EC Enterprise Applications

Auto Added by WPeMatico

Auto Added by WPeMatico

Last year, Seattle-based network security startup ExtraHop was riding high, quickly approaching $100 million in ARR and even making noises about a possible IPO in 2021. But there will be no IPO, at least for now, as the company announced this morning it has been acquired by a pair of private equity firms for $900 million.

The firms, Bain Capital Private Equity and Crosspoint Capital Partners, are buying a security solution that provides controls across a hybrid environment, something that could be useful as more companies find themselves in a position where they have some assets on-site and some in the cloud.

The company is part of the narrower Network Detection and Response (NDR) market. According to Jesse Rothstein, ExtraHop’s chief technology officer and co-founder, it’s a technology that is suited to today’s threat landscape, “I will say that ExtraHop’s north star has always really remained the same, and that has been around extracting intelligence from all of the network traffic in the wire data. This is where I think the network detection and response space is particularly well suited to protecting against advanced threats,” he told TechCrunch.

The company uses analytics and machine learning to figure out if there are threats and where they are coming from, regardless of how customers are deploying infrastructure. Rothstein said he envisions a world where environments have become more distributed with less defined perimeters and more porous networks.

“So the ability to have this high-quality detection and response capability utilizing next generation machine learning technology and behavioral analytics is so very important,” he said.

Max de Groen, managing director at Bain, says his company was attracted to the NDR space, and saw ExtraHop as a key player. “As we looked at the NDR market, ExtraHop, which [ … ] has spent 14 years building the product, really stood out as the best individual technology in the space,” de Groen told us.

Security remains a frothy market with lots of growth potential. We continue to see a mix of startups and established platform players jockeying for position, and private equity firms often try to establish a package of services. Last week, Symphony Technology Group bought FireEye’s product group for $1.2 billion, just a couple of months after snagging McAfee’s enterprise business for $4 billion as it tries to cobble together a comprehensive enterprise security solution.

Powered by WPeMatico

Software as a service has been thriving as a sector for years, but it has gone into overdrive in the past year as businesses responded to the pandemic by speeding up the migration of important functions to the cloud. We’ve all seen the news of SaaS startups raising large funding rounds, with deal sizes and valuations steadily climbing. But as tech industry watchers know only too well, large funding rounds and valuations are not foolproof indicators of sustainable growth and longevity.

Failing to come across as a unique, differentiated company will likely mean settling for an exit that feels mediocre instead of incredible.

To scale sustainably, grow its customer base and mature to the point of an exit, a SaaS startup needs to stand apart from the herd at every phase of development. Failure to do so means a poor outcome for founders and investors.

As a founder who pivoted from on-premise to SaaS back in 2016, I have focused on scaling my company (most recently crossing 145,000 customers) and in the process, learned quite a bit about making a mark. Here is some advice on differentiation at the various stages in the life of a SaaS startup.

Differentiation is crucial early on, because it’s one of the only ways to attract customers. Customers can help lay the groundwork for everything from your product roadmap to pricing.

The more you know about your target customers’ pain points with current solutions, the easier it will be to stand out. Take every opportunity to learn about the people you are aiming to serve, and which problems they want to solve the most. Analyst reports about specific sectors may be useful, but there is no better source of information than the people who, hopefully, will pay to use your solution.

The key to success in the SaaS space is solving real problems. Take DocuSign, for example — the company found a way to simply and elegantly solve a niche problem for users with its software. This is something that sounds easy, but in reality, it means spending hours listening to the customer and tailoring your product accordingly.

Powered by WPeMatico

What happens to technology companies with slowing growth and a rising focus on profitability before they reach behemoth scale? How much does the market value hypergrowth?

Just because a technology startup has a hot start, that doesn’t mean it will grow quickly forever. Most will wind up somewhere in the middle — or worse. Put simply, there is a larger number of tech companies that do fine or a little bit worse after they reach scale.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But what every investor hopes for is the hot company that can keep growth alive even after reaching material scale, running through walls, competitors, economic headwinds and anything else that comes its way. Those companies don’t end up worth a few hundred million, or a billion, but can end up valued in the dozens of billions or more.

In reverse, tech companies — even those with strong gross margins — with slipping growth can see their multiples compress rapidly. Then, the vultures circle.

In reverse, tech companies — even those with strong gross margins — with slipping growth can see their multiples compress rapidly. Then, the vultures circle.

Which explains some of the news we’ve seen recently in the market. As Dropbox comes under fresh pressure from external parties, joining its erstwhile rival Box in the public-market growth penalty box, we’re seeing companies like Braze, Gong, Shippo and others rip ahead with rapid-fire funding rounds or public brags about their growth.

While the differential between the two groups is clear, it’s still worth exploring in more detail. Let’s talk about the growth dividend. Or, if you’d prefer, the existential cost of growth deceleration.

