EC entrepreneurship

Auto Added by WPeMatico

Auto Added by WPeMatico

Viewed from the outside, board selection and corporate governance can seem like a bit of a black box — particularly at a startup. Generation Investment Management partner Dave Easton spoke at TechCrunch Early Stage about how to build a board as a founder, and specifically how to build a board you can live with. Easton’s own ample experience serving on boards as both a full member and as an observer, as well as Generation’s focus on building sustainable, ethically managed, mission-driven businesses helped peel back the curtain on the murky topic of good governance.

Easton noted that many boards end up overcrowded — in terms of both the number of people and also the background of those present. Mixing up the type of board members you have managing your corporate governance is key, he said, especially as a company grows in size and maturity.

In terms of fields, the sorts of things that we find that often go wrong is when your board is stacked full of investors. I think investors are great — I’m an investor. I think there are super useful things investors do. But five investors is not very useful, right — it’s just more people who will generally think the same. So a typical thing that we’re doing when we come in is, we’re saying we’re not taking a board seat, we’re gonna give our board seats to an operator — someone who actually knows what they’re doing. When you’re in the earliest stages it’s probably fine to avoid operators and just have one or two investors. Particularly operators who come from, like bigger company backgrounds, they’re not necessarily so helpful when you’re getting product-market fit. But as you get bigger and bigger, you know, operators start to trump investors, and we think boards need to move more heavily in that direction. (Time stamp: 09:34)

On the subject of what should actually take place at well-run board meetings, Easton said that one of the most common pitfalls he’s encountered is when management sort of performatively offers up subjects for debate. It’s something that’s easy to do, but it also ends up not only being wasteful of the time of those present, it also leaves a bad taste in basically everyone’s mouths.

Powered by WPeMatico

In an earlier article, I wrote about how and when to build go-to-market teams at deep tech companies. There, I noted that it is more important for growth hires at deep tech companies to have functional expertise than industry expertise.

But how do deep tech companies connect and cultivate strong relationships with talented nontechnical growth people outside of their industry? In this article, I answer this question, articulating exactly how to:

Incredible growth people are independent and creative and are drawn to environments that explicitly value these traits.

Underscore the autonomy. Incredible growth people are independent and creative and are drawn to environments that explicitly value these traits. Growth talent wants to know that they have room to experiment, fail and iterate with the support and trust of their company. Highlight the creative agency you give to your growth team. Paint the role as one of managing a subset of the startup and its initiatives.

Show you are ready for a growth marketer. Do not expect your growth person to be a panacea for the company. Growth people work cross-functionally, but there are boundaries where the growth role starts and ends. Growth people cannot sell a product that is not ready. Growth people cannot fix product bugs. Growth people cannot replace excellent customer service. Ensure your role description is clear on what the growth person would do and what they would lean on other teams for. Demonstrate that you have a team structure in place where a growth marketer could fit in and thrive.

Articulate your talent needs. Growth is a broad category. Some growth marketers are more creative. Others are more quantitative. Some have more industry experience. Others have more functional experience. Be clear on what type of growth marketer you need and how this person’s talents would complement those of the existing team.

Generate excitement and establish credibility. People can naturally be skeptical about new technologies and younger companies. Do anything you can to ameliorate these concerns. Link to relevant news articles from well-known publications and thought leaders in your industry. Incorporate customer testimonials that speak to the transformative impact your product creates. Name drop well-known advisors, investors and team members.

Powered by WPeMatico

June 4, 2019 should have been one of the happiest days of my life.

At 11:30 a.m., a press release hit the wire announcing that the cybersecurity company I had spent more than eight years building was being acquired by a larger cybersecurity player.

What’s not to love about a successful exit? I’d be set financially, the investors who had given us $70 million would make money, and the technology we created would get new legs in an organization with broader reach and resources.

Still, I had regrets. For one thing, I initially hadn’t wanted to sell. (More on that later.) For another, I was nagged by the feeling that our company had fallen short of its true potential, and that the reason was me — specifically, several rookie mistakes I made as a first-time entrepreneur.

