eBay

Auto Added by WPeMatico

Auto Added by WPeMatico

There’s a strategic cost to the defection of Visa, Stripe, eBay, and more from the Facebook -led cryptocurrency Libra Association . They’re not just names dropping off a list. Each potentially made Libra more useful, ubiquitous, or reputable. Now they could become obstacles to the token’s launch or growth.

Fearing regulators’ inquiries not just into their Libra involvement but the rest of their businesses, these companies are pulling out at least for now. None had made precise commitments to integrating Libra into their products, and they’ve said they could still get involved later. But their exit clouds the project’s future and leaves Facebook to absorb more of the blowback.

Here’s what each of the departing Libra Association members brought to the table and how they could spawn new challenges for the cryptocurrency:

With one of most widely-accepted payment methods, Visa could have helped make Libra universally spendable. It’s also one of the most prestigious names in finance, lending deep credibility to the project. Visa’s departure leaves Libra looking more like tech companies barging into payments, conjuring fears of their move fast, break things approach that could cause financial ruin if Libra runs into problems. It also could leave Libra with a much weaker presence in brick-and-mortar shops. No one will want to own a cryptocurrency that doesn’t appreciate in value and can’t be easily spent.

The involvement of MasterCard alongside Visa made Libra look like the incumbents adapting to modern technologies. This made it less threatening, and gave cryptocurrency an air of inevitability. MasterCard would have also brought an even wider network of locations where Libra could one day be used for payment. Now MasterCard and Visa might actively work against Libra to prevent their payment methods being made obsolete by Libra and its elimination of transaction fees through the blockchain. Two of Libras biggest allies could become its biggest foes.

Facebook has repeatedly told regulators that its Calibra app plus integrations into Messenger and WhatsApp would not be the only Libra wallets, pointing to PayPal . Facebook’s head of Libra David Marcus told Congress when asked about the social network’s outsized power to exploit Libra through its own Calibra wallet that “you have companies like PayPal and others that will, of course, collaborate, but [also] compete with us”. Now Facebook won’t have a scaled payment method it doesn’t own to point to as a likely alternative for people who don’t want to trust Facebook’s Calibra, Messenger, or WhatsApp to be their Libra wallet. The Libra Association also loses PayPal’s enormous network of online merchants that accept it, plus the inroad to integration into its peer-to-peer payback app Venmo. PayPal convinced the mainstream public to trust online payments — the exact kind of trust Facebook desperately needs. The fact that Marcus was also the former president of PayPal but couldn’t keep it in the association raises concerns about the group’s coalition-building prowess.

Stripe’s enormous popularity with ecommerce vendors made it a valuable Libra Association member. Together with PayPal, Stripe facilitates a huge portion of online transactions outside of China. Its ease of integration made it a top pick for developers Facebook surely hoped would build atop Libra. Stripe’s exit destroys a critical bridge to the fintech startup ecosystem that could have helped institutionalize Libra. Now the association will have to work on engineering payment widgets from scratch without Stripe’s assistance, which could slow adoption if it ever launches.

There’s a clear reason all these payment processors bailed. Senators Brian Schatz (D-HI) and Sherrod Brown (D-OH) wrote a letter to Visa, MasterCard, and Stripe’s CEOs this week explaining that “If you take this on, you can expect a high level of scrutiny from regulators not only on Libra-related activities, but on all payment activities.”

As one of the longest standing ecommerce companies, eBay bolstered beliefs that Libra could be used to power transactions between untrusted strangers without a costly middleman. It might have also put Libra into practice on one of the top western online marketplaces outside of Amazon. Without destinations like eBay onboard, average netizens will have fewer opportunities to be exposed to Libra’s potential to eliminate transaction fees.

One of the lesser-known Libra Association members, Mercado Pago helps merchants receive payments via email or in installments. The idea of connecting financially underserved populations has been core to Facebook’s pitch for why Libra should exist. The Libra Association has been light on the details of how exactly it serves this demographic, relying on the inclusion of partners like Mercado Pago to help it figure this out later. Mercado Pago’s departure leaves Libra looking more like a financial power grab rather than a tool to assist the disadvantaged.

On Monday, the remaining Libra Association members will meet to finalize the initial member list, elect a board, and create a charter to govern the project. This forced the hands of the companies above, who had their last chance to depart this week before being pulled deeper into Libra.

UNITED STATES – JULY 16: David Marcus, head of Facebook’s Calibra digital wallet service, prepares to testify during the Senate Banking, Housing and Urban Affairs Committee hearing on “Examining Facebook’s Proposed Digital Currency and Data Privacy Considerations” on Tuesday, July 16, 2019. (Photo By Bill Clark/CQ Roll Call)

Who’s left includes venture capital firms, ride sharing companies, non-profits, and cryptocurrency companies. They are less tied up with the status quo of payment processing, and therefore had less to lose. The blockchain-specific companies were likely hoping to piggyback on financial giants like Visa to get Libra approved and create more legitimacy for their industry as a whole.

These partners could help fund an ecosystem of Libra developers, create daily use cases, spread the system in the developing world, and push for alliances between Libra and cryptocurrency players. Facebook will need to fight to keep them aboard if it wants to avoid Libra looking like a unilateral disruption of the economy.

For Libra to actually launch, Facebook needs to make serious concessions and divert from its initial vision. Otherwise if it continues to butt heads with regulators, more members could flee. One option floated by Libra Association member Andreessen Horowitz’s a16z Crypto partner Chris Dixon was for Libra to be denominated in US dollars instead of a basket of international currencies. That might lessen fears that Libra intends to compete directly with the dollar.

It’s become apparent that Facebook will not get its ideal cryptocurrency out the door. This is the brand tax of 100 scandals coming back to bite it. Now the best it can hope for is to get even a watered-down version launched, prove it can actually help the underbanked, and then hope to convince regulators it’s well-intentioned.

Powered by WPeMatico

The day of reckoning for the “flexible office space as a startup” is coming, and it’s coming up fast. WeWork’s IPO filing has fired the starting gun on the race to become the game-changer both in the future of property and real estate but also the future of how we live and work. As Churchill once said, “we shape our buildings and afterwards our buildings shape us.”

Until recently, WeWork was the ruler by which other flexible-space startups were measured, but questions are now being asked if it deserves its valuation. The profitable IWG plc, formerly Regus, has been a business providing serviced offices, virtual offices, meeting rooms and the rest, for years, and yet WeWork is valued by 10 times more.

That’s not to mention how it exposes landlords to $40 billion in rent commitments, something which a few of them are starting to feel rather nervous about.

Some analysts even say WeWork’s IPO is a “masterpiece of obfuscation.”

Powered by WPeMatico

The unchecked digital land grab for consumers’ personal data that has been going on for more than a decade is coming to an end, and the dominoes have begun to fall when it comes to the regulation of consumer privacy and data security.

We’re witnessing the beginning of a sweeping upheaval in how companies are allowed to obtain, process, manage, use and sell consumer data, and the implications for the digital ad competitive landscape are massive.

On the backdrop of evolving privacy expectations and requirements, we’re seeing the rise of a new class of digital advertising player: consumer-facing apps and commerce platforms. These commerce companies are emerging as the most likely beneficiaries of this new regulatory privacy landscape — and we’re not just talking about e-commerce giants like Amazon.

Traditional commerce companies like eBay, Target and Walmart have publicly spoken about advertising as a major focus area for growth, but even companies like Starbucks and Uber have an edge in consumer data consent and, thus, an edge over incumbent media players in the fight for ad revenues.

with a big hand making stop gesture (No!)")

Image via Getty Images / alashi

By now, most executives, investors and entrepreneurs are aware of the growing acronym soup of privacy regulation, the two most prominent ingredients being the GDPR (General Data Protection Regulation) and the CCPA (California Consumer Privacy Act).

