e-commerce

Auto Added by WPeMatico

Auto Added by WPeMatico

Carsome, which bills itself as Southeast Asia’s largest e-commerce platform for used cars, announced it has closed a $30 million Series D. The funding was led by Asia Partners, with participation from returning investors Burda Principal Investments and Ondine Capital.

The startup described this as one of the largest “all-equity financings to date in Southeast Asia’s online automotive industry.” Part of the Series D may be used for mergers and acquisitions to consolidate the company’s supply chain.

Founded five years ago in Malaysia, Carsome’s platform serves both C2C and B2C segments, and ensures quality by conducting inspections before vehicles are listed on its platform. It now has 1,000 employees and claims to transact 70,000 cars on an annualized basis, totaling $600 million.

In a press statement, co-founder and group chief executive officer Eric Cheng said that the company, which now also operates in Indonesia, Thailand and Singapore, doubled its monthly revenue over the past six months, compared to pre-pandemic levels. The company says that this is partly because more people and businesses are buying their own cars for safety reasons.

While sales of new vehicles have plummeted around the world, used car sales, especially through e-commerce platforms, are recovering more quickly, according to Counterpoint Research. This largely because people want to avoid public transportation and ride-hailing, but also want cheaper options.

Other used car platforms in Southeast Asia include Carro, OLX Autos (formerly called BeliMobilGue) and Carmudi.

Powered by WPeMatico

Ever since the pandemic hit the U.S. in full force last March, the B2B tech community keeps asking the same questions: Are businesses spending more on technology? What’s the money getting spent on? Is the sales cycle faster? What trends will likely carry into 2021?

Recently we decided to join forces to answer these questions. We analyzed data from the just-released Q4 2020 Outlook of the Coupa Business Spend Index (BSI), a leading indicator of economic growth, in light of hundreds of conversations we have had with business-tech buyers this year.

A former Battery Ventures portfolio company, Coupa* is a business spend-management company that has cumulatively processed more than $2 trillion in business spending. This perspective gives Coupa unique, real-time insights into tech spending trends across multiple industries.

Tech spending is continuing despite the economic recession — which helps explain why many startups are raising large rounds and even tapping public markets for capital.

Broadly speaking, tech spending is continuing despite the economic recession — which helps explain why many tech startups are raising large financing rounds and even tapping the public markets for capital. Here are our three specific takeaways on current tech spending:

Tech spending ranks among the hottest boardroom topics today. Decisions that used to be confined to the CIO’s organization are now operationally and strategically critical to the CEO. Multiple reasons drive this shift, but the pandemic has forced businesses to operate and engage with customers differently, almost overnight. Boards recognize that companies must change their business models and operations if they don’t want to become obsolete. The question on everyone’s mind is no longer “what are our technology investments?” but rather, “how fast can they happen?”

Spending on WFH/remote collaboration tools has largely run its course in the first wave of adaptation forced by the pandemic. Now we’re seeing a second wave of tech spending, in which enterprises adopt technology to make operations easier and simply keep their doors open.

SaaS solutions are replacing unsustainable manual processes. Consider Rhode Island’s decision to shift from in-person citizen surveying to using SurveyMonkey. Many companies are shifting their vendor payments to digital payments, ditching paper checks entirely. Utility provider PG&E is accelerating its digital transformation roadmap from five years to two years.