I don’t stew about those errors any longer. In fact, I believe my miscues at my first startup will help define my career from here on out. That’s why, as I grow my next company, I’m thinking about not only the things I want to do but those I’d never do again.

Here are five of them.

In management theory terms, I was a “pacesetter.” I’d be the first to jump into any project or task, I’d execute it as quickly as possible and I expected everyone else to keep up. I thought that was how a startup leader acted — super helpful and scrappy.

But it came at a big price: disempowerment of the team. I was hoarding not only control — nobody felt like they personally owned anything — but also the institutional knowledge that needs to be spread around as a company grows. I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.

I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.

After a few years, I had a frustrating sense that I had all the answers and no one else did. Well, no wonder.

I’m now leaving the pacesetting to NASCAR and marathons.

I believed all I had to do was say something once and everyone would get it. I became irritated when that didn’t happen. “We talked about this three months ago,” I’d bark. Intimidated team members would say to themselves, “Yeah, but we really only got 50% of it.”

Powered by WPeMatico

Twenty years ago Drupal and Acquia founder Dries Buytaert was a college student at the University of Antwerp. He wanted to put his burgeoning programming skills to work by building a communications tool for his dorm. That simple idea evolved over time into the open-source Drupal web content management system, and eventually a commercial company called Acquia built on top of it.

Buytaert would later raise over $180 million and exit in 2019 when the company was acquired by Vista Equity Partners for $1 billion, but it took 18 years of hard work to reach that point.

When Drupal came along in the early 2000s, it wasn’t the only open-source option, but it was part of a major movement toward giving companies options by democratizing web content management.

Many startups are built on open source today, but back in the early 2000s, there were only a few trail blazers and none that had taken the path that Acquia took. Buytaert and his co-founders decided to reduce the complexity of configuring a Drupal installation by building a hosted cloud service.

That seems like a no-brainer now, but consider at the time in 2009, AWS was still a fledgling side project at Amazon, not the $45 billion behemoth it is today. In 2021, building a startup on top of an open-source project with a SaaS version is a proven and common strategy. Back then nobody else had done it. As it turned out, taking the path less traveled worked out well for Acquia.

Moving from dorm room to billion-dollar exit is the dream of every startup founder. Buytaert got there by being bold, working hard and thinking big. His story is compelling, but it also offers lessons for startup founders who also want to build something big.

In the days before everyone had internet access and a phone in their pockets, Buytaert simply wanted to build a way for him and his friends to communicate in a centralized way. “I wanted to build kind of an internal message board really to communicate with the other people in the dorm, and it was literally talking about things like ‘Hey, let’s grab a drink at 8:00,’” Buytaert told me.

He also wanted to hone his programming skills. “At the same time I wanted to learn about PHP and MySQL, which at the time were emerging technologies, and so I figured I would spend a few evenings putting together a basic message board using PHP and MySQL, so that I could learn about these technologies, and then actually have something that we could use.”

The resulting product served its purpose well, but when graduation beckoned, Buytaert realized if he unplugged his PC and moved on, the community he had built would die. At that point, he decided to move the site to the public internet and named it drop.org, which was actually an accident. Originally, he meant to register dorp.org because “dorp” is Dutch for “village or small community,” but he mistakenly inverted the letters during registration.

Buytaert continued adding features to drop.org like diaries (a precursor to blogging) and RSS feeds. Eventually, he came up with the idea of open-sourcing the software that ran the site, calling it Drupal.

About the same time Buytaert was developing the basis of what would become Drupal, web content management (WCM) was a fresh market. Early websites had been fairly simple and straightforward, but they were growing more complex in the late 90s and a bunch of startups were trying to solve the problem of managing them. Buytaert likely didn’t know it, but there was an industry waiting for an open-source tool like Drupal.

Powered by WPeMatico

The lure of subscription pricing is the guarantee of recurring revenue for your business. Once a customer flips the switch to turn on your subscription, it’s easy money:

While that’s true, converting a subscription customer isn’t as simple as flipping a switch. You can build a platform, launch with fanfare, offer all sorts of incentives and trials to attract potential customers — and watch as they disengage and lapse into limbo.

