ec china

Auto Added by WPeMatico

Auto Added by WPeMatico

China is becoming a superpower in the tech industry. According to Straits Times, China is the only place in the world where it takes less than six years for a startup to become a unicorn — it takes seven years in the U.S., eight years in the U.K. and 11 years in Germany. Despite geopolitical tensions and recent amendments in CFIUS, it is hard to ignore China.

When I joined Runa Capital almost a year ago, my task was to help our portfolio companies enter the Chinese market, find the right partners and raise funding from Chinese investors. And almost on every call with our startups, colleagues from Runa or other global VCs, I heard: Is it a good idea to raise from a Chinese VC? Is it OK to co-invest with Chinese investors? I was surprised to learn that there is little research answering such questions, as there is a lack of adequate information in English about Chinese investments.

Access to the Chinese market seems to be an obvious reason to invite Chinese funds aboard, but only about 20% of Western startups with Chinese capital have operations in China.

So as a Mandarin-speaking specialist, I decided to fill this gap by conducting a study based on Chinese VC database ITjuzi (the Chinese version of Crunchbase) with the help of our powerful data science resources developed by Danil Okhlopkov.

Below, I will try to answer the following questions using statistics and a case-based approach:

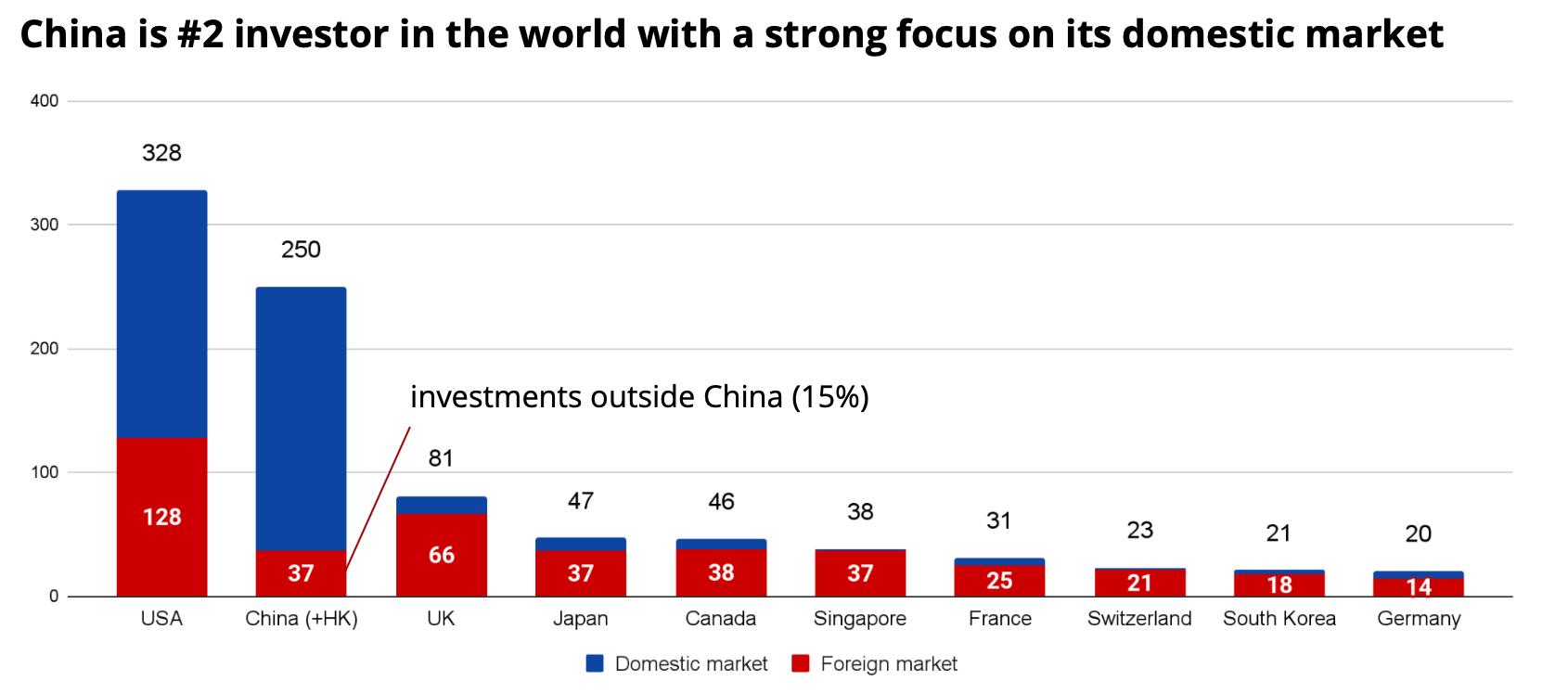

After studying data from ITjuzi, we estimated that Chinese funds invested around $250 billion in 2020 (three times higher than the figure reported in Crunchbase). This figure puts Chinese VC investments only 30% lower than investments by U.S. funds, but three times that of U.K. funds and 12.5 times more than German funds.