Powered by WPeMatico

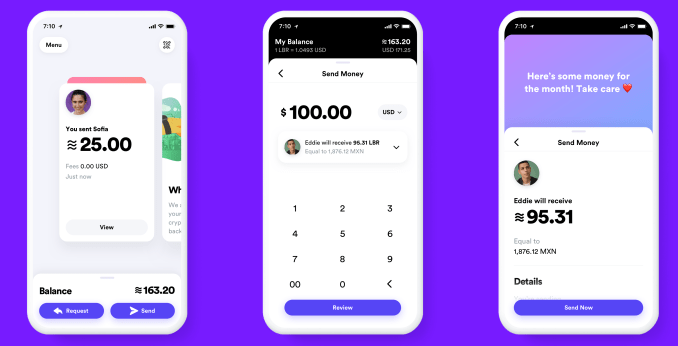

Facebook has finally revealed the details of its cryptocurrency, Libra, which will let you buy things or send money to people with nearly zero fees. You’ll pseudonymously buy or cash out your Libra online or at local exchange points like grocery stores, and spend it using interoperable third-party wallet apps or Facebook’s own Calibra wallet that will be built into WhatsApp, Messenger and its own app. Today Facebook released its white paper explaining Libra and its testnet for working out the kinks of its blockchain system before a public launch in the first half of 2020.

Facebook won’t fully control Libra, but instead get just a single vote in its governance like other founding members of the Libra Association, including Visa, Uber and Andreessen Horowitz, which have invested at least $10 million each into the project’s operations. The association will promote the open-sourced Libra Blockchain and developer platform with its own Move programming language, plus sign up businesses to accept Libra for payment and even give customers discounts or rewards.

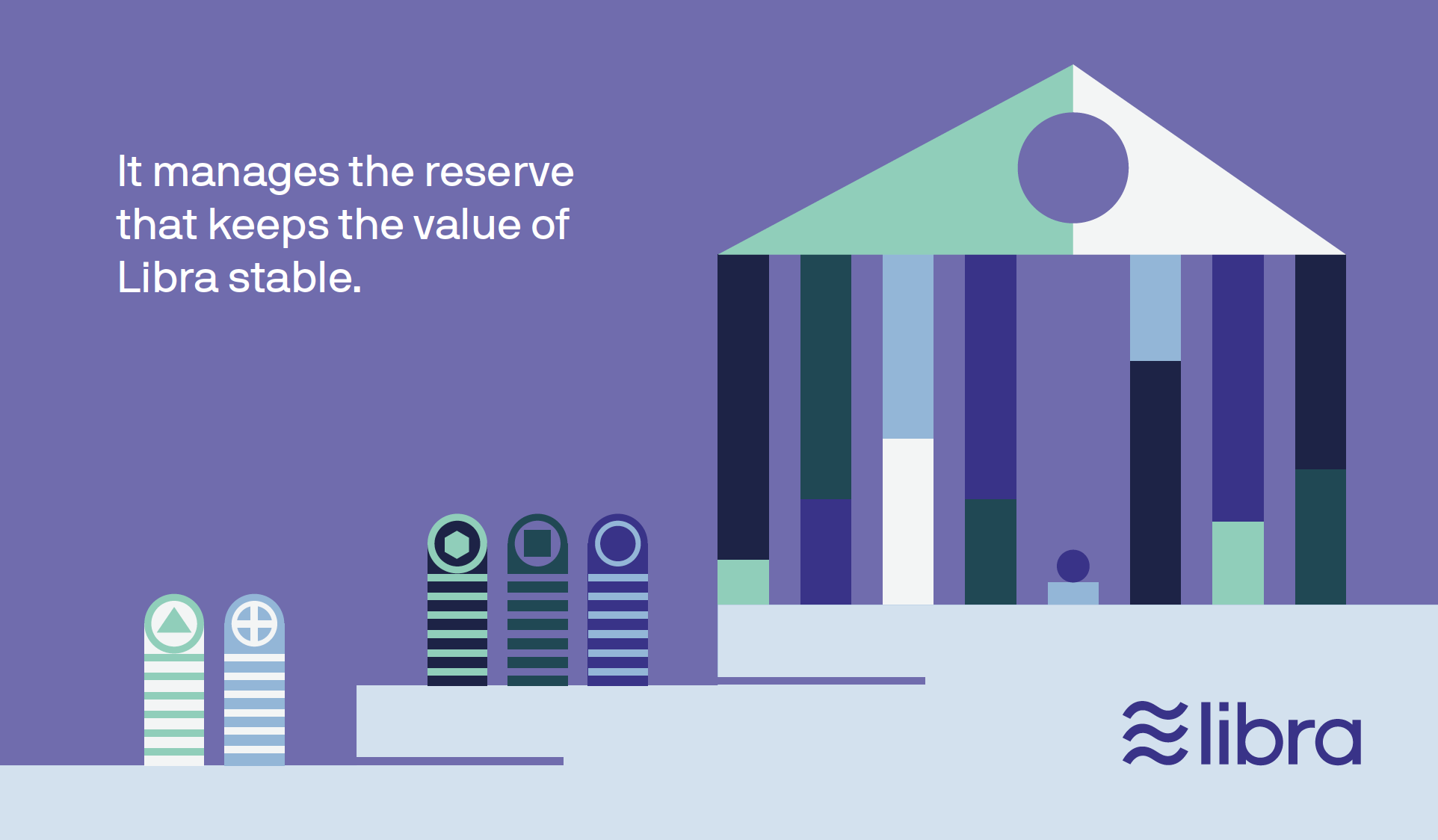

Facebook is launching a subsidiary company also called Calibra that handles its crypto dealings and protects users’ privacy by never mingling your Libra payments with your Facebook data so it can’t be used for ad targeting. Your real identity won’t be tied to your publicly visible transactions. But Facebook/Calibra and other founding members of the Libra Association will earn interest on the money users cash in that is held in reserve to keep the value of Libra stable.

Facebook’s audacious bid to create a global digital currency that promotes financial inclusion for the unbanked actually has more privacy and decentralization built in than many expected. Instead of trying to dominate Libra’s future or squeeze tons of cash out of it immediately, Facebook is instead playing the long-game by pulling payments into its online domain. Facebook’s VP of blockchain, David Marcus, explained the company’s motive and the tie-in with its core revenue source during a briefing at San Francisco’s historic Mint building. “If more commerce happens, then more small businesses will sell more on and off platform, and they’ll want to buy more ads on the platform so it will be good for our ads business.”

In cryptocurrencies, Facebook saw both a threat and an opportunity. They held the promise of disrupting how things are bought and sold by eliminating transaction fees common with credit cards. That comes dangerously close to Facebook’s ad business that influences what is bought and sold. If a competitor like Google or an upstart built a popular coin and could monitor the transactions, they’d learn what people buy and could muscle in on the billions spent on Facebook marketing. Meanwhile, the 1.7 billion people who lack a bank account might choose whoever offers them a financial services alternative as their online identity provider too. That’s another thing Facebook wants to be.

Yet existing cryptocurrencies like Bitcoin and Ethereum weren’t properly engineered to scale to be a medium of exchange. Their unanchored price was susceptible to huge and unpredictable swings, making it tough for merchants to accept as payment. And cryptocurrencies miss out on much of their potential beyond speculation unless there are enough places that will take them instead of dollars, and the experience of buying and spending them is easy enough for a mainstream audience. But with Facebook’s relationship with 7 million advertisers and 90 million small businesses plus its user experience prowess, it was well-poised to tackle this juggernaut of a problem.

Now Facebook wants to make Libra the evolution of PayPal . It’s hoping Libra will become simpler to set up, more ubiquitous as a payment method, more efficient with fewer fees, more accessible to the unbanked, more flexible thanks to developers and more long-lasting through decentralization.

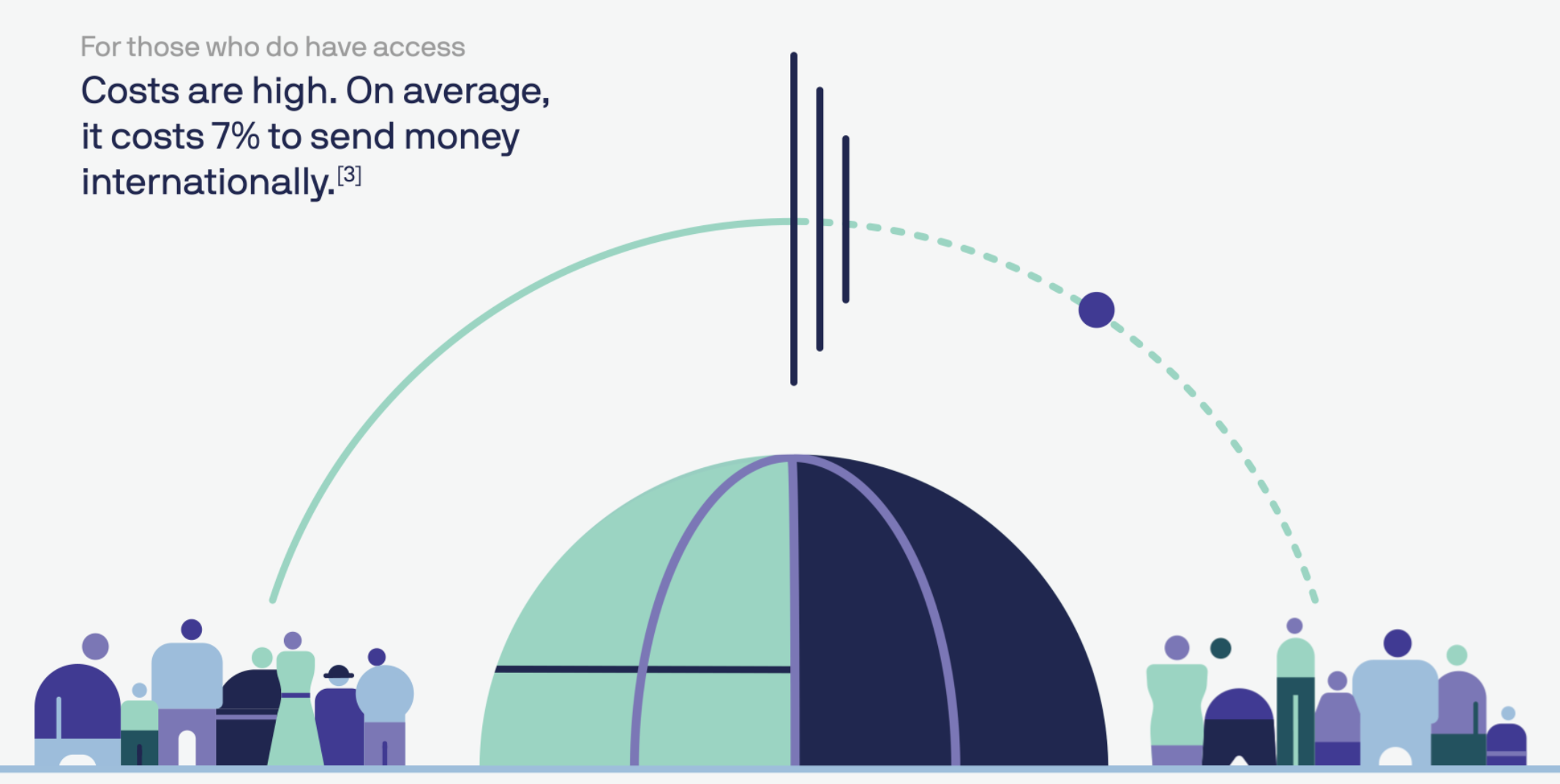

“Success will mean that a person working abroad has a fast and simple way to send money to family back home, and a college student can pay their rent as easily as they can buy a coffee,” Facebook writes in its Libra documentation. That would be a big improvement on today, when you’re stuck paying rent in insecure checks while exploitative remittance services charge an average of 7% to send money abroad, taking $50 billion from users annually. Libra could also power tiny microtransactions worth just a few cents that are infeasible with credit card fees attached, or replace your pre-paid transit pass.

…Or it could be globally ignored by consumers who see it as too much hassle for too little reward, or too unfamiliar and limited in use to pull them into the modern financial landscape. Facebook has built a reputation for over-engineered, underused products. It will need all the help it can get if wants to replace what’s already in our pockets.

By now you know the basics of Libra. Cash in a local currency, get Libra, spend them like dollars without big transaction fees or your real name attached, cash them out whenever you want. Feel free to stop reading and share this article if that’s all you care about. But the underlying technology, the association that governs it, the wallets you’ll use and the way payments work all have a huge amount of fascinating detail to them. Facebook has released more than 100 pages of documentation on Libra and Calibra, and we’ve pulled out the most important facts. Let’s dive in.

Facebook knew people wouldn’t trust it to wholly steer the cryptocurrency they use, and it also wanted help to spur adoption. So the social network recruited the founding members of the Libra Association, a not-for-profit which oversees the development of the token, the reserve of real-world assets that gives it value and the governance rules of the blockchain. “If we were controlling it, very few people would want to jump on and make it theirs,” says Marcus.

Each founding member paid a minimum of $10 million to join and optionally become a validator node operator (more on that later), gain one vote in the Libra Association council and be entitled to a share (proportionate to their investment) of the dividends from interest earned on the Libra reserve into which users pay fiat currency to receive Libra.

The 28 soon-to-be founding members of the association and their industries, previously reported by The Block’s Frank Chaparro, include:

Facebook says it hopes to reach 100 founding members before the official Libra launch and it’s open to anyone that meets the requirements, including direct competitors like Google or Twitter. The Libra Association is based in Geneva, Switzerland and will meet biannually. The country was chosen for its neutral status and strong support for financial innovation including blockchain technology.

To join the association, members must have a half rack of server space, a 100Mbps or above dedicated internet connection, a full-time site reliability engineer and enterprise-grade security. Businesses must hit two of three thresholds of a $1 billion USD market value or $500 million in customer balances, reach 20 million people a year and/or be recognized as a top 100 industry leader by a group like Interbrand Global or the S&P.

Crypto-focused investors must have more than $1 billion in assets under management, while Blockchain businesses must have been in business for a year, have enterprise-grade security and privacy and custody or staking greater than $100 million in assets. And only up to one-third of founding members can by crypto-related businesses or individually invited exceptions. Facebook also accepts research organizations like universities, and nonprofits fulfilling three of four qualities, including working on financial inclusion for more than five years, multi-national reach to lots of users, a top 100 designation by Charity Navigator or something like it and/or $50 million in budget.

The Libra Association will be responsible for recruiting more founding members to act as validator nodes for the blockchain, fundraising to jump-start the ecosystem, designing incentive programs to reward early adopters and doling out social impact grants. A council with a representative from each member will help choose the association’s managing director, who will appoint an executive team and elect a board of five to 19 top representatives.

Each member, including Facebook/Calibra, will only get up to one vote or 1% of the total vote (whichever is larger) in the Libra Association council. This provides a level of decentralization that protects against Facebook or any other player hijacking Libra for its own gain. By avoiding sole ownership and dominion over Libra, Facebook could avoid extra scrutiny from regulators who are already investigating it for a sea of privacy abuses as well as potentially anti-competitive behavior. In an attempt to preempt criticism from lawmakers, the Libra Association writes, “We welcome public inquiry and accountability. We are committed to a dialogue with regulators and policymakers. We share policymakers’ interest in the ongoing stability of national currencies.”

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

A Libra is a unit of the Libra cryptocurrency that’s represented by a three wavy horizontal line unicode character ≋ like the dollar is represented by $. The value of a Libra is meant to stay largely stable, so it’s a good medium of exchange, as merchants can be confident they won’t be paid a Libra today that’s then worth less tomorrow. The Libra’s value is tied to a basket of bank deposits and short-term government securities for a slew of historically stable international currencies, including the dollar, pound, euro, Swiss franc and yen. The Libra Association maintains this basket of assets and can change the balance of its composition if necessary to offset major price fluctuations in any one foreign currency so that the value of a Libra stays consistent.

The name Libra comes from the word for a Roman unit of weight measure. It’s trying to invoke a sense of financial freedom by playing on the French stem “Lib,” meaning free.

The Libra Association is still hammering out the exact start value for the Libra, but it’s meant to be somewhere close to the value of a dollar, euro or pound so it’s easy to conceptualize. That way, a gallon of milk in the U.S. might cost 3 to 4 Libra, similar but not exactly the same as with dollars.

The idea is that you’ll cash in some money and keep a balance of Libra that you can spend at accepting merchants and online services. You’ll be able to trade in your local currency for Libra and vice versa through certain wallet apps, including Facebook’s Calibra, third-party wallet apps and local resellers like convenience or grocery stores where people already go to top-up their mobile data plan.

Each time someone cashes in a dollar or their respective local currency, that money goes into the Libra Reserve and an equivalent value of Libra is minted and doled out to that person. If someone cashes out from the Libra Association, the Libra they give back are destroyed/burned and they receive the equivalent value in their local currency back. That means there’s always 100% of the value of the Libra in circulation, collateralized with real-world assets in the Libra Reserve. It never runs fractional. And unliked “pegged” stable coins that are tied to a single currency like the USD, Libra maintains its own value — though that should cash out to roughly the same amount of a given currency over time.

When Libra Association members join and pay their $10 million minimum, they receive Libra Investment Tokens. Their share of the total tokens translates into the proportion of the dividend they earn off of interest on assets in the reserve. Those dividends are only paid out after Libra Association uses interest to pay for operating expenses, investments in the ecosystem, engineering research and grants to nonprofits and other organizations. This interest is part of what attracted the Libra Association’s members. If Libra becomes popular and many people carry a large balance of the currency, the reserve will grow huge and earn significant interest.

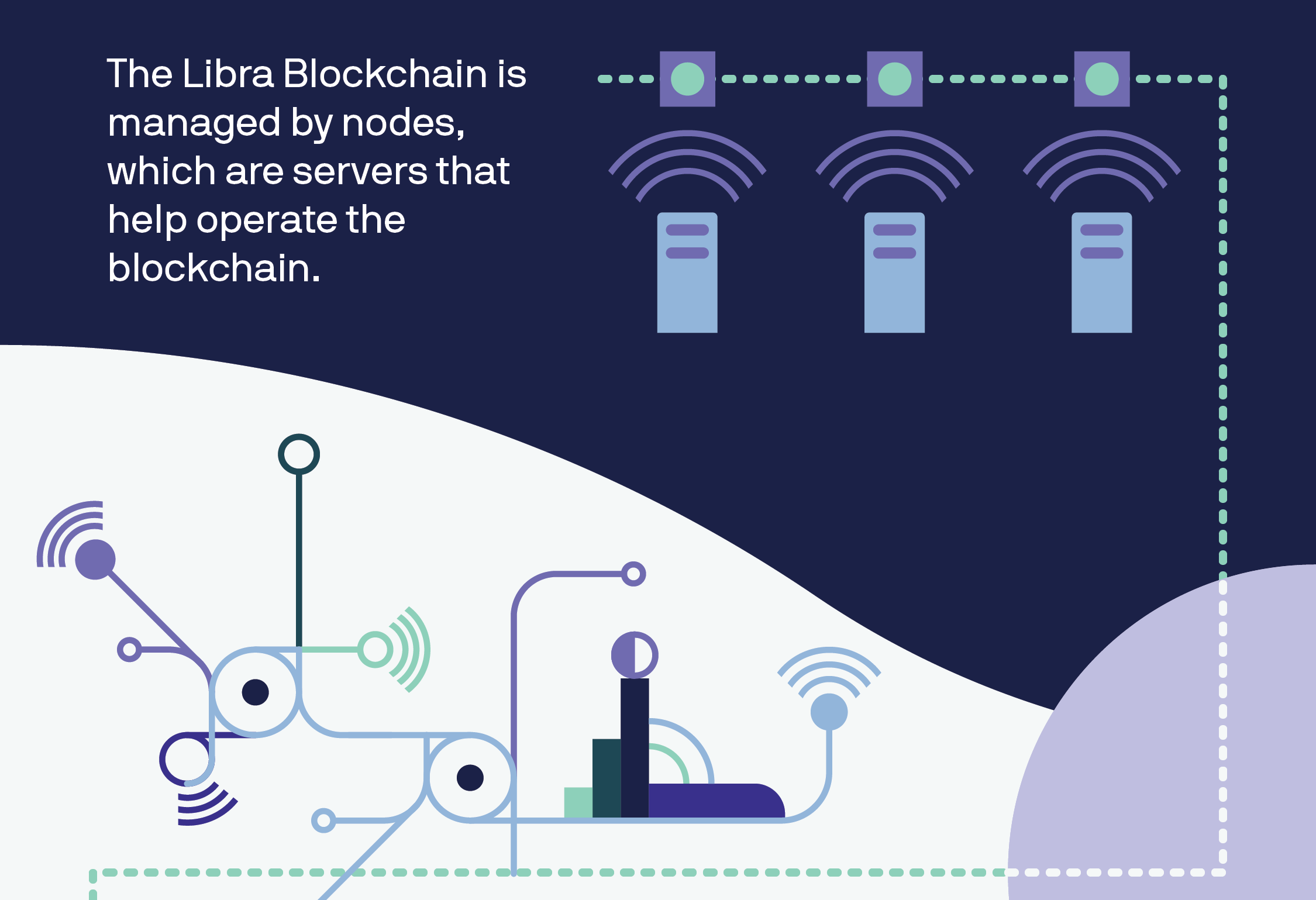

Every Libra payment is permanently written into the Libra Blockchain — a cryptographically authenticated database that acts as a public online ledger designed to handle 1,000 transactions per second. That would be much faster than Bitcoin’s 7 transactions per second or Ethereum’s 15. The blockchain is operated and constantly verified by founding members of the Libra Association, which each invested $10 million or more for a say in the cryptocurrency’s governance and the ability to operate a validator node.

When a transaction is submitted, each of the nodes runs a calculation based on the existing ledger of all transactions. Thanks to a Byzantine Fault Tolerance system, just two-thirds of the nodes must come to consensus that the transaction is legitimate for it to be executed and written to the blockchain. A structure of Merkle Trees in the code makes it simple to recognize changes made to the Libra Blockchain. With 5KB transactions, 1,000 verifications per second on commodity CPUs and up to 4 billion accounts, the Libra Blockchain should be able to operate at 1,000 transactions per second if nodes use at least 40Mbps connections and 16TB SSD hard drives.

Transactions on Libra cannot be reversed. If an attack compromises over one-third of the validator nodes causing a fork in the blockchain, the Libra Association says it will temporarily halt transactions, figure out the extent of the damage and recommend software updates to resolve the fork.

Transactions aren’t entirely free. They incur a tiny fraction of a cent fee to pay for “gas” that covers the cost of processing the transfer of funds similar to with Ethereum. This fee will be negligible to most consumers, but when they add up, the gas charges will deter bad actors from creating millions of transactions to power spam and denial-of-service attacks. “We’ve purposely tried not to innovate massively on the blockchain itself because we want it to be scalable and secure,” says Marcus of piggybacking on the best elements of existing cryptocurrencies.

Currently, the Libra Blockchain is what’s known as “permissioned,” where only entities that fulfill certain requirements are admitted to a special in-group that defines consensus and controls governance of the blockchain. The problem is this structure is more vulnerable to attacks and censorship because it’s not truly decentralized. But during Facebook’s research, it couldn’t find a reliable permissionless structure that could securely scale to the number of transactions Libra will need to handle. Adding more nodes slows things down, and no one has proven a way to avoid that without compromising security.

That’s why the Libra Association’s goal is to move to a permissionless system based on proof-of-stake that will protect against attacks by distributing control, encourage competition and lower the barrier to entry. It wants to have at least 20% of votes in the Libra Association council coming from node operators based on their total Libra holdings instead of their status as a founding member. That plan should help appease blockchain purists who won’t be satisfied until Libra is completely decentralized.

The Libra Blockchain is open source with an Apache 2.0 license, and any developer can build apps that work with it using the Move coding language. The blockchain’s prototype launches its testnet today, so it’s effectively in developer beta mode until it officially launches in the first half of 2020. The Libra Association is working with HackerOne to launch a bug bounty system later this year that will pay security researchers for safely identifying flaws and glitches. In the meantime, the Libra Association is implementing the Libra Core using the Rust programming language because it’s designed to prevent security vulnerabilities, and the Move language isn’t fully ready yet.

Move was created to make it easier to write blockchain code that follows an author’s intent without introducing bugs. It’s called Move because its primary function is to move Libra coins from one account to another, and never let those assets be accidentally duplicated. The core transaction code looks like: LibraAccount.pay_from_sender(recipient_address, amount) procedure.

Eventually, Move developers will be able to create smart contracts for programmatic interactions with the Libra Blockchain. Until Move is ready, developers can create modules and transaction scripts for Libra using Move IR, which is high-level enough to be human-readable but low-level enough to be translatable into real Move bytecode that’s written to the blockchain.

The Libra ecosystem and the Move language will be completely open to use and build, which presents a sizable risk. Crooked developers could prey on crypto novices, claiming their app works just the same as legitimate ones, and that it’s safe because it uses Libra. But if consumers get ripped off by these scammers, the anger will surely bubble up to Facebook. Yet still, Calibra’s head of product tells me, “There are no plans for the Libra Association to take a role in actively vetting [developers],” Calibra’s head of product Kevin Weil tells me.

Even though it’s tried to distance itself sufficiently via its subsidiary Libra and the association, many people will probably always think of Libra as Facebook’s cryptocurrency and blame it for their woes.

Read our full story on the dangers of Libra’s unvetted developer platform

The Libra Association wants to encourage more developers and merchants to work with its cryptocurrency. That’s why it plans to issue incentives, possibly Libra coins, to validator node operators who can get people signed up for and using Libra. Wallets that pull users through the Know Your Customer anti-fraud and money laundering process or that keep users sufficiently active for over a year will be rewarded. For each transaction they process, merchants will also receive a percentage of the transaction back.

Businesses that earn these incentives can keep them, or pass some or all of them along to users in the form of free Libra tokens or discounts on their purchases. This could create competition between wallets to see which can pass on the most rewards to their customers, and thereby attract the most users. You could imagine eBay or Spotify giving you a discount for paying in Libra, while wallet developers might offer you free tokens if you complete 100 transactions within a year.

“One challenge for Spotify and its users around the world has been the lack of easily accessible payment systems – especially for those in financially underserved markets,” Spotify’s Chief Premium Business Officer Alex Norström writes. “In joining the Libra Association, there is an opportunity to better reach Spotify’s total addressable market, eliminate friction and enable payments in mass scale.”

This savvy incentive system should massively help ratchet up Libra’s user count without dictating how businesses balance their margins versus growth. Facebook also has another plan to grow its developer ecosystem. By offering venture capital firms like Andreessen Horowitz and Union Square Ventures a portion of the reserve interest, they’re motivating to fund startups building Libra infrastructure.

So how do you actually own and spend Libra? Through Libra wallets like Facebook’s own Calibra and others that will be built by third-parties, potentially including Libra Association members like PayPal. The idea is to make sending money to a friend or paying for something as easy as sending a Facebook Message. You won’t be able to make or receive any real payments until the official launch next year, though, but you can sign up for early access when it’s ready here.

None of the Libra Association members agreed to provide details on what exactly they’ll build on the blockchain, but we can take Facebook’s Calibra wallet as an example of the basic experience. Calibra will launch alongside the Libra currency on iOS and Android within Facebook Messenger, WhatsApp and a standalone app. When users first sign up, they’ll be taken through a Know Your Customer anti-fraud process where they’ll have to provide a government-issued photo ID and other verification info. They’ll need to conduct due diligence on customers and report suspicious activity to the authorities.

From there you’ll be able to cash in to Libra, pick a friend or merchant, set an amount to send them and add a description and send them Libra. You’ll also be able to request Libra, and Calibra will offer an expedited way of paying merchants by scanning your or their QR code. Eventually it wants to offer in-store payments and integrations with point-of-sale systems like Square.

The Libra Association’s e-commerce members seem particularly excited about how the token could eliminate transaction fees and speed up checkout. “We believe blockchain will benefit the luxury industry by improving IP protection, transparency in the product life cycle and — as in the case of Libra — enable global frictionless e-commerce,” says FarFetch CEO Jose Neves.

Facebook CEO Mark Zuckerberg explained some of the philosophy behind Libra and Calibra in a post today. “It’s decentralized — meaning it’s run by many different organizations instead of just one, making the system fairer overall. It’s available to anyone with an internet connection and has low fees and costs. And it’s secured by cryptography which helps keep your money safe. This is an important part of our vision for a privacy-focused social platform — where you can interact in all the ways you’d want privately, from messaging to secure payments.”

By default, Facebook won’t import your contacts or any of your profile information, but may ask if you wish to do so. It also won’t share any of your transaction data back to Facebook, so it won’t be used to target you with ads, rank your News Feed, or otherwise earn Facebook money directly. Data will only be shared in specific instances in anonymized ways for research or adoption measurement, for hunting down fraudsters or due to a request from law enforcement. And you don’t even need a Facebook or WhatsApp account to sign up for Calibra or to use Libra.

“We realize people don’t want their social data and financial data commingled,” says Marcus, who’s now head of Calibra. “The reality is we’ll have plenty of wallets that will compete with us and many of them will not be in social, and if we want to successfully win people’s trust, we have to make sure the data will be separated.”

In case you are hacked, scammed or lose access to your account, Calibra will refund you for lost coins when possible through 24/7 chat support because it’s a custodial wallet. You also won’t have to remember any long, complex crypto passwords you could forget and get locked out from your money, as Calibra manages all your keys for you. Given Calibra will likely become the default wallet for many Libra users, this extra protection and smoother user experience is essential.

For now, Calibra won’t make money. But Calibra’s head of product Kevin Weil tells me that if it reaches scale, Facebook could launch other financial tools through Calibra that it could monetize, such as investing or lending. “In time, we hope to offer additional services for people and businesses, such as paying bills with the push of a button, buying a cup of coffee with the scan of a code or riding your local public transit without needing to carry cash or a metro pass,” the Calibra team writes. That makes it start to sound a lot like China’s everything app WeChat.

Facebook got one thing right for sure: Today’s money doesn’t work for everyone. Those of us living comfortably in developed nations likely don’t see the hardships that befall migrant workers or the unbanked abroad. Preyed on by greedy payday lenders and high-fee remittance services, targeted by muggers and left out of traditional financial services, the poor get poorer. Libra has the potential to get more money from working parents back to their families and help people retain credit even if they’re robbed of their physical possessions. That would do more to accomplish Facebook’s mission of making the world feel smaller than all the News Feed Likes combined.

If Facebook succeeds and legions of people cash in money for Libra, it and the other founding members of the Libra Association could earn big dividends on the interest. And if suddenly it becomes super quick to buy things through Facebook using Libra, businesses will boost their ad spend there. But if Libra gets hacked or proves unreliable, it could cost lots of people around the world money while souring them on cryptocurrencies. And by offering an open Libra platform, shady developers could build apps that snatch not just people’s personal info like Cambridge Analytica, but their hard-earned digital cash.

Facebook just tried to reinvent money. Next year, we’ll see if the Libra Association can pull it off. It took me 4,000 words to explain Libra, but at least now you can make up your own mind about whether to be scared of Facebook crypto.

Powered by WPeMatico

Fertility services are raising venture cash left and right. Last week, it was Dadi, a sperm storage startup that nabbed a $2 million seed round. This week, it’s Extend Fertility, which helps women preserve their fertility through egg freezing.

Headquartered in New York, the business has secured a $15 million Series A investment from Regal Healthcare Capital Partners to expand its fertility services, which also include infertility treatments, such as in vitro and intrauterine insemination. The company has also appointed Anne Hogarty, the former chief business officer at Prelude Fertility and vice president of international business at BuzzFeed, to the role of chief executive officer. Hogarty replaces Extend Fertility co-founder Ilaina Edison, who had held the C-level title since the business launched in 2016. Edison will remain on the startup’s board of directors.

Extend Fertility, in its New York cryopreservation and embryology lab and treatment center, completed 1,000 egg-freezing cycles in 2018.

“A lot of amazing things have happened for women over the last century,” Hogarty told TechCrunch earlier this week. “Now, women are permitted and encouraged to seek higher education, pursue a career, follow their dreams and end up with a partner who’s the right partner, not just any partner. Doing all those things has pushed the window for when women want to start a family from their 20s to their 30s and unfortunately, one thing that has not changed in that time is the biological clock.”

Hogarty explained Extend’s fertility services are more affordable than other options because the service was built specifically with egg freezing in mind, and the company later expanded to offer infertility treatments, whereas other services were established to provide IVF and other infertility treatments and integrated cryopreservation tools later.

“We are really purpose-built to be an egg-freezing-first company, where many legacy institutions that were providing infertility services have legacy costs that come with … inefficiencies bred over decades and outmoded technology in their labs that may not be the most efficient and effective,” she said. “We have a state of the art lab with the latest equipment.”

“It’s the classic innovator dilemma,” she added. “Infertility services are extraordinarily expensive and reproductive endocrinology is a new area of medicine. There are a lot of people and institutions that have been taking inordinate amounts of money for their infertility services so they weren’t looking to serve this population of women looking to preserve their fertility.”

One egg-freezing cycle with Extend costs women $5,500, and additional cycles come at a sticker price of $4,000. Each cycle includes a fertility assessment, private consultation, anesthesia and any monitoring a patient may need during their cycle. The costs don’t include medication, however. Extend can prescribe medications — which typically cost between $2,000 and $5,000 for fertility patients — but they still need to go through a third party to get their prescriptions filled and paid for.

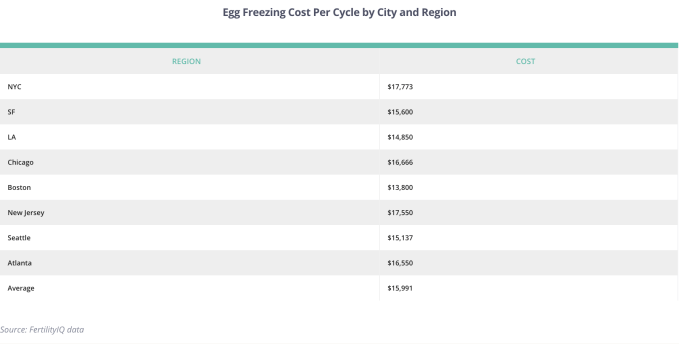

For reference, FertilityIQ, an online platform for researching fertility care providers and treatments, says the typical cost per cycle for egg freezing is more than $17,000 in New York City or $15,600 in San Francisco. Most egg-freezing services, including Extend, do not accept insurance, as most insurance providers don’t cover the steep costs of fertility or infertility treatments.

Some companies, however, are beginning to offer benefits that cover these costs. Facebook and Apple, for example, began subsidizing egg-freezing procedures for employees in 2014. Spotify and eBay, for their part, will pay for an unlimited number of IVF cycles.

Hogarty said Extend’s price point makes it one of the lowest-cost players in the market.

“We want as many women as possible to benefit from the advances from egg-freezing technology,” she said.

Extend Fertility, which has previously raised $10 million, plans to use the latest investment to open labs in new markets and expand its infertility services.

Powered by WPeMatico

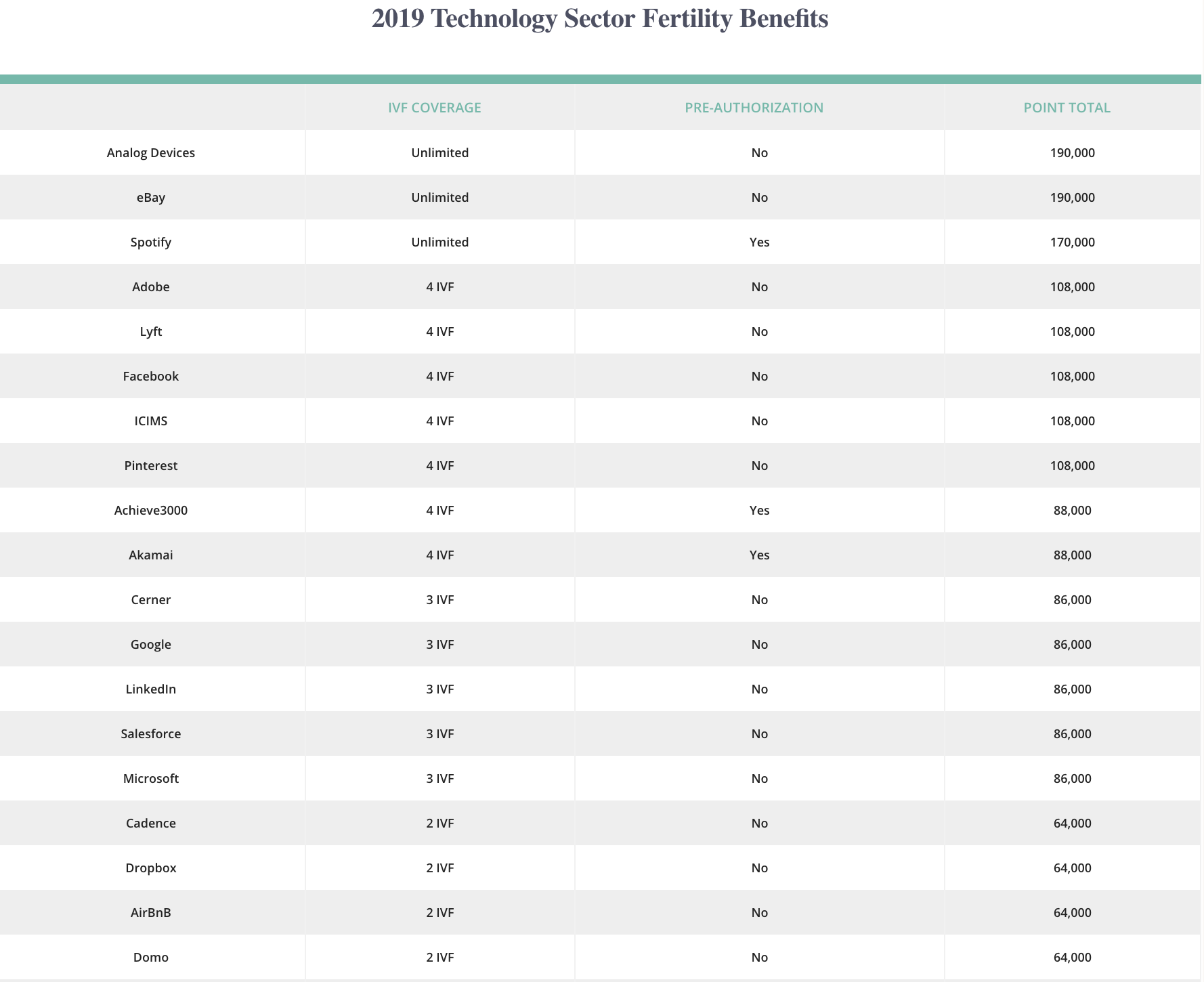

The technology sector awards women and same-sex couples the most comprehensive fertility benefit packages, according to a survey by FertilityIQ, an online platform for fertility patients to review doctors and research treatments.

The company asked 30,000 in vitro fertilisation (IVF) patients across industries about their employers’ — or their spouse’s employer’s’ — 2019 fertility treatment policy, and allocated points based on their support for IVF procedures and egg freezing, among other services.

Silicon Valley semiconductor business Analog Devices and eBay led the ranking. The two companies offer employees unlimited IVF cycles with no pre-authorization requirement, meaning employees do not need permission from insurance providers before seeking certain medical services. Pre-authorization has historically impacted lesbian, gay or unpartnered employees from accessing care quickly or at all, FertilityIQ co-founder Jake Anderson explained

Spotify, Adobe, Lyft, Facebook and Pinterest were amongst the highest-ranked technology businesses, too.

“I think a lot of people see the tech sector as being unenlightened when it comes to family values but it’s still the sector that makes the fertility benefits the most widely acceptable,” Anderson, a former consumer internet investor at Sequoia Capital, told TechCrunch.

FertilityIQ’s fertility benefits survey results.

Despite an initial outpouring of skepticism, Facebook and Apple became leaders in the fertility benefit category when they began paying for their female employees to freeze their eggs in 2014. Since then, smaller firms have opted to beef up those benefits to stay competitive with their much larger and richer counterparts.

“The Lyfts, the Airbnbs and the Ubers of the world, who clearly need to compete for those companies for talent, have effectively matched those companies dollar-for-dollar despite a much smaller war-chest,” Anderson said. “These companies that are worth 1/1000th of these bigger companies are effectively going toe-to-toe to offer whatever women need.”

Anderson and his wife, FertilityIQ co-founder Deborah Anderson, noticed improved benefits in 2018 from companies implicated by the #MeToo movement, such as Vice Media, Under Armour and Uber.

“Silicon Valley is notorious for talent moving around on you but it’s probably not coincidental that some of the companies that were in the spotlight in the #MeToo movement have added really generous benefits,” Deborah Anderson told TechCrunch.

Uber, for example, now pays for its employees to complete two IVF cycles but still requires pre-authorization.

One in 7 Americans struggle with infertility and the rate of IVF procedures only continues to increase, with the latest data indicating a 15 percent year-over-year growth rate. IVF costs roughly $22,000 per cycle, per FertilityIQ’s survey, a cost which has similarly increased 15 percent since 2015.

That’s a whole lot of cash for a fertility patient to dole out. If companies foot the bill, they’ll have a better shot at retaining talent.

“Best we can tell, there is no question that employees that get this benefit and use it are more loyal and more likely to stick around,” Jake Anderson said. “The company that helps you build your family is the company that you remain committed to.”

Powered by WPeMatico

Every year I teach an MBA course at Stanford about the exciting opportunities for tech investors and entrepreneurs in developing economies. When we designed the syllabus back in 2013, Rocket Internet was still firing on all cylinders on four continents. The unapologetic machine built to copy big American internet companies created billions of dollars for the Samwer brothers and its backers. During Rocket’s golden years, the best startups in the developing economies seemed to inevitably have an original reference in Silicon Valley.

Accordingly, we added a class about the opportunity of replicating business models to seize this information arbitrage. Call it the second-mover advantage.

Despite my conviction about the model, the copycat word — short for replicating startups and attached to these ventures — annoyed me from the start. More than a term to describe a straightforward recipe to launch, I see it as an unconscious way to belittle an entire group of hard-charging founders and investors.

Indeed, while in foreign eyes, we have been building a Mexican Kickstarter, a Middle Eastern Uber, an Indian Amazon or a Colombian Postmates, I argue visionary founders are taking a simple idea that already exists and creating new worlds.

On the internet, there are Einsteins and there are Bob the Builders. I’m Bob the Builder. Oliver Samwer, founder of Rocket Internet

While impact is the final goal, founders can approach the journey in different ways. The most common approach in the startup world is to use the business method, or more pompously, the design thinking methodology. “Fall in love with the problem, not the solution,” mentors keep telling a succession of startup clusters in acceleration programs. The best and “leanest” way to product market fit is by starting small then keep iterating the solution until you nail it.

A second way to start is favored by engineers and scientists: Take a new promising technology or a forgotten molecule, then find a big problem. Keep iterating until you find a problem worth solving, like a hammer looking for a nail.

A third way is starting like painters create, building skills by copying classics, or like a new chef cooks by starting with iconic recipes: replicate a proven idea and iterate until you find traction.

Until a few years ago it was ostensibly the only way to scale in developing economies. The model helped raise local capital from risk-averse investors who needed reassurance. The playbook to scale was unfolding a couple of years ahead and served as a guide to founders without previous startup experience and no local role models. The potential acquirer was identified and sometimes contacted in advance. Founders weren’t crazy and investors weren’t dumb.

Replicating a business model has served in emerging ecosystems as the gateway to entrepreneurship and venture investing.

Photo courtesy of Flickr/A_Marga

According to conventional wisdom, new ecosystems around the world grow through the following three stages, be them in developing economies or more developed countries. First, local and foreign entrepreneurs replicate successful models focused on local markets. Then as the ecosystem evolves, founders start applying existing technologies to solve local problems. Finally, as the tech space matures, new technologies begin to flourish.

In my opinion, those stages never happen sequentially as stated by ecosystem observers. Successful startups that started with a foreign inspiration can outgrow the master. If they are not bought into submission by the first mover, some of the most famous copycats reinvented the original and made it better: Mercado Libre is much more relevant in the e-commerce space than eBay . Flipkart is hardly an Amazon, not to mention WeChat. These companies are in turn some of the most prolific tech innovators on the globe. Truly ecosystems evolve organically in unique ways reflecting their history, geopolitical environment, economic structure and cultural features.

Two ways to defend the status quo: “It’s been done before” and “It’s never been done before.” –Thibault @Kpaxs

Recently, it’s hard to hear American observers use the word copycat to describe any American company. After all, Guilt replicated VentesPrivees and Lime, Chinese dockless bike sharing and many more examples. All American startups are treated as innovators while the rest as mere followers.

Recently, Chinese or Indian startups seem to be given the benefit of the doubt regarding their originality. Is it because these regions have become more innovative? Maybe. But it’s also because these ecosystems have gained the respect of Silicon Valley. Indeed, Chinese consumer tech surpassed decisively the U.S. as the most important country in terms of investments.

So here’s my humble suggestion to our wealthier and more accomplished colleagues: stop using the c-word with founders. It’s offensive. Most probably, these founders are facing more challenges to build their companies and lower odds for success that the first mover. If anything, they have more merit than the originals.

As for founders, when they call you a me-too, remember all teams started somewhere, somehow. In fact, most started like Bob the Builder before turning into Einsteins. The truth is, it doesn’t matter where you start. You can start by applying a new technology or protocol. You can start with a problem you feel passionate about. You can start by replicating a business model. It doesn’t really matter if you take a big swing at the future and trust you will figure out how to make it happen. It doesn’t matter what label they use while you change the world for the better.

Powered by WPeMatico

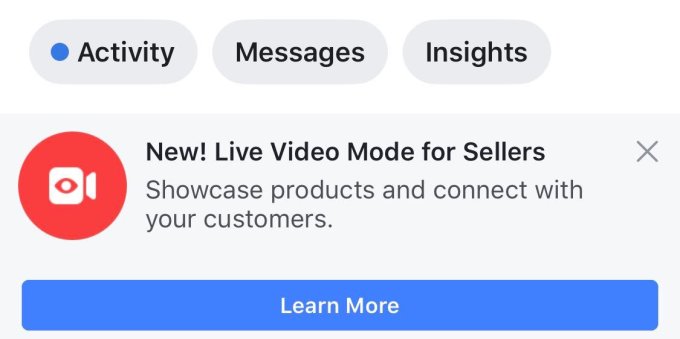

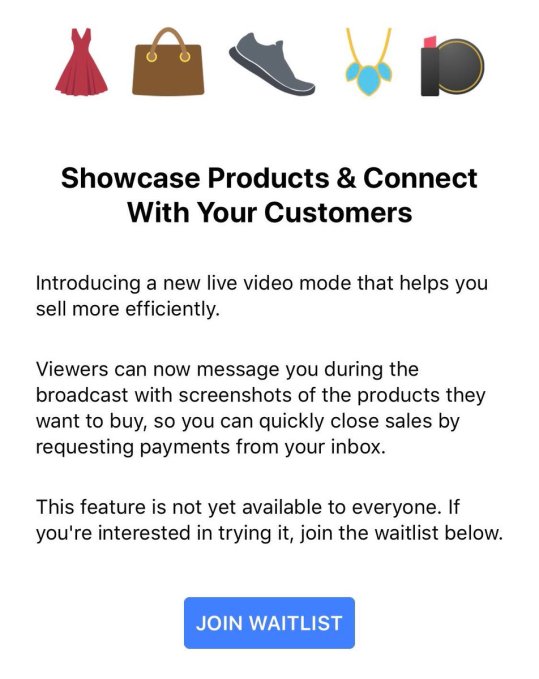

Want to run your own home shopping network? Facebook is now testing a Live video feature for merchants that lets them demo and describe their items for viewers. Customers can screenshot something they want to buy and use Messenger to send it to the seller, who can then request payment right through the chat app.

Facebook confirms the new shopping feature is currently in testing with a limited set of Pages in Thailand, which has been a testbed for shopping features. The option was first spotted by social media and reputation manager Jeff Higgins, and re-shared by Matt Navarra and Social Media Today. But now Facebook is confirming the test’s existence and providing additional details.

The company tells me it had heard feedback from the community in Thailand that Live video helped sellers demonstrate how items could be used or worn, and provided richer understanding than just using photos. Users also told Facebook that Live’s interactivity let customers instantly ask questions and get answers about product specifications and details. Facebook has looked to Thailand to test new commerce experiences like home rentals in Marketplace, as the country’s citizens were quick to prove how Facebook Groups could be used for peer-to-peer shopping. “Thailand is one of our most active Marketplace communities” says Mayank Yadav, Facebook product manager for Marketplace.

The company tells me it had heard feedback from the community in Thailand that Live video helped sellers demonstrate how items could be used or worn, and provided richer understanding than just using photos. Users also told Facebook that Live’s interactivity let customers instantly ask questions and get answers about product specifications and details. Facebook has looked to Thailand to test new commerce experiences like home rentals in Marketplace, as the country’s citizens were quick to prove how Facebook Groups could be used for peer-to-peer shopping. “Thailand is one of our most active Marketplace communities” says Mayank Yadav, Facebook product manager for Marketplace.

Now it’s running the Live shopping test, which allows Pages to notify fans that they’re broadcasting to “showcase products and connect with your customers.” Merchants can take reservations and request payments through Messenger. Facebook tells me it doesn’t currently have plans to add new partners or expand the feature. But some sellers without access are being invited to join a waitlist for the feature. It also says it’s working closely with its test partners to gather feedback and iterate on the live video shopping experience, which would seem to indicate it’s interested in opening the feature more widely if it performs well.

Facebook doesn’t take a cut of payments through Messenger, but the feature could still help earn the company money at a time when it’s seeking revenue streams beyond News Feed ads as it runs out of space there, Stories take over as the top media form and user growth plateaus. Hooking people on video viewing helps Facebook show lucrative video ads. The more that Facebook can train users to buy and sell things on its app, the better the conversion rates will be for businesses, and the more they’ll be willing to spend on ads. Facebook could also convince sellers who broadcast Live to buy its new Marketplace ad units to promote their wares. And Facebook is happy to snatch any use case from the rest of the internet, whether it’s long-form video viewing or job applications or shopping to boost time on site and subsequent ad views.

Increasingly, Facebook is setting its sights on Craigslist, Etsy and eBay. Those commerce platforms have failed to keep up with new technologies like video and lack the trust generated by Facebook’s real-name policy and social graph. A few years ago, selling something online meant typing up a generic description and maybe uploading a photo. Soon it could mean starring in your own infomercial.

[PostScript: And a Facebook home shopping network could work perfectly on its new countertop smart display Portal.]

Powered by WPeMatico

When Amazon rolled out its membership-based two-day shipping service in 2005, e-commerce and customer expectations around fulfillment speed changed forever.

Today, more than 100 million people use Amazon Prime. That means, 100 million people are fully accustomed to two-day shipping and if they can’t have it, they shop elsewhere. As The Wall Street Journal’s Christopher Mims recently put it: “Alongside life, liberty and the pursuit of happiness, you can now add another inalienable right: two-day shipping on practically everything.”

Only recently have Amazon’s competitors begun to offer similar fast delivery options. About two years ago, Walmart launched its own free two-day delivery service for its owned-inventory; eBay followed suit, establishing a three-day or less delivery guaranteed option for shoppers in March 2017.

To power these Prime-like delivery options, Walmart, eBay and the Canadian e-commerce business Shopify are relying on a little upstart.

One-year-old Deliverr helps businesses offer rapid delivery experiences to their customers. Today, the company is announcing a $7.1 million Series A led by Joe Lonsdale’s 8VC, with participation from Zola founder Shan-Lyn Ma, Flexport chief executive officer Ryan Peterson and others.

The San Francisco-based startup uses machine learning and predictive intelligence to determine which of its warehouses to store its client’s goods.

Currently, Deliverr operates out of more than 10 warehouses in Texas, Missouri, Pennsylvania, Ohio and New Jersey, among other states, though co-founder Michael Krakaris says that number is growing every week. Its customers typically store inventory in three to five different locations based on Deliverr’s predictive algorithms.

Unlike Amazon, which owns more than 75 fulfillment centers, Deliverr doesn’t own its warehouses. Krakaris describes the company’s strategy as a sort of Uber for fulfillment.

“Uber didn’t change the physical infrastructure of cars. They didn’t build their own taxis. What they did was create software that could connect excess capacity drivers,” Krakaris told TechCrunch. “Most warehouses aren’t going to be full. We are going in and filling that extra space they wouldn’t otherwise fill.”

One of the startup’s tricks is to use brand-neutral packaging so any and all marketplaces could theoretically power fulfillment through Deliverr. Amazon, of course, sticks a Prime sticker on all its outgoing packages. And because Amazon’s fulfillment service is used by some eBay sellers, eBay items are known to show up at customers’ homes in Amazon-branded packaging. Not a great look for eBay.

“You need an independent fulfillment service that can handle all these different fulfillment channels and be neutral,” Krakaris said.

Deliverr plans to use the investment to scale its team and ink partnerships with additional online retailers.

Powered by WPeMatico

After finally settling on a new apartment, packing your last box and rushing out to pick up your moving van for the measly three hours you could book it — have you ever taken a moment to think, “Wow, this is so easy?”

Nope, and neither has anybody else. But Shyft, a logistics platform company based in San Francisco, is hoping to change that.

Originally named Crater, the company announced today a re-brand of its name and mission to focus on helping improve the corporate relocation process for millions of movers per year. The company is bringing with it three years of experience developing software and technology to help moving companies provide better estimates and service to customers.

“We spend hours thinking about these global citizens who are moving everyday and literally shifting their lives,” Shyft CMO Rajiv Parikh told TechCrunch. “They’re moving to new communities, they’re finding new schools, they’re finding new opportunities. It’s a monumental and pivotal moment in someone’s life.”

The process works two-fold. First, Shyft is continuing its partnerships with moving companies and selling its software to them in order to help update their portals and make the process as seamless as possible for their existing customers. As part of these partnerships, Shyft is able to create a reliable network of moving companies and services that it can utilize in the second part of its service — connecting with corporate Fortune 500 companies to help their transferees easily and intuitively complete their moving process.

Through the platform, employees planning a move can fill out information like how many boxes they’re moving, what their housing needs will be and even what kind of food they like and dietary restrictions they have. With this data, Shyft will help direct them to the services they need and work to help them best integrate into their new communities.

Shyft works with corporate companies’ lump-sum funds to help employees find the best price possible for their move. And transferees can use the services for free (or be reimbursed the difference).

“A traditional moving company is focused on moving — dollars and cents — [and] they want the largest and the biggest moves out there,” Shyft CEO Alex Alpert told TechCrunch. “From our perspective, we’re agnostic to that. If it’s in someone’s best interest to sell their sofa and buy a new one, we want to help facilitate that.”

In a recent collaboration with eBay, the company says it has seen large increases in the number of employees using its portal instead of trying to figure out logistics on their own.

“We have monitored the use of Shyft in our lump sum program and have seen a marked increase in the willingness of employees to engage with Shyft to identify the best solution to their moving needs,” eBay Director of HR Global Mobility Eric Halverson said in a statement. “Shyft is helping our employees optimize their lump sum allowance with a variety of moving solutions geared to their personal needs and circumstances.”

Alpert says that Shyft is now focusing on growing and refining its service, and this summer was accepted to join Moderne Venture’s summer Passport Program. The seven-month industry immersion program is designed to help companies refine their go-to-market strategies and network with others working in the real estate, finance, insurance and home-services spaces.

Powered by WPeMatico