Contrary to popular belief, subscription pricing doesn’t work because of the lower price point that a monthly installment allows.

That’s the actual guarantee that comes with subscription pricing, which will happen unless you cultivate a funnel that catches potential subscribers as soon as they learn about your product and follows them until their very last sign-in.

I built my first subscription-model product in 1999. I’m currently in early-access on my latest, and I’ve launched a bunch more along the way.

While the customer dynamic has changed over the last 20 years, the conversion process has not. In fact, it’s actually gotten easier to convert and retain customers through the subscription funnel.

Here’s what I’ve learned.

Subscription pricing is a hot trend in just about every business in every industry. Pay-as-you-go is the new normal from software to retail to service.

In my mind, the major shift occurred when mobile phones started pricing unlimited usage per period instead of fixed or cost per minute. Once usage limits were removed, use cases exploded and the promise of a truly mobile computer was finally realized.

Makers of all stripes learned that lesson: From razors to video streaming to accounting software, pricing models have emerged that focus on time periods instead of units.

But contrary to popular belief, subscription pricing doesn’t work because of the lower price point that a monthly installment allows. It’s effective because a subscription reorients each customer’s mind from product function to value proposition.

I don’t care what kind of German engineering went into my razor blades, as long as I have working blades when I need them.

As an entrepreneur, you probably use at least one digital subscription service to build your own product and company, if not several. In fact, just to get to the MVP of my new project, I subscribed to AWS, MailChimp, Zapier and Bubble. I’m still on the free tier of a few more services for some lower-priority features. There’s a few more I quit or never tried.

Thus, you know that value prop plays a big part of whether the customer will pay and stay. So reinforcing your value proposition should play a big part in every level of your customer funnel.

A subscription-pricing model without an ability to track the steps in the conversion funnel will result in all the headaches of subscription pricing without any of the benefits.

Powered by WPeMatico

During my five years with Global Founders Capital, Rocket Internet’s $1 billion VC arm, I saw more than a hundred of Rocket’s incubated companies attempt to internationalize. For background, Rocket Internet has helped launch some very successful businesses internationally, including HelloFresh ($12.9 billion market cap), Lazada ($1 billion exit to Alibaba), Jumia ($3.2 billion market cap), Zalando ($21.2 billion market cap) and many others. Rocket often followed the Blitzscaling model popularized by Reid Hoffman — earning them an appearance in his book of the same name.

After an initial success helping Groupon scale internationally via a merger with Rocket’s incubation firm CityDeal, Rocket’s team have aggressively scaled businesses from Algeria to Zimbabwe — sometimes in a matter of weeks. No surprise, Rocket also has a graveyard of failed companies that were victims of bad internationalization efforts.

Many companies make the costly mistake of launching abroad too soon.

My personal observations on Rocket’s successes and failures start with this crucial point: These learnings might not apply to your unique combination business model, market and timing. No matter how well you prepare and plan your internationalization, in the end you need to be agile, alert and smart as you dip your toes into your first foreign market.

Internationalization can be a big driver of growth and consequently enterprise value, which is why investors always push for it. But going abroad can also destroy value just as quickly. As a founder, it’s your job to manage financial and operational risks. Finding the right balance between keeping costs in check and not underinvesting can mean doing things more slowly than your board would like. For example, you might launch new markets sequentially instead of rolling 10 out at the same time.

Adopt a “hire slow, fire fast” mentality for your expansion strategy. Don’t be afraid to pull the plug if things don’t work out.

Our team at Heartcore Capital use the following framework and learnings to guide internationalization strategies for our portfolio companies. A successful internationalization strategy needs to answer and address the “Four Ws”: When, Where, Which and With whom to internationalize. (Regarding the fifth W from journalism, you should not need to ask the “Why” question if you want to build a large business!)

Many companies make the costly mistake of launching abroad too soon. They look at internationalization as a detached function, isolated from the rest of the business and then launch their second market prematurely. Follow this simple rule: Wait to internationalize until you hit product/market fit.