The news this week that Dropbox has attracted an activist shareholder should not have been a surprise. Its former rival Box is in the midst of a long-running struggle with an activist investor of its own. (More here.)

Powered by WPeMatico

Confluent became the latest company to announce its intent to take the IPO route, officially filing its S-1 paperwork with the U.S. Securities and Exchange Commission this week. The company, which has raised over $455 million since it launched in 2014, was most recently valued at just over $4.5 billion when it raised $250 million last April.

What we can see in Confluent is nearly an old-school, high-burn SaaS business. It has taken on oodles of capital and used it in an increasingly expensive sales model.

What does Confluent do? It built a streaming data platform on top of the open-source Apache Kafka project. In addition to its open-source roots, Confluent has a free tier of its commercial cloud offering to complement its paid products, helping generate top-of-funnel inflows that it converts to sales.

Kafka itself emerged from a LinkedIn internal project in 2011. As we wrote at the time of Confluent’s $50 million Series C in 2017, the open-source project was designed to move massive amounts of data at the professional social network:

At its core, Kafka is simply a messaging system, created originally at LinkedIn, that’s been designed from the ground up to move massive amounts of data smoothly around the enterprise from application to application, system to system or on-prem to cloud — and deal with extremely high message volume.

Confluent CEO and co-founder Jay Kreps wrote at the time of the funding that events streaming is at the core of every business, reaching sales and other core business activities that occur in real time that go beyond storing data in a database after the fact.

“[D]atabases have long helped to store the current state of the world, but we think this is only half of the story. What is missing are the continually flowing stream of events that represents everything happening in a company, and that can act as the lifeblood of its operation,” he wrote.

That’s where Confluent comes in.

But enough about the technology. Is Confluent’s work with Kafka a good business? Let’s find out.

Powered by WPeMatico

Another week, another unicorn IPO. This time, Sprinklr is taking on the public markets.

The New York-based software company works in what it describes as the customer experience market. After attracting over $400 million in capital while private, its impending debut will not only provide key returns to a host of venture capitalists but also more evidence that New York’s startup scene has reached maturity. (More evidence here.)

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Sprinklr last raised a $200 million round at a $2.7 billion valuation in September 2020. That round, as TechCrunch reported, also included a host of secondary shares and $150 million in convertible notes. Inclusive of the latter instrument, Sprinklr’s total capital raised to date soars above the $500 million mark.

Temasek Holdings, Battery Ventures, ICONIQ Capital, Intel Capital and others have plugged funds into Sprinklr during its startup days.

Temasek Holdings, Battery Ventures, ICONIQ Capital, Intel Capital and others have plugged funds into Sprinklr during its startup days.

Sure, Robinhood didn’t file last week as many folks hoped, but the Sprinklr IPO ensures that we’ll have more than just SPACs to chat about in the coming days. But one thing at a time. Let’s discuss what Sprinklr does for a living.

Sprinklr’s IPO filing and corporate website suffer from a slight case of corporate speak, so we have some work to do this morning to determine what the company does. Here’s what the company says about itself in its filing:

Sprinklr empowers the world’s largest and most loved brands to make their customers happier.

We do this with a new category of enterprise software — Unified Customer Experience Management, or Unified-CXM — that enables every customer-facing function across the front office, from Customer Care to Marketing, to collaborate across internal silos, communicate across digital channels, and leverage a complete suite of modern capabilities to deliver better, more human customer experiences at scale — all on one unified, AI-powered platform.

Not very clear, yeah? Don’t worry, I’ve got you. Here’s what the company actually does:

Powered by WPeMatico

The notion of digital transformation evolved from a buzzword joke to a critical and accelerating fact during the COVID-19 pandemic. The changes wrought by a global shift to remote work and schooling are myriad, but in the business realm they have yielded a change in corporate behavior and consumer expectation — changes that showed up in a bushel of earnings reports this week.

TechCrunch may tend to have a private-company focus, but we do keep tabs on public companies in the tech world as they often provide hints, notes and other pointers on how startups may be faring. In this case, however, we’re working in reverse; startups have told us for several quarters now that their markets are picking up momentum as customers shake up their buying behavior with a distinct advantage for companies helping customers move into the digital realm. And public company results are now confirming the startups’ perspective.

The accelerating digital transformation is real, and we have the data to support the point.

What follows is a digest of notes concerning the recent earnings results from Box, Sprout Social, Yext, Snowflake and Salesforce. We’ll approach each in micro to save time, but as always there’s more digging to be done if you have time. Let’s go!

Kicking off with Yext, the company beat expectations in its most recent quarter. Today its shares are up 18%. And a call with the company’s CEO Howard Lerman underscored our general thesis regarding the digital transformation’s acceleration.