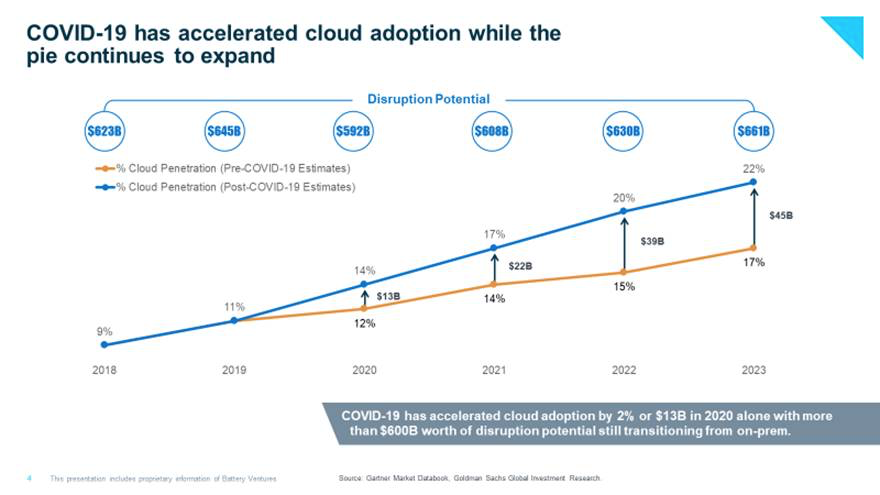

The second wave of adaptation has also pushed many companies to embrace the cloud, as this chart makes clear:

Image Credits: Battery Ventures (opens in a new window)

Similarly, the difficulty of maintaining a traditional data center during a pandemic has pushed many companies to finally shift to cloud infrastructure under COVID. As they migrate that workload to the cloud, the pie is still expanding. Goldman Sachs and Battery Ventures data suggest $600 billion worth of disruption potential will bleed into 2021 and beyond.

In addition to SaaS and cloud adoption, companies across sectors are spending on technologies to reduce their reliance on humans. For instance, Tyson Foods is investing in and accelerating the adoption of automated technology to process poultry, pork and beef.

Mention “digital product company” in the past, and we’d all think of Netflix. But now every company has to reimagine itself as offering digital products in a meaningful way.

Powered by WPeMatico

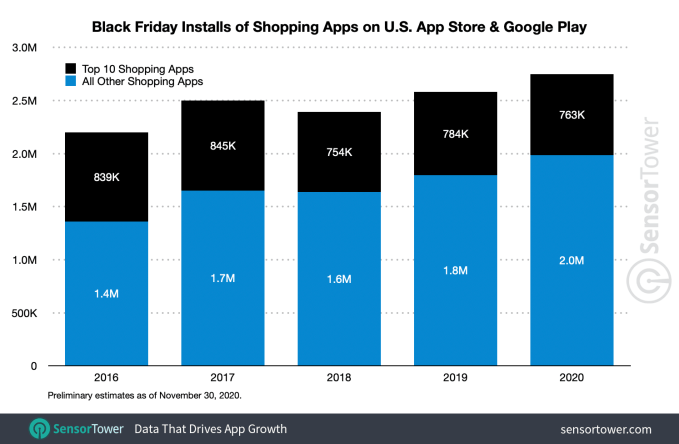

Many U.S. consumers spent this year’s Black Friday sales event shopping from home on mobile devices. That led to first-time installs of mobile shopping apps in the U.S. to break a new record for single-day installs on Black Friday 2020, according to a report from Sensor Tower. The firm estimates that U.S. consumers downloaded approximately 2.8 million shopping apps on November 27th — a figure that’s up by nearly 8% over last year.

However, this number doesn’t necessarily represent faster growth than in 2019, which also saw about an 8% year-over-year increase in Black Friday shopping app installs, the report noted. This could be because mobile shopping and the related app installs are now taking place throughout the month of November, though, as retailers adjusted to the pandemic and other online shopping trends by hosting earlier sales or even month-long sales events.

Image Credits: Sensor Tower

The data seems to indicate this is true. Between November 1 and November 29, U.S. consumers downloaded approximately 59.2 million shopping apps from across the App Store and Google Play — an increase of roughly 15% from the 51.7 million they downloaded in Novenber 2019. That’s a much higher figure than the 2% year-over-year growth seen during this same period in 2019.

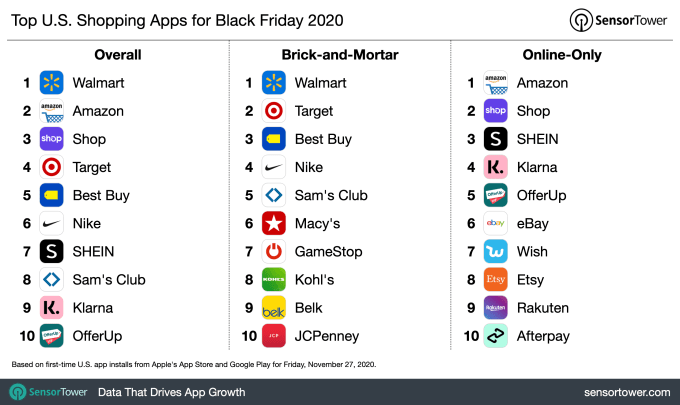

Another shift taking place in mobile shopping is the growing adoption of apps from brick-and-mortar retailers. During the first three quarters of 2020, apps from brick-and-mortar retailers grew installs 27%. This trend continued on Black Friday, when five out of the top 10 mobile shopping apps were those from brick-and-mortar retailers, led by Walmart.