How do you know exactly when you’ve reached product/market fit? According to Marc Andreessen, “Product/market fit means being in a good market with a product that can satisfy that market.” He adds that experienced entrepreneurs can usually feel if they’ve reached this point.

Let’s take the man for his word and move on to the actual argument: Until you have product/market fit, you will not be able to distinguish between what you’ve learned from your business model and what you’ve learned from your in-country experience. Mistakes will compound. Complexities and costs will multiply. I contend that insufficient understanding of their business and operating model is the main reason why companies fail with their expansion strategies.

Founders should also consider the underlying costs of internationalizing before they decide to expand (more about this in the “What” section below). Some companies are global by default — think mobile gaming companies — or simply require language localization. Others need to build new warehouses, hire local teams or build entirely new products. The costs and respective risks of expanding prematurely depend heavily on the business model.

There are edge cases where companies need to move quickly to internationalize for strategic reasons — despite uncertainty about their market fit. For instance, companies like Groupon or those engaged in food delivery face winner-takes-most markets, where opportunities for product differentiation are limited. “Blitzscaling” makes sense in cases like these.

However, you should tread carefully if your only reason to start scaling abroad is a large fundraise or to match a competitor’s internationalization efforts. Scaling prematurely for the wrong reasons might just cost you your entire company.

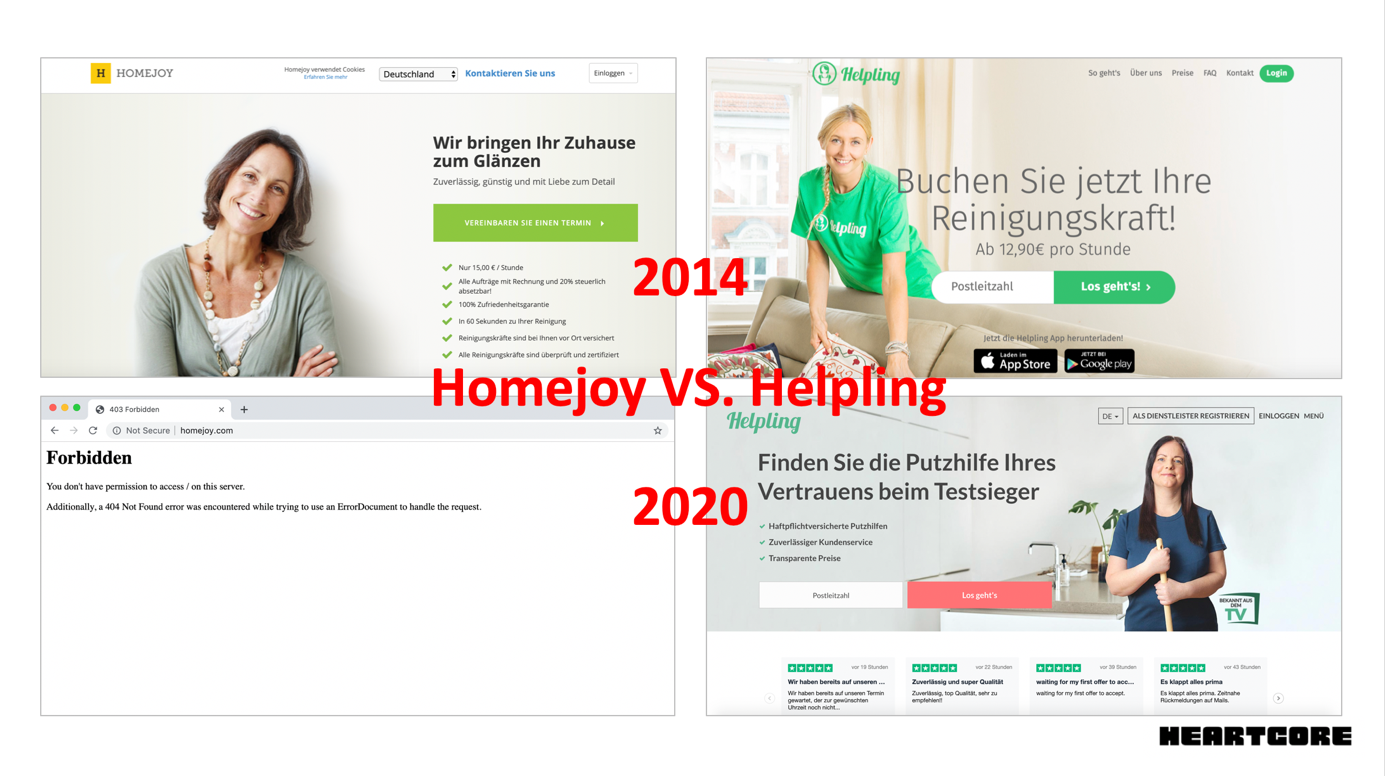

When Rocket Internet announced it would launch the Homejoy model into European markets with Helpling, the American “original” company launched quickly in Germany in an effort to squash their new competitor. In the early days of “on-demand everything,” a managed marketplace for cleaning services sounded like the next unicorn in the making.

In 2013, Homejoy had a fresh $24 million Series A from Google Ventures and First Round — considered a huge round at a time when Instacart had just raised an $8 million Series A and Snapchat had done a $13 million Series A round. It must have seemed like a good idea to squash the German competition early.

As it turned out, Homejoy’s product was not yet ready to scale internationally. Just 13 months after launching in Germany, Homejoy had to cease operations globally, while Rocket’s Helpling is still alive and kicking. Helpling focused carefully on product, automation and making their unit economics work. A rush to crush an international competitor caused the demise of a would-be unicorn.

Homejoy expanded internationally in 2014 in a rush to squash a new German competitor Helpling. Their websites in 2020 show starkly different outcomes. Image Credits: Homejoy/Helpling