In brief, Yext’s evolution from a company that plugged corporate information into external search engines to building and selling search tech itself has been resonating in the market. Why? Lerman explained that consumers more and more expect digital service in response to their questions — “who wants to call a 1-800 number,” he asked rhetorically — which is forcing companies to rethink the way they handle customer inquiries.

In turn, those companies are looking to companies like Yext that offer technology to better answer customer queries in a digital format. It’s customer-friendly, and could save companies money as call centers are expensive. A change in behavior accelerated by the pandemic is forcing companies to adapt, driving their purchase of more digital technologies like this.

It’s proof that a transformation doesn’t have to be dramatic to have pretty strong impacts on how corporations buy and sell online.

Powered by WPeMatico

Hot off the heels of our look into Marqeta’s IPO filing and dives into SPACs for Bright Machines and Bird, we’re parsing the WalkMe IPO filing. Later this week, Squarespace will direct list and we’ll see IPOs from Oatly and Procore. It’s a super busy time for public debuts of all sorts.

Given how hectic the IPO market is, we’re going to skip our usual throat clearing and dig into WalkMe’s IPO document. As always, we’ll start with a brief overview of its product and then move into discussing its financial performance.

Image Credits: Alex Wilhelm

WalkMe is the second Israel-based technology company to file to go public this week: No-code startup Monday.com is also pursuing an American IPO.

Alright! Into the breach.

WalkMe’s software provides visual overlays on websites that help users navigate the product in question. I base that explanation on my time at Crunchbase, which was a customer during at least part of my time there. WalkMe is popular with marketing teams who want to introduce users to a new or refreshed experience.

Per the company’s F-1 filing, other elements of its service that matter include its onboarding system and what WalkMe calls Workstation, or its “single interface to the applications within an enterprise and simplifies task completion through a natural language conversational interface and automation.” We’re including that last feature because it says “automation,” which, in the wake of the UiPath IPO, is a word worth watching. Investors are.

At a high level, WalkMe is a SaaS business, which means that when we digest its results we are digging into a modern software company. Let’s do just that.

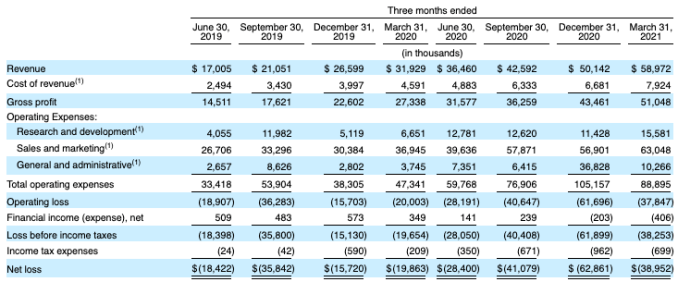

From 2019 to 2020, WalkMe grew its revenues from $105.1 million to $148.3 million, a gain of 41%. In its most recent quarter, the company’s growth rate slowed: From Q1 2020 to Q1 2021, WalkMe’s top line grew 25% from $34.2 million to $42.7 million.

In SaaS terms, WalkMe calculates that its annual recurring revenue, or ARR, grew from $131.2 million at the end of 2019 to $164.3 million in 2020. In more granular terms, the company’s ARR grew from $137.8 million to $177.5 million in the first quarters of 2020, and 2021, respectively.

Powered by WPeMatico

The influence of a founder on their company’s culture cannot be overstated. Everything from their views on the product and business to how they think about people affects how their company’s employees will behave, and since behavior in turn informs culture, the consequences of a founder’s early decisions can be far-reaching.

So it’s not very surprising that Expensify has its own take on almost everything it does when you consider what its founder and CEO David Barrett learned early in his life: “Basically everyone is wrong about basically everything.” As we saw in part 1 of this EC-1, this led him to the revelation that it’s easier to figure things out for yourself than finding advice that applies to you. Eventually, these insights — and the adventurous P2P hacker attitude he nurtured alongside his colleagues and Travis Kalanick at Red Swoosh — would inform how he would go about shaping Expensify.

Expensify’s culture can’t be separated from its hiring and growth processes — by joining the company, employees self-select into a group that isn’t likely to get hung up about trade-offs.

It’s striking how Expensify has managed to maintain this character 13 years later, even on the threshold of an IPO. How did this happen? During a series of interviews in February and early March, we found the answer is tied to the level of thought and effort this expense management business puts into its culture.

You see, the people at Expensify are prepared to invent their own playbook, develop it and, if needed, rewrite it completely. Its HR policies and strategy are tailored to find people who would have fun building an expense management product. It has a unique growth and recognition scheme to offset the drawbacks of a flat organizational structure. It’s even got a “Senate” that vets all major decisions. No kidding.

All this, and more, has ultimately helped Expensify reach more than 10 million users and achieve $100 million in annual revenue with just 130 employees. Let’s take a closer look at how Expensify makes it happen.