Image Credits: Sensor Tower

Walmart saw the highest adoption this year, with around 131,000 Black Friday installs, followed by Amazon at 106,000, then Shopify’s Shop at 81,000. Combined, the top 10 apps saw 763,000 total new installs, or 27% of the first-time downloads in the Shopping category.

Because the firms are only looking at new app installs, they aren’t giving a full picture of the U.S. mobile shopping market, as many consumers already have these apps installed on their devices. And many more simply shop online via a desktop or laptop computer.

To give these figures some context, Shopify reported on Saturday it had seen record Black Friday sales of $2.4 billion, with 68% on mobile. And today, Amazon announced its small business sales alone topped $4.8 billion from Black Friday to Cyber Monday, a 60% year-over-year increase, but it didn’t break out the percentage that came from mobile.

Sensor Tower and rival app store analytics firm App Annie largely agreed on the top five shopping apps downloaded this Black Friday. They both saw Walmart again beating Amazon to become the most-downloaded U.S. shopping app on Black Friday — as it did in 2019. The two firms reported that Amazon remained No. 2 by downloads, followed by Shopify’s Shop app, then Target. However, Sensor Tower put Best Buy in fifth place, followed by Nike, while App Annie saw those positions swapped.

Image Credits: App Annie

The rest of Sensor Tower’s top 10 included SHEIN, Sam’s Club, Klarna, then Offer Up, while App Annie’s list was rounded out by SHEIN, Sam’s Club, Wish, then Offer Up.

The pandemic’s impact may not have been obvious given the growth in online shopping this year, but the recession it triggered has played a role in how U.S. consumers are paying for their purchases. “Buy Now, Pay Later” apps like Klarna were up this year, even breaking into the top 10 per Sensor Tower’s data. The firm also noted that many new shopping apps launched this year focused on discounts and deals, and retailers ran longer sales this year, as well.

Powered by WPeMatico

French startup Ankorstore has raised a $29.9 million Series A round (€25 million) with Index Ventures leading the round. Existing investors GFC, Alven and Aglaé are also participating.

Ankorstore is building a wholesale marketplace that connects independent shop owners with brands selling household supplies, maple syrup, headbands, bath salts, stationery items and a lot more. That list alone should remind you of neighborhood stores that sell a ton of cutesy stuff that you don’t necessarily need but that tend to be popular.

The company works with 2,000 brands and 15,000 shops. And the startup isn’t just connecting buyers and sellers, as it has a clear set of rules. For instance, the minimum first order is €100, which means that you can try out new products without ordering hundreds of items at once.

By default, Ankorstore withdraws the money 60 days after placing an order. Brands get paid upon delivery. And of course, buying from several brands through Ankorstore should simplify your admin tasks.

Ankorstore is currently live in eight countries — France, Spain, Austria, Germany, Belgium, Holland, Switzerland and Luxembourg. France is the biggest market followed by Germany. Up next, the startup plans to launch in the U.K. in 2021.

In many ways, Ankorstore reminds me of Faire, the wholesale marketplace that has raised hundreds of millions of dollars in the U.S.

“There are a number of different retail marketplaces connecting retailers with makers and brands. Where we believe we differ is in our clear focus on the independent shop owner, offering the tools and the terms that make it really easy and cost-effective to discover and access some of the most desirable up-and-coming brands,” Ankorstore co-founder Pierre-Louis Lacoste said.

Given that the startup is working with small suppliers, chances are they’re only selling their products in Europe. So there should be enough room for a European leader in that space that I would describe as wholesale Etsy-style marketplaces with a strong focus on curation.

Image Credits: Ankorstore

Powered by WPeMatico

Squarespace is adding a new monetization option for websites built on the platform: Member Areas, where businesses can charge for access to exclusive content.

