary resources to rebuilding legacy infrastructure (and doing so in a way that prioritizes equitable access).

With this emphasis on inclusivity and social innovation, the tech community has the ability to address a range of lifestyle and well-being issues: infrastructure, transportation and mobility, law enforcement, environmental monitoring and energy allocation.

In this time of reset for cities, what smart city technologies will transform how we live our lives? What kinds of technology will make the biggest impact on cities in the next 12 months? Which smart cities are ahead of the curve?

To unpack these questions and more, we conducted the SmartCityX Survey of industry experts — including smart city investors, corporate and municipal thought leaders, members of academia and startups on the front lines of urban innovation — to help provide valuable insights into where we’re heading. Below you’ll find some key takeaways:

Critical infrastructure topped the list of most prominent issues facing today’s cities, followed closely by traffic and transportation. Cisco may have left the party too soon, but others, including countless startups, are lining up and capitalizing on future growth opportunities in the space. A couple of recent data points that support this trend — particularly as it relates to infrastructure rebuilding, IoT and open toolkits to connect fragmented technologies — include the following:

Smart Infrastructure is paramount to Smart City success. It’s crucial that this infrastructure be “architected” as opposed to just connected. This is the only way to truly achieve seamless interoperability while ensuring scalability, reliability, security and privacy. Technology companies that offer robust architectural components and/or platforms stand to deliver tremendous stakeholder value and outsized returns to investors. — Sue Stash, general partner, Pandemic Impact Fund

When asked what will accelerate innovation and change in cities, an overwhelming majority cited COVID-19 as the primary factor, followed by remote work, which has accelerated the adoption of online collaboration tools and forced legacy companies to complete multiyear digital transformation projects in a matter of months. The biggest opportunity is to build cities back better and smarter, focusing on new infrastructures that do more with less, and for most of us, that begins and ends at home.

Powered by WPeMatico

Jim Jackson developed timber and farmland in Eastern Washington, protected from coastal rains by the peaks of the Cascade mountains, building out a clutch of apple farms and other properties on the state’s sunny side for 40 years.

Traditionally, he raised money to expand operations for his farms through his existing network, which meant asking previous investors to pool together and come up with the cash.

But more recently, Jackson turned to a fundraising platform that operates entirely online. Like hundreds of other farmers, he’s using a service called AcreTrader to raise money for agricultural development projects. AcreTrader is one of a growing number of companies revolutionizing the way farm and forestland are acquired, developed and commercialized across the United States.

There’s lots of farmland in the U.S. Bill Gates, Microsoft founder and the world’s third-richest man, is the nation’s largest owner of farmland, holding roughly 242,000 acres. That number seems high until you compare it with the 897.4 million acres of land that are currently arable and used for farming in the U.S.

Another 823 million acres of forests dot the United States, the majority of which are privately owned.

Taken together, that’s a massive amount of real estate with economic potential that’s traditionally been accessible only to the ultrawealthy to acquire and finance for development. Now, startups like AcreTrader and others including Tillable, ($8.3 million) FarmTogether ($3.7 million), and Harvest Returns are bringing marketplace models to the farming world — potentially bringing hundreds of thousands of investable acres to financiers looking to diversify.

Powered by WPeMatico

It’s a busy day in IPO-land: Olo has raised its IPO range and DigitalOcean is giving us a first look at what it may be worth when it debuts.

That Olo raised its IPO price is not a huge surprise, given the software company’s rapid growth and profits. In the case of DigitalOcean, we have more work to do as its approach to growth is a bit different.

Let’s explore both companies’ pricing intervals through our usual lens of revenue multiples, market comps and general SaaS sass. We’ll do this in alphabetical order, which puts the cloud infra company up first.

According to its S-1/A filing, DigitalOcean expects its IPO to price between $44 and $47 per share. The price range is a coup for the company’s private investors, who as recently as the company’s 2020 Series C paid about $10.59 each for the company’s shares. Andreessen Horowitz is going to do very well, having led the company’s Series A at a per-share price of just more than $2. IA Ventures, which led DigitalOcean’s seed round, according to Crunchbase, paid just $0.26 per share back in the 2012-2013 time frame. That’s going to convert well.

In valuation terms, the company’s simple share count post-IPO will be 105,303,340, or 107,778,340 if its underwriters purchase their option. At $44 to $47 per share, DigitalOcean is worth $4.72 billion to $5.07 billion, including shares designated for its underwriters.

The company’s fully diluted valuation is higher. At midpoint, Renaissance Capital estimates DigitalOcean’s diluted valuation is $5.6 billion. That works out to a little under $5.8 billion at $47 per share.

Taking a look at DigitalOcean’s Q4 2020 revenue of $87.5 million, the company closed last year on a run rate of $350 million. Or a revenue multiple of 14.5x at the upper end of its nondiluted valuation, and around 16.5x at the upper bound of its diluted worth.

Powered by WPeMatico

Commitments to carbon neutrality keep coming from all corners of the business world — over the past few weeks, companies ranging from the fast-casual restaurant chain Sweetgreen to the security-focused networking IT company Palo Alto Networks to the online craft retailer Etsy committed to net-zero carbon emission plans.

As the companies look for ways to reduce their energy consumption, they’re turning to carbon offset programs as a stopgap measure until the energy grid decarbonizes, they implement technologies to reduce their energy consumption, or both.

This push toward corporate sustainability is creating all kinds of strange bedfellows and startup opportunities, with major corporate offset programs and the establishment of new startups focused on offsets creating channels for sustainable technologies to get to market.

The latest example of a company leveraging a sustainability angle to tie a corporate partner even closer to their business is the agreement between Delta and Deloitte, which involves the accounting and consulting firm paying Delta for renewable jet fuel to offset the emissions of its corporate travel.

To be clear, a better policy for Deloitte would be to cut back on non-essential travel significantly and focus on doing as much remote work as possible to reduce the need for flights. But in some cases business travel is unavoidable, and most folks want to get back to a pre-pandemic normal, which — at least in the U.S. and other countries — will include significantly ramping up air travel for a percentage of the population.

As the BBC noted, air travel accounts for roughly 5 percent of the emissions that contribute to global climate change, but only a small percentage of the world actually uses air transport. According to one analysis from the International Council on Clean Transport, just 3 percent of the world’s population flies regularly. And if everyone in the world did fly, aircraft emissions would top the CO2 emissions of the entire U.S.

Which brings us back to Deloitte and Delta and startups.

Delta’s deal to buy sustainable aviation fuel that would offset a portion of the carbon emissions associated with Deloitte’s business travel is one small step toward greening the airline industry, but the question is whether it’s a significant first step or just an attempt to greenwash the unsustainable travel habits of a consulting industry that prides itself on such perks.

Powered by WPeMatico