EC Ecommerce and D2C

Auto Added by WPeMatico

Auto Added by WPeMatico

Mayfield partner Navin Chaddha and Poshmark founder and CEO Manish Chandra met all the way back in 2003, well before Poshmark was even a glimmer in his eye. They stayed connected over the years, through Chandra’s sale of his startup Kaboodle to Hearst and after he left.

At a breakfast one morning, Chandra told Chaddha he was going to try to do everything from his iPhone for the next six months.

Over the course of that time, the idea for Poshmark started to percolate into something more concrete. Chandra, following Kaboodle, knew he wanted to do several things differently. The first was create an engagement and revenue model that was symbiotic, rather than starting with engagement and having to build out a business model later. He also knew he wanted to start with people first, and build a founding team that had deep DNA in the fashion world to pair with his technical background.

He met Tracy Sun, brought her on, and got to work.

This was back in 2011, and Chandra was absolutely adamant that he wanted Poshmark to be an app, not a website. So adamant, in fact, that during beta he actually provided 100 users with video iPods. (He recalled that he only got 20% of them back.)

“Lead with love, and the money comes.” It’s one of the cornerstone values at Poshmark. The company practiced that early on by holding IRL, and then virtual, parties, allowing users to show each other their wares and create an engagement cycle that offered instant gratification. The user base grew from 100 to 150 to 1,000 and so on.

“We still to this day use a similar kind of strategy in a much more compressed timeframe as we go to different countries,” said Chandra. “We focus on building the community first and then scale that community.”

Chaddha and Mayfield led the company’s Series A deal a decade ago. On the latest episode of Extra Crunch Live, Chandra and Chaddha sat down with us and walked us through that original Series A pitch deck (which you can check out below). They also participated in the Pitch Deck Teardown, giving their expert feedback on decks submitted by the audience. If you’d like your deck to be featured on a future episode of Extra Crunch Live, hit up this link.

Time stamp — 11:00

Poshmark was built on a couple fundamental premises. The first was that the iPhone would transform the way we do just about everything. The second was more pointed: That fashion, at the time underserved by technology, was a discovery process over a direct search process. A decade ago, Chandra envisioned a fashion marketplace that mimicked shopping in the real world — walk into a shop and let natural attraction do its thing — without holding any inventory.

Powered by WPeMatico

We’ve reached the end of Y Combinator’s biggest Demo Day, which saw more than 300 companies pitching back-to-back over eight hours.

Earlier, we highlighted some of the companies that caught our eye in the first half of the day. Now we’re back with our favorite companies from the second half. From a marketplace to help you resell formalwear to a startup that offers self-driving street cleaners, it’s quite the mix.

If you’d like to browse all of the companies from this batch YC has a catalog of publicly-launched W21 companies here.

Heading into this particular demo day, I had my eyes peeled for startups focused on delivering services via an API instead of offering managed software. Happily, there have been a number to dig into, including Pitbit.ai, Bimaplan, Enode and Terra.

Terra stood out to me because it solves a problem I care deeply about, namely fitness data siloization. My running data is stuck in one app, biking data in another, and my weight-lifting data is stuck in my head, though I doubt Terra has an API for that interface quite yet.

What Terra does is permit fitness app developers to better connect their services, which permits the sharing of data back and forth. Presenters likened their startup to Plaid — a popular thing to do in recent quarters — saying that what the fintech startup did for banking data, Terra would do for fitness and health information.

Getting developers to sign on will be tricky, as I presume all of the apps I use in an exercise context would prefer to be my main workout home. But I don’t want that, so here’s hoping Terra realizes its vision.

— Alex

Calling itself “Shopify for beauty and wellness” in Latin America, AgendaPro wants to help small businesses in the region book customers online and collect payments.

The company’s idea isn’t as radical as some companies that we heard from today — Carbon capture! Faster drug discovery! — but the company did share several metrics that made us sit up. First, AgendaPro has reached $152,000 in MRR, or just over $1.8 million in ARR. And representatives shared that its gross margins are 89%. As far as software margins goes, that’s pretty damn good.

The startup has more than 3,000 merchants using its service at the moment, and it claims that there are more than four million businesses that it could service. If AgendaPro can get software and payments revenues from even a respectable fraction of those companies, it will be a big, big business. And who doesn’t love vertical SaaS?

— Alex

One of the holy grails of biochemistry is a programmable DNA machine. These tools can essentially “code” a molecule so that it reliably sticks to a specific substance or cell type, which allows a variety of follow-up actions to be taken.