Fig. 1 — Comparison of investment from different countries in 2020, $bn. Source: Crunchbase, ITjuzi. Image Credits: Denis Kalinin

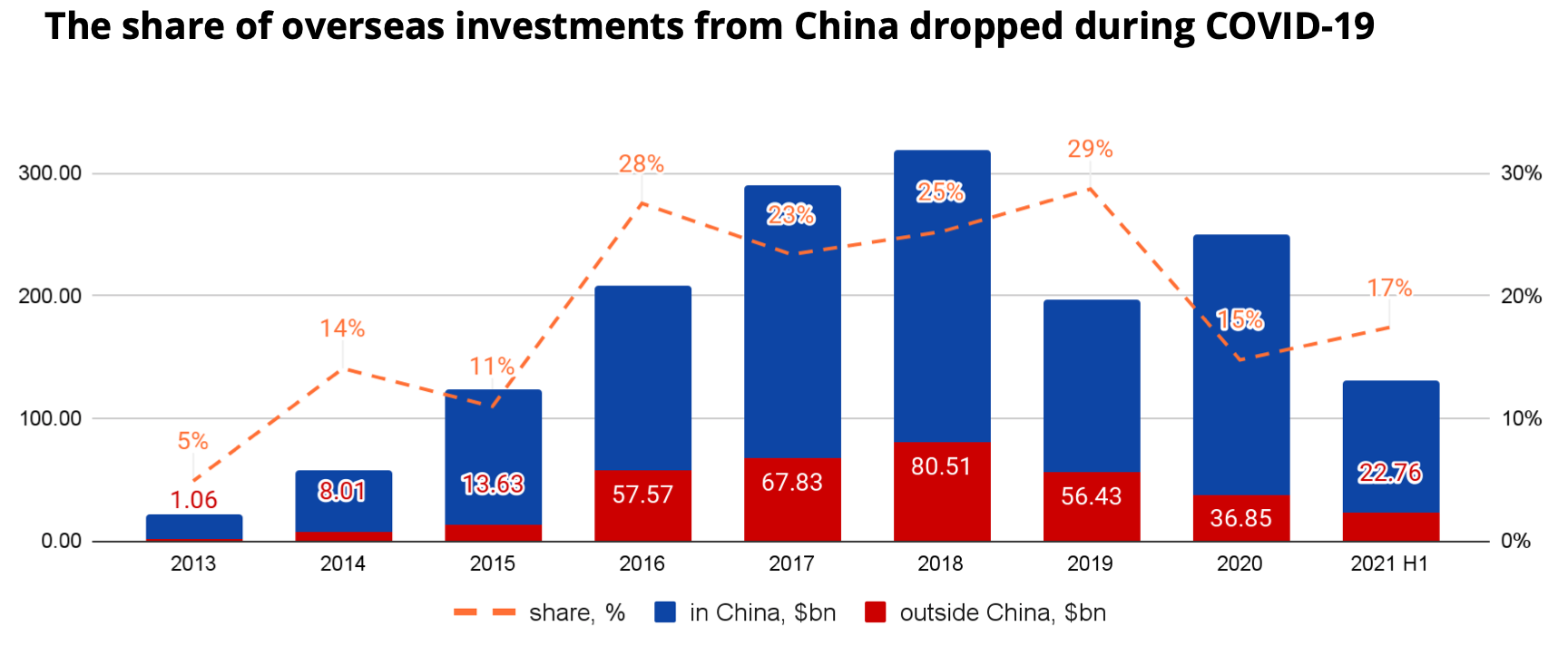

However, only 15% of investments in 2020 and 17% of investments in the first half of 2021 were in companies outside China, significantly lower than in 2019. This appears to be because during COVID, China’s economy recovered much faster than other countries’, so many Chinese investors preferred to redirect their capital flows to the domestic market.

On the other hand, there is great potential for overseas investments to rebound as soon as the borders reopen and the global economy starts to recover.

Fig. 2 — Dynamics of Chinese investments. $bn. Source: Crunchbase, ITjuzi. Image Credits: Denis Kalinin

We can also see that Chinese investors are eyeing European startups favorably, which is related to U.S.-China geopolitical tensions as well as the fact that the European VC market is becoming mature.

