EC Consumer Applications

Auto Added by WPeMatico

Auto Added by WPeMatico

If we are not careful, every entry of this column could consist of SPAC news.

Special purpose acquisition companies, or blank-check companies, whatever you prefer to call them, are enormous business today. But they aren’t the only thing going on, and we’ll get to other things shortly. Consider this an apology for having written about SPACs twice in two days.

Yesterday, we considered the rise of the VC-led SPAC and whether venture capital groups that offer seed-through-SPAC money will wind up with advantage in the market over firms that specialize on any particular startup stage. Sticking to the blank-check theme, this morning we’re looking into two SPAC-led deals, namely those involving Rover and MoneyLion.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

We’re doubling up to prevent more SPAC-related posts. And we’ve selected Rover because Chewy, another pet-themed entity, is an already-public company. As both were venture-backed, we may be able to contrast their trading performance post-debut. Sadly, Chewy is focused on pet e-commerce while Rover is more centered around pet services, but they may prove close enough for some loose comparisons.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup, one that TechCrunch has covered extensively. If its SPAC-assisted vault into the public markets goes well, it could smooth the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised capital.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup, one that TechCrunch has covered extensively. If its SPAC-assisted vault into the public markets goes well, it could smooth the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised capital.

So this is a SPAC post, but as we’ll largely be looking at the financial health of two companies that we’ve heard about for ages and never got to see inside of, I hope you join me all the same.

We’re starting with the Rover investor presentation, before zipping over to MoneyLion’s own.

Rover is merging with Nebula Caravel Acquisition Corp., which is affiliated with True Wind Capital. The deal gives Rover an anticipated market cap of around $1.6 billion, with around $300 million in cash on its books.

So, how attractive is this new unicorn? You can find its investor deck here, if you want to read along as we peek.

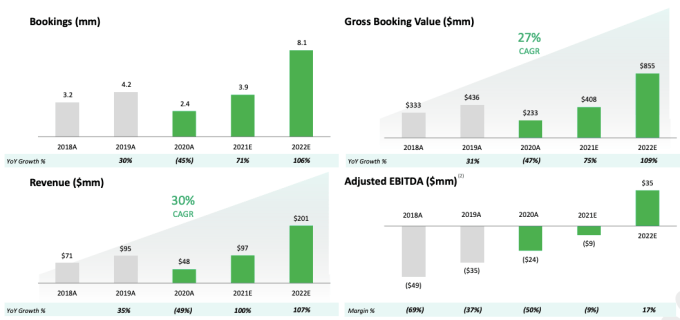

First up, the company stresses rising use of digital services in the last year thanks to the pandemic and the fact that pet ownership is growing. Both of which are true. We’ve seen the accelerating digital transformation for both companies and consumers. And if you’ve tried to adopt a pet lately, you’ve seen how few are left waiting for forever homes.

With those things behind it, you might be wondering why Rover is pursuing a SPAC-led debut as well. If its market is hot and it has previously raised venture capital, why not just go public via an IPO? Because 2020 was tough on the company.

Image Credits: Rover

Revenue dipped from $95 million in 2019 to just $48 million last year. Bookings fell from 4.2 million to 2.4 million over the same time frame, leading to gross booking value falling from $436 million in 2019 to $233 million in 2020. Why? Because everyone was stuck at home. With their pets. A situation that limited demand for Rover-delivered pet services.

Powered by WPeMatico

Metromile began trading as a public company yesterday. Its exit from the private market was accelerated by its decision to combine with a special purpose acquisition company, or SPAC.

Such transactions have exploded in popularity in recent years, bridging the gap between a host of richly valued private companies and endless bored capital. SPACs raise cash, go public and then merge with a private entity. The SPAC then dissolves itself into the combined entity, a process that often includes an additional slug of money (PIPE) for good measure.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

SPAC-led debuts can move faster than a traditional IPO, making them attractive to companies in a hurry. And with more visibility into how much capital might be raised than during a traditional public-offering pricing run, they can smooth worries amongst target-companies regarding how much cash they can attract by leaving the private-market fold.

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

But with many more SPACs coming our way, we took Metromile’s debut as a learning moment. To that end, we got on the horn with CEO Dan Preston to chat about what the day meant for his company, and to elicit a note or two on the SPAC process for our own enjoyment.

TechCrunch asked Preston about the SPAC world and how his combination came about. He said his firm started by dipping its toe into the blank-check waters, kicking off with a small set of conversations, chats that quickly gathered traction.

But don’t take that to mean that any company will elicit a similar market response. Preston said SPACs are designed for a specific class of company; namely those that want or need to share a bit more story when they go public. Younger companies, in other words, for whom a traditional S-1 filing might not be provide a sufficient summation of its potential.

Powered by WPeMatico

The IPO frenzy is not letting up, Bumble informed the world this morning.

Per a new SEC filing, the dating company raised its target IPO price range, indicating that its previous attempt to quantify its per-share value was an undershoot. This means we’ll need to calculate a host of new valuations and revenue multiples for the company.

But more than that, we have a question to answer: Is Bumble aiming for a Match.com price, despite not being as profitable as its already-public rival? The last time we covered the pair, Bumble’s implied revenue multiples were discounted compared to Match, but with this new price, has the smaller company gained ground?

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

And if so, does it mean that we’re seeing more public market enthusiasm for private companies? We’ll find out.

When it comes to the frenetic demand for IPO shares from public investors, I am reminded of a particular Dilbert. In this particular strip, Wally gets fired and is then hired back as a consultant. People outside the company appear smarter, he said, so he’s now back and getting paid more money than before.

This, but for private companies going public. Some companies appear to have huge promise while private, only to fizzle slowly while public. Or they manage huge price gains during their IPO process, only to cede those wins after they have a few trading months under their belt.

Is that what’s going to happen with Bumble?

Bumble targeted a $28 to $30 per-share IPO price when it first set a range, implying a greater than $1 billion raise. Now the company is selling more shares at an even higher price. From 34.5 million shares to 45 million, and at a new $37 to $39 per share price range, Bumble could raise $1.66 billion to $1.76 billion in its IPO.

And that’s not counting its underwriters’ option of 6.75 million shares, which might bring its total raise to $2.02 billion at the top end of its new pricing interval.

What is Bumble worth at those new prices? Using its simple, shares-outstanding post-IPO count of 112,745,301 — inclusive of its underwriters’ option — the company would be worth $4.17 billion to $4.4 billion.

Powered by WPeMatico