EC Edtech

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s a story common to all sectors today: investors only want to see ‘uppy-righty’ charts in a pitch. However, edtech growth in the past 18 months has ramped up to such an extent that companies need to be presenting 3x+ growth in annual recurring revenue to even get noticed by their favored funds.

Some companies are able to blast this out of the park — like GoStudent, Ornikar and YouSchool — but others, arguably less suited to the conditions presented by the pandemic, have found it more difficult to present this kind of growth.

One of the most common themes Brighteye sees in young companies is an emphasis on international expansion for growth. To get some additional insight into this trend, we surveyed edtech firms on their expansion plans, priorities and pitfalls. We received 57 responses and supplemented it with interviews of leading companies and investors. Europe is home 49 of the surveyed companies, six are based in the U.S., and three in Asia.

Going international later in the journey or when more funding is available, possibly due to a VC round, seems to make facets of expansion more feasible. Higher budgets also enable entry to several markets nearly simultaneously.

The survey revealed a roughly even split of target customers across companies, institutions and consumers, as well as a good spread of home markets. The largest contingents were from the U.K. and France, with 13 and nine respondents respectively, followed by the U.S. with seven, Norway with five, and Spain, Finland, and Switzerland with four each. About 40% of these firms were yet to foray beyond their home country and the rest had gone international.

International expansion is an interesting and nuanced part of the growth path of an edtech firm. Unlike their neighbors in fintech, it’s assumed that edtech companies need to expand to a number of big markets in order to reach a scale that makes them attractive to VCs. This is less true than it was in early 2020, as digital education and work is now so commonplace that it’s possible to build a billion-dollar edtech in a single, larger European market.

But naturally, nearly every ambitious edtech founder realizes they need to expand overseas to grow at a pace that is attractive to investors. They have good reason to believe that, too: The complexities of selling to schools and universities, for example, are widely documented, so it might seem logical to take your chances and build market share internationally. It follows that some view expansion as a way of diversifying risk — e.g. we are growing nicely in market X, but what if the opportunity in Y is larger and our business begins to decline for some reason in market X?

International expansion sounds good, but what does it mean? We asked a number of organizations this question as part of the survey analysis. The responses were quite broad, and their breadth to an extent reflected their target customer groups and how those customers are reached. If the product is web-based and accessible anywhere, then it’s relatively easy for a company with a good product to reach customers in a large number of markets (50+). The firm can then build teams and wider infrastructure around that traction.

Powered by WPeMatico

The Chinese government’s crackdown on its domestic technology industry continues, with Tencent under fresh pressure despite the company’s efforts to follow changing regulatory expectations.

News broke over the weekend that Beijing filed a civil suit against Tencent “over claims its messaging-app WeChat’s Youth Mode does not comply with laws protecting minors,” per the BBC. And NetEase, a major Chinese technology company, will delay the IPO of its music arm in Hong Kong. Why? Uncertain regulations, per Reuters.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The latest spate of bad news for China’s technology industry follows a raft of regulatory changes and actions by the nation’s government that have deleted an enormous quantity of equity value. After a period of relatively light-touch regulatory oversight, domestic Chinese technology companies have found themselves on defense after the Chinese Communist Party (CCP) came after their market power in antitrust terms — and some of their business operations from other perspectives. Sectors hit the hardest include fintech and edtech.

Gaming is also in the CCP crosshairs.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

NetEase stock traded around $110 per share in late July. It’s now worth around $90 per share after expectations shifted in light of the gaming news, indicating that investors are concerned about its future performance. Tencent’s Hong Kong-listed stock has also fallen, from HK$775.50 to HK$461.60 this morning.

Tencent tried to head off regulatory pressure, announcing changes to how it controls access to its games after the government’s shot across the bow. The effort doesn’t appear to have worked. That Tencent is being sued by the government despite its publicly announced changes implies that its proposed curbs to youth gaming were either insufficient or perhaps moot from the beginning.

Powered by WPeMatico

U.S. edtech company Duolingo released a revised IPO price range this morning, boosting its potential per-share value to $100 after initially targeting a range that topped out at $95 per share.

Per the unicorn’s SEC filings, Duolingo is now targeting a $95 to $100 per share IPO price range, up from $85 to $95 per share, or a gain of around 12% at the bottom and 5% at the top.

TechCrunch previously called the Duolingo debut a bellwether of sorts for the larger U.S. edtech ecosystem; if Duolingo can price and trade well, investors in private companies may be more willing to invest, given a more proven and attractive exit market. On the other hand, if Duolingo prices weakly or trades poorly, the company could place a wet blanket atop the startup edtech world.

The fact that Duolingo is raising its IPO price range indicates that we are more likely on the path for a strong offering than a weak one.

For edtech companies that have hit unicorn status — like Masterclass, Course Hero, Quizlet and Outschool — it’s good news. For reference, those companies have raised $461.4 million, $97.4 million, $62 million and $130 million, respectively, per Crunchbase data.

The terms of the company’s IPO have not changed, aside from its proposed price. So, Duolingo is still selling 3.7 million shares in its debut, and some 1.41 million shares will be sold by existing equity holders. The company’s underwriters also reserved their right to buy 765,916 shares of the company’s stock at IPO price in the 30 days following its debut.

At the upper and lower bands of the company’s IPO price, its simple valuation excluding underwriter shares now lands between $3.41 billion and $3.59 billion. Inclusive of its greenshoe offering, those numbers rise to $3.48 billion and $3.67 billion.

Recall that when private, Duolingo’s November 2020 Series H valued the company at just over $2.4 billion. So long as Duolingo prices in its range, it will provide investors with a nice bump in the value of their investment. Duolingo was valued at just $1.6 billion in mid-2020, indicating that it has more than doubled in value since that investment.

Powered by WPeMatico

The Exchange spent a little time on Friday ruminating on the impact of then-rumored regulation in China targeting its edtech sector. News that the Chinese government intended to crack down further on the education technology market hit shares of public, China-based edtech companies. It was a mess.

Then over the weekend, the rumors became reality, and the impact is still being felt today in the global markets.

But there’s more. China is also bringing new regulatory pressure on food-delivery companies and Tencent Music. More precisely, we’ve seen successive market-dynamic-changing moves from the Chinese government in the last few days, coming as 2021 had already proved to be a turbulent environment for China-based technology companies.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Today we have to do a little bit of work to understand precisely what is going on with the various regulatory changes. Why? Because the Chinese venture capital market is a key player in the global venture scene. And Chinese startups have gone public on both Chinese, Hong Kong and U.S. exchanges; there’s a lot of capital tied up in companies impacted today — and possibly tomorrow.

For startups, the regulatory changes aren’t a death blow; indeed, many Chinese tech startups won’t be affected by what we’ve seen thus far. And upstart tech companies in sectors less likely to be targeted by central authorities may become more attractive to investors than they were before the regulatory onslaught kicked off. But on the whole, it feels like the risk profile of doing business in China has risen. That could curb the pace at which capital is invested, cut valuations and lower interest in the Chinese startup market from private-market investors able to invest globally.

Let’s parse what’s changed, examine market reactions and then consider what could be next. We want to better understand today’s Chinese startup market and what its new form could mean for existing players and future performance.

The edtech clampdown did not start last week. China’s edtech sector started to rack up penalties and fines in June, which led to what the Asia Times called “warning bells” in the sector. From there, things went from penalties to punishing regulatory changes.

Powered by WPeMatico

News that China’s government may force domestic tutoring-focused companies to go nonprofit is taking a huge bite out of the value of several technology companies. Bloomberg notes that the value of companies like New Oriental Education & Technology Group and TAL Education are tumbling in light of the news, which would constitute merely the latest salvo against tech companies in the autocratic country.

New Oriental’s Hong Kong-listed shares fell 44.22% in after-hours trading after the nonprofit news broke, while NYSE-shares of TAL are off an even sharper 51.75% in pre-market trading. With Yahoo Finance listing a roughly $13.8 billion market cap for TAL ahead of its impending declines at the market open, billions of equity value are about to get deleted. The list goes on: China Online Education Group is off 39.97% in after-hours trading, for example.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

A new decision by China’s government to exert more control over a sector of its domestic economy should not surprise. And we shouldn’t be shocked that online tutoring is in the country’s targets; today’s news is a follow-up to prior regulatory action in the sector from earlier in the year.

As China has become synonymous with edtech startups in recent years, the news impacts more than just public companies. The expected rules change may also hit a host of private, venture-backed companies.

As China has become synonymous with edtech startups in recent years, the news impacts more than just public companies. The expected rules change may also hit a host of private, venture-backed companies.

For example, what will happen to Yuanfudao? The company was valued at $15.5 billion last year, offering what TechCrunch described as “live tutoring, an online Q&A arm and a math-problem-checking arm.” Will the company see its wings clipped?

Or how about Zuoyebang, which raised $1.6 billion in a single round last year? TechCrunch wrote that Zuoyebang offers “online courses, live lessons and homework help for kindergarten to 12th grade students.” Is it in trouble as well?

All this comes on the same day that shares in Zomato began to float, with the Indian online food delivery company seeing its shares close up nearly 65% in their first day’s trading. TechCrunch has viewed the Zomato IPO as a possible bellwether for the larger Indian startup market, and the results augur well for other growth-focused, loss-making unicorns in the country.

Powered by WPeMatico

Last week was a good one for edtech in Europe.

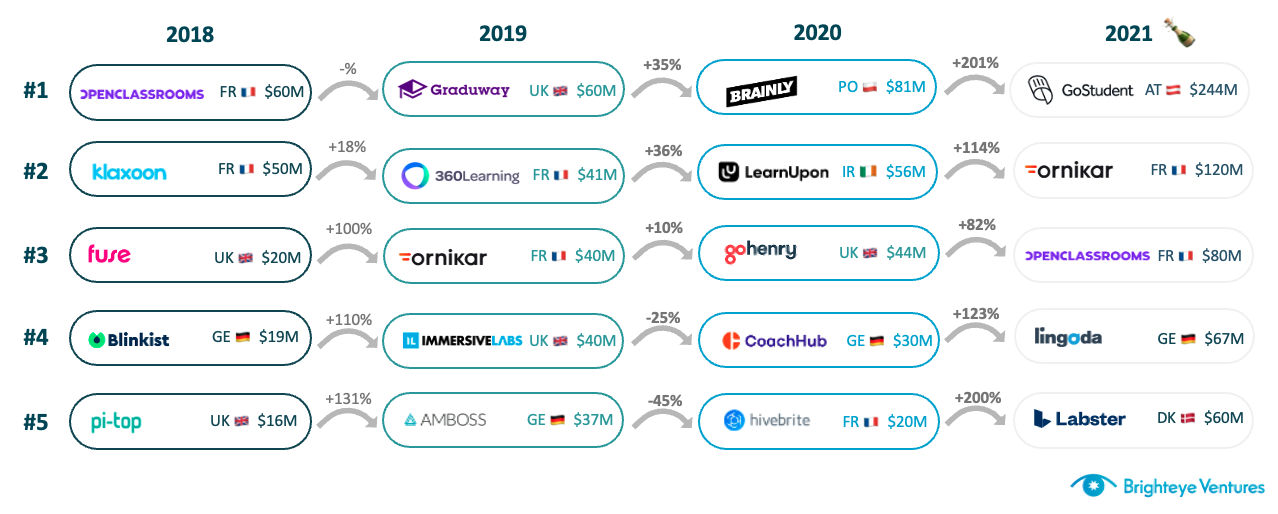

GoStudent became Europe’s first edtech unicorn (IPO’d companies aside), raising its third round in 12 months and the biggest ever in the sector in Europe. Brighteye Ventures’ analysis showed that VC investments in European edtech had breached $1 billion in a calendar year for the first time, even without GoStudent’s mega-round, with six months left to go.

Edtech deal flow in 2021 looks set to match or even outpace 2020 levels, per the report: At $9.4 million, average deal size is triple 2020 levels; seven companies have raised $50 million in five different markets; and the U.K. has more than three times as many deals as the next individual market.

Deal-size progression in edtech over the years. Image Credits: Brighteye Ventures

It’s interesting that we are not seeing enormous increases in deal count. The $1.05-billion mark in the report is spread across 111 transactions — there were 237 in 2020, so we could expect a similar total this year. More funding and stable deal count of course means that we are seeing significant increases in deal size.

It seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

We can draw a few conclusions from this. We can construe that companies created last year and in previous years matured significantly during the pandemic due to increased demand. Moreover, this rapid natural selection process provided insights on verticals and possible winners.

Lastly, it seems generalist investors are recognizing that edtech investments can reap outsized returns, similar to sectors like deep tech, health tech and fintech.

This is contributing to larger early rounds than we have seen in previous years — investors can’t pick the winner, but they can slant the playing field instead. We therefore expect to see a surge in the number of pre-seed, seed and Series A rounds in the second half of 2021, as companies founded during the pandemic begin to raise meaningful funding.

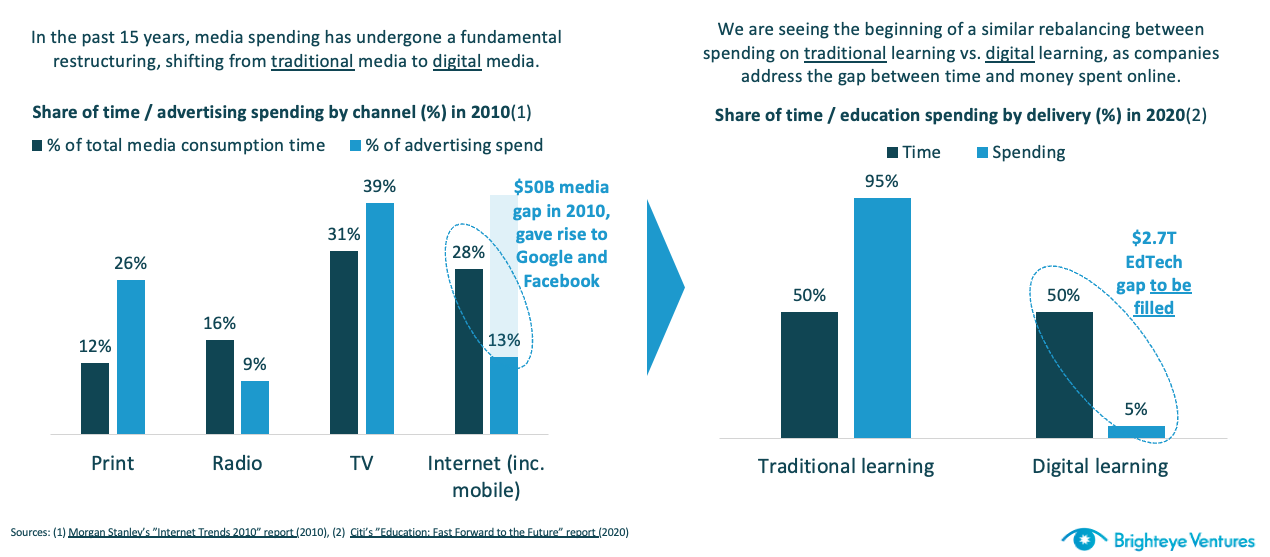

Another reason that edtech is being taken seriously by generalist investors is that the true size of the market (and the extent of digitization to come) is becoming more conceivable.

Edtech spending is growing like media spending did in the 2010s. Image Credits: Brighteye Ventures

Powered by WPeMatico

Duolingo filed to go public yesterday, giving the world a deep look inside its business results and how the pandemic impacted the edtech unicorn’s performance. TechCrunch’s initial read of the company’s filing was generally positive, noting that its growth was impressive and its losses modest; Duolingo recently began making money on an adjusted basis.

While the company’s top-level numbers are impressive, we want to go one level deeper to grow our understanding of the company beyond our EC-1.

Duolingo is likely entering a period in which it will have to invest heavily in features like pronunciation, efficacy and new apps — which could come at a steep upfront cost.

First, we’ll explore the growth of Duolingo’s total user base, how much money it makes per active user, and how effectively the company has managed to convert free users to paid products over time. The numbers will set us up to understand what else can be learned about Duolingo’s business beyond our original deep dive into the company’s finances — specifically underscoring the pressure cooker it finds itself in when looking for new revenue sources.

Starting with Duolingo’s growth in total active users, guess how fast they rose from 2019 to 2020. Hold that number in your head.

The actual numbers are as follows: In 2019, Duolingo closed the year with 27.3 million monthly active users (MAUs); it wrapped 2020 with 36.7 million MAUs. That’s a gain of 34%. If we narrow our gaze to Q1 2021 numbers compared to Q1 2020, we can see that Duolingo’s MAUs rose from 33.5 million to 39.9 million, or growth of around 19%.

The bulk of Duolingo’s growth, then, came in early 2020 when we consider its pandemic bump. Put more simply, the company scaled from 27.3 million MAUs at the end of 2019 to 33.5 million MAUs at the end of Q1 2020; from then, the company added 3.2 million more MAUs throughout 2020 and 6.4 million during the next four quarters.

Another lens through which to view the numbers is simply a recognition that first-quarter results at Duolingo appear to be stronger than results in the rest of the year, perhaps due to New Year’s resolutions to learn a new language or brush up on a second language learned in high school.

Next, let’s examine Duolingo’s monetization efforts regarding converting free users to paying users.

Here we can see a very different growth story. While the company’s MAUs rose 34% from 2019 to 2020, the company’s paying users rose from 900,000 at the end of 2019 to 1.6 million at the end of 2020. That is a far sharper gain of 84% on a year-over-year basis.

So, while Duolingo did see material user growth during 2020, it saw turbocharged expansion in the users it was able to shake revenue from. Improved monetization, more than acceleration in user growth, was the pandemic’s effect on Duolingo.

What can we see in the company’s more recent results? From Q1 2020 to Q1 2021, Duolingo’s paid subscribers rose from 1.1 million to 1.8 million, a gain of around 64%. That was a slower pace than the company managed more generally in 2020, which matches Duolingo’s slower revenue growth in Q1 2021 than it recorded in 2020.

The number is still strong, we think. But not as impressive as the more than 100% revenue expansion that the company put on the board last year.

In percentage terms, 3.3% of Duolingo’s MAUs were paid subscribers in 2019. That figure rose to 4.4% in 2020. And in Q1 2021, it reached 4.5%. Duolingo rounds that number to 5% in its S-1, which feels somewhat aggressive to us, given the somewhat modest pace at which the metric is improving. Here’s the wording:

As of March 31, 2021, approximately 5% of our monthly active users were paid subscribers of Duolingo Plus. Our paid subscriber penetration has increased steadily since we launched Duolingo Plus in 2017 and, combined with our user growth, has led to our revenue more than doubling every year since.

A gain of 0.1 percentage point in a quarter is growth, we suppose.

Next, let’s chat about revenue per MAU. To get consistent numbers, we’ll divide quarterly revenues by MAU figures from the same period. So, we’ll compare Q4 2019 revenue at Duolingo with its year-end MAU figure. We’ll do the same for 2020, and for Q1 2021 we’ll use both numbers from that period.

Powered by WPeMatico

ApplyBoard, a startup that helps international students find opportunities to study abroad, announced today that it has nearly doubled its valuation in a little over a year. The Ontario-based company is now worth around $3.2 billion after raising a $300 million Series D round led by the Ontario Teachers’ Pension Plan Board.

Startups that help students navigate institutional bureaucracy so they can get more value out of their educational experience may become a growing focus for investors as consumer demand for virtual personalized learning increases.

ApplyBoard makes money from revenue-sharing agreements with colleges and universities. If a student attends a college after using their services, ApplyBoard receives a cut of the tuition. Meanwhile, the service, which helps students search and apply to schools, is free to use.

Co-founder and CEO Martin Basiri did not share specifics on revenue, but he confirmed that his company is growing its sales at a 400% year-over-year rate in 2021. For context, sales in 2019 hit $300 million, meaning that ApplyBoard is making at least $1.2 billion in sales this year.

These figures violate the prevailing edtech narrative from last year: Higher ed is dead! Students don’t want to attend college anymore. Bring back the gap year, but make it permanent!

Instead, this company is proving that the university tech stack is more lucrative than many assumed, especially if you look beyond content offerings and into back-end marketing support.

My take: Startups that help students navigate institutional bureaucracy so they can get more value out of their educational experience may become a growing focus for investors as consumer demand for virtual personalized learning increases.

ApplyBoard’s recent fundraising efforts shed a light on its strategy to become, effectively, a tech-savvy guidance counselor for the approximately 200,000 students that it has served to date.

The company raised a $55 million extension round in September to bring on a partner, Education Testing Services (ETS) Strategy Capital, the venture arm of the world’s largest nonprofit education testing and assessment organization. ETS helps administer the TOEFL English-language proficiency test and the GRE graduate admissions test.

The synergies there led ApplyBoard to launch ApplyProof, a service that helps admissions and immigrant officers verify documents that international students need to apply to colleges around the world. Today’s financing event similarly brings in a strategic investor, Ontario Teachers’ Pension Plan.

“The demand remains high post-pandemic and we continue to see a strong, pent-up demand from students wishing to study abroad,” Basiri said. “Students want a seamless and pain-free application process and be able to have all the information they need to make an informed decision.”

Powered by WPeMatico

After years in the backwaters of venture capital, edtech had a booming 2020. Not only did its products become must-haves after schools around the globe went remote, but investors also poured capital into leading projects. There was even some exit activity, with well-known edtech players like Coursera going public earlier this year.

But despite a rush of private capital — which has continued into this year, as we’ll demonstrate — edtech stocks have taken a hammering in recent weeks. So while venture capitalists and other startup investors are pumping more capital into the space in hopes of future outsize returns, the stock market is signaling that things might be heading in the other direction.

Who’s right? One investor that The Exchange spoke to noted that market turbulence is just that, and that he’s tuning into activity but not yet changing his investment strategy. At the same time, the recent volatility is worth tracking in case it’s a preview of edtech’s slowdown.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Let’s look at the changing value of edtech stocks in recent months, parse some preliminary data via PitchBook that provides a good feel for the directional momentum of edtech venture capital, and try to see if there’s irrational exuberance among private investors.

You could argue that it’s public investors who are suffering from irrational pessimism and that private-market investors have the right of it. But since public markets price private markets, we tend to listen to them. Let’s go!

We’re sure that you want to get into the private-market data, so we’ll be brief in describing the public-market carnage. What follows is a digest of edtech stocks and their declines from recent highs:

Powered by WPeMatico

Education may well be the most important activity we conduct as a society — and it may also be the hardest space to build a startup in. Selling to school districts and universities is notoriously difficult, but enticing consumers is even harder. Learning takes focus, patience, tenacity and resources, and most consumers would prefer to watch some lip-sync videos on TikTok than stare at math equations (not to mention that such entertainment is free). Engagement and education feel aggressively at odds, which limits the way that startups can scale and succeed.

Yet, the revulsion VCs have traditionally had for the space has slowly dissipated over the past 10 years. Consumer and enterprise startups in edtech are increasingly attracting funding, and there is a growing crop of edtech-focused investors who are betting big on the future here. What’s changed isn’t the market or its potential, but rather the perception that ambitious and sustainable companies can truly be built in education.

One of the companies that has led the charge in transforming those perceptions is Pittsburgh-based Duolingo. It’s a language-learning app that has caught fire. From humble origins a decade ago as a translation platform for news agencies, it’s now used by 500 million people across the world to learn Spanish, English, French and more, all while generating bookings of $190 million in 2020. It’s a smashing success, but a success that was hard earned after a years-long effort of product and revenue experimentation to find its current niche.

TechCrunch’s writer and analyst for this EC-1 is Natasha Mascarenhas. Mascarenhas has been covering edtech from the very first day she joined TechCrunch as a venture capital and startups writer, and she has built up a reputation as a fearless chronicler of this increasingly vital ecosystem. The lead editor of this package was Danny Crichton, the copy editor was Richard Dal Porto, and illustrations were created by Nigel Sussman.

Duolingo had no say in the content of this analysis and did not get advance access to it. Mascarenhas has no financial ties to Duolingo or other conflicts of interest to disclose.

The Duolingo EC-1 comprises four main articles numbering 12,200 words and a reading time of 48 minutes. Here’s what’s in store:

And finally, note that Duolingo CEO and co-founder Luis von Ahn is coming to Disrupt, so make sure to grab your tickets because the conversation will continue there.

We’re always iterating on the EC-1 format. If you have questions, comments or ideas, please send an email to TechCrunch Managing Editor Danny Crichton at danny@techcrunch.com.

Powered by WPeMatico