Chief Product Officer Paul Gubbay said that particularly in the midst of the pandemic, businesses on Squarespace “want to experiment with different ways to make money.” They can already use the platform to sell products and services, and even to schedule appointments, but with Member Areas, “We allow you to sell your expertise, to sell your content.”

That could, of course, mean an online publication that wants to paywall some of its articles, but it could also mean a chef who wants to charge for access to cooking videos and recipes, or a fitness instructor hoping to make money from online classes.

Group Product Manager Kimberly Lin showed me how Member Areas are integrated into a Squarespace website, allowing the website owner to assign different access requirements to different pages — some could require a recurring membership fee, while others require a one-time payment and still others can be free with registration.

Squarespace also supports different membership tiers, as well as publishing member-only podcasts and newsletters. Site creators get access to CRM data on each of their members, with plans for more segmentation tools in the future.

Squarespace is making this available as an add-on to the core website building platform, with pricing starting at $9 per month. Gubbay emphasized the “simplicity” of adding these features to an existing Squarespace website, making it easy to put “anything you want” behind a paywall.

Lin also said that by integrating with the website builder, Squarespace can offer page protection that’s “truly secure,” because visitors can’t circumvent it by simply tracking down a paywalled URL.

As an early success story, Gubbay mentioned a jewelry merchant on Squarespace that started scheduling sessions where she gives design advice, then created Member Areas with videos and other jewelry-related content.

“First and foremost, we want to make sure we have product-market fit,” Gubbay added. “But I think what we’re going to be interested in doing as we move forward is helping people understand that, guiding them to the parts of the platform where they become a multi-modal seller.”

Powered by WPeMatico

Subscription services are on the rise. During the pandemic, Americans have been spending more time at home and more money on the digital products that make navigating our new normal easier.

More than ever, Americans’ lives are aided by companies like Netflix, Instacart and, of course, Amazon, which reported record-setting earnings from its 2020 Prime Day savings event.

A recent survey even found that spending on subscription services had more than tripled since March, with one in three respondents saying they’d purchased a new online subscription while quarantining.

Now, a new concern lingers: Is the market getting oversaturated? The question doesn’t just apply to streaming services and food delivery companies — it’s an issue financial technology businesses can’t afford to ignore.

As subscriptions become an increasingly alluring business model, fintechs will be forced to consider whether this proven strategy is worth the risk.

In the CompareCards survey, two-thirds of respondents said they purchased a new streaming service mainly for entertainment. Still, that doesn’t mean there isn’t room for fintechs to carve out their own space.

Bradley Leimer, co-founder of the financial consulting firm Unconventional Ventures, said he’s certainly seen more fintechs exploring subscription models. As Leimer explained, the financial services industry may have not fully embraced the idea, but it’s “starting to take notice.” Leimer, who has more than 25 years of experience in the industry, believes fintechs can learn a lot from subscription services — provided they’re willing to look in the right place.

One major lesson? Transparency. Subscription services give companies an opportunity to be upfront about their fees, as well as their benefits.

“When we talk about subscriptions, the more clear and more transparent we are, the better,” Leimer said.

Acorns is an easy case study. The microinvesting app offers three subscription levels — lite, personal and family — each with a clearly explained list of features. For what it’s worth, the company added more than 2 million users between March 2019 and March 2020, according to Forbes.

Leimer said fintechs should also take note of the way subscription services collaborate. For example, he pointed out how Amazon users can add an HBO subscription to their Prime Video account, essentially “bundling” two subscriptions into one. Fintechs, Leimer said, could stand to take a page out of that playbook.

“There are a lot of ways to sort of skin that cat — for a fintech company to generate income and for a customer to get value on top of that,” Leimer said.

Powered by WPeMatico

Great Jones is expanding into a new area of the kitchen tomorrow, with what co-founder and CEO Sierra Tishgart described as the startup’s biggest launch since it released its first products two years ago.

Ahead of launching the new bakeware line, Great Jones is announcing that it has raised $1.75 million in new funding.

The money comes from notable figures in the e-commerce world — Fellow founder Jake Miller and Very Great founders Eric Prum and Josh Williams — along with restauranteurs including Mimi Cheng’s co-founder Hannah Cheng, Lilia founder Sean Feeny, Kopitiam co-owner Moonlynn Tsai and Konbi co-owner Akira Akuto.