It’s clear Expensify’s unusually high employee-to-revenue ratio is intentional: “We want the fewest people necessary to get the job done,” Barrett says. But how do you actually achieve it? How do you hire and keep people who can deliver such results? Barrett had to learn how the hard way.

Expensify’s first team was based in San Francisco and comprised Barrett’s old Red Swoosh and Akamai colleagues, who joined a few months after Akamai fired him. A small team was enough to get started, but it was much more difficult to hire additional people. Barrett is eager to clarify the Valley is not really the best place to recruit talent: “Sure, Silicon Valley has a ton of really awesome people, but all of them have jobs!,” he says.

Powered by WPeMatico

At long last, the Monday.com crew dropped an F-1 filing to go public in the United States. TechCrunch has long known that the company, which sells corporate productivity and communications software, has scaled north of $100 million in annual recurring revenue (ARR).

The countdown to its IPO filing — an F-1, because the company is based in Israel, rather than the S-1s filed by domestic companies — has been ticking for several quarters, so seeing Monday.com drop the document on this Monday morning was just good fun.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The Exchange has been riffling through the document since it came out, and we’ve picked up on a few things to explore. We’ll start by looking at the company’s revenue growth on a historical basis to see if it has accelerated in recent quarters thanks to the pandemic. Then, we’ll turn to profitability, cash burn, share-based compensation expenses and product vision.

We’ll wrap at the end with a summary of what we’ve learned and also make sure to check out the company’s marketing spend, because I’m sure you’ve seen its digital ads.

It’s a lot to chew through, so no more dilly-dallying. Into the numbers!

As always, we’re starting with revenue growth because it’s still the single most important thing about any venture-backed company.

This is great news for the startup, its employees and its investors. From 2019 to 2020, Monday.com grew its revenues from $78.1 million to $161.1 million, or 106%.

From Q1 2020 to Q1 2021, the company’s revenues grew from $31.9 million to $59 million. That’s about 85% growth. So, by what measure do we mean that the company’s revenue growth is accelerating? Its sequential-quarter revenue growth is picking up. Observe the following:

Image Credits: Monday.com F-1 filing

From Q2 2019 to Q3 2019, the company added around $4 million in revenue. From Q2 2020 to Q3 2020, that number was $6.1 million. More recently, the company’s revenue added $7.6 million from Q3 2020 to Q4 2020, which accelerated to $8.8 million from the final quarter of 2020 to the first quarter of 2021. Of course, from an ever-larger base, the company’s growth rate may decline. But the super clean and obvious expanding sequential revenue gains at the company are solid.

The fact that it added so much top line in recent quarters also helps explain why Monday.com is going public now. Sure, the markets are still near record highs and the pandemic is fading, but just look at that consistent growth! It’s investor catnip.

Powered by WPeMatico

Although recurring revenue businesses have been around for a long time, the trend toward a subscription economy has escalated rapidly in the last few years. IDC expects that by 2022, 53% of all software revenue will be purchased with a subscription model. Even the car subscription market is set to grow by 71% by 2022.

Many types of businesses are looking for ways to earn recurring revenue — and it has gone beyond business-to-consumer companies like Netflix and Dollar Shave Club. Business-to-business companies are also joining in, even those with products that last a long time. For instance, elevator-maker Otis offers Otis ONE, a subscription-connected elevator solution that offers predictive maintenance insights.

Subscription billing options should make it easy to manage all types of subscriptions, including integrating analytics to provide a more complete picture of the subscriptions landscape.

Subscription business models are attractive, but there are two major pitfalls. At the top of the list is payment. Regardless of company size, there’s an ongoing need to convince customers to sign up long term.

Companies also need to accommodate new payment methods and ensure ongoing compliance with interstate and international tax laws. As a result, the payment process can quickly become painful.

As any company with recurring revenue scales, it becomes increasingly challenging to manage subscriptions, especially with homegrown systems, changing subscription offers and the complexities of converting customers from free trials to paid subscriptions. Subscription billing options should make it easy to manage all types of subscriptions, including integrating analytics to provide a more complete picture of the subscriptions landscape.

Businesses also have to keep in mind that every time they add more product categories or expand into new geographies, they need to tack on extra software code to change their operations and stay sales-tax-compliant. As they expand globally, this can become an obstacle to rapid growth and flexibility.

To keep the company focused and maintain growth without having to expend resources, subscription businesses need a specialized billing system so they can focus on customer acquisition and revenue growth rather than staying on top of billing complexity.

The second issue: How do businesses cover the funding gap between when customers sign up and when they pay? In the subscription economy, companies that would previously receive a customer’s payments all at once now earn revenue spread across a monthly or quarterly subscription fee.

Powered by WPeMatico