When deciding which new international market to tackle, it is vital to do your homework. Analyze the competitive environment, partner availability, infrastructure, culture, regulation and synergies with your home market.

In the early days of e-commerce, it was rather easy to analyze if a market was an expansion target. In the absence of professional competition, Rocket chose new countries based solely on GDP and internet penetration.

Powered by WPeMatico

In 20 years of working for startups, I’ve never seen as many plot twists and turns as I have in the last several months. Times are tough.

But, from the perspective of raising capital, 2020 has not been an awful time to be a startup founder. The world has changed, but the fundamentals of raising capital are the same. In the first half of the year, VCs invested $129 billion, and Q3 is up 9% year-over-year, reports Crunchbase.

After the screeching halt to business in April subsided, founders and investors, people who are generally comfortable with uncertainty, got back to work raising and investing.

Choosing the right VC is one of the most important decisions startup founders will make. In good times, the choice can make or break a startup. When times are bad, it’s even more likely that the wrong VC partner could be the catalyst that starts a downward spiral. With many funds still looking to make investments before the end of the year and startups jockeying for cash, founders need to know how to find the right investor.

With many funds still looking to make investments before the end of the year and startups jockeying for cash, founders need to know how to find the right investor.

It’s not about simply choosing an investor — you are hiring your next boss. The investor should be someone you feel comfortable working with and working for.

You don’t want an investor who is checked out, but too much focus isn’t good, either. And, you don’t want an investor who is completely agreeable since your best outcome will be driven by a constructively demanding advisor.

My company, Quiq, had several term sheets when the dust settled on our Series B pitch meetings. Since the financial terms were similar, selecting an investor was made on a more subjective basis and boiled down to two fundamental questions:

Powered by WPeMatico

General Catalyst has made early bets on some of the biggest companies in tech today, including Airbnb, Lemonade and Warby Parker.

We sat down with Katherine Boyle and Peter Boyce, who co-lead the firm’s seed-stage investments, to discuss what they look for in founders, which sectors they’re most excited about and how business has changed in the wake of the COVID-19 pandemic.

This conversation is part of our broader Extra Crunch Live series, where we sit down with VCs and founders to discuss startup core competencies and get advice. We’ve spoken to folks like Aileen Lee, Mark Cuban, Roelof Botha, Charles Hudson and many, others. You can browse the full library of episodes here.