NEA partner Liza Landsman invested as well, and Tishgart said that Sweetgreen’s Nic Jammet and Parachute’s Ariel Kaye have joined the startup’s board of directors. Tishgart noted that Great Jones has worked on collaborations and product partnerships with many of these investors, and she also pointed to Kaye and Parachute as providing a model for how Great Jones can grow.

“To me, starting with sheets, [Kaye] has taken a product which people loved and thoughtfully expanded to a broad selection,” Tishgart said.

She sees a similar path for Great Jones — just as Parachute has become a “one-stop shop” for the home, Tishgart wants her startup to do the same for your kitchen. Great Jones launched with pots, pans and a Dutch oven, then added a baking sheet and is now expanding into a whole line of bakeware.

Image Credits: Great Jones

The new bakeware products (many of them inspired by classic Pyrex designs) include the Sweetie Pie ceramic pie dish, the Hot Dish ceramic casserole dish, the Breadwinner loaf pan, the Patty Cake cake pan and a new broccoli-colored version of the Holy Sheet baking sheet. You can buy the pieces à la carte (the Holy Sheet is $35, the pie pans are $45 and the bread pans are $65 for a pair) or purchase the whole set for $245.

Tishgart added that the company has had a “really, really busy year” with lockdowns and social distancing.

“People are cooking more than ever,” she said. “This is a category and an industry that have really been able to thrive on this.”

At the same time, Tishgart emphasized that the growing interest from millennials and younger consumers is a long-term trend that won’t go away when the pandemic is over — with the rise of celebrity chefs, high-profile restaurants and more food content than ever, food and cooking have become a bigger “cultural force” than ever.

There have been challenges as well, particularly as the pandemic has affected supply chains. Tishgart said the company has spent much of the year “chasing product,” but it benefited from using a variety of materials and working with a variety of manufacturers.

“This is one thing that upfront made for a more complicated supply chain,” she said. “But it’s a strong saving grace now, because we’re not reliant on one factory or one part of the world.”

The funding, Tishgart said, will allow Great Jones to invest in further product development and production. And while there are plenty of other cookware startups raising funding, she said that “it’s motivating, it’s exciting to see how other people interpret it” and that the different brands “all speak to different customers.”

Powered by WPeMatico

So much can change in a day.

This morning, news that a trial COVID-19 vaccine candidate had an effective rate of more than 90% shook the financial world. The Pfizer vaccine is reportedly so effective, the company “will have manufactured enough doses to immunize 15 to 20 million people” by the end of the year, according to the New York Times, appears to have given investors the green light to pile back into companies harmed by the pandemic.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

The shift of money from shares that proved popular during the summer is massive and abrupt. Zoom and Peloton are down sharply this morning, while Uber and Lyft are soaring. Indeed, the Dow Jones Industrial Average and S&P 500 indices are up around 4.8% and 3.3% respectively, while SaaS and cloud share are off 3.5%.

Investors are taking money out of companies that were expected to do well thanks to the pandemic and moving that capital into firms that were weakened by the pandemic.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Our question for this morning: what do these changes mean for the economic forces that have broadly favored venture-backed startups? What happens to high-flying startups if the pandemic trade flips? What’s next for insurtech, edtech, fintech and SaaS? Let’s discuss.

Short-term market movements do not always predict the future accurately, so we should not treat today’s trading as gospel.

That said, it’s not hard to draw some basic conclusions from the trading activity. Here’s what I think we can deduce from today’s stock market activity:

Powered by WPeMatico

Startups involved in B2B e-commerce such as Faire and Mirakl have burst out of the gates in 2020. Almost overnight, these startups transformed into consequential platforms, earning billion-dollar valuations along the way. The B2B e-commerce industry has broad reach, encompassing everything from commerce infrastructure and payments technology to procurement and supply-chain solutions. But one area of the B2B e-commerce sector holds outsized promise: marketplaces.

These venues for buyers and sellers of business-related products are exploding in popularity, fueled by better infrastructure, payments and security on the back-end and companies’ increased need to conduct business online during the pandemic.