Powered by WPeMatico

China’s technology scene has been in the news for all the wrong reasons in recent months. In the wake of the scuttling of Ant Group’s IPO, the Chinese government has gone on a regulatory offensive against a host of technology companies. Edtech got hit. On-demand companies took incoming fire. Ride-hailing? Check. Gaming? You bet.

The result of the government fusillade against some of the best-known companies in China was falling share prices. The damage topped $1 trillion among just public Chinese companies listed abroad.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

What about startups in sectors that were reformed overnight? If their public comps are any indication, even more wealth was deleted in the recent wave of crackdowns.

The Exchange was curious about the impact of the Chinese government’s actions on the venture capital market. The Chinese startup economy has produced a number of world-leading companies. Tencent and Alibaba, yes, and even Baidu have become well-known for a reason. Could regulatory changes shake up the venture model that helped grow the country’s largest tech concerns?

After we checked in on the same question this Monday, SoftBank provided a partial answer, noting yesterday that it is pausing investments in China. The Japanese teleco, conglomerate and investing powerhouse has been deploying capital at a rapid pace in recent weeks. That will slow, at least in China. Here’s the WSJ:

The regulatory initiative in China has become so unpredictable and widespread that SoftBank and its funds are planning to hold off on investing much more there until the risks become clearer, [SoftBank CEO Masayoshi Son] said at an earnings press conference in Tokyo.

Is SoftBank early to its decision to shake up its investing strategy, missing Chinese deals for some time? Or is it late? We secured data from PitchBook and Traxcn that paints a somewhat surprising picture of venture capital activity at least thus far in Q3 2021.

But first, a reminder of how well China’s venture capital market was performing as 2020 eased its way into 2021.

But first, a reminder of how well China’s venture capital market was performing as 2020 eased its way into 2021.

China had a reasonably good Q2 2021 despite the turmoil.

Sure, funding flowing into Chinese startups was down 18% compared to Q4 2020, per CB Insights, but that quarter had recorded an all-time high of $27.7 billion. With $22.8 billion raised, Q2 2021 still did better than every other quarter since Q2 2016 with the exception of Q2 2018, Q4 2020 and Q1 2021. Indeed, the ecosystem had started to cool down in late 2018 before picking up pace again at the end of 2020.

However, that’s only one way to look at the numbers. If you compare recent Chinese venture results with other regions, it underperformed. During Q2 2021, U.S. funding reached a new high of $70.4 billion, with places like Latin America, Canada and India also establishing new records.

This also means that China lost ground as to its share of global startup deal-making, and the same goes for unicorn creation. According to Tech Buzz China’s summary of CB Insights data, the U.S. accounted for 132 unicorn births between January 1 and June 16, 2021, compared with just three in China.

Slightly falling quarterly venture capital totals and a notable decline in unicorn formation does not a startup winter make. So let’s look at what’s happened more recently.

The thesis that there would be an instantly obvious slowdown in Chinese venture capital activity is not supported by the data we secured.

Powered by WPeMatico

The Exchange spent a little time on Friday ruminating on the impact of then-rumored regulation in China targeting its edtech sector. News that the Chinese government intended to crack down further on the education technology market hit shares of public, China-based edtech companies. It was a mess.

Then over the weekend, the rumors became reality, and the impact is still being felt today in the global markets.

But there’s more. China is also bringing new regulatory pressure on food-delivery companies and Tencent Music. More precisely, we’ve seen successive market-dynamic-changing moves from the Chinese government in the last few days, coming as 2021 had already proved to be a turbulent environment for China-based technology companies.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Today we have to do a little bit of work to understand precisely what is going on with the various regulatory changes. Why? Because the Chinese venture capital market is a key player in the global venture scene. And Chinese startups have gone public on both Chinese, Hong Kong and U.S. exchanges; there’s a lot of capital tied up in companies impacted today — and possibly tomorrow.

For startups, the regulatory changes aren’t a death blow; indeed, many Chinese tech startups won’t be affected by what we’ve seen thus far. And upstart tech companies in sectors less likely to be targeted by central authorities may become more attractive to investors than they were before the regulatory onslaught kicked off. But on the whole, it feels like the risk profile of doing business in China has risen. That could curb the pace at which capital is invested, cut valuations and lower interest in the Chinese startup market from private-market investors able to invest globally.

Let’s parse what’s changed, examine market reactions and then consider what could be next. We want to better understand today’s Chinese startup market and what its new form could mean for existing players and future performance.

Let’s parse what’s changed, examine market reactions and then consider what could be next. We want to better understand today’s Chinese startup market and what its new form could mean for existing players and future performance.

The edtech clampdown did not start last week. China’s edtech sector started to rack up penalties and fines in June, which led to what the Asia Times called “warning bells” in the sector. From there, things went from penalties to punishing regulatory changes.

Powered by WPeMatico

{kind=link}