Check out our full conversation with Boyce and Boyle in the YouTube video below, or skim the text for the highlights.

Katherine Boyle: I look for what I would call this obsessive trait, where they are learning more about the regulatory complications, where they are constantly trying to figure out how to solve a problem.

I’d say that the common theme among the founders that I support are that they have this sort of obsessive gene or personality, where they will go deeper and deeper and deeper. When we invest in these companies, it becomes very clear that they often have sort of a contrarian view of the industry. Maybe they are not industry-native. They come at it from a different perspective of problem solving. They’ve had to defend that thesis for a very, very long time in front of a variety of different customers and different people. In some ways, that makes them much stronger in terms of the way they approach problems.

Peter Boyce: I think the first would be being magnetic for talent. It ends up influencing the speed of learning and development. Really incredible founding teams that can be magnetic for talent and learning just kind of spirals out of control in really good ways over time. I really look for the speed and the sources of learning. And can folks be really intentional? Can they get the right set of advisors and teammates around them?

The second would be the personal connection to the problem space. It’s like there’s this kind of deep-seated source of energy and fuel that actually isn’t going to run out. Catherine and I’ve been lucky to work across a number of different particular thematic areas, but the thing they have in common is just this personal connection to how and why their business needs to exist. Because I just think that that fuel doesn’t run out, you know what I mean? Like, that’s renewable.

Boyle: If you’re someone who’s comfortable presenting on Zoom, making connections on Zoom, or using Signal and using Twitter and being very online, then I 100% think that you can make investments, build community and build connections through digital worlds and digital platforms. If you really like that in-person connectivity, then you might consider staying in a tech hub, or you might consider sort of these distanced walks until things go back to normal.

Powered by WPeMatico

At the end of 2019, no one would have predicted what an unpredictable and difficult year it has been for both startups and VCs in the fundraising world. Now we are staring down the end of 2020 and looking toward what we all hope is a better, safer 2021. What will this new year bring? With an end-of-year sprint to close deals, the anticipation of a new presidential administration and the hope of a COVID-19 vaccine on the horizon, startups and VCs know that change is on the horizon — but how much of that change will be positive?

As 2020 proved, no one can say for sure what 2021 will bring, but I’d like to put a few predictions on the table based on DocSend’s data and research, including the DocSend Startup Index, as well as some trends I’ve seen and my own experiences. These predictions center around how we’ll fundraise post-pandemic, how the funding divide may widen for some, what fundraising activity could look like into 2021, a few sectors we think will fare well and will incorporate some tips on how to succeed in the new year, no matter what comes our way.

The pandemic forced all of us to drastically change how we work and interact with colleagues and clients. When the pandemic subsides and vaccines are widely available, in-person meetings and gathering back at the office will definitely resume, but it’s safe to say the old ways of networking and fundraising won’t shift back 100%. Founders and VCs alike have navigated the ups and downs of remote networking and fundraising interactions and will stick to what works and what doesn’t.

Is traveling to a conference the best way for a founder to have a chance at meeting the VC who is right to support their business? Will a VC want to drive an hour through Bay Area traffic for an in-person status update meeting on their latest investment? Zoom fatigue aside, video conference calls do have some benefits — efficiency, no travel time — although not all meetings are best conducted virtually.

No matter what 2021 has in store, founders can still take proactive steps to help them succeed in their fundraising efforts.

The extent to which businesses go in-person or stick to virtual meetings could depend directly on what round of fundraising they are working toward or have completed. Businesses in the pre-seed round might stick with more Zoom meetings in order to conserve resources.

Founders in the seed round will likely split between video and in-person meetings as they are under pressure to show traction in this round, as we found in our report on seed fundraising, yet will also need to conserve resources and time. For Series A, they might have to meet less in person because they have established relationships with their investors. Series B might see more in-person meetings as their business has reached a level of complexity that is difficult to communicate via a deck or video conference.

Powered by WPeMatico