Even before the pandemic, B2B marketplaces were expected to generate $3.6 trillion in sales by 2024, up from an estimated $680 billion in 2018, according to payments research firm iBe TSD. They were already growing more quickly than most B2C marketplaces that predated them, and when COVID shutdowns hit, many companies scrambled to shift all purchasing online. A survey of business buyers conducted by Digital Commerce 360 found that 20% of purchasing managers spent more on marketplaces, and 22% spent significantly more, during the pandemic.

For many entrepreneurs running B2B marketplaces, the pandemic created new demand for their platforms. Yet to convince businesses to make a permanent shift to online purchasing, B2B marketplaces cannot simply remain stagnant, serving as simple transactional platforms. Those that innovate now to introduce adjacent services will emerge as winners in the next few years, with some inevitably becoming billion-dollar companies.

As a venture capital investor in B2B e-commerce companies, I’m carefully watching the industry and have seen several forward-thinking business models emerge for B2B marketplaces. The predominant revenue model of B2C marketplaces, the gross merchandise value (GMV) take rate, or percentage of each transaction, doesn’t always translate well in the B2B world. Instead, B2B marketplaces are discovering creative new ways to monetize their networks, ensuring their approach is tailored to the complex and nuanced world of B2B e-commerce. I’ll delve into each of these models below, providing examples of marketplaces that have successfully begun implementing them.

What makes B2B transactions unique? Before discussing how B2B marketplaces can deploy new business models, it’s important to think about how B2B transactions typically work.

Payment methods: There are four main ways to make a B2B payment: paper check, ACH transfer, electronic fund transfer (wires), and credit/debit cards. Nearly half of B2B payments are still made by paper check, but digital payment solutions are quickly gaining.

Financing: It is customary in B2B transactions to pay “with terms,” such as net 30 or net 60, effectively giving a line of credit to the business buyer that enables them to send payment after delivery of the good or service. Supply-chain financing and dynamic discounting are two mechanisms business buyers use to settle invoices with suppliers on preferred timelines.

Bulk discounts: Business buyers often expect and receive discounts in return for placing high-volume orders. While not a concept unique to B2B, negotiated or custom volume discounts can complicate the checkout process.

Contractual pricing: Businesses often enter into enterprise-level pricing agreements with their suppliers. In some B2B verticals, such as the veterinary supplies market, there is little consistency and transparency regarding the market price of any given item; instead, each buyer pays a bespoke price tied to contractual agreements. This dynamic typically benefits suppliers, which can price discriminate based on buyers’ ability and willingness to pay.

Delivery method and timing: Unlike consumers, businesses may place orders for goods but delay delivery for weeks or months. This is particularly common in the commodities market, where futures contracts specify a commodity to be delivered on a certain date in the future. B2B transactions typically include a negotiation on delivery method and timing.

Insurance: Business buyers frequently purchase insurance as part of their transactions, particularly in high-value verticals such as jewelry. Insurance is designed to protect against damage to the goods in transit or theft.

Compliance: In some verticals, particularly those related to healthcare and chemicals, there is a heavy compliance burden to ensure goods are properly sourced and transported. Is the seller legally registered to sell and transport sensitive goods such as medical equipment or pharmaceuticals?

With all of these considerations, it’s no wonder B2B e-commerce has been slower to digitize than B2C. From product discovery through the checkout process, a consumer buying a bag of licorice looks nothing like a retailer buying 100,000 bags of licorice from a distributor. The good news for B2B marketplace founders is that, based on the parameters above, there are many creative ways to extract value from transactions that go beyond the GMV take rate. Let’s explore some of the creative ways to monetize a B2B marketplace.

Powered by WPeMatico

PayPal this week laid out its vision for the future of its digital wallet platform and its PayPal and Venmo apps. During its third-quarter earnings call on Monday, the company said it plans to roll out substantial changes to its mobile apps over the next year to integrate a range of new features, including enhanced direct deposit, check cashing, budgeting tools, bill pay, crypto support, subscription management, buy now/pay later functionality and all of Honey’s shopping tools.

While PayPal had spoken in the past about bringing Honey’s capabilities into PayPal, CEO Dan Schulman detailed the integrations PayPal has in store for the deal-finding platform it bought last year for $4 billion, as well as a timetable for both this and the other app updates it has in store.

The Honey acquisition had brought 17 million monthly active users to PayPal. These users turned to Honey’s browser extension and mobile app to find the best savings on items they want to buy, track prices and more.

But today, the Honey experience still remains separate from PayPal itself. That’s something the company wants to change next year.

According to Schulman, the company’s apps will be updated to include Honey’s shopping tools, like its Wish List feature that allows you to track items you want to buy, price monitoring tools that alert you to savings and price drops, plus its deals, coupons and rewards. These tools will become part of PayPal’s checkout solution itself.

That means the company will be able to track the customer from the initial deal-hunting phase where they’re indicating their interest in a certain product, target them with savings and offers, then guide them through its checkout experience all in one place.

PayPal will also provide “anonymous demand data” to merchants based on consumer engagement with Honey’s tools to help them drive sales, the company said.

What’s more, PayPal put timeline on the Honey integrations and the other updates it plans to roll out over the course of the next year.

Bill Pay will start to roll out this month, PayPal said, with a large redesign of the digital wallet experience expected for the first half of 2021. Much of the new functionality will be arriving in the second quarter and the second half of the year, with a goal of having the majority of the changes rolled out by the end of next year.

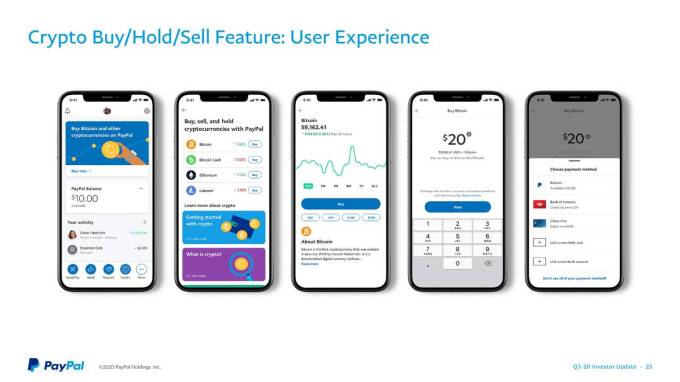

This also includes PayPal’s plans for cryptocurrencies, announced at the end of October. The company aims to support Bitcoin, Ethereum, Bitcoin Cash and Litecoin at first, initially in the U.S.

Speaking to investors during the earnings call, Schulman also noted when PayPal plans to bring crypto to more users and geographies. He said the ability to buy, sell and hold cryptocurrencies will first arrive in the U.S., then will roll out to international markets and the Venmo app in the first half of next year. (Currently, PayPal is offering U.S. users to join a waitlist for the new crypto features in-app).

Image Credits: PayPal

This change will allow PayPal’s users to shop using cryptocurrencies across the company’s 28 million merchants without requiring additional integrations on merchants’ part. The company explained this is due to how it will handle the settlement process, where users will be able to instantaneously transfer crypto into fiat currency at a set rate when checking out with PayPal merchants.

“This solution will not involve any additional integrations, volatility risk or incremental transaction fees for either consumers or merchants, and will fundamentally bolster the utility of cryptocurrencies,” said Schulman. “This is just the beginning of the opportunities we see as we work hand in hand with regulators to accept new forms of digital currencies,” he added.

PayPal also recently joined the “buy now, pay later” race with its new “Pay in 4” installment program that lets consumers split purchases into four payments. This debuted in France ahead of its late August U.S. launch and has since rolled out to the U.K. (as Pay in 3). This too, will become more integrated into the company’s apps in the months ahead.

Venmo — which the company expects to reach $900 million in revenues next year — will see the expansion of business profiles, and will gain crypto capabilities, more basic financial tools and shopping tools, as well as a revamp of the “Pay with Venmo” checkout experience.

Schulman referred to the company’s plans to overhaul its Venmo and PayPal apps as a “fundamental transformation,” due to how much new functionality they will include as the changes roll out over the next year as well as the new user experience — basically, a redesign — that will allow people to move easily from one experience to the next instead of having to change apps or use a desktop browser, for example.

PayPal’s earnings hadn’t excited Wall Street investors this week, sending the stock down on its lack of 2021 guidance. But the year ahead for PayPal’s digital wallet apps looks to be an interesting one.

Powered by WPeMatico