For instance, a DNA machine could lock onto COVID-19 viruses and then release a chemical signal indicating infection before killing the virus. The same principle applies to a cancer cell. Or a bacterium. You get the picture — and it looks like Atom Bioworks has something a lot like this.

Powered by WPeMatico

Non-fungible tokens (NFTs) offer new ways for consumers to collect, wear and trade fashion online, and now that most fashion shows have scaled back or gone virtual, they may become an important tool for the industry.

Because some of the most profitable NFTs are produced by celebrities with teams, it makes sense that music corporations, fashion brands and designers are venturing into the NFT market as well. Just this month, sneaker brand RTFKT Studios garnered $3.1 million in seven minutes by selling crypto collectibles. In December 2020, NFT startup Enjin partnered with Netherlands-based fashion house The Fabricant on a virtual collection. Real-life fashion brands use NFTs for marketing in virtual worlds like Minecraft, plus several Atari and Microsoft video games.

The fundamental value NFTs offer to bridge virtual fashion items with video games is the option to secure custody of the item for use in other games or mobile apps.

“Brands are coming up with some creative solutions because the pandemic is persistent, and fashion is something that is so close to our identities,” said Bryana Kortendick, Enjin’s VP of operations and communications. “You can snap a photo of yourself wearing your Atari-branded NFTs. You’ll also be able to wear them in video games.”

Breakout NFT star Beeple said he imagines a future where fashion NFTs could be redeemed for specific items in physical stores, especially at luxury retailers like his former client Louis Vuitton.

“You can relate NFTs to clothing in new and interesting ways,” he said. “This will be seen as the next chapter of digital art history. This is a continuation of digital art history that started decades ago, by that I mean art made on a computer and distributed through the internet.”

Fashion designers like Schirin Negahbani are already creating NFTs that represent actual clothing. Precisely because multimillion-dollar NFT sales are breaking records, spectators have been prompted to question the role speculative trading plays in this trend.

Textile designer Amber J. Dickinson says fashionable NFTs shouldn’t primarily be viewed as speculative trading opportunities. “The way I think fashion translates to the digital world is to view an NFT as a collectible piece of the garment for history,” said Dickinson, known for hand-made silk scarves and her work with Alexander McQueen. “I would only buy art as a piece that I liked. Whether digital or in the real world, I don’t take an investor’s point of view.”

There are many fashion fans who disagree with Dickinson, preferring to invest through assets like Birkin bags. They may have a different approach to NFTs. The DIGITALAX crypto fashion platform, for example, is being built with a plethora of trading features. As for Dickinson, she said she is still looking for her tribe of crypto-savvy artists on Twitter.

Powered by WPeMatico

Another day brings another pubic debut of a multibillion dollar company that performed well out of the gate.

This time it’s Coupang, whose shares are currently up just over 46% to more than $51 after pricing at $35, $1 above the South Korean e-commerce giant’s IPO price range. Raising one’s range and then pricing above it only to see the public markets take the new equity higher is somewhat par for the course when it comes to the most successful recent debuts, to which we can add Coupang.

The company’s mix of rapid growth and slimming deficits appear to have found an audience among public money types, so let’s quickly explore the price they paid. What was the company worth at its IPO price, and what is worth now? And, of course, we’ll want to calculate revenue run rates for each figure.

Oh — we’ll also need to calculate how much money SoftBank made. Inverted J-Curve indeed!

As Renaissance Capital notes, Coupang boosted its share allocation to 130 million shares from 120 million. This made the value of both primary and secondary shares in its public offering worth a total of $4.55 billion. That’s a lot of damn money.

At its IPO price of $35, the same source pegged the company’s fully diluted IPO valuation at $62.9 billion. By our accounting, the company’s simple valuation at its IPO price came to $60.4 billion. Those numbers are close enough that we’ll just stick with the diluted number out of kindness to the company’s fans.

Doing some quick math, Coupang is worth around $92 billion at the moment. That’s a huge number that nearly zero companies will ever reach. Some do, of course, but as a percentage of startups that start it’s an outlier figure.

Powered by WPeMatico

Another day, another venture-backed IPO filing. Today it’s ThredUp, a used-goods marketplace that is approaching the public markets in the wake of Poshmark’s own strong debut.

Both companies have a related market focus, albeit different approaches to selling used goods. Poshmark allows users to sell clothing items through its app. ThredUp, in contrast, acquires goods from users and sells them itself.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

But while Poshmark had profits to brag about in its own IPO filing, ThredUp does not and is also growing more slowly, expanding revenues just 13.6% in 2020. Reading its S-1 filing, it’s clear ThredUp did not have the best 2020, thanks in part to COVID-19.

This morning, let’s get into the numbers posted by the company backed by Trinity Ventures, Redpoint, Highland Capital Partners and Goldman Sachs to decide if it’s just merely to catch Poshmark’s wave, or if its business is a fine machine in its own right.

To understand ThredUp’s business, we have to get into the mechanics of how it sells things. The company has two methods: direct sales and consignment. In the former, ThredUp buys goods and sells them. It then “recognize[s] revenue on a gross basis” and generates gross profit after deducting “inventory cost, inbound shipping and inventory write-downs, as well as outbound shipping, outbound labor and packaging costs.”

That is the model that ThredUp is leaving behind. After shifting to “primarily consignment sales” in 2019, the company’s business has skewed sharply in that direction. Consignment works by having consumers send ThredUp their goods, which it holds, and perhaps sells, remitting to the user a portion of the sale price. The method reduces write-downs and boosts gross margins.

Consignment sales at ThredUp “recognize revenue net of seller payouts,” deducting “outbound shipping, outbound labor and packaging costs” to reach gross profit results.

The revenue-mix focus change can be seen in how ThredUp generated gross profit in 2018, 2019 and 2020. In those years, consignment gross profit came to 38%, 67% and 81% of total gross profit. ThredUp’s business today is effectively a large, digital consignment effort.

What impact has that shift had on the company’s financial health? Let’s find out.

ThredUp posted $129.6 million in 2018 revenue, a figure that grew to $163.8 million in 2019 and $186 million in 2020. The company’s growth slowed from 26.4% in 2019 to 13.6% in 2020, a sharp deceleration. But at the same time, the portion of ThredUp revenues that came from consignment sales grew to 74% from 60%. Did that change have a material impact on the company’s gross margins, thus rendering its slow growth more palatable?

Not really. The company’s gross margins came to 68.7% in 2019 and 68.9% in 2020. That’s about as flat as Texas. And notably the number stayed flat despite the company noting that consignment revenues had stronger gross margins in 2019 and 2020 (77% and 75%, respectively) than its other model (57% and 51%, respectively).

Powered by WPeMatico

Earlier today, South Korean e-commerce and delivery giant Coupang filed to go public in the United States. As a private company, Coupang has raised billions, including capital from American venture capital firm Sequoia and Japanese telecom giant SoftBank and its Vision Fund.

Coupang’s revenue growth is nothing short of fantastic.

Coupang’s offering, coming amidst the public debut of a number of well-known technology brands, will be a massive affair. Its first S-1 filing indicates that its IPO will raise capital in the range of $1 billion, far larger than the $100 million placeholder that is more common.

But the company’s scale makes its lofty IPO fundraising goals reasonable. Coupang is huge, with revenues north of $10 billion in 2020 and in improving financial health as it scales. And its revenue growth has accelerated.

Perhaps that explains why the company is reportedly targeting a valuation of $50 billion.

This afternoon, let’s dig into the company’s historical growth, its improving cash flow and its narrowing losses. Coupang’s debut will create a splash when it lands, so we owe it to ourselves to grok its numbers.

And as there are other e-commerce brands with a delivery function waiting in the wings to go public — Instacart comes to mind — how Coupang fares in its IPO matters for a good number of domestic startups and unicorns.

The company’s growth across the last half-decade is impressive. Observe its yearly revenue totals from 2016 through 2020:

Sure, some of that 2020 growth is COVID-19 related, but even taking that into account, Coupang’s revenue growth is nothing short of fantastic. And what’s better is that the company has cut its losses in recent years:

Powered by WPeMatico

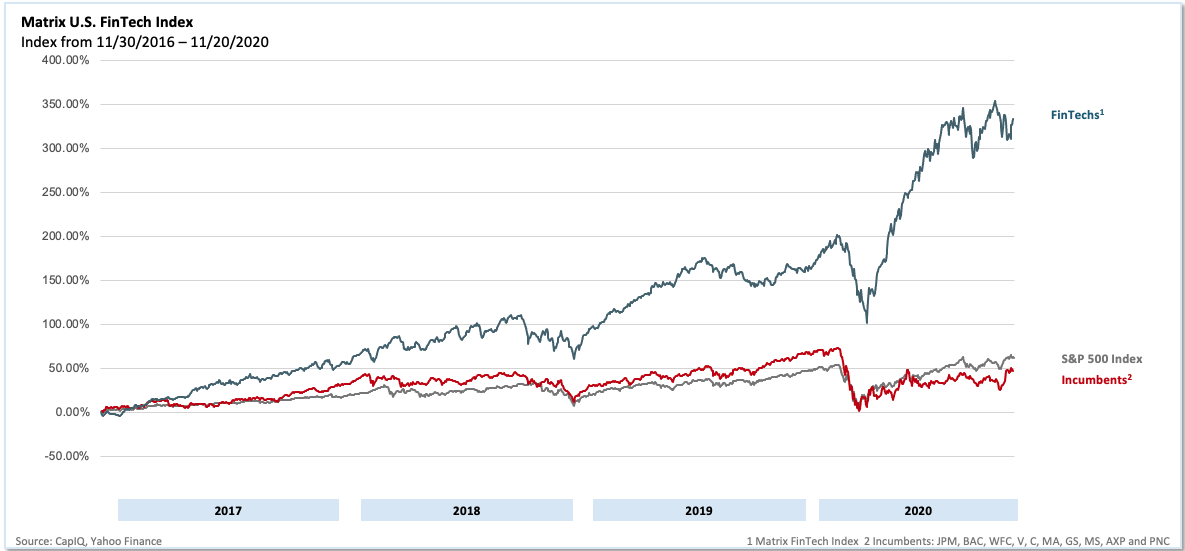

Three years ago, we released the first edition of the Matrix Fintech Index. We believed then, as we do now, that fintech represents one of the most exciting major innovation cycles of this decade. In 2020, all the long-term trends forcing change in this sector continued and even accelerated.

The broad movement away from credit toward debit, particularly among younger consumers, represents one such macro shift. However, the pandemic also created new, unforeseen drivers. Among them, millennials decamped from their rentals in crowded cities to accelerate their first home purchases to the benefit of proptech companies and challenger mortgage players alike.

E-commerce saw an enormous acceleration in growth rates, furthering adoption of online payments platforms. Lastly, low interest rates and looming inflation helped pave the way for the price of Bitcoin to charge toward $30,000. In short, multiple tailwinds combined to produce a blockbuster year for the category.

In this year’s refresh of the Matrix Fintech Index, we’ll divide our attention into three parts. First, a look at the public stocks’ performance. Second, liquidity. Third, we highlight one major trend in the sector: Buy Now Pay Later, or BNPL.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index. While the underlying performance of these companies was strong, the pandemic further bolstered results as consumers avoided appearing in-person for both shopping and banking. Instead, they sought — and found — digital alternatives.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index.

Our own representation of the public fintechs’ performance is the Matrix Fintech Index — a market cap-weighted index that tracks the progress of a portfolio of 25 leading public fintech companies. The Matrix fintech Index rose 97% in 2020, compared to a 14% rise in the S&P 500 and a 10% drop for the incumbent financial service companies over the same time period.

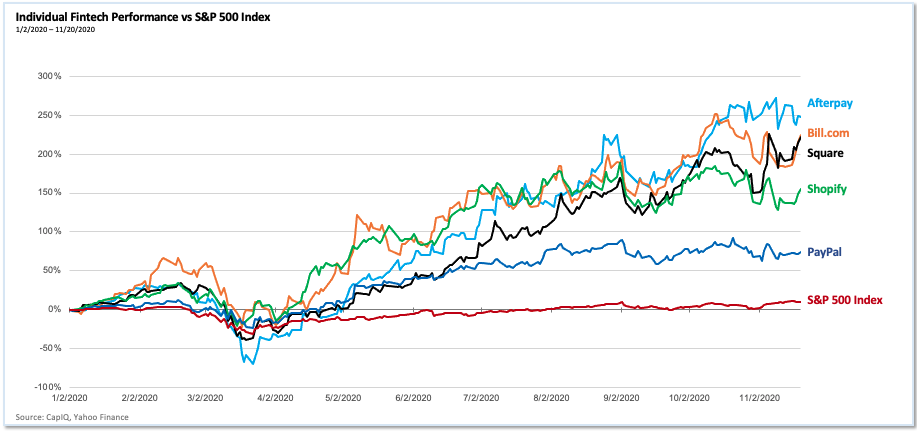

2020 performance of individual fintech companies vs. SPX Image Credits: CapiQ, Yahoo Finance

Matrix U.S. Fintech Index, 2016 -2020 Image Credits: CapiQ, Yahoo Finance

E-commerce undoubtedly stood out as a major driver. As a category, retail e-commerce grew 35% YoY as of Q3, propelling PayPal and Shopify to add over $160 billion of market capitalization over the year. For its part, PayPal in the third quarter signed up 15 million net new active accounts (its highest ever).

Powered by